Designed_for_Filing_Not_for_Families_Reimagining_Tax_Credit_Delivery_2025-05-20

Table of Contents

Abstract

Tax credits like the Earned Income Tax Credit and Child Tax Credit are among the most effective anti-poverty tools in the United States. Yet millions of eligible families are missing out on this critical financial support. This report from the New Practice Lab reframes tax credit access as a service delivery challenge, analyzing why so many low-income households struggle to claim tax credits and receive the support they’re owed.

Grounded in a user journey framework, the report maps barriers across three phases of the benefits experience: learning about tax credits, applying for them through filing, and ultimately receiving support. It draws on a nationwide survey of over 5,000 respondents and qualitative research with 25 Illinois residents to surface key challenges—including misinformation about eligibility, outsized fears of making a mistake, unaffordable filing help, documentation barriers, and disconnects between tax credits and other public support programs.

The report offers five actionable recommendations for state agencies. These include (1) tailoring outreach and messaging to reflect real-life motivations and behavioral archetypes, (2) reframing tax filing as a supportive, not punitive, process to reduce fear, (3) coordinating with existing government support programs, (4) expanding filing options for households currently excluded from access, and (5) recognizing that support through tax credits shouldn’t hinge on perfect paperwork—reaffirming the role of revenue departments not just as compliance enforcers, but as benefits administrators, especially for economically vulnerable families.

Acknowledgments

The author would like to thank Lindsey Wagner, a design researcher and consultant with the New Practice Lab, in particular, for her qualitative research in Illinois and her contributions to the section on taxpayer archetypes.

Further, the New Practice Lab would like to express our gratitude to those who provided valuable research, insights, and feedback throughout the production of this report: Meegan Dugan Adell, Alejandra Ponce de Leon, Soren Spicknall, Simone Brody, Ayushi Roy, Amira Boland, Nhi Nguyễn, Nikki Lee, and Brett Maney.

Editorial disclosure: The views expressed in this report are solely those of the author and do not necessarily reflect the views of New America, its staff, fellows, funders, or board of directors.

Downloads

Overview: Tax Credits as a Service Delivery Challenge

We know tax credits work. Decades of research—including work by the Center on Budget and Policy Priorities and the IRS—show that tax credits like the Earned Income Tax Credit (EITC) and the Child Tax Credit (CTC) reduce poverty, improve child outcomes, and boost household stability. Yet access remains uneven: One in four children under 17 didn’t receive the full CTC in 2023, and one in five families eligible for the EITC don’t claim it each year. As the EITC marks its 50th anniversary, there is growing momentum to reimagine how we deliver these critical supports.

Millions of low-income households (many of whom are not required to file taxes due to their income level) miss out on valuable tax credits each year because they struggle to access them through the tax system or don’t realize they qualify. Unlike other public benefits, tax credits are only available to those who file a tax return, making the path to receiving them feel more like a compliance exercise than a support system. Even though tax credits are designed to offer financial relief, they don’t always feel like help.

Tackling service delivery challenges is gaining momentum at the local, state, and federal levels. There is a growing body of evidence showing that tools from behavioral science, service design, product development, and community engagement can improve public services. Yet tax credit uptake challenges are still rarely framed—or addressed—as service delivery challenges. A core principle across these disciplines is simple and essential: Begin with a deep understanding of the people programs are meant to serve.

Before launching this research, the New Practice Lab conducted a landscape analysis of existing studies on households that don’t regularly file taxes. That review found that while there was strong existing research on the demographic characteristics of these households, there was less evidence around the specific logistical barriers they face, and how those barriers shape implementation challenges for government agencies. Building on that gap, we conducted a mixed-methods study to better understand tax filers and potential filers, focusing on the emotional, logistical, and informational hurdles that prevent people from filing—and ultimately, what it would take to deliver tax credits more effectively.

This research draws on two components:

- A nationwide survey of 5,012 respondents (64 percent of whom had not filed taxes in the last three years, and 88 percent of whom had annual household incomes under $65,000)

- A qualitative study with 25 low-income residents from Illinois (all of whom had applied for or received state benefits in the past year)

More details on the study methodologies are provided at the end of this report.

This report shares six reasons why tax credits often fail to reach the people who need them, along with actions governments—particularly state Departments of Revenue (DORs)—can take to start addressing these barriers.

We’ve structured these findings through the lens of how people typically navigate a public benefit journey: learning about, applying for, and receiving support.

I. Learning: Awareness and Exploration

The first breakdown often happens before someone even considers claiming credits on their tax return: Many people either don’t know tax credits exist or don’t believe it’s worth going through the intensive filing process when they aren’t required to file based on their income.

Awareness Gaps Keep Eligible People from Accessing Credits

While filing taxes is an obligation for some, it is an opportunity for many others. For low-income households—especially those below the filing threshold—not filing is often not about apathy or avoidance. It is a genuine belief that they don’t need to or are not allowed to file.

“I only work side jobs, so I don’t have enough money to file.”

—Survey respondent, living in a household with one child under six years; $10,000–$25,999 annual household income; hadn’t filed taxes in three years

“I have yet to reach an income that requires [me] to file for taxes.”

—Survey respondent, employed with multiple employers; <$10,000 annual household income; hadn’t filed taxes in three years

People repeatedly told us, “I don’t make enough to file.” While this is often legally true, it can come at a real financial cost—many were still likely eligible for tax credits even if they weren’t required to file.

Among low-income households earning under $26,000 that hadn’t filed taxes in the past three years, one-third (33 percent) said they didn’t file because they believed their income was too low. Yet within this group, 20 percent had earned income from work (including jobs with one or more employers, gig or freelance work, or self-employment), and 37 percent had at least one child in their household—factors that likely would have made many of them eligible for tax credits had they filed.

“I’ve never heard of tax credit[s].”

—Survey respondent, living in a multigenerational household with one child; <$10,000 annual household income; hadn’t filed taxes in three years

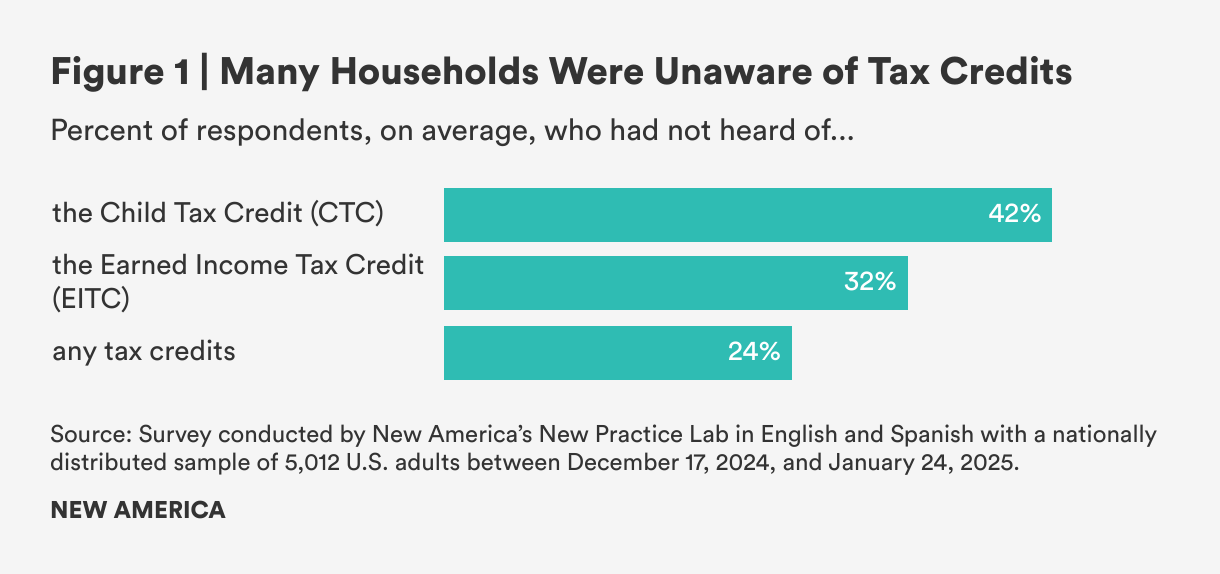

When asked about their awareness of tax credits, on average, 42 percent of households had not heard of the Child Tax Credit (CTC); 32 percent had not heard of the Earned Income Tax Credit (EITC); and 24 percent had not heard of any tax credits.

