Guaranteed Income and the Safety Net

Introduction

“Our people need [the cash], they put it to work, it alleviates stress, it helps our folks focus on raising their children, getting an education, better opportunities, and we all deserve that.”

— Mayor LaToya Cantrell, New Orleans, La.

Since the onset of the COVID-19 crisis there has been an increase in bipartisan support for guaranteed income (GI) programs, possibly due to the far-reaching harm caused by the pandemic, and in response to the federal government’s provision of direct cash payments to individuals.

Despite this growing support, cash transfers are still a divisive political issue. Long-standing debates about the “deserving” and “undeserving” poor remain deeply embedded in the United States’ cultural narrative, and opponents of guaranteed income policies sometimes question whether people—particularly those with little income and wealth—will make good financial decisions if given direct cash payments.

We have addressed these questions in previous briefs, and speakers from our virtual event, The Potential of a Guaranteed Income: A Conversation with Four Mayors, have touched on them as well. As Mayor Lauren Poe of Gainesville, Fla. told participants:

“There’s a very old trope that poor people don't know how to spend their money correctly and that's why they're poor, and it’s both a classist and typically racist argument that’s made…We don't ask our senior citizens to validate how they spend their social security check, we trust them with that payment. We haven’t asked people how they’re going to spend their extended child tax credit…'Are you going to spend this on your children? Show us how.’ But yet when we talk about giving assistance to people living in poverty we want to control how they spend that money. We take away their agency.”

Some opponents of guaranteed income also question whether cash payments will reduce labor market participation. While more research on this is needed, the Stockton Economic Empowerment Demonstration (SEED) experiment provided some evidence that labor market participation increased in response to its guaranteed income payments, primarily because recipients were able to access reliable transportation to and from work, and to find care for loved ones while they worked. This aligns with our understanding that, contrary to the “welfare queen” stereotype, people tend to prioritize the best financial decisions for themselves and their families when given the resources.

No matter where one falls on the questions of politics, impact, and deservedness around guaranteed income, the reality is that cash transfer movements continue to grow. Because of this, we will focus the attention of this piece not on the efficacy of a guaranteed income, but instead on how it might be implemented in complementary and additive ways to existing safety net supports. Specifically, we will examine what is known—and what is yet to be discovered—about the relationships between guaranteed income interventions and other social safety net policies.

Minding the Gaps: When the Safety Net is Not Enough

“We get calls to our office saying ‘You know, my car got towed, and I don’t have that $100… first I have to pay the ticket, and now I have to go get it out, get the car, and if I don’t get the car there’s a fee associated with keeping that car.’ So that’s just one example of what I’ve seen here, that direct cash assistance can really help our families.”

— Mayor Sumbul Siddiqui, Cambridge, Mass.

Guaranteed income advocates point out that cash could be a way to reach families who are unserved or underserved by existing safety net programs. These include people who qualify for these programs but still experience pressing needs, as well as those who might not qualify for government support but still struggle to thrive economically in increasingly inequitable communities.

Even for those who do qualify for government aid, the country’s current systems too often fall short, leaving policy holes that workers, local governments, and businesses must try to patch up themselves. Despite eligibility for programs like Special Supplemental Nutrition Program for Women, Infants, and Children (WIC) or Section 8 housing, many families face difficulty pulling together enough cash for basic needs like medical care, child care, and bills. In addition, there are many individuals eligible to access certain safety net programs—for example the Supplemental Nutrition Assistance Program (SNAP)—who still do not end up participating in these programs due to multiple barriers to access. Organizations like One Degree work to bridge this gap by providing an online resource for individuals to find localized public resources. However, even these tools still require individuals entitled to benefits to understand their eligibility and seek out resources independently. By providing cash payments directly to eligible individuals, guaranteed income models sidestep the challenge of reaching qualified individuals who do not have the time or resources to seek enrollment or to balance multiple safety net program requirements and offices.

