Vicki Shabo

Senior Fellow for Gender Equity, Paid Leave & Care Policy and Strategy, Better Life Lab

Wage Replacement, Duration, and Funding in U.S. State Paid Family and Medical Leave Programs

This document has been updated multiple times since its original June 2021 publication to reflect newly passed or modified state paid leave programs, new data on state programs, and benefit and contribution information. It will continue to be updated periodically as new information is available.

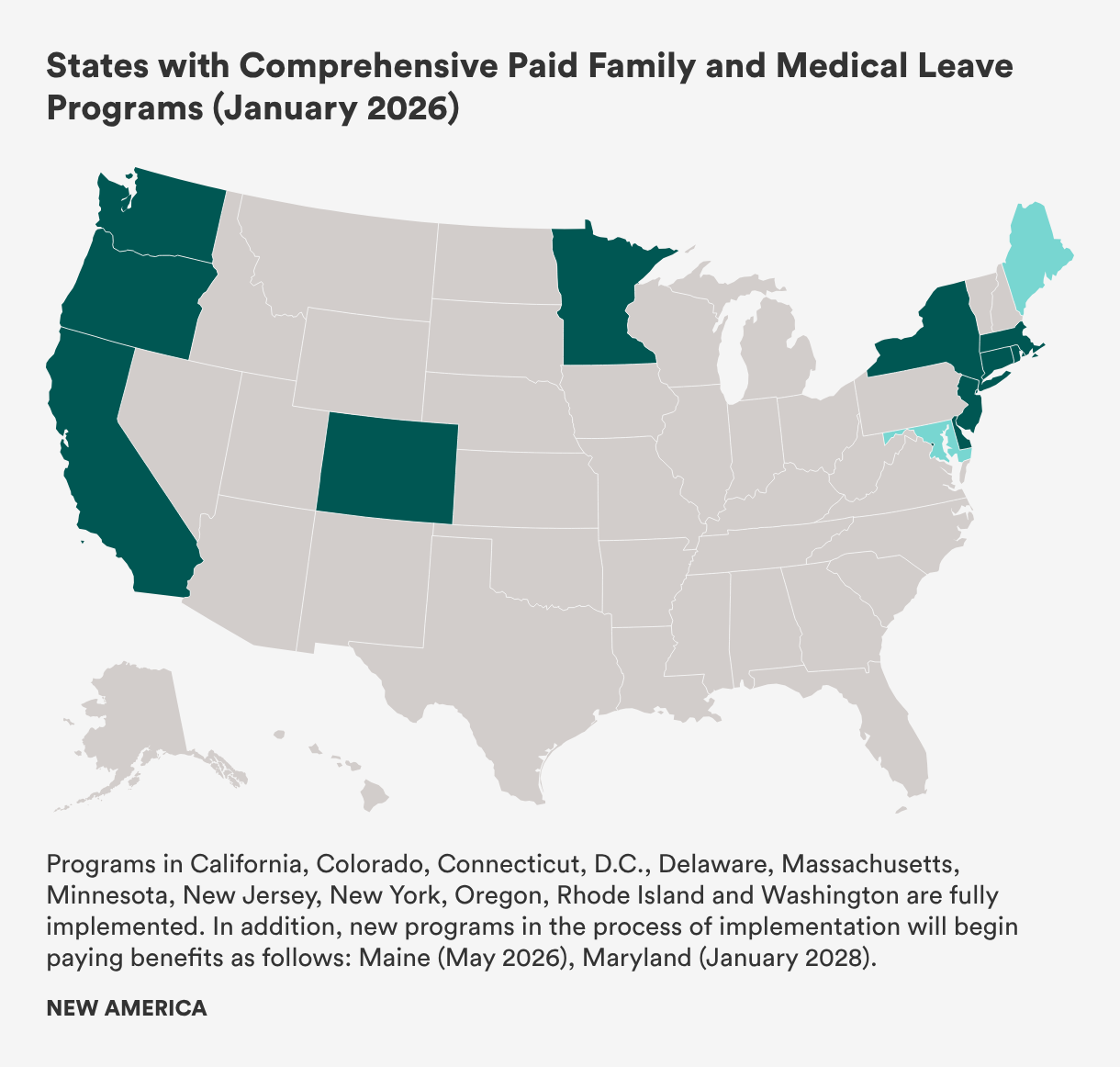

As of January 2026, 13 states plus the District of Columbia (DC) have or will soon have statewide paid family and medical leave programs in place.

California, Colorado, Connecticut, Delaware, DC, Massachusetts, Minnesota, New Jersey, New York, Oregon, Rhode Island, and Washington currently make paid leave benefits available to workers.