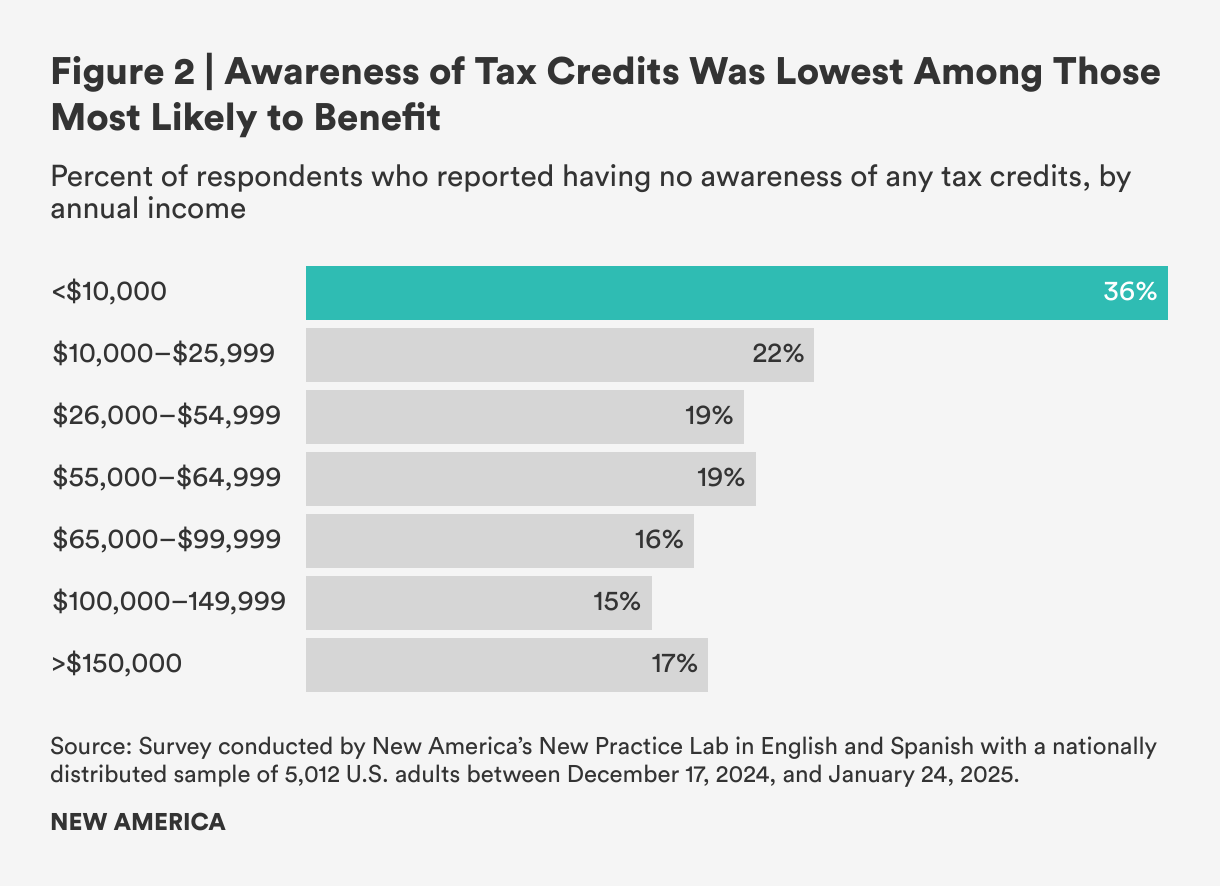

Awareness was lowest among those most likely to benefit. Among households earning under $10,000 annually, 36 percent were unaware of any tax credits, more than double the rate among households earning over $150,000 (17 percent). Within this lowest-income group in our survey, 40 percent of employed households hadn’t heard of the EITC, and 47 percent of households with children hadn’t heard of the CTC.

When asked why they had not claimed credits, low-income non-filing households cited overlapping concerns: 40 percent believed their incomes were too low to qualify, 24 percent found it challenging to understand which credits they were eligible for, 16 percent were worried that claiming credits might affect other benefits like Medicaid or the Supplemental Nutrition Assistance Program (SNAP), 16 percent didn’t know how to claim credits, and 12 percent said they couldn’t find the help they needed. A few more shared “other” reasons but did not mention the specific reasons or restated previous reasons worded differently.

Some people, like those receiving Social Security Disability Insurance (SSDI), were especially confused about their tax eligibility, particularly when they were simultaneously employed. Twenty-five percent of SSDI recipients in our sample reported employment, but 55 percent of these employed SSDI recipients had not filed taxes at all, and another 14 percent had filed inconsistently. While SSDI alone doesn’t qualify someone for the EITC, many of these individuals may still have been eligible based on their earned income.

“I don’t have to file because I never make enough.”

—Survey respondent, employed with one employer and receiving SSDI payments; $10,000–$25,999 annual household income; hadn’t filed taxes in three years

“I find knowing how to start challenging. I have questions like who do I connect with, and how will my income be affected? It’s a lot of steps that don’t always appear coherent.”

—Illinois study participant, receiving SSDI payments

Some simply assumed they were doing everything right, until asked more directly. Their filing habits had become routine, shaped by early experiences or advice that hadn’t changed over time, even as their life circumstances did. This kind of path dependency, or “status quo bias” (repeating what’s familiar without re-evaluating), can prevent people from realizing that tax credits might help in new ways. When awareness of credits was low—especially during major life changes like becoming a caregiver or taking on new forms of work—it was easy to overlook that tax filing could offer meaningful support.

“I never thought about [tax credits]…I just filed my taxes the same way I have been doing since I was 17 years old.”

—Survey respondent, 35–44 year old legal guardian/foster parent to two children; <$55,000 annual household income; had filed taxes every year for the past three years but had never claimed tax credits

In our Illinois interviews, several participants were surprised to learn that they were eligible for credits, especially after we clarified that different types of labor, like gig work, caregiving, or selling goods online, could count toward income. Slightly different eligibility rules across federal and state programs added to the confusion.

“Oh, so I can file taxes if I was an Uber driver? I didn’t know that!”

“That’s awesome that I can include income from driving and selling goods online…I did not know that.”

“I didn’t even know you can get an income credit on state taxes…I didn’t use to file state because I didn’t want the state to take it from me. Maybe had I known, it might have boosted me up to pay off those tickets, and I still would have gotten a portion back.”

Tax credit programs are designed to reward work and caregiving by providing financial or family support, but the impact of these incentives is limited when people don’t know they exist.

Diverse Motivations and Multiple Sources of Information Shape Credit Uptake

Across our survey and qualitative research in Illinois, one theme stood out: Families don’t think about taxes in one uniform way. While some file annually, others file occasionally or not at all—often based on whether the refund feels “worth it,” and whether they trust the process or fear it will interfere with other benefits.

Their motivations, filing behaviors, and barriers are shaped by life experiences, financial pressures, and personal networks.