In addition, there are many people who are not benefits-eligible but are still struggling. Currently, 44 percent of Americans aged 18-65 are considered “low-wage workers,” and 39 million workers earn less than $15 an hour. Even in many inexpensive U.S. markets, a wage of $15 an hour is not considered a good or promising living wage. This contributes to 35 million households (29 percent)—which is more than double the number living in poverty—qualified as “asset-limited, income-constrained, and employed” (ALICE). Those in this category earned above the federal poverty level, but less than the cost of living in their county. These families are sometimes excluded from benefits or receive very limited safety net assistance, even though they may have a hard time making ends meet.

These kinds of financial pressures have clear implications for health. For one, they have driven a 20 year trend of more people working multiple jobs, with women holding multiple jobs more often than men. Much of this work takes place within the gig economy, which, while sometimes touted for its flexibility and choice, also typically involves a lack of security, stability, and health benefits. Working extra hours not only has negative effects on overall health, but it also reduces the amount of time one has available for self-care, family-care, education, and leisure. Notably, it was toward these categories of expenses where many SEED participants chose to direct their guaranteed income payments.

Guaranteed income payments can also fill in safety net gaps that arise in times of emergency. These often take the form of medical care, home repair, auto repair, or even tax penalties. Only 4 in 10 Americans can afford an unexpected $1,000 expense without borrowing, using a credit card, or taking out a personal loan. These emergency expenses add up and can have ripple effects over time, impacting an individual's access to education, their ability to find and retain work, their susceptibility to predatory payday lending, their reliance on potentially also-vulnerable friend and family networks, and their overall health.

In the near-term, guaranteed income initiatives present an opportunity to fill in the gaps where the safety net falls short. When families are able to determine for themselves how to spend a flexible cash payment, they are able to make rational investments that can adapt to their unique circumstances.

How Guaranteed Income and Safety Net Policies Interoperate

“Our social safety net healthcare providers are absolutely overextended, under-resourced and unable to deliver the quality and quantity of healthcare that they would like to. So we need to look at other ways of helping [people living in poverty], because the traditional system is broken, has been for some time, and is not going to be fixed overnight.”

— Mayor Lauren Poe, Gainesville, Fla.

The federal social safety net is commonly understood to include the following programs:

- SNAP/Electronic Benefits Transfer (EBT), a program that provides nutrition assistance to low-income individuals and families through a monthly benefit.

- WIC, a program that provides nutritious foods and education for women, infants and children up to age five who are at nutritional risk.

- Pell Grant, a post-secondary education grant for students with exceptional financial need.

- Tax policies, including mortgage deductions, healthcare exclusions, and the Earned Income Tax Credit (EITC). These policies are aimed at supporting working families with low- and moderate- incomes. Annually, the EITC lifts 5 to 6 million people out of poverty.

- Social Security, a benefit for retired and disabled workers, as well as survivors of deceased workers. In 2021, 65 million Americans per month will receive a Social Security benefit.

- Medicaid or marketplace health insurance subsidies and coverage. Medicaid is a joint federal and state program that provides health coverage to over 72.5 million Americans.

- Housing Choice Voucher Program (Section 8), a program that financially assists low-income families, the disabled, and the elderly with housing.

These programs have been criticized by some as having a racist and classist history, underpinned by narratives portraying low-income communities of color as less capable or less deserving of opportunity. Some proponents of guaranteed income argue that if we truly want to build a system in which the end-goal is health and economic stability for all, cash could be key, supplementing the goals of existing programs by creating more flexible avenues for individuals to fill their needs. For example, while a program like SNAP nominally aims to end hunger, it limits what kinds of food participants can get and where it can come from; cash transfers can fill those remaining gaps, working around some of the systemic limitations in safety net programs’ design and making the journey to their end-goals more efficient and effective.

In addition to serving as a last mile addition to existing safety net programs, guaranteed income recipients are also able to provide for themselves in ways that the existing safety net does not accommodate for at all. Below is a list of the main types of expenses that Stockton SEED pilot participants were able to support because of their direct cash payments. These items would not be covered under the current suite of safety net benefits, yet are essential for individuals and families to thrive and build financial security. (For more on the health equity findings from Stockton’s SEED pilot, refer to Exploring SEED: A Guaranteed Income Demonstration’s Health Equity Implications.)

