Strategies for Increasing Uptake of the Earned Income Tax Credit

In the CARES Act, Congress authorized $1,200 Economic Impact Payments (EIPs) to nearly all American adults to help families weather the fallout of the coronavirus pandemic. The delivery of the stimulus checks, which were structured as advance credits on 2020 taxes, was delegated to the Internal Revenue Service. While the implementation was far from perfect, as we have previously documented, the IRS successfully issued over 160 million payments in a matter of months — and, indeed, the campaign to distribute EIPs was among the most intensive and proactive efforts the IRS has ever undertaken to get funds to people in need.

The EIP campaign stands in stark contrast to the relatively meager measures implemented yearly to ensure takeup of another anti-poverty tax credit, the Earned Income Tax Credit (EITC). The EITC pays some low-income Americans more than twice as much as the EIP — and yet, for years, 20 percent of eligible households have not claimed these payments, impacting about 5-6.5 million households.1 As the EIP program winds down, it is an opportune moment to take stock of the extraordinary steps the IRS implemented to get those payments to people in need, and how they can be repurposed, annually, for the EITC.

In this post, we discuss three categories of actions Congress and the IRS could undertake to apply the lessons of the EIP to the EITC, building on infrastructure created this year:

- Using lightweight forms and proactive outreach to bring households who do not file taxes (so-called “non-filers”) into the system.

- Automating—or greatly facilitating—EITC payments to eligible tax filers.

- Improving actual payment delivery to meet the needs of recipients.

