Table of Contents

Background

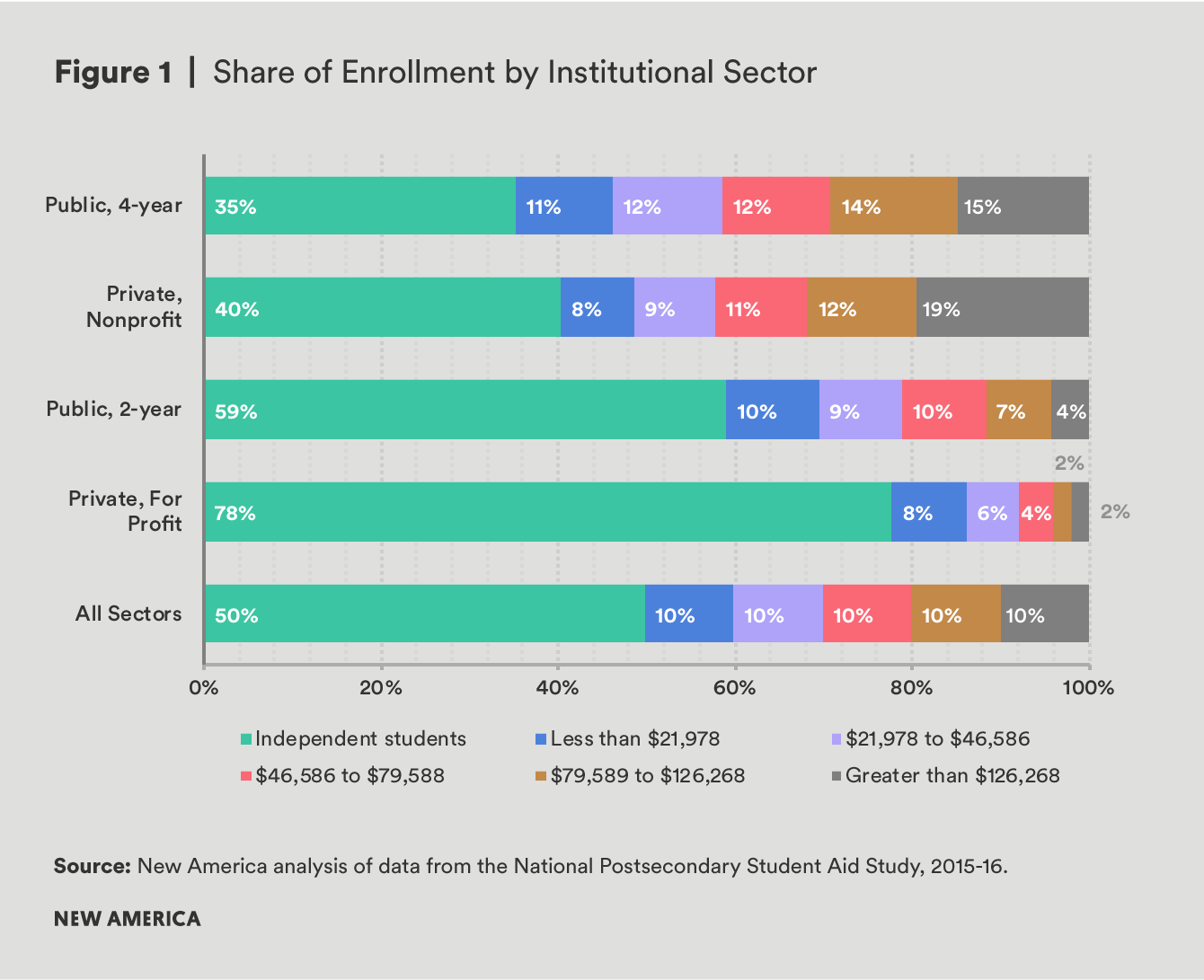

Our analysis shows that a similar share of students borrow for their education, regardless of their family incomes. But on average, students from families in lower socioeconomic brackets1 tend to enroll in open access schools, including community colleges and for-profit institutions, more often than their upper-income peers. In comparison, wealthier students are much more likely to be found at nonprofit and public four-year universities.

