Zachary D. Blizard

Data Analytics and Research Manager, Center for the Study of Economic Mobility

Amidst skyrocketing home prices and a nationwide undersupply of housing, more and more homes are being purchased with cash. A rise in cash purchases suggests that it’s investors and wealthy buyers that are increasingly purchasing property, and not buyers that need to spread the cost of homeownership over a long period of time via a mortgage loan.

If cash purchases mean that fewer homes are being purchased using mortgage loans, what does that mean for buyers who not only lack the wealth to purchase a home outright with cash, but are also traditionally underserved by credit markets?

Loans insured by the Federal Housing Administration (FHA) were intended specifically for these buyers; the FHA provides mortgage financing to those who lack the savings and the credit to qualify for a loan in the conventional market (where loans are not backed by the federal government). As such, FHA loans are a vehicle to homeownership for many first-time or low-and-moderate income buyers, often in communities of color.

In this analysis, we use Home Mortgage Disclosure Act (HMDA) data to assess whether FHA lending is meeting its intended purpose. Specifically, we assess FHA lending in the overall mortgage market and in the small dollar mortgage market (which we define as loans below $100,000) in North Carolina from the 2007-2009 financial recession until 2021, the last year data is available.

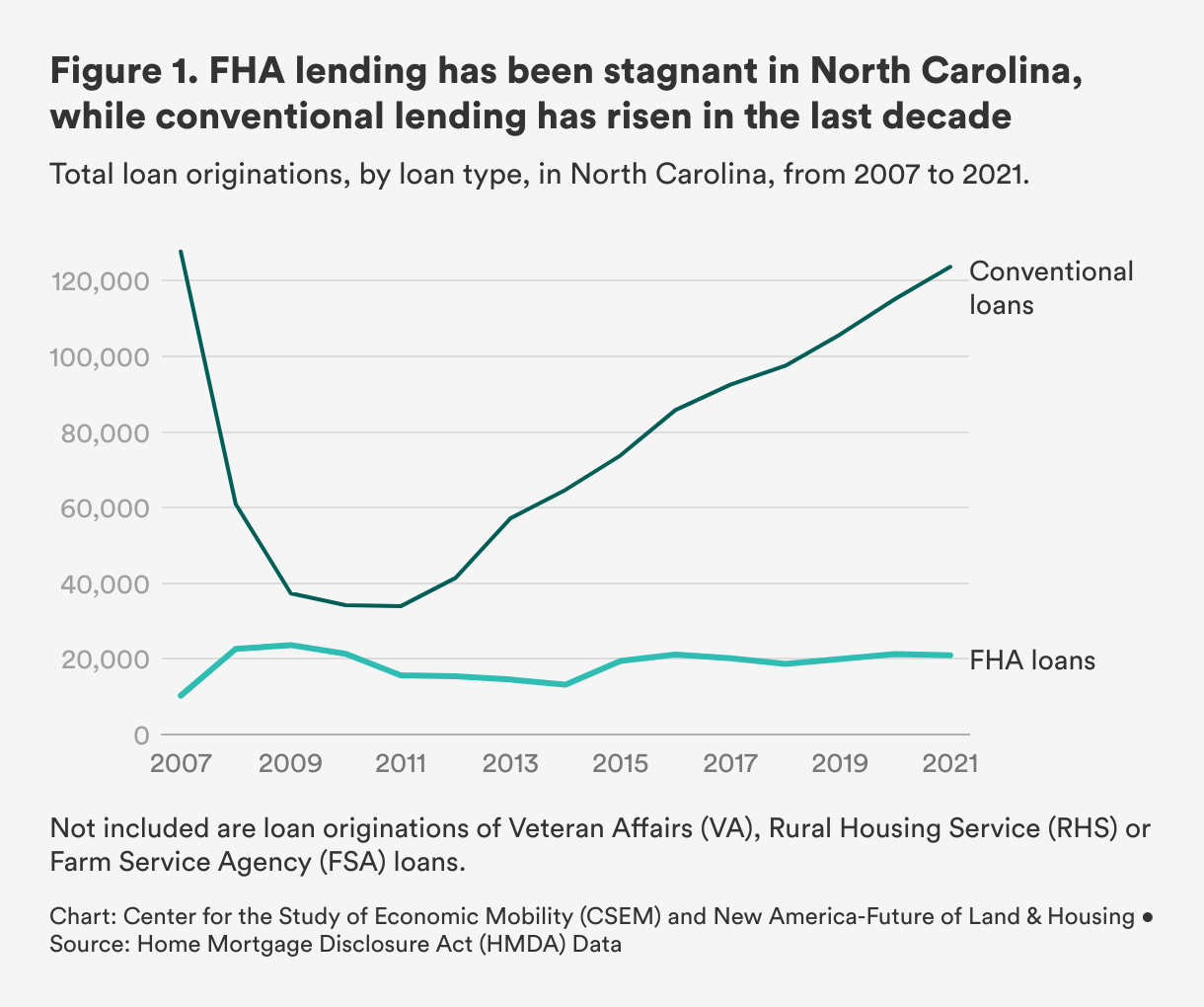

To assess trends in overall mortgage lending during and after the 2007 financial crisis, we chart the total volume of FHA and conventional loans originated from 2007 to 2021 in North Carolina (Figure 1).

During the 2007-2009 financial crisis, the volume of conventional loans originated in North Carolina plummeted by 71 percent (from 127,721 to 37,339). Over this same time period, the volume of FHA loans more than doubled (from 10,275 in 2007 to 23,648 in 2009).

Despite this initial decline, conventional lending has grown precipitously since 2011, by almost 265 percent, and by 2021, has nearly reached pre-financial crisis lending levels. FHA lending, on the other hand, has remained more or less stagnant over time. Between 2015 and 2021, the number of FHA loans originated each year remained consistent around 20,000 loans.

