Sarah Sattelmeyer

Project Director, Education, Opportunity, and Mobility

Why borrowers default on their student loans and how the system jeopardizes their economic security

Today, approximately 7.5 million Americans are in default on their federal student loans. Borrowers enter default when they miss 270 days’ worth of payments, and being behind on student loan bills comes with severe financial consequences. Borrowers in default can, for example, be charged high collection fees and have portions of their wages, tax refunds, and federal benefits withheld—including Social Security, the Earned Income Tax Credit, and the Child Tax Credit.

Default not only causes family financial insecurity, but it also contributes to the racial wealth gap and related economic disparities. Those mostly likely to default—Black, Hispanic and Latina/o, and Native American borrowers; low-income and low-wealth families; first generation college students; and those who leave school without completing a degree or credential, among others—have also been hit hardest by the COVID-19 pandemic. But even in the best of times, these communities are often the least able to afford the penalties that come with default due to a history of structural discrimination and racism in our systems of education and justice, the labor market, and mechanisms through which families build and access wealth.

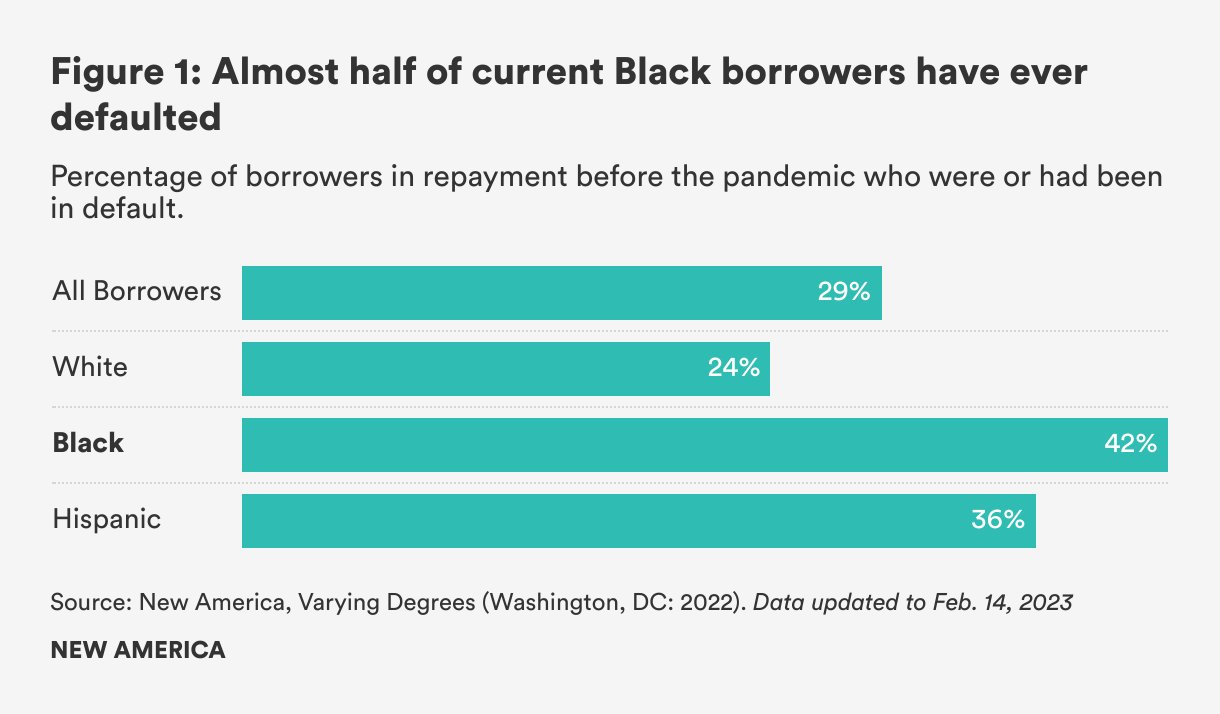

According to forthcoming data from New America’s Varying Degrees survey, approximately one-third of borrowers in repayment on their loans before the pandemic—including almost half of Black borrowers (42 percent)—have ever defaulted, rates that have remained high over time.[1] (See Figure 1.) Similar borrowers with incomes below $30,000 also report disproportionately high rates of default (46 percent). And 62 percent who are in default or defaulted previously have children.

