Tia Caldwell

Senior Policy Analyst, Higher Education

Almost all HBCUs & MSI graduate programs pass

New gainful employment regulations proposed by the Biden administration promise to be the strongest consumer protections for college students in years. The rules would prevent for-profit and short-term certificate programs with high debt burdens or low earnings from remaining eligible for federal student aid. Low-performing programs at nonprofit and public institutions, which cannot lose access to federal aid based on gainful employment outcomes under current law, may need to notify prospective students of poor debt-to-earnings outcomes.

A key question is whether the rule can catch low-performing programs without punishing programs that add value for low-resourced and historically disadvantaged students. Previous estimates from New America suggest that, on the whole, the rules successfully thread this needle. While many programs at profit-driven schools will lose eligibility for federal aid unless they improve, there will be minimal disruptions at nonprofit and public schools, including Historically Black Colleges and Universities (HBCUs), Hispanic-serving institutions (HSIs), and other minority-serving institutions (MSIs).

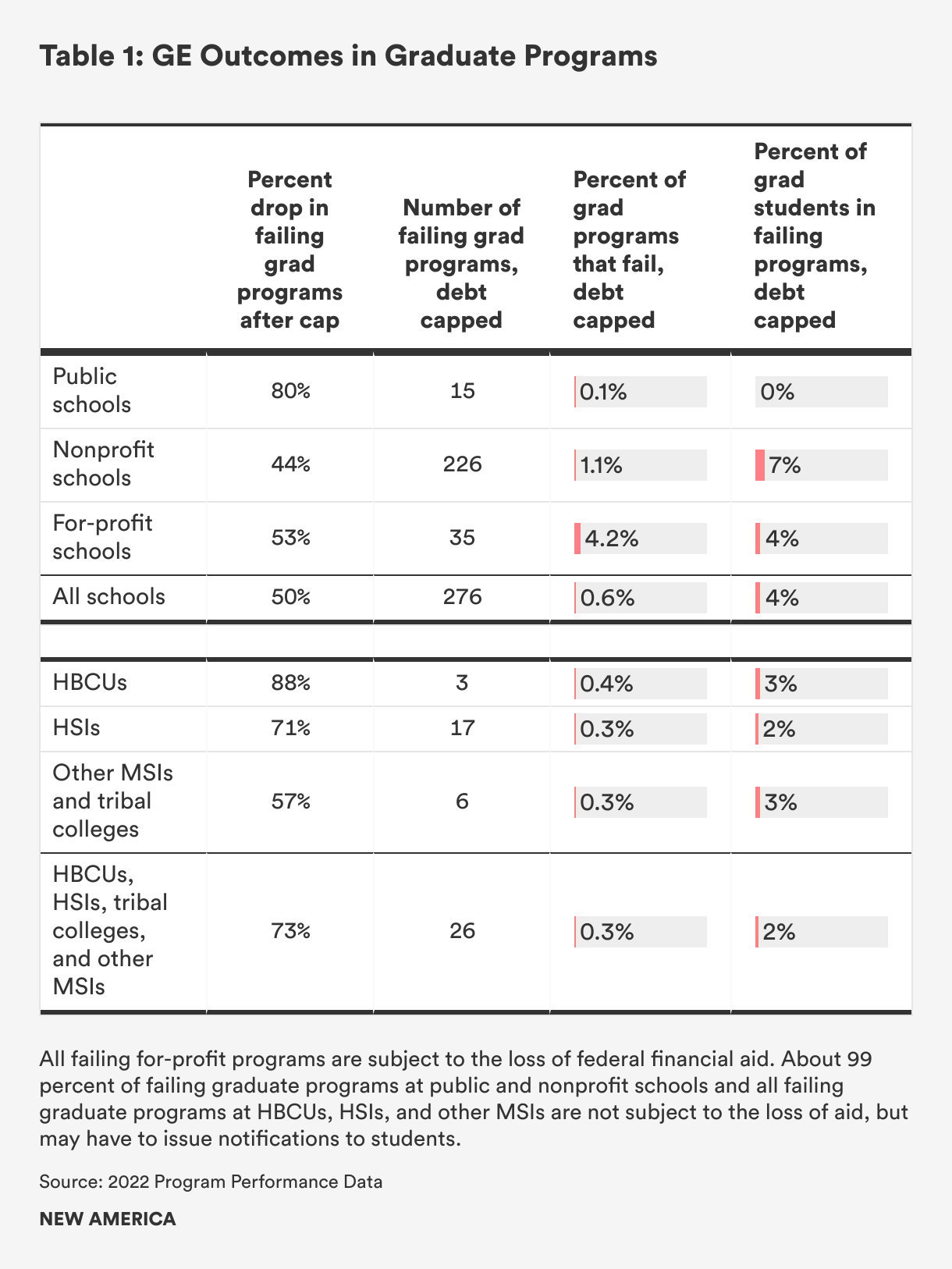

Previous projected failure rates at mission-driven schools were already low, but in this analysis, we show that even those projected failures were overstated. Earlier estimates did not account for a key detail of the proposed rule – a cap on the amount of debt considered in the debt-to-earnings test that excludes borrowing for living costs. This detail matters: once we approximate the effect of the debt cap, total failures drop by about ten percent, and nearly all graduate and professional programs at HBCUs, HSIs, and other MSIs pass the gainful employment test.

The cap will limit countable debt to the cost of net tuition, fees, books, and supplies. Debt that students take out above this amount, such as loans needed for food, housing, or other living expenses, will not be counted. The cap ensures that gainful employment’s debt measurement is a function of what schools charge their graduates, not a function of students’ overall financial need. Thanks to the cap, schools charging low tuition will not be punished for admitting students who need to borrow for the costs of living, and schools providing institutional grant aid will be credited with a lower tuition cap.

Although the debt cap is fundamental to the debt-to-earnings test, data limitations prevented previous estimates of gainful employment passage rates from considering the cap. As the Department of Education explained, properly implementing the cap “requires additional institutional reporting of relevant data items not currently available to the Department.” Instead, using the data schools already report on tuition and other costs, we were able to approximate the impact of the cap. (Since we do not observe institutional grant aid, our estimated cap is likely higher on average than the actual cap, and overestimates failures among programs that offer grant aid to most students. See the Methods section for more about our estimates.)

