Vanessa Rangel

Senior Program Associate, New America Chicago

The Earned Income Tax Credit (EITC) is the federal government’s largest benefit for workers who have low to moderate income and has been proven to be an effective anti-poverty program. It is estimated about 25 million eligible workers and families received about $60 billion in EITC benefits nationwide as of December 2021, and the average amount of EITC received was about $2,411.[1] Families and individuals who qualify for EITC tend to be those who are living paycheck to paycheck and benefit greatly from the credit. Almost three-quarters of its benefits go to families with annual incomes below $25,000,[2] so it is targeted enough to impact the low- to moderate-income families it aims to assist.

As of June 2022, 31 states plus the District of Columbia and Puerto Rico have enacted their own version of the federal EITC.[3] Missouri and Washington passed legislation in 2022 to establish their own version of the credit starting in tax year 2023. States typically utilize federal EITC eligibility rules to determine if one qualifies and are given a percentage of their federal credit (except Minnesota and eventually Washington where the credit is structured as a percentage of income).

In Illinois, those who qualify for the federal EITC will generally qualify for Illinois’ Earned Income Tax Credit (EIC) and receive 18 percent of their federal credit.[4] Starting tax year 2023, Illinois’ EIC will increase to 20 percent and eligibility has been expanded to childless workers aged 18 to 24 and 65 and older, as well as immigrants who file taxes using an ITIN number.[5] Like many other states, Illinois’ EIC is a refundable tax credit, meaning that the credit can not only reduce the dollar amount people may be liable to pay back in taxes but can also result in a refund if the credit is greater than the total amount they owe. Thus, Illinois’ EIC can be an important tool to combat poverty in conjunction with the federal credit and make the tax system more equitable for low-income Illinoisans.

Unfortunately, not everyone in the United States or Illinois claims the dollars they should receive. According to IRS data, approximately 22 percent of all eligible taxpayers did not claim the federal credit in tax year 2018.[6] Similarly, Illinois’ participation rate for eligible taxpayers in Tax Year (TY) 2018 landed at 78.4 percent.[7] Furthermore, the number of people in Illinois receiving the EITC dropped each year between 2017 and 2020, going from 932,000 to 883,000.[8] There are many reasons why someone may fail to claim the credit federally or through the state, and there is much work to be done to narrow the gap in participation.

The State of Illinois recognized this issue and decided to try a different, more proactive approach that greatly simplified the process for taxpayers. In 2019, following outreach by nonprofit advocates, the Pritzker administration and the Illinois Department of Revenue (IDOR) began conversations around a pilot that could help reimagine how tax credits are administered to better reach the people they are meant to serve. Using IRS data, they decided on a new outreach initiative for Illinois residents who claimed the federal EITC but did not file an Illinois income tax return and likely qualify for the state credit. Instead of waiting for taxpayers to realize the government owed them money, the department created a simple, safe process that allows individuals to claim their missing tax credit quickly.

The pilot has been successful in assisting over 22,000 Illinoisans to file their state tax refunds by streamlining an often cumbersome and intimidating tax system. With the expiration of the Child Tax Credit’s (CTC) one year expansion in January 2022, efforts to make tax filing and tax credits accessible are even more pressing so that the federal EITC and state EIC can reach those who need the additional financial support following the pandemic. This policy brief will examine how the pilot has been conducted over the last few tax seasons as well as key takeaways and policy recommendations to inform other states, legislators, public service administrators and others who may want to pursue similar policy options.

In 2019, the staff at the IDOR began exploring several ideas for how to reach a larger group of individuals who were eligible for the EIC after the Governor’s Office expressed interest in the issue based on recommendations from nonprofit advocates. The goal was to ensure that more individuals who were eligible for the state EIC were able to claim the credit more easily. This goal became even more important at the beginning of the pandemic in 2020 when millions of people had been laid off or furloughed and struggled to pay basic expenses.