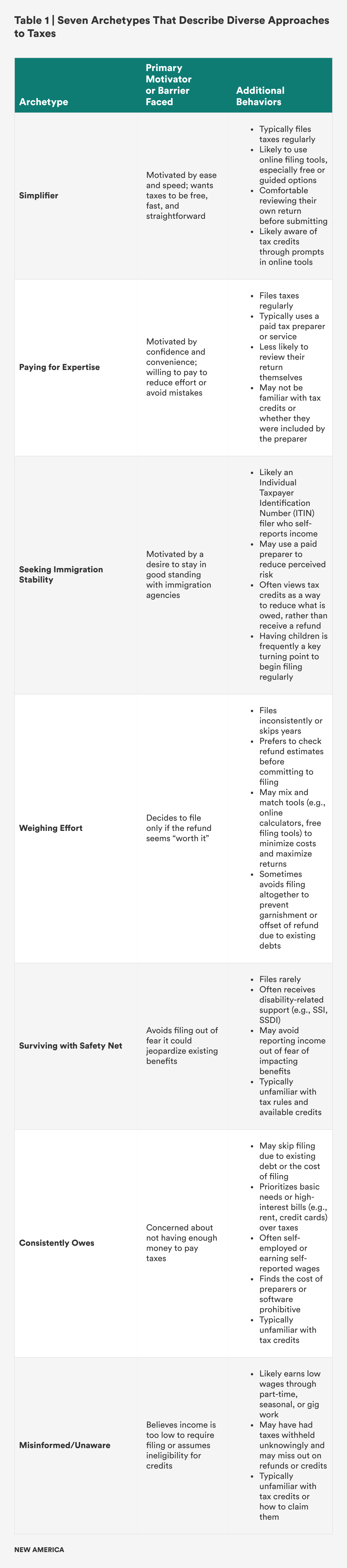

Within the families we spoke to in Illinois, we identified seven behavioral archetypes that help explain these patterns:

- Simplifier: wants taxes to be free and fast; avoids unnecessary steps

- Paying for Expertise: will pay for filing to reduce risk or effort

- Seeking Immigration Stability: wants to remain in good standing with immigration agencies

- Weighing Effort: will file only if the refund feels “worth it”

- Surviving with Safety Net: worries that filing could jeopardize benefits

- Consistently Owes: may have other debts that are a higher priority to pay than taxes

- Misinformed/Unaware: believes income is too low to file or assumes they’re ineligible for credits

Table 1 below outlines each behavioral archetype along with their primary motivations or barriers to filing, and highlights behavioral patterns that may shape how they approach taxes and tax credits.

Simplifiers may respond to language about ease and speed: “File in 10 minutes, for free.” Those worried about benefit loss might appreciate reassurances: “Filing won’t impact your SNAP or housing.” Those misinformed or unaware may need help understanding why they should file or that they were eligible for credits.

This variety matters. Standard messages about “filing for tax credits” can miss the mark, especially for those who don’t plan to file or who don’t associate taxes with benefits. In fact, families we interviewed in Illinois said that language about “missing money” or “extra income” resonated far more than tax-specific terms like “credits” or “returns.” This is consistent with findings from quantitative studies in behavioral science that emphasize amounts lost.

The qualitative study in Illinois explored how behaviors, motivations, and barriers around taxes and government benefits could influence which introductory messages an individual prefers when learning about a new state tax service. The findings suggest that “one-size-fits-all” messaging was generally less effective than more tailored approaches. Given a range of sample text messages, nearly every participant selected at least one message that corresponded with an archetype reflective of their screening responses and many also chose messages that spoke to secondary motivations, highlighting the value of segmentation in communication design.

Participants in our Illinois study reflected on how the test messages they received seemed to cater to their unique needs:

“They were direct and used the right tone. It’s like they are helping me out instead of just giving the message.”

“[The message] felt relevant to me considering I pay to get help with my taxes, so I’m definitely interested in learning about the easier way that is free.”

Timing mattered, too. Many people in our interviews said they wanted to learn about tax-related opportunities early in the fall—before commercial tax preparers start calling, and to give them plenty of time to learn about the program ahead of the next tax season. They also suggested syncing with tax season to provide actionable reminders, which could be especially helpful for those less familiar with the system and have also previously been shown to make a difference in increasing filing.

In addition to motivations and timing, our survey highlights the central role played by trusted messengers. The survey revealed that people turn to a range of sources when learning about government benefits and tax credits, and, on average, the most utilized channels for gathering information were:

- Friends, neighbors, or family (49 percent)

- Google or other online searches (48 percent)

- IRS website (42 percent)

- In-person preparers (38 percent)

- Online tax software (25 percent)

Importantly, people reported turning to multiple sources: On average, people named at least three trusted sources, underscoring the importance of multi-channel outreach. As one survey respondent put it:

“I decipher information from a combination of places before making a decision.”

For most, trusted messengers are personal—a friend who’s done their taxes before, a daughter who keeps up with tax rules, or a family member who works as a preparer. Participants in the nationwide survey valued these sources for their trustworthiness, accessibility, and shared lived experience:

“My son helps me, and I trust him.”

“My friend does them for me because I can’t afford a preparer.”

“The answers I seek come from trusted friends and people in the community…because I see them regularly, and they know what’s most helpful for me.”

“My friends and family would not lie to me. So I trust their recommendation.”

Even among those who used official or professional services, trust was closely tied to experience and relationships. In-person tax preparers were valued for their qualifications, personal reputations, and the sense of being in safe hands:

“I’ve known the woman for most of my life. She’s a CPA.”

“They are nonprofit organizations, so I trust them.”

“I trust the tax people [unions, worker advocacy groups, and local tax prep support] more than the ones online.”

“Tax preparers are a good legal source…I like the online options, but I just don’t feel confident doing it myself.”

Tax software and online platforms also earned trust—particularly among regular filers—because of their ease of use, error detection capabilities, and clear language:

“It flags my errors.”

“They know what they are doing, and I trust them.”

“They are a legit business, and their information is easy to read.”

“They are all accredited companies.”

Many saw official sources like mail or flyers from the government as reliable simply because they were official:

“I like to go directly to the source.”

“It’s my government, and I trust them highly.”

“They’re not trying to sell me something.”

“Because it’s the only place to get this information.”

While mail and flyers from the government were less commonly cited overall (12 percent), those who did receive them were more likely to have claimed tax credits (nearly 70 percent said they had claimed credits).

Some families in the Illinois study highlighted barriers to receiving physical mail and wanted reminders through email or text, especially if they had moved or lacked stable housing. Survey data reflected these preferences: 57 percent of respondents preferred communication by email, 47 percent by mail (primarily those 44 and older), 35 percent by text message (more common among those under 44), and 24 percent by phone call. On average, people selected 1.6 communication preferences, suggesting that most wanted to receive information through more than one channel.

“Mail and email, in case something gets lost.”

“It’s tricky because sometimes I don’t get the mail. If I don’t get the mail, I didn’t get that redetermination in time. Then, I have a breach in my food stamps…it might be double trips to the food pantry. They don’t send you email reminders…I like text reminders…or even if they just post it on the website.”

Some in the Illinois study also noted a lack of faith in being given flyers in person at local state offices.

“I feel like if the flyer’s not right there on their desk, they might not give it to you. I’ve been in the office and seen really valuable information just sitting on someone’s desk, or posted on a bulletin board where no one notices it. If you don’t happen to see it or it’s not handed to you, it’s just good information going to waste.”

Through our Illinois study, we also heard that many families were learning about government benefits more broadly from schools, early intervention specialists, medical providers, libraries, or local community organizations. Of the survey respondents, 14 percent mentioned local community centers, libraries, or local events as trusted sources of information.

“I tend to do it alone because I don’t want to pay that $400 or $500 tax preparer fee. But usually, I get help from the library or something like that. Or use a free website. Or try to call as much as I can when I’m not understanding something.”

Ultimately, people don’t absorb tax information in isolation. They interpret it through trusted messengers, layered sources, and personal thresholds for effort and risk.

Recommendations for Implementation

Tailor Messages to Real-Life Motivations

Effective messaging must reflect how people actually seek information and make decisions.

To improve credit uptake, outreach must feel relevant, trusted, and empowering. That means moving away from one-size-fits-all campaigns. Notably, no one in our interviews said they were overwhelmed by too much information; more and well-placed outreach is not only helpful but welcome.

Outreach strategies should reflect how people learn and validate information—through a mix of formal and informal, personal and institutional sources. Within these message delivery channels, the content should also be relevant to varying barriers and motivations. Taxpayers and credit-eligible families benefit from hearing messages in multiple places and from multiple messengers.

