Sarah Sattelmeyer

Project Director, Education, Opportunity, and Mobility

Survey Results Show Vulnerable Student Loan Borrowers Are at Risk of Missing Out on Debt Relief

Over the last several years, the Biden administration has taken important steps toward ensuring the student loan repayment system is more affordable, accessible, and does not trap borrowers in a lifetime of debt. It has made a host of loan discharge and forgiveness programs, including the borrower defense to repayment process, total and permanent disability discharges, and the Public Service Loan Forgiveness Program (PSLF), easier to access.[1] It has provided temporary relief for borrowers in default along with a more permanent pathway to being current on their loans through the Fresh Start program.[2] And, among many other efforts—including up to $20,000 in loan cancellation awaiting a ruling from the Supreme Court—it is reforming the loan servicing system to increase transparency and accountability.[3]

However, the Department of Education’s newly proposed income-driven repayment (IDR) plan may do the most, in the long term, to provide relief to borrowers struggling with student debt. The plan would lower payments for many, help them manage balance growth, require shorter repayment periods for those with the lowest balances, and reduce burdensome enrollment and recertification processes.[4] For the first time, borrowers who fall behind on their loans could be automatically enrolled in—and many of those in default would be able to access—an IDR plan.

IDR plans base payments on a borrower’s income and family size, which means that those who make the least can have low or even $0 payments due each month.[5] Borrowers’ remaining balances are forgiven after a set number of payments, and those enrolled in IDR plans are less likely to default on their loans.[6] But borrowers need to take action to receive these benefits by opting into an IDR plan. (Even under the administration’s new proposal, borrowers who fall behind on their loans must have consented to sharing their tax information to be automatically enrolled.) IDR plans, like many of the student loan initiatives mentioned above, are not automatic. And some borrowers may have started off at a disadvantage. Traditionally, the programs have been confusing and complex to administer, and the Department and its contractors have a history of providing inadequate repayment information to borrowers and mishandling the implementation of existing IDR programs.[7]

New analysis from New America’s latest nationally representative Varying Degrees survey—which was administered in 2022 and includes interviews with 1,156 student loan borrowers—shows that the borrowers who could benefit the most from repayment relief are at highest risk of missing out on these new benefits. It does not have to be this way. Low-income and low-balance borrowers, those who have defaulted on their loans, and borrowers approaching retirement are the least likely to know about IDR plans. But when these borrowers do know about IDR, they are the most likely to enroll.

As the Department rolls out its new IDR plan and other opt-in initiatives, it will need to automate access, adapt materials to reach vulnerable populations, engage in widespread outreach with trusted partners, and provide strong oversight of its contractors. But large-scale communication efforts are expensive, and the Department’s Office of Federal Student Aid (FSA), which oversees these programs, has never had so much to do with so few resources to go around. Ultimately, ensuring that the most vulnerable borrowers are able to access repayment relief must involve action from the Department and its contractors, funding from Congress, and engagement from the higher education community.

Seventy-three percent of borrowers in the Varying Degrees sample reported knowing about IDR. This widespread knowledge—as also reported in other surveys—is a good news story.[8] It is likely due, at least in part, to the broad availability of IDR plans; widespread and targeted efforts from government, consumer groups, and others to increase borrower awareness and access; and an increase in public attention to student loans over the last several years, including a focus on PSLF.[9] (To qualify for PSLF, borrowers typically have to be making payments under an IDR plan.)

Varying Degrees data show that 45 percent of borrowers have enrolled in an IDR plan at some point during their time in repayment. Those currently in IDR overwhelmingly agreed that they needed to be enrolled in the plan to manage their bills and the amount of time spent in repayment. Nine in 10 agreed that IDR was the only way they could afford their loans. And more than eight in 10 said they chose IDR because it provided access to eventual loan forgiveness, for which they are eligible after 20 to 25 years’ worth of qualifying payments.