Maine’s program will begin making benefits available in May 2026, and Maryland will begin paying benefits in 2028, after several implementation delays.[1],[2]

Without a federal paid family and medical leave program—like the U.S. House of Representatives considered and passed in 2021 as part of the Build Back Better Act but the Senate failed to take up—states are laboratories for innovation.

This explainer is a companion to Paid and Unpaid Leave Programs in the United States. It addresses policymakers’ questions about paid family and medical leave program design, benefits, and funding methods. It shows that the value delivered by comprehensive paid leave programs comes at an affordable cost.

This explainer also touches on a voluntary paid leave program models, both those in New Hampshire and Vermont, and another alternative—the authorization of private paid leave insurance coverage for employers to purchase in Alabama, Arkansas, Florida, Kentucky, South Carolina, Tennessee, Texas, and Virginia. However, these are not comprehensive programs, do not guarantee access to private-sector workers, and neither the New Hampshire approach nor the authorization approach appear to have meaningfully expanded access to paid leave.

Paid leave prevents workers and their families from falling down a financial rabbit hole when breadwinners need time away from their jobs to care for a loved one or address their own serious health issue. This is a critically important matter of equity and security because just 27 percent of workers have paid family leave through their jobs absent a state policy, and low-wage workers are 10 times less likely to have access to paid family leave than the highest-paid workers.

In 2018, Brandeis University researchers estimated that a typical worker would forgo more than $9,500 in lost wages to take 12 weeks of family or medical leave without pay. While on leave, workers still need to afford basic expenses to keep their families afloat. Paid leave can provide the security to meet these basic financial obligations.

Urban Institute research released in 2024 estimates that a comprehensive paid family and medical leave program modeled on the proposed federal FAMILY Act would reduce poverty among leave-takers by 16 percent, especially for Black and Latine families. Access to FAMILY Act benefits would also increase net income for nearly 90 percent of families, with the largest increases benefiting families with low incomes.