Effective outreach looks like:

- Partnering with trusted messengers. Tailored, culturally relevant messages resonate more than one-size-fits-all campaigns. Collaborate with local organizations, tax preparers, and accountants in under-filing ZIP codes; use Google Ads; leverage state Department of Revenue (DOR) websites; and partner with non-DOR benefits agencies to reach people where they already are. Messaging should be simple, repeatable, and ideally reinforced by sources families already trust.

- Tailoring messaging to behavioral archetypes. Filing and claiming behaviors are governed by distinct fears and motivations. Outreach efforts should either (1) cover a range of concerns in a single campaign to reach multiple archetypes at once, or (2) tailor specific messages to match the audience you are speaking to. For example, an outreach campaign through human services agencies might prioritize alleviating fears about losing benefits, while outreach through workforce development centers could emphasize financial gain.

- Using more than mail. Many families miss or never receive physical mail, or prefer more than one mode of communication. Supplement mailed communications with email or text reminders, and post updates directly on agency websites and benefits portals.

- Reaching out early and often. Government communication should be simple, timely, and consistent. Start sharing tax credit opportunities in the fall, ahead of the next tax season, and before commercial tax preparers begin heavy marketing, to give families time to understand all their options.

If we want more people to file and claim the support they’re eligible for, tax outreach needs to be more than a one-time message or announcement. It should be part of an ongoing relationship built on consistent timing and consistent messaging.

II. Applying: Application and Eligibility

Even when people are aware of tax credits, requesting support presents its own set of emotional and procedural barriers, and the ultimate filing action is intimidating and complex.

Many Fear an Honest Mistake on Their Tax Return Could Lead to Serious Consequences

For many people, filing taxes and claiming tax credits doesn’t just feel complicated; it feels risky.

“If you mess up, you can go to jail.”

—Survey respondent, <$10,000 annual household income; hadn’t filed taxes in three years

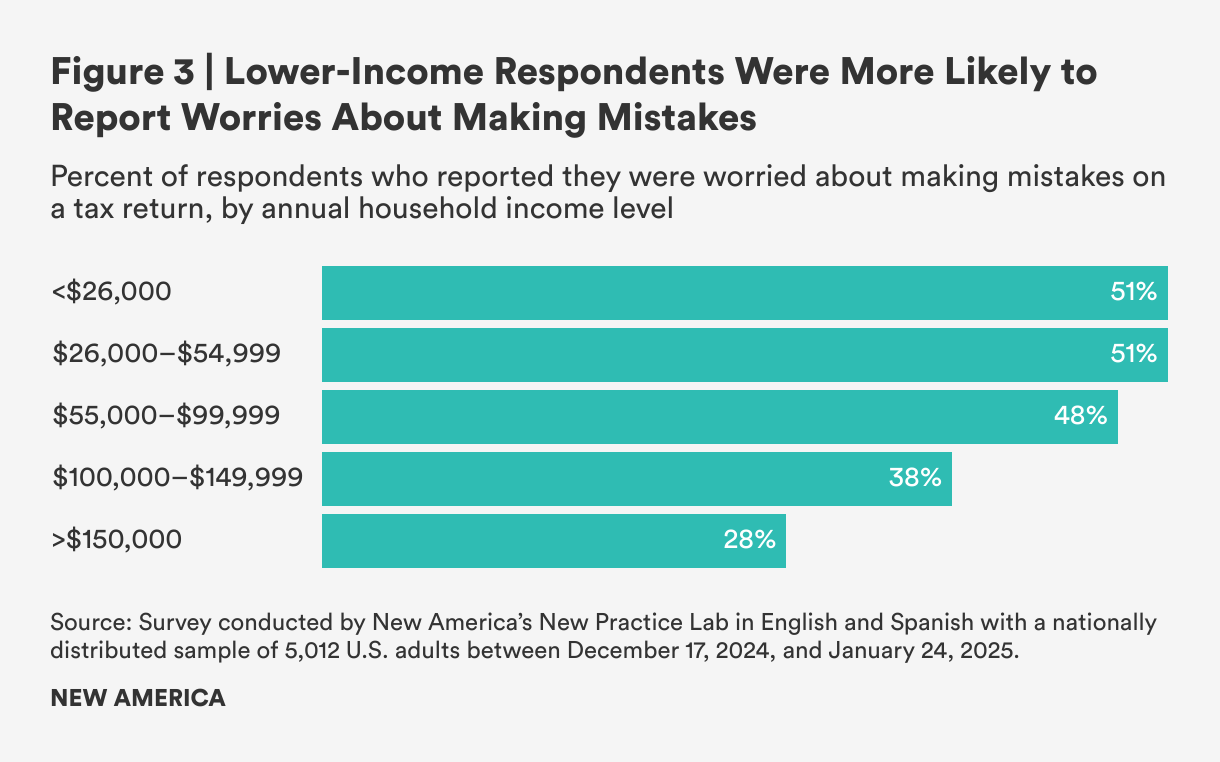

Across the country, people shared a common fear: that a simple mistake on their return could lead to penalties, audits, or even legal trouble. In our survey, more than half of the respondents identified the fear of making a mistake as a barrier to filing. This fear was especially acute among lower-income households: 51 percent of households earning under $26,000 cited it, compared to just 28 percent of those earning over $150,000 annually.

These fears have real consequences: 61 percent of respondents who were afraid of making mistakes had not filed taxes in the past three years. Even when they did file, they were more likely to miss out on tax credits (44 percent of people in this group said they had claimed tax credits before, compared to 55 percent of those who didn’t share this fear).

“I wasn’t properly taught how to do anything, and I don’t know where to begin. I’m scared I’ll do something wrong and be penalized for an honest mistake.”

“A friend I helped to file their taxes was afraid to claim any credits because he hadn’t filed since 2013.”

Overall, about one in four survey respondents (27 percent) said they found it difficult to file taxes because they had multiple income sources or jobs. While this number is not meant to represent all taxpayers, it signals a significant implementation barrier for credit access—especially as gig work and nontraditional income become more common. Sixty percent of gig workers and 54 percent of self-employed respondents reported being afraid of making mistakes. When asked about challenges they faced, gig or freelance workers shared that managing expenses and earnings was difficult:

“Complexity of gig work…tracking receipts, mileage, etc., makes taxes hard.”

“I’m not great at math.”

“When I work gigs or am self-employed, I have to report my earnings for taxes multiple times a year. It’s hard and confusing.”

Reducing perceived risk, especially for those with non-W-2 income, is essential to improving participation and ensuring that those who qualify for support can confidently claim it.

Others shared how disconnected they felt from the tax system altogether:

“I’ve never really done taxes because I’ve always worked in construction, and people get a better deal when they pay cash.”

“Honestly, it’s been a very long time since I filed because for a lot of my younger years, I was terrible at keeping a job.”

This isn’t just a technical issue; it’s an emotional one. In a system that often assumes individuals are tax experts, or requires them to navigate complex rules and jargon on their own, the fear of getting it wrong can quietly and powerfully shut people out from critical support.

Filing Feels Too Complex to Do Alone, but Help Is Too Expensive

Filing taxes is supposed to help people access the money they’re owed, but for many, it comes with a price: in time, energy, or dollars they can’t spare.

The cost of filing was another commonly cited barrier to claiming credits: 36 percent of survey respondents identified cost as a barrier. For many, the decision to pay for tax help was driven not just by convenience but also by the fear of making a mistake. The desire for professional support often reflected a lack of confidence in navigating the process alone.

“I would like to e-file without using TurboTax so I could do it totally for free and not spend part of my refund on it, but I’m scared I’ll get it wrong.”

—Survey respondent, living in a household with two children; $10,000–$25,999 annual household income; filed every year for past three years

For low-income families already navigating instability, even a $40 software fee or a few hundred dollars for a preparer can mean choosing between filing and meeting a basic need.

“I had to skip paying my January electric bill in order to buy tax software.”

—Survey respondent, married with two children and working as a gigworker/freelancer; $10,000–$25,999 annual household income

“It’s like a mortgage payment.”

