Zachary D. Blizard

Data Analytics and Research Manager, Center for the Study of Economic Mobility

This analysis is part of a joint partnership between the Future of Land and Housing Program at New America and The Center for the Study of Economic Mobility (CSEM) at Winston-Salem State University investigating access to homeownership in Forsyth County, North Carolina.

“Wall Street is trying to buy most of the homes in the U.S.” — A real estate agent in Winston-Salem, North Carolina

“Hedge funds are essentially purchasing the homes that the middle class should be buying, and renting them back to them." — Another Winston-Salem real estate agent

The concerns voiced by these real estate agents in the local housing market of Forsyth County, North Carolina (where Winston-Salem is located) mirrors a national conversation about the impact of investors in real estate. Are Wall Street hedge funds, private equity firms and other large investors really purchasing homes in the U.S. at higher rates than ever before? Or is this mostly perception, fueled by an ultra competitive housing market amidst a nationwide lack of housing?

These questions are difficult to answer, in part because existing data sources make it challenging to identify real estate investors, and even more difficult to distinguish between different kinds of investors. As a result, existing metrics to assess investor activity in the housing market either lump all investors together, or use differing methods to identify investors, making cross-study comparisons difficult.

In this blog post, we use purchasing behavior to distinguish large investors from small investors, shedding light on trends and spatial concentration of large investor activity over the last 20 years. We focus our analysis on Forsyth County, North Carolina, though given how many housing markets are facing projected growth in rental prices (and thus exhibit profit-making potential for investors), this analysis can shed light on large investor activity in other housing markets across the country as well.

Investors have long had a presence in the U.S. housing market, but not all investors are created equal; they differ by size, motive and intended use. A unifying characteristic across investors is that they typically do not live in the homes they purchase, and instead purchase homes with an intent to "flip and sell" or to use as a rental properties.

Investors have historically been individuals or small companies that own one or a handful of homes, and for whom income from real estate typically supplements income from employment. But in addition to these ‘mom-and-pop’ investors, there are also large investors, often backed by institutional or private capital, who purchase housing as a long-term, profit-generating activity. Though large investor activity in housing markets across the U.S. became more pronounced after the 2007-2009 financial crisis, current housing market conditions indicate that large investors will likely continue to see financial returns from real estate investment.

Large investors have unfettered access to capital and can work at a scale and speed that exceeds that of the most savvy small investor or wealthy cash-buyer.

Large investors enjoy the same advantages as small investors–they can streamline the home purchasing process and circumvent many of the traditional hurdles, like appraisals and inspections. But because they are typically backed by hedge fund money or private equity, large investors tend to have unfettered access to capital and can work at a scale and speed that exceeds that of even the most savvy small investor or wealthy cash-buyer.

The concerns expressed by real estate agents on the ground in Winston-Salem, as well as the recent media focus, suggests that purchases of homes by large investors may be different and more pernicious than small investor activity. (For example, see recent reporting in the Wall Street Journal, The New York Times, and NPR.) Do bulk home purchases by large investors – oftentimes sight unseen – adversely impact the ability of low-and-moderate income buyers to purchase homes, especially when they are relying on mortgage loans? Are large investors driving up home prices and housing loss through eviction and foreclosure? And if so, how does this impact differ from that of small investors?

To address these questions, we first need to define what constitutes a large investor in a local housing market and then figure out how to identify these entities using available data. For this analysis, we developed our own method to identify large investors, and use it to assess trends and spatial concentration over the last 20 years. We outline our methods later in this post, but in short, we define large investors as those who purchased 5 properties in one year or 20 or more properties over 20 years.

Using our method to identify large investors, we investigate who is driving investor purchases in Forsyth County–large or small investors.