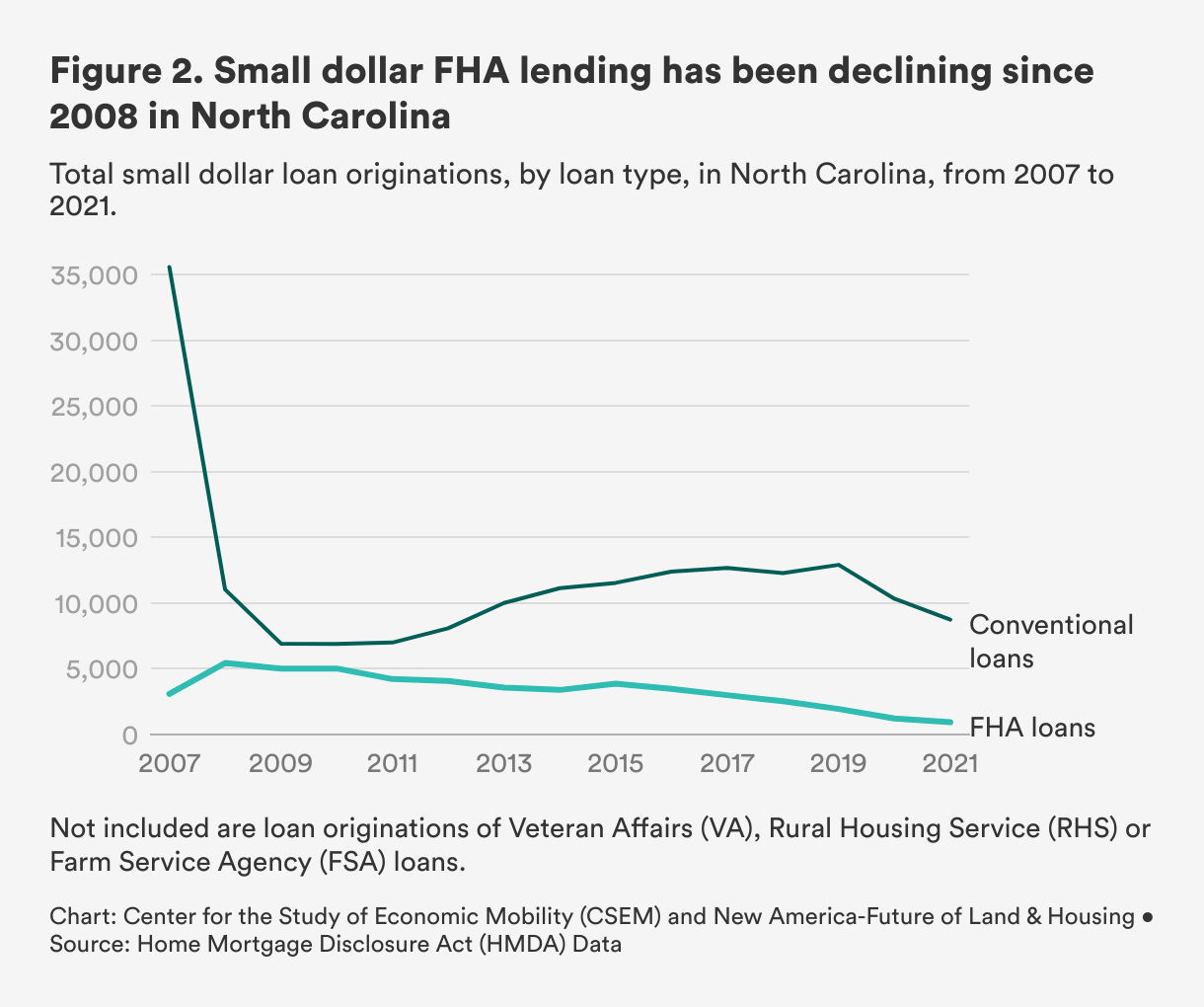

Figure 2 charts the total volume of FHA and conventional small dollar loans (those below $100,000) from 2007 to 2021 in North Carolina. Compared to FHA and conventional lending in the overall mortgage market in Figure 1, conventional and FHA small dollar lending have seen overall declines after the 2007-2009 financial crisis, despite fluctuating over time.

While conventional small dollar loan originations began to increase in 2011 following a precipitous decline, they are far from reaching their pre-financial crisis levels. Small dollar FHA loans, on the other hand, have been steadily declining since 2008; only 941 small dollar FHA loans were originated statewide in 2021, down from 5,437 at the peak in 2008.

