Tia Caldwell

Senior Policy Analyst, Higher Education

And lifelong debt for low-income borrowers

About a year ago, House Republicans unveiled the College Cost Reduction Act, a sweeping 220-page plan aimed at overhauling the country’s college financing. As Republicans prepare to take control of the presidency, House, and Senate, now is the time to take a closer look at the details of the ambitious bill. Among its many provisions—ranging from capping loans to scrapping consumer protections—the changes to student loan repayment stand out for contradicting conservative values. Republicans have long believed that well-off borrowers should repay their loans, while relief should be targeted to borrowers in need. Yet the College Cost Reduction Act (CCRA) would do exactly the opposite, lavishing subsidies on high-income borrowers while offering no relief to low-income borrowers.

Under the CCRA, borrowers would have just two repayment options: the current standard 10-year plan and a new “repayment assistance plan.” In a standard plan, borrowers make even monthly payments covering interest and principal for 10 years. The repayment assistance plan would set payments at 10 percent of a borrower’s income above 150 percent of the poverty line. This matches the monthly payment amounts required in the existing income-driven repayment plans PAYE and IBR. In contrast, the income-driven repayment plan SAVE, which was introduced by the Biden administration but may be rescinded during the Trump administration, requires borrowers to pay a lower percentage of their income.

The repayment assistance plan differs from all other income-driven repayment plans by not offering time-based forgiveness. To become debt-free using the repayment assistance plan, borrowers must repay the amount due or make payments that reach the dollar equivalent of total payments due under a 10-year standard plan. In comparison, all existing income-driven repayment plans forgive any remaining balance after 20 or 25 years of payments—or as few as 10 years for low-balance borrowers using the SAVE plan.

The repayment assistance plan includes subsidies to help borrowers pay down their debt if they do not reach the amount due in a 10-year standard plan. Like the SAVE plan, the repayment assistance plan waives interest if the borrower's monthly payment is too low to cover the interest payment. For borrowers whose payments are above $0, another subsidy ensures that the loan principal is reduced by at least half of each payment.