- Auto repair and transportation costs: Participants used cash to support vehicle maintenance, payments, fares, and fuel costs. These, in turn, enabled them to travel across the community more easily, to access more or better work, or to access public services, including greenspaces.

- Credit rescue and debt pay-down: Multiple participants paid off mounting bills and paid down debts in order to begin building savings.

- Healthcare emergencies and co-pays: In cases where Medicaid didn’t cover the cost of a health expense or co-pays were too costly, participants were able to supplement their health needs with guaranteed income.

- Leisure, athletics, and gifts for children: Cash payments improved individual and relational health through access to downtime, children’s extracurricular activities and athletics, and family gifts. Leisure is essential for improving mental health, long-term decision-making, and quality time, and the ability to give gifts at culturally significant moments such as birthdays and holidays can support families’ sense of pride and mutual caring.

- Moving to improved and safer housing, securing housing, and doing home repairs: Some participants said they were able to save enough in the program to move into better neighborhoods, or to improve their current homes.

- Reduced work hours to allow for self-care, family care, leisure, education, or new pursuits: In cases where participants held multiple jobs, some were able to reduce their hours or workload and instead spend that time pursuing other important experiences and opportunities. Participants reported being able to develop more secure attachments to their remaining work due to the decreased income volatility.

- Travel: Participants were better able to travel in order to stay connected with their families and to make time for one another.

While these are the expenses families are prioritizing now, potential new investments in social services and public policy—such as a higher minimum wage and a more accessible, navigable unemployment insurance system—could shift this picture. Understanding guaranteed income as one element of a complex safety net system will be critical to targeting cash transfer policies as other elements of the system evolve.

Guaranteed Income and Benefits Loss: Challenges and Solutions

“Poverty is a policy failure, not a personal failure.”

— Mayor Libby Schaaf, Oakland, Calif.

“Means-tested” safety net benefits are those that determine eligibility based on recipients’ income or other available resources. Guaranteed income policies can negatively impact some recipients’ eligibility for these types of programs when the added income raises them above benefit qualification thresholds. A 2020 article covering the Magnolia Mothers Trust documented this effect:

“Though the payments have made her life more comfortable, [one recipient] said there are some downsides. An increase of $12,000 a year to some women’s incomes could mean that they no longer qualify for food stamps or Medicaid. ‘In reality the caps are so low that the moment you get something like Magnolia Mother’s Trust, it makes all of those resources that sometimes are needed unavailable,’ she said. [The recipient] said she has not been hurt by the payments, but other women in the program have told her that it’s made their lives more difficult. ‘Some mentioned that they would rather not have the $1,000 because of the headache,’ she said. [Aisha] Nyandoro said there is a reduction in benefits for some mothers, averaging $300 to $400 each month, because of the ‘punitive aspect of the social safety net.’”

In 2020, SEED researchers published a case study on how the SEED pilot tried to mitigate these kinds of benefits cliffs, in which they outlined three models that policymakers and practitioners are currently using in response to this challenge:

- Do not address it at all: For example, the recent federal pandemic stimulus policies haven’t specified how these payments will interact with recipients’ other means-tested benefits.

- Replace all benefits with GI: Andrew Yang’s Freedom Dividend proposed that recipients should choose between receiving $1,000 in cash or receiving their other benefits. The SEED researchers point out that this approach has been proven at least once to be unfeasible, when recipients in the SIME/DIME guaranteed income experiments of the 1970s refused to enroll in the pilots until it was promised that their other benefits wouldn’t be taken away.

- Help recipients utilize guaranteed income alongside other benefits: This is the approach that SEED and other pilots associated with the Economic Security Project have taken, with the goal of helping cash transfers authentically augment wages and/or existing government support. A monthly cash payment of $500, for example, is not enough for most families to stop working, and might not completely replace the value of their other safety net programs, but alongside these resource streams could be enough to provide new stability.

The projects taking this third approach are pioneering solutions to avoiding GI-related benefits cliffs. Some of these emerging best practices include:

- Allowing each household to determine which individual amongst them is the best fit to apply for the cash transfer program: Hypothetically, this would allow someone in the household who is not a recipient of other benefits to apply for guaranteed income, in order to preserve the benefits received by another household member. It stands in contrast to a common approach that prioritizes more randomized impact evaluation, in which researchers might put specifications on whom in a household should apply, versus allowing participants to self-select into the program.