—Illinois study participant, a veteran, describing the cost of a tax preparer

“Taxes have to be on pause…there were so many years during the pandemic when there was so little work. You know, people have to eat. So the debt got big, and we’re still paying it off.”

—Illinois study participant, a mother and unpaid caregiver

Despite the cost, most survey respondents used professional tax help at some point. Of those who had filed in the past, 70 percent reported using a preparer, 15 percent filed on their own, and 16 percent filed with help from friends or family. Of those who filed on their own or with help from family or friends, 22 percent mentioned that they had done so because they did not know that free or cheap tax preparation services were available.

Those who used services like TurboTax (58 percent), H&R Block (36 percent), or IRS Free File (17 percent) appreciated the convenience, and over 90 percent said they would use a tax preparation service again, even though affordability still came up again and again as a barrier.

“It was hard to find completely free filing anywhere.”

—Survey respondent, a single parent with one child under six; $10,000–$25,999 annual household income

“Certain websites I’ve tried…like Credit Karma where everything was completely free, but you did everything yourself. It wasn’t like doing TurboTax online, where they help you a little bit.”

—Illinois study participant, a father and warehouse worker who filed taxes inconsistently

And even though many relied on tax preparation services for their ease of use and built-in error detection, 21 percent still ran into problems. Among those who reported issues with their tax prep experience:

- 28 percent said they had been charged unexpected or high fees

- 15 percent could not access free filing support despite seeking it

- 15 percent were encouraged to open financial products (e.g., refund anticipation loans or advance refund loans) that reduced their refund

For some, it just didn’t feel worth it. Respondents described skipping tax filing altogether because the effort or cost didn’t seem justified by the refund they expected. When filing feels complicated, and the financial return is uncertain or minimal, some decide it’s not worth the trouble.

“I had a CPA do them three years ago…paid $200, got a $28 refund.”

“I would love some help in claiming my tax credits for EITC. Figuring out the details is not worth the time and effort against the small amount of tax credits I might be able to claim.”

“It’s not worth it to go through the trouble to pay someone to do it if you don’t get much back.”

A third of respondents (34 percent) said they struggled to understand tax instructions or found the language too technical. This difficulty wasn’t due to a language barrier: 98 percent of respondents said they had accessed tax materials in their preferred language, even among those who found the jargon hard to follow.

“Don’t have all the correct W-2 forms or whatever they’re called…it’s too high-class, written for only college people, not for the blue-collar workers.”

“I don’t understand a lot of the questions being asked.”

“You have to learn the laws and the new rules and regulations each year.”

“I have a form of dyslexia with numbers. I don’t make enough money to pay someone to do them professionally.”

Of those surveyed, 27 percent of respondents mentioned that they found it difficult to file taxes because they had multiple income sources or jobs, and 25 percent did not know how to report self-employment or gig income. People shared how hard it was to know which documents were needed, what qualifies as income, or whether they’d done things correctly.

“This year is going to be difficult because I’m now self-employed, and I have no idea what I need or if I’ll even qualify for my child tax credits.”

—Survey respondent, living in a household with two children; $26,000–$54,999 annual household income; had filed every year for the past three years

Parents in the qualitative study in Illinois also mentioned that using online tax software like TurboTax helped them be more aware of tax credits. The platforms guided them through eligibility questions and clearly showed whether credits were applied.

But for those who filed on their own or with less-guided tax software, claiming credits required knowing exactly what to fill in, and many didn’t.

“I may not claim credits if I file without a professional…not sure whether or not I could get some sort of legal trouble for claiming something falsely—accidentally, of course.”

—Survey respondent, a single parent of three; unhoused; $10,000–$25,999 annual household income

Documentation and Identity Verification Challenges Block Filing

“I don’t know if I’m going to file that this year because I don’t really understand the 1099 form or know how or where to get it…it’s different from a W-2. Completely different.”

“I was homeless…my tent got flooded. I lost everything.”

For many, the filing process didn’t just feel expensive or difficult; it felt inaccessible. The act of filing breaks down not just because of technical tax forms or costs, but because people lack the documents, access to technology, or verification tools they need to even get started.

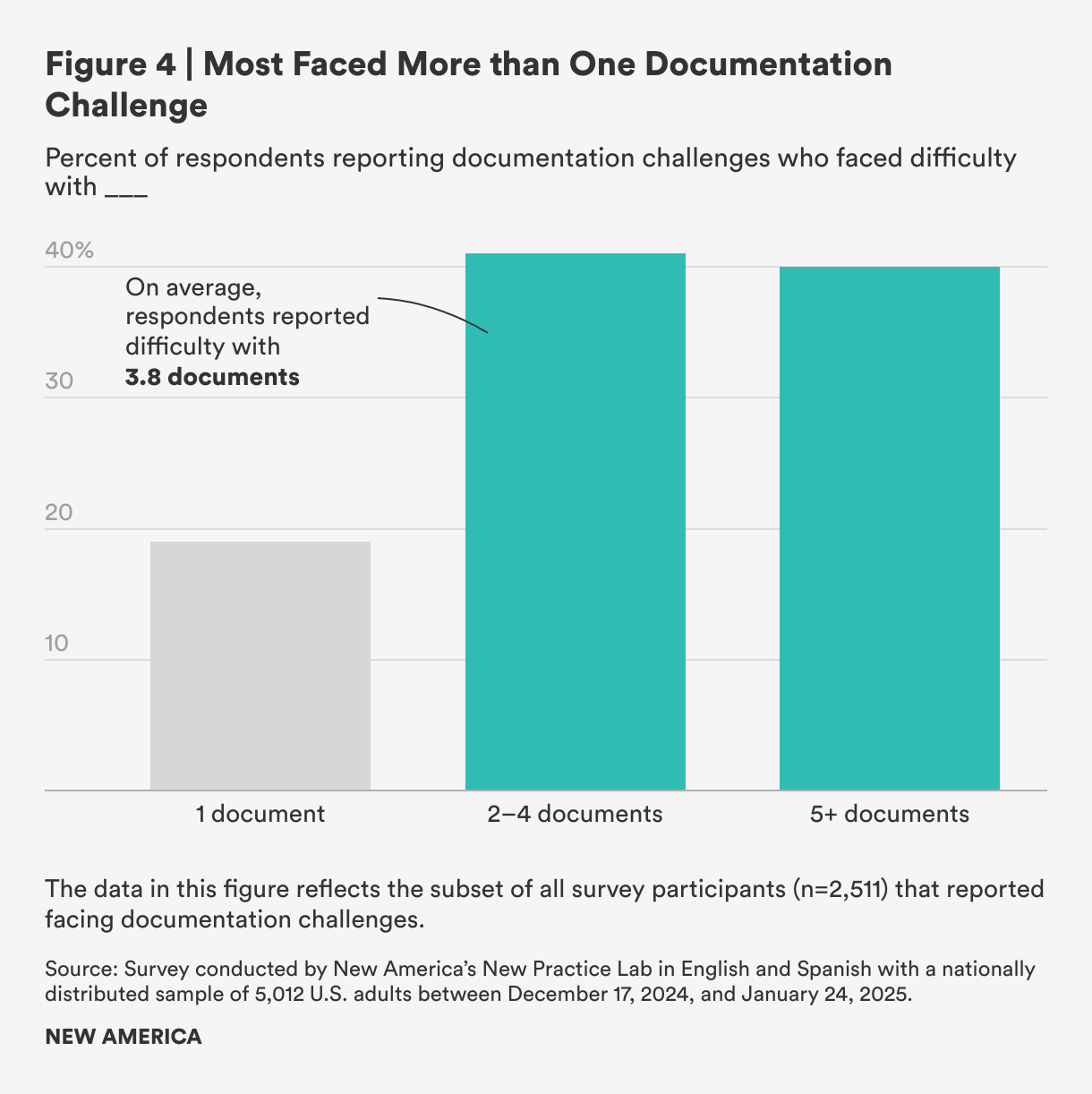

Fifty percent of respondents said they had trouble gathering documents. The most common challenges with documentation were missing wage documents (40 percent), missing proof of Social Security or Tax ID numbers (37 percent), difficulty documenting expenses (36 percent), missing or incomplete banking or financial information (33 percent), and difficulty documenting non-wage income, such as earnings reported on a 1099 (32 percent).

