Tia Caldwell

Senior Policy Analyst, Higher Education

Disproportionately women and people of color, they are no better off than peers with only a high school education

The number of Americans nearing retirement age with student loan debt skyrocketed 500 percent in the last two decades. While some of these borrowers hold loans taken out to help a relative attend college, our first blog in this series highlights that many, if not most, still owe debt from their own college experience. In this post, we explore the demographics and financial well-being of older Americans with student loan debt from their own education.

A recent working paper by staff at the Federal Reserve provides key context for understanding this population. The researchers found that most people who borrow for college enjoy similar lifetime wage and savings boosts as other college-educated people. Student loan borrowers likely use this increased income to repay their debt over the years. By the time they approach retirement, most have paid off their student loans and built up retirement savings. This finding matches other research indicating that higher education is a good lifetime investment for most students, even the students that have to borrow to attend college.

But the Federal Reserve’s working paper suggests that a sizable number of borrowers are not so lucky. These borrowers never see the hoped-for financial return on their educational investment. We know from our previous work that the low return on investment may be because students attended a low-quality or predatory program, did not complete a degree, experienced health issues, and/or experienced racial discrimination and systemic inequities in the labor market. These borrowers struggle with their payments over the years, often experiencing growing balances and defaults, even as others who did see an earnings boost from college pay down their loans. As they near retirement age, the borrowers still in the repayment system are, according to the Federal Reserve researchers, “no better off than their peers who did not go to college.”