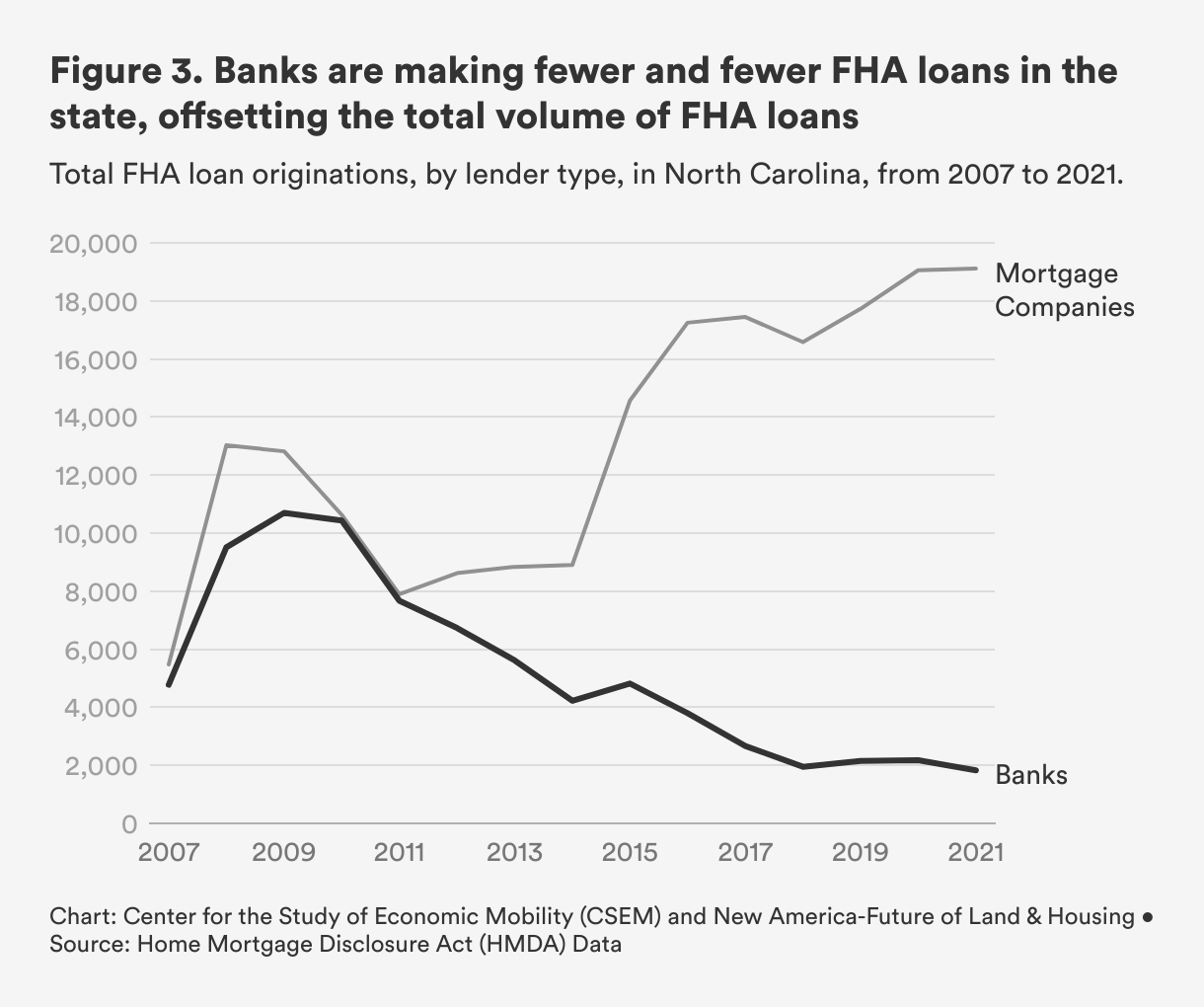

One reason why FHA lending may be stagnant relative to conventional lending in both the overall mortgage market and the small dollar market is that banks have been originating fewer and fewer FHA loans over time. To understand trends in the type of FHA lender, we examined whether FHA loans were originated by a bank or a mortgage company.[2]

The stagnation in FHA lending is driven largely by the withdrawal of banks from this market.

Banks are institutions that are allowed to receive and accept financial deposits, or depository institutions, whereas mortgage companies provide loans, but are not depository institutions. Because mortgage lending is the primary business operation for mortgage companies, but a subset of banks business operations, they face different regulations. The three largest banks in our HMDA North Carolina dataset are Wells Fargo, BB&T (now Truist), and Bank of America, and the three largest mortgage companies are Movement Mortgage, Quicken Loans, and Fairway Independent Mortgage.

Figure 3 charts the volume of FHA lending by banks and mortgage companies in North Carolina from 2007 to 2021 in the overall mortgage market. The steady decline in FHA lending by banks since 2009, relative to the explosive rise in FHA lending by mortgage companies after 2014, is notable. FHA loans originated by banks declined nearly 83 percent between the height of FHA bank lending in 2009 and 2021 (from 10,700 loans to 1,800 loans). FHA loans originated by mortgage companies, on the other hand, have more than doubled since 2014 (from 9,000 in 2014 to 19,000 in 2021).