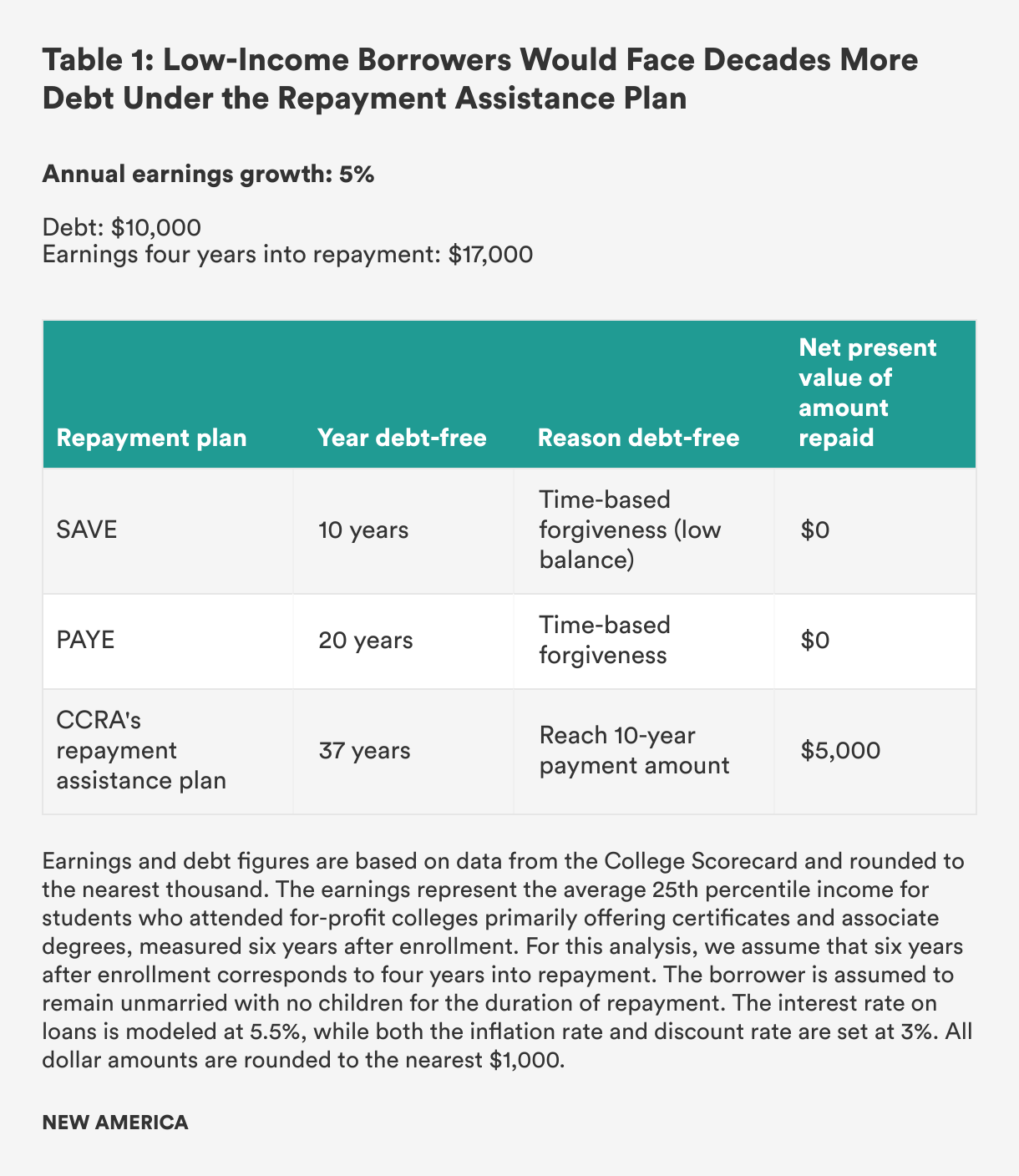

While the CCRA’s repayment assistance plan may sound generous, the lack of time-based forgiveness is a huge blow to low-income borrowers. Take, for example, a student who enrolls in a for-profit university that offers mainly certificates and associate degrees. A typical borrower at this type of college would take out appropriately $10,000 in student loans and earn around $34,000 six years after enrolling. But many fare worse; a quarter earn less than $17,000 six years after starting college. Table 1 shows the projected repayment outcomes of a borrower with 25th percentile earnings and median debt under the repayment assistance plan. For comparison, the table also shows outcomes under the PAYE plan, which often requires the same monthly payments as the repayment assistance plan, and the SAVE plan.

Under both SAVE and PAYE, this borrower’s income is too low to repay anything before reaching time-based forgiveness. Forgiveness occurs after 20 years under PAYE and after 10 years under SAVE because of the borrower’s low balance. Since the CCRA’s repayment assistance plan does not offer time-based forgiveness, a borrower in that plan would still owe their full balance at year 20. By year 22, the borrower’s income would outflank poverty by enough to enable small payments. After another 15 years, those payments would finally add up to the total due in a 10-year plan, triggering forgiveness. In total, this struggling borrower would hold debt for 37 years under the CCRA plan.

