Key Findings

In approaching this topic, we sought to answer a fundamental question: Can a civil society organization accept donations in virtual currency—and, if so, how?

Overall, we found that the regulatory frameworks within the scope of our study were generally amenable toward virtual currency donations. In every country surveyed, the answer to whether charities could receive tax-benefited contributions of virtual currencies is at least a qualified “yes.” As we explain in further detail, CSOs interested in collecting virtual currency donations are usually advised to adhere to existing guidelines for the acceptance of other non-cash donations: when in doubt, document the value and means of donation; disclose to tax authorities and regulators in compliance with appropriate laws, erring on the side of more disclosure, rather than less; or decline the contribution if there are serious concerns about conflicts of interest, regulatory considerations, asset management expertise, donation valuation, or any other reason a charity might typically decline a donation.

In every country surveyed, the answer to whether charities could receive tax-benefited contributions of virtual currencies is at least a qualified “yes.”

The policy landscape is still unfolding, and details, including regulatory development and risk management, are uncertain. For example, in the United States, the Internal Revenue Service (IRS) added a new clarification in December 2019 to its informal guidance on virtual currency, requiring virtual currency donors to receive appraisal for donations worth $5,000 or more—presumably after a majority of 2019 virtual currency donations were already made and accepted.1 Just a few weeks later, without public notice or explanation, the IRS deleted significant examples from that informal guidance.2

We also find that frameworks to regulate virtual currency donations can be guided by previous efforts to regulate other forms of in-kind donations. Sometimes virtual currency donations are seen as a novel undertaking due to unique technical features (such as wallets, digital custody, encryption, and key management), forms of traceability (via public blockchains or other shared database designs), and methods of valuation (i.e. assessing the worth of virtual currencies traded on just a few, highly volatile, markets). But in reality, this phenomenon may not be unique: Charities have long been able to accept donations in the form of cash, securities/commodities, real property, and art. The various rules that govern those scenarios apply with equal measure here. Though art and diamonds can be hard to value or are sometimes subject to theft or money laundering concerns, countries have not banned charities from accepting them.

Moreover, many of the policy values underlying virtual currency donations are timeless: balancing recordkeeping requirements with donor privacy, fostering technological innovation while still ensuring consumer protection, allowing for efficient and quick donations while also guarding against money laundering, and protecting the public interest in promoting CSOs. Officials in different countries may have found different ways to balance these numerous values, but they have each struck a balance nonetheless.

Regulatory Trends

In many countries surveyed, there were few or no regulations that apply specifically or in much detail to charitable organizations with regards to virtual currencies. Nations we examined tended to take a hesitant approach to regulatory action in the space, typically extending and applying existing charity and tax laws to the donation and receipt of virtual currency donations. Six other trends are worth highlighting up front:

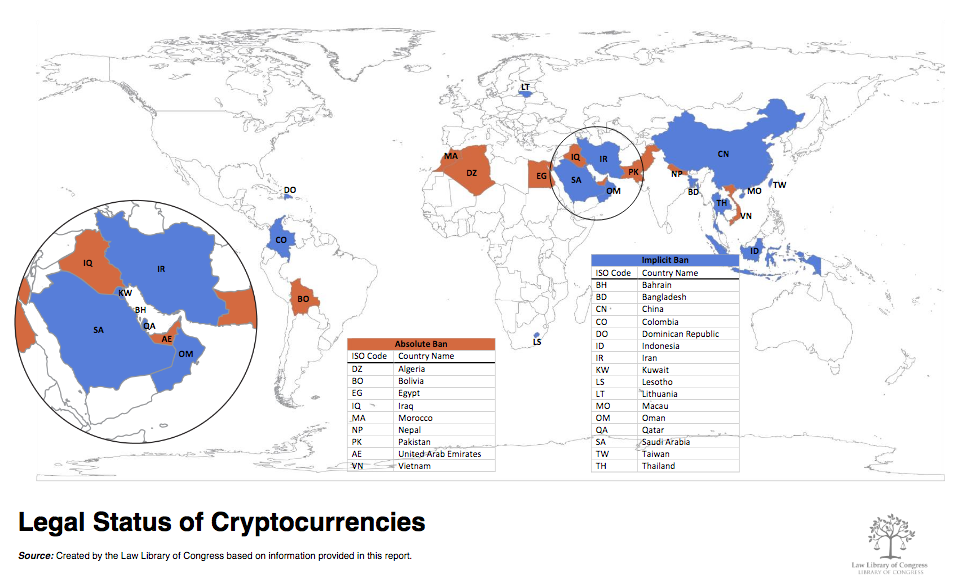

- We did not observe regulatory momentum towards banning virtual currency donations or treating them as categorically exceptional. The nations that have expressly or implicitly banned virtual currencies (pictured below, as of June 2018) are outside of the set of countries examined for this report.3 In fact, some large countries that banned virtual currency trading, such as India, have recently overturned those prohibitions.4 Worldwide, however, there is little public data to illuminate whether or how often individuals or entities are actually reporting virtual currency donations to local tax authorities. Nor is there comprehensive and publicly-available information about the incidence of tax authorities or other regulators using other enforcement mechanisms, such as investigations, audits, fines, warning letters, or rejected tax applications in response to virtual currency donations. While Denmark does not ban virtual currencies, their practical use is somewhat limited by law: In 2014 the Danish Tax Authority issued a binding opinion stating that invoices cannot be denominated in virtual currency but must instead be issued in the official Danish currency (Kroner) or another recognized currency.5

2. We found overlapping and sometimes conflicting bodies of regulation or guidance regarding virtual currencies, which complicates matters for charities and donors alike. Such examples speak to the need, both within and across governments, to engage in greater inter-agency coordination and public-facing clarification.6 Despite some proposals that certain countries form a new agency to coordinate virtual currency regulation within each jurisdiction,7 countries have not yet created these bodies and we expect that a number of existing agencies will continue to concurrently engage in regulation and oversight absent clearer guidance. Moreover, international harmonization of virtual currency regulations at this early stage could carry both benefits and costs, and there may be advantages from a comparative policy perspective to, at this stage, letting different international regulatory approaches continue to evolve.8

3. The bulk of regulators’ attention in the virtual currency space has been focused on protecting consumers and investigating the issuance, sale, and promotion of digital tokens, sometimes referred to as initial coin offerings (ICOs), and prosecuting virtual-currency-related scams.9 For example, we found ICO-specific statements and guidance across nearly all countries surveyed, including Australia, Bermuda, Denmark, Malta, Singapore, Switzerland, and the United States. The overarching concern here is the use of misleading or downright fraudulent ICOs to entice retail investors, skirt securities law, and engage in capital formation by another name.10 Regulators’ focus on ICOs suggests comparatively less attention and, at this point, scrutiny, have been focused on donations of virtual currency.

4. Some jurisdictions, such as Malta and Singapore, have attempted to position themselves as especially friendly to virtual currency activities and innovation as a means of attracting investment and commerce. Malta uses a hybrid regulatory regime, the Virtual Financial Assets Framework, that is still technically operating under the European Union (EU) umbrella.11 Singapore has created a regulatory sandbox (and a “sandbox express”), that invites firms to apply to experiment with innovative financial services under a relaxed legal and regulatory regime.12 Singapore’s aim is to encourage financial technology experimentation, innovation, market testing, and wide adoption.13 The Monetary Authority of Singapore also announced in January 2020 that it had received 21 applications for new digital bank licenses.14 By contrast, the EU’s recent passage of the Fifth Anti-Money Laundering Directive (AMLD5) created stringent new requirements for providers of virtual currency transfers.15 It also led several companies, including one that had recently received a multimillion-dollar round of venture capital funding, to shut down entirely, while others announced plans to relocate out of the EU in favor of more virtual-currency-friendly jurisdictions.16 We did not observe similar relocation efforts by international charities to avoid or avail themselves of such regulations.

