Julia Craven

Senior Writer and Editor, Better Life Lab

As with all racist injustices facing the most vulnerable populations, it does not have to be this way.

Every year, more than 25 percent of Black children living in rental households receive an eviction filing, according to new data released in the fall of 2023. This makes Black children and their mothers the demographic most at risk of experiencing an eviction in the United States. Children under age 5 are at highest risk. Many of these children live in households where a Black woman’s name is the only one on the lease. Black women renters who have a child living in their home comprise 28.3 percent of the average annual rate for eviction filings, the highest of any race and gender group. Now that more precise data exists showing who is most likely to face the threat of eviction, this research scan explores the severe disruption that an eviction can cause to a family’s stability, which can lead to a cascade of adverse effects on a Black family’s health and well-being—such as low birth weights, an increased risk of common childhood diseases, poor cognitive development, and heightened food insecurity, along with broader socioeconomic implications. This overview also scans the policy landscape and real-world solutions, including creative uses of pandemic-related federal American Rescue Plan Act funds, to show comprehensive social, legal, and legislative reforms that ensure housing security and social equality for two of our nation’s most vulnerable demographics.

While 2.7 million households receive an eviction filing annually, when all the people living in those homes are accounted for, the number of individuals threatened with eviction jumps to 7.6 million, and the number of those evicted via court order jumps to 3.9 million—a breathtaking leap highlighting how many people are potentially crushed under the weight of America’s housing crisis.

The key word, however, is “households.” Before new data from Princeton University’s Eviction Lab was released this fall, only household figures were calculated since court filings for formal evictions only list the names of those on the lease. This resulted in an incomplete picture of who is most impacted by evictions in the U.S. Now, using data from the Census Bureau, the Eviction Lab has shown that the demographic most at risk of experiencing an eviction in the U.S. are children—specifically Black children and their mothers. The Eviction Lab worked with the Census Bureau to probabilistically link the names and addresses on eviction filings with respondents to the 2006-2015 American Community Survey. Using this information, the Lab took a remarkably uninformative document—the formal court filing—and crafted a more fully fleshed-out profile of who receives eviction filings.

More than half of households that receive an eviction filing have a child living within the home, and nearly 33 percent of the population threatened with a filing is under the age of 15. Further, more than 10 percent of children under the age of five live in rental households threatened with an eviction each year, and 5.7 percent are evicted. Black children are especially at risk: the study found that more than 25 percent of Black children live in rental households that receive an eviction filing. For Black children under the age of five, 12.4 percent experience an eviction every year.

“Over 50 percent of eviction filings in this country are against a Black family,” said Carl Gershenson, the director of the Eviction Lab and one of the co-authors of the report, in a sit-down interview with New America’s Better Life Lab and the Future of Land and Housing teams.

Black renters comprise 18.6 percent of America’s renter population, yet they make up 51.1 percent of those affected by an eviction filing and 43.4 percent of those evicted nationally. Within this demographic, Black women with children are the most vulnerable, comprising 28.3 percent of the average annual rate for eviction filings and 12 percent of those evicted via court order—the highest of any other group.

Contrary to common assumptions, yearly income doesn’t explain the vast difference in eviction risk for Black households and white households. The eviction risk for Black households earning more than $80,000 is still higher than it is for a white household earning under $20,000 a year. This disparity aligns with other disparate outcomes for Black Americans that do not improve as socioeconomic status rises—such as maternal mortality, debt burden, and experiencing police violence.

“We have in our data families earning over $100,000 a year—Black families—who are still evicted. That just does not happen in white neighborhoods,” said Gershenson. “That’s almost impossible to observe in a white neighborhood and happens with some regularity in Black neighborhoods.”

While income doesn’t offer an answer to this disparity, anti-Black racism certainly does. America’s eviction crisis and how it harms Black families is a direct result of centuries of racist policies that successfully undermined our communities.

Before Eviction Lab’s data was released, I reported on eviction diversion programs in my work at the Better Life Lab—mainly how they affect Black women's and children's health. When it comes to the myriad of health risks that uniquely affect Black folks, especially women and children, eviction falls under the radar because it is routinely viewed as a housing problem, even though access to adequate housing is a social determinant of health and well-being. Below is an overview of the stakes for Black mothers and children who suffer under the racist thumb of America’s eviction crisis, the health consequences of experiencing such a disruptive life event during childhood, and potential, non-exhaustive solutions based on widely available data and research.

