Oversold?

In Kansas Governor Kathleen Sebelius’s Democratic response to President Bushs final State of the Union Speech Monday night, she touted a new law to reduce the costs of college loans as one of the major accomplishments of the new Democratic Majority in Congress. She was referring to enactment of the College Cost Reduction and Access Act of 2007, which among other things reduces interest rates on federally subsidized student loans. It was a big pat on the back for Congressional Democrats, who made cutting student loan interest rates in half a central part of their 2006 campaign. But Democrats should be careful not to oversell their achievement, as very few borrowers will get the full interest rate cut promised.

To be fair, under the new law, borrowers will also benefit from increased loan forgiveness for work in public service, substantially increased Pell Grant aid, and a decreased financial aid penalty associated with student work and savings. Indeed, the new law represents a significant increase in federal student aid. Higher Ed Watch has lauded it in the past.

The Fine Print

But when it comes to the much ballyhooed student loan interest rate reduction, take a look at the fine print. The College Cost Reduction and Access Act of 2007, signed into law on Sept. 27, 2007, does cut student loan interest rates in half. But it slowly phases in those cuts on new student loans only, achieving the promised 50 percent cut by the 2011-12 school year. After that date, interest rates on new loans revert back to the current fixed 6.8 percent interest rate. The cliff-like, expiration of budget policies is usually done to comply with (or avoid) budget rules, such as the fast-track procedure in Congress called reconciliation. That is the case with the interest rate cut, and it is also the reason why the 2001 and 2003 Bush tax cuts expire.

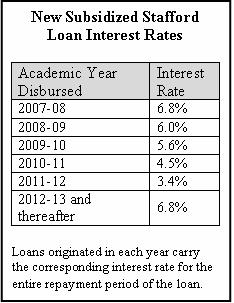

The College Cost Reduction and Access Acts student loan interest rate reductions will take place in increments as outlined in the table below. Loans disbursed in each year shown will carry the reduced interest rate for the life of the loan. A freshman entering college in the fall of 2008 will have four sets of loans at four different interest rates. And no borrower will have more than one years worth of loans at a rate cut in half of what it was in 2006, because only those loans disbursed in 2011-12 carry the 3.4 percent interest rate. Loans issued in the 2012 school year revert to the current 6.8 percent rate. (Click here for an explanation of why the rate cut phases in and reverts back.)

The College Cost Reduction and Access Acts student loan interest rate reductions will take place in increments as outlined in the table below. Loans disbursed in each year shown will carry the reduced interest rate for the life of the loan. A freshman entering college in the fall of 2008 will have four sets of loans at four different interest rates. And no borrower will have more than one years worth of loans at a rate cut in half of what it was in 2006, because only those loans disbursed in 2011-12 carry the 3.4 percent interest rate. Loans issued in the 2012 school year revert to the current 6.8 percent rate. (Click here for an explanation of why the rate cut phases in and reverts back.)

The most a borrower could save under the new laws interest rate cut is $216 a year ($3,240 over the life of the loan) on a maximum cumulative debt of $17,125 repaid over a 15 year period. That works out to $18 a month. Many borrowers will save less because they will not qualify for the maximum loan amount, or because they will enter college after 2008 and will not be able to take advantage of each years lower interest rates before they revert back to 6.8 percent.

And More Fine Print

The interest rate reductions only apply to Subsidized Stafford loans, and only for undergraduate study. Unsubsidized loans — which are similar to subsidized loans except they accrue interest while a borrower attends school — will continue to carry the current rate of 6.8 percent. Borrowers can qualify for either federal unsubsidized Stafford loans or subsidized, or a mix of the two, depending on the adjusted gross income (AGI) of a borrowers parents at the time he or she attends college and their school’s cost of attendance. Currently, about two-thirds of Subsidized Stafford loan recipients come from families with an AGI under $50,000, while one-fourth come from families with an AGI between $50,000 and $100,000.

The Policy Problem

There is a fundamental issue with the interest rate cut. Eligibility for the reduced interest rates is calculated based on the pre-college income of the student’s family, with no regard for the student’s earnings after graduation day. Moreover, the borrowers who qualify for the loan will not benefit while in school, but over the 10 to 20 years the loan is in repayment.

The NCES Baccalaureate and Beyond Survey suggests that years after graduating, the incomes of students with subsidized Stafford loans and those with non-subsidized Stafford loans are the same. Therefore, the interest rate cut provides a subsidy to students who come from low-income families, despite the fact that over the years of repayment they earn just as much as the borrowers who did not qualify for the lower rate loans. Is anyone surprised? After all, college is supposed to equalize earnings and employment opportunities. In short, the lower rates are a poorly targeted subsidy.

In sum, the interest rate cut isnt as much of benefit as advertised, nor is it targeted to those students who need it most, at the time when they need it most.

Issues

Programs/Projects/Initiatives

Related

Enrolled But Not Protected: Young Parenting Students Face Eviction at Alarming Rates