Tia Caldwell

Senior Policy Analyst, Higher Education

New Department of Education data reveal a worrisome trend

Almost 7 million people, about one in six federal student loan borrowers, are in default on their loans. By all accounts, defaulting on a student loan is an upsetting and financially calamitous experience. Borrowers default when they miss 270 days’ worth of payments. Soon after, they can have their tax refunds and paychecks garnished, their credit scores fall, and their eligibility for more student aid revoked. Beyond these tangible effects, people in default on their loans often feel stressed and hopeless as they struggle to find a way out of their financial difficulties.

While the personal toll of default—and the fact that the most vulnerable borrowers are disproportionately likely to default—are well-documented, the specifics of default patterns, such as the timing, duration, and financial recovery, are not as well understood. Little is known about these aspects of default because the Department of Education (the Department) rarely releases detailed information about default. But in late 2023, the Department broke this pattern by publishing summary tables as part of an ongoing rulemaking process.

These new data reveal a concerning trend: millions of Americans are trapped in long-term default. Our analysis suggests many of these borrowers did not receive appropriate assistance navigating the overly complicated options for exiting default, and most have too few resources to repay their loans—even when subject to forced collections.

For this post, we define long-term defaulters as borrowers who first defaulted at least seven years ago and are still in default, either because they remained in default the entire time or because they exited but re-defaulted. Although defaults typically disappear from credit reports after seven years, there is no statute of limitations on collections. As a result, those stuck in long-term default continue to experience severe financial consequences, and borrowers have, until recently, not been able to earn any credit towards loan forgiveness while in default.

All borrowers analyzed in this blog defaulted on their loans prior to March 2020. Student loan collections have been paused since then but will resume after September 2024. Recent improvements to the repayment system will hopefully make new defaults less common and provide additional options for those in default, although the problem of long-term default will persist for many.