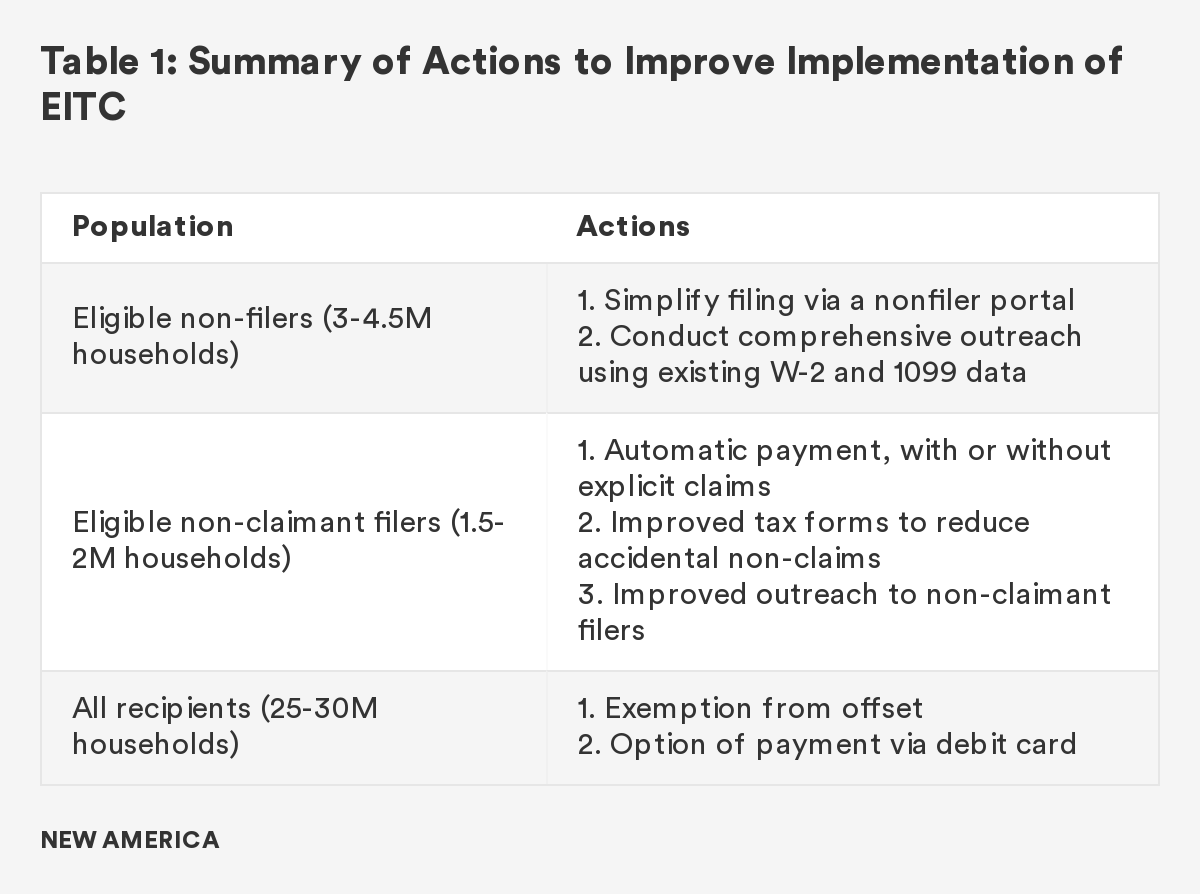

The actions are summarized in Table 1:

As we discuss below, these categories are to a degree interchangeable; the more the IRS can automate payments wholesale, for example, the less urgent it is to bring non-filers formally into the system. Congress and the IRS would be well-advised, though, to pursue all courses of action at once.

1. Bringing Non-filers Into the System

For both the EIP and the EITC, the vast majority of the challenge lies in reaching households who do not file taxes—so-called non-filers. Around 30 million households—including nearly 10 million with earned income—do not file taxes each year,2 largely because their income is low enough that they are not by law required to do so. With the EIP, nearly all distribution challenges stemmed from trying to reach this population. With the EITC, two thirds of eligible non-recipients are non-filers, representing 3-4.5 million households.3 In a system that relies on tax returns, non-filers are nearly invisible, existing outside of the core IRS processing pipeline, with only incomplete data. Turning them into filers is the simplest way to get them benefits.

Non-filers exist because filing taxes is hard. Modest interventions like the FreeFile program have proven insufficient to make tax filing easy and free for all Americans. In the long run, the IRS should pursue reforms to make it easier for everyone to file taxes. Efforts like GetYourRefund.org, created by Code For America, are powerful tools in this regard, and should be expanded. In the short term, though, the IRS can take two key steps to bring more EITC-eligible non-filers into the system — steps it took for the EIP this year.

1A. Simplified Filing Via the Non-Filer Portal

To facilitate access to EIPs, the IRS created the so-called “non-filer portal,” by which households who are not required to file taxes could “register” for the EIP without filing a complete tax return. In practice, the portal was a form to submit a simplified tax return, containing just enough information for the IRS to calculate and issue the EIP. The hypothesis was that a streamlined form, advertised as something less than a tax return, would attract more households than the famously daunting tax filing process.

The hypothesis was correct: according to incomplete government data, about 8 million households used the portal, out of an estimated 10-13 million who could have.

The IRS can and should apply the same lesson to the EITC: a simplified portal, allowing eligible households to sign up for the EITC without going through the complete traditional tax filing process, would bring more non-filers in the door. In fact, the IRS already agreed to do this, telling Senator Sherrod Brown in a June 30 hearing that such a step is indeed “the future of the IRS.”

This portal should be updated so that it provides sufficient information to the IRS to calculate and disburse the EITC. As one of us previously wrote at greater length, the IRS would have sufficient information regarding residency and dependents to do so if the portal requested the following items:

- Did you (and your spouse, if filing married-filing-jointly) have your principal residence in the U.S. for more than six months of the year?

- Would you like the IRS to compute your eligibility for and amount of the Earned Income Tax Credit?

- If a taxpayer enters dependents, the form would additionally ask: Did this child live with you in the U.S. for more than six months of the year?”

Meanwhile, if and when the IRS proceeds with the EITC portal, it should also make a few key functional improvements, as the EIP version was plagued by a variety of usability issues:

- The portal was not mobile responsive, a major problem in a country where almost 20 percent of low-income people only access the Internet via smartphones;

- The portal was available only in English and Spanish, a major problem in a country where more than 20 million people primarily speak other languages;

- As with so many IRS forms, the portal was written in legalese rather than plain language, making it inaccessible for many families; and

- The portal was not sufficiently clear about which populations were eligible to use it, causing many households—according to the IRS—to use it inappropriately.

In revamping the portal for EITC, the IRS should use modern web design best practices, including intensive user testing and plain language standards, to ensure the tool can indeed be used by its intended users.

