America’s air transport system is vital to the economic health of the nation, and to the well-being of every region of the country. Yet across much of America, the air transport system is breaking down as the few surviving airlines simultaneously jack up fares and slash service. This means citizens can’t get where they need to go. And it means large and vibrant cities – including St. Louis, Cincinnati, Pittsburgh, and Memphis – are having trouble keeping what businesses they have, let alone attracting new investors.

While most observers blame fuel prices, our research shows that the collapse in service began long before the recent spike in oil prices, hencewill likely continue even if oil prices come down. The real culprit is Congress’s 1978 decision to “deregulate” airline service. Although the Airline Deregulation Act did initially lead to lower prices, it is now clear that those prices came at the cost of older planes, fewer seats, worse service, more disruptions, lower wages for flight attendants and mechanics, and the cutting off of large swaths of America from the rest of the world.

In this report we review the history of the thinking that led to the Airline Deregulation Act and the results of that decision, and compare this experience with what earlier generations of Americans learned from the regulation of the railroads. We recommend that Congress revisit its 1978 decision, and begin a wholesale restructuring of the industry.

See below for the full report, or download it here.

I. Introduction

In 1978 president Jimmy Carter signed the Airline Deregulation Act, thereby ending government regulation of airline routes and pricing. Since then most Americans have adopted a pretty standard line about the results. On the one hand, complaining about the indignities of flying – overbooked, late, or canceled flights; surly flight attendants; lousy in-flight food service; and high fees for checked baggage – has become a staple of American life, much like complaining about cable TV providers or health insurance companies. On the other hand, it remains conventional wisdom, at least among policymakers, that increased competition has made air travel cheaper and available to a much broader segment of the public. Yet we now find ourselves at a moment when nearly all the promises of this Act have either proved false or run their course.

For more than a generation, the industry as a whole has suffered under a business model that has slowly undermined its solvency. Despite massive consolidation, steep cuts in service levels, slashed wages and benefits, sharply rising fares, and huge direct and indirect subsidies, U.S. airlines lost money in all but three years between 2001 and 2010, according to the industry’s trade group, for a cumulative net loss of $62.9 billion. Even before the recent bankruptcy of American Airlines, the value of all publicly traded U.S. airline stocks amounted to only $32.3 billion, less than that of Starbucks. [1]

That number would be even lower were it not for the major subsidies the industry has extracted from taxpayers. These include not just the billions spent by state and local governments to construct and maintain airports, and the $15 billion in loan guarantees the industry received in the aftermath of 9/11. They also include tens of billions in unfunded pension liabilities that major airlines have shoved onto taxpayers by declaring bankruptcy, as United and US Airways did in the last decade and American Airlines has been trying to do now.

Other U.S. airlines continue to benefit from special provisions passed by Congress in 2007 that allow them to underfund their pension plans, so in the future taxpayers are likely to be paying even more of the cost of flying yesterday’s planes. Yet even though these and other public subsidies dwarf those provided to Amtrak or General Motors, only one U.S. airline, Southwest, still has an investment-grade credit rating. Since 1978, almost all new start-ups have either failed or been absorbed.

The broader consequences to the public have been even starker. Loss of air service to major Americans cities has created significant regional inequities and appears to be hindering the efficiency and resiliency of the economy as a whole. Over the last five years, service to medium-sized airports fell by 18 percent.[2] Adjusted for growth of the economy, airline capacity is now at its lowest level since 1979, according to the trade group Airlines for America. And despite an improving economy, the industry has announced plans to cut another 1.5 percent of available seat miles in the first half of this year. Today, such major heartland cities as Cincinnati, St. Louis, Pittsburgh, and Memphis are increasingly cut off from each other and the global economy due to drastically curtailed airline service and monopolistic fares.

High fuel prices, to be sure, are a factor in this tale of woe. In 1999, fuel comprised 10 percent of an airline’s budget; now it ranges from 30 to 40 percent. But high fuel costs are not sufficient to explain the continuing deterioration of airline service in America. Nor can we blame the problem on the effects of the Great Recession. After decades in which the price of energy has risen and fallen and the economy has boomed and busted, the long-term trend is clear: The airline industry has been in turmoil and decline for more than thirty years, barely able to earn its cost of capital in the best of times and only then by cutting service and quality. It is now evident that the industry’s problems are structural and deepening, as is the crisis faced by cities and industries that depend now more than ever on frequent, affordable air service to remain competitive in the global economy. The purpose of this report is to re-examine the legacy of the Airline Deregulation Act and to propose workable solutions to better align the industry with the public it is intended to serve.

II. A System That Worked

Until 1978, the United States viewed airline service as a “public convenience and necessity” and used a government agency – the Civil Aeronautics Board, or CAB – to assign routes and set fares. This regulation was designed to ensure that citizens in cities of comparable size received roughly equal service, in terms of both quality and price. The government also made sure that smaller cities maintained vital links to the national air network.