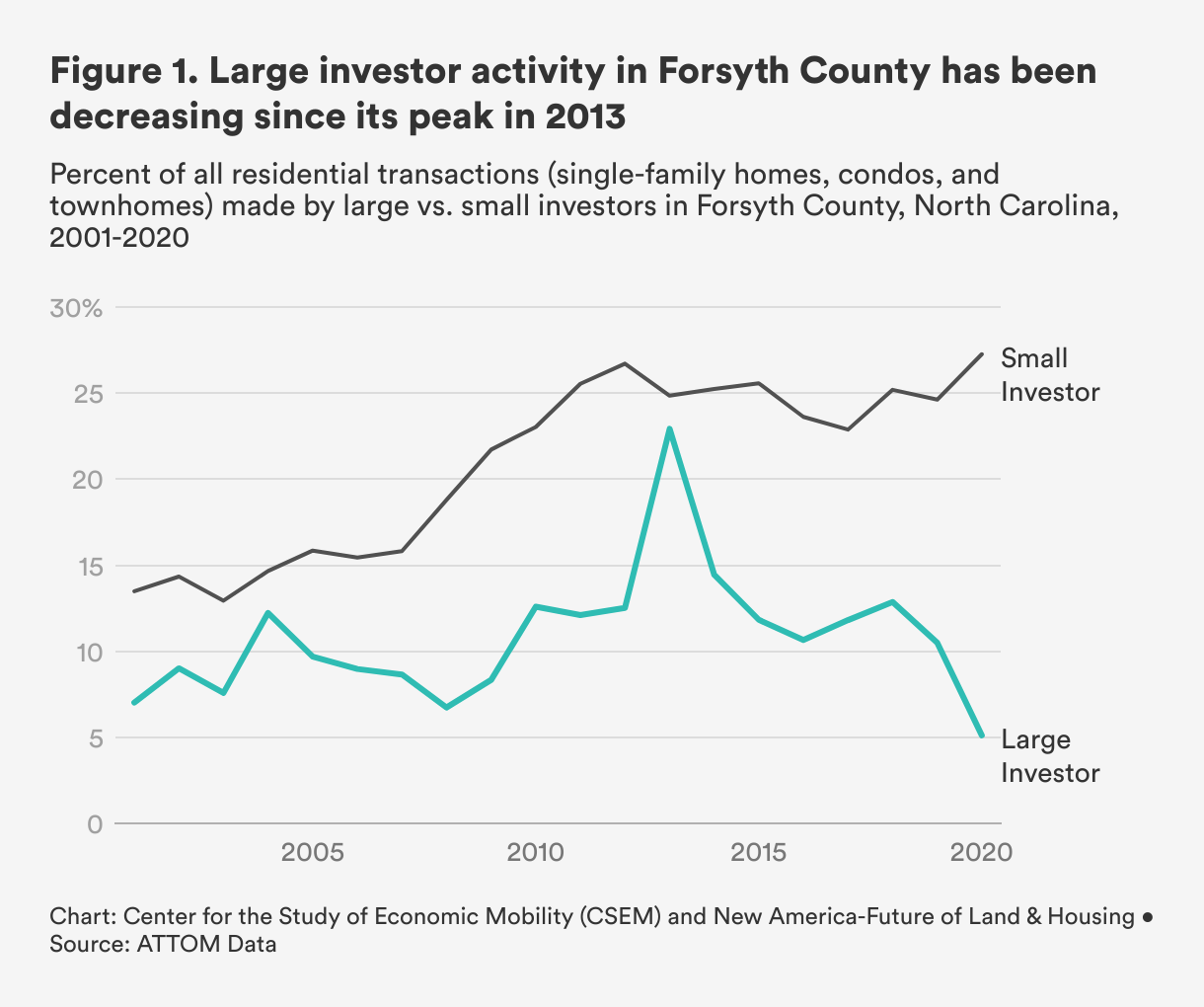

Figure 1 shows the percent of all transactions (for single family homes, condos, and townhomes) involving a large investor and a small investor between 2001 to 2020 in Forsyth County. In an average year over this 20-year time span, 9.7 percent of the homes purchased in Forsyth County were bought by a large investor, whereas 20.9 percent were purchased by small investors.[1]

Interestingly, the share of purchases made by a large investor has been steadily decreasing since its peak in 2013. In 2009, the percentage of large investors entering the local housing market jumped from 8.3 percent to 12.6 percent, and remained above 10 percent until 2020, when it dropped to a 20-year low (5.1 percent). This could be in large part to the COVID-era foreclosure moratorium; whether large investor activity resumes its pre-pandemic levels beyond 2020 remains to be seen.

