Historically Black Colleges and Universities (HBCUs) are institutions of higher learning established prior to 1964 with the education of black Americans as their primary mission. Many were founded and developed in an environment of post-slavery segregation when most postsecondary institutions were not open to young people of color.

In 1862, the U.S. Congress passed the Morrill Land-Grant Act giving federal land to states for the purpose of opening colleges and universities to educate farmers, scientists and teachers. Of the institutions of higher education created under this significant investment at the federal level, only one, Alcorn State University in Mississippi, was open to blacks and thus designated as a black land-grant college. Not until 1890, with the passage of the second Land-Grant Act, were states required to open their Land-Grant institutions to black students or allocate monies to black institutions that could serve as alternatives to their white counterparts. This led to the creation of 16 exclusively black institutions, most of them public schools. Throughout the years that followed, the Freedmen’s Bureau, black churches and the American Missionary association founded many of the additional institutions that would later become HBCUs.

Over time, enrollment at HBCUs increased, as did financial support from the government and private foundations. Still, finances were a challenge for these institutions, and for the students they served, until they received federal designation and support in 1965 under the Higher Education Act. Today, HBCUs are funded under Title III-B of the Higher Education Act. This program was created to bolster HBCUs’ capacity and ensure that they provide a full range of postsecondary opportunities for young black Americans. Title III-B authorizes both mandatory and competitive funds for undergraduate, graduate and professional programs at eligible institutions “to strengthen academic, administrative, and fiscal capabilities.”

Title III

HBCUs are represented in Part B of Title III of the Higher Education Act. There are seven sections to the “Strengthening Historically Black Colleges and Universities” section of the law:

- § 1060. Findings and purposes

- § 1061. Definitions

- § 1062. Grants to institutions

- § 1063. Allotments to institutions

- § 1063a. Applications

- § 1063b. Professional or graduate institutions

- § 1063c. Reporting and audit requirements

In particular, the findings and purposes of the law acknowledge that HBCUs have contributed to the effort to attain equal opportunity in postsecondary education for black, low-income and educationally disadvantaged Americans; that state and federal governments discriminated in the allocation of land and financial resources to support black public institutions under the Morrill Act of 1862; that the current state of black colleges is partly attributable to this discriminatory practice; and, that financial assistance, especially for physical plants, financial management, academic resources and endowments are necessary to rectify past practices and help decrease future dependence on federal funds.