While the consequences can be severe for those who enter default, surprisingly little data exist about borrowers’ experiences when they are behind on their payments. In addition, the default system itself is hard to analyze because it is complex; governed by multiple laws, related regulations, and administrative processes; and largely overseen by a different set of contractors than those that manage loan repayment for borrowers in good standing.

This analysis uses aggregate data from a nationally representative survey of 1,609 student loan borrowers, including an oversample of those who reported defaulting on a loan.[2] The survey was conducted in 2021 by NORC at the University of Chicago on behalf of the Pew Charitable Trusts. While Pew’s publicly available data are not disaggregated by important demographic categories like race, gender, completion status, income, and school type, this issue brief highlights why borrowers default, how being in default affects their economic security, and opportunities for reform.[3]

Key findings include:

Since the start of the pandemic in March 2020—and through at least August 2022—the government paused payments and interest for most student loan borrowers and collections for those in default. The Biden administration also plans to allow borrowers currently in default to reenter repayment in good standing (with a “fresh start”) on their loans, intends to propose new regulations addressing debt collection, and will likely provide borrowers in default with access to more affordable payment plans through the ongoing regulatory process.[4] But more must be done to reform the default system, including making it easier for borrowers to exit default and avoid redefaulting and protecting the financial security of borrowers in default.

While these reforms to the default system are necessary, they are also not sufficient. Policymakers must help borrowers avoid default in the first place by reducing or eliminating the need for loans; ensuring borrowers get financial returns on their higher education investments; and making the repayment system truly affordable, accessible, and one that does not trap borrowers in debt. The Biden administration must also extend the current payment pause to ensure the Department of Education can implement both plans to support struggling borrowers and for debt cancelation before repayment restarts.