This compilation reveals America’s eviction crisis as a public health emergency that must be addressed using a health equity lens.

Economic disenfranchisement. Unpaid rent is the cause of most eviction filings and court-ordered evictions. For Black moms, this creates a compounded financial burden: Not only are Black mothers more likely to be evicted, but 68 percent of them are their household’s sole or primary breadwinner. This earning obligation coincides with being on the short end of the racial wealth and pay gaps. Full-time working Black women earn 67 cents to the dollar as compared to their white, non-Hispanic male counterparts. This limits the amount of money available for rent and affects any chance of building longer-term financial safety nets—such as an emergency fund to weather job losses. According to the Urban Institute:

Black households have just 15 percent of the wealth of white households, and this has not changed much over time. For Black women, the gap is also stark. For instance, single Black women household heads with a college degree have 38 percent less wealth ($5,000) than single white women without one ($8,000). Among married women who are the head of the household, Black women with a bachelor’s degree have 79 percent less wealth ($45,000) than white women with no degree ($117,200) and 83 percent less wealth than those with one ($260,000). Marital status and education do not close the gap.

Racist policies. Racist policies historically target and disenfranchise Black families. An investigation by WNYC found that high eviction rate patterns follow the path of the Great Migration. “The great northern migration is a major way station on the road to today's eviction crisis—and the interrelated racial wealth gap,” said journalist Brooke Gladstone. “The net worth of the typical Black household is just 15 percent of the typical white one, and the gap is growing.”

As Black Americans fled the Jim Crow policies that dominated the South, rampant racism stayed tight on their trail. Nationwide, Black folks were barred by local officials from participating in President Franklin Delano Roosevelt’s New Deal programs. Agricultural and domestic workers couldn’t draw social security benefits, a guideline that disproportionately targeted Black Americans. The same officials lobbied to ensure these occupations were excluded from the codes of fair competition—a measure enacted under the 1933 National Industrial Recovery Act that fixed wages within industries—meaning Black Americans, by and large, did not receive the new minimum wages set under the New Deal. Other industries, such as restaurants, simply fired Black folks before paying them more. When the Federal Housing Administration was established in 1934 to boost homeownership, the agency wouldn’t insure mortgages for homes in or near Black communities—a policy known as redlining—which thwarted Black homeownership. Further, Black Americans were denied the educational opportunities and low-cost loans afforded to their white counterparts under the G.I. Bill.

This medley of racism prevented Black Americans from accessing one of the surest ways to build and maintain wealth: owning a home.

Racist policies specifically targeting Black women and children. American social systems have always preyed on Black mothers—particularly at the intersection of housing and other programs designed to provide socioeconomic relief. A prime example of this is “man-in-the-house” policies, which prevented mothers from receiving welfare if they were thought to be living with, or having an intimate relationship with, a single man capable of working for pay and supporting a family. (In a sick twist of American irony, the discriminations outlined in the previous section are what prevented many Black Americans from being able to support a family on a single, or even dual, household income.)

“Man-in-the-house” policies were a paternalistic way of framing social programming. The thinking was that married or otherwise coupled women shouldn’t work because men should earn enough money to support their families. So, since the underlying crux was that women shouldn’t work, qualifying single women would receive benefits so they could stay at home with their children. To enforce this rule, caseworkers would pop up at homes in the middle of the night, a practice that disproportionately targeted Black women. If a man was thought to be living in the house—a definition that fluctuated with each caseworker—the woman’s benefits were threatened. The caseworker would often deduce this based on something as ridiculous as a hat hanging in a closet or a pair of socks.

“Man-in-the-house” policies were struck down by the Supreme Court in 1968, but they set the stage for the punitive measures currently used to regulate housing. According to research from sociologist Rahim Kurwa, housing voucher regulations—like the prohibition of unauthorized residents—are an extension of this policy. According to the Department of Housing and Urban Development (HUD), misrepresenting family composition, which can entail having an “unauthorized resident” living in the home, is, at best, considered an omission by the resident and, at the most extreme, is considered abuse or fraud. Any distinction between intentional and unintentional misreporting of family composition is the responsibility of the relevant public housing agency. (Such a policy not only imposes on the personal lives of people living in public housing but also aligns the housing and criminal justice systems, argues Kurwa.)