Despite the rise in FHA lending by mortgage companies in North Carolina, the total volume of FHA loan originations is offset by the decline in FHA lending by banks. Put another way, the stagnation in FHA loan originations is driven largely by the withdrawal of banks from the FHA loan market.

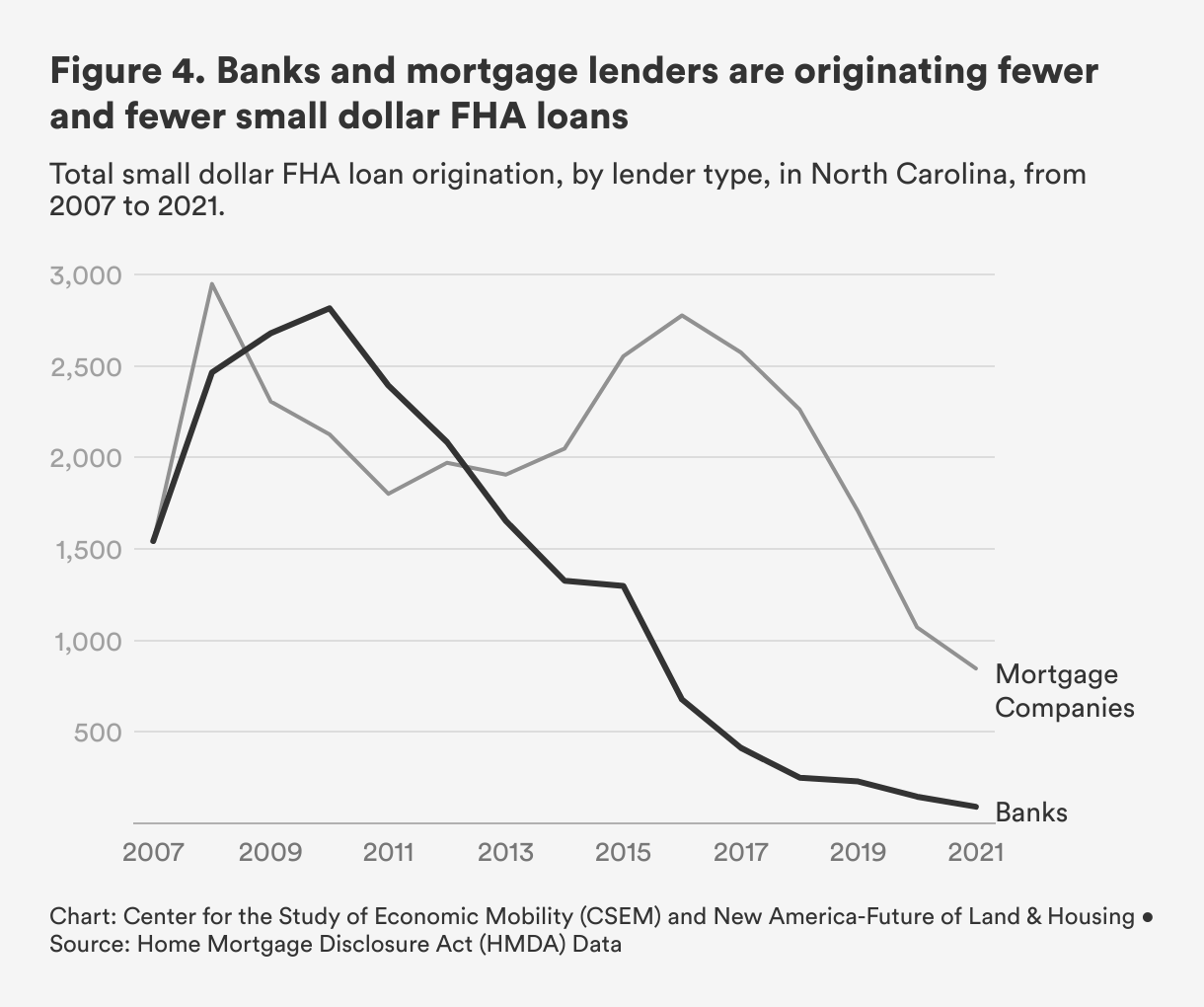

Figure 4 charts the volume of FHA lending by banks and mortgage companies in North Carolina from 2007 to 2021, only among the market for small dollar FHA loans. Unlike in the overall FHA loan market, both banks and mortgage companies have originated fewer and fewer small dollar FHA loans over time.

The decline in small dollar FHA lending by banks in North Carolina began in 2010. Banks originated 2,815 small dollar FHA loans in 2010, dropping to 91 FHA loans by 2021. The decline in small dollar FHA lending by mortgage companies began years later, in 2016, but has seen a similar rate of decline as banks since then.

In sum, banks are originating fewer and fewer FHA loans in both the overall FHA and small dollar FHA market, while FHA loans originated by mortgage companies is only declining for loans below $100,000, but skyrocketing in the overall FHA mortgage market.