This regulatory regime had problems. Unable to compete on price, airlines competed instead on service quality, sometimes to excess. Notoriously, some even offered piano bars to their first class passengers. Many flights flew at 50 percent of capacity. But on balance, the system worked well at combining quality service and reasonable prices with regional equity, particularly when compared to today. The classic system – based mainly on point-to-point service rather than hubs – was also less likely to seize up when a storm or other event shut down a single major airport. Figure 1 (Source: Economic Policy Institute)

Though it is often forgotten, under the old regulatory regime airline fares fell dramatically, thanks largely to high levels of technological innovation. The introduction of the DC-8 and other mass-market jets during the 1960s and early 1970s vastly expanded travel to such tourist destinations as Florida’s Disney World and much of the Caribbean. By 1977, 63 percent of Americans over 18 had taken a trip on an airplane, up from 33 percent in 1962.[3] Indeed, after adjusting for changes in energy prices, a 1990 study by the Economic Policy Institute concluded that airline fares fell more rapidly in the 10 years before 1978 than during the subsequent decade (figure 1).[4]

Meanwhile, the airline industry, protected from ruinous competition and manipulation by financiers, remained reasonably profitable. It was well able to finance continuous improvements in new and dramatically faster, safer, more efficient aircraft, while also providing secure middle-class jobs for pilots, mechanics and other personnel. By the early 1970s, the U.S airline system was by far the best in the world.

In the late 1970s, however, powerful voices began calling to dismantle the very regulatory regime that had widely democratized airline travel. The prime impetus came from liberal Democrats, including Ralph Nader, Ted Kennedy, Kennedy’s then-Senate aide Stephen Breyer, and an economist named Alfred Kahn, whom Carter had chosen to run the CAB. At the time, proponents argued that the change was needed to benefit the “the consumer.” Many pointed to the example of Southwest Airlines, which got its start in 1971 by flying only within Texas, thereby escaping regulation by the CAB, which had no oversight over intrastate travel. Southwest’s success with discount fares particularly resonated with liberals at a time when inflation was one of liberalism’s greatest liabilities, and when the ascendant consumer movement made low prices a liberal imperative.

Ideological currents on the left further galvanized the movement. Ralph Nader, for example, promoted the 1960s “New Left” notion that the New Deal regulatory state had been captured by incumbent industries, leading to what he called “corporate socialism.” Under the CAB, no new national airline had emerged since the 1930s (although a number of strong regional carriers – like Piedmont and Ozark – were successfully launched). Protected from competition, both airline management and unions had become overpaid and sclerotic at the expense of “the consumer,” Nader argued – and never mind if workers in those industries and their unions were stalwart members of the Democratic coalition.

Although proponents packaged the proposed changes as a process of “deregulation,” technically the plan was merely to shift regulation away from the close oversight of the CAB to the more hands-off approach of the Antitrust Division of the Department of Justice. The Carter Administration accepted both the analysis and the language used to sell it. Indeed, the administration soon went on also to “deregulate” the railroad, trucking, and natural gas industries, and to take the first steps toward rolling back banking regulation as well. That most management in these industries resisted such changes at the time only confirmed the belief of many liberals that “deregulation” was needed. Any trend toward monopoly, they reassured themselves, would be checked by rigorous antitrust enforcement.

At first, the program – which was embraced by many free market economists and the incoming Reagan Administration – seemed to pay off. To be sure, many communities instantly lost air service, and the industry rapidly restructured into the hub-and-spoke system that still exists today, leading to the elimination of many direct flights. But the early years of the new regime also saw a burst of competition and price cutting in the airline industry.

What both policymakers and the public generally missed was that the positive effects would be temporary and that many of them would have occurred under the old system too. The price of energy cratered in the mid-1980s, making it possible to cut fares and expand service. This outcome, however, was an effect of a temporary oil glut – not of the Airline Deregulation Act. A study published in the Journal of the Transportation Research Forum in 2007 confirms this. Except during a brief period after 9/11, airlines’ overall fares have continued to fall more slowly since the Act than they did before, even as fares to many midsized cities have skyrocketed.[5]

The contrast becomes starker if one considers the continuous decline in service quality, such as more overbooked planes flying to fewer places, fewer direct flights, and the lost ability to make last-minute changes in itineraries without paying exorbitant fares. The hub-and-spoke model that major airlines adopted soon after the Airline Deregulation Act has also created a more fragile, less resilient system, where bad weather in one city cascades into delays and cancellations throughout the country. As airlines have merged and further consolidated their hubs, the system has become even more brittle.[6] Indeed, the only sphere in which airline service has improved during the last generation is safety – the one area of regulation the federal government did not abandon.