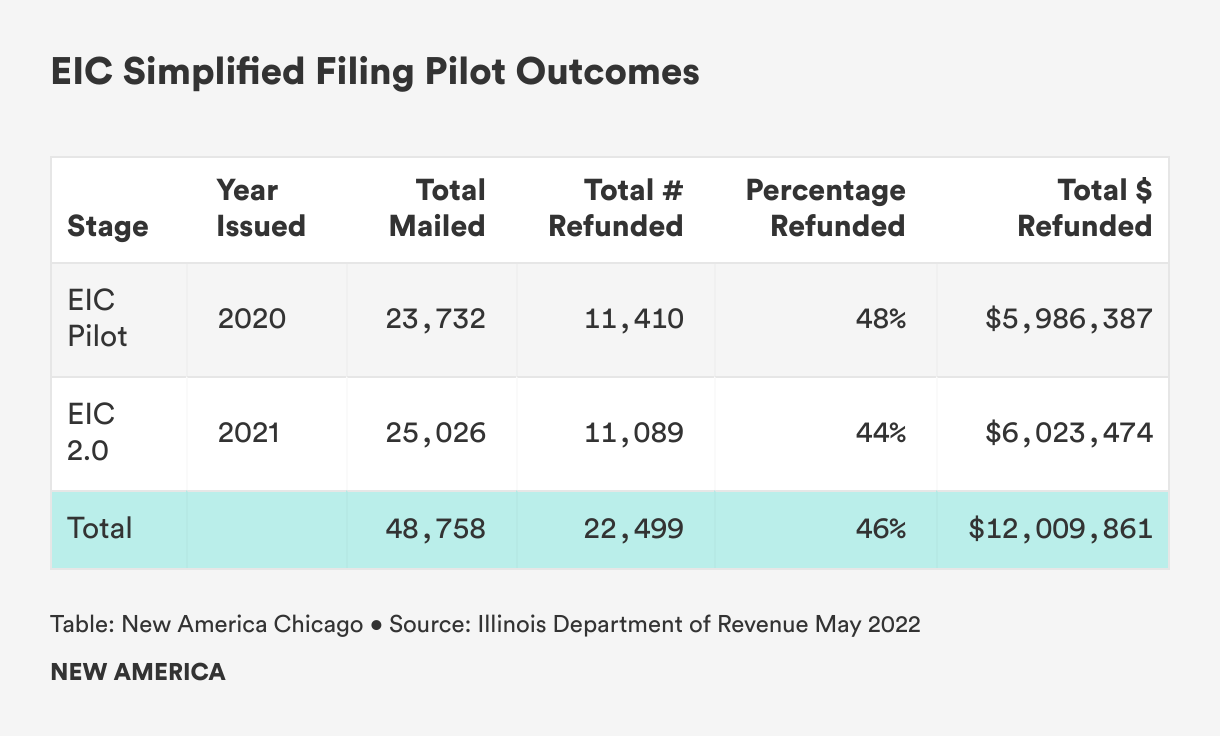

After exploring several ideas, the department ultimately decided to pursue a populated return based on their internal capabilities and the data available to them from the IRS. They rolled out the pilot in October 2020 with 23,732 letters sent out to Illinois residents and another 25,026 letters sent out in 2021. The response to the pilot has been excellent and in 2021 the department integrated the process into their annual workflow.

Target Population

Most efforts to increase uptake of the EITC focus on access to much needed cash for lower income individuals and families. Broadly speaking, as of 2021 individuals who earn under $57,414 per year were eligible for both the federal EITC and Illinois EIC, with people at the lower end of the income spectrum less likely to claim the money as they earn less than the federal income requirement to file or face other systemic barriers.[9] Additionally, the EITC has historically focused on helping people with minor children. For example, in 2020 parents of children were eligible for a much larger refund check (maximum federal EITC of $6,600) than adults without dependents who could claim a maximum of $538.