Types of Institutions

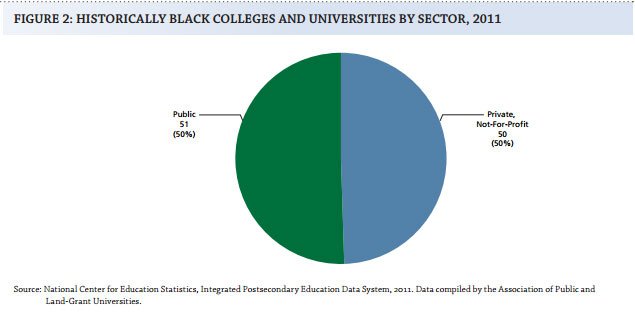

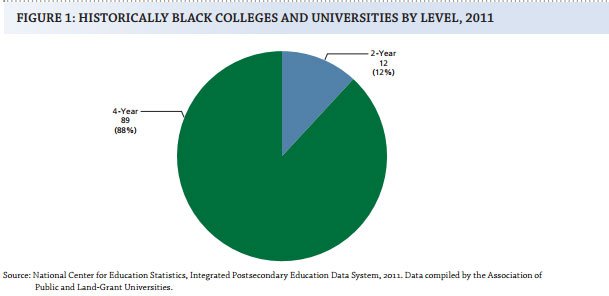

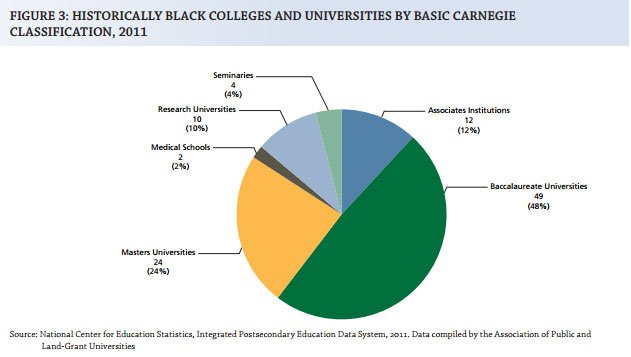

While HBCUs are connected in mission and history, they are not a monolith. There is incredible diversity within the sector with regard to institution type: 87% of HBCUs are four-year institutions, 51% are public, 17% are land grant institutions, 10% are research institutions, 23% are masters universities, 48% are baccalaureate universities, 4% are seminaries and 2% are medical schools. Together HBCUs enroll over 300,000 students.

The three figures below illustrate this institutional breakdown:

Demographics

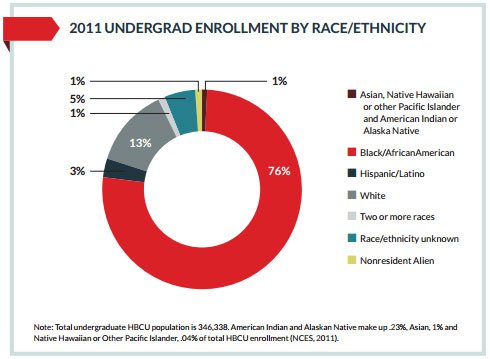

There are currently more than 100 HBCUs in 19 states, and while they were originally founded to educate black students, over time their student bodies have become more racially diverse. In 2011, non-black students made up 19% of enrollment. Still, the majority of students (76%) served by HBCUs are African Americans.

In addition to serving a high proportion of students of color, HBCUs also serve a high percentage of low-income students. Over 70% of students attending HBCUs receive Pell Grants.

HBCUs are clustered mostly in the South and Southeast with Alabama, Georgia and North Carolina having the highest concentration of these institutions. Because many HBCUs were founded after the Civil War during widespread segregation, they are clustered where the need for institutions that were willing to serve black students was greatest.

Click here for a complete list of HBCUs and their locations.

Changes in Enrollment

From 2000-2010, HBCUs saw dramatic changes in enrollment. The percentage of Asian students more than doubled, Latino student enrollment increased by 90%, American Indian student enrollment increased by 56% and white student enrollment increased by 55%. As a whole, enrollment increased by 42% (mostly at public institutions; a trend seen at non-black institutions as well). Then, in 2011, enrollment declined by 14%, erasing much of the increase made in the prior ten years. Scholars believe this may have been due to the changes in the Parent PLUS loan criteria (see Challenges Facing HBCUs below) as well as increased options at non-black colleges for students of color.

Given the 2011 drop in enrollment, the relevancy of HBCUs has recently become the focus of much inquiry (some of these discussions will be explored below). Many argue that without HBCUs and their contributions in awarding degrees to African-American students, America cannot produce enough highly skilled workers. Despite their relatively small enrollment and graduation numbers compared to non-black institutions, HBCUs produce 16% of all bachelor’s degrees earned by African-Americans, 25% of all bachelor’s degrees in education earned by African-Americans and 22% of all bachelor’s degrees in STEM fields earned by African American students.

HBCU Funding

HBCUs in good standing (not under any formal sanction from their accrediting body) receive an annual allocation through Title III of the Higher Education Act (HEA) to support their programming efforts. This formula takes into consideration three sets of data: the number of an institution’s Pell Grant recipients, graduates and graduates who go on to graduate or professional school. In the 2011 allocation, HBCUs received $236,991,068 in total funding, which went to 96 institutions. HBCU funding is only one piece of a larger allocation of Minority Serving Institution (MSI) funds. In FY2013, all MSI programs under the HEA were appropriated $776 million; these funds were distributed to more than 960 institutions.

The allowable uses for HBCU funds are as follows:

- Student services;

- Faculty and staff development;

- Purchasing or renting educational and laboratory equipment;

- Constructing or renovating instructional facilities;

- Tutoring or counseling students to improve academic success;

- Establishing or enhancing a program of teacher education designed to qualify students to teach in a public elementary or secondary school;

- Establishing community outreach programs that encourage elementary and secondary students to develop academic skills and interest to pursue a postsecondary education;

- Education designed to improve the financial literacy and economic literacy of students and families;

- Acquiring property to improve campus facilities; and,

- Using up to 20% of the grant award to establish or increase an institution’s endowment.