Crucially, of those who mentioned facing documentation challenges, 80 percent faced challenges with more than one document type (reporting challenges with 3.8 documents, on average), suggesting that these issues are layered rather than isolated incidents.

“Too much paperwork, too many questions. I don’t have any of my receipts from a couple of years back, and I don’t know how to file my taxes.”

—Survey respondent, living in a household with two children; hadn’t filed taxes in three years

Others told us about lost or expired IDs, difficulty obtaining or locating a spouse’s death certificate, or records destroyed in extreme circumstances—like the respondent who was living in a tent when a flood destroyed their paperwork.

Approximately 15 percent of survey respondents reported identity verification issues when trying to file. Among those who faced this challenge:

- 34 percent struggled with navigating ID.me

- 22 percent encountered mismatched records, such as outdated addresses, name changes, or incorrect Social Security numbers

- 20 percent couldn’t proceed because of errors on prior tax returns

- 20 percent said they simply did not have identity documents

“You have to wait to see if it’s accepted or rejected. I’ve been rejected about eight times! It was for something simple, like a wrong digit on my Social Security number. I didn’t understand what I was doing wrong…I called the IRS a few times and they finally explained it.”

—Illinois study participant, a mother and a part-time paid caregiver; had filed taxes inconsistently

Digital access was another limiting factor: 12 percent of respondents said they lacked access to a reliable computer or internet. People also mentioned that their phones had been stolen, their accounts were locked, or that they lacked a permanent address to receive or store tax documents.

“I couldn’t get my W-2—they were done digitally, and my phone was stolen. I’ve never been able to recover my account and don’t know how to proceed with filing my taxes.”

—Survey respondent, living in a multigenerational household with three children and one elderly dependent; $55,000–$64,999 annual household income; hadn’t filed taxes in three years

Recommendations for Implementation

Reframe Filing as Supportive—Not Punitive

“I want to be able to have that reassurance that I can come back to this…and say, “Hey, this wasn’t right,’ and they can double-check…and say, well, ‘Let's fix it together.’”

Perception matters. State Departments of Revenue (DORs) can help reduce fear and build confidence by shifting the tone of their communications and making it clear that trusted support is available.

Instead of focusing on enforcement, penalties, or compliance in outreach to economically vulnerable households, messaging should highlight the resources available to help along the way—like tax assistance centers, free filing tools, and clear sources of information—and focus on the real, tangible benefits of claiming tax credits, such as help with food, housing, or child care. While most state DORs may not have the capacity to coach people through their taxes directly, there are small, meaningful ways to ease anxiety and help people feel safer navigating the system.

How state DORs can reduce fear and build confidence:

- Emphasize financial support, not penalties. Make it clear that filing is an opportunity to access resources for low-income households, not just a legal obligation.

- Normalize mistakes. Communicate that the system allows for learning and correction. Filing shouldn’t feel like a one-shot test. Small missteps happen, and they can be fixed.

- Improve tone and clarity. Review and revise common messages (like error alerts, follow-ups, or help prompts) to be plainspoken, clear, and reassuring rather than intimidating.

- Offer simple guidance on common errors. Even one-pagers and short FAQs on frequent mistakes can help people feel more confident, especially if these are available early in the filing process or shared proactively.

- Include actionable links to resources. Provide links to free state-verified filing tools, community organizations, nonprofits offering tax assistance services, or even maps showing nearby Volunteer Income Tax Assistance (VITA) center locations—reinforcing that help exists and no one is expected to do this alone.

- Train frontline staff, community partners, and adjacent benefits agencies to reinforce supportive messaging. Many people are more comfortable asking questions in familiar spaces. Equip trusted intermediaries with talking points that reflect this tone.

By treating mistakes as normal and solvable and framing filing as a gateway to critical support (not a trap), states can make tax filing feel safer, more approachable, and more worth it for the people who stand to gain the most.

Expand Access to Tax Credit Options

Even with free and simplified tax filing tools, many low-income households face steep barriers to accessing tax credits. For these low-income households, especially those below the federal threshold for filing, the process of claiming credits like the Earned Income Tax Credit (EITC) or Child Tax Credit (CTC) should not require completing a full tax return.

Instead, states can design streamlined pathways that meet people where they are, using only the minimum information needed to verify eligibility (e.g., income, household size, or dependent status). This approach can:

- lower the barrier for people who aren’t otherwise filing

- reduce the risk of incomplete or inaccurate filings just to access benefits

- create a stronger safety net for those with the least financial and administrative bandwidth

Some public benefits programs have used simplified application processes:

- In April 2020, the IRS launched a non-filer tool to provide Economic Impact Payments (EIP) more quickly to those who did not have a return filing obligation, including those with too little income to file.

- The Supplemental Nutrition Assistance Program (SNAP) has introduced the Elderly Simplified Application Project (ESAP), which helps adults 60+ and those with disabilities by removing barriers to recertification—waiving interviews and using data crossmatches to verify eligibility—making it easier for vulnerable participants to maintain access to food benefits.

- The temporary 2021 Advance Child Tax Credit also demonstrated how tax benefits can be delivered proactively: Most eligible families received monthly payments automatically if they had filed taxes in 2019 or 2020 or used the EIP non-filer tool. Others could enroll through a simplified online portal designed specifically to help previous non-filers access the credit with minimal paperwork.

States can look to other proactive models. For example, in 2019, the Illinois Department of Revenue (IDOR) piloted a proactive and simplified approach to help eligible households access tax credits. It identified residents who had claimed the federal EITC, but hadn’t filed a state return and likely qualified for the state EITC. Rather than requiring a full return, IDOR offered a simple, secure pathway for people to claim their credit. The pilot helped over 22,000 Illinoisans access refunds and has since been integrated into the state’s regular workflow.

When combined with free simplified tools such as Direct File, these delivery choices can reduce administrative burden and increase critical tax credit access among low-income households.

States don’t need to overhaul the entire system to make progress. They can start by building flexible, lower-friction alternatives for economically vulnerable households most likely to benefit.

Support Through Tax Credits Shouldn’t Depend on Perfect Paperwork

Simplified filing has gained much-needed momentum in recent years—particularly efforts to pre-fill income using employer-reported wage data. About 20 percent of our survey respondents said they had trouble accessing their W-2s or wage information, and for this group, prefilled income data could make a meaningful difference in helping them access tax credits.

But for most, income reporting wasn’t the only or biggest hurdle. Eighty percent of respondents who faced documentation challenges dealt with far more complex issues: expired or missing IDs, identity verification problems, locked accounts, trouble tracking expenses, or paperwork lost during housing instability. These barriers can prevent people from completing the filing process, even if their income is correctly prefilled.

Simplifying access to wage data is one important piece of the puzzle, but it is not a silver bullet. To truly expand access, we need filing pathways that work even when paperwork is incomplete or hard to retrieve.

These could include:

- Simplified forms for accessing credits that gather only critical items needed for credit determination for low-income households that are not required to file taxes

- Opt-in programs that use existing state data, such as health and human services information, to estimate eligibility and conduct outreach to the right individuals (see next section)

- Partnerships with trusted intermediaries (like local caseworkers) who can help verify information

- Additional ID verification options, such as using documents already submitted in the past or to state benefits programs, or enabling in-person or video-based verification through community organizations

These approaches aren’t intended to replace full tax returns for most taxpayers, but they can help low-income households currently locked out of the system even when they are eligible for support.

III. Receiving: Delivery and Access

For those already engaged with public programs, existing touchpoints—like recertification or caseworker interactions—offer trusted opportunities to share information about tax credits and help families access what they’re eligible for.

Tax Credits Feel Disconnected from Other Government Support

Many low-income households are already connected to government programs, but credits through the tax system often feel separate from other supports they rely on.