For this pilot, IDOR identified several different groups of individuals who currently do not receive the state EIC, but may be eligible. These groups included people who claimed the EITC on their federal returns but did not claim it on the state level, as well as others who did not file taxes altogether but may still be eligible for the EITC based on their income. Ultimately due to restrictions on available income data and fraud concerns, IDOR decided to pursue the pilot with those who had claimed their federal EITC but had not filed taxes on the state level at all. These individuals were chosen because they are the easiest to identify, and IDOR already had access to all of the income data and other details needed to generate a return. In addition, already having a federal EITC amount on hand made it easier to calculate the percentage for Illinois’ EIC and generate a state return.

Rolling out the Pilot

In order to increase access to the state EIC for people who were eligible but had not yet claimed it, IDOR sent out a letter and pre-populated form with information already submitted to the IRS by tax filers. Because individual tax filers technically have three years to file taxes without penalty if they do not owe money, the department started with tax year 2018 and included subsequent tax years in the following rounds of the pilot.

The notice sent out to Illinois residents consisted of two letters: 1. a Notice of Unclaimed Earned Income Credit (ITR-61-EIC) that informs the recipient they may be eligible to receive a tax refund due to an unclaimed Illinois EIC, as well as information on when and how to respond; and 2. The Examiner’s Report (EDA-131) which details the existing information from the federal tax return and allows recipients to check for accuracy.[10] If the recipient feels that the information on the report is accurate and wants to claim the proposed refund, they sign the letter and return it to IDOR for processing. To make the process even more convenient for taxpayers, the team allowed for responses online rather than just mailing the return. Respondents can take a picture of their signed return with their phone and email the photo back to IDOR. IDOR staff credits this functionality with increasing the pilot’s uptake rate because it was simple and accessible to participate.

Key Challenges

With any new initiative, there are hurdles and unforeseen challenges that occur. Here are some key challenges that IDOR staff had to overcome in order to keep the pilot on track. Sharing these problems will hopefully help other implementing agencies prevent unnecessary setbacks.

Integrating the Pilot into Department Workflow

Because of the pilot’s successful first year, IDOR decided to streamline the mailing process year over year and integrate the outreach letters into their annual workflow. The newness of the pilot and additional work posed processing challenges for the Federal State Exchange Unit (FSEU) team, a small unit that works on tax enforcement efforts. The large influx of state returns was very labor intensive, so the team sought to find new ways to complete each year’s returns in addition to their normal workload.

In the second round of the pilot or EIC 2.0, IDOR staff was able to better integrate the process into their existing workflow by issuing a portion of the letters each month rather than one bulk mailing and automated some of the processes. The monthly mailings have eliminated the need for an annual retraining on the mailing process and eased the volume of letters being sent out through their mailroom. A total of 25,026 letters were sent out for this round of the pilot as of April 2022.

One complication in the mailing process is the length of time it takes to do accurately and well. A thorough and iterative approach is necessary to capture as many eligible participants as possible. Each time staff prepares for a mailing, they utilize the most recent IRS data available to include those who file late or an amended return. They send out notices for each tax year until the statute of limitations runs out. As a result, each round of mailing takes a year and a half to send letters to all eligible Illinoisans.

Pilot Outcomes

The pilot demonstrated impressive numbers during its first year of implementation. The first round of the pilot began with one bulk mailing sent out in October 2020. The second round of mailings which occurred in 2021. By April 2022 the department had fully completed two rounds of mailings for a total of 48,758 letters and planned a third round to start in May 2022, which will include tax years 2019 and 2020.

With a response rate of 48 percent, the department gave refunds to nearly half of its intended recipients by the end of the pilot’s first year. In the second year of the project, IDOR was able to issue refunds to 44 percent of recipients. This is considerably higher than past pilots in the early 2000’s in New York[11] and California[12]. However, this may be due to the fact that this pilot focused on people who had already claimed the federal EITC.

In total over two years, the pilot issued refunds of over $12 million to low and middle-income Illinoisans, with slightly fewer refunds the second year but a higher dollar amount. Nearly all of the refunds went out to individuals or couples earning less than $44,885 per year.