Complaints about unauthorized residents can possibly lead to eviction via “immediate termination” from a voucher program. “The subjects of these complaints are often Black women,” writes Kurwa, “and the resulting evictions compound patterns of racial segregation.”

Health consequences. Evictions upend a family’s sense of stability and predictability—two factors necessary for children to thrive—and stable housing is critical to healthy childhood development. Disruptions due to eviction can lead to low birth weights, premature births, poor cognitive development, infant mortality, and heightened food insecurity. When we consider the Eviction Lab’s data that evictions disproportionately affect young Black children, a demographic that is already more likely to experience adverse health outcomes as infants and as they age into adults, the long-term health effects of eviction on Black Americans become more salient.

“Eviction often leads to residential instability, moving into poor quality housing, overcrowding, and homelessness, all of which [are] associated with negative health among adults and children," according to researchers at Boston University’s School of Public Health.

There’s a clear connection between adversity in childhood and increased risk for a range of adverse health consequences during adulthood. The first 1,000 days of a child’s life— from the time of conception to two years old—is a period of significant development for the brain, body, and immune system. Any stress or instability during this time can affect the baby and their future.

Maternal stress can lead to reduced brain activity in infants. Kids who are exposed to high levels of psychological stress, including “toxic stress,” have a higher risk of contracting common childhood diseases. When these children age into adulthood, they’re met with an increased chance of developing diabetes, heart disease, various cancers, depression, substance abuse disorders, and other mental health conditions—adverse health outcomes that Black people are more likely to experience anyway. Children who have been evicted are also hospitalized more during childhood than children who have never experienced an eviction.

The “vicious cycle” of poverty. Then, there’s the aftermath of an eviction. Families attempting to find their footing and secure housing post-eviction can lead to evicted tenants forgoing medical care, food, or climate-appropriate clothing, according to sociologists Rachel Kimbro and Matthew Desmond, the founder and principal investigator of the Eviction Lab. Mothers employed at the time of eviction are more likely to be laid off or fired due to juggling multiple stressors and, understandably, choosing to focus on securing housing instead of their daily work duties.

Being evicted is a driver of poverty and multiple circumstances that foster poor health.

Interactions with punitive social systems. An eviction can open the door for child protective services to remove children from their parents’ care, for instance, as well as potentially lead to harmful interactions with armed law enforcement. Across the country, various city marshals, sheriff’s offices, and other armed law enforcement officers handle removing people from their homes. It’s well-documented what public health risks exist for Black families when they interact with police forces, including, but not limited to:

Child care deserts. More than half of Americans live in a child care desert, which the Center for American Progress defines as “any census tract with more than 50 children under age five that contains either no child care providers or so few options that there are more than three times as many children as licensed child care slots.” Black women are more likely to live within a child care desert and have a tougher time accessing affordable options.

The exorbitant cost of child care. A January report from the Women’s Bureau of the Department of Labor found that child care costs between eight and 19.3 percent of the median family’s income per child—shares that are “untenable” for many families. For Black mothers, this compounds with the racial wealth and pay gaps, meaning it’s even less likely that they can afford to outsource child care, a reality that becomes more brutal when we consider that Black women are more likely to be their family’s breadwinner.

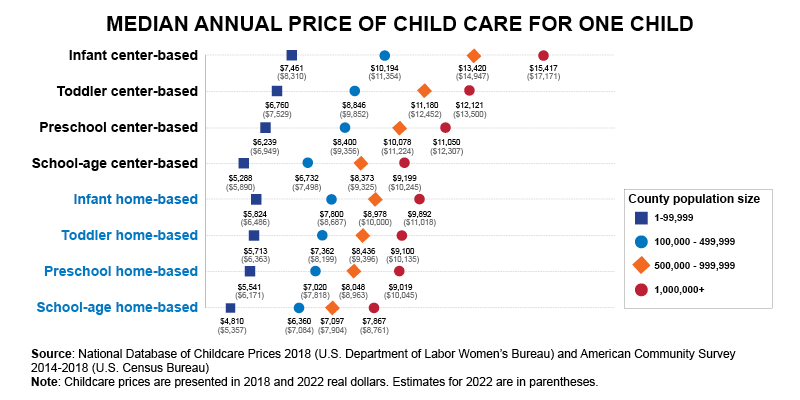

During New America’s sitdown with Gershenson, I noted that higher eviction rates for families with young children track with how expensive child care is for the same demographic. Though child care is costly for children of all ages, it is priciest for children between zero and five since younger children, particularly infants, need more care.