5. We did not observe additional requirements for civil society organizations receiving donations of virtual currencies beyond existing best practices regarding anti-money laundering (AML) and countering the financing of terrorism (CFT) guidelines. To the extent charitable organizations accept anonymous donations and follow existing AML/CFT guidelines, they should continue to do so with regard to virtual currencies.17 In some countries, such as South Africa, is it not clear that AML/CFT rules apply to virtual currencies at all.18

6. A number of countries are exploring the issuance of their own sovereign virtual currency, often known as a Central Bank Digital Currency (CBDC). This fast-moving space has recently garnered serious attention from a wide range of monetary policymakers. In January 2020, several major central banks—the Bank of Canada, the Bank of England, the Bank of Japan, Sveriges Riksbank (in Sweden), and the Swiss National Bank, along with the Bank for International Settlements—announced they had formed a group to assess potential use cases for CBDCs.19 While the legal status of CBDCs is beyond the scope of this report, it is reasonable to assume that they would be treated as legal tender in a given country, could be given to a charity, much like cash or a check today, and may become just as attractive a medium of donation as alternative virtual currencies.

Best Practices

For Civil Society

CSOs interested in collecting virtual currency donations should generally adhere to guidelines for the acceptance of other non-cash donations: When in doubt, document (the value and means of donation), disclose (to tax authorities and regulators in compliance with appropriate laws, erring on the side of more disclosure, rather than less), or decline the contribution (if there are serious concerns about a conflict of interest or donor motives). Charities just beginning to accept virtual currencies may also consider partnering with domestic, regulated virtual currency exchanges and/or custodians, in order to streamline processes around asset acceptance, custody, and liquidation.

For Donors

For donors of virtual currency, best practices are similar to those applicable to donations of equity or property. If donors wish their donations to be tax-benefited, that usually requires giving to a tax-exempt domestic CSO (located in the same country as the donor) and documenting the donation with a receipt from the charity. As a rule of thumb, donors of higher amounts of virtual currencies hoping to receive tax benefits should obtain at least one independent, written appraisal of the value of their virtual currency donations and retain receipts of the donations.

For donors of virtual currency, best practices are similar to those applicable to donations of equity or property.

For Charities

Virtual currency donations also raise considerations for charities receiving them. Like a receipt of equity, a crucial initial question for the CSO will be determining what portion, if any, to immediately liquidate, and what portion to hold on for short-, medium-, or long-term appreciation. Moreover, like a receipt of equity, CSOs should take care to avoid the appearance of conflicts of interest—e.g., where a board member has substantial existing interest in a virtual currency or affiliated entity. Regulatory risk is greater in cases where the classification of the virtual currency donated is unclear (we found this to be the case for many virtual currencies, with the exception of Bitcoin and in some cases Ether), and CSOs should take care to establish with a reasonable basis that the virtual currencies are legal to possess and sell within their jurisdiction. CSOs that may not feel technologically savvy enough to self-custody (see Appendix 1: Virtual Currency Terminology) may also consider accepting virtual currency donations through a third-party custodian with expertise in securing and handling these assets. As a matter of board governance, it may also be prudent to adopt policies or pass resolutions documenting why and how the board is accepting virtual currency donations and how its investment strategy would apply to them.20

For Policymakers

For policymakers and regulators, putting forth consistent virtual-currency-specific tax and donation-compliance guidance, such as FAQs and other communications from the IRS in the United States,21 could ease uncertainty and encourage more virtual currency donations. Direct engagement among regulators, industry, and consumers, whether in public hearings or private consultations, is often fruitful. In addition to less formal regulatory tools—like issuing non-binding guidance, conferring with virtual currency businesses and consumers, and improving policy coordination—policymakers should continue to advance black letter law, like regulations, statutes, and case law, that would help both donors and recipient organizations alike in facilitating charitable contributions that are fully compliant with existing law and appropriately tax-benefited.

Open Questions

In light of the widespread lack of virtual-currency-specific charity guidance, it may be necessary in some cases for CSOs and donors to engage the democratic process, asking regulators to provide a no-action letter or encouraging lawmakers to draft new legislation that clearly establishes these rules and ameliorates these inter-agency disagreements. Despite the rise in virtual currency value and interest, most countries have passed little new virtual-currency-specific black letter law. The U.S. Congress’s quiescence on new virtual-currency-specific legislation, in particular, may contribute to the consistent reluctance of other countries to take first steps.