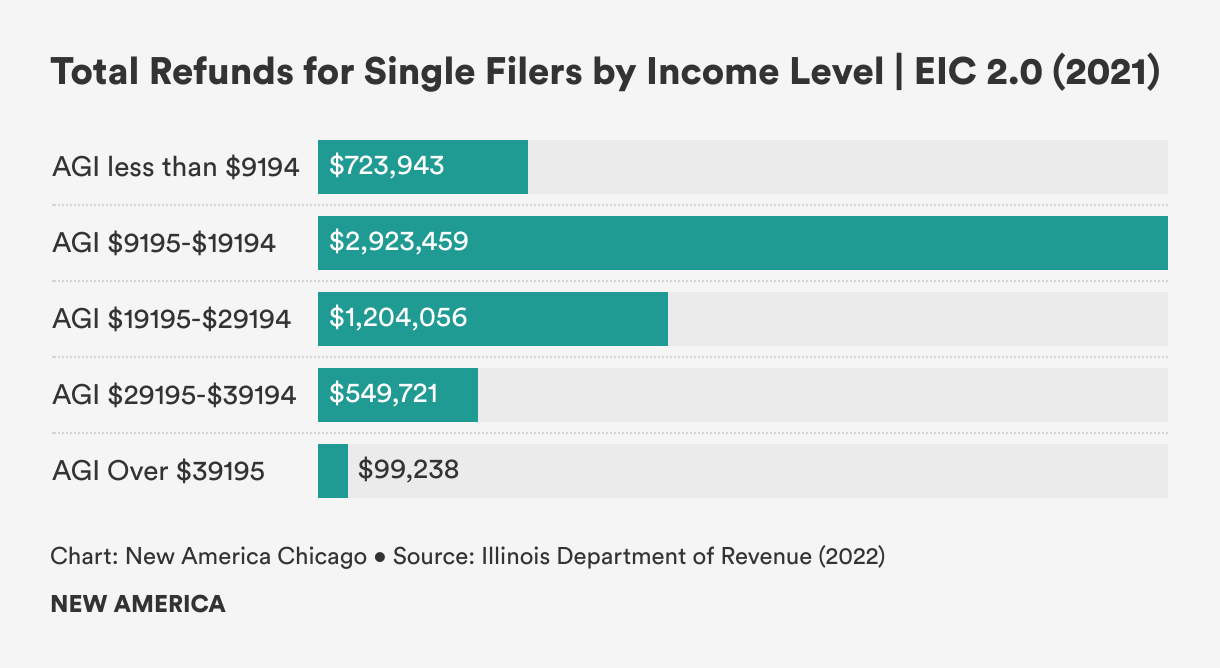

The pilot was particularly successful at reaching one of the groups least likely to claim their EITC, low-income, single filers.[13] Just over 80 percent of dollars issued the first year and second year went to single filers earning less than $29,194 a year. In the second year of the pilot this totaled $4.85 million and just over 9,000 refunds for struggling Illinoisans, a similar pattern to the first year.