For wealthy students and families who are able to pay a significant amount out of pocket, many still take on loans, likely in order to attend more expensive schools that they perceive to be a better investment in their future.2 Additionally, for these students and their families, taking out student loans may be more desirable than paying out of pocket due to the convenience, relatively low interest rates, and flexible repayment terms available on federal loans. Conversely, many low- and middle-income students are not able to draw on family support and savings or other external resources in the same way. For them, federal or private loans may be a necessary source of funding regardless of where they choose to go to school, so many low- and middle-income students who borrow could be doing so for entirely different reasons than their wealthier peers.

For students who lack sufficient financial resources to cover non-tuition expenses, research shows that the shortfall can have a profound impact on their experiences in college. For instance, a 2014 study found that nearly two-thirds of college students had neglected to buy a textbook because it was unaffordable, and half reported taking fewer or different classes because of textbook costs.3 More worrisome, a nationally representative Urban Institute study of undergraduate students found that 11 percent of students at four-year colleges struggled to pay for food, along with 14 percent of students at vocational schools.4 The study also found that over the post-recession years, community college students were especially struggling, when as many as one in five were food insecure.5

Many low- and middle-income students who borrow could be doing so for entirely different reasons than their wealthier peers.

However, with nearly 7 million federal student loan borrowers currently in default6—a designation that can harm borrowers’ credit, lead to wage garnishment and loss of federal benefits or tax refunds, and often increases the amount borrowers owe7—taking on debt for higher education is not a decision that should be entered into lightly. These risks associated with borrowing can lead students to borrow less than they need or cause them to eschew borrowing altogether, even when unmet need is high.8 Discomfort with debt can also cause students to forgo higher education completely if they cannot afford to cover unmet need out of pocket. In these cases, borrowing (or borrowing more) could help close critical deficits. According to a study by Benjamin Marx and Lesley Turner, community college students with unmet need who borrowed more both enrolled in and completed more credits than those who did not. The research team also concluded that students who borrowed performed better academically as a result of their borrowing.9

There are risks to colleges when students take on federal debt, and these risks are more severe for some colleges than others. Indeed, as the cost of higher education has risen for both students and taxpayers, federal policymakers have expressed interest in strengthening accountability metrics for student outcomes, with a particular focus on whether students are able to repay their loans.10 These policies strive to protect students and taxpayers from risky debts, by cracking down on schools where students default at high rates, or whose former students have debt levels that make repayment difficult in light of their post-graduation earnings.11 However, while penalizing programs with poor loan outcomes makes sense, the near-exclusive emphasis on loan outcomes has unintended consequences: rather than focusing on improving loan repayment by raising graduation rates or the economic value of degree programs, many schools are instead looking for ways to limit student borrowing in the first place.12 Others are jettisoning federal student loans altogether to avoid the threat of losing access to other forms of federal financial aid.13

These risks to colleges are somewhat constrained by federal limits on student borrowing. The amount of federal loans available to undergraduates is limited in two ways: through loan limits, and through the school’s total cost of attendance.

Students face limits on federal loans that range from $5,500 to $12,500 per year, depending on whether the student is considered dependent or independent and how far along she is in her education. Federal student loans also come with aggregate caps of $31,000 to $57,500 for undergraduates. While the availability of private student loans, federal Parent PLUS loans, and loans from a variety of other sources such as a state or a school means that students are technically able to borrow above these specified thresholds, these other loans are much less common than federal student loans. For instance, while 36 percent of undergraduates borrow federal direct loans, only 4 percent of parents borrow federal loans on their behalf, and only 6 percent of students borrow non-federal loans.14 In fact, less than half (45 percent) of all borrowers take on the maximum annual federal direct loan for which they are eligible. This means that in practice, many students and their parents are unwilling or unable to borrow in excess of—or even up to—their federal direct student loan eligibility.15

We rely on a conservative definition of the amount borrowed for non-tuition costs by considering any grant aid received or any loans borrowed by students or their parents, and from both federal and other sources, to be applied first to tuition payments, with any excess funds then attributable to non-tuition expenses.

Given that federal student borrowing limits are fixed regardless of how much a student is paying in tuition, and that other types of loans are relatively rare, colleges with high tuition leave less room for a student to borrow for non-tuition expenses because a student may reach his annual loan limits more quickly. This means that students with the greatest room to borrow for their non-tuition expenses are those who attend low-tuition schools.