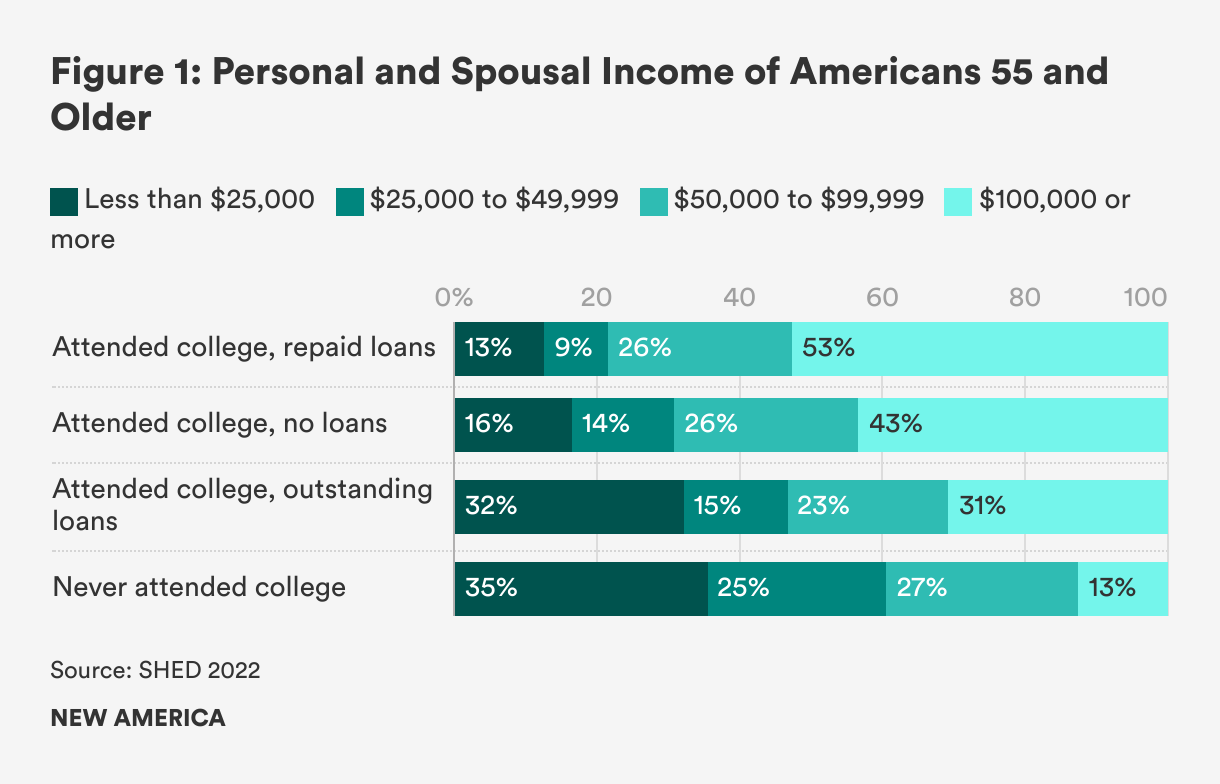

We build on these insights by analyzing the well-being of older Americans using the 2022 Survey of Household Economics and Decisionmaking (SHED). We compare four distinct groups of individuals 55 and older: those that attended college and did not borrow (45 percent), those that borrowed for their college education and repaid their loans (17 percent), those that still hold outstanding debt from their college loans (5 percent), and those that never attended college (34 percent). (These numbers total to more than 100 percent due to rounding.)

Like the Federal Reserve researchers, we find that older Americans who attended college and repaid their loans tend to be relatively well off: more than half (53 percent) make over $100,000, including income from their spouse (Figure 1). This is slightly higher than the proportion earning more than $100,000 among seniors who went to college and did not take out loans (43 percent), likely because these borrowers have higher levels of education. In contrast, approximately one-third of seniors who have not yet repaid their student loans earn less than $25,000, a similar percentage to those who never went to college.

