Rachel Fishman

Director, Higher Education

Today, New America’s Education Policy Program released the fourth in a series of College Decisions Survey briefs that analyze new survey data about what prospective college students know about the college-going and financing process. Part IV: Understanding Student Loan Debt focuses on prospective and recently-enrolled college students’ perspectives on taking out and repaying student loans. It looks at estimates of the amount students plan to borrow, their monthly payments, and their repayment strategies.

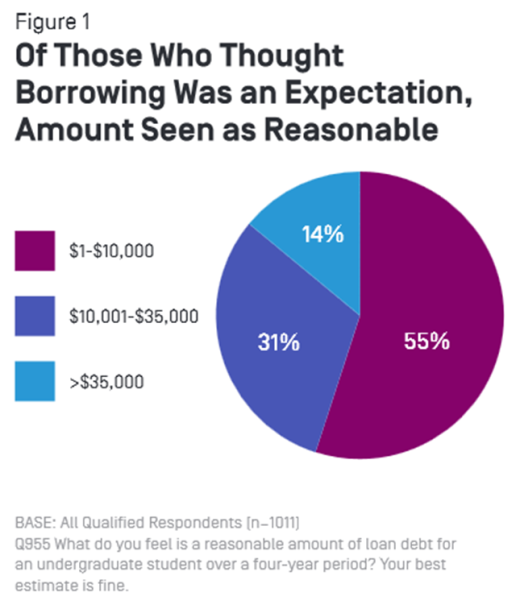

It’s well-known that graduating from college with debt has become a reality for the majority of American college students, but this study sought to better understand what amount students thought is reasonable to borrow for their undergraduate education. Most students (87 percent) thought that some debt was reasonable, but they varied widely on how much they think they should personally borrow for their undergraduate degree. Of those who thought borrowing for an undergraduate education was a reasonable expectation, 55 percent said the total amount borrowed should be $10,000 or less, and another 31 percent indicated borrowing should be kept to between $10,001 and $35,000. The median amount students deemed reasonable was $10,000 over four years of college.

However, when students intending to borrow were asked how much debt they actually expected to accumulate, the median amount jumped to $15,000 over four years. Some outlying students estimated they would borrow much more, pulling the average expected loan debt much higher to $25,295.

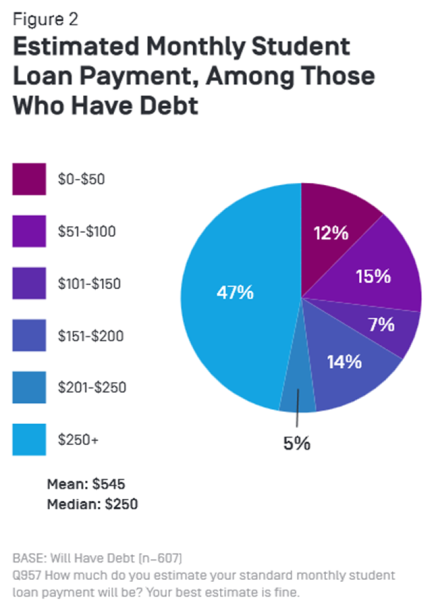

Prospective and recently-enrolled students also have a difficult time estimating their monthly student loan payment. Students who anticipate borrowing estimate that they will repay $545 per month, on average. Using the repayment estimator that the U.S. Department of Education Federal Student Aid office provides, the monthly payment on the estimated average debt of $25,295 at current interest rates would be approximately $260 on the ten-year standard repayment plan.

It's clear that prospective and recently-enrolled students struggle to understand exactly how student loan repayment is structured compared to how much they’re borrowing. Three possible policy changes could greatly improve student understanding of their debt and repayment options:

Read more about these recommendations here.

Director, Higher Education

Senior Policy Analyst, Center on Education & Labor