Impact of HBCUs

Though, 22% of HBCUs have graduation rates that exceed the national average for African-Americans at all institutions of higher education (42%), overall, HBCU graduation rates are low (30%). However, recent research indicates that HBCU graduation rates compare favorably with other (non-black) institutions when student-level factors are taken into consideration (e.g. low-income students, first-generation students and students whose pre-college education was inadequate). A recent report from the United Negro College Fund states that “…were HBCUs and non-HBCUs to enroll demographically identical populations of students, HBCUs would retain and graduate students at higher rates than their counterparts.”

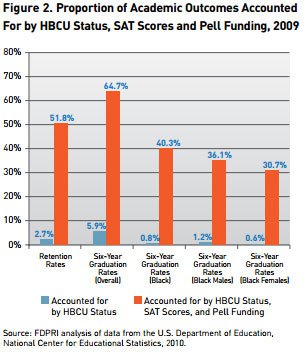

While retention rates are also low at HBCUs (about 60%), once again, research suggests that when controlled for SAT scores and Pell status, which many argue are proxies for socioeconomic status and academic preparedness, HBCU retention rates are on par with or even surpass non-HBCUs.

Differences among students might indeed explain the disparities in both graduation and retention rates given that HBCUs and non-HBCUs are not serving identical student populations. HBCUs primarily serve low-income, first-generation students (nearly 3 in 5 students) and over 25% of HBCUs are open admission institutions (compared with 14% of non HBCUs). Researchers have found that academic preparedness and socioeconomic status account for over 50% of students’ likelihood to persist into the second year of college. These same factors also account for 64.7% of students’ likelihood of graduation. Using only HBCU status to predict retention rates did not result in a statistically significant difference between HBCUs and non-HBCUs.

While standard graduation and retention rates may be a complex and sometimes controversial measure of impact, it is clear that HBCUs have a significant impact on black professional and educational success, particularly in the Science, Technology, Engineering, and Mathematics (STEM) fields. HBCUs are responsible for producing:

- 18% of ALL engineering degrees earned by African American students;

- 31% of ALL biological science degrees earned by African American students;

- 31% of ALL mathematics degrees earned by African American students;

- 21% of ALL business and management degrees earned by African American students;

- 42% of ALL agricultural science degrees earned by African American students; and,

- 17% of ALL health profession degrees earned by African American students.

Beyond STEM impact, a study in 2011 indicated that black graduates of black colleges have a career advantage over black graduates of other colleges in terms of employment rates, salary and other measures of career success (for example, doctors or lawyers who worked in low-income communities got credit for their success in the metric). Furthermore, HBCU students report more frequent and favorable relationships with their professors, earn higher college grades, report greater gains in critical and analytical thinking, and are more likely to earn a graduate or professional degree than their black peers at predominantly white institutions. Scholars cite the mission and history of HBCUs as the reason for these greater impacts on graduates.

Challenges Facing HBCUs

While there are real and demonstrated positive impacts associated with attending HBCUs; these institutions and their students also face real and demonstrated challenges as well. Some of the most prominent and most common are:

- Tightened credit eligibility for the Parent PLUS loans

Since the Parent PLUS loan program was modified in 2011 to tighten credit eligibility, many families have found it difficult to obtain a Parent PLUS loan. In the fall of 2012, 14,616 students at HBCUs learned that their parents’ applications for PLUS loans were rejected under this tightened eligibility. As a result, HBCU enrollment dropped and HBCUs lost an estimated $168 million from students who were not able to finance their education.

- A lack of academic preparedness and a need for remedial education

Data indicates that a high proportion of black students begin their postsecondary careers in remedial courses, particularly when they are enrolled at HBCUs. Because of the low success/passage rates associated with these courses many states are questioning their efficacy and are reducing funding for these courses or outright prohibiting them at four-year public colleges. As a result, HBCUs and other minority-serving institutions are left to educate and support students who are academically under-prepared in other ways and/or with very limited resources.