The data reveals that large investor purchases in Forsyth County are still a small proportion of the housing market, especially relative to small investor purchases, purchases by wealthy individuals, and purchases by owner-occupants who are likely to use a mortgage. This suggests that the increase in investor purchases over time, shown in previous analysis, is likely not driven by large investors, but by individual investors and/or wealthy individuals.

Understanding the price of homes that large investors tend to purchase can shed light on who is most impacted by their presence–other investors or middle class families hoping to build wealth and lay down roots?

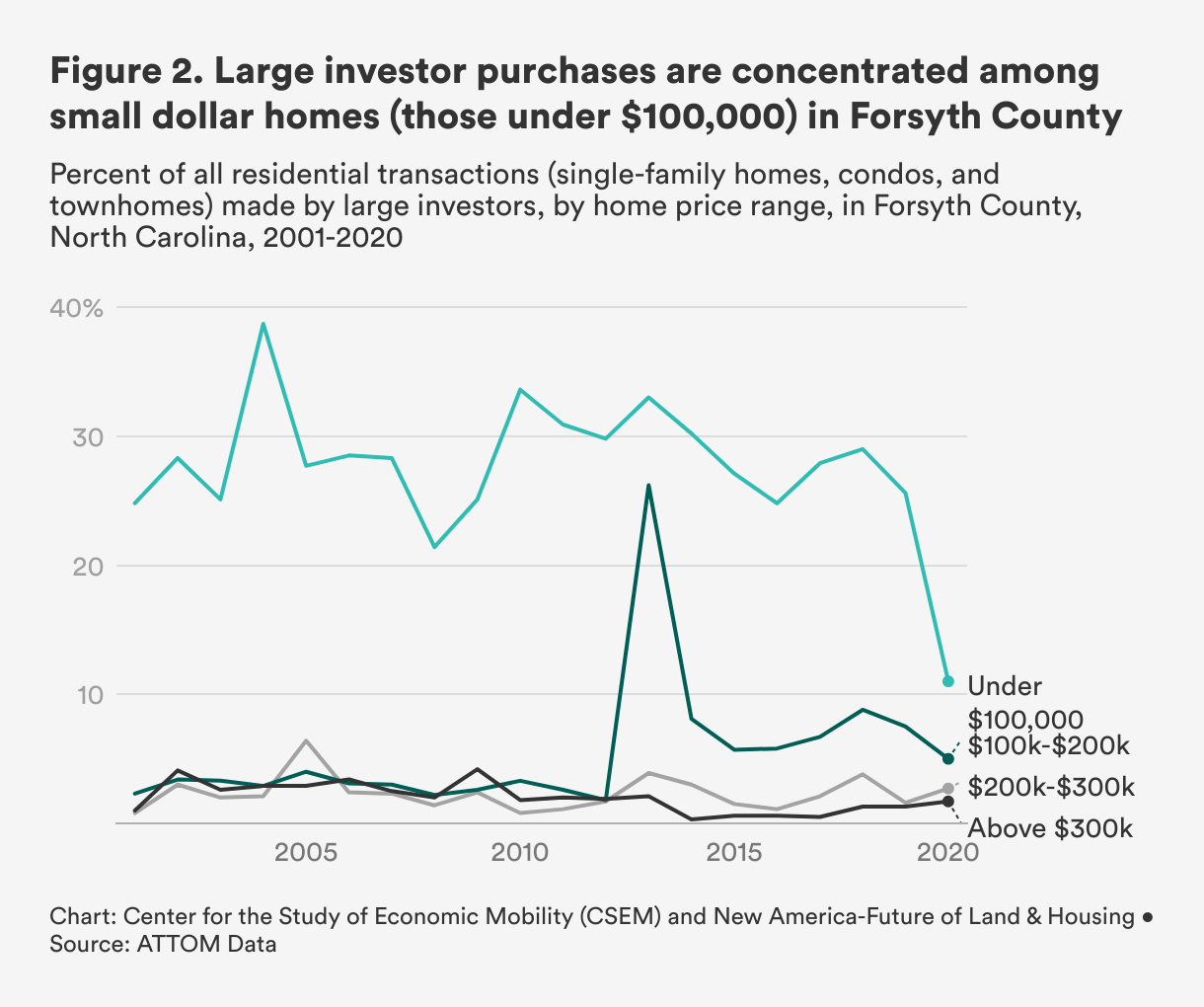

Figure 2 segments large investor purchases into four home price ranges, from below $100,000 to over $300,000. Over this 20-year period, we see that large investor activity is concentrated in the market for small dollar homes (those under $100,000). On average over these 20 years, large investors account for 28 percent of home purchases in the small dollar housing market, but less than 10 percent of the market for homes that cost above $100,000.

While there's reason to think that the relatively inexpensive homes that investors tend to purchase are more likely to be the same ones that are accessible to low-and-moderate income families, experts have also noted that large investors typically do not compete with average middle-class families using a mortgage, and are instead competing with other investors. That's because these more inexpensive homes are likely to be older and require significant repair–something investors are much better-suited to take on, financially and operationally. In Forsyth County, we found the relatively worse condition of homes, combined with the stricter eligibility criteria on mortgage loans designed to serve lower-income buyers, can prevent those using mortgages from being able to purchase these homes altogether.