III. Flights Cancelled

The full cost of abandoning regulation by the CAB must also consider the slow strangulation of heartland cities. An attractive revenue source in an era when greater levels of competition incentivized greater spread of service, many of these routes have now been discarded as drains on revenue. Even major midsize cities now face drastic flight reductions and have been left to wearily watch their airports clear out. Especially in recent years, the trend has become a noticeable factor in retarding the economic development of particular regions, and perhaps of the nation as a whole. This feature of today’s airline service is all but invisible to those who enjoy highly competitive service on major routes such as New York to Los Angeles. But if you have to travel to cities like Cincinnati, Pittsburgh, Memphis, and St. Louis, you know firsthand how hard it has become to do business in such major centers of commerce and industrial production, which are increasingly cut off from each other and from the global economy.

This drastic slashing of airline service is one of the main effects of the dramatic round of mergers in the industry over the last decade, a time that saw Delta buy Northwest (2008), United buy Continental (2010), Frontier purchase Midwest (2010), Southwest acquire Air Tran (2010), and now US Airways poised to buy American Airlines (if American doesn’t buy US Airways first). (This followed the merger of Air-Tran and Valujet (1997), American’s purchase of TWA (2001), and America West’s purchase of US Airways (2005)). In instance after instance, such mergers were followed by the cutting back of routes and seats, and sometimes the elimination of entire hubs.

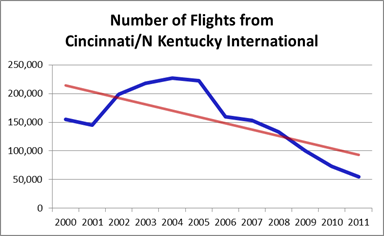

The trend is well illustrated by Cincinnati. Its metro area houses the headquarters of 10 Fortune 500 companies and 17 Fortune 1000 companies, including Procter & Gamble, Chiquita Brands International, Macy’s, and Kroger’s grocery chain. With a population of 2.1 million, it’s the 24th largest metro area in the U.S. Yet running a national, much less international business out of Cincinnati is becoming more and more problematic for a simple reason: impossible air service. Figure 2 (Source: Bureau of Transportation Statistics)

As recently as 2004, Cincinnati/North Kentucky Airport (CVG) was a major hub for Delta, offering non-stop flights to 129 major cities, including Frankfurt, Amsterdam, London, and Paris. But today, the number of flights has fallen by two thirds and an entire concourse stands eerily empty (figure 2). At the same time, flights out of the airport have the highest fares in the country. This means that if you live or do business in Cincinnati, it’s hard to fly anywhere without paying a fortune and waiting to change planes in someplace like Charlotte.

The implications for Cincinnati’s economic development are already apparent. Last fall Chiquita announced it would be moving headquarters to NASCAR Plaza in uptown Charlotte, just a 13-minute drive from that city’s busy international airport. A global business with operations in 70 countries, the company can’t thrive without the regular and reliable flights Cincinnati once offered. CEO Fernando Aguirre was reluctant about uprooting his and his employees’ lives, but explains that the situation had become untenable. “We’ve been dealing with the logistics of our business and the airport for so long now that everyone knew that the likelihood of moving was very high. It was just a matter of where and when.”[7]

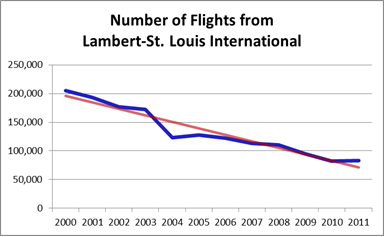

St. Louis is another example of a heartland city whose economic development is now being determined in large part by the calculations of airlines executives and their financiers. The city has seen its available seat miles – an industry measure of capacity – fall to a third of levels in 2000, following American Airlines’ takeover of TWA and Lambert International Airport’s subsequent downgrading as a mid-continental hub (figure 3).[8] Two of its five concourses are now virtually empty, and another, which used to house the TWA hub, is only partially used. A second runway, which required demolishing hundreds of homes and cost the taxpayers a billion dollars to finish in 2006, is now redundant.“This scenario,” notes Alex Marshall, a senior fellow at the Regional Plan Association, “can be likened to states building highways, and then having General Motors, Ford and other auto companies suddenly telling their drivers to use different roads.”[9] Figure 3 (Source: Bureau of Transportation Statistics)

St. Louis’s loss of service comes despite the fact that the population of the St. Louis metropolitan area, the 18th largest in the U.S., grew by more than 4 percent between 2000 and 2010. St. Louis is also the home of 21 Fortune 1000 companies, and is a major center for such international players as Anheuser-Busch InBev, Monsanto, Boeing, Emerson Electric, Express Scripts, and Nestlé Purina.[10] The metro area GDP, which is also propelled by such major research institutions as Washington University and a fast-growing medical sciences sector, rivals that of oil rich Qatar. Yet like many other midsize American cities, St. Louis’s economic development is now hostage to the shifting, closed-door deals and mergers of a mere handful of airline executives. The prevailing mood was captured by a St. Louis Post-Dispatch editorial that quoted “The Serenity Prayer” in advocating philosophical acceptance of the distant forces shaping the region.[11]