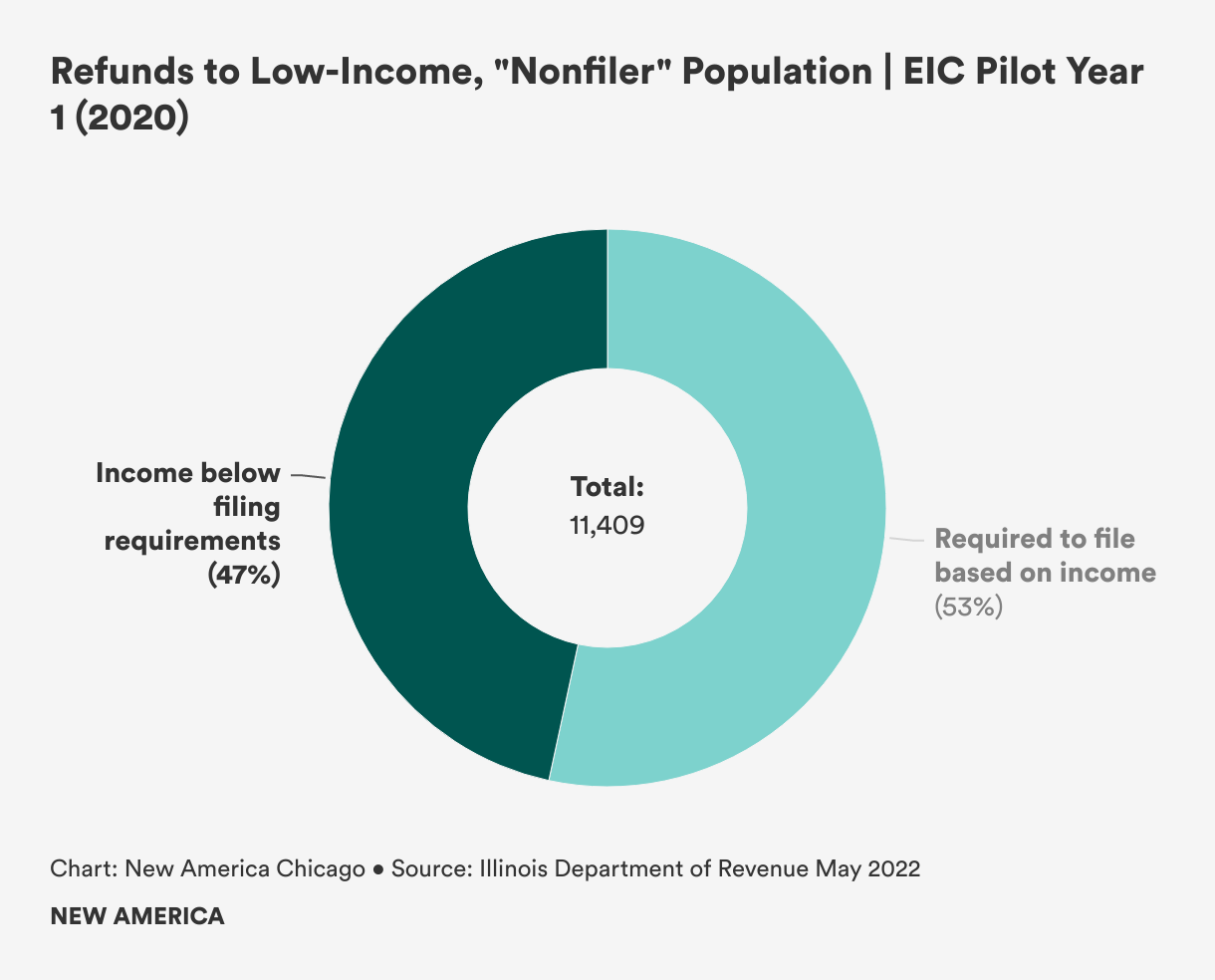

The numbers are good but not as striking for individuals who do not need to file taxes because their income is too low, generally referred to as non-filers. Those under 65 years old filing as single do not need to file federal taxes if their income is under $12,550 per year or under $25,100 for those filing jointly. For the first year of the pilot, around one third ($1.96 million) of the total dollars were distributed to people who normally earn too little to file taxes, with most being single filers. Nearly half (47 percent) of all first year refunds went out to people traditionally considered nonfilers.

Around two-thirds of the money ($4 million) went to individuals who are normally required to file because of their income level. However, digging into those numbers shows the pilot was especially successful at reaching single filers who earn over the filing threshold but are still low-income. Nearly 54 percent of the total dollars ($3.2 million) that year went out to single filers earning more than $12,550 but less than $29,194 per year. This level of data was not available for the second year, but a similar pattern is suggested.