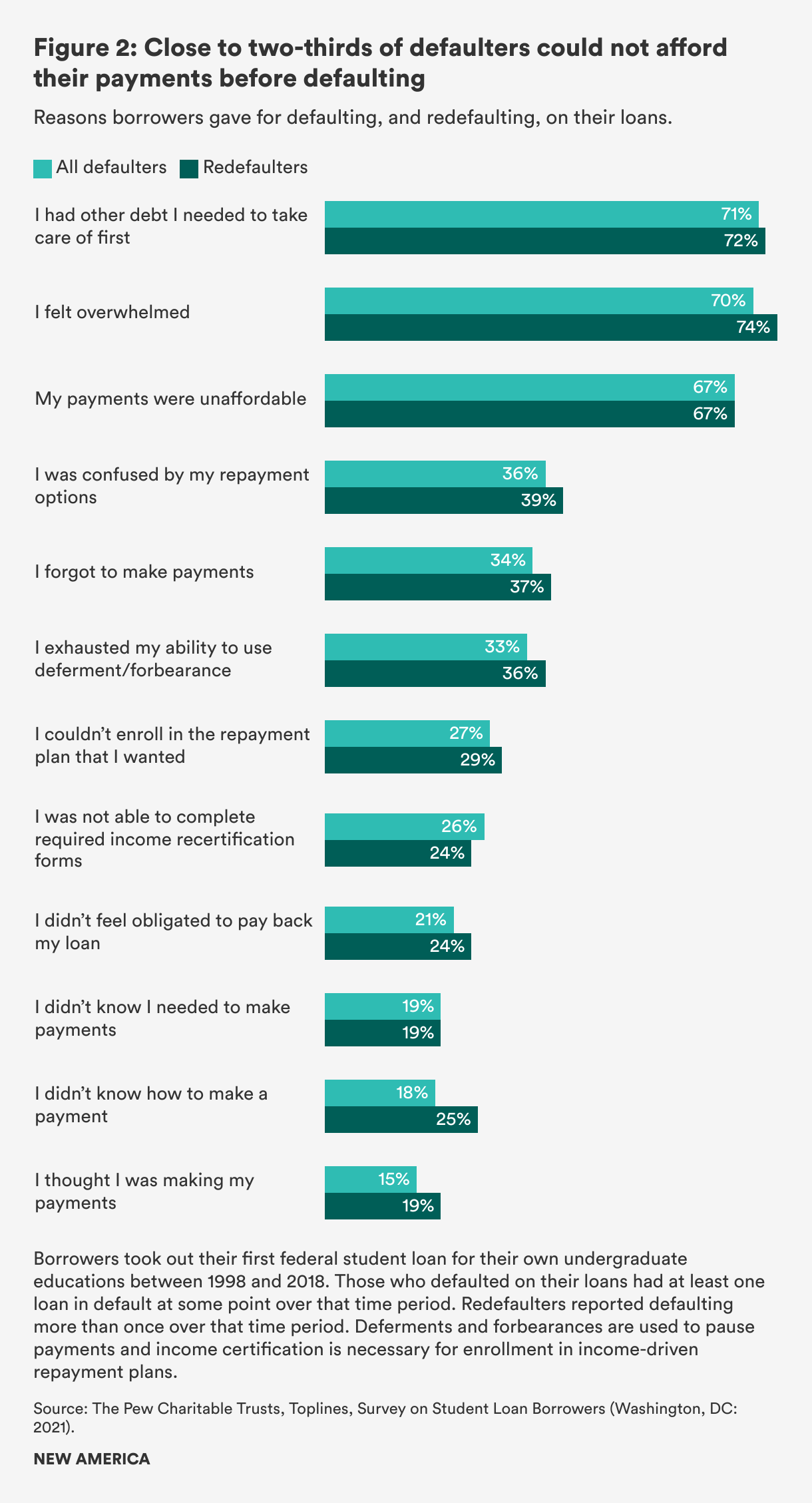

Close to two-thirds of borrowers who defaulted reported doing so because they were not able to afford their payments (67 percent) or had other debt they needed to take care of first (71 percent). (See Figure 2.) A similar number (70 percent) also indicated that they felt overwhelmed—likely with their finances and existing commitments, the student loan repayment system, or both. Borrowers who reported defaulting more than once over the last two decades said they defaulted again for the same key reason: they remained financially insecure.

Financial hardship can contribute to and be caused by defaulting on a student loan. Research indicates that low-income and low-wealth families are more likely than their higher resource peers to experience income volatility and unemployment. And those that borrow are more likely to default on their student loans and have other debt in collections. (See Appendix A for additional information on which borrowers are most at risk of defaulting on a student loan.)

Many borrowers are managing unexpected expenses—including for medical care or home or car repair—in addition to bills for groceries, transportation, and child care. And low-resource communities and families of color are more likely to devote more of their resources toward essentials like housing, meaning they have less money to put toward student loans.

Financial insecurity can be exacerbated by a confusing student loan repayment system that can propel borrowers toward default instead of providing accessible pathways toward affordable payments or loan discharges. A third of defaulters reported doing so because they were confused by their repayment options (36 percent), had exhausted their ability to pause payments (33 percent), or forgot to make payments (34 percent). And one-quarter reported defaulting because they were unable to enroll in their chosen repayment plan (27 percent) or complete required paperwork (26 percent). (See Figure 2.)

While the complexity of the repayment system affects most borrowers—only 27 percent of all survey respondents reported finding it straightforward and easy to navigate—achieving success can be particularly difficult for those with the fewest resources. Research from other fields, such as behavioral economics, and stories from recent focus groups and interviews highlighting borrowers’ experiences in repayment, underscore the fact that economic instability can chip away at the bandwidth that families have to manage complicated systems, especially when many in default are also using safety net programs, which have their own complex application processes and program requirements.

Borrowers must make a host of complex decisions among a variety of repayment plans and options. Income-driven repayment plans calculate monthly payments based on a borrower’s income and family size. Enrolling in these plans results in lower payments for many borrowers, and bills can be as little as $0 for those with earnings close to the poverty line. Borrowers in income-driven plans have lower rates of default. However, it can be difficult to enroll and remain in these plans because of confusing annual paperwork requirements; many who might benefit may not be able to access these programs and the forgiveness promised at the end of 20 to 25 years’ worth of payments. And, for some, these payments are still unaffordable.

The ability to make payments based on income—or to pause payments using deferments and forbearances—are important protections. But when borrowers’ payments are less than the interest that accrues on their loans, their balances grow over time. This balance growth not only comes with financial consequences as borrowers can pay more over time, but it also comes with psychological consequences as borrowers feel like they cannot make a dent in their debt and there is no end in sight. On top of this complexity, the Department of Education and its contractors have a history of providing inadequate information to borrowers, mishandling implementation of existing programs, and lacking strong oversight and standards that lead to borrower success.