- Building relationships with local implementers to help them classify guaranteed income in low-risk ways, or to waive guaranteed income where possible: Frontline workers at local agencies are often the gatekeepers who determine how rules are interpreted and implemented with potential recipients. When policies change—or when policy priorities appear to be in conflict—these workers’ judgment calls can be the difference between a family retaining its support or being cut off from it. When guaranteed income pilot staff can connect with these frontline workers to explain the purpose and ideal implementation of rules that might be impacted by guaranteed income, it can increase the likelihood that those workers will interpret policies in favor of allowing recipients to keep their benefits. Where possible, pilot staff can forge waiver agreements with local agencies to completely exclude guaranteed income payments from means-tested benefit calculations.

- Ensuring that total guaranteed income payments do not exceed the IRS gift limit of $15,000 per year: This reduces the risk of hitting a benefits cliff for some—though not all—types of benefits, but only if the income is understood and interpreted correctly by local implementers.

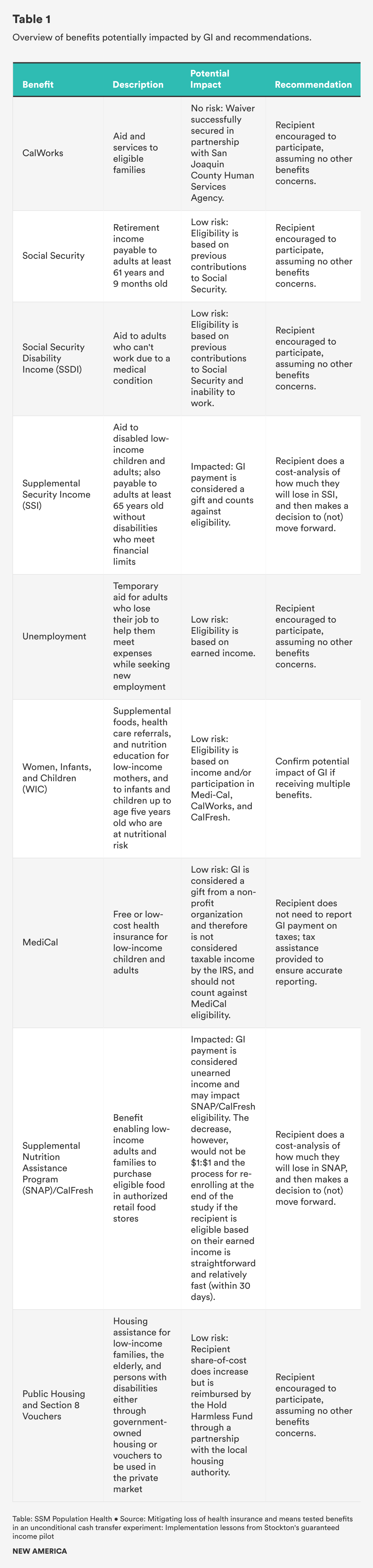

- Understanding how guaranteed income could impact eligibility for each local, state, and/or national benefits program: One challenge to making generalizations about how guaranteed income will coexist with other benefits is the wide range of variables driving whether recipients are eligible for other safety net support. These variables can include eligibility restrictions, income, location, and availability of program funding. Staff at specific guaranteed income programs can do some of this more individualized analysis ahead of time, as SEED staff did to create its table, “Overview of benefits potentially impacted by GI and recommendations.” This table outlined each benefit program its pilot recipients might be participating in, the potential impact of guaranteed income payments on eligibility for that benefit, and recommendations for how pilot staff should counsel potential participants as to whether or not to move forward with SEED participation.

- Targeting guaranteed income supports to recipients ineligible for other safety net programs: The Compton Pledge effort is explicit in its focus on residents who are formerly incarcerated and/or undocumented, which makes them ineligible for most other public benefits. New efforts in Oakland (Calif.), Gainesville (Fla.) and Durham (N.C.) are also focused on residents returning from incarceration

When safety net benefits are lost due to guaranteed income payments, emerging best practices include:

- Reserving money in a fund to reimburse the value of lost benefits: Based on a practice that originated with the Alaska Permanent Fund Dividend, pilots like Compton Pledge and SEED have developed “Hold Harmless Funds” to help bridge gaps left when benefits are revoked.