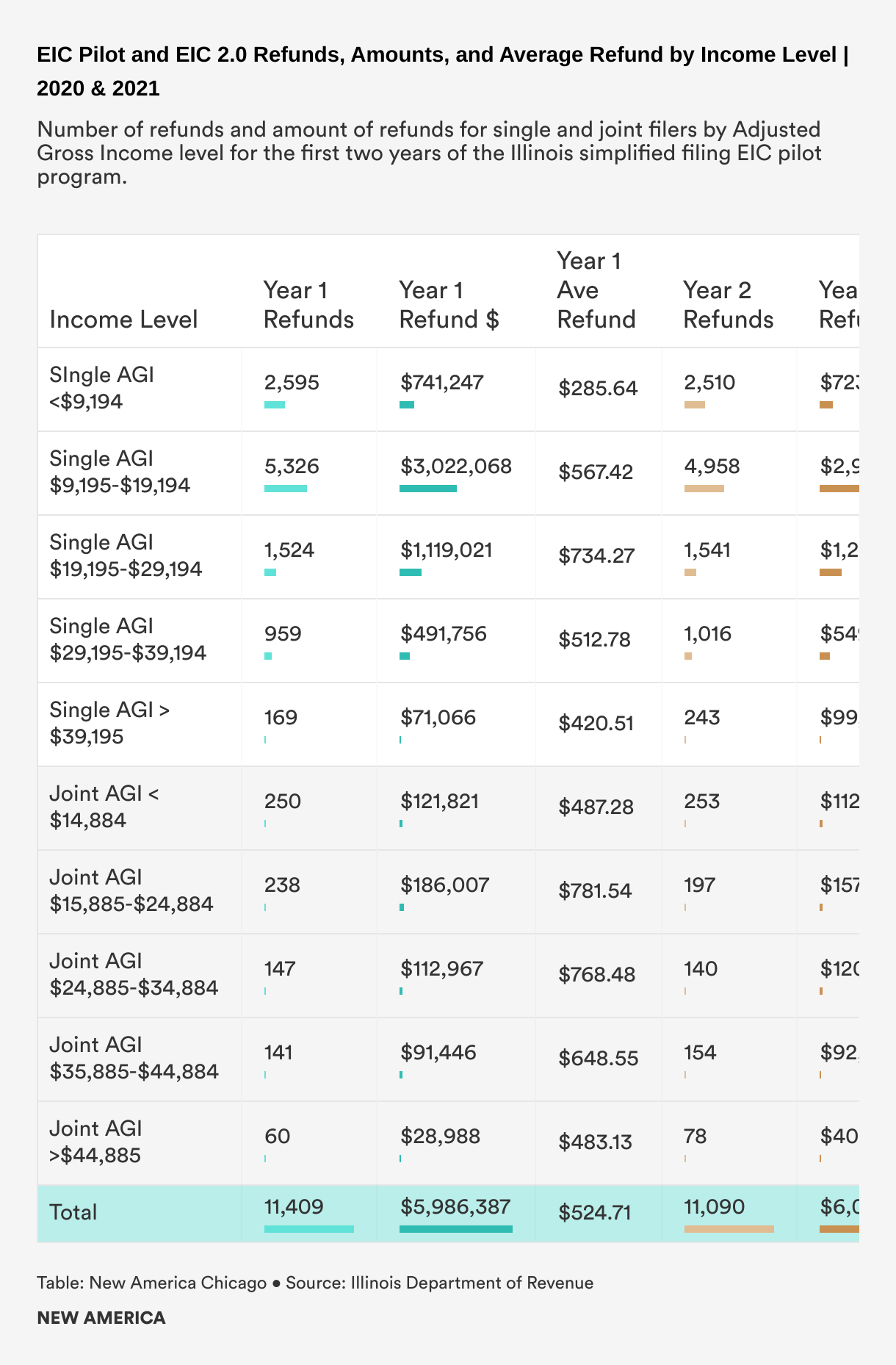

For more detailed information on the number of refunds issued by income level for each round of the pilot, see Appendix A.