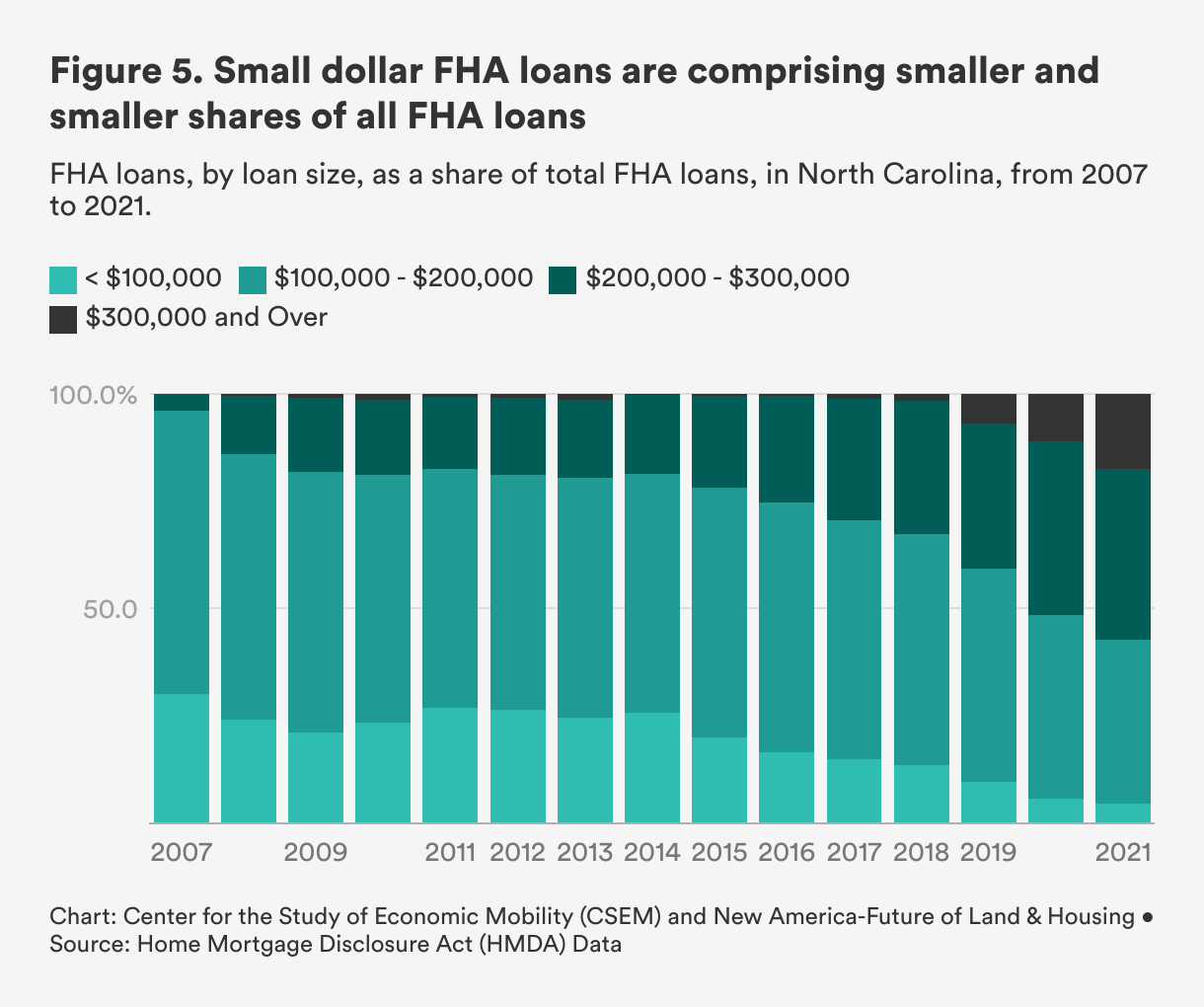

To better understand trends in the size of FHA loans over time, we assess the share of various FHA loan amounts in North Carolina from 2007 to 2021 (Figure 5).

Small dollar FHA loans as a share of all FHA lending has decreased over time, from 30.1 percent in 2007 to 4.5 percent in 2021. This same trend can be seen from FHA loans between $100,000 and $200,000, which used to be the most common range for FHA loans, but have decreased as a share of all FHA loans, from 55.9 percent in 2007 to 38.1 percent in 2021.

FHA loans between $200,000 and $300,000, on the other hand, increased from 4 percent in 2007 to 39.9 percent in 2021. FHA loans $300,000 and over were non-existent in North Carolina in 2007, but have since climbed to 17.5 percent of all FHA loans originated in 2021.

We see that FHA loans have steadily been shifting away from both small dollar loans and loans between $100,000 and $200,000, and moving towards loans that are $200,000 and above.

Across the state of North Carolina, it is clear that access to mortgage financing designed for first-time and low-and-moderate income home buyers has been steadily declining. While there is a patchwork of efforts to address gaps in mortgage lending for those traditionally excluded from homeownership, what’s needed is a well-functioning and coordinated lending market for those who do not have the kind of wealth or institutional resources to purchase homes using cash.