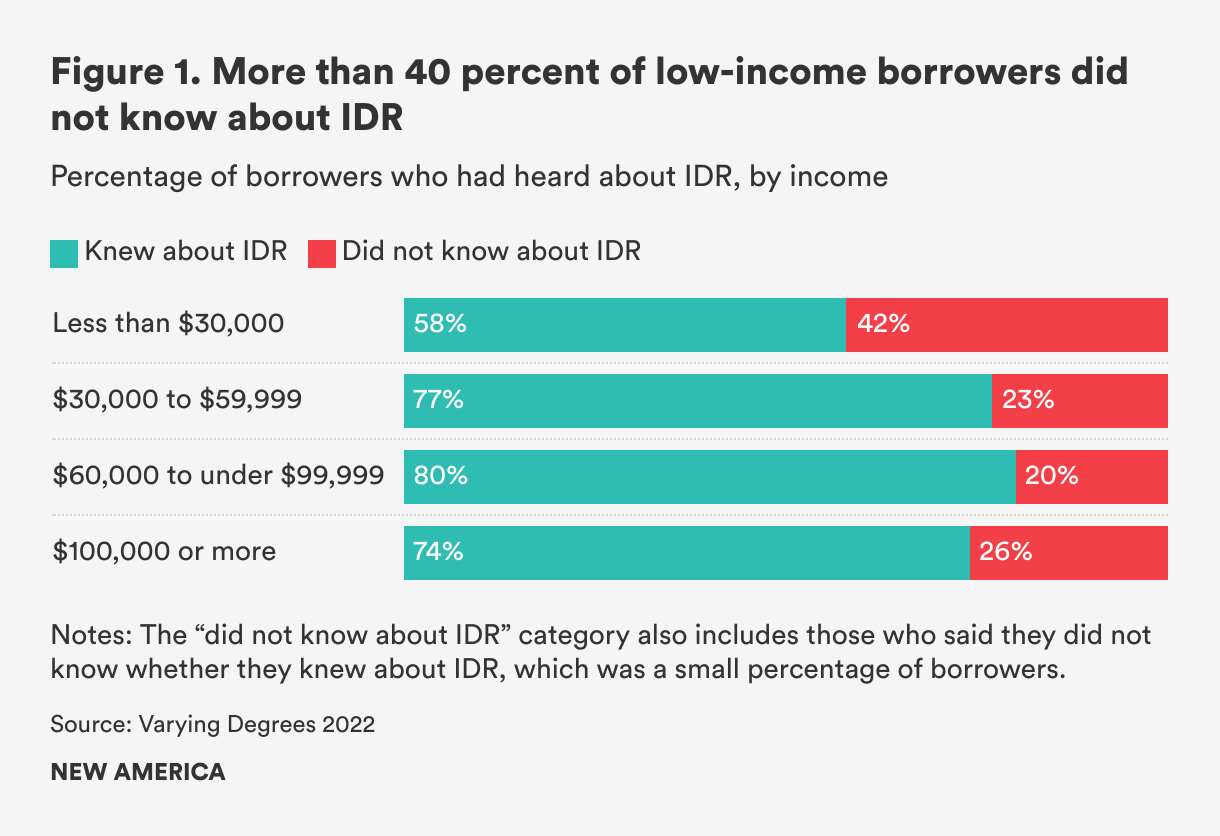

IDR is designed to provide relief for borrowers with lower than expected earnings, but only 58 percent of borrowers with incomes under $30,000 reported knowing about IDR, compared to three-quarters or more of borrowers in higher-earning groups (see Figure 1). Borrowers earning less than $30,000 would be eligible for $0 payments in the Department’s proposed new IDR plan, slated to be released later this year.[10] Borrowers in this income group would also have low or $0 payments in currently available IDR plans.[11] Those who described themselves as not at all financially secure, no matter their income level, were also less likely to have heard of IDR than their very financially secure peers.