1B. Outreach Letters

As of September, the portal had succeeded in bringing millions of households into the EIP pipeline—but millions more had not yet used it, due perhaps to lack of awareness or the usability issues identified above. So, the IRS undertook another key step: it used its vast dataset of Forms W-2 and 1099 to identify remaining EIP-eligible non-filers and reached out to them directly via mail, sending 9 million letters to likely-eligible households.

This effort is a proof of concept: as so many advocates have long pointed out, the IRS has data on most households, even those who do not file taxes. That’s because even nonfiler households generally receive income tracked on “information returns”—primarily, IRS Forms W-2 and 1099. By one estimate, this information return system covers 99.5 percent of American adults. Even if the IRS does not have sufficient information to calculate and pay credits, it has more than enough information to reach out to people who do not file.

The IRS can and should use the same process to reach out to EITC-eligible non-filers in future years, directly encouraging them to register for the EITC via the portal. Moreover, this effort can be much more intensive than the one instituted for EIP. The IRS should create a comprehensive, targeted outreach and follow-up program, not merely send one piece of mail that might be overlooked. Among other steps, the IRS should partner with trusted community-based organizations (CBOs) or state and local authorities to perform more intensive outreach.4

2. Automating—or Facilitating—Payments to EITC-eligible Filers

Most of the attention in closing the EITC participation gap has historically been paid to non-filers. But one third of EITC-eligible nonrecipient households do in fact file taxes. Under current IRS rules, the EITC is paid only if it is specifically claimed on the tax return, and 1.5-2 million tax filing households simply fail to do so.5

There are in principle a few solutions, all of which are intertwined. The best option is to automate the payments, regardless of whether they are explicitly claimed. A second option is to improve the design of the core tax forms, so that it is harder for households to overlook claiming the EITC. And a third option is to follow up aggressively with non-claimant filers, and solicit the additional information needed to make the payment. As discussed below, how much can be done via each of these means is dependent on legislative changes Congress makes to the program, and changes in regulatory posture from the IRS.

2A. Automatic Payments

Automatic payments were the keystone of the EIP program. For the most part, rather than wait for in-need households to proactively navigate byzantine tax forms to request an EIP, the IRS simply paid them using the best information on hand.

As one of us previously argued at greater length, the IRS has sufficient data from a standard tax return to automatically pay the EITC to childless households who do not claim it. The sole data element not clearly available to the IRS is proof that the taxpayer lived in the United States for six months of the tax year. But the IRS can infer this from data provided on information returns, and can accept the risk of mild overpayments in a few edge cases. And if the IRS and Congress do not feel comfortable accepting this risk with the program as written, it would of course be trivial for Congress to waive the requirement entirely.

The situation is somewhat more complicated for households with children. As currently written, the regulations defining a qualifying child under EITC are far too complex for the IRS to infer eligibility and make automatic payments to households that do not explicitly claim the credit. The question is, however: why have such complex rules? The rules are ostensibly intended to ensure that multiple taxpayers do not claim the same child; but the IRS could simply track which children are claimed by different taxpayers, and ensure that this does not occur. If Congress and the IRS were serious about getting this assistance to low-income families, the rules governing EITC payments for those with dependents could be greatly simplified, to the point that households with children, like their childless counterparts, could receive an automated EITC based on information in a basic tax return.

Indeed, in a June 2020 Senate hearing, IRS Commissioner Rettig signalled his openness to such a simplification during questioning from Senator Cantwell. The current rule complexity makes filing harder, makes automation nearly impossible, and makes the IRS’s job more difficult, all while accomplishing no substantive policy goals. The rules should be rewritten, and the payments automated.

2B. Improved Tax Forms

To the degree that Congress or the IRS is unsatisfied by the automation options outlined above—if the IRS is unwilling to accept a risk of small errors, and Congress is unwilling to simplify the requirements—the IRS can also modify the core tax forms to reduce the number of eligible filers who unintentionally fail to claim the credit. Specifically, the IRS could ensure it requests enough information from Form 1040 that it can make payments to the vast majority of EITC-eligible households automatically. The IRS has resisted making such edits before, arguing they run counter to the IRS’s core mandate, but the EITC should be important enough and central enough to the IRS’s mission to justify editing the core tax forms.

The simplest case in this regard is for childless households, for whom the only missing data at present is confirmation of six months’ U.S. residency. As the Treasury Inspector General for Tax Administration (TIGTA) argued in 2018, it would be trivial to add to Form 1040 a question confirming this residency requirement, thus ensuring that the IRS has this data point for all filers, and can automate payments to childless workers.