Thus, the fact that large investor activity is concentrated in the small dollar housing market in Forsyth County suggests that large investors in this market are likely competing with other kinds of investors, and not necessarily families who intend to live in their home (and notably not those who intend to purchase it with a mortgage). It is important to note that this speaks more to the dearth of flexible financing options that work well for low-and-moderate income buyers purchasing homes in this price range, and less to investors intentionally avoiding competition with families who could most benefit from homeownership.

What Happened in 2013? Enter American Homes 4 Rent

In 2013, we observed a huge spike in large investor purchases for homes between $100,000 and $200,000–the price range of homes that many low-and-moderate income buyers in Forsyth County tend to qualify for. Large investor activity in this price range jumped from 2 percent in 2012 to 26 percent in 2013 and then down to 8 percent in 2014. From 2014 to 2020, large investor purchases in this price market remained between 5 percent to 8 percent, never dropping down to pre-2013 levels.

According to our data, American Homes 4 Rent–a publicly traded company based out of California–drove the spike in large investor purchases in 2013. American Homes did not purchase any homes in Forsyth County between 2001 to 2012, but bought approximately 505 homes in 2013, accounting for nearly 40 percent of large investor purchases this year. Ninety-four percent of the homes they purchased were in the $100,000 to $200,000 price range. Post-2013, their presence in the Forsyth County housing market continued, though their purchasing leveled off: in 2014, they bought approximately 100 homes (or 12 percent of all large investor purchases), and in 2015, they bought approximately 67 homes (or 9 percent of all large investor purchases).[2]