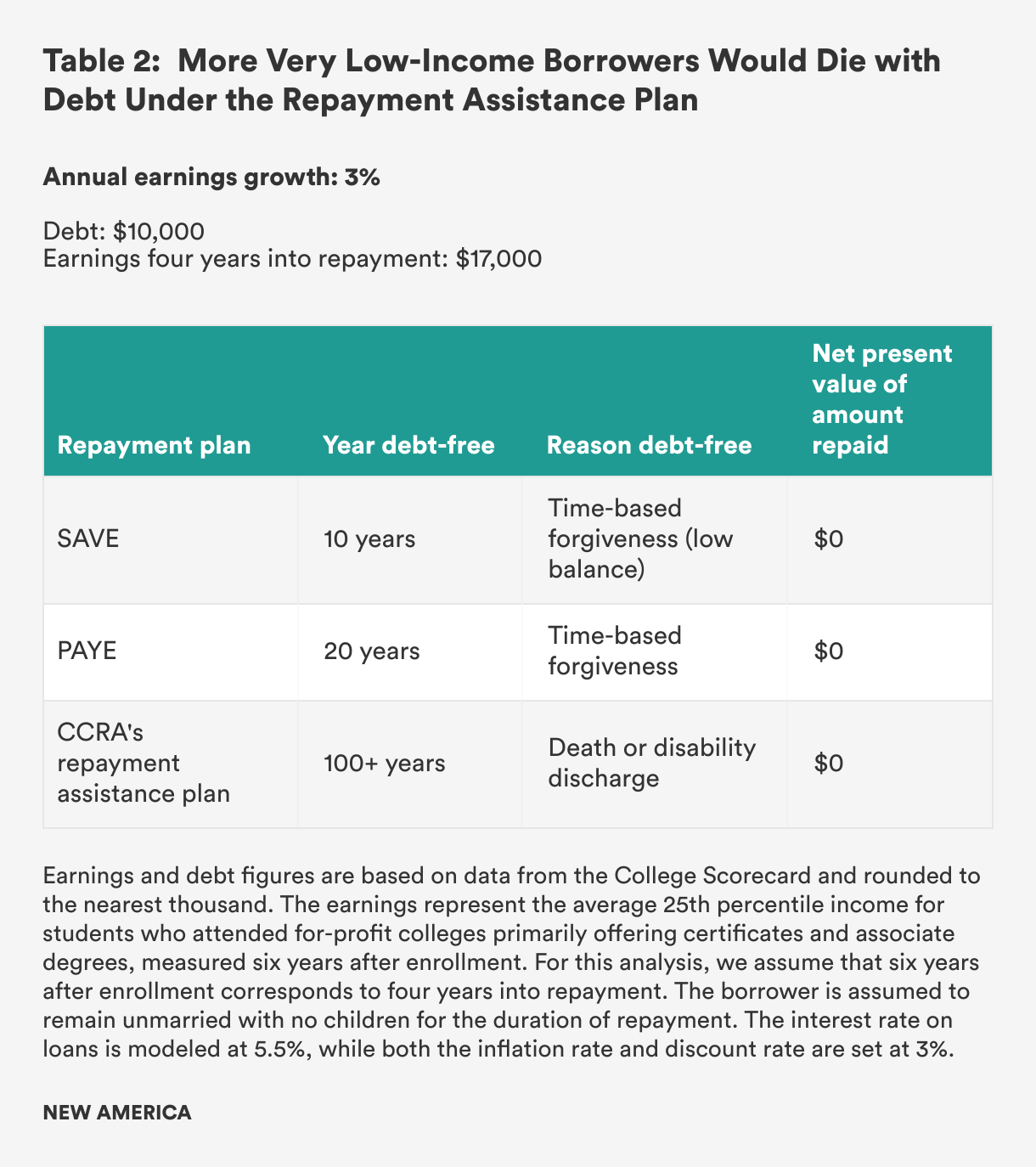

Now imagine that our unlucky borrower’s income grows at the same rate as inflation, rather than faster than inflation (Table 2). Their income would never exceed 150 percent of the poverty line, so their monthly payments would always be $0. Therefore, under the repayment assistance plan, they would never receive a principal subsidy and never accrue any credit towards eventual forgiveness. For this borrower, debt relief would come only through a work-ending disability or death.

Because the repayment assistance plan does not offer time-based forgiveness, it condemns many borrowers who experience the worst luck, like poor health or an industry downturn, to a lifetime of debt. Even the bill’s authors do not seem to want this. The official fact sheet on the CCRA claims—inaccurately—that the bill “provides repayment assistance to struggling borrowers to ensure they always see progress towards paying off their loans.” Reinstituting time-based forgiveness would bring the bill's impact closer in line with its stated intent.

Tying forgiveness to the 10-year standard plan amount, rather than a fixed length of time, has another unfortunate and perhaps unintended consequence: it disproportionately subsidizes high-income, high-balance borrowers. To see why, consider that the repayment assistance plan would let borrowers make lower payments, which stretches the repayment term beyond 10 years. Longer repayment periods cost the government: payments made further in the future are worth less due to inflation, and the government cannot use or invest those funds in the meantime. By forgiving loans once borrowers repay the nominal 10-year repayment amount—regardless of the accumulated interest—the government is handing out subsidies, particularly to those borrowers with larger balances.