The outlook is again less clear for households with children, for whom the regulations are complex enough that the present rules cannot easily be compressed into Form 1040. However, if Congress were to significantly simplify the rules governing eligible children, the IRS could perhaps infer EITC eligibility from a modified listing of dependents provided on Form 1040.

2C. Outreach to Non-claimant Filers

Depending on how aggressive Congress and the IRS are in taking the above steps, there are still likely to be EITC-eligible households who slip through the cracks of automation and improved forms—who file taxes via normal means, fail to claim the credit, and cannot have their payment automated. For these households, the IRS should conduct intensive outreach to facilitate claiming the credit.

In fact, the IRS already does some such outreach: each year the IRS sends several hundred thousand notices to likely EITC-eligible households, called the CP-09 for households with children, and the CP-27 for households without. The notices alert taxpayers that they may be eligible for EITC, and allow them to claim it by filling out and returning an enclosed form. This program is a powerful proof of concept, but could be very meaningfully improved in several ways.

First, according to TIGTA estimates, the IRS only sends these letters to about 20percent of non-claimant filers, sending 350,000 letters while 1.8 million households are non-claimant filers. TIGTA reports that the IRS does this to ensure it is only sending letters to households it is quite confident are eligible. This explanation does not pass muster; the IRS has sufficient data to be fairly confident about the eligibility of nearly all households. This outreach should be conducted to every household more likely than not to be eligible.

Second, as with the proposed letters to non-filers, the outreach campaign should consist of more than a single letter. The IRS has detailed data on non-claimant filers, including addresses and other personally identifiable information. It should prioritize making contact with them via mail, text, and email if possible, and collaborate with local actors in a position to do more direct outreach.6

Third, and perhaps most importantly, the IRS must do a better job of designing, user testing, and proofreading the CP-09 and CP-27 letters. The letters are not only a mess of legalese incomprehensible to many families; they also, frequently, contain highly misleading language, if not outright errors.

In 2018, TIGTA found that the CP-09 sent out in 2015 and 2016 contained fundamental errors regarding the eligibility rules, which implied hundreds of thousands of eligible households were not in fact eligible for the credit. Incredibly, IRS leadership knew about these errors for two years before taking action to correct them. And yet, despite TIGTA’s reprimands, the 2019 versions of the CP-09 and CP-27 also contain serious errors. First of all, the 2019 form, covering tax year 2018, erroneously refers in its eligibility criteria to 2016 rather than 2018. Still worse, the eligibility criteria that TIGTA criticized in 2018 were still written incorrectly. The third page contains a list of four statements; if any of them do apply to the taxpayer then the taxpayer is not eligible. The second reads: “I did not have earned income or excess investment income in 2016 [sic].” The first half of this is correct; someone without earned income in the year is not eligible. But the second half is inverted; someone who did have excess investment income is ineligible. The sentence should read: “I did not have earned income in 2016; or I did have excess investment income in 2016.” (Better yet, the sentence should be divided into two different criteria.) To make matters worse, the form refers taxpayers to Publication 596 to define “excess investment income.” But that phrase is nowhere to be found in Publication 596. Errors of this magnitude in a tax return would lead low-income families to be audited and likely denied their EITC, but the IRS continues to make them year after year.

The IRS’s inattention to detail in these forms is inexcusable—and is compounded by the agency’s unacceptable inability to correct errors within a reasonable timeline. Especially if automation and tax form simplification do not reduce the number of non-claimant filers, the IRS must give the CP-09/CP-27 program the attention it needs to succeed. Letters must be streamlined, simple, accurate, and timely. Moreover, as TIGTA argued, the IRS must establish procedures for notifying and assisting taxpayers who receive erroneous forms.

Despite all these drawbacks, the CP-09 and CP-27 programs lead an additional 175,000 people to claim the EITC in an average year (although, given the small number of notices sent, this increases overall participation by less than 1 percent). If the letters were written correctly and clearly, and paired with outreach via other means, this follow-up campaign could easily sweep up the majority of non-claimant filers.