The situation is much the same in Memphis. Designated a hub by Northwest in 1986, its international airport undertook record-breaking expansion projects to house the airline and its regional carrier, Northwest Airlink.[12] As elsewhere, lack of competition at the airport led to record high airfares, but high prices haven’t been enough to preserve service (figure 4).[13] Delta’s acquisition of Northwest allowed the executives of the Atlanta-based airline to strip away the airport’s hub status, just as they did to Cincinnati. In March 2011 the post-merger airline announced it would cut 25 percent of its flights from the city. Flights to Eastern Europe and the Middle East have been slashed entirely, while service to Paris and Rome will be infrequent.[14] Figure 4 (Source: Bureau of Transportation Statistics)

The loss of connectivity affects Memphis in ways big and small. The Folk Alliance music conference, annually held in downtown Memphis, recently announced it would move to Kansas City starting in 2014, due partly to airport hassles.[15] The Church of God in Christ, too, decided to move its yearly convention out of Memphis recently, breaking 100 years of tradition. When Mayor A.C. Wharton visited the Church to lure its 50,000 convention attendants back to Bluff City, he learned of the material culprit that had pushed the spiritual gathering away: air fares.[16]

Pittsburgh is another example of a major city whose culture and economy are increasingly determined not by its underlying fundamentals but by the dictates of an ever-more concentrated, yet failing airline industry. After it lost most of its steel industry in the 1970s, the city adjusted so that it could compete in the emerging global economy. When the city played host to the G-20 Summit in 2009, President Obama hailed Pittsburg’s transformation “from a city of steel to a center for high-tech innovation – including green technology, education and training, and research and development.” Forbes that same year named Pittsburgh one of America’s best cities for job growth, while the Economist lauded its cosmopolitan cultural amenities, from the top-flight Pittsburgh Symphony Orchestra to the Pittsburgh Opera.[17]

But Pittsburgh’s renewal as a vibrant, creative, international city is in doubt due to the downscaling of its international airport, which now stands largely empty. Pittsburgh International, which the city went deeply into debt to turn into a showcase during the 1990s, then offered more than 600 daily nonstop flights.[18] But beset by financial struggles, US Airways decided to cut a third of its flights in 2003.[19] Service further tumbled after it merged with America West in 2005 and decided to concentrate its hub operations in Philadelphia and Charlotte instead.[20] In 2000 US Airways provided 80 percent of total flights from Pittsburgh; today it provides less than 10 percent of them.[21] Its daily flights have plunged from 542 to around 68, causing the shuttering of half the gates at the airport, as well as parts of two concourses (figure 5).[22] Figure 5 (Source: Bureau of Transportation Statistics)

K&L Gates, one of the country’s largest law firms, used to hold its firm-wide management meeting near its Pittsburgh headquarters, but after the hassle flying there became excessive, the firm began hosting its meeting outside of New York and Washington, DC instead. The University of Pittsburgh Medical Center, the biggest employer in the region, reports that its researchers and physicians are increasingly choosing to drive to professional conferences whenever they can.[23] Flying between Pittsburgh and New York or Washington can easily take a whole day after having to change in Philadelphia or Charlotte.

Left unaddressed, the issue is bound to keep costing these regions jobs and investment. Already Pittsburgh International supports almost 4,000 fewer jobs and $130 million less in economic activity than it did four years ago.[24] Top business leaders in St. Louis recently listed air transportation as one of the main problems facing growing companies in the region.[25] And 40 percent of Memphis businesses surveyed said their future investment in the city would partly depend on its air service.[26]

The real effects may be far worse than the numbers show. Patrick Ewing, who visits local companies on behalf of the Economic Development Division in Cincinnati, notes that what was once a competitive advantage for the region has now become a major weakness. “The big firms conduct much of their screening before even reaching out to us, so we don’t have an accurate sense of how many opportunities we might have missed because of the flight levels,” Ewing said. “It is possible businesses now aren’t even considering us to begin with.”

Compounding these losses are the millions in tax dollars that many regions are now forced to pay to buy back service. Since losing its hub status Pittsburgh International has received $60 million in public funds.[27] The state partnered with local businesses to coax Delta into resuming nonstop flights to Paris, agreeing to compensate the airline for losses.[28] Most recently the airport announced lower fees for any carrier willing to offer flights – a taxpayer-backed concession with few long-term guarantees that the public will ever see its money paid back.[29] A similar task force in Cincinnati recently announced it was hiring an outside consulting firm to advise it on how to win back more service.[30]

IV. Lessons Unlearned

Many readers may be inclined to see these deficiencies of the U.S. airlines system as inevitable “market” outcomes. If Chiquita was meant to remain headquartered in Cincinnati, or if Pittsburgh was meant to build on its transition from a dying old-line industrial city, then market processes would all but automatically summon forth the necessary air service. But while trusting entirely in private investment decisions may work well in some economic realms, it is deeply problematic in the sorts of high fixed cost, networked industries like airlines upon which the entire U.S. economy depends.