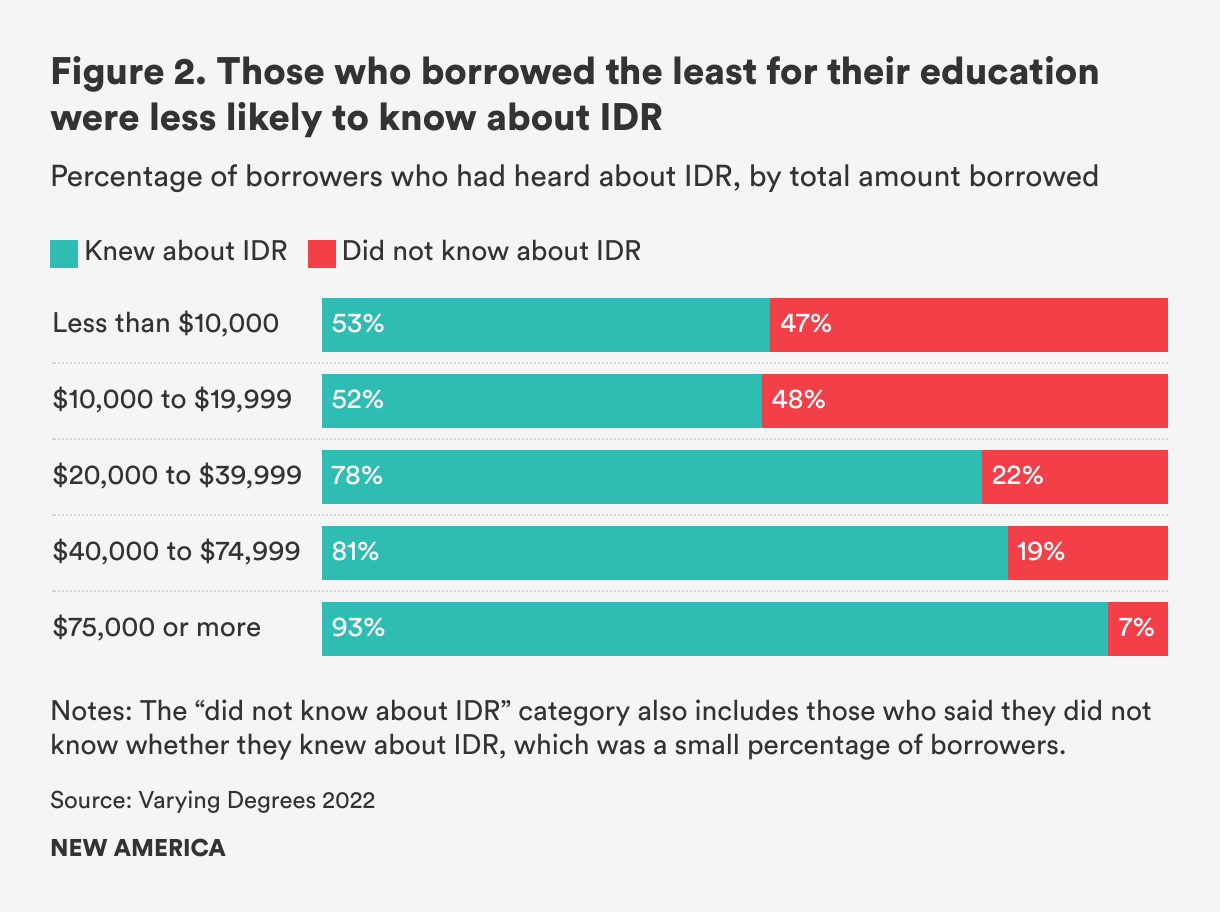

Those who borrowed less for their education were also less likely to know about IDR—only about half of low balance borrowers did (see Figure 2). These borrowers were less likely to have completed a degree or credential than those who borrowed more. Among those who borrowed $10,000 or less in the Varying Degrees sample, 54 percent did not complete the degree or credential for which they took out their loans, compared to just 10 percent of borrowers who took out more than $75,000.[12] Forty-two percent of borrowers who took out $10,000 or less in student loans earned less than $30,000 per year.

Having debt without the financial return on their higher education investment, and especially without knowledge of IDR, made these borrowers more likely to default on their loans. In addition to lowering payments for many borrowers, the Biden administration’s IDR proposal includes a new benefit for low-balance borrowers. Those borrowing $12,000 or less could reach forgiveness after making 10 years’ worth of qualifying payments.[13] The administration’s plan to cancel up to $10,000 for most borrowers, and up to $20,000 for eligible borrowers who received Pell Grants, would wipe out the entire loan balances of most low-balance borrowers. But borrowers must know about both of these initiatives in order to access them.