Recently, the Department of Housing and Urban Development (HUD) issued a request for information on existing barriers to small dollar FHA loans (read the response submitted by CSEM and New America). With sustained attention on this issue, we can better understand and address the declines in FHA lending, including why banks are withdrawing from the overall and small dollar FHA market.

Endnotes

[1] Home Mortgage Disclosure Act (HMDA) is a publicly available data source on mortgage activity across the U.S. We use HMDA data on mortgage loan originations, where loan applications were for the purpose of buying a home as a primary residence.

[2] We used Legal Entity Identifier (LEI) codes–a unique identifier for entities involved in financial transactions–to identify lenders in the HMDA data. We then created a distinct list of lenders to designate the lender type. We identified distinct name characteristics to establish the lender type, and when no helpful name characteristics existed, we Googled the entity for more information. The name characteristics used to identify banks included “Bank”, “Bankers”, “Savings and Loans”, or “Bank and Trust.” For mortgage companies, the entity could neither be a bank or a credit union, and the name had to include “Mortgage” or “Loan”.

This blog post is part of a joint partnership between the Future of Land and Housing Program at New America and The Center for the Study of Economic Mobility (CSEM) at Winston-Salem State University investigating access to affordable homeownership in North Carolina.

Data Analytics and Research Manager, Center for the Study of Economic Mobility

Deputy Director, Future of Land and Housing Program