3. Other Delivery Changes

3A. Exempt EITC from Offset

The Treasury Offset Program allows state, local, and federal agencies to deduct money from government payments to individuals indebted to the government; for example, child support payments can be deducted before an individual even receives their check. Anti-poverty programs and entitlement programs have, historically, been exempt from most offset. The government recognizes correctly that these programs are putting critical money in the pockets of in-need people, and that debt settlement is a secondary concern. But the EITC, like other tax returns, is subject to offset. Indebted families may not see their EITC money at all.

The EIP was not subject to offset. Congress recognized, correctly, that the EIP was an anti-poverty program implemented via the tax code, not a regular tax return. Congress should recognize the same for the EITC. Most EITC recipients are very low-income, and taking away their check will quite literally perpetuate their poverty. Low-income workers should be able to decide how to use that money, and where their priorities lie.7

3B. EITC Payment Via Debit Card

At the beginning of the EIP program, payments were available only via paper check and direct deposit, much like normal tax returns—but, in May, the IRS announced that 4 million households would receive their payments on prepaid debit cards. Providing payments on debit cards is a critical accessibility step for the 5.4 percent of American households (over 7 million households) who are unbanked. These families cannot receive direct deposits, and generally must pay sky-high fees to cash checks at predatory businesses. To receive their tax refunds, many of these households rely on Refund Anticipation Checks (RACs), in which predatory tax preparers open temporary bank accounts to receive the refund, charging handsome fees for doing so. Debit cards are a simple way around this issue, and the IRS should make them available for the EITC.

As with the nonfiler portal, there are several implementation lessons learned from the EIP that the IRS should take into account before expanding the use of debit cards. First, the method should be the taxpayer’s choice; sending some households debit cards at random does more harm than good. Second, if the taxpayer already has a Direct Express federal debit card (from, e.g., the Social Security Administration), the IRS should offer the option of paying the EITC to this card rather than issuing a new one. Third, the IRS must improve the literal mailings that deliver cards to households. The EIP debit cards arrived in unmarked envelopes for security reasons, leading large numbers of households to unintentionally discard them. Before rolling out debit cards for EITC, the IRS should figure out a strategy that balances security and usability. Finally, the IRS should negotiate better terms for cardholders than those they negotiated for the EIP, which imposed relatively high fees for withdrawals and card replacements, and limits on daily transfers. These details matter for families living paycheck to paycheck.

* * *

The EITC is the nation’s largest anti-poverty program for non-seniors, and, for better or worse, it is likely to remain so for the foreseeable future. If the EITC is how we choose to support the neediest among us, it is long past time to take seriously the mandate that everyone eligible receives the money they deserve. To its great credit, and despite historic challenges, the IRS took this mandate seriously in distributing Economic Impact Payments. It is time to apply this same seriousness of purpose to the EITC. The relatively simple measures outlined in this article would represent an important step in this direction.

Downloads

Citations

- Estimates of the eligible nonrecipient population vary. In 2018, the Treasury Inspector General for Tax Administration (TIGTA) reported 5 million eligible nonrecipients, alongside 18.5 recipients, for a receipt rate of 78.8%. Other reports put the number higher, source ; CBPP reports that over 22 million households annually receive the credit, source, and IRS reports an annual non-receipt rate of 78%, source. This would imply 6-6.5 million unserved eligible households. A reliable estimate could be constructed through linking of IRS and Census records.

- Cilke (2011) estimates around 30 million non-filer households, of whom one quarter have earned income, source.

- TIGTA estimates 3.3 million households; but if the larger estimates of the unserved population prove correct, this number could be larger.

- The IRS is legally prohibited from directly sharing taxpayer data with outside organizations, but there are ways that IRS could enlist the help of local actors regardless. One solution is to broadly share data on zip codes with high concentrations of eligible nonrecipients, so that community organizations can geographically target their outreach efforts. The IRS also may be able to share more detailed household-specific information with state and local authorities, who could effect more direct outreach. The IRS should explore the extent to which such disclosures can be made, consistent with privacy law.

- Again, the uncertainty in this estimate stems from the uncertainty as to how many eligible nonrecipients there are.

- As noted above, there are some legal restrictions on how IRS can partner with outside actors in this regard.

- At the very least, if Congress feels there must be an offset, it should be a fraction of the EITC check.

More About the Authors

Cassandra Robertson

Gabriel Zucker

Fellow, Public Interest Technology

Nina Olson

Executive Director, Center for Taxpayer Rights

Programs/Projects/Initiatives

Related