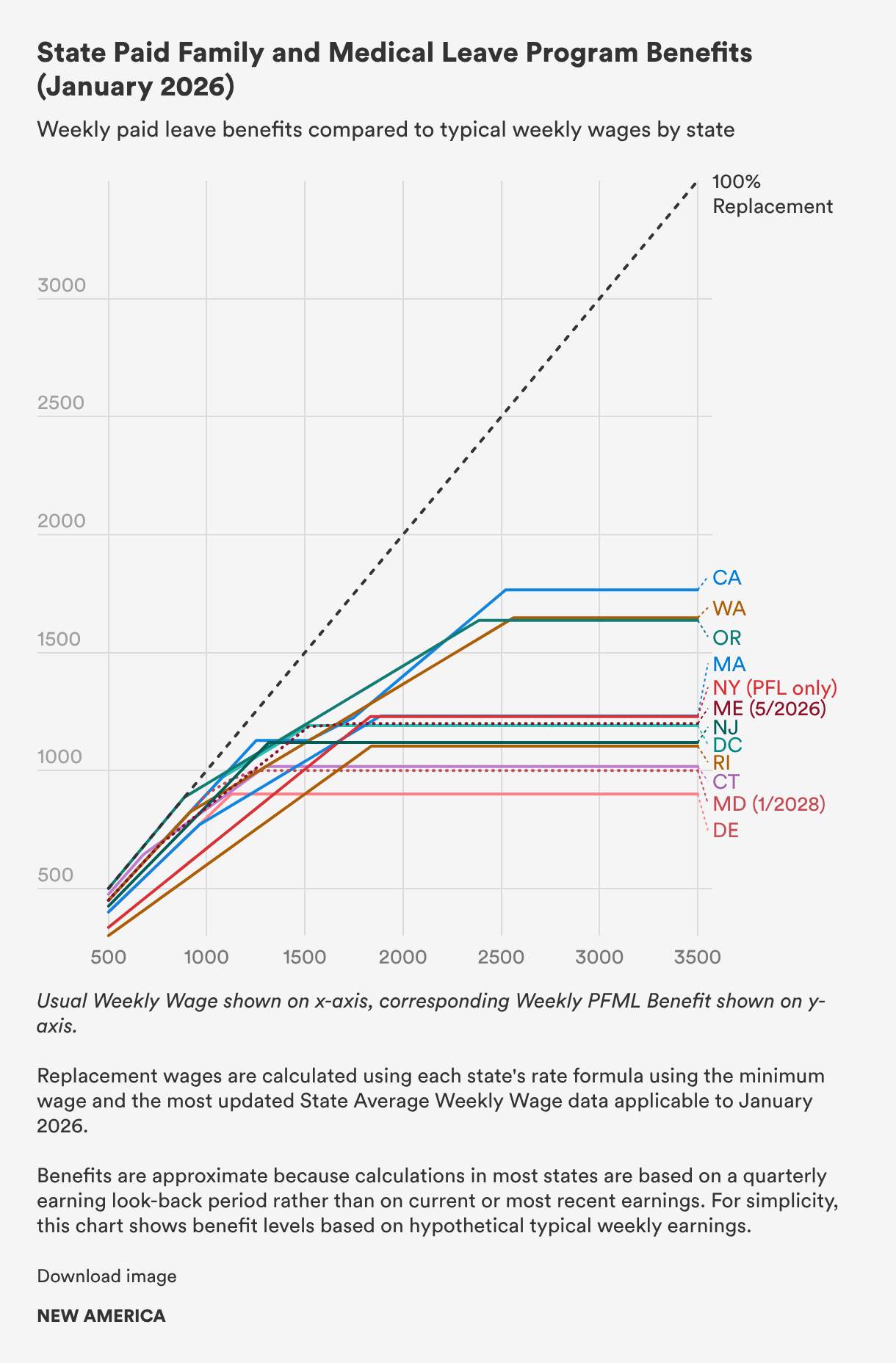

The country’s first two paid family leave programs, in California and New Jersey, began by replacing a fixed percentage of a worker’s typical wages when the worker needed to take paid family or medical leave (55 percent and 67 percent, respectively). These two states have subsequently raised their wage replacement rates and one—California—abandoned a fixed percentage of wages for a sliding-scale approach.

The next two programs to pass—Rhode Island and New York—also take a fixed percentage approach but have not updated their wage replacement rates of 60 percent and 67 percent, respectively, though Rhode Island is slated to increase wage replacement to 70 percent in 2027 and to 75 percent in 2028.

Delaware, which passed in 2022 and began paying benefits on January 1, 2026, follows this older model of applying a uniform wage replacement rate but follows best practices recommended by researchers to set wage replacement at 80 percent of a worker’s average weekly wage—allowing lower-wage workers to use needed paid leave without falling into poverty and enabling middle-wage workers to continue to meet their basic household expenses.

Most newer programs have adopted a sliding-scale approach to paid leave benefit payments and provide higher wage replacement to lower-wage workers. This helps to make leave more affordable and accessible to people often living paycheck to paycheck.

Maine and Maryland, when they begin to pay benefits in May 2026 and January 2028, respectively, will also provide up to 90 percent of low-wage workers’ typical wages.

The figure below shows the approximate benefit that workers at different wage levels can expect to receive in each state’s current or forthcoming program. A supplementary table shows approximate wage replacement for workers who are paid minimum wage, average weekly wages, or fractions or multiples of the state average weekly wage (SAWW) in each state. (Notes [3] to [16] provide more information about wage replacement rates.)

To compare apples to apples, we calculate benefits using the 2026 minimum wage and the SAWW that the state is using to calculate paid leave, workers’ compensation, or unemployment benefits in 2026. Benefit amounts are also not exact since most states use a look-back period on recent wages rather than the exact wage a worker typically receives when they take leave.