The prices in the graphic above, sourced from the Women’s Bureau report, are the cost for one child. When accessible and affordable child care isn’t available, finding and keeping employment is more challenging, which can lead to the cycle of poverty, instability, and stress persisting.

Diversion programs. Philadelphia’s Eviction Diversion Program (EDP) requires landlords to participate in a 30-day mediation with tenants who owe less than $3,000 in back rent before pursuing a formal eviction. It began as a city pilot initiative and was bolstered by federal COVID-19 relief funding into a national exemplar of eviction prevention, with 85 percent of cases reaching a settlement or an agreement to continue negotiations beyond the mandated 30 days. The program has been incredibly beneficial to Black women raising children in Philadelphia, where, according to city data, 74 percent of evictions involved a Black tenant, 70 percent involved a woman, and 50 percent involved a parent or caretaker.

Philly’s EDP program is bolstered by being coupled with rental assistance. Between May 2020 and January 2023, Philadelphia’s Emergency Rental Assistance Program distributed almost $300 million in federal, state, and local emergency COVID-19 relief funds to more than 46,500 households, according to city data.

This program was in former Philadelphia city council member Helen Gym’s mind for quite some time before she sat down to write the legislation. She never forgot how evictions influenced her experiences as a teacher decades prior. “I'd have fourth, fifth, and sixth graders who would be there one day and not be there the next,” Gym said in an interview with me this summer. “And it wasn't like I got a notice—I was often told by another 10-year-old in the class that the family had been evicted and that student would no longer be showing up in school.”

Robust rental assistance programs. During the pandemic, emergency rental assistance programs distributed $46 billion to keep more than 10 million renters housed. Most of these programs are now inactive due to a lack of funding, and evictions are back to pre-pandemic levels in many places across the country. The relationship between rental assistance and eviction diversion is critical—and Philadelphia’s coupling of the two is a prime example of how it changes the dynamics in landlord-tenant mediations. Bluntly, the possibility of a landlord getting back rent paid compels them to participate in the diversion program. Most importantly, it allows a tenant to stay housed.

“We still see a dramatic reduction in evictions even without rental assistance, but [the diversion program] works its best [with assistance],” Philadelphia Councilmember Jamie Gauthier told me. “We're able to get the best outcomes. We were able to resolve almost all mediations and disagreements between landlords and tenants when we [had] access to plentiful rental assistance.”

“During the pandemic, we were able to reduce evictions in Philadelphia through EDP by 75 percent—and [federal] funds were a huge, huge piece of that,” she added.

Rental assistance programs aren’t perfect and require an infusion of money and care to continue functioning. Some local housing agencies sent funds to the wrong parties, for instance, which resulted in some landlords not getting paid promptly or at all—a bureaucratic disaster that makes them less likely to be patient with tenants during the application phase for the funds. On a larger scale, states began to run out of money, which put millions of tenants' housing in limbo.

Immediate sealing of eviction records. According to the Center for American Progress, “Eviction records keep individuals and families locked in a cycle of poverty; force people to live in unsafe housing; and cause homelessness and a host of other collateral consequences.” The “Scarlet E,” as it’s called, can follow renters for years after an eviction case goes to court—even if the tenant won their case. Automatic sealing or expungement protections are active in 10 states and the District of Columbia as of fall 2023. Some jurisdictions seal records for all types of eviction records, while others will only lock records in particular circumstances. Arizona, for instance, will only seal eviction records in cases filed for back rent or noncompliance with a lease.

However, automatically sealing all eviction cases upon filing would protect the most vulnerable tenants by reducing their chances of experiencing housing instability in the future by preventing the “Scarlet E” from being attached to their records in the first place.

Universal right to counsel for all tenants facing eviction. Legal representation is only guaranteed for defendants in criminal cases, not civil cases like eviction proceedings. Only 1 percent of tenants have legal representation in an eviction case compared to 90 percent of landlords. (Often, the landlord’s attorney shows up in their place, allowing the landlord to avoid the stress of getting to and from court.)

Right-to-counsel laws have tangible benefits for those facing eviction. According to the National Low Income Housing Coalition, tenants with legal representation are more likely to stay in their homes, avoid the “Scarlet E” stigma, and receive extended time to vacate the property if the court rules against them.