A collaborative design process, a clear vision and support from the top, and department-wide commitment were all essential to the success of the pilot. Several different departments had to work closely together to ensure the process was coordinated and protected against potential fraud. Because the teams believed in the goals and approach of the pilot, they were able to work together efficiently to establish the workflows needed to succeed and discover solutions to new problems.

The team had to be thoughtful about how to conduct each aspect of the pilot and needed a centralized force to keep the project running smoothly across departments. One of the most important success factors was the presence of a strong project manager who worked closely with IDOR’s Chief-of-Staff and oversaw the collaboration of each team. The project manager worked to ensure good communication and a safe space for questions, concerns, progress reporting, and recognition of team investments.

The project manager also instituted an iterative, team-oriented framework that was unique from other IDOR projects. The teams met bi-weekly, with the project manager meeting with specific teams on alternating weeks, including those who could make policy decisions and those involved with programming and testing. Decisions, questions, and concerns were documented, and notes were issued after each meeting. The bi-weekly format allowed for timely analysis and elevation of decision points. Developers would elevate questions that were answered by policymakers the next week; this in turn provided clear direction to the developers allowing for focused work. Having a diverse group of staff working closely together led to solutions to challenges coming from unexpected staff members. Members of the team also noted that one unexpected benefit of rolling out the pilot during the pandemic was that experts from different departments were able to meet regularly via video call and decisions were made collectively during meetings, keeping the project moving along quickly.

Lastly, because of misconceptions and mistrust the public has surrounding the tax return process IDOR made it a priority to promote the pilot publicly in order to help legitimize the program and improve the participation rate. They created a webpage on the IDOR website that included details about the pilot. They also issued a press release and communicated this program through their social media accounts and to their email subscribers to spread the word. People tend to have a lot of fear associated with the tax filing process and institutions involved, so these steps were vital to making a pilot like this a success.

Thanks to this pilot program, thousands of low- to middle-income Illinoisans received much needed cash during a difficult economic time. The pilot was remarkably successful. However, many more low-income Illinoisans could benefit from this poverty-fighting policy. By expanding the pilot to more complex use cases in phases, the State of Illinois could build upon the success of this pilot to provide simplified access to tax credits for struggling families in Illinois. In addition, implementation would help low-income individuals who would not otherwise benefit from the 2022 expansion to the state EIC to access the EIC. These recommendations are also relevant to other states and mirror recommendations from our New America colleagues on steps federal policymakers can take to improve access to the federal EITC.

For all of these recommendations, additional funding would be essential to ensure the departments involved have sufficient staff to enact these changes well.

EIC 4.1: Improve Access for Low-Income Non-Filers

EIC 4.2: Reduce Costly Barriers to Access

EIC 5.0 Simplified Access for Newly Struggling Families

EIC 6.0 Simplified Support for Simple Cases

Illinois’ pilot to make the state Earned Income Tax Credit more accessible was incredibly successful and demonstrates the potential for a simpler approach to taxes that makes government work better for the public. The pilot expanded access to the state credit for lower income, single adults, one of the groups most unlikely to claim their EITC. This provides proof that a simpler way of providing this poverty-fighting tax credit to more low-income people is possible both at the federal and state levels. As states look to provide more financial stability for struggling communities, this could be a game changer. Illinois can and should begin a staggered effort to expand this pilot to the many struggling individuals who do not currently file federal taxes in order to reach additional populations that could benefit from the much needed cash assistance.

Thank you to all of the staff at the Illinois Department of Revenue for implementing this important pilot. To those who took the time out of their very busy schedules for interviews, it was a pleasure learning from each of you and we could not have written this brief without your valuable input: Whitney Elders, Jason Poling, Jim Nicholson, Brian Fliflet, Roger Koss, Maura Kowracki, Terry Horstman, and Kelly Frantz.

Thank you also to our funders The Chicago Community Trust and the Steans Family Foundation.