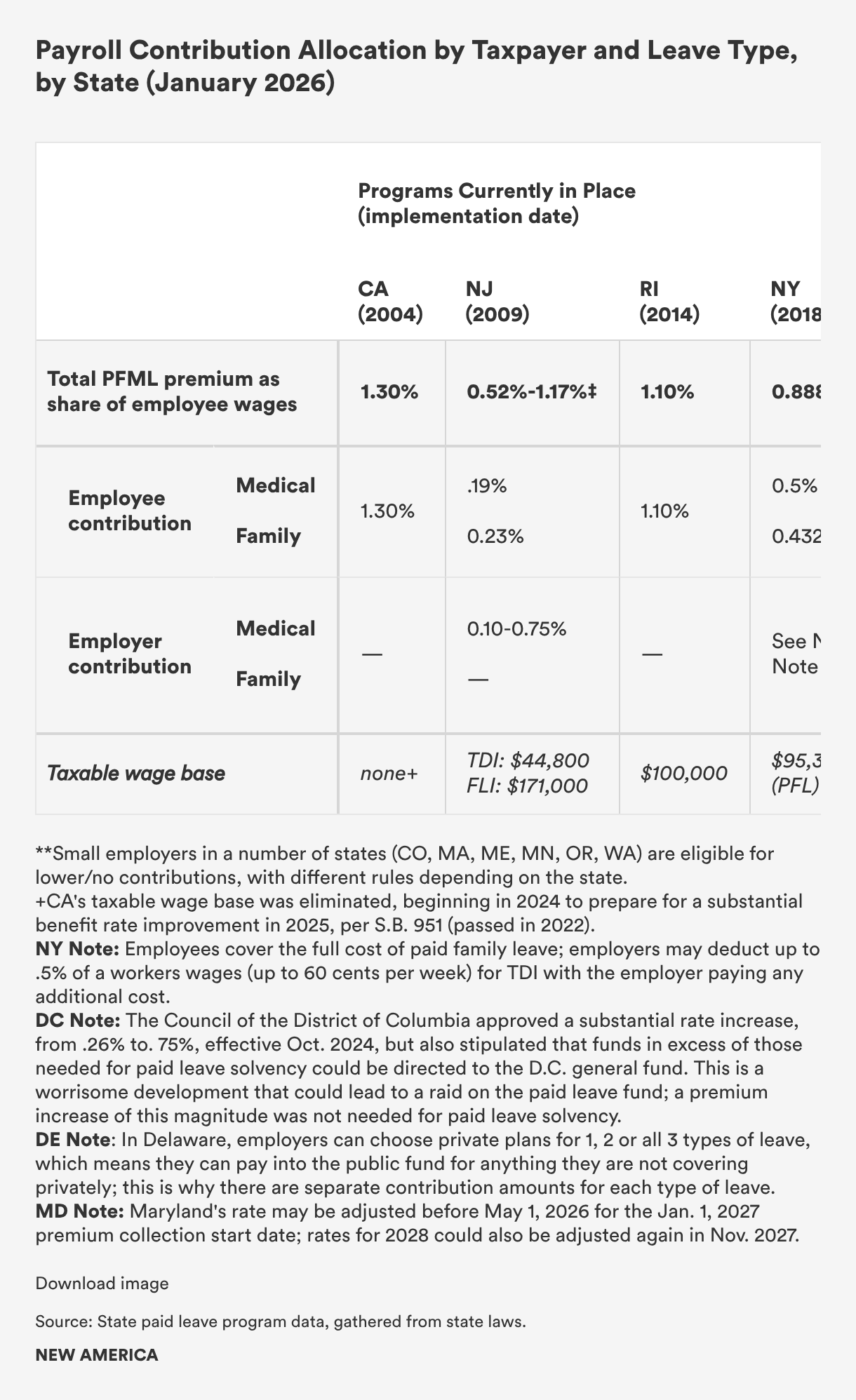

Comprehensive state programs are funded through small, mandatory payroll deductions from employers, employees, or both. Tax rates are no more than 1.3 percent in any state in 2026, and most are 1 percent or less. In each state other than New York, the money is pooled into a statewide social insurance fund from which benefits are paid; in New York, private insurers and a state insurance fund, similar to a public option, exist side by side.[17]

Each state’s program covers, at a minimum, core reasons for leave: care for a new child, care for a family member with a serious health issue, and care for one’s own serious health issue. Some also cover military families’ need for leave related to deployment and safe leave for people dealing with domestic violence, stalking, and sexual assault.