- Helping recipients re-apply for public benefits: Pilots that invest in individualized case management for participants can wrap up their commitment to residents by helping those who have lost benefits reapply for them once guaranteed income payments end.

- Sharing stories of benefits loss to change systems: Many guaranteed income pilots — including Magnolia Mothers Trust, Compton Pledge, and SEED — are pairing their on-the-ground work with narrative change efforts, in the hopes that changing the stigmas around poverty can eventually lower barriers to accessing the safety net. When recipients of guaranteed income lose benefits, it highlights that current means tests are often too low. Aisha Nyandoro of Magnolia Mothers Trust spoke to this in Essence, saying, “That’s the story we don’t talk about, how it’s virtually impossible to claw yourself out of poverty, and that’s problematic.”

- Ensuring that guaranteed income payments are robust enough to outweigh potential losses: The Magnolia Mothers Trust pilot found that its participants on average lost $300-$400 worth of benefits per month by participating in its program, but Nyandoro asserts that “with the net gain of $600 to $700 cash without strings, mothers still indicate that having the cash is a greater benefit.”

Full Table 1 – pictured above found in the SEED Report.

As SEED researchers wrote in their case study, “While most GI experiments operate within the existing benefits structure, little is known about how cash transfers may interact with the social safety net in the US… at this point, [it] is essentially a policy and implementation gray space carrying competing sets of mandates and ethical dilemmas.” While the potential for benefits loss—as well as the potential interventions for addressing it—are mostly untested, the explosion of guaranteed income pilots across the country will begin providing many opportunities for further exploration. This is an area for potential investment in research for health equity funders and policymakers.

Long-term Policy Pathways and Implications

Guaranteed income is riding a wave of momentum that continues to bring the concept from theory into reality, with clear paths for expansion at both federal and state levels. Some of these are outlined below.

American Families Plan and Expansion of the Child Tax Credit

The American Rescue Plan expanded the existing Child Tax Credit (CTC), increasing the total possible payment from $2,000 to $3,600 per child, and making even the lowest-income families eligible to receive the full amount. It has also made the credit available as a monthly payment, one reason why many guaranteed income stakeholders have championed the policy. In an NPR interview, journalist Jason DeParle asserted that this CTC expansion is essentially a guaranteed income program, saying, “Politically, [the CTC] has advanced because saying that we're offering a child tax credit sounds less ambitious or less revolutionary than, say, we're providing a guaranteed income for families with children. But I think the latter is more accurate.”

Subsequently, President Biden proposed the American Families Plan, which aims to reduce child poverty and support families through investments in child care and education as well as policies like paid family and medical leave and unemployment insurance. The American Families Plan would make this round of changes to the CTC permanent, indefinitely sustaining low-income families’ ability to claim the credit, and extending the increase in the total credit amount until 2025.

Some progressive critics believe the American Families Plan doesn't commit to enough, particularly to lower prescription drug prices and expand Medicare. In addition, while 88 percent of the country’s youth qualify for the expanded CTC—with an expected impact of cutting child poverty nearly in half—the American Rescue Plan’s version of the CTC still does not allow undocumented youth to access the benefit. More conservative critics of the plan question its $1.8 trillion cost (which would be paid for through taxes on the wealthy and increased capital gains taxes on those making over $1 million), the expanded role of government in family care, and whether family care and workforce policies should be considered part of infrastructure. However, internationally the United States ranks last in family-friendly policies, and in the economic fallout of the pandemic, there is a clear need to improve the effectiveness of the safety net, promoting economic stability and family security to create strong and healthy communities.

Insufficiencies in family friendly policies and economic stability are indicated by the common use of guaranteed income by SEED participants to offset many of the costs that public policy could otherwise cover. For example, passing a federal policy like paid family and medical leave, tied to the individual rather than the workplace, might change how recipients use their guaranteed income. This is one area for potential research investment as the conversation about the American Families Plan unfolds. Other potential advocacy investments include ensuring that undocumented youth can benefit from the CTC, and lifting up narratives of families who received the CTC to demonstrate the impacts of the policy, and of cash-focused policies like it.