- An absence of collective action among HBCU leadership

While some HBCUs boast visionary leaders guiding their individual campuses to success, there are issues HBCUs face as a group, including HBCU appropriations and changes in federal student aid policy. Many HBCU advocates argue that without a cohesive strategy among HBCU presidents to work through a variety of issues and advocate for their support together, success by individual colleges cannot be sustained in the long term.

- Low retention and graduation rates

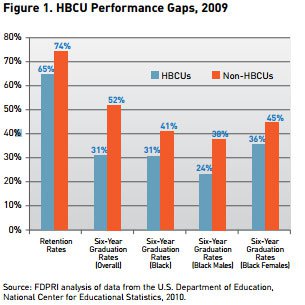

Some research indicates that when socioeconomic status and academic preparedness are taken into consideration, HBCU graduation rates equal or surpass those of their predominantly white institutional peers; without this consideration, HBCU graduation rates are more than 21 points lower than their peer institutions, and retention rates are 9 points lower than those of non-HBCUs. The figure below illustrates these findings.

- High debt burdens

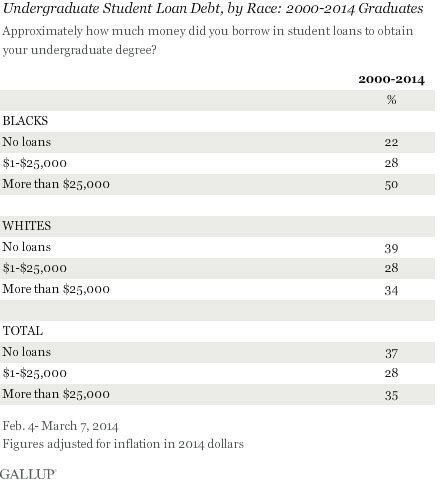

Financially, HBCU graduates are more likely than graduates of other colleges to complete their degrees with student loan debt and greater amounts of debt. Half of all HBCU graduates from 2000-2014 reported graduating with more than $25,000 in loan debt, while only 34% of predominantly white college graduates reported similar debt levels. Only 22% of HBCU graduates left school with no debt, compared to 39% of graduates at non-HBCUs. These differences can be explained in part by the fact that nearly 78% of all HBCU grads now take on loans to finance their education, compared to just over 60% of their peers at predominantly white institutions. What’s more, black college graduates are 17 points more likely to graduate with debt than white college graduates.

Below is a breakdown of undergraduate student loan debt by race:

- Issues with Accreditation In 1928, the Southern Association of Colleges and Schools (SACS) began to formally accredit HBCUs. Since then, many HBCUs have faced challenges maintaining their accreditation. Between 1998 and 2013, SACS put 29 HBCUs on warning and 20 on probation; it revoked the accreditation of four HBCUs. HBCUs make up 13% of SACS membership yet constitute 25% of SACS sanctions. It is critical for HBCUs to meet accreditation requirements in order to maintain eligibility for federal financial aid for their students and families.

Reflections on HBCU Reform Advocates, researchers and the HBCU community grapple with how HBCUs can move forward in a productive and sustainable way. Many ask how these institutions might be more impactful. To this end, many reforms have been suggested by HBCU and MSI researchers and scholars, some of which are mentioned below. At the very least, there appears to be general agreement that because HBCUs serve as unique access centers for a diverse set of low-income, first-generation students, conversations about their strengths and weaknesses should not be deficit-based but instead take into account the successes HBCUs have with the students they serve and the challenges inherent in serving those students.

Among the suggestions for reform found in the literature:

- Strengthen Institutional Governance

Improving the internal government structures of HBCUs will help level the playing field with other institutions. This could be accomplished by re-examining the makeup and reach of governing boards, improving faculty professional development, strengthening enrollment management and implementing more effective student supports. Given their stark financial realities, HBCUs would also likely benefit from finding innovative ways to increase the efficient use of their current funds. This could be achieved by finding and applying best practices in higher education governance and institutional management. Institution strengthening may also involve employing new methods for faculty recruitment.