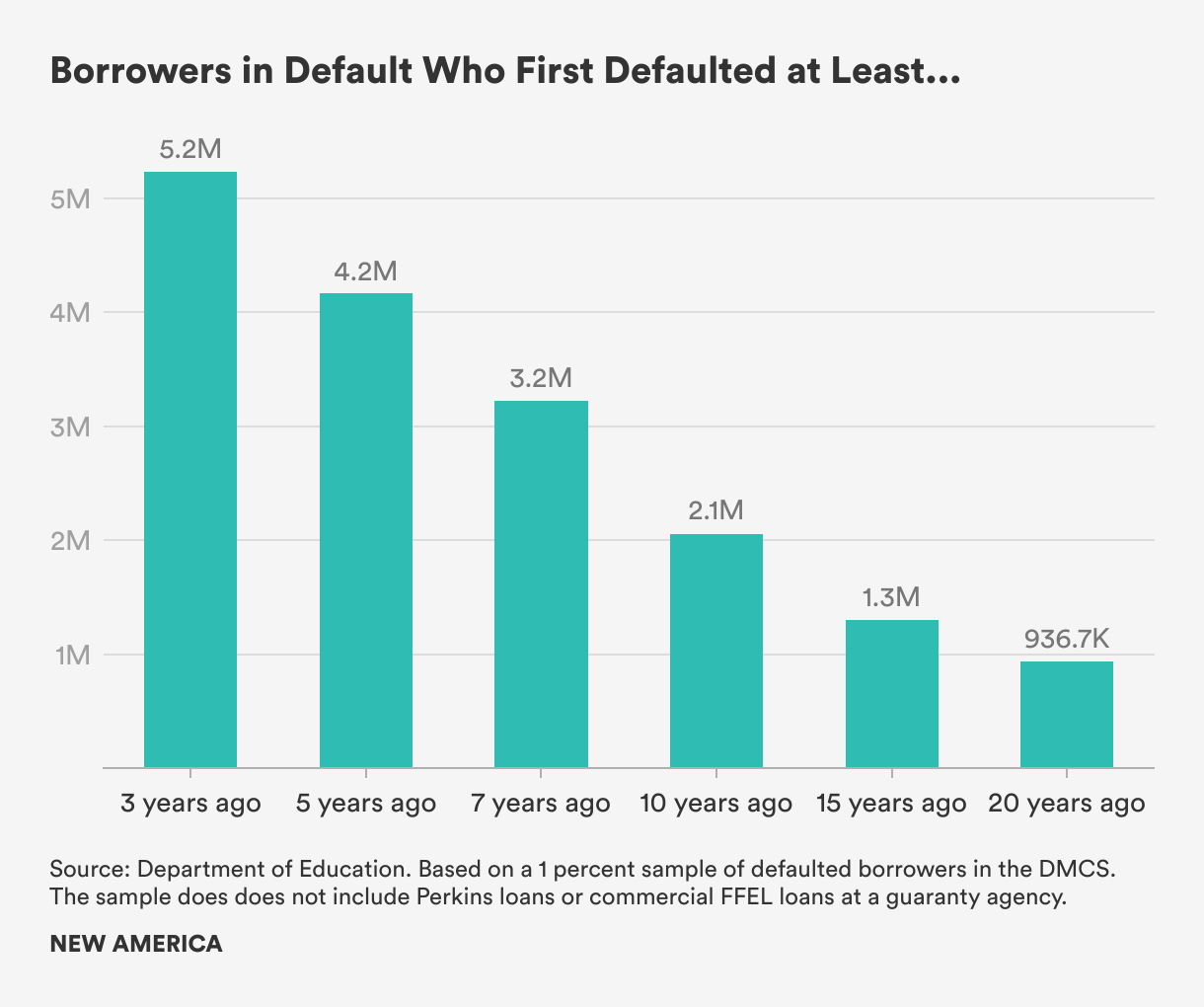

The new data confirm what surveys, credit bureau data, and qualitative research have suggested: many borrowers struggle with student loan defaults for multiple years, some for decades. Forty-five percent of those in the Department’s sample of defaulted borrowers, approximately 3.2 million people, first had one of their loans enter default seven or more years ago. Many of these long-term defaulters have been struggling for even longer. Almost 2.1 million borrowers (29 percent of those in the default sample) first defaulted a decade or more ago, and 937,000 borrowers (13 percent) first defaulted 20 or more years ago.