Students are also constricted in how much they can borrow by the cost of attendance of their school. Cost of attendance is a federally-defined term that includes both direct costs and non-tuition expenses and is the estimated budget for one academic year. Colleges have significant discretion to estimate non-tuition expenses as they see fit, and these estimates are factored into the total cost of attendance, which can have a major impact on the amount that students are able to access in both grants and loans.16 For instance, if a school takes a conservative approach to estimating non-tuition expenses, students may be restricted in the amount of financial aid they can access. This cap cannot be exceeded from all sources of financial aid, including federal loans to students or their parents, any state and institutional aid, and even private loans. However, students rarely borrow the full amount of their cost of attendance; on average, borrowers in 2015–16 took on $8,746 less than their cost of attendance minus any grant or scholarship aid. Just 16.5 percent of borrowers take on the full amount for which they are eligible based on their cost of attendance and any grants or scholarships received.17

This report explores the share of students borrowing for their non-tuition costs and how much money they borrow. Since educational loans can be used for any element of a student’s cost of attendance, we do not attempt to differentiate where individual pots of money are allocated. Instead, we rely on a conservative definition of the amount borrowed for non-tuition costs by considering any grant aid received or any loans borrowed by students or their parents, and from both federal and other sources, to be applied first to tuition payments, with any excess funds then attributable to non-tuition expenses. Under our model students can only be said to borrow for non-tuition costs if the amount they borrow exceeds their tuition charges after grants and scholarships from all sources have been taken into account. This allows for a consistent evaluation of borrowing for non-tuition costs.

Citations

- We include independent students as a single category, because NPSAS does not contain information on parental income and because substantially less variation in income levels exists for these students. For instance, about half of all independent students earn less than $20,000 per year, while about 20 percent earn over $50,000. In contrast, among dependent students less than 20 percent of students are from families making less than $20,000 and 20 percent are from families earning more than $125,000.

- Beth Akers, Kim Dancy, and Jason Delisle, The Affordability Conundrum: Value, Price, and Choice in Higher Education Today (New York: Manhattan Institute, April 12, 2017), source.

- Ethan Senack, Fixing the Broken Textbook Market: How Students Respond to High Textbook Costs and Demand Alternatives (Washington, DC: Student Public Interest Research Groups, January 2014), source.

- Kristin Blagg, Craig Gundersen, Diane Whitmore Schanzenbach, and James P. Ziliak, Assessing Food Insecurity on Campus (Washington, DC: Urban Institute, August 2017), source.

- Ibid.

- Federal Student Aid (website), “Federal Student Loan Portfolio,” U.S. Department of Education, March 2018, source.

- Federal Student Aid (website), “Don’t Ignore Your Student Loan Payments or You’ll Risk Going into Default,” U.S. Department of Education, n.d. source.

- Aliza F. Cunningham and Deborah A. Santiago, Student Aversion to Borrowing: Who Borrows and Who Doesn’t (Washington, DC: Institute for Higher Education Policy and Excelencia in Education, December 2008), source.

- Benjamin M. Marx and Lesley J. Turner, Student Loan Nudges: Experimental Evidence on Borrowing and Educational Attainment (College Park, MD: University of Maryland, January 2018), source.

- Federal accountability measures are currently confined to federal loan outcomes, but recent attempts to include private and institutional debt in an accountability framework have caused some concern for administrators. In particular, the Gainful Employment regulations codified in 2014 intended to hold colleges accountable for all student debt and stoked debate about the appropriate way to address money borrowed for living expenses.

- U.S. Department of Education, “Obama Administration Announces Final Rules to Protect Students from Poor-Performing Career College Programs,” press release, October 30, 2014, source.

- Ben Barrett and Amy Laitinen, Off Limits: More to Learn Before Congress Allows Colleges to Restrict Student Borrowing (Washington, DC: New America, May 2017), source.

- Debbie Cochrane and Laura Szabo-Kubitz, States of Denial: Where Community College Students Lack Access to Federal Student Loans (Oakland, CA: The Institute for College Access and Success, June 2016), source.

- Ibid.

- Ibid.

- Robert Kelchen, Braden J. Hosch, and Sara Goldrick-Rab, “The Costs of College Attendance: Trends, Variation, and Accuracy in Institutional Living Cost Allowances” (paper presentation, Association of Public Policy and Management, October 2014), source.

- Based on authors’ calculations using 2016 National Postsecondary Student Aid Study (NCES 2018484, restricted use data license), source.