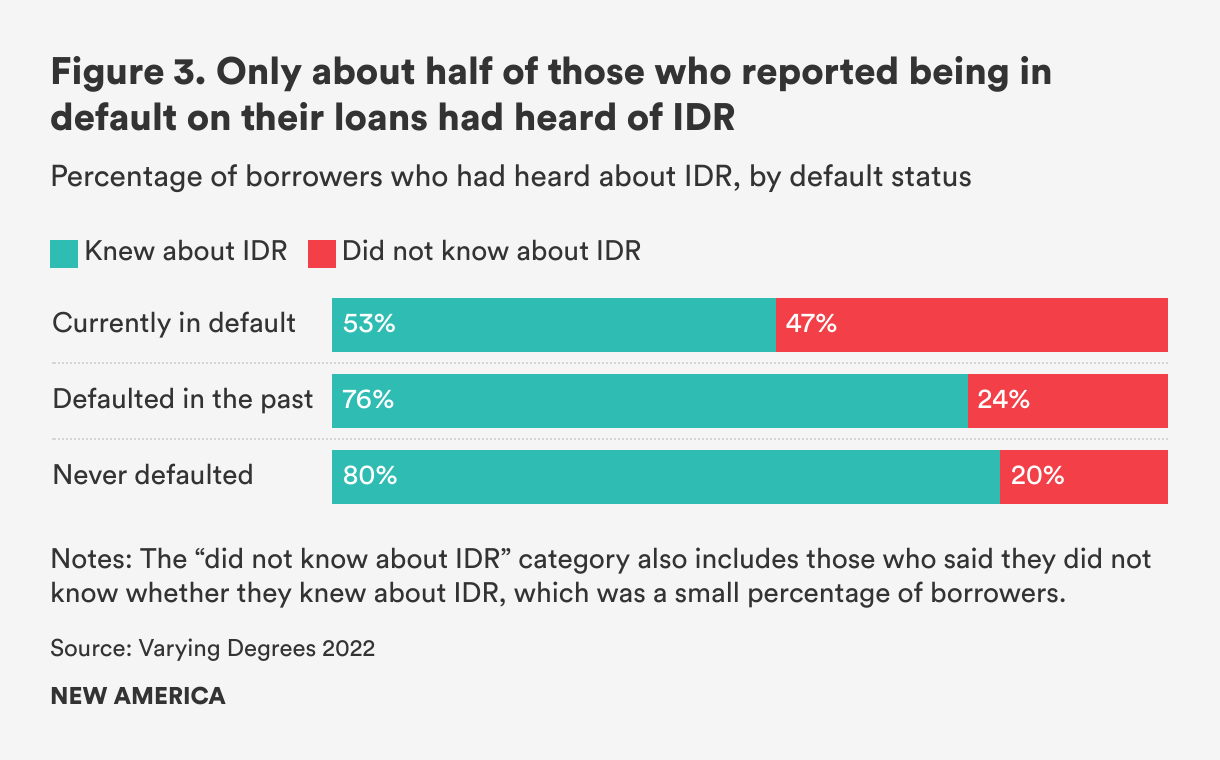

Around half of those in default on their loans had heard of IDR compared to more than three-quarters of other borrowers, including those who had defaulted in the past or never defaulted at all (see Figure 3). Many of these borrowers would have likely had incomes low enough to qualify for a $0 IDR plan.[14]

Those who had previously defaulted on their student loans but since returned them to good standing likely heard about IDR, and many likely used it, as part of the process to exit default.[15] According to Varying Degrees data, while only one-third of borrowers who were currently in default had ever been in IDR at some point, almost two-thirds of those who had previously defaulted had experience in an IDR plan. But in New America’s focus groups with defaulted borrowers, participants reported not being informed about IDR at all or when it would have been most beneficial to them; many languished in default for years before learning about this option.[16]