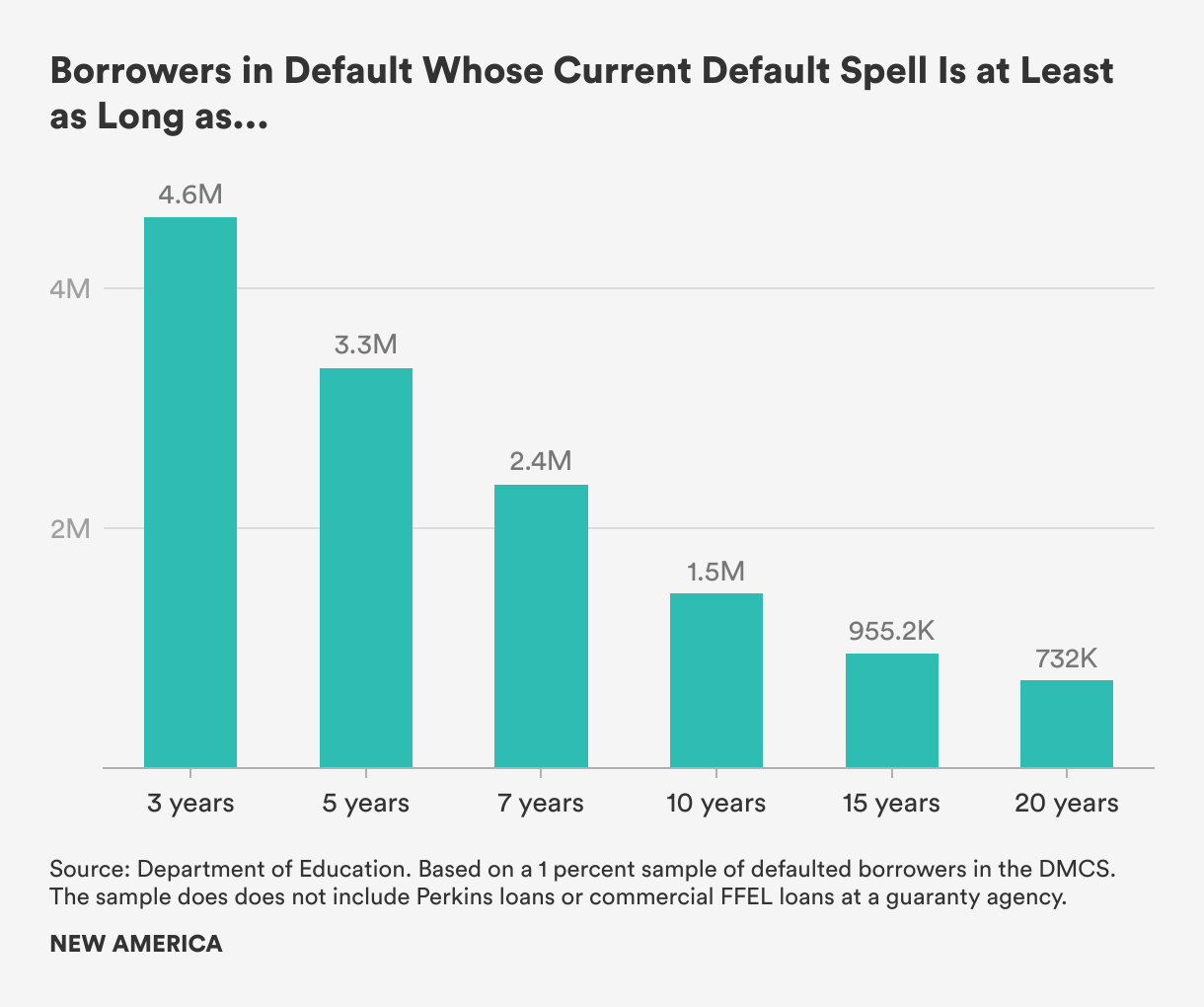

Close to three-quarters of long-term defaulters remained in default continuously since their first default. The result is that almost 2.4 million borrowers in the Department’s data have spent seven or more consecutive years trapped in default. That includes 1.5 million borrowers who have been in default for a decade or more and 732,000 borrowers who have been in default continuously for two decades or more.

Borrowers have several options for exiting default without fully repaying their debt. However, some pathways can be used only once and are confusing or hard to access. The high number of long-term defaulters points to both the complexity of the system and long-standing communication breakdowns between the Department and its contractors and vulnerable borrowers. For example, in focus groups, many people who had defaulted on their student loans said they had not realized they could exit without fully repaying their debt.

The remaining quarter of borrowers in long-term default were able to successfully exit default, only to re-default within the seven year period. Their experiences reflect past problems connecting borrowers who exit default with affordable repayment options (the Biden administration has taken steps to improve the transition from default to repayment going forward).