- Grow Enrollment and Resources

Because HBCUs have traditionally been dependent on tuition dollars, they need to grow enrollment to ensure their financial futures. In addition to broadening recruitment and increasing diversity (see next bullet point), one way to raise enrollment involves strengthening the pipelines between the K-12 system and HBCUs to increase the number of African-American students who are eligible and prepared to participate in postsecondary education. Increasing retention will also stabilize enrollments and revenue by ensuring students persist year to year.

Institutions can also increase available funding by increasing alumni giving and finding major corporate and foundation donors. They could also make a case to state and federal governments that additional funds are necessary to address the unique needs of HBCU students.

- Embrace Diversity

Many suggest that a key to maintaining enrollments and financial solvency will be to embrace racial diversity on HBCU campuses. HBCUs may want to consider becoming centers of access for a more diverse set of students including Latino, American Indian, Asian, white and international students. This will require reflection on how HBCU culture and climate may be affected. HBCU missions may need to be clarified, restated or updated to adequately serve new and additional groups of students.

- Improve Student Outcomes

While HBCUs’ impact on STEM outcomes is impressive, there is a clear need to improve their overall graduation and retention rates. This will require developing strategies that provide students who are Pell-eligible and first-generation college goers with strong supports. These supports may include focusing curricula on areas of strength at particular institutions and building a talented faculty around those areas. HBCUs have been criticized for offering too many majors without sufficient quality control on courses and faculty.

Student outcomes may also be improved by using data in a more consistent and meaningful way to track student progress and provide additional support (i.e. remedial education) to struggling students. Additionally, boosting student advising and development so that students are connected to real work and research opportunities while in school can also drive at better academic outcomes. Many advocates will say there is another layer here—engaging the media to tell a more complete and fair story with regard to outcome measures (for instance, reporting graduation rates and retention rate comparisons controlled for income status).

- Improve the Perception and Transparency of HBCUs

Improved internal and external communication about the successes and challenges HBCUs face would help to identify HBCU champions; institutions that could then inform stakeholders (e.g. prospective students and families, current students, alumni, policymakers) about the positive progress at HBCUs. Key to improved communication is the willingness to present accessible and up-to-date information about institutional outcomes and struggles. While many HBCUs may be concerned that increased transparency could illuminate additional problems, transparency could also help them share their narrative in a more compelling way. This in turn could lead to greater public and financial support. As one HBCU scholar has pointed out, “institutions of higher education have not excelled at transparency, but HBCUs need to embrace this challenge, both because they have no choice and because it will help combat misperceptions, engage potential partners, and facilitate a stronger fiduciary role on the part of trustees and agencies.”

Student voices are an important piece of the HBCU story. The excerpt below, from an HBCU grad and current high school counselor shows why:

“It is very empowering to find yourself in a situation where you are in the majority. All of a sudden, you are no longer a Black person, you are a person. You do not question whether or not the treatment you received and/or the grade you were given were a result of race because race becomes a non-issue. You are exposed to a spectrum of people of color who are successful, which is contrary to the portrayal of minorities, specifically African-Americans, in the mainstream media…You find yourself surrounded by professional, credentialed people of color, Ph.D.s, professors, deans, administrators, scholars, etc., who are brilliant and worldly.”

NCES Fast Facts on HBCUs: http://nces.ed.gov/fastfacts/display.asp?id=667

Congressional Record Service: MSIs in HEA

Repositioning HBCUs for the Future: http://www.aplu.org/document.doc?id=4943

The exact number can be difficult to determine given changes in accreditation status of some HBCUs.

The Changing Face of Historically Black Colleges and Universities: http://www.gse.upenn.edu/pdf/cmsi/Changing_Face_HBCUs.pdf

HBCUs Facing the Future: http://www.fordfoundation.org/pdfs/library/facing-the-future.pdf

Congressional Record Service: MSIs in HEA

Understanding HBCU Retention and Completion: http://www.uncf.org/fdpri/Portals/0/Understanding_HBCU_Retention_and_Completion.pdf

Understanding HBCU Retention and Completion: http://www.uncf.org/fdpri/Portals/0/Understanding_HBCU_Retention_and_Completion.pdf

Tiffany Jones, SEF Presentation at PNPI’s MSI Seminar in Atlanta, GA (October 2014).