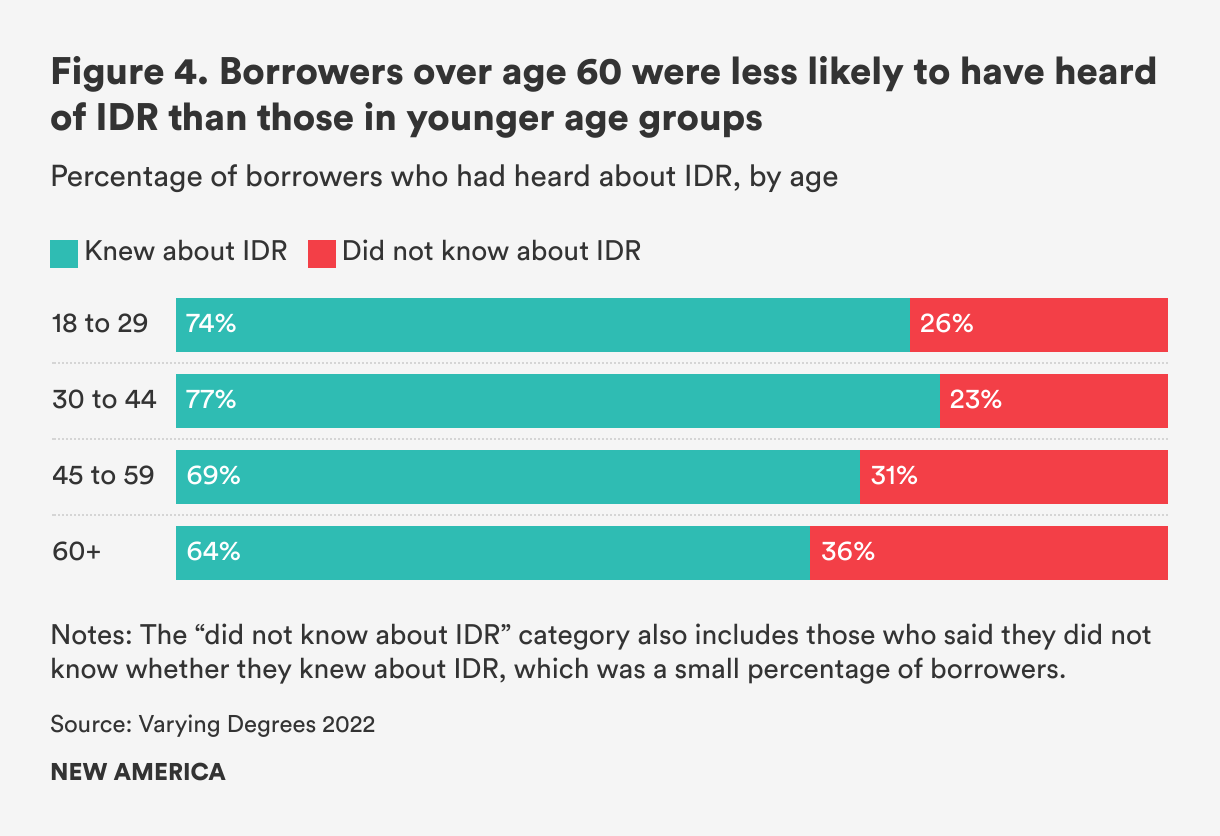

Varying Degrees data also indicate that borrowers over age 60 were less likely to have heard of IDR than younger borrowers: 64 percent of them knew about it, compared to 74 percent of those under 30 and 77 percent of those ages 30–44. This difference is not a product of time in repayment. Those who had entered repayment more recently were just as likely to know about IDR as borrowers who entered repayment 10 or more years ago, when fewer IDR options were available (see Figure 4).

Borrowers nearing retirement age who still owe on loans they took out for their education are particularly likely to need repayment relief. Government survey data show that one in four of these borrowers makes less than $25,000 and the same portion struggle to pay their monthly bills.[17] According to researchers at the Federal Reserve, borrowers with outstanding student loan debt when they hit retirement age “are no better off than their peers who did not go to college.”[18]

These borrowers may need different types of assistance than younger borrowers. Much of the outreach from the Department and its contractors relies on borrowers having access to the internet and smartphones. While engagement with technology among older Americans has increased in recent years, large connectivity gaps remain.[19]

Varying Degrees data show that similar percentages of borrowers by race—74 percent of white, 73 percent of Black, and 71 percent of Latina/o borrowers—reported knowing about IDR. This may seem surprising, given the well-documented disparities within the student loan system and the fact that people of color are overrepresented among low-income borrowers and those currently in default, both groups less likely to know about IDR.[20]

However, high IDR awareness across groups may be explained by non-white borrowers’ higher probability of having ever defaulted. According to Varying Degrees data, 71 percent of white borrowers reported never defaulting, compared to 44 percent of Black borrowers and 52 percent of Latina/o borrowers. (The survey does not have a large enough sample size to report IDR knowledge by race and default status.)

In addition, Black borrowers are more likely to borrow more than their white peers, meaning they are overrepresented among higher-balance borrowers, a group with greater knowledge of IDR.[21] If differences in default rates and balance sizes contribute to similar rates of IDR awareness, this means that white borrowers are not only learning about IDR in time to prevent a potential default (while many Black and Latina/o borrowers are not) but also facing less interest accrual throughout the repayment process.