[1] “Statistics for Tax Returns with the Earned Income Tax Credit (EITC),” IRS website, last modified Mar 10, 2022, https://www.eitc.irs.gov/eitc-central/statistics-for-tax-returns-with-eitc/statistics-for-tax-returns-with-the-earned-income

[2] Hilary Hoynes and Jesse Rothstein. “Tax Policy Toward Low-Income Families,” NBER Working Paper No. 22080. (March 2016): https://www.nber.org/papers/w22080

[3] “States Can Adopt or Expand Earned Income Tax Credits to Build Equitable, Inclusive Communities and Economies,” CBPP website, last modified Mar 24, 2022, https://www.cbpp.org/research/state-budget-and-tax/states-can-adopt-or-expand-earned-income-tax-credits-to-build

[4] “Illinois Earned Income Tax Credit (EITC) and Earned Income Credit (EIC),” IDOR website, accessed June 2022, https://www2.illinois.gov/rev/programs/EIC/Pages/default.aspx

[5] Bill Status of SB0157, ILGA website, accessed June 2022, https://ilga.gov/legislation/billstatus.asp?DocNum=0157&GAID=16&GA=102&DocTypeID=SB&LegID=129172&SessionID=110&SpecSess=

[6] “EITC Participation Rate by States Tax Years 2011 through 2018”, IRS website, last modified December 6, 2021, https://www.eitc.irs.gov/eitc-central/participation-rate/eitc-participation-rate-by-states

[7] “EITC Participation Rate by States Tax Years 2011 through 2018”, IRS website, last modified December 6, 2021, https://www.eitc.irs.gov/eitc-central/participation-rate/eitc-participation-rate-by-states

[8] “Statistics for Tax Returns with the Earned Income Tax Credit (EITC),” IRS website, last modified Mar 10, 2022, https://www.eitc.irs.gov/eitc-central/statistics-for-tax-returns-with-eitc/statistics-for-tax-returns-with-the-earned-income#Previous%20Tax%20Years

[9] “The IRS as a Benefits Administrator,” New America, last modified March 24, 2021; Joseph V. Hotz and John Karl Scholz, “The Earned Income Tax Credit,” NBER Working Paper no. w8078, (January 2001); Nada Eissa and Hilary Hoynes, “Behavioral Responses to Taxes: Lessons from the EITC and Labor Supply,” NBER Working Paper no. w11729, (November 2005); Janet Currie, “The Take-up of Social Benefits,” in Alan Auerbach, David Card, and John Quigley (eds). Poverty, the Distribution of Income, and Public Policy, (2006), John Iselin, Taylor Mackay, and Matthew Unrath, “Measuring Take-up of the California EITC with State Administrative Data,” California Policy Lab, July 13, 2021

[10] IDOR website, accessed June 2022, https://www2.illinois.gov/rev/individuals/Pages/FSEU.aspx

[11] Testimony of Sam Miller, Assistant Commissioner of NYC Department of Finance, November 17, 2009, PDF: chrome-extension://efaidnbmnnnibpcajpcglclefindmkaj/http://clkrep.lacity.org/onlinedocs/2009/09-2750_misc_11-17-09.pdf

[12] “What was the experience with return-free filing in California?,” Tax Policy Center, last modified May 2020, https://www.taxpolicycenter.org/briefing-book/what-was-experience-return-free-filing-california

[13] Joseph V. Hotz and John Karl Scholz, “The Earned Income Tax Credit,” NBER Working Paper no. w8078, (January 2001); Janet Currie, “The Take-up of Social Benefits,” in Alan Auerbach, David Card, and John Quigley (eds). Poverty, the Distribution of Income, and Public Policy, (2006); John Iselin, Taylor Mackay, and Matthew Unrath, “Measuring Take-up of the California EITC with State Administrative Data,” California Policy Lab, July 13, 2021

Senior Program Associate, New America Chicago

Director, New America Chicago