With air service, one factor is basic physics. It requires a tremendous amount of energy just to get a plane in the air. This means the per-mile cost to the airlines of short-haul service is always going to be higher than that of long-haul service, regardless of how the industry is organized. Yet the value of airline service to the public and the economy depends in great part on providing connectivity to as many places as possible. Thus, without some form of cross-subsidization between short hauls and long hauls, the economic benefits of the network will be compromised. Fewer people will be flying to fewer places, which by itself hinders economic activity, while the high fixed cost of the remaining service has to be spread among a diminished number of passengers.

This highlights another problem that inevitably leads to declining service in the absence of smart regulation of airline markets. It costs virtually the same to maintain an air traffic control tower, a runway, and ticketing and baggage-handling facilities whether an airport serves five or 50 flights a day, or whether each plane carries five or 50 passengers. So the per-passenger cost on low-volume routes is necessarily more than on high-volume routes, which again requires some form of cross-subsidization if robust connectivity is to be maintained.

Dealing with high fixed costs is a challenge common to virtually all networked industries, and, in one way or another, America has grappled with the problem throughout its history. The Founders understood that private enterprise could not by itself provide postal service to everywhere that needed it, due to the high cost of delivering mail to smaller towns and far-flung cities. They explicitly wrote the solution into the Constitution, which establishes a government monopoly to take on the challenge of providing the necessary cross-subsidization. (That monopoly did so, in large part, by charging the same amount to mail a letter across the country as across town.)

Throughout most of the 19th century and much of the 20th, generations of Americans similarly struggled with how to maintain an equitable and efficient railroad network, and for much the same reason. During various railroad bubbles, exuberant investors would build lines to the farthest corners of the continent, much like start-up airlines did in the 1980s. But over time, the high fixed cost of railroading and the basic economics of any networked industry left all but the core of the emerging system unprofitable before it received the benefits of government regulation. In the 1870s, railroads accounting for more than 30 percent of domestic mileage failed or fell into court-ordered receivership.[31]

This was true even though most railroads maintained a near or total monopoly in most of the intermediate towns through which they ran. As Charles Francis Adams wrote in his 1878 book, Railroads: Their Origin and Problems:

Every local settlement and every secluded farmer saw other settlements and other farmers more fortunately placed, whose consequent prosperity seemed to make their own ruin a question of time. Place to place, or man to man, they might compete; but where the weight of the railroad was flung into one scale, it was strange indeed if the other did not kick the beam.[32]

Matters soon got worse. High fixed costs combined with ruinous competition in the early railroad industry created an overwhelming business incentive to consolidate and downsize – again, much like what is happening in the airline industry today. And consolidation in turn led to even more monopoly power – not just over small and midsize communities but over large cities as well. By the 1880s, the fortunes of such major cities as Philadelphia, Baltimore, St. Louis, and Cincinnati rose and fell according to how various railroad financiers or “robber barons” combined and conspired to fix rates. Just as Americans scream today about the high cost of flying to a city like Cincinnati, where service is dominated by a single carrier, Americans of yesteryear faced impossible price discrimination when traveling or shipping to places dominated by a single railroad “trust” or “pool.”

This, more than any other factor, is what led many Americans of previous generations to embrace the idea that government must play a role in regulating railroads and other networked industries essential to the working of the economy as whole. “While the result of other ordinary competition was to reduce and equalize prices,” Adams noted, “that of railroad competition was to produce local inequalities and to arbitrarily raise and depress prices. The teachings of political economy were at fault.”[33]

And indeed they were. The practical response was to create the Interstate Commerce Commission in 1887 – a move that most citizens viewed as essential to preserving free-enterprise, fair markets, and the American way of life. The ICC took on the task of moderating the price discrimination that railroads practiced, evening out the burden among different regions and classes of passengers and shippers in a way that allowed railroads to earn enough money to cover their fixed costs, improve their infrastructure, and give their investors a fair reward. In effect, the profits railroads earned on some highly trafficked long-haul routes came to be rechanneled by government policy to cover the cost of providing balanced and affordable service throughout the country. Railroads were regulated much as telephones and power companies came to be—as natural monopolies that would be allowed to remain in private hands and earn a profit, but not at the cost of skewing the overall efficiency, distribution, and fairness of the American economy.