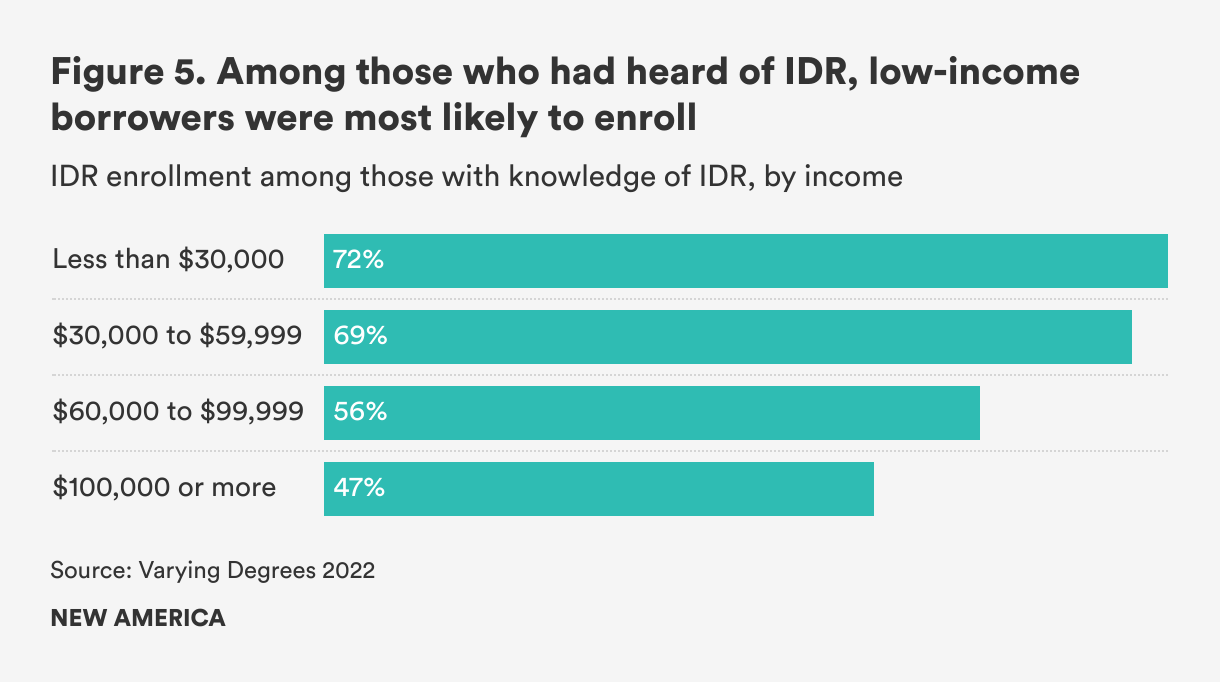

Varying Degrees data indicate that, among those who are aware of IDR, vulnerable borrowers are often more likely than their more privileged peers to enroll. Among only the borrowers who had heard of IDR, 72 percent with incomes under $30,000 had enrolled, compared to only 47 percent of borrowers with incomes over $100,000 (see Figure 5).

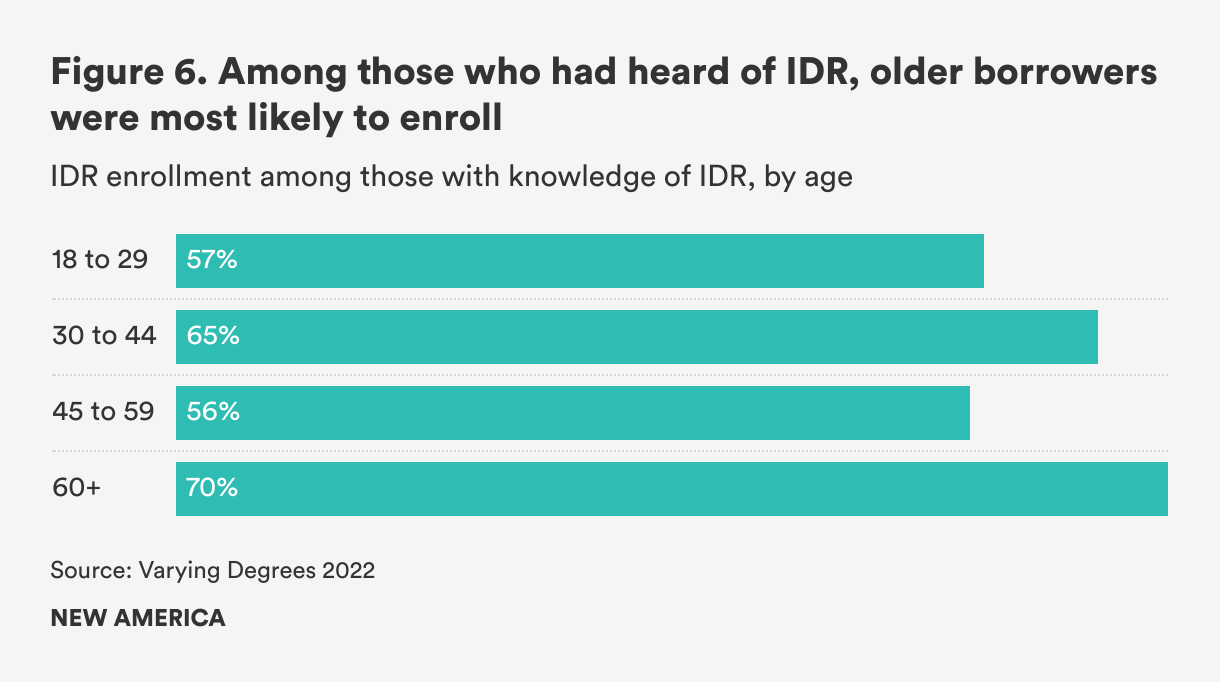

Other groups of vulnerable borrowers were also likely to choose IDR once they knew about it. Borrowers 60 and over in this group were 13 percentage points more likely to enroll than those under 30 (see Figure 6). In addition, financially insecure borrowers (at any income level) and borrowers who had previously defaulted enrolled in IDR at higher rates than their more financially secure peers and those who had never defaulted. And those who borrowed less than $10,000 enrolled in IDR plans at rates approaching those who borrowed much more.