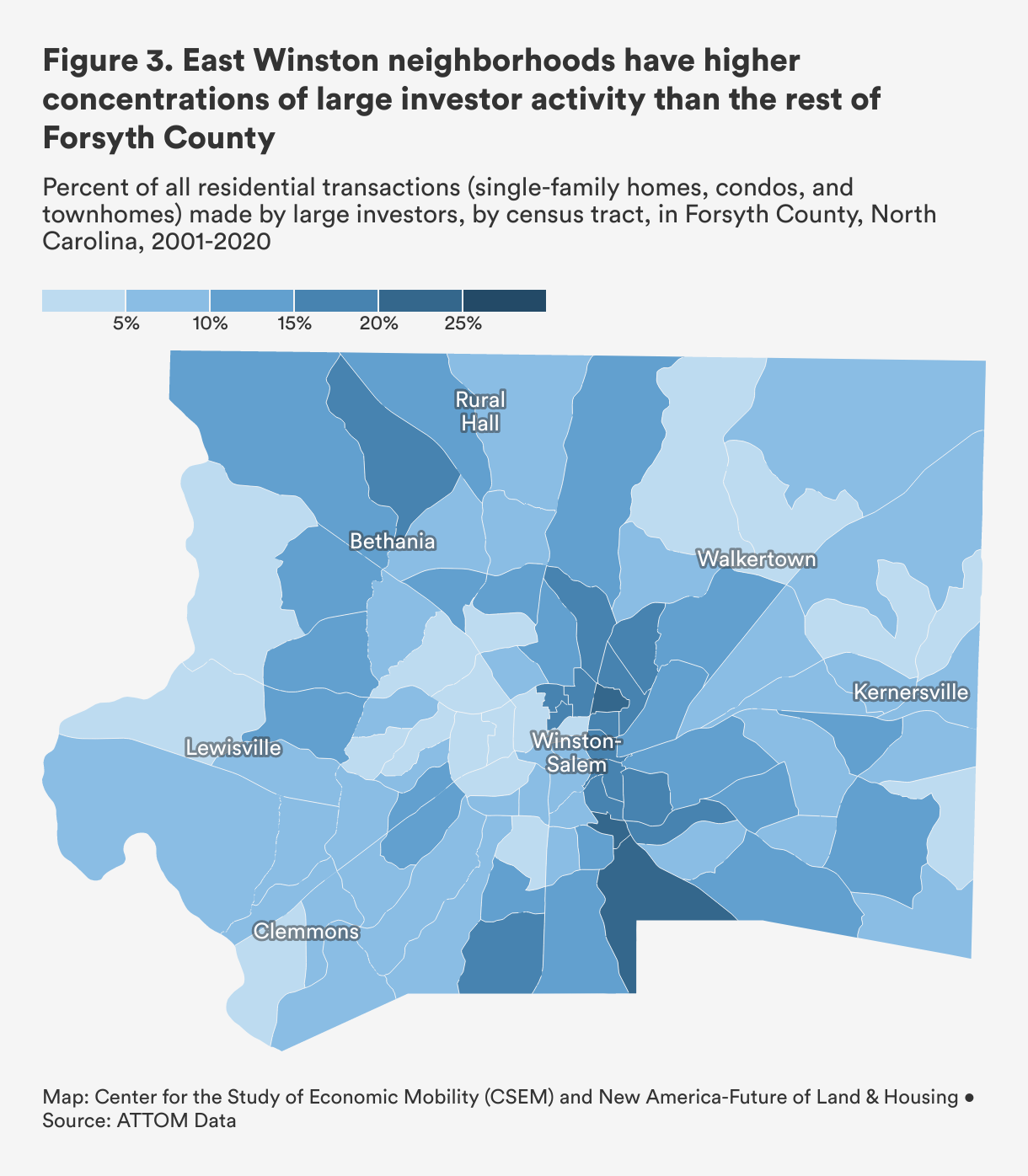

Understanding where in Forsyth County large investor purchases are concentrated can also tell us more about which communities are disproportionately impacted. Figure 3 visualizes large investor activity at the census tract-level in Forsyth County, using data from 2001 to 2020.

We see that census tracts located in East Winston have higher concentrations of large investor activity than the rest of Forsyth county. These neighborhoods are majority Black and Hispanic and physically cut off from the rest of Winston-Salem by a four-lane highway. While large investor activity averages around 10 percent of home purchases in Forsyth County across twenty years, large investor purchases in tracts in East Winston census tracts average 16.8 percent of all home purchases, whereas large investor purchases in the rest of Forsyth County average 8.1 percent. A disproportionate share of investor activity in Black neighborhoods tracks with other metro areas across the country.