The process was messy and far from flawless. Striking the right balance required that Americans hash out what would today be called an “industrial policy,” and to do so in sometimes minute detail, such as setting the relative prices of shipping hogs verses hams from Dubuque to Chicago. During long periods, populist demand for low fares harmed the industry, when it resulted in actions that prevented railways from earning their cost of capital. But overall, government regulation of railroad pricing and routes worked better than letting a few financiers rule the system for their own private benefit. During this period, the country emerged as an industrial powerhouse, while at the same time managing to protect the competitiveness of small-scale entrepreneurs and of midsize manufacturing in cities like Cincinnati and St. Louis. It wasn’t that the government picked winners or losers; rather, it prevented the machinations of railroad financiers from doing so.

V. The Limits of Antitrust

The condition of today’s airlines industry would not surprise Charles Francis Adams, Louis Brandeis, and many other Americans who struggled in the late 19th and early 20th centuries with how to harness the emergence of railroads, telephones, electrical power, and other networked industries to public purposes. They would recognize the familiar boom-and-bust cycle of new entrants that occurred in the early period after the Airline Deregulation Act and the subsequent trend toward consolidation, deteriorating service, and increasing price discrimination. They would understand, in other words, that the main goal of regulation is not to promote unfettered competition within a network, but to shape that competition – which is natural in all human endeavors – to be constructive rather than destructive.

Indeed, going forward, all industry forecasts call for further consolidation and continually rising fares and fees, accompanied by declining service on all but the most heavily trafficked routes. From time to time, short-term fare wars may break out on particular routes, particularly if any team of investors is foolish enough to bring a new start-up airline to town. Periodic dips in energy prices may bring a temporary reprieve. But over time, experience has shown that nearly all start-ups are eventually crushed by incumbent carriers, which – despite their increasing consolidation, heavy public subsidies, and reductions in vital service to major cities – remain serially unable to earn even their cost of capital over time.

The landscape might have looked better if the Department of Justice had not largely abandoned antitrust action during the early years of the Reagan administration. Steady deal-making throughout the 1980s yielded mergers between Delta and Western Airlines, Northwest and Republic Airlines, and American and Air California, and resulted in raids on Eastern and TWA by the financiers Frank Lorenzo and Carl Icahn. Of the merger activity in the last decade, only the proposed tie-up between US Airways and United Airlines in 2000 drew notable resistance from the DOJ. Many – Kahn and other advocates of “deregulation” included – have blamed lax antitrust enforcement for present failures.[34]

But in practice, it is not at all clear that antitrust regulation of the airline industry would have worked as the original advocates of the Airline Deregulation Act envisioned. “Antitrust is a very difficult tool to use,” notes former congressman Jim Oberstar, who voted for the Act at the time but now acknowledges that Congress was wrong to rely on antitrust. “It’s like trying to use a sledge hammer when what you need is a ball peen hammer for a very delicate task.”

More fundamentally, even strong and strategic antitrust enforcement would not have solved the industry’s underlying problem. This is because airlines –just like railroads, waterworks, electrical utilities, and most other networked systems –require concentration both to achieve economies of scale and to enable the cross-subsidization between low- and high-cost service necessary to preserve their value as networks. With this in mind, the industry’s ongoing consolidation is more a symptom of the flawed business model created by the Airline Deregulation Act than a cause. When it comes to network monopolies that provide essential services to the public, there is no equitable or efficient alternative to having the government regulate or coordinate entry, prices, and service levels –no matter how political the process may be.

This is easy to see in extreme examples. It would be outrageously inefficient if each city had scores of waterworks and sewers, and also needlessly unfair; millions of Americans would still be waiting for indoor plumbing, just as millions had to wait decades for telephone and electrical service, until the government stepped in to enforce cross-subsidizing interventions like the New Deal’s rural electrification program.

Transportation in all its forms is not much different, as most people can see easily when it comes to highways. If we had a “deregulated” private interstate system, we would have lots of high-quality toll roads running straight and fast between the largest population centers — indeed, probably far more than we need. And from time to time, exuberant entrepreneurs might try to make a profit by constructing a new artery road here or there as well. (This was, in fact, the basic plan of many of America’s early long-distance road developers, back in the 1920s.)[35] But the high fixed cost of building roads would mean that most smaller cities either would remain off the network or would have to pay such high tolls that they would never stand a chance of growing. Either way, owners of major highways, seeking to avoid competition, would gradually buy up owners of lesser highways, and then each other, until everyone was paying exorbitant tolls and the whole economy suffered. That was the lesson previous generations learned from railroads. The current generation is learning it all over again, from our experience with “deregulated” airlines.