This pattern suggests not only that those most likely to struggle to repay their loans see value in enrolling in IDR plans but also that at least some of these borrowers are able to overcome the administrative barriers to use IDR (as described in the next section) at least once. Counter to the narrative that vulnerable borrowers are sitting on the sidelines, Varying Degrees data also show other evidence that many are engaging to access benefits and proactively managing their accounts. For example, during the pandemic—a period in which payments, interest, and collections have been paused for most borrowers—older borrowers, lower-income borrowers, and Black and Latina/o borrowers were more likely than younger, higher-income, and white borrowers to report having updated their repayment plans and consolidated their loans, perhaps to access more generous IDR plans or temporary expansions to the PSLF program. Given this engagement, the question becomes: Why do so few vulnerable borrowers know about these plans? And among those who do have knowledge, why are more not able to access IDR and maintain their enrollment over time?

For borrowers, knowledge of IDR is critical. But knowledge alone does not ensure that they are able to benefit from the program. Long-term success for borrowers means being able to easily enroll in IDR the first time, recertify year after year, and leave the plan if they feel like another plan or option would better meet their needs. Borrowers surveyed in Varying Degrees who exited an IDR plan reported multiple reasons for doing so, but many who left still needed repayment relief.

More than half reported that they left a plan at least in part because they were worried about interest accrual and balance growth. In existing IDR plans, balances can grow even when borrowers make their required payments if those payments are too small to cover the interest that accrues on their loans, an issue that would be eliminated for many borrowers in the administration’s proposed new IDR plan.

To enroll and stay enrolled in IDR, borrowers are required to certify their incomes and family sizes annually.[22] Close to half reported leaving because they struggled with the annual recertification process, and a similar number indicated that their IDR payment was still not affordable. These respondents may have left IDR even when they still wanted to be enrolled or needed repayment relief.

Even though some vulnerable borrowers are able to access IDR at least once, many who would benefit most from IDR fail to stay enrolled. Among those in the Varying Degrees sample who had been enrolled but subsequently left an IDR plan, only one-third reported doing so because they could afford their payments. Over 60 percent of borrowers who left IDR were now in default or had previously defaulted, compared to only a quarter of other borrowers.

Borrowers’ concerns with the growth of their balances, frustrations with paperwork requirements, and inability to afford payments on existing IDR plans are well documented and were a driving force behind the Department’s recent effort to reform the IDR program.[23] But surprisingly, approximately half of those who left IDR said that they exited because they no longer qualified. And almost half of borrowers who had never enrolled in IDR, and said they did not plan to, reported making this choice because they did not think they qualified for IDR.

This could reflect the fact that, to qualify for some IDR plans, borrowers must have incomes low enough that they pay less on the IDR plan than they would otherwise.[24] Borrowers who miss payments while enrolled in an IDR plan and eventually default on their loans also (currently) lose eligibility for IDR while in default. However, because most non-defaulted borrowers can access (or take steps to access) an IDR plan, this response could also reflect the complex nature of the student loan repayment system. Borrowers may be confused when confronted with the many different options they have for managing payments, which vary based on the type of loans they hold, and they may hear from a variety of entities charged with explaining a complicated system.[25]

But much of this was likely also caused by inadequate assistance. The Department and its contractors have a history of providing insufficient and incorrect repayment information to borrowers and mishandling the implementation of existing IDR programs.[26] Reports from a government watchdog and others have identified ongoing shortcomings in how the program is administered.[27]

For the Department, providing access to IDR plans is necessary but not sufficient. Availability of these programs neither ensures that borrowers are aware of them and can enroll nor means that its contractors are providing adequate information and service. Disparities in knowledge and usage rates of IDR found in Varying Degrees data are concerning in and of themselves, and they likely extend beyond IDR to other programs. Vulnerable borrowers may also be disproportionately likely to miss out on student loan discharges, PSLF, debt cancellation, a Fresh Start for defaulted borrowers, and information that is distributed about the eventual restart of repayment. Without effective implementation of these initiatives, the borrowers most in need of repayment relief will continue to be left behind.

In order to boost enrollment among the most vulnerable borrowers, the Department must make it easier for borrowers to access IDR and other relief programs. It must quickly finish implementing the FUTURE Act, a 2019 law that allows the IRS to share certain tax information with the Department, streamlining the process for enrolling in IDR plans and making recertification automatic for borrowers who agree to having their data shared.[28] This means that, for many borrowers, being able to enroll in IDR once would turn into years of access. And the Biden administration’s new IDR proposal (using systems set up via the FUTURE Act) would automatically enroll borrowers who miss payments into an IDR plan.[29] This will ensure that many more vulnerable borrowers enter and remain in IDR.

Research in other fields finds that automatic enrollment increases program participation by simplifying the application process and reducing the number of decision points for consumers.[30] The administration’s proposal to automatically enroll delinquent borrowers into IDR is a great step towards more automation, and it should automate other programs and services whenever possible. In the near-term, the Department can automatically enroll eligible borrowers into IDR at other transition points, such as when they enter and exit default.