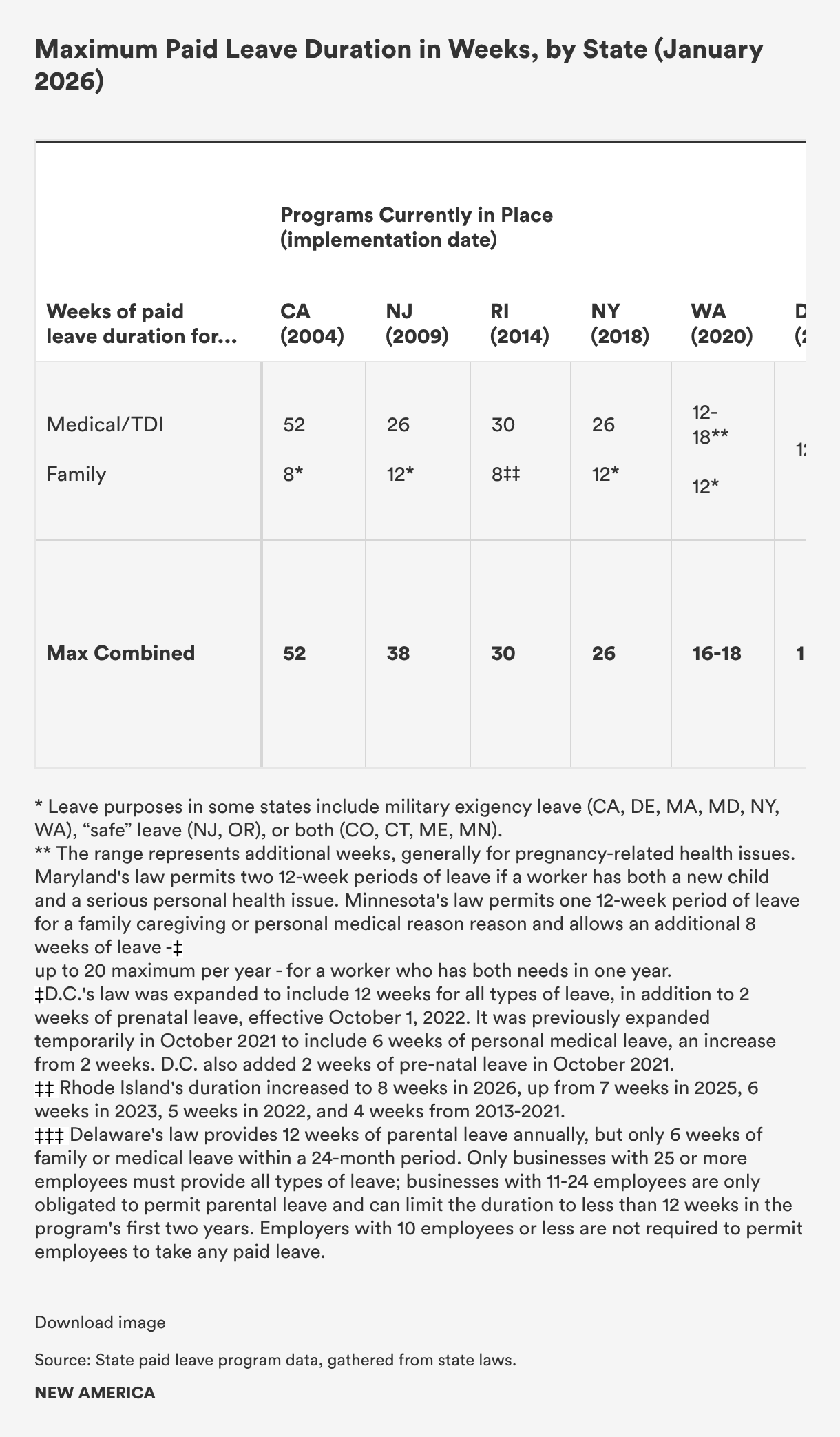

The two tables below show the contribution levels for employees and employers and the taxable wage base on which premiums are calculated and provide context for what these contributions “buy” in terms of the paid family and medical leave available to workers, including each state’s duration of paid leave. (Notes [18] to [31] provide more information about payroll tax rates, benefit caps, and duration.)

In brief, each state passed programs to provide paid leave and collect payroll contributions, and most administer benefits to eligible workers. States need to build up their funds before making wage replacement benefits available to workers, which means there is usually a lag between the passage of legislation, the collection of premiums, and the availability of benefits to workers.

The family caregiving portion of nearly all state paid leave programs allows workers to take paid leave to care for a range of family members—parents, spouses, children, and grandparents in all; and grandchildren, siblings, parents-in-law, and domestic partners in most—and seven newer or newly expanded laws also include “chosen” family members.

The funding for the programs is sufficient to cover all the caregiving purposes and relationships that the laws include. The inclusion of extended family members does not add appreciably to program costs, and broad family coverage is particularly important to ensure that people of color (who disproportionately have extended family care responsibilities), LGBTQ+ people, and people with disabilities and their caregivers can realize the promise of paid leave programs.

Comprehensive, universal state paid leave models provide substantial financial security to working people at minimal individual cost, usually for an adequate number of weeks. Federal lawmakers can use these parameters in assessing paid leave policy options and designing a national program.

Two new approaches to paid family and medical leave policy were implemented in 2023 but have yet to show real impact.

In New Hampshire, the Governor created a program that covers public sector workers with six weeks of paid family leave at 60 percent of their typical wages—this is substantially less time and lower rate replacement than most programs in states with comprehensive, universal policies. Private employers can purchase paid family and medical leave insurance through this plan if they choose to do so, and workers whose employers do not offer paid family leave insurance can purchase insurance privately and have premium contributions deducted from their paychecks.

Only one insurer (MetLife) bid for a contract with New Hampshire to provide this insurance product, and the rates they estimate charging employers are higher in most cases than payroll contributions in states with paid family and medical leave programs. In 2025, just under 18,000 workers, or 2.5 percent of the New Hampshire workforce, were covered through this program. Of these, just over 9,361 were state employees who were automatically covered, while 7,633 were covered through an employer’s voluntary plan, and 919 opted into individual coverage.

Vermont has adopted a system like New Hampshire’s, but administered by the Hartford insurance company. State workers were covered as of mid-2023, while private employers’ participation opened in July 2024 and individuals could begin buying coverage in July 2025. As of August 2025, just under 10,000 workers—a tiny fraction of the workforce—were covered.