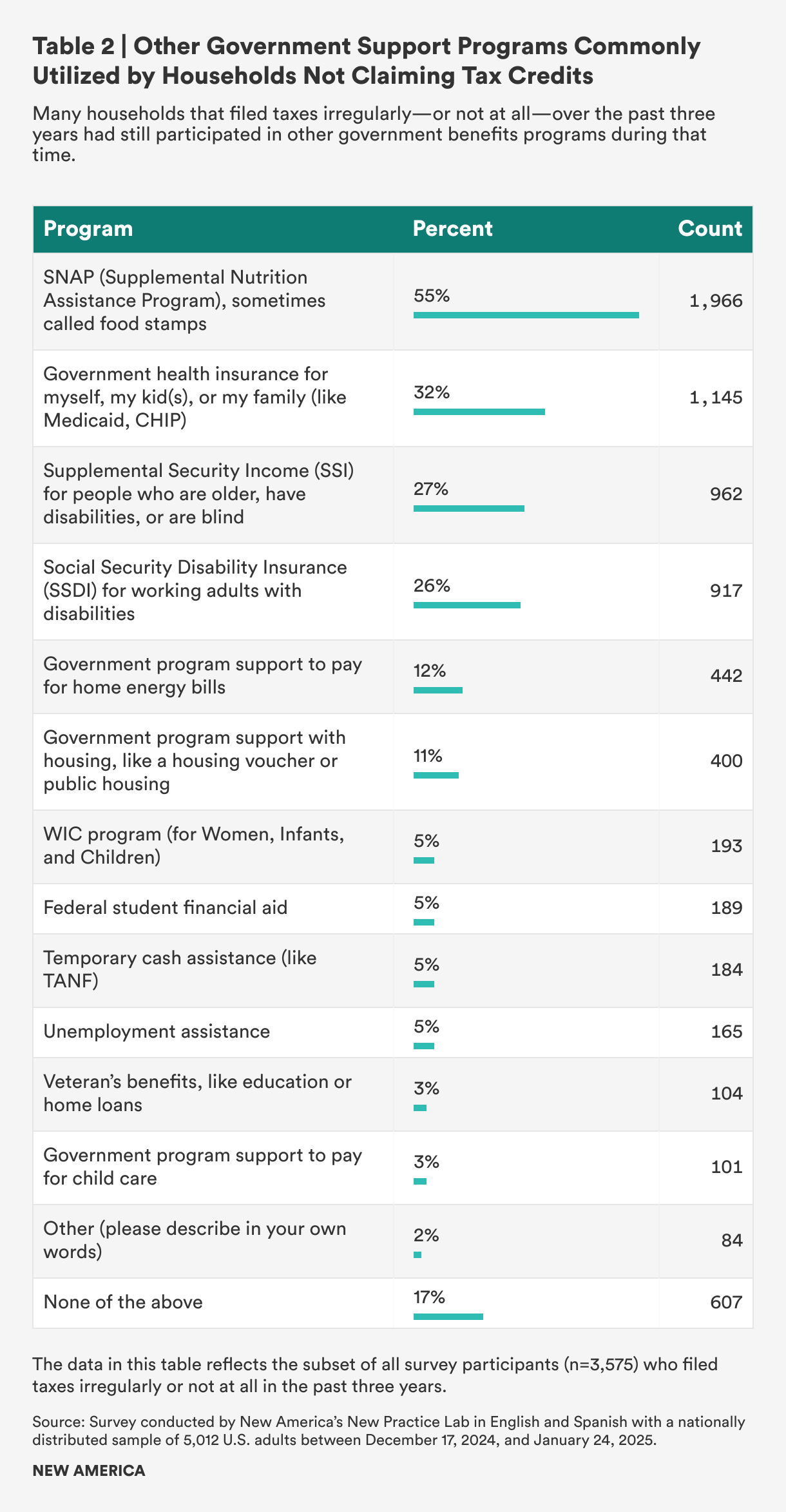

Of households who had not filed taxes at all or irregularly in the past three years, 84 percent had participated in at least one other government support program during that time period. On average, respondents (or someone in their household) had participated in 1.7 government support programs over the past two years, with participation highest among those who had not filed taxes at all (two programs on average).

“The information’s already in the system because of SSDI and SNAP. Why can’t they just file for me?”

Commonly used government support programs among households that did not file or filed taxes irregularly included:

- Supplemental Nutrition Assistance Program, or SNAP (55 percent)

- Government health insurance (32 percent)

- Supplemental Security Income, or SSI (27 percent)

- Social Security Disability Insurance, or SSDI (26 percent)

- Home energy bills (12 percent)

- Housing support (11 percent)

In both survey responses and interviews, many households expressed interest in getting help with filing to alleviate stress or simplify the process. One idea that we presented in our interviews in Illinois and re-tested in the survey was a process that could prefill parts of a tax return using information already provided to other state agencies, with the filer reviewing and approving it before submission.

Overall, 70 percent of all respondents said they were either very (36 percent) or slightly (34 percent) interested in this kind of support. Interest rose significantly among those already interacting with multiple government support programs:

- 62 percent interest among those with no other program participation

- 71 percent interest among those participating in one to two programs

- 81 percent interest among those participating in five or more programs

Respondents wanted agencies to use the data they already have to reduce administrative burden and simplify access. While the rising interest with higher participation may suggest greater comfort, trust, or familiarity with agencies connecting them to benefits, it could also reflect fatigue from repeatedly providing the same information across multiple systems to “the government” as a single perceived entity.

Respondents told us it would save time, reduce anxiety, and build confidence:

“ANYTHING filled in for me would be amazing during such a stressful time.”

“I have bad anxiety about forms, this would relieve stress.”

“The government already has the info. Why not use it?”

For some, the idea was appealing only when introduced by agencies people already trust—like their SNAP office or a known caseworker:

“If my taxes were to be prefilled by the county building where I received my SNAP and CalWORKS benefits I wouldn’t mind it at all. They already know what I make so it only makes sense that could help with the pre-fill tax form.”

“That’ll be wonderful because it would be confidential with someone you’re talking to at a program you already know…And like I said, with the cost of living right now, anything helps.”

At the same time, not everyone was on board. About 17 percent of respondents said they wouldn’t be interested, and another 12 percent were unsure. Concerns ranged from distrust of government systems to fears about mistakes and scams:

“I don’t trust the government to get my info right.”

“One more place things could get messed up.”

“Could be a scam, I wouldn’t be sure.”

While fully pre-filled tax returns may not be widely feasible in the near term, the strong interest we heard points to a broader need: People want simpler, more supported filing experiences, especially when introduced by trusted sources like SNAP caseworkers or local community organizations.

Small, actionable steps can still make a big difference: Using known data to pre-populate income or household size in reminder notices, or sending personalized prompts like “You may qualify for $X in tax credits,” can lower the barrier to filing.

The goal isn’t to do everything at once—it is to offer help that feels familiar, reliable, and easy to act on. Trust, familiarity, and control are essential ingredients for effectively reaching people.

Recommendations for Implementation

Integrate Tax Credits into Support Families Already Receive

Most low-income households are already connected to public programs like SNAP, Medicaid, or housing assistance. These agencies have regular, high-touch interactions with families and are seen as trusted sources of support, making them a powerful starting point for accessing tax credits.

States can take a “crawl–walk–run” approach to help households see tax credits as part of the broader benefits system and streamline access, starting with simple, actionable steps that are already within reach:

- Introduce the Department of Revenue (DOR) through trusted partners. Equip trusted benefits agencies to give families a simple heads-up: “You might hear from the DOR about tax credits you may be eligible for.” Even this small touchpoint can reduce skepticism and increase familiarity.

- Use existing benefits data to trigger targeted outreach. Agencies can use existing (if incomplete) data to verify tentative eligibility and send personalized messages like “You may be eligible for $X,XXX in tax credits” based on known income and household data.

- Build secure data-sharing agreements. Trusted agencies can play a critical role in helping households connect data they’ve already provided with the DOR, even if the original agency a family is connected to isn’t managing credit delivery itself.