Expansions of the Earned Income Tax Credit

Like guaranteed income, the EITC is focused on “ensuring a basic level of economic support”—ideally, creating a floor beneath which people cannot fall. It has been shown to significantly combat family poverty and reduce racial economic gaps, and advocates of guaranteed income are often also advocates for expanding and updating the EITC, as a way of “essentially providing the same benefit as a guaranteed income,” but with the ease of “making use of an administrative system that is already in place.” However, unlike guaranteed income, the EITC benefit is connected to work: people who earn $0 in a year will not receive any money from the EITC. It is also strongly focused on supporting families with children; in 2020 it provided a maximum benefit of just over $500 for childless workers.

Various academics and policymakers have proffered new tax credit ideas based on the EITC, or have suggested changes to the EITC itself that expand its reach and/or bring it closer to a guaranteed income model. These include:

- The 2018 LIFT the Middle Class Act from then-Sen. Kamala Harris (D-Calif.), proposing a new credit accessible to more people, but still requiring recipients to work.

- The ESP-supported Cost of Living Refund/Working Families Tax Credit championed by Robert Reich, a set of amendments to the EITC that would be available monthly, would be available to families up to the median income, would increase the maximum amount receivable, and would begin to detach the EITC from paid work by including caregivers and low-income students.

- The 2019 BOOST Act from Rep. Rashida Tlaib (D-Mich.), which would be available even to people who did not earn a paycheck, and could be distributed monthly

- Guaranteed Income for the 21st Century, recently released by The New School Institute on Race and Political Economy, which is perhaps one of the most radical reimaginings of the EITC to date. In addition to making payments available monthly, it aims to completely eliminate poverty, and to begin closing racial wealth gaps.

“Our guaranteed income program dramatically expands the structure of the EITC to guarantee income, eliminate poverty, and lift more families into the middle class. Under these terms, a maximum refund lifts a household earning $0 up to the level of the poverty line, with a gradual phase-down beginning for households above $10,000 or $15,000 (for single-adult households and two-adult households, respectively) until phasing out at approximately the national median household income, at $50,000 or $70,000 respectively. Every individual adult is qualified to receive annual monetary support of up to $12,500, regardless of their household composition or filing status. Families with children will also receive an additional grant for every child.”

California’s Investment in Guaranteed Income

California lawmakers recently approved the nation’s first state-funded guaranteed income program. The $35 million plan allows local governments to apply for money and run guaranteed income programs that distribute unrestricted cash monthly to pregnant people and young adults transitioning out of foster care. This policy comes after the early success of guaranteed income initiatives in Stockton and Santa Clara county. These investments into guaranteed income pilot programs will provide more state-wide quantitative and qualitative data on the policy, which could serve federal policymakers as they work to understand the impact of guaranteed income as a tool for economic equity.

Effectiveness, Efficiency, and Equity: Political Considerations and Remaining Questions

The potential for guaranteed income, universal basic income, or revamping of existing social safety nets will continue being debated, tested, and tweaked at local and national levels. The effectiveness, efficiency, and equity of these policies will continue to be contestable, yet important, lenses for considering how to advance or halt these policies.

While politicians and advocates use various arguments for or against guaranteed income programs, most seek to answer the same basic questions: Which policies will be the most efficient, effective, and equitable? Efficiency and effectiveness are two of the most bipartisan lines of argumentation, while questions of equity often fall along party lines. Dissent about equity often derives from differing beliefs about the degree to which historical and present policies and systems have provided, and continue to provide, relative advantage to certain people—most notably based on race.