What follows is a brief PLUS Loan primer, from The Parent Trap: Parent PLUS Loans and Intergenerational Borrowin: “Congress created the Parent PLUS Loan program in 1980, primarily to help middle- and upper-middle- income families access funds to send their children to expensive private colleges. Initially, the loan was capped at $3,000 per academic year (about $8,500 in today’s dollars) with an aggregate limit of $15,000 (about $42,500 in today’s dollars). In 1992, lawmakers removed PLUS loan limits, allowing parents to borrow up to the full COA of colleges. At the same time, in order to protect parents, they restricted eligibility to parents without an adverse credit history. Today, Parent PLUS loans are more like private loans than federal student loans. PLUS loans have a relatively high interest rate—a fixed rate of 7.9 percent for the 2012-13 academic year. And because of its relatively high origination fee of 4.2 percent, the loan’s annual percentage rate (APR) is over 9 percent. Interest starts accruing once the loan is disbursed, and parents can either start making payments right away or defer them until the student drops below half-time status. Students don’t have to undergo a credit check to access federal student loans because loans made to students are a direct investment in building their human capital. Presumably, once the student graduates, he will be able to obtain a job and have the resources to pay back the investment the federal government made. Since loans to parents do not assume increased wages, they have to meet a minimum credit standard to qualify. The credit check for a PLUS loan is more lenient than the one that a private lender would conduct. Instead of considering a parent’s income or ability to repay the loan, it looks only at a parent’s adverse credit history. And the absence of any credit history is not considered a sign of an adverse credit history. In fact, up until 2011-12 it was easier for parents to apply for a loan than it was for a student, as parents did not have to fill out the Free Application for Federal Student Aid (FAFSA) to obtain a PLUS loan. Additionally, PLUS loans have no cap—parents can borrow up to the full COA for an institution. This is a stark contrast with federal Stafford loans, which are capped at between $5,500 and $7,500 a year for dependent students. COA can include many factors, but usually consists of: tuition and fees; room and board; books and supplies; transportation; and loan fees. The average COA per year at a public four-year school in 2011-12 was $23,200, compared with $43,500 at private, nonprofit institutions, and $29,000 at for-profit institutions. Like other student loans, Parent PLUS loans are seldom dischargeable in bankruptcy. But even more dangerous for borrowers, they also don’t normally qualify for some of the most flexible repayment options designed to help struggling borrowers, like IBR. As a result, parents who find themselves in over their heads on PLUS loan debt can be forced to make difficult decisions like delaying retirement or may even face Social Security garnishment. Even though the PLUS loan program was established to help middle- and upper-middle income families, the program has expanded substantially over time to provide access to credit for lower and moderate-income parents to send their children to expensive colleges. The enormous growth of the program happened after the peak of the Great Recession in 2009, at a time when family net worth diminished while college prices soared. According to The Chronicle of Higher Education, the government issued $10.6 billion of Parent PLUS loans in 2011, $6.3 billion more in inflation-adjusted dollars than it did in 2000. During that time, the number of families served almost doubled to approximately one million in 2011. And since many colleges use Parent PLUS loans to fill the gap between what they charge and the federal, state, and institutional aid their students receive, parents turned toward these easily available loans to ensure their children could attend the college of their dreams.”

The Parent Trap: Parent PLUS Loans and Intergenerational Borrowing: http://education.newamerica.net/sites/newamerica.net/files/policydocs/Corrected-20140110-ParentTrap.pdf

MSIs in Developmental Education: http://files.eric.ed.gov/fulltext/ED529085.pdf

Repositioning HBCUs for the Future: http://www.aplu.org/document.doc?id=4943

Understanding HBCU Retention and Completion: http://www.uncf.org/fdpri/Portals/0/Understanding_HBCU_Retention_and_Completion.pdf

Black College Grads More Likely to Graduate with Debt: http://www.gallup.com/poll/176051/black-college-graduates-likely-graduate-debt.aspx

Repositioning HBCUs for the Future: http://www.aplu.org/document.doc?id=4943

HBCUs Facing the Future: http://www.fordfoundation.org/pdfs/library/facing-the-future.pdf

Myths About Attending a Historically Black College: http://www.schoolguides.com/collegesearch/myths_about_attending_a_historically_black_college.html

Issues

Related

Quality Principles for Workforce Pell Programs