When borrowers default, their accounts can change hands multiple times, and they may hear from a variety of entities charged with explaining a complicated system. Thus, even with perfect program implementation, borrowers may have lost touch with or not received or acted on communication from the Department and its contractors, making it more likely that they will receive spotty or insufficient information. Loan servicers—organizations responsible for collecting payments and helping borrowers manage their loans when they are in good standing—send defaulted loans back to the Department which, until recently, could then send those accounts to private collection agencies.[5] If borrowers manage to exit default, their loans are handed back to a loan servicer. (See Appendix B for more information about these hand-offs and what it means to default on a student loan.)

These hand-offs can make it challenging for borrowers to know the status of their loans and whom to trust for assistance. Among those polled who indicated they had experienced default, 18 percent were unsure about whether they were in default immediately before the pandemic. And one in five defaulters (20 percent) reported not knowing how many times they had defaulted.

The severe financial consequences that come with default can push economically insecure families into (or further into) poverty. For example, once in default:

The government and its contractors can collect using multiple of these mechanisms at the same time, meaning that some borrowers, for example, may have their wages garnished while also having federal benefits withheld. As a result, borrowers can pay more, and more quickly, after they enter default than they are required to when they are current on their loans. And there is no statute of limitations for collecting federal student debt. (See Appendix C for more information about the punitive nature and consequences of the student loan default system.)