This coordination doesn’t require perfect eligibility matching or full integration across systems. In fact, what we’ve heard in past state engagements is that non-DOR agencies are often hesitant and don’t have the capacity to manage tax credit delivery directly. However, they can still be powerful bridges, helping DOR become a more trusted and familiar face and a member of the broader support system.

Ultimately, coordinated outreach is just one piece of the puzzle. To create truly connected and accessible support, infrastructure and policy must evolve in tandem:

- Align eligibility criteria across programs. Programs often use different rules for determining eligibility (like income cutoffs or household composition). Aligning these criteria across benefits (such as syncing SNAP and state Child Tax Credit income thresholds) can make cross-agency coordination easier and more accurate.

- Establish clear, limited data-sharing agreements between agencies. Limit the type and amount of personal data shared across agencies to only what’s necessary to verify eligibility (e.g., income range or number of dependents). Include clear language on how data will be used, stored, and protected, and ensure that individuals are informed when their information is being shared, including for their benefit.

- Give people control. Transparency builds trust. Allow individuals to opt in to receive help with tax credits using their existing benefits data. Make clear what data is being used and for what purpose.

Even modest steps toward this—supported by aligned eligibility, inter-agency trust, and privacy safeguards—can open new pathways for delivering tax credits in ways that feel safer, simpler, and more connected to the public programs families already rely on. Done well, this can also reinforce the idea that tax credits are part of the broader system of support for families.

Rethinking How the Tax System Delivers Essential Support

There’s growing urgency and opportunity to rethink how we deliver financial support to the families who need it most. Tax credits like the Earned Income Tax Credit and Child Tax Credit are meant to provide critical relief, helping people cover essentials like housing, child care, and everyday expenses.

Yet today, accessing that support often requires navigating a tax system that feels confusing, unfamiliar, or risky, especially for economically insecure households.

Households earning less than $65,000 a year are exactly the type of families that tax credits—through flexible, critical cash support—are meant to help. Yet these households are often the least likely to know the credits exist, to understand if they qualify, or to feel confident that filing taxes won’t create new problems. This isn’t a personal failure; it’s a structural one.

It’s worth asking: Should the tax system be the only way to deliver these benefits? Other programs like SNAP, Medicaid, and housing assistance already engage families through trusted, regular interactions. While these systems face their own challenges, they offer powerful entry points for connecting people to tax credits.

Filing through the tax system has real advantages: It combines compliance and benefits access into a single process. But when that process feels out of reach and complicated, it undermines tax credit delivery. Although simplification efforts like the IRS Direct File pilot are promising and urgently needed, access to critical support shouldn’t hinge solely on fixing the tax system.

If tax credits continue to run through the tax system, then the system itself needs to evolve. State Departments of Revenue must take on a broader role: not just enforcing compliance but proactively helping people access what they’re owed. That means simplifying pathways, coordinating with other programs, and showing up where families already are.

Ultimately, tax credits are only as effective as the systems that deliver them. And when those systems are designed with economically vulnerable families in mind, they work better for everyone.

Meeting the Moment with Meaningful Collaboration

There is no single silver bullet for increasing tax credit uptake. People choose not to file taxes for many reasons: Some correctly understand that they are not legally required to because of their income level, while others are deterred by fear, confusion, cost, complex life circumstances, or a lack of awareness that tax credits could make filing worthwhile. A one-size-fits-all solution won’t work. Increasing access requires a multi-pronged strategy that reflects how people actually live: personalized outreach that is relevant, timely, and delivered through trusted messengers; streamlined and connected systems; and policies that meet families where they already are.

Government leaders across state and local levels are already beginning to explore new ways to close the gap between policy and people. At the New Practice Lab, we’re eager to help accelerate that work. We’re partnering with states to pilot new credit uptake strategies, improve cross-agency data use, and design tools that make it easier for families to receive the support they are owed.

We’d love to connect with you if you’re a state tax agency or administrator interested in reimagining your role as a benefits provider. We’re also convening a small cohort of state Departments of Revenue to explore and test strategies for improving the uptake of credits like the Earned Income Tax Credit and Child Tax Credit. Whether you’re building from scratch or refining what’s already in place, this is a chance to learn together and identify what’s next.

Please reach out to npl_work@newamerica.org if you’re interested in collaborating or speaking with us.

Methodology

Nationwide Survey of 5,000+ Respondents

We conducted an online survey in English and Spanish with a nationally distributed sample of 5,012 U.S. adults between December 17, 2024, and January 24, 2025. The survey oversampled individuals from low-income households (88 percent had annual household incomes under $65,000) who either filed taxes inconsistently or not at all in the past three years.

All participants were between 18 and 64 years old, and responses were collected from all 50 U.S. states, Washington, DC, and the U.S. Virgin Islands.

We applied quota sampling based on age, household income, and tax filing behavior to ensure adequate representation of lower-income and inconsistent or non-filing households.

The final sample included:

- 63.7 percent who had not filed taxes at all in the past three years

- 7.6 percent who had filed inconsistently (some years but not others)

- 28.7 percent who had filed taxes every year

The sample included a racially and ethnically diverse group (with 7 percent of the respondents selecting multiple identities): 65 percent white, 25 percent Black, and 11 percent Hispanic/Latino, with smaller representation from Native American (3 percent), Asian/Pacific Islander (3 percent), and other (0.9 percent) backgrounds.

We implemented quality control measures through our survey partner, Qualtrics, including screening for duplicate or bot responses, detecting straight-lining behavior, randomizing response order where applicable, and removing responses completed in significantly less time than the average, which could indicate low-quality or inattentive participation.

Respondents were asked about:

- their households’ tax filing and tax credit claiming behaviors and experiences

- employment and family structures

- barriers to claiming tax credits

- awareness of tax credits

- trusted sources of information for tax and other benefits information

- participation in other government support programs

- comfort with data sharing and integrated service delivery models

Unless otherwise noted, all figures referenced in this article represent statistically significant findings from the survey and are calculated based on item-level response rates, not total sample size.

Qualitative Study with 25 Low-Income Residents in Illinois

In parallel with the national survey, we conducted a qualitative study with 25 low-income residents across Illinois between September 2024 and February 2025. This qualitative research aimed to surface emotional drivers, motivations, and lived experiences that shape how people approach tax filing.

Participants were primarily recruited through New America Chicago’s partnership with the Coalition on Family Issues (COFI), with additional outreach through community organizations, local Craigslist postings, and families in New America Chicago’s CivicSpace cohort.

The study included:

- Group discussions (two sessions): Hosted during regular COFI parent meetings, these sessions explored perceptions of a potential partnership between the state Department of Human Services (DHS) and the state Department of Revenue to improve access to tax credits. Participants raised concerns about access, prompting a deeper exploration of how past interactions with public agencies shape attitudes toward tax filing.

- In-depth interviews (in English and Spanish): One-on-one, semi-structured interviews with nine participants provided insight into how personal and family experiences with state benefits and tax systems influence filing behavior and credit awareness. Interviews explored familiarity with credits, sources of confusion or misinformation, and how previous public system experiences shape filing decisions. Participants represented a range of family structures and filing patterns across Illinois.

- In-person co-design workshop: In partnership with state representatives, a design session with 10 residents focused on co-creating messaging strategies and identifying optimal communication timing for a new tax service. The session emphasized collaborative problem-solving and centering participant voice.

- Messaging survey (in English and Spanish): Participants who had filed taxes at least once in the past three years were first assigned a behavioral archetype based on filing motivations and barriers. They were then shown a scenario involving a text message from DHS about a new tax service. From a set of 11 messages (both generic and archetype-tailored), they were asked to select up to three that resonated most.

Insights from this study informed the development and refinement of behavioral archetypes that represent distinct mindsets and patterns around tax behavior. These emerging archetypes are helping to inform our work on messaging, potential policy friction points, and approaches to more personalized support for low-income families.

More About the Authors

Devyani Singh

Data and Strategic Impact Lead, New Practice Lab

Issues

Programs/Projects/Initiatives

Related