In Virginia in 2022, the state legislature granted the state insurance commission the authority to approve the sale of family leave insurance products in the state. There are no specific parameters that insurance products must offer in terms of duration, wage replacement, family members covered, or any other specific details. As of December 2025, just two insurers are approved to offer a family leave insurance product, and there is no public information on whether employers have purchased it.

In 2023, five additional states (Alabama, Arkansas, Florida, Tennessee, and Texas) enacted similar laws based on an insurance industry model bill. In 2024, Kentucky and South Carolina did the same.

A recent report by New America and the National Partnership for Women & Families found that few insurers are selling products in these states, and there is no public information on whether employers are purchasing these products. There are also concerns about policy parameters, pricing, and access to information about the availability of products, as well as concerns about insurance regulators’ understanding of these products and oversight.

[1]Maryland’s program was initially set to begin collecting contributions in October 2023 and begin paying benefits in January 2025; the bill had passed in a veto override vote in 2022, and the outgoing administration did not make as much progress as was needed to meet this timeline. In 2023 and 2024, Governor Wes Moore signed legislation making some adjustments to the program and providing for a longer implementation timeline. The timeline was delayed again in the 2024 and 2025 legislative sessions. Contributions will now begin on January 1, 2027, and benefits will begin in January 2028.

[2]Minnesota simultaneously began paying benefits and taking in payroll contribution premiums in January 2026. The state bill appropriated general revenue to enable benefits and contributions to begin simultaneously, rather than contributions beginning a year or more in advance of benefit payment availability; see Article 3. The Maine law passed as part of a budget agreement in 2023; the program began collecting premiums in January 2025 and will start paying benefits in May 2026. Delaware passed as stand-alone legislation in 2022; payroll contributions began in January 2025, and benefits began in January 2026.

[3]In California, the benefit amount depends on the highest quarter of earnings during a base period (first four of last completed calendar quarters before starting date of claim). Beginning in 2025, workers with quarterly wages of at least $722.50 up to 70 percent of the average quarterly wage will receive 90 percent of their wages, and workers with higher wages will receive 70 percent of their usual wages, up to a cap of $1,765/week in 2026 (which is 63 percent of the SAWW). See this 2026 benefit FAQ from the California Employment Development Department and a benefits calculator.

[4]In New Jersey, as of July 1, 2020, claimants are paid 85 percent of their average weekly wage. In 2026, the maximum weekly benefit is $1,119 per week. See New Jersey Department of Labor. Prior to July 2020, claimants were paid two-thirds of their average weekly wage, up to a maximum of $667 per week.

[5]In Rhode Island, wage replacement is equal to 4.62 percent of the wages paid to employees in the highest quarter of the base period. In 2026, the maximum benefit is $1,103. See Rhode Island Department of Labor.

[6]In New York, as of 2021 after four years of scaling up, the wage replacement rate reached its full amount of 67 percent of employee’s weekly wage up to 67 percent of SAWW. The maximum benefit in 2026 is $1,228.53. See New York Paid Family Wage Benefit Calculator. Temporary disability insurance has different wage replacement in New York, and the maximum benefit is just $170 a week; this is the only state in which TDI and PFL programs have different payment rates. Advocates are working to update TDI in New York.

[7]In Washington state, the wage replacement rate is 90 percent of the employee’s wage up to 50 percent of SAWW plus 50 percent of employee’s wage over 50 percent of SAWW. Maximum benefit in 2026 is $1,647 (90 percent of SAWW). See Washington Paid and Medical Leave calculator.

[8]In DC, the wage replacement calculation is based on the minimum wage. The replacement rate is 90 percent of the employee’s wage up to 150 percent of DC’s minimum wage x 40 plus 50 percent of the employee’s wage over 150 percent of DC’s minimum wage x 40. Maximum benefit is $1,190 a week for 2026. See DC Benefits Calculator.

[9]In Massachusetts, wage replacement rate is 80 percent of the employee’s wage up to 50 percent of SAWW plus 50 percent of the employee’s wage over 50 percent of SAWW. Maximum benefit for 2026 is $1,230.39, which is 64 percent of SAWW. See Massachusetts Benefit Calculations.

[10]In Connecticut, the wage replacement calculation is based on minimum wage. Replacement rate is 90 percent of employee’s wage up to minimum wage x 40 plus 60 percent of employee’s wage over minimum wage x 40. Maximum benefit is minimum wage x 60, $1,016.40 in 2026. See Connecticut Paid Leave.

[11]In Oregon, the wage replacement rate is 100 percent of the employee’s wage up to 65 percent of SAWW plus 50 percent of the employee’s wage over 65 percent of SAWW. Maximum benefit is 120 percent of SAWW and minimum benefit is 5 percent of SAWW. The maximum benefit for 2026 is $1,636.56. See Paid Leave Oregon Benefits Calculator.