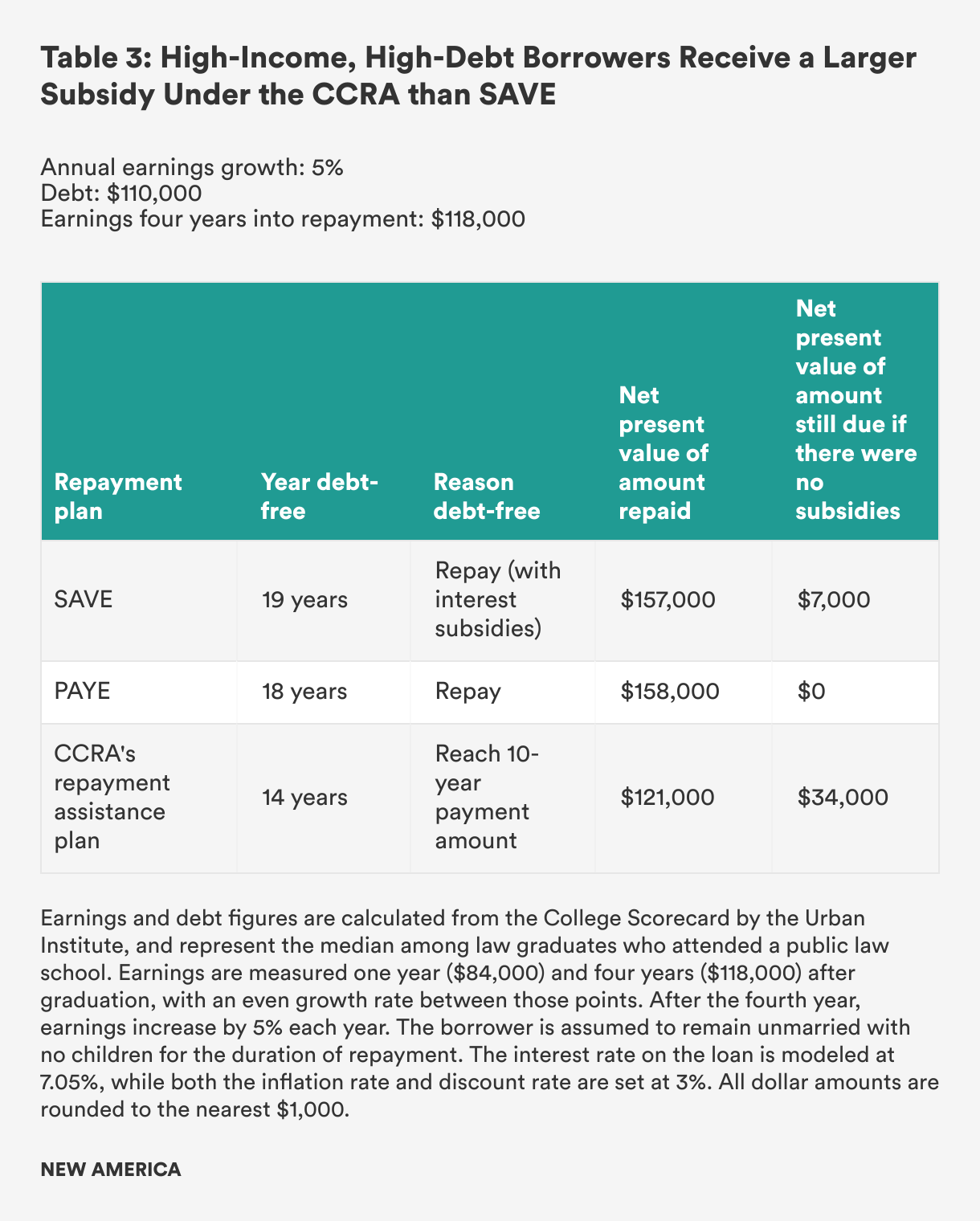

Consider a typical law graduate from a public university, whose repayment trajectory was first modeled by the Urban Institute. This borrower takes on about $110,000 in student loans and, four years after graduation, earns approximately $118,000. Under the SAVE plan, the borrower would benefit from modest interest subsidies in the early repayment years and go on to pay off the loan in just under 20 years (see Table 3). The PAYE plan, which requires higher monthly payments but has no interest subsidy, enables the borrower to fully repay the debt in 18 years.

The proposed repayment assistance plan is far more generous than either other plan. By year 14, the borrower would pay the equivalent of the 10-year payment amount (in nominal terms) and receive forgiveness. This forgiveness would be financially significant for the borrower and the government. Without the subsidies and early forgiveness in the proposed repayment assistance plan, the borrower would still owe over $30,000 at year 14.

Under the proposed repayment assistance plan, a typical lawyer trained at a public university would pay $36,000 less than they would under SAVE—an outcome that is at odds with the Republican vision for repayment reform. When Republicans called for ending SAVE, they criticized the “arbitrary subsidies that will […] support well-off doctors and lawyers.” Yet, despite their own warnings about runaway graduate debt and SAVE’s generous repayment terms, they introduced a plan that helps those borrowers more than SAVE, exacerbating those very problems.

If Republicans are looking to stand by their conservative values, other recent proposals will serve them better. In June 2023, a group of Republican Senators led by Senator Bill Cassidy introduced the Lowering Education Costs and Debt Act. These Senators proposed an income-driven repayment plan with time-based relief after as little as 10 years for borrowers with low balances. This approach would ensure graduate borrowers pay their fair share and is aligned with the standard private sector practice of writing off uncollectible debt.

In contrast, the CCRA would trap low-income borrowers in lifelong debt while delivering the largest subsidies to affluent graduate borrowers of any income-driven repayment plan in history. Given this, any policymaker interested in fairness for taxpayers and students may want to take a closer look at the CCRA’s details.

Senior Policy Analyst, Higher Education