Before capping median debt, around 2 percent of all postsecondary programs enrolling 8 percent of students were projected to fail gainful employment, including 22 percent of for-profit programs and 1 percent of public and nonprofit programs. All failing for-profit programs are subject to the loss of federal aid. In contrast, more than 90 percent of students in failing programs at public and nonprofit schools (both with and without the debt cap) are in programs that may have to notify students of poor outcomes, but are not at risk of losing federal aid.

Capping median debt at direct costs lowers total gainful employment failures for all students by around 10 percent. Across all sectors, the newly passing programs are concentrated at the graduate level. Strict federal loan limits constrain how much undergraduates can borrow, preventing high undergraduate borrowing for living expenses. In contrast, graduate-level students are allowed to borrow to cover their entire cost of attendance, including living expenses. Because of this, and because the highest-quality cost data covers more students at the graduate level, we focus the rest of our analysis on graduate programs.

Even without the debt cap, most graduate programs at mission-driven schools were projected to fare well under gainful employment. Just 1 percent of graduate programs with 8 percent of graduate students at public and nonprofit schools were projected to fail. The direct-cost cap would reduce these numbers by more than 50 percent (See Table 1). We estimate only 4 percent of public and nonprofit graduate students will be in failing programs.

Failures in previous estimates were especially overstated among institutions that serve many students of color. With the debt cap in place, only 17 programs making up just 2 percent of HSI graduate enrollment fail, out of over 5,000 programs. This corresponds with more than a 70 percent drop in the share of HSI graduate students enrolled in failing programs.

Graduate program failures at HBCUs were previously overstated more than any other sector. The percentage of graduate students in failing programs falls by over 80 percent, and by 15 percentage points, once median debt is capped. Only 3 out of 810 graduate programs at HBCUs fail, and those programs serve just three percent of HBCU graduate students. Accounting for the debt cap has a sizable impact on HBCUs as a whole; the number of undergraduate and graduate students in failing programs declines by more than 25 percent.