VI. Charting Forward

While free market ideology paints regulation as interfering with an organic, self-correcting force, the reality is that every market is always regulated; it is just a question of which actors regulate the market, and to what end. Though called “deregulation,” the 1978 Act merely traded regulation by government in the public interest for regulation by private actors for private interest. As Paul Stephen Dempsey and Andrew Goetz have noted:

The net result of deregulation is that the five-member Civil Aeronautics Board has, in effect, been replaced by the chief executive officers of the largest five or six airlines. If we learned nothing else from the era of railroad robber barons, we should have learned that the transportation industry has too many social and economic externalities to allow it to be manipulated by a handful of unconstrained monopolists. The quasi-public utility nature of the transportation industry suggests the need for enlightened regulation in the public interest.[36]

Worse, in the case of airlines, the public – including millions of citizens who never fly – continues to foot the bill through billions in subsidies and pension guarantees, not to mention funding and maintenance of airport and airway infrastructure. To subject flight levels and routes to some minimal public standards and oversight is not just a need, but a right of citizenship.

Any form of public regulation can, sure enough, be taken to excess. Kahn used to complain that his desk at the CAB was piled with papers demanding answers to trivial questions, such as, “How many travel agents may a tour operator give free passage to inspect an all-inclusive tour? And must those agents then visit and inspect every one of the accommodations in the package?” Enlightened regulation certainly need not concern itself with this level of detail.

The old CAB also suffered from being overly focused on air transport, as opposed to taking a more integrated view of the transportation system as a whole. On many heavily traveled, short-haul routes, high-speed rail would be a far more economically viable – and more environmentally friendly – option than deeply subsidized airline service, especially if airlines and rail terminals are combined to make for easy connectivity, as is the case in most other industrialized nations. Yet the bureaucratic organization of the CAB, as with U.S. transportation policy planning generally, was concentrated only on isolated specific modes. A more balanced regulatory structure will lead to a more balanced transportation system, while also guarding against any tendency toward capture by specific transportation industries and interests.

Going forward, enlightened regulation also need not entail the explicit rate- and route-setting of the CAB. It could instead simply ensure that competition-driven outcomes remain within certain parameters. For example, it could introduce price floors and ceilings to generate fares that more reflect the cost of a flight rather than the degree of monopolization in any given market, as Dempsey & Goetz have recommended. It could also introduce capital-reserve requirements to encourage more sound economic footing.

Whatever the specific policies, two goals should be foremost:

(1) Develop an industry economically stable enough to earn its cost of capital, invest in technological improvements, absorb price shocks without disrupting access to travel, and treat both passengers and employees with dignity.

(2) Shift the industry away from a business model that assesses each flight on its stand-alone profitability and towards a system that considers the society-wide purposes of the transportation system, with the ability to achieve cross-subsidies between different regions, routes, and modes as needed to ensure equitable access across the country and balanced economic development.

Currently most Americans are entirely bound to whatever flight levels and fares corporate whims and appetites dictate. The choice is clear. We can either watch our air transportation system continue to erode and turn further against public purposes, or claim it back.

[1] “Toward Global Competitiveness, Economic Empowerment and Sustained Profitability,” Airlines for America, February 8, 2012.

[2] Jad Mouwad, “Air Service Cutbacks Hit Hardest Where Recession Did,” New York Times, July 8, 2011.

[3] Passenger traffic grew almost 500 percent in 20 years: 49 million passengers enplaned in 1958, compared to 240 million in 1977. In 1962 just 33 percent of all Americans over 18 had taken a trip on an airplane; by 1977 63 percent had. “Air Transport 1977: The Annual Report of the U.S. Scheduled Airline Industry,” Airlines for America (formerly Air Transport Association), 1977, http://www.airlines.org/Documents/economicreports/1977.pdf

[4] Stephen Paul Dempsey, “Flying Blind: The Failure of Airline Deregulation,” Economic Policy Institute, 1990.

[5] David B. Richards, “Did Passenger Fare Savings Occur After Airline Deregulation?” Journal of the Transportation Research Forum 46, No. 1 (2007).

[6] A series by the Chicago Tribune vividly captures how isolated disruptions can ripple into network-wide gridlock. See Louise Kiernan, “The Longest Day,” Chicago Tribune, November 19, 2001.

[7] Will Boye, “Chiquita’s CEO talks about relocation,” Cincinnati Business Journal, December 16, 2011.

[8] Available seat miles (ASM) in 2000: 17,059,622. ASM in 2010: 5,415,760. Bureau of Transportation Statistics.

[9] Alex Marshall, “Airport Economics: Big city airports need federal regulations to help weather airline instability,” Governing, April 2010.

[10] “Fortune 1000 Companies and Forbes Largest Private Companies,” St. Louis Regional Chamber & Growth Association, http://www.stlrcga.org/x2629.xml

[11] “Lambert Airport’s loss of hub status reinforces need to change things we can,” St. Louis (MO) Post-Dispatch, September 23, 2009.

