Consolidation Loan Irony

Blog Post

June 11, 2008

When interest rates on variable rate Stafford loans reset this July to a low 3.61 percent (4.25 percent after the six-month grace period for recent graduates) the consolidation loan market, once robust and competitive, will be a shadow if its former self. There are policy explanations, economic explanations, and of course, political explanations for the change in the consolidation market. And like many things in student loan policy, the story is filled with irony.

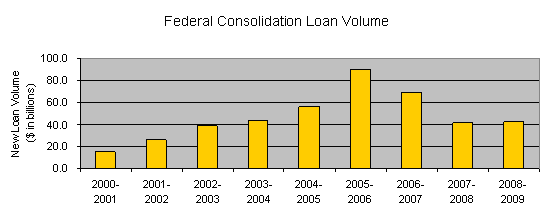

Not Many Loans Left to Consolidate

Not Many Loans Left to Consolidate

As we pointed out earlier this week, borrowers with variable rate Stafford loans (those originated before July 2006) will be able, as of July 1st, to lock in the new low rate for the lives of their loans by refinancing. However, demand for this option may be low, as few borrowers are likely to have any unconsolidated, variable rate Stafford loans left (consolidation is a one-time option). From 2002 to 2006, interest rates on these loans dropped so low that nearly all borrowers who were eligible at the time to consolidate their loans did so, locking in rates between 2.77 and 5.30 percent. For a brief time, even borrowers still enrolled in school could refinance their loans, though in-school consolidation was discontinued as part of the Higher Education Reconciliation Act of 2005. What’s more, new loans taken out since July 2006 all carry fixed interest rates, removing the main benefit of consolidation.

And Not Many Consolidators Left Either

But those few borrowers with eligible loans looking to refinance today aren’t likely to find their mail boxes stuffed with consolidation offers. Back in the go-go consolidation days, free market competition in the program was fierce and lenders offered all sorts of borrower benefits to win business, from reduced interest rates to reductions in the total loan balance. It was the kind of dynamic that one would expect the staunchest supporters of the Federal Family Education Loan (FFEL) program (many of whom are Republicans) to laud. After all, FFEL supporters' favorite buzzwords are “free-market,” “private-market,” “borrower benefits,” and “competition.”

Instead, many of the staunchest supporters of FFEL -- including the Republican leaders of the education committee in the House of Representatives and the Bush Administration (see the FY2008 budget) -- pursued policies to squash the consolidation market, by making the program less attractive for borrowers and loan consolidation companies alike. They argued that consolidators did not “invest in the FFEL program” since these companies didn’t originate loans when borrowers entered school, only afterward. Consolidation critics also argued that the program was too costly, and poorly targeted, by providing generous federal subsidies to borrowers who did not necessarily need the help. Indeed, that argument has merit, but one couldn’t help get a whiff of pretense.

In reality, those who fought to squash the consolidation market did so as a political favor to the big loan companies. To protect their loan portfolios, Sallie Mae, Citibank and others had to compete with consolidators and match the generous borrower benefits these companies were offering, which ate into their profits. The Sallie Maes of the world wanted the student loan consolidation market to go away. FFEL supporters in Congress wanted to help the big lenders stamp out the competition and eliminate the borrower benefits resulting from it.

Subsidy Cut for Consolidators

While the fixed interest rates on new Stafford loans removes much of the incentive for borrowers to refinance, and has largely aided consolidation opponents in curtailing competition for loans, recent subsidy cuts are a final blow.

The College Cost Reduction and Access Act reduced subsidies on consolidation loans and Stafford loans by the same amount. But an existing “rebate” on consolidation loan subsidies -- which Congress put in place in 1993 -- effectively reduces the consolidation subsidy by a further 1.05 percentage points compared to an unconsolidated loan. Lenders today complain that the credit crunch and subsidy cuts have made Stafford loans unprofitable. If so, then consolidation loans are an even bigger loss. [Information on how the loan subsidies work is available here.]

Irony for FFEL Supporters

Borrowers should expect to find few, if any, lenders willing to consolidate loans given the state of the market. As our earlier post pointed out, borrowers can always refinance their loans into the Direct Lending even if they have FFEL loans. That’s likely to lead to an uptick in volume of Direct Consolidation Loans.

Ah, the irony.

Supporters of FFEL who espouse the virtues of competition and borrower benefits have helped to squash both in the consolidation loan market. As a result, these same FFEL supporters, who loath the Direct Loan program, may have actually encouraged borrowers to refinance their FFEL loans into Direct Lending.

Maybe irony isn’t the word. Poetic justice, perhaps?