Amy Laitinen

Senior Director, Higher Education

The COVID-19 pandemic and resulting economic crisis has brought unprecedented challenges to higher education. Since summer, New America has partnered with the State Higher Education Executive Officers Association (SHEEO) to understand the impacts of the pandemic on institutional policies, consumer protection, and finance through interviews with representatives from institutions and systems of higher education, professional associations, and students. This blog is part of a series in which we sum up findings from these interviews. You can explore findings regarding the pandemic's impacts on institutional finance here, and institutional policy here.

The COVID-19 pandemic has left college students around the country scrambling: facing income loss and new caretaking responsibilities that make enrolling in higher education much harder and struggling to succeed in the world of online learning, but left with few opportunities and potentially unaffordable student debt if they leave school without completing their programs.

Unfortunately, even with a vaccine in the works, the light at the end of the tunnel is still a long way off. The Great Recession saw a spike in postsecondary enrollment that accompanied high rates of unemployment. The increase was particularly pronounced at for-profit colleges, many of which engaged in aggressive and predatory recruiting efforts that spawned the eventual collapse of giants like Corinthian Colleges and ITT Tech and a later influx of claims for student loan relief from borrowers. Outstanding student loan debt drastically increased during those years, and the growth at for-profit and two-year institutions fueled an increase in student loan defaults. The question with the current pandemic and recession, of course, is which of these concerns will be repeated?

To find out, New America and the State Higher Education Executive Officers (SHEEO) Association have interviewed dozens of experts, including student advocates, accrediting agencies, state authorizing officials, and industry watchers. We’ve also closely followed publicly traded higher education companies’ quarterly earnings statements, tracked Title IV volume and enrollment fluctuations, and assessed the financial viability of private colleges in the system.

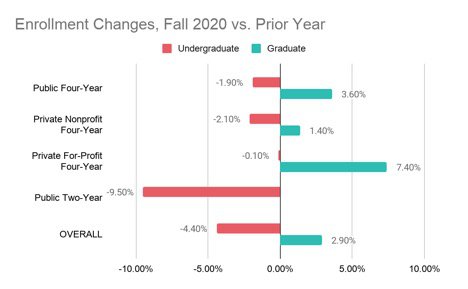

In part, it’s too soon to say whether or how history will repeat itself. Postsecondary enrollment usually jumps when unemployment is high, in a counter-cyclical relationship; in particular, for-profit colleges and community colleges see new enrollment. But the public health crisis has meant the trends are not so clear-cut. Undergraduate enrollment at public and nonprofit four-year colleges this fall was down by around 2 percent compared with last year. But enrollment in community colleges’ certificate and associate degree programs, which usually grow during a recession, were steeply down, by more than 9 percent. Meanwhile, graduate enrollment has increased, especially at for-profit colleges.

Our interviewees told us this was true for a number of reasons: increased caretaking responsibilities among community college students, the sense that the current economic downturn is temporary, and an aversion to online learning or insufficient access to the technology needed for it. Enrollment of first-time, first-year students has dropped precipitously; Black, Hispanic, and Native American enrollment of first-year students is all down by more than a quarter at community colleges, and by 18 to 23 percent nationally. These trends are concerning for a lot of reasons.

For starters, increases in graduate enrollment (particularly at for-profit colleges) are likely to lead to substantial increases in student debt — and are often offered without evidence that those programs will lead to valuable credentials for the student. Grad PLUS loans aren’t included in the cohort default rate metric, which tests colleges on their students’ ability to repay their loans after leaving school; and with little transparency into their programs, are often able to charge too much in exchange for little value.

At the same time, declines in undergraduate enrollment will leave many institutions desperate. This semester, even many of the colleges that remained mostly or entirely online in the fall plan to reopen their doors. That will likely exacerbate the pandemic, but school officials told us they see reopening campuses as essential for ensuring students are willing to enroll — and pay tuition, room, and board.

Many are doubling down on recruiting and enrolling more students to fill the gaps in their budgets, too. As The Century Foundation has reported, some colleges are beginning to adopt pandemic-related marketing and COVID-related enrollment incentives for prospective students. Other schools are looking ahead to the future, our interviewees told us, and pursuing long-term contracts with companies that will offer online programs for the school in exchange for a cut of the revenue — creating incentives for those online program management (OPM) companies, which often handle recruitment of students, to aggressively enroll new students and lower the bar for admission.

Those approaches should raise alarms among regulators concerned with protecting would-be students. But regulators must also be wary of the schools that won’t make it through the crisis. While there hasn’t been a rush of college closures since the start of the pandemic, the CARES Act funding from March played a big role in helping to plug this year’s budget holes. And no doubt, the $23 billion passed in additional funding around the end of the year will provide substantial additional relief. Our interviews revealed that many colleges are hanging on by a thread, hoping for more federal relief funding and a return to normalcy. With margins for many colleges tight even before the start of the pandemic, not all schools will make it; permanent closures will, eventually, likely hit.

But our monitoring of actions from states, accreditors, and the Department of Education has surfaced another concern: inaction. In the early days of the pandemic, regulators were—rightly—seeking to provide substantial flexibility to help schools close their campuses and wind down their spring semesters without too much red tape.

More than nine months in, little has changed. States, accreditors, and the federal government have all largely maintained the flexibilities offered for the spring 2020 semester. While accrediting agencies are generally now requiring institutions that hadn’t previously offered distance education to seek approval, that’s about the only new requirement that’s been levied consistently — despite reports that many students are dissatisfied with their online learning experiences. Most states and accrediting agencies aren’t collecting new or timely data on things like student retention, faculty engagement in online courses, institutional finances, or enrollment declines/increases, although some have conducted surveys among their member institutions. And few are taking steps, beyond reiterating their current policies, to facilitate credit transfer for students who choose to move institutions. While several accreditors noted concern about increased interest in the use of OPM contracts, and the likelihood of permanent closures among struggling institutions, most of them haven’t issued any guidance to schools or established any new protections since the start of the pandemic reflecting that concern.

Congress has sometimes followed suit. Provisions in the CARES Act and the end-of-year funding package provided funding directly to institutions (and, through them, to students); flexibility on institutional refunds and the measurement of satisfactory academic progress; and other waivers and wiggle room. But only a few provisions have addressed key consumer protection concerns. For instance, the CARES Act and the end-of-year package both limited the use of institutional relief dollars from being spent on payments to contractors for pre-enrollment recruitment activities — a nod to the risk of online program management companies. And a later proposal by House Democrats (not included in the legislation passed by Congress) allowed certain institutions at risk of failing federal financial responsibility rules to avoid a requirement to post a letter of credit with the Department, provided they began to establish plans for winding down in the event of permanent closure. But efforts to protect consumers have largely stagnated. And as one expert put it to us, “Institutions have… convincingly positioned real regulatory relief as a freebie for Congress to give them,” appealing next to their $120-billion ask for funding, of which lawmakers have provided only a portion.

As the pandemic wears on, the status quo becomes less and less acceptable. And the risks to students continue to grow — that their colleges will fail to provide a high-quality educational experience in the online environment, or engage in predatory or aggressive recruiting practices, or even shutter altogether without warning. Without action, we could be doomed to repeat the mistakes of the Great Recession.

Enjoy what you read? Subscribe to our newsletter to receive updates on what’s new in Education Policy!

Senior Director, Higher Education

Policy Analyst, Higher Education

Project Director, Higher Education