[12] “Our History,” Memphis International Airport, http://www.memphisairport.org/about/history

[13] “2nd-Quarter 2011 Domestic Air Fares Rose 8.5 percent from 2nd Quarter 2010,” Bureau of Transportation Statistics, http://www.bts.gov/press_releases/2011/bts063_11/html/bts063_11.html

[14] Wayne Risher, “Squeezing capacity: Delta Air Lines profits, Memphis loses, as it cuts routes,” Commercial Appeal, October 25, 2011; Andy Ashby, “More Delta flight cuts from Memphis coming, website says,” Memphis Business Journal, October 10, 2011.

[15] Folk Alliance president Louis Jay Meyers cited inadequate space at the Memphis hotel where it usually held the festival, in addition to hassles with the airport. “Memphis is one of the most expensive airports in the country. And they’re cutting international flights all the time, which is a problem for our (overseas) members,” he said. Bob Mehr, “Folk Alliance to leave Memphis,” Commercial Appeal, November 1, 2011.

[16] The latest instance of air fares diverting activity from Memphis led the Mayor to conclude that the issue now warranted serious attention. “It’s no longer something only the bloggers are talking about. We’re seeing it everyday. We have to zero in on that,” he said. Tealy Devereaux, “COGIC Quit Memphis Over Air-Fare,” MyFoxMemphis, 9 November, 2011.

[17] David J. Lynch, “Pittsburgh’s heart of steel still beats amid transformed city,” USA Today, September 22, 2009; Tara Weiss, “Ten Cities for Job Growth in 2009,” Forbes, January 5, 2009; “The revival of Pittsburgh: Lessons for the G20,” Economist, September 17, 2009.

[18] Mark Belko, “US Airways cuts nonstop flights to Florida,” Pittsburgh Post-Gazette, September 5, 2008.

[19] Bureau of Transportation Statistics.

[20] Dan Fitzpatrick, “US Airways ends flights from Pittsburgh to 5 cities,” Pittsburgh Post-Gazette, May 17, 2007.

[21] US Airways flew 95,461 flights out of Pittsburgh in 2000; in 2010 it flew 5,016. Bureau of Transportation Statistics.

[22] Mark Belko, “Silence is deafening in airport concourses,” Pittsburgh Post-Gazette, November 11, 2007.

[23] According to UPMC spokeswoman Susan Manko, “They’re still going [on trips] but it’s more time consuming and inconvenient. The flights aren’t offered at convenient times. More and more people are driving rather than flying whenever they can, like to Washington, DC.” Mark Belko, “Business fliers find it tough to get here,” Pittsburgh Post-Gazette, May 3, 2009.

[24] “The Economic Impact of Aviation in Pennsylvania,” Pennsylvania Department of Transportation, Bureau of Aviation, prepared by Wilbur Smith Associates, 2011.

[25] “Survey of ‘Top 50’ Award Nominees Reveals Top Issues Facing Growing Companies in St. Louis Region,” St. Louis Regional Chamber & Growth Association, November 10, 2010.

[26] “An Economic Assessment of the Impact of the Memphis International Airport,” Sparks Bureau of Business and Economic Research, Fogelman College of Business & Economics, The University of Memphis, April 2009.

[27] Tom Fontaine, “Consultant: Entice airlines by offering subsidies,” Pittsburgh Tribune-Review, June 14, 2011.

[28] Thomas Olson, “Delta plans to expand service to Paris,” Pittsburgh Tribune-Review, November 17, 2010.

[29] Tom Fontaine, “International airport lowers fees; more service sought,” Pittsburgh Tribune-Review, October 15, 2011.

[30] Dan Monk, “Air service consultant hired by CBC, Cincinnati chamber,” Business Courier, September 30, 2011.

[31] Gerald Berk, Alternative Tracks, The Constitution of the American Industrial Order: 1865-1917 (Baltimore: Johns Hopkins University Press, 1994), 47.

[32] Charles Francis Adams, The Railroad Problem (New York: Cosimo, 2005), 125.

[33] Adams, The Railroad Problem, 119.

[34] After two decades of seeing deregulation’s outcomes, Kahn remained adamant that antitrust enforcement would have produced a more fair and stable industry. “I’ve been saying for these 20 years when you deregulate an industry, the antitrust laws become more important rather than less. That’s because now customers are dependent not on regulators to protect them but on competition.” Charles Boisseau, “Has freedom resulted in fairness,” Houston Chronicle, March 31, 1998.

[35] Earl Swift, The Big Roads: The Untold Story of the Engineers, Visionaries, and Trailblazers Who Created the American Superhighways(New York: Houghton Mifflin Harcourt, 2011).

[36] Paul Stephen Dempsey and Andrew R. Goetz, Airline Deregulation and Laissez-Faire Mythology (Connecticut: Quorum Books, 1992), 339.

Downloads

More About the Authors

Phillip Longman

Senior Fellow

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}