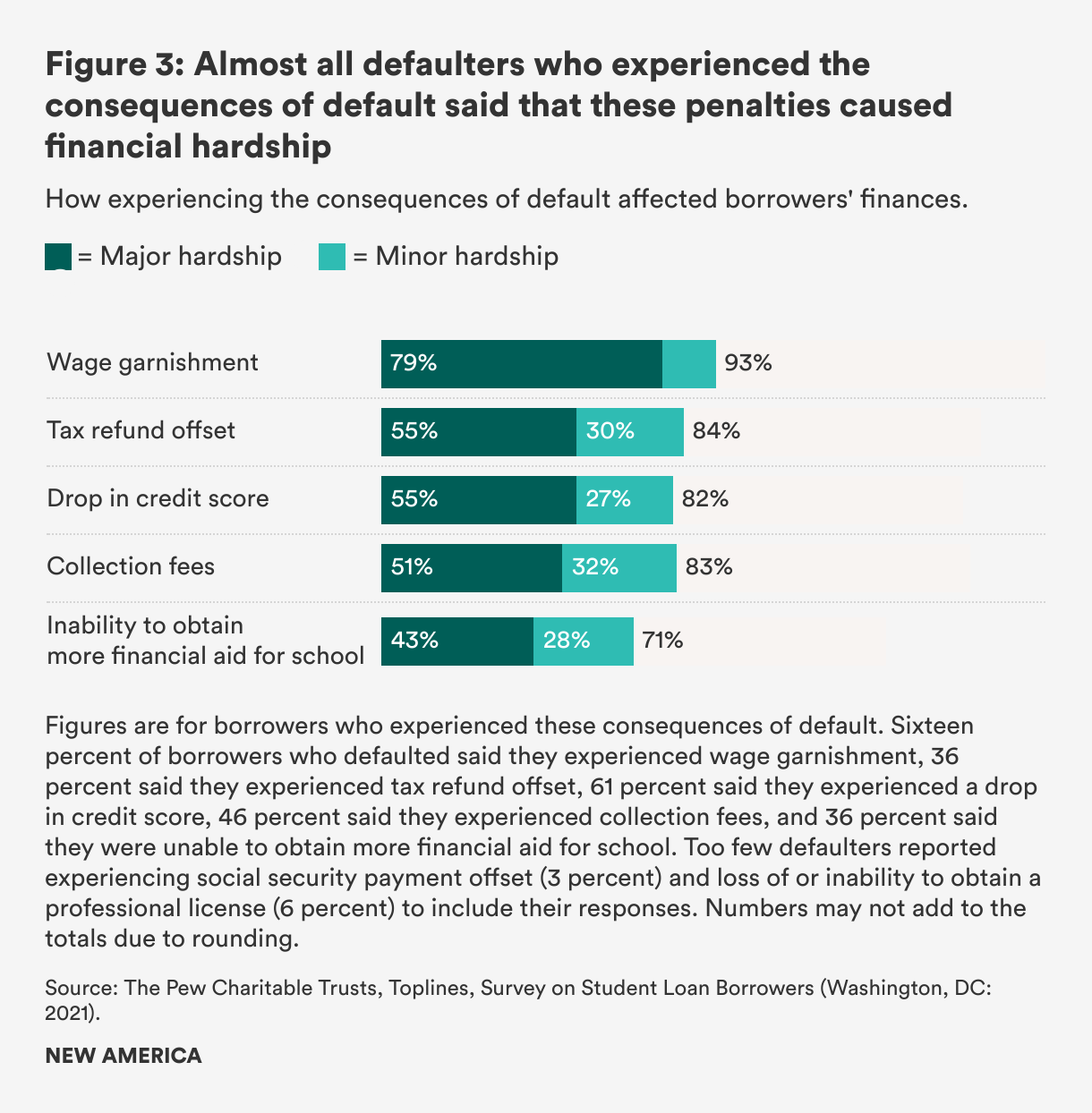

A majority of borrowers who experienced the financial consequences of default indicated that the penalties jeopardized their economic security. Almost all defaulters (93 percent) who reported experiencing wage garnishment—and more than eight in ten of those who experienced tax refund offset (84 percent), a drop in credit score (82 percent), and collection fees (83 percent)—said that these penalties caused financial hardship. (See Figure 3.) Many reported not having heard of some or all of these penalties before defaulting, so they may have surprised some families with tight budgets and little margin for error.

It is not surprising, then, that borrowers’ main reasons for getting out of or trying to get out of default centered around financial security. Almost half (45 percent) reported wanting to end a financial consequence of default including improving a credit score or ending wage garnishment, tax refund offset, or withholding of Social Security payments. Ten percent wanted to be able to take out additional loans to return to school, potentially to unlock the opportunities that come with completing a degree or credential.

While the publicly available data used in this analysis do not allow for the disaggregation of data by race, gender, income, and other important demographic factors, prior research shows that these financial hardships are disproportionately experienced by those from traditionally underserved and under-resourced communities. For example, Black borrowers, among other borrowers of color, are more likely to have student debt and default on their loans. Low-income and low-wealth borrowers and those who are older, have not completed a degree or credential, attend a for-profit college, are student parents, and are first-generation college students, among others, are more likely to default on their loans. (See Appendix A for additional information on which borrowers are most at risk of defaulting on a student loan.)

Instead of providing a way to help borrowers get back on their feet, the default system traps borrowers in debt, accelerates the growth of their balances, and further jeopardizes their economic security. There are few pathways out of default, some of which can be used only once, and borrowers face different processes and fees for each option. (See Appendix D for more information about pathways to exit default.)