[12]Colorado’s wage replacement formula follows Washington state’s: 90 percent of the employee’s wage up to 50 percent of SAWW plus 50 percent of the employee’s wage over 50 percent of SAWW, and the maximum benefit is 90 percent of SAWW. For 2026, the maximum benefit is $1,381.45. See Colorado Benefits Calculator.

[13]Maryland’s wage replacement rate is 90 percent for workers with an individual average weekly wage that is 65 percent or less of SAWW plus 50 percent of wages that are above 65 percent of SAWW. The maximum benefit will be $1,000 a week beginning in January 2028 annually thereafter; the minimum benefit is $50 a week. See Maryland FAMLI program information.

[14]Delaware’s wage replacement rate is 80 percent of the individual’s average weekly wage, up to a cap of $900 per week in the program’s first two years (2026 and 2027), with annual adjustments thereafter. The minimum benefit is $100 a week (including full wage replacement for workers who make less than $100 per week but are otherwise eligible for the program). See Delaware Benefits Calculator.

[15]Minnesota’s wage replacement is in three tiers: 90 percent up to half of SAWW; 66 percent of workers’ wages that fall between over half and the full SAWW; and 55 percent for wages that exceed the SAWW. The maximum benefit is the same as the SAWW, which is calculated annually and is $1,423 in 2026. See Minnesota Benefits Calculator.

[16]Maine’s wage replacement rate is 90 percent for workers with an individual average weekly wage that is 50 percent or less of SAWW plus 66 percent of wages that are above 50 percent of SAWW. The maximum benefit is the SAWW, which is $1,198.84 in 2026. See Maine Benefits Estimator Tool.

[17]Some states permit employers to self-insure or purchase third-party insurance; the state regulates and enforces this process but, with the exception of New York, very few employers participate in these voluntary plans and participate in the state fund.

[18]California’s law was passed in 2002, implemented in 2004, and has been amended multiple times, including in 2022 to greatly increase wage replacement beginning in 2025. The maximum length of family leave increased from six to eight weeks on July 1, 2020. See SB 83 and tax rates and wage bases. On January 1, 2021, individuals became eligible to receive up to six weeks of military exigency leave; see California Employment Development Department. In 2026, payroll tax contributions are 1.3 percent, a slight increase from the 1.2 percent rate charged in 2025.

[19]In New Jersey, 2019 legislation made changes to the state paid family leave program. Some changes took effect in January 2020, and others took effect on July 1, 2020. See tax rates and wage bases, and see TDI for workers and employers. Note that TDI contributions for employers vary based on how often their workforce uses TDI (“experience rating”); this is the only state to experience-rate its TDI contributions. In 2026, workers will pay .19 percent in TDI premiums, down from .23 percent in 2025 after a two-year holiday in 2023 and 2024. Rates for FLI decreased to .23 percent in 2026, from .33 percent in 2025.

[20]See Rhode Island tax rates and wage bases. Rates for 2026 are 1.1 percent, returning to 2024 levels, but—beginning in 2026—premiums are assessed on more of workers’ earnings in order to pay for higher wage replacement rates. Rhode Island allows for a maximum of 30 weeks of combined annual disability and family leave. Beginning in 2026, one week of leave is available for bone marrow donation, and 30 days is available for organ donation. See Rhode Island TCI claimant pamphlet for 2026.

[21]See New York tax rates and wage bases. The taxable wage base cap is equal to the SAWW. Employers are required to provide TDI and may take up to a 0.50 percent payroll tax from employees to cover benefits (but only up to $0.60 per week). New York’s paid family leave can be used for military exigency leave. Workers’ family leave contribution rate in 2026 is .432, a slight increase from 2025’s .373 percent, but less than rates in 2023 and 2024.

[22]See Washington state tax rates and wage bases. The taxable wage base cap is the Social Security cap. Small businesses with fewer than 50 employees are not required to contribute to premiums but are incentivized to do so. Some individuals can qualify for up to 16 to 18 weeks combined leave (e.g., individuals who experience complications in pregnancy may be eligible for 18 weeks of leave). Washington’s law includes military exigency leave; see Washington Paid Leave. In 2023, Washington began to allow seven days for a pregnancy loss or loss of a child. Washington’s contribution rate in 2026 is 1.12 percent.

[23]See DC tax rates. DC extended the duration of paid family and medical leave to a total of 12 weeks beginning in October 2022, up from an interim increase in 2021 and the program’s initial offering of just two weeks of paid medical leave, six weeks of paid caregiving leave, and eight weeks of paid parental leave. DC also offers two weeks of prenatal leave, as of October 2021; see DC Paid Family Leave. DC reduced employer payroll contributions from .62 percent to .26 percent in 2022 and kept premiums there for 2023 and 2024. In 2025, the Council approved a premium increase to .75 percent, and that is the same rate applied in 2026. The DC paid leave fund is available for other purposes due to a 2025 statutory change allowing excess funds to be transferred to DC’s general fund. See more here (section 12a, page 18).