These lower failure rates reflect mission-driven schools’ commitment to keeping tuition relatively affordable for their high-need students. Consider Howard School of Law, an HBCU program that previously had been projected to fail the debt-to-earnings test. While the median Howard Law graduate leaves the program with about $150,000 in debt, a third of that is above the $100,000 charged for tuition, fees, and books over the course of the three-year program. (While $100,000 is a lot of money, more than half of all law schools charge even higher direct costs). The typical Howard Law graduate goes on to make over $70,000 three years after graduation, enough to support debt from the price of tuition and other direct costs. With the cap in place, successful programs like Howard Law, which are not subject to the loss of federal aid dollars under gainful employment, will not have to issue notifications to students.

The fact that prestigious programs like Howard Law pass gainful employment after the debt cap reflects well on the fairness of the test. We know that graduate programs at HBCUs, HSIs, and other MSIs are important for increasing diversity in positions of power and improving economic mobility. HBCUs produce many more Black professionals than their small numbers would suggest, graduating half of Black doctors and attorneys and 40 percent of Black engineers. HBCUs have been held up as successful case studies for increasing diversity among the highest-earnings fields, while other MSIs have also been a source of study for best educational practices. Hispanic-serving institutions, which represent approximately 20 percent of the higher education sector yet enroll around 40 percent of Latino graduate students, have been shown to provide the most economic mobility for their students.

Our findings are a testament to the success of HBCUs and minority-serving institutions, which have achieved a higher passage rate than other graduate programs, all while supporting historically disadvantaged students with limited budgets. The findings also underscore the Department of Education’s success in carefully considering the ramifications and fairness of each detail of the proposed gainful employment rule.

To estimate which programs would pass and fail the proposed gainful employment regulations, the Department of Education released 2022 Program Performance Data (PPD). The data are imperfect estimates because data for some parts of the test are not currently collected. Colleges will need to report the costs and institutional aid for each program to implement the debt cap for the debt-to-earnings ratio. Since those data do not yet exist, the Department of Education estimated passage rates without capping debt amounts.

New America approximated the debt cap using the tuition data that schools already report to the Department of Education, compiled by the Urban Institute. Schools currently share program-level tuition for several professional graduate programs and short-term programs. They also report average listed tuition for all other graduate programs and all undergraduate programs for in-state and out-of-state students. We used these variables to approximate the median graduates’ tuition costs. We used in-state tuition if more than half of students attended in-state and out-of-state tuition if fewer than half of students attended in-state. We added the costs of books and supplies, which are reported as the average for undergraduates across an institution. When the costs of books and supplies were not available, we added $1,300 per year, the average among the schools with data.

We multiplied the yearly cost of tuition, fees, books, and supplies cost by the typical length of the program to arrive at the estimated direct-cost debt cap. For example, yearly costs were multiplied by two for associate degree programs and by four for bachelor's degree programs. As in the original PPD, our debt measure does not include private loan debt, which might push debt slightly higher. But our direct-cost cap likely leans too high (meaning it overestimates program failures) because we use listed tuition rather than tuition minus institutional aid.

New America made one other small adjustment to the 2022 Program Performance Data. The proposed rule says that the earnings of certain professional-level programs were set to missing in the PPD. This was done because earnings are measured at 3 years in the PPD data but, according to the proposed rule, will be measured at 6 years if programs require a residency. Yet the PPD does include non-missing data for the programs that likely require residencies. We switched medical, dental, and osteopathy professional programs to missing, as the Department seemed to intend, for both the unadjusted and debt-capped estimates. While we think the change increases the accuracy of the estimates, it does not substantially change the results. The change affects only 22 failing programs, and the proportion of students in failing programs changes by only half a percentage point.

This is part of a collection of New America's recent work on gainful employment. Read about: Earlier analysis of how MSIs do under GE | MSI analysis updated with new data | Our support for the proposed rule | Ways to strengthen the rule | One borrower's experience without GE protections | GE's earnings threshold compared to a minimum wage

Senior Policy Analyst, Higher Education