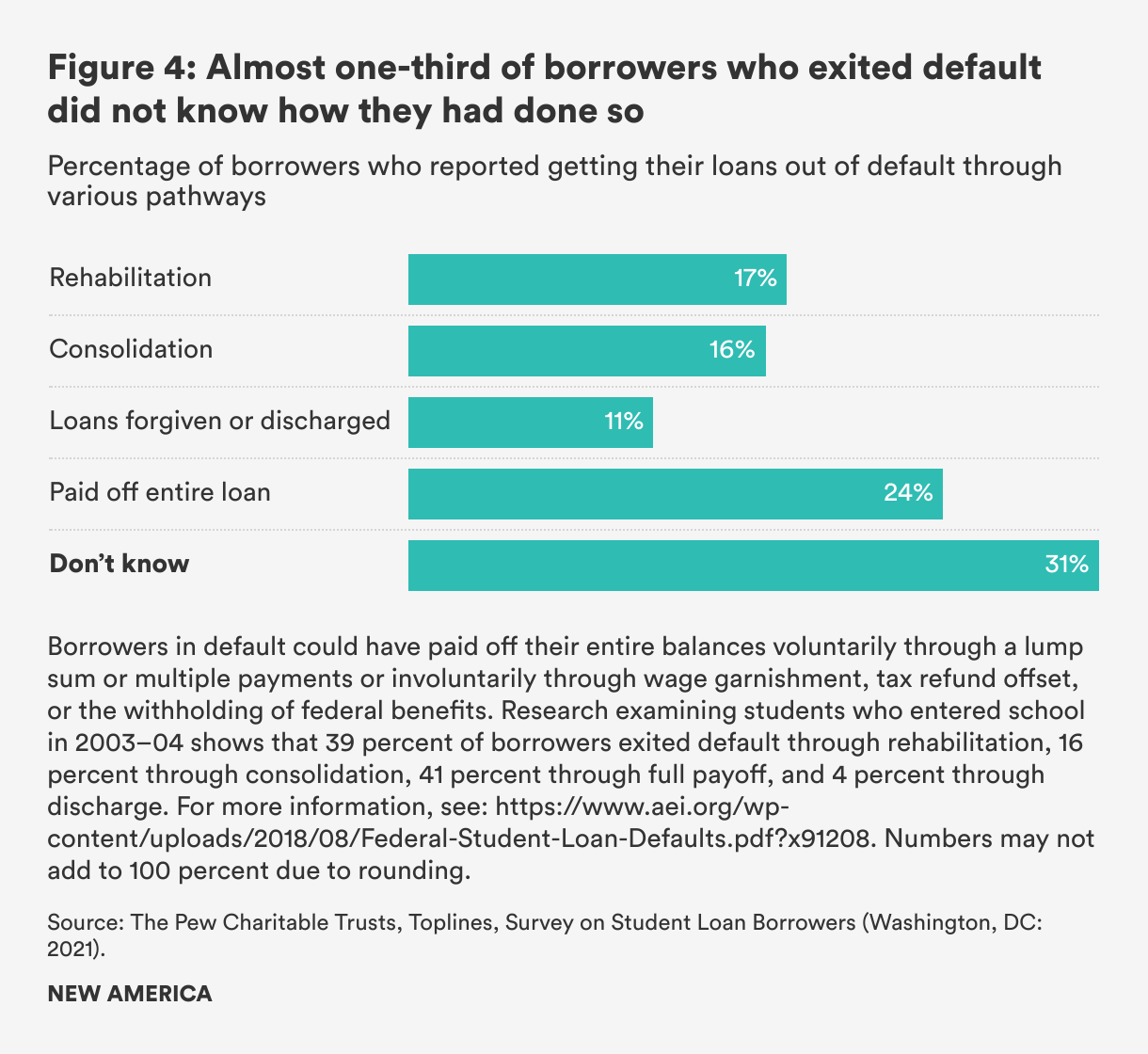

Among those who reported currently being in default (or not knowing the status of their loans immediately prior to the pandemic), 20 percent said they tried to get their loans out of default but were not able to, and one-quarter (25 percent) did not know if they had ever previously gotten their loans out of default. In fact, among those who had gotten their loans out of default, almost one-third (31 percent) said they did not know how they had done so. (See Figure 4.)

Research indicates that approximately one-third of borrowers exit default after two years and slightly more than half exit after three. But many borrowers remain trapped for longer periods or default more than once. This means that they can experience punitive consequences multiple times, have fewer pathways to exit, or, as described above, not know the status of their loans or how to get back into good standing. In fact, some borrowers’ only way out of default is to repay their principal, interest, and fees in full.

Among those defaulters who reported experiencing wage garnishment, more than half (53 percent) had their wages withheld for a year or more. Almost two-thirds (63 percent) of those who reported having their tax refunds offset also indicated it happened for a year or more; more than a quarter (28 percent) said it happened for three or more years. Some of these borrowers may have experienced wage garnishment and tax refund withholding (and other consequences) simultaneously.

A majority of borrowers who defaulted (73 percent) reported communicating with a loan servicer before defaulting. However, perhaps as a result of the complexity described earlier in this piece, almost half (48 percent) reported not knowing how to contact their servicer prior to entering default.[6] As a result, much of this engagement was likely originated by the servicer as the borrower missed payments and became more and more delinquent on his or her loans. Similarly, after defaulting, a majority of borrowers (66 percent) reported communicating with a collection agency; they were also more likely to report that the agency initiated the communication.

Defaulters who reported rarely or never communicating with their servicers said they did not reach out because they could not afford their payments (81 percent) or felt overwhelmed by other events in their lives (77 percent), echoing the reasons they gave for defaulting. Among defaulters who reported rarely or never communicating with collection agencies, the majority (68 percent) also reported being overwhelmed by other events in their lives.

Examining communication between servicers and borrowers in repayment and between previous collection agencies and borrowers in default is important to understanding where reforms are needed to help borrowers avoid default and ensure they are able to exit. While the aggregate data available for this analysis cannot be used to assess many specifics about that communication—including its frequency and consistency, the effectiveness of outreach, reasons for engagement, and how issues were resolved—it does point to the fact that contact alone is not enough. In addition to targeted, consistent, and high quality communication—and holding contractors accountable when they fail to serve borrowers— the system must take into account borrowers' complex realities. The Department must automate and eliminate barriers and “friction points” wherever possible and ensure that borrowers have a clear point of contact throughout repayment.[7]

These data also provide a warning for the end of the payment pause. When borrowers currently in default were asked about how they planned to engage with the system post-pause (the survey was administered before the “fresh start” for borrowers was announced), 26 percent said they did not plan to reach out to a collection agency or would wait for the collector to reach out, and 25 percent said they did not know. A government report released in January indicated that contact information is missing for one-quarter of borrowers in default. Without additional supports, these borrowers are at risk of redefaulting.