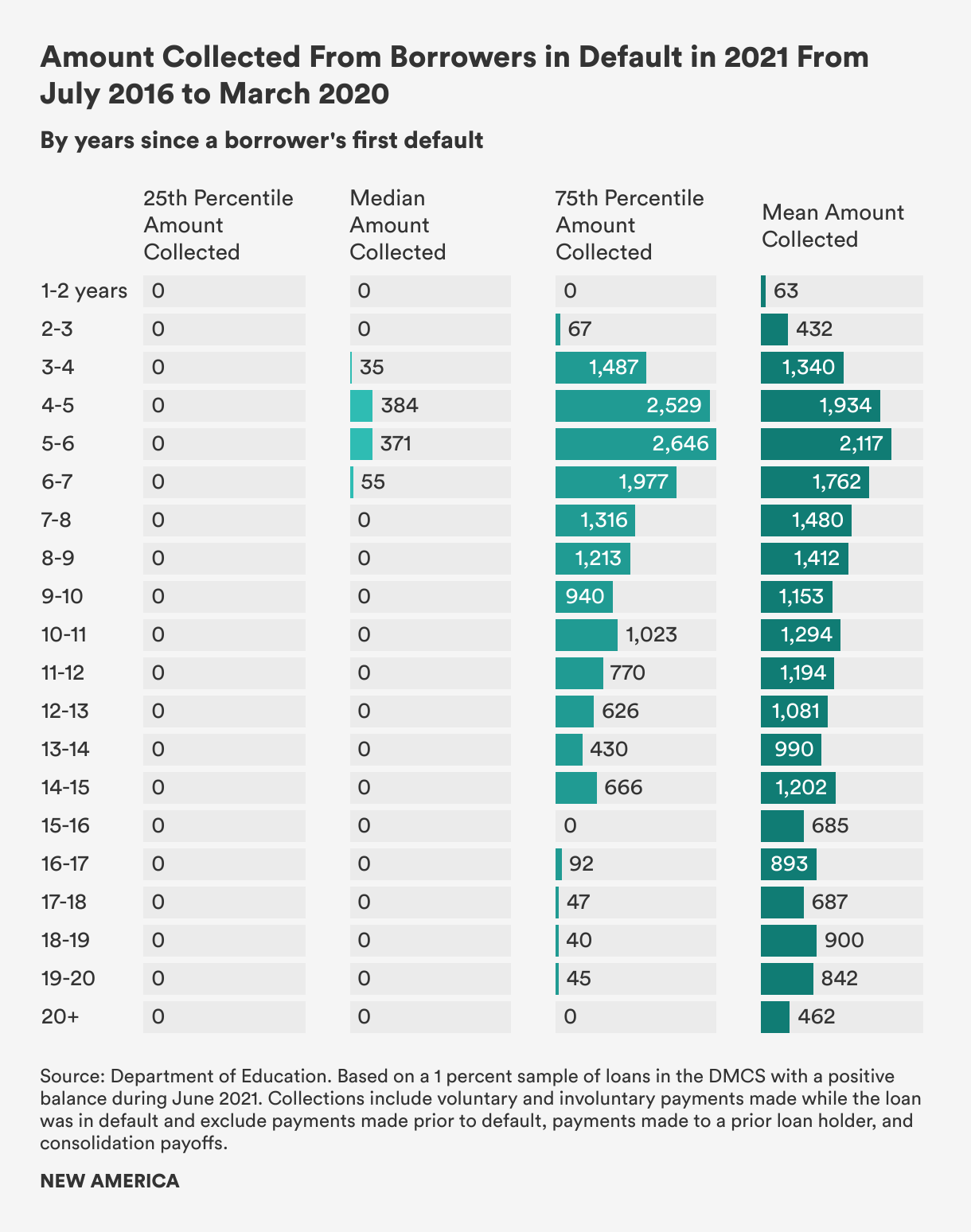

While borrowers are in default, the government has the authority to garnish wages, reclaim tax refunds, and take portions of Social Security payments. Although the Department estimates it recoups more than 75 percent of the balances of loans that enter default, little is recovered from most borrowers in long-term default. Over the three and a half years between July 2016 and March 2020, the default system collected nothing—including through both voluntary payments and involuntary collections—from the typical borrower who first defaulted seven or more years ago and is included in the Department’s data. Collections become even less fruitful as time in default extends beyond seven years. The default system recouped less than $100 from 75 percent of borrowers who first defaulted at least 15 years ago.

These low recovery rates are likely due to widespread financial hardship among those in long-term default. For example, government agencies estimate that 80 percent of those in default earn less than 150 percent of the federal poverty guidelines, suggesting that low collections are a result of borrowers having few resources from which to collect.

Some readers might wonder how collections are profitable when median collections are so low. Average (mean) collections are much higher than median collections because the Department collects large amounts from a small subset of borrowers in default. Average collections among borrowers who have ever entered default, as opposed to borrowers who are currently in default, are likely even higher. When collections result in a loan being completely repaid or returned to good standing, the borrower falls out of the sample of current defaulters. Borrowers who experience high collections may be especially likely to bring their loans out of default.

Unable to find a way to leave default and unable to repay their debts, long-term defaulters remain stuck in default even as interest continues to accrue on their loans. Many also saw their balances grow during repayment, since interest accumulates during many types of loan pauses, in income-driven repayment plans (other than the new SAVE plan), and when borrowers are delinquent on their loans en route to default.