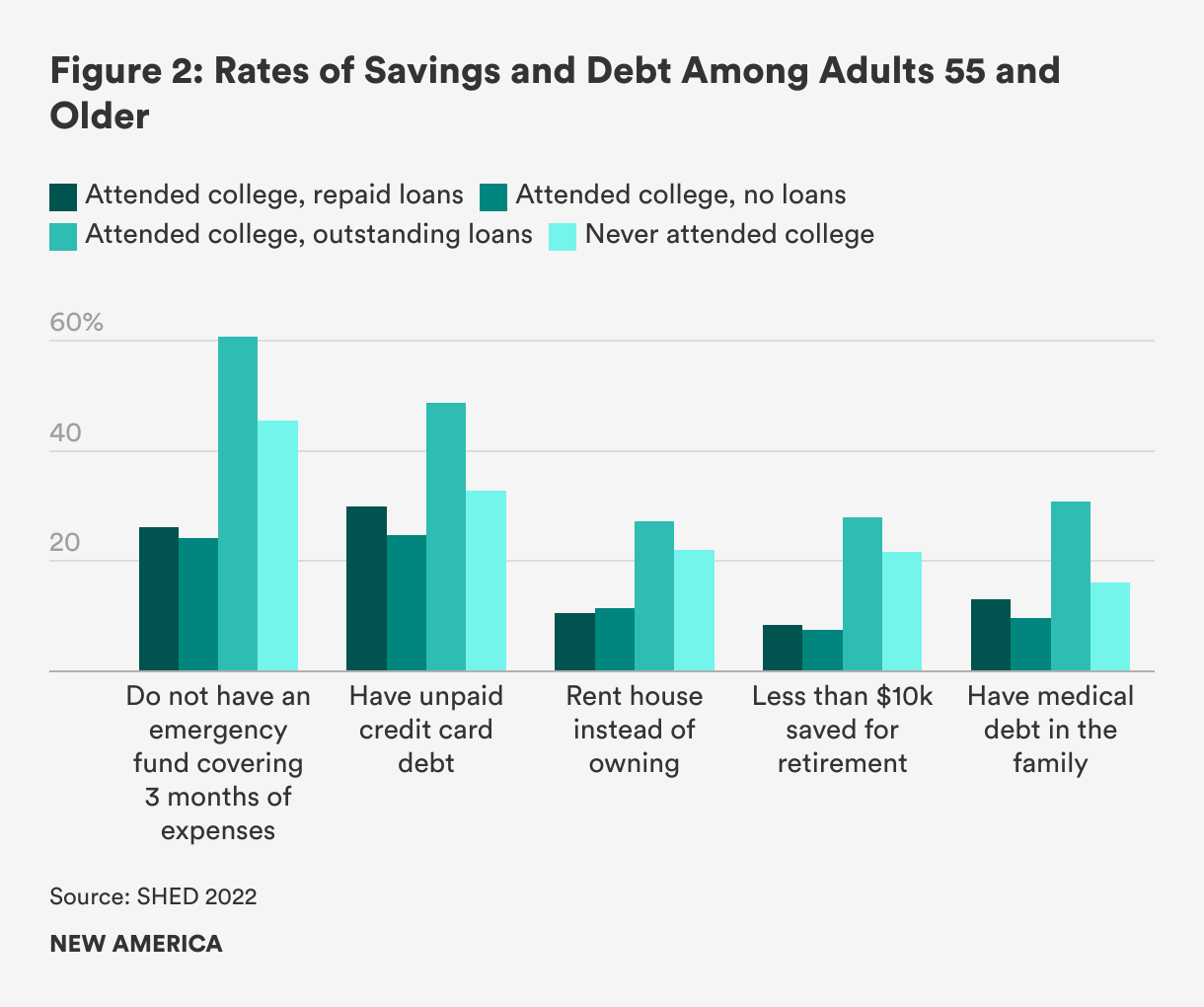

Borrowers with outstanding student loans who are age 55 and older fare the same or worse than their high school-educated peers in measures of wealth and financial hardship (Figure 2). Their homeownership rates, which have been falling over time, are similar to the rates of those who never attended college. Their cash savings are unusually low: 61 percent say they do not have an emergency fund that could cover expenses for three months, compared to 46 percent of seniors who never attended college. Twenty-eight percent have less than $10,000 saved for their retirement, a higher rate than other college attendees and non-college-educated peers. In addition to having low savings and assets, these borrowers are more likely to have debt other than student loans. About one in three have medical debts, double the rate among seniors who never attended college. Half have unpaid credit card debt, compared to a third of older adults who did not attend college.