The Department of Education and Congress must design a student loan system that makes it easier for borrowers to exit default, prevents redefault, and protects families’ financial security. A well-designed system should take families’ financial realities into account; be easier to access and understand, including being as automated as possible; and create an environment in which the Department and its contractors are held to high standards and work together to ensure borrowers succeed in repayment. While reforms to the default system are necessary, they are also not sufficient. Policymakers must help borrowers avoid default in the first place.

Streamline the Process for Borrowers to Exit Default and Make it Easier to Avoid Redefaulting

Those in default must be able to exit more easily and quickly and the terms and conditions for borrowers exiting default must be consistent.

Protect the Financial Security of Borrowers in Default

The financial consequences of default must be less punitive.

Prevent Defaults in the First Place

While helping borrowers avoid default has not been the focus of this paper, a host of opportunities for reform also exist in this space.

Finally, the Biden administration should extend the current payment pause to ensure the Department of Education can implement both plans for the initiatives mentioned above and for broader debt cancelation before repayment restarts.

The default system exacts severe financial consequences on families that can often least afford them, creating and exacerbating economic insecurity. While there is still more to know about borrowers’ experiences in default, one thing is clear: without reforms, the student loan system will continue to trap borrowers in debt instead of serving as a pathway toward upward economic mobility.

To view the appendices for Trapped by Default please click here.

The author would like to thank Rachel Fishman and Tia Caldwell for editing this brief, Sabrina Detlef for her copyediting support, and Riker Pasterkiewicz, Julie Brosnan, and Fabio Murgia for their communication and data visualization support. The author would also like to thank the Student Loan Research team at the Pew Charitable Trusts for reviewing an early draft.

This analysis was funded by The Joyce Foundation. New America thanks the foundation for its support. The findings and conclusions contained within are those of the author and do not necessarily reflect positions or policies of the reviewers or funder.

[1] Varying Degrees is New America’s nationally representative annual survey seeking to better understand how Americans feel about higher education. The 2022 survey was conducted by NORC at the University of Chicago between April 19 and May 19, 2022, and oversampled individuals with student loans. The margin of error for the general population was +/- 3.47 percentage points, and the margin of error for the student loan borrower sample was +/- 4.04 percentage points.

[2] The survey examines the experiences of borrowers who took out their first federal student loans for their own undergraduate educations between 1998 and 2018. In this issue brief, “those who defaulted,” or “defaulters,” are borrowers who had at least one loan in default at some point over that period, even if they did not have outstanding federal student loan debt or federal loans in default at the time the survey was administered.

[3] This analysis is adapted from the author’s work for the National Association of Student Financial Aid Administrators’ (NASFAA) Protecting Borrowers and Advancing Equity project. Some of this information also appears in NASFAA’s May 2022 report.

[4] A recent delay in this process could postpone these benefits for defaulted borrowers.

[5] At the time this survey was administered, the Department contracted with these collection agencies to manage the loans of borrowers in default; it has since ended those contracts.

[6] A smaller percentage of borrowers who did not experience default reported communicating with a loan servicer (61 percent). These non-defaulters may not have had a reason to contact their servicers, and servicers might not have had a reason to regularly reach out. In fact, 84 percent of non-defaulters who reported rarely or never communicating with their servicers said they communicated as needed and 66 percent said they were paying as usual and everything was fine. But, unlike those in default, 75 percent of non-defaulters reported knowing how to get in touch with servicers if needed.

[7] The Department of Education’s Office of Federal Student Aid (FSA) has announced a plan to move toward a single FSA brand for communication with borrowers. While this will likely reduce confusion, FSA must also ensure that individual actors operating under this brand can be held accountable.

[8] Incarcerated borrowers will soon have their access to Pell Grants restored. The Department must make sure those in default have access to “fresh start” to guarantee their eligibility for this financial aid.

[9] Through the ongoing negotiated rulemaking process, the Department has signaled a willingness to include policy provisions that permit those in default to access income-driven plans and must ensure that those provisions are included in the final rule.

Project Director, Education, Opportunity, and Mobility