Our previous investigation, conducted in partnership with the Center for the Study of Economic Mobility (CSEM) at Winston-Salem State University, into the market for small dollar homes in Forsyth County finds that low-and-moderate income buyers who could otherwise afford to purchase a home are having an increasingly difficult time competing in today’s housing market. We found that an increased use of cash to buy homes under $100,000, combined with a decline in mortgage lending for homes and higher denial rates on these homes, likely contributes to crowding out home buyers who rely on traditional mortgages.

While our analysis suggests that large investors are not the main drivers of investor activity in Forsyth County, that doesn't mean there is no cause for concern. Notably, low supply and high demand for housing in housing markets across the country suggests that real estate will continue to be a lucrative investment for large investors for years to come. And as long as large investor activity grows in certain markets, or even if it continues apace, it is critical we establish a baseline so that we can track the short and long-term impacts in local housing markets and nationwide over time, notably if these impacts are concentrated among lower-income Black and Hispanic communities, as they are in Forsyth County. Without ongoing assessment, ensuring that homeownership–and all its wealth-building potential–is accessible to all, and not just the cash-strapped and resource-rich, becomes difficult.

Our analysis uses residential transaction data from ATTOM Data Solutions in Forsyth County, North Carolina between 2001 and 2020. Our dataset for this analysis includes transactions involving an independent buyer and seller (i.e., arm’s length) for three types of housing: single-family homes; condominiums; and townhomes (excluding mobile homes, modular homes, multi-family dwellings, among others)

To identify a large investor purchase,[3] the entity associated with the transaction in the data must meet one of the following criteria:

From our perspective, purchasing 5 properties in one year or 20 or more properties over 20 years requires a level of capital and operational efficiency that differentiates these investors (i.e. large investors) from traditional ‘mom-and-pop’ landlords or wealthy cash-buyers (small investors). Once an entity is designated as a large investor, any purchase they made over the twenty-year time period is classified as a large investor purchase.[4]

Endnotes

[1] We identify small investors for the purposes of this analysis as purchasing entities who use cash, but who are not considered large investors (see our methodology to identify large investors at the end of this post).

[2] Using ATTOM data, we manually reviewed the name of the purchaser to create a variable for purchases made by American Homes 4 Rent and their subsidiary companies (for example, American Residential Leasing Company). Given that some subsidiary companies may use naming conventions that differ substantially from the parent company, the estimates provided in this analysis may undercount the number of homes purchased by American Homes 4 Rent in Forsyth County.

[3] ATTOM’s data included a large investor variable of their own, which uses a threshold of 10 or more purchases within the last 12 months. Using ATTOM’s variable, a buyer located in Forsyth County that purchased 5 properties a year for 20 years, amassing 100 properties over time, would not be considered a large investor. Since our focus is on a local housing market, we felt this threshold resulted in an undercount of large investors.

[4] Our previous research uses cash purchases as a proxy for investor purchases, since the majority of people cannot afford to purchase a home without a mortgage loan. While 77 percent of large investor purchases were made in cash in 2020, it’s important to note that our definition of large investors can apply to a home purchased with a mortgage or with cash. This is because some entities who fit the large investor criteria use mortgage financing, notably when purchasing a bundle of homes. We found that using the payment mechanism to identify large investors would not only result in an undercount, but that the advantages of large investors extend beyond their payment mechanism, as many of these kinds of investors buy homes sight unseen, and have the operational efficiences and capital to invest far more in the renovation of homes than the average small investor or owner-occupant.

We’d like to thank members of the Consumer and Home Financing team at Pew Charitable Trusts for their review of this analysis: Tara Roche, Tracy Maguze, Rachel Siegel, and Adam Staveski.

Data Analytics and Research Manager, Center for the Study of Economic Mobility

Deputy Director, Future of Land and Housing Program