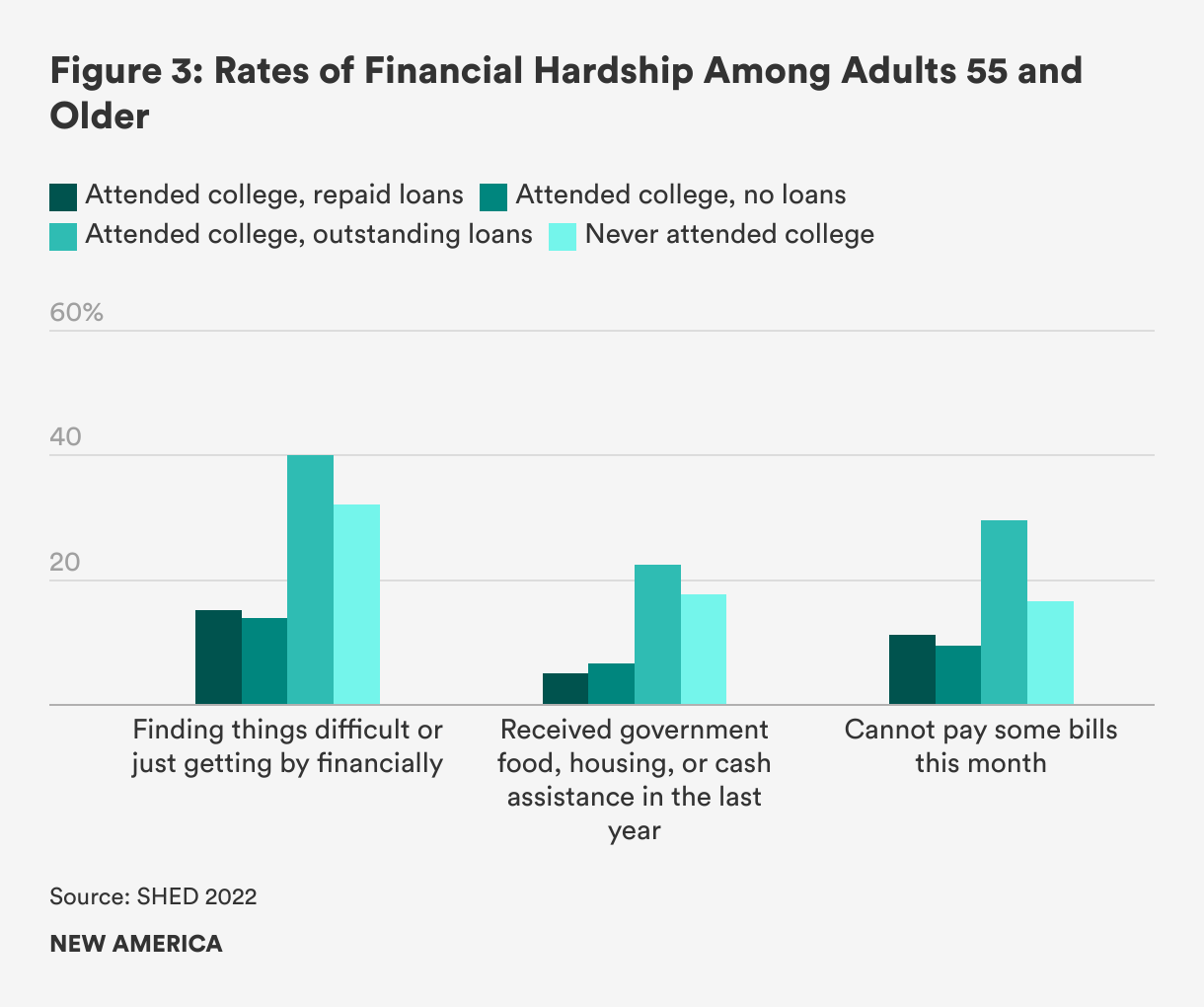

With low incomes and limited savings, many of these borrowers find it hard to make ends meet. Figure 3 shows that 40 percent of older adults with outstanding loans for their own education say they are just getting by or finding it difficult to manage financially. Almost a quarter received government food, housing, or cash assistance in the last year, and close to a third cannot pay all of their monthly bills, including student loans. In 2019, before the pandemic payment pause, 29 percent of older borrowers with outstanding debt from college reported being behind on their student loans, compared to 16 percent of this group of younger borrowers. These rates of hardship are similar to or higher than the rates among seniors who never attended college and much higher than borrowers who have already repaid their student loans.