Communication about IDR needs to emphasize the program features that resonate most with those who struggle with repayment. Varying Degrees data suggest that borrowers value lower payments, access to early forgiveness, and a limit on balance growth. Randomized control trials have also found that messages emphasizing the insurance benefits of IDR and the downsides of inaction are effective in encouraging enrollment.[31] The Department should also create messaging that emphasizes that borrowers qualify for programs like IDR, PSLF, Fresh Start, and loan cancellation and that the processes to apply are easy.

Including checklists of all required information, waiving or simplifying enrollment requirements, and providing more personalized and just-in-time information may also help borrowers avoid confusion and save time and effort.[32] In addition, vulnerable borrowers are likely to benefit from multiple Department relief programs, making cross-messaging critical. Every engagement with a borrower provides an opportunity to screen for and provide information about enrollment in IDR, access to Fresh Start, and discharge and cancellation programs.

In addition to using promising practices identified through student loan-related data and research, the administration can look across government and to other fields—including health care and human services—for outreach and engagement models. For example, research on vulnerable populations emphasizes the importance of engaging members of the affected communities in designing messaging campaigns.[33] Incorporating stakeholder feedback can be time-intensive and costly, but this engagement is necessary to build trust.[34] And work that looks into boosting vaccination rates also emphasizes the importance of transparent and consistent information to address misinformation and concerns.[35] This communication, and communication about student loans, should happen on multiple platforms and platforms that are easily accessible by those—like older Americans—who may not use technology as their main method of communication.

Interagency data matches to identify those eligible for low or $0 IDR payments or various discharge and forgiveness programs should remain a goal for the Department. Strategies to boost health insurance enrollment include engaging with consumers when they interact with different parts of the government and data-sharing across agencies.[36] But in the shorter term, trusted partners at community centers, faith-based organizations, educational institutions, benefits providers, and others are important partners for informing borrowers about the student loan-related benefits available to them and ensuring they have the resources to apply. Community and consumer group engagement contributed to the successes of the recent PSLF waiver.[37]

Research that examines communication about Medicaid enrollment suggests that using mass marketing campaigns, through print and broadcast media, which include state and community leaders and celebrities delivering the message are effective in delivering information to large groups.[38] Venues such as churches, college campuses, and grocery stores are also important for getting out the message.

In the existing student loan servicing contracts, contractor performance metrics and incentives are not always aligned with borrower success and can contribute to inconsistent and often inadequate service. The Department has also faced challenges holding contractors accountable for poor borrower outcomes and errors. In late April, FSA announced that it had awarded new servicing contracts, which include more coordinated websites and account access, provide additional cybersecurity, increase borrowers’ ability to manage their accounts online, strengthen accountability and penalties for poor service, and provide resources for supporting the most vulnerable borrowers.[39]

While a step in the right direction, even with these new contracts, the Department must provide strong oversight and continue to partner with other government entities to ensure that its contractors give consistent and accurate information and assistance—and engage in effective outreach—to borrowers. It is also important that the Department provide consistent and adequate communication to contractors and ensure this new system is phased in with the least disruption to borrowers, especially as new regulations, programs, and reforms come online.

The Department needs resources to smoothly implement the new IDR plan and the other relief programs; to communicate with borrowers about their options and the resources available to access them; to build out systems to facilitate automation; to stand up a new servicing system with strong accountability, sufficient oversight, and support for vulnerable borrowers; and to fix other systemic issues in the student loan system that have been accumulating for decades. If the system does not have adequate funding from Congress, even when relief programs are available, those who most need the support are likely to be left behind.

The sixth annual Varying Degrees survey was administered by NORC at the University of Chicago using NORC’s AmeriSpeak Panel. The nationally representative survey was fielded between April 19, 2022 and May 19, 2022. The 2022 survey placed an additional emphasis on collecting detailed information about individuals with student loans and how they were managing repayment during the COVID-19 pandemic. There were 1,156 respondents in the student loan borrower sample. The margin of error was ±4.04 percentage points.

In this analysis, “borrowers” are those who took out loans for their own educations and were not currently in school. Statistics reported here may not match statistics available in the Varying Degrees Explore the Data tool.[40]

The authors would like to thank Rachel Fishman for editing this brief, Sabrina Detlef for her copyediting support, and Fabio Murgia and Mandy Dean for their communication and data visualization support.

This analysis was supported by the Bill & Melinda Gates Foundation and Arnold Ventures. New America thanks the foundations for their support. The findings and conclusions contained within are those of the authors and do not reflect positions or policies of the funders.

Project Director, Education, Opportunity, and Mobility

Senior Policy Analyst, Higher Education

Senior Policy Manager, Higher Education