[24]See Massachusetts tax rates and wage bases. Small businesses with fewer than 25 employees are not required to contribute to premiums. The taxable wage base cap is the Social Security cap. Note that the maximum length of leave is capped at 26 weeks per year (12 weeks of family leave, 20 weeks of medical leave, and 26 weeks to care for a wounded service member). See Massachusetts Family and Medical Leave. Massachusetts’ contribution rate dropped from .68 percent in 2022 to .63 percent in 2023, but jumped to .88 percent in 2024 and has remained there in 2025 and 2026.

[25]See Connecticut tax rates and wage bases. Workers pay the .5 percent payroll tax rate, which has been stable for all program years from 2022 through 2026. The taxable wage base cap is the Social Security cap. Note that the maximum annual length of leave is 12 weeks plus an additional two weeks for a health condition resulting from pregnancy. Connecticut’s law includes both military exigency leave and “safe” leave for survivors of family violence. Connecticut caps military exigency leave at 26 weeks per two-year period.

[26]In Oregon in 2026, workers and businesses will continue to contribute a combined 1 percent of payroll, just as in 2024 and 2025. The taxable wage base cap is the Social Security cap. Oregon’s law includes “safe leave” for survivors of domestic violence, sexual assault, and stalking. Small businesses are not required to contribute to the program.

[27]In Colorado, the statute prescribed tax rates and wage bases set at .9 percent with contributions split between workers and employers for the program’s first two years, 2024 and 2025. In 2026, the rate dropped slightly to .88 percent. The taxable wage base is the Social Security cap. Small businesses are not required to contribute to the program. Colorado’s law was expanded beginning in 2026 to include an additional 12 weeks of leave for parents with babies in a neonatal intensive care unit—the first state in the country to offer NICU leave. The law also includes both military exigency leave and “safe” leave for survivors of domestic violence, stalking, and sexual assault. See Colorado Department of Labor and Employment.

[28]In Maryland, the rate that workers and employers will contribute has initially been set at .9 percent, shared equally, but subsequent legislation now sets May 1, 2026, as a new date by which a final rate must be specified. Maryland’s law also includes employer-side contribution exemptions for businesses with fewer than 15 employees. The taxable wage base is the Social Security cap. Maryland’s law covers military exigency leave. See Maryland FAMLI Employers Page.

[29]In Delaware, the statute prescribes the tax rate but does not specify a limit on the taxable wage base, however, the implementing agency has set the rate at the Social Security wage base. Delaware’s contribution amounts are subdivided by statute for each type of leave—parental (.32 percent), medical (.4 percent), and family care (.08 percent)—and the statute includes a trigger that would reduce benefit levels if contribution amounts exceed 1 percent. In addition, coverage and eligibility rules are restrictive: Businesses with fewer than 10 employees are not covered, either for contributions or for benefits to workers, and businesses with 11 to 24 workers only contribute for parental leave, and their employees are only covered for parental leave. Even within covered businesses, only workers who meet FMLA eligibility criteria are eligible for paid family and medical leave benefits. Delaware’s law includes military exigency leave. See Delaware Department of Labor.

[30]In Minnesota, the 2026 contribution rate is .88 percent, divided between workers and employers. The statute also permits employers to purchase either type of leave separately, with the other type covered by the state program at a reduced cost. Employers can seek 50 percent of the premium cost from employees. Businesses with fewer than 30 employees may exclude a portion of payroll expenses ($12,500 for each employee, up to $120,000) for the first 20 employees and $12,000 for the 21st through 29th employee. Employees must still pay the employee portion of the premium and are not affected by this wage exclusion. See this Employer Resource Toolkit. Minnesota’s law includes both military exigency leave and safe leave.

[31]In Maine, the statute sets a maximum initial contribution rate of 1 percent. Employers with 15 or more workers must pay 100 percent of premium costs and may seek 50 percent from their employees; in businesses with fewer than 15 workers, employers remit only 50 percent of the premium, which is deducted from employees’ pay. See Maine Department of Labor. Maine’s law covers both “safe” leave and military exigency leave.

[32]MetLife’s filings in New Hampshire are available here (tracking numbers META-133327697 and META-133327714). A spreadsheet submitted with likely rates for employers in different industries and with different workforce demographics shows a huge variation in expected rates, many exceeding the cost of paid leave in states with universal, mandatory contributions.

Senior Fellow for Gender Equity, Paid Leave & Care Policy and Strategy, Better Life Lab