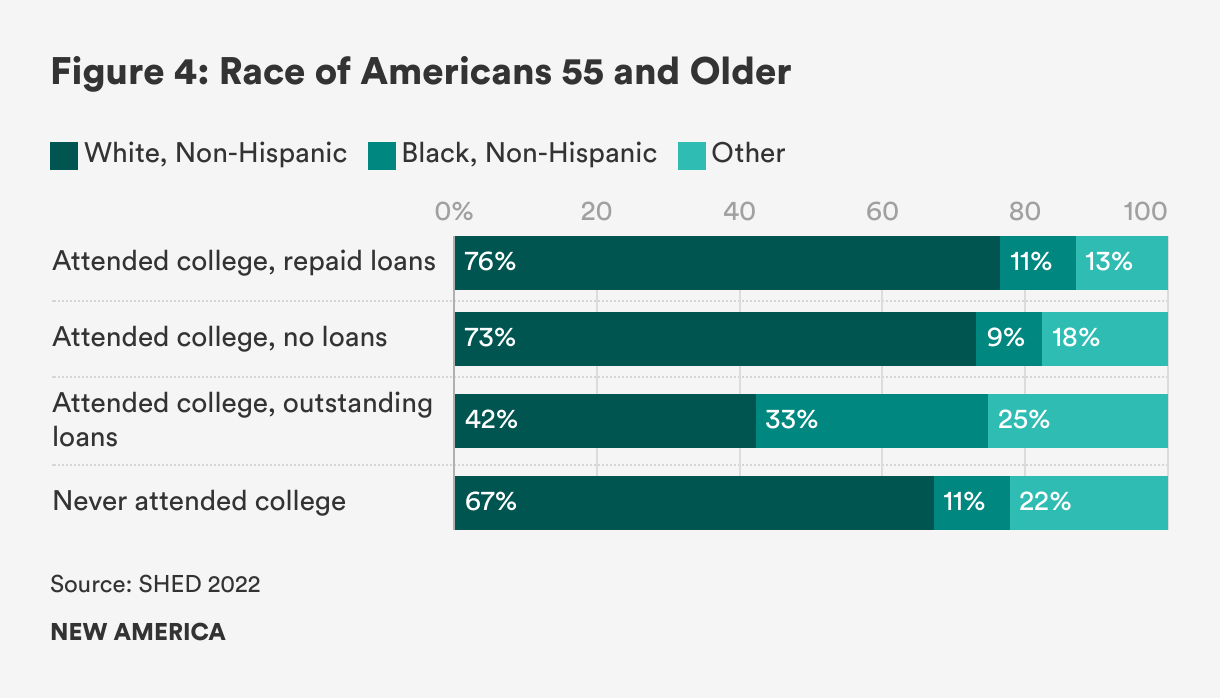

Demographic trends provide further evidence that disadvantaged college students are less likely to repay their student loans before retirement age. According to the SHED, about one in ten of the older Americans who attended college and did not borrow or already repaid their student loans is Black or African American (see Figure 4). In contrast, one in three older Americans with outstanding student loans is Black. African Americans are more likely to attend underfunded schools, come from a family with low wealth, face labor market discrimination, and experience poorer health outcomes and care. These factors mean that Black borrowers are less likely to keep up with interest on their loans and more likely to default over time. While the small sample size in this analysis prohibits a finer breakdown, other borrowers of color are also overrepresented among seniors with outstanding student loan debt. Similarly, women, who are more likely to be in poverty than men, make up 51 percent of older Americans who attended college but 61 percent of older borrowers with outstanding student loan debt.

The SHED contains other hints about why this subset of college attendees had a less fruitful college experience than others. These borrowers were four times more likely than other college attendees to have gone to a for-profit college, which are often expensive and low-value. Thirty-five percent never completed a postsecondary degree, which tends to lead to lower wages, compared to 17 percent of those who repaid their loans and 30 percent of all college attendees.

Survey data also confirm that older borrowers with outstanding debt attended college decades ago. As noted in our first blog in this series, the Survey of Consumer Finances shows that heads of households over 55 with their own student loans have been in repayment for an average of 14 years. According to the SHED, older Americans with outstanding loans earned their highest degree (which could have occurred earlier than their most recent school attendance) an average of 26 years ago, compared to 38 for college attendees who repaid their loans. Although borrowers with outstanding loans attended school more recently than those who repaid their debts, both groups have had many years to recoup their college investments and repay their loans.

Overall, survey data paint a picture consistent with the story told by Federal Reserve researchers. College works out well for most students, including students who take out loans. Yet a subset of students does not see income gains after college, perhaps because they attended a low-value program, did not complete their degree, or faced systemic barriers in the labor market and beyond. Their low incomes and low savings make it hard to repay their loans over the years, even as their peers exit repayment. By the time these college attendees near retirement, they are no better off than if they never attended higher education in the first place.

New America would like to thank the RRF Foundation for Aging for its support of this work.

Enjoy what you read? Subscribe to our newsletter to receive updates on what’s new in Education Policy!

Senior Policy Analyst, Higher Education

Project Director, Education, Opportunity, and Mobility