Mayor LaToya Cantrell describes her personal experience of growing up and seeing her Black mother “use safety net resources, [and she] used it wisely and raised her children,” as a counter-narrative to racialized prejudices that opponents of guaranteed income policies and the broader cadre of safety net supports often refer to directly or indirectly in their critiques of these policies. Mayor Cantrell continues that growing up “hearing all of the misconceptions… ‘you’re on welfare,’ or ‘you’re poor, you don’t want to work,’ or ‘you’re lazy’… it’s racial as well, to the Black and the Brown in terms of that. So for me it was demonstrated in my home and in my family and in my community, that just a little bit can get you over that hump, and to get you well on your way.” She invokes this lived experience, as well as her professional expertise, to advocate the pilot guaranteed income program in her city, New Orleans: “In our city, I see the need and absolutely know that… we can get people to pivot to a more sustainable quality of life, if we give them the opportunity. So this is just another way for our people to meet their immediate needs and then be able to start to place themselves into a more just environment in terms of training and workforce, so that they can be whole, and they can be dignified.”

Beliefs about what makes people whole and dignified, while not directly stated in policy, are often implicitly or explicitly stated in rhetoric used to argue for and against policies—particularly social safety net policies. The two-party system in American politics can cause partisan divides that, at their extremes, can posit that an opposing political party does not value nor care enough about certain individuals based on their socioeconomic status or belonging to a particular demographic group; however, research and writings on moral psychology and reasoning illustrate how individuals from both parties are guided by a different ordering of similar values, and vote to affirm and sustain their moral interests. To bridge this divide and work towards major bipartisan policy initiatives—such as those that seek to dramatically change social safety net policies and programs—politicians and advocates often seek to create a sense of cohesion and a moral reimagining of what policy can do to improve the lives and wellbeing of individual Americans and society as a whole. Mayor Libby Schaaf illustrates an example of partisan-bridging commentary, affirming the need for broad coalition building and fast action to address the challenges families are facing and pointing to action taken in the wake of the COVID-19 crisis:

“We just got through this year, and while it was so full of loss and suffering, it also was full of amazing resilience. We saw our whole country come together with a sense of urgency and determination to stop people from being harmed. We need to bring that same sense of urgency and this knowledge that we can do amazing things when we put our collective minds to it. There's an appetite for radical imagination that we never had before.”

As safety net policies develop and change, it will be important to understand what community members might invest in if more emergent needs were covered by improved public systems, including early and post-secondary education, investments in mental wellness, and child and elder care. In addition, to dispel the misconceptions and stigmas surrounding poverty and access to the safety net, guaranteed income stakeholders must invest in narrative work showing the resilience that individuals and families demonstrate when provided stability and financial resources. New data from emerging monthly cash transfer policies—including positive narratives and improved health outcomes within communities—could help establish the case for the effectiveness, efficiency, and equity of guaranteed income, and for reimagining the safety net even more broadly.

Conclusion

“The momentum [from COVID] is critical as we continue to collect data that shows a guaranteed income is essential to address these decades of economic inequity…seeing that momentum grow and to see some of the bipartisan support really does give me a lot of hope.”

— Mayor Sumbul Siddiqui, Cambridge, Mass.

Guaranteed income programs are worth exploration by a diverse range of safety net stakeholders, whether one’s goals are to increase the efficiency and effectiveness of government supports, to provide individuals with greater financial choice and freedom, to illuminate new narratives about the trustworthiness and deservedness of people living in poverty, or to undo harms caused by structural racism. Because of guaranteed income’s potential promise as a policy tool it is essential to continue understanding how it might— and whether it should— function alongside the traditional social safety net. Do guaranteed income policies support existing programs more effectively when they are time-bound or permanent, or when targeted toward certain demographic groups? Is guaranteed income best used to buy time while policymakers fix more traditional safety net systems? Or should it supplement or replace the safety net in the short- or long-term? What new best practices can pilot programs leverage to maximize the benefits their participants receive? The current questions provide rich ground for further exploration by funders, policymakers and practitioners, with the potential to increase the efficacy of guaranteed income, and ultimately, to continue moving toward an economy in which everyone can thrive. Throughout this process, it will be essential to listen and learn from cash recipients, and to bring their lived expertise to bear in designing systems that will better serve all.

Acknowledgments

Developed with the generous support of:

Blue Shield of California Foundation

Downloads

More About the Authors

Roselyn Miller Champion

Grant Analyst, City of Portland

Rachel Alexander