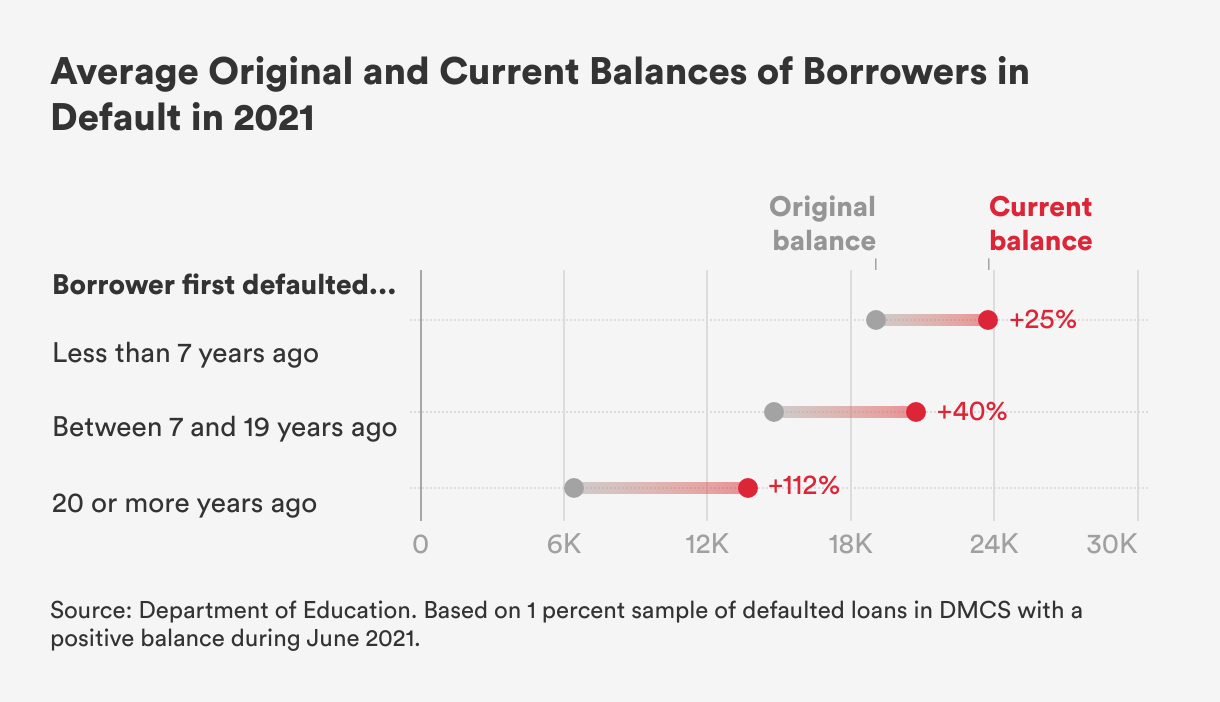

As a result, the average balance of a borrower in default and in the Department’s data has increased over the life of the loan to about $21,000, or $5,500 more than the average original balance. The growth is even more striking for extremely long-term defaulters: current balances are more than double the original principal among those in default who first defaulted twenty or more years ago.

Borrowers in long-term default are unable to keep up with interest, on average, despite originally taking out little debt. The average original balance of borrowers who first defaulted between seven and 19 years ago is only around $14,800, while the average original balance of borrowers who defaulted over 20 years ago is just $6,500. Original median balances are likely even smaller than the means reported in the data. Over 60 percent of borrowers in default did not complete their degree, which often results in lower levels of student debt due to shorter periods in school. But even relatively low levels of debt can be unaffordable for students from low-income backgrounds who do not see a return from a college degree.

The new data paint a picture of a student loan default system that is trapping millions of low-resource borrowers in years-long financial purgatory. These long-term defaults help nobody. As a first step towards ending long-term defaults, the Department and its contractors must increase efforts to inform those in default about options to exit. For instance, it must spread the word about the temporary Fresh Start initiative, a program that provides a fast, easy-to-access pathway out of default.

The Department should also provide borrowers suffering from long-term default with loan cancellation as an acknowledgement of the uncollectable nature of their debts. During an on-going rulemaking process, the Department suggested the important step of a one-time forgiveness of debt older than 20 or 25 years. Other forgiveness policies are still needed to help future and current long-term defaulters who took out debt more recently than 20 or 25 years ago. These policies could count time in default towards income-driven repayment forgiveness as the Department is already doing for periods borrowers spent in repayment through its one-time count adjustment. And the Department should develop guidelines for when to cancel the loans of borrowers who have spent long periods in default with uncollectable debt. As these new data prove, the Department has little to gain by keeping these debts on the books.

Senior Policy Analyst, Higher Education

Project Director, Education, Opportunity, and Mobility