Kansas City allocated funds from the American Rescue Plan to implement a right-to-counsel ordinance—a decision that slashed evictions by 86 percent—following a campaign launched by civil rights-oriented organizations, including KC Tenants, Stand Up KC, Missouri Workers Center, Heartland Center for Jobs and Freedom, and others. Kansas City is now allocating city funds to run the program because it’s been so successful. Only 16 other major cities, one county, and four states have these right-to-counsel laws.

In Washington, D.C., six nonprofits, 19 private law firms, and the D.C. Access to Justice Commission have been working together to offer free legal representation to tenants during eviction proceedings starting in November 2023. (In late 2023, The District of Columbia has yet to codify the right-to-counsel.)

Guaranteed income for low-income Americans. Unlike a universal basic income, guaranteed income takes an equitable approach by providing cash payments to people living in poverty or to those without reliable income. The goal of a guaranteed income is to create an “income floor” that prevents people from living in poverty and addresses historical and systemic barriers that cause economic hardship. According to Ms. Magazine, this measure could be critical to keeping Black families afloat:

By prioritizing Black women, guaranteed income has the potential to make a difference for those struggling the most, and alleviate some of the racialized disadvantages low-income people of color face. In 2021, when parents received monthly payments through the expanded child tax credit (CTC), child poverty decreased by around 30 percent, with the CTC reaching more than 61 million children.

But in January, after the six months of payments ended, low-income Black and Latino families were hit hard: The childhood poverty rate rose from 12 percent in December to 17 percent in January—and soared to over 23 percent for Latino children and 25 percent for Black children.

Guaranteed basic income could bode well for reducing evictions since such a program would enable people to better afford housing.

Universal care infrastructure. Building a universal care structure is one part of a broader network of care reforms that would aid in preventing children and their families from being evicted in the first place. This includes but isn’t limited to culturally-competent universal care for kids ages zero to five; universal summer school and afterschool programs; and universal paid family and medical leave.

The need is urgent, and the benefits are immense. The U.S. invests among the lowest amount in child care compared to its peer nations, which leaves families with a bill that is too high for most. The Women’s Bureau report found that child care costs in every county in the United States exceed the affordability threshold of seven percent of family median income. Infant care costs more than in-state college tuition in more than 25 states. Parents are paying as much or more than their rent or mortgage for this level of child care because it takes a lot of people to provide adequate child care. Depending on state regulations, one teacher can take care of as many as 30 kindergarteners. Still, teacher-student ratios are much lower for younger children, with one teacher only being able to care for four, five, or six infants or toddlers at a time. Despite the demands on their labor and the skill set required, many child care providers and teachers make poverty wages.

Although the federal government does provide states with funds to help very low-income families pay for child care, the program is woefully underfunded. Publicly funded child care subsidies must be retooled to reach the eight million children who qualify for them. Right now, the money only helps two million children, a mere 25 percent of qualifying kids.

An affordable, high-quality, universal child care infrastructure with a well-paid, well-trained care workforce is urgently needed for families with young children. The money to kick start this effort exists: for instance, many states and localities haven’t allocated or spent all of the $350 billion in federal funds from the American Rescue Plan—money that must be allocated by the end of 2024* and spent by 2026.

While this isn’t enough funding to build and sustain a universal care infrastructure, it is a starting point to show what’s possible.

The eviction crisis in America has far-reaching repercussions, especially for Black women and their families. The intersection of racist policy, eviction, and inadequate access to child care has helped craft a dire reality for the health and well-being of Black communities. Solutions to this problem exist, but they require both immediate and long-term attention. Programs like Philadelphia’s Eviction Diversion Program, universal right-to-counsel laws, guaranteed income, good jobs with living wages and reasonable hours, and family-supportive policies would significantly reduce the number of annual evictions and thwart the subsequent harmful effects. Building a robust and universal care infrastructure will also play a pivotal role in preventing many evictions from occurring in the first place. It's time for policymakers to reevaluate and realign their priorities, ensuring everyone, particularly the most marginalized, has access to safe, affordable, stable housing.

*A previous version of this post stated that ARPA funds needed to be allocated by the end of 2023. They must be obligated by December 31, 2024.

Senior Writer and Editor, Better Life Lab