Achieving greater regulatory clarity may be especially important for CSOs interested in holding onto virtual currency donations rather than converting the donations immediately to a fiat currency. This may occur in cases where the CSO believes the donations might appreciate in value. For example, CSOs that several years ago received numerous donations in Bitcoin and immediately converted them into fiat currency likely lost out on millions of dollars in potential gains due to Bitcoin’s subsequent appreciation. Although immediate liquidation is simpler from a tax, technology, and investment standpoint, we should expect interest in saving particular virtual currencies to persist so long as these virtual currencies continue to hold and/or appreciate in value. In these and similar cases of saving virtual currency donations, regulatory considerations tend to follow similar considerations as charities accepting and saving donations of securities, including guarding against possible conflicts of interest with regard to the board of directors and ensuring the equities are properly registered with authorities.

For regulators and policymakers, tools like questionnaires and account auditing may be more effective than outright bans or hard to meet licensure requirements that could curb the total number of donations or move more donation transactions off the books. In some contexts, the public and private sectors could benefit from the creation of regulatory sandboxes that facilitate transparent experimentation at relatively modest scale. The insights derived from these efforts can help shape adaptation of future regulatory regimes as the space continues to evolve.

…the public and private sectors could benefit from the creation of regulatory sandboxes that facilitate transparent experimentation at relatively modest scale.

Tax evasion, money laundering, and terrorist financing are all legitimate areas of government concern regarding for-profit and tax-exempt organizations alike. For example, the recent growth in tax-exempt donor advised funds (DAFs) in the United States may create both useful new tax savings for individual donors and also, in some circumstances, the potential for misuse.22 Concerns about DAFs may also extend to donations of virtual currencies, insofar as they could conceivably allow a donor to receive a multi-year tax deduction for an illiquid virtual currency donation at a high valuation (even momentarily), without requiring or ensuring those funds are ultimately distributed or put towards charitable causes.23 Other potential public interest concerns may arise in evaluating tax-exempt status for virtual-currency-specific foundations—philanthropic organizations directly affiliated with the companies or organizations that created or manage a given virtual currency—both in the United States and abroad, including monitoring for conflicts of interest, for-profit motives, and distributions to affiliated entities. There are a number of virtual currency entities abroad, often styled as scientific foundations, that contribute to the development, distribution, and/or marketing of a given virtual currency, and hold large sums of it. Separately, there have also been several high-profile instances of individuals pledging sizable virtual currency donations—garnering significant attention (to their companies and currencies) in so doing—but never following through with a donation. While the problem of unfulfilled pledges may or may not be a legal problem, per se, it dovetails with concerns about potential profit-oriented motives, ICO issuances, and evaluating how much CSOs are benefiting from certain virtual currencies.24

Technical familiarity is another key question for charities considering accepting and custodying virtual currencies. How equipped are charities to securely custody these assets, manage their price volatility and regulatory risk, and properly account for them on all tax documents? Charities and regulators alike may benefit from more hands-on training and question and answer opportunities with industry professionals. Lawmakers may consider taking Canada’s lead and require asset managers and virtual currency custodians to meet particular expertise or certification requirements before allowing them to custody virtual currencies on behalf of charity clients.25

Charities and regulators alike may benefit from more hands-on training and question and answer opportunities with industry professionals.

Virtual Currency Donations

- Executive Summary

- Introduction

- About Our Organizations

- Methodology and Terminology

- First Principles of Civil Society

- Blockchain and Digital Currency

- Use Cases

- Key Findings

- Other Findings

- Conclusion

- Appendix 1: Virtual Currency Terminology

- Appendix 2: International Highlights

- Appendix 3: Australia

- Appendix 4: Bermuda

- Appendix 5: Canada

- Appendix 6: Denmark

- Appendix 7: Malta

- Appendix 8: Singapore

- Appendix 9: South Africa

- Appendix 10: Switzerland

- Appendix 11: United Kingdom

- Appendix 12: United States

Citations

- Internal Revenue Service, Frequently Asked Questions on Virtual Currency Transactions (Dec. 2019), source ; see also United States Government Accountability Office, Virtual Currencies: Additional Information Reporting and Clarified Guidance Could Improve Tax Compliance (Feb. 2020), source at 2 (“However, part of the 2019 guidance is not authoritative because it was not published in the Internal Revenue Bulletin (IRB). IRS has stated that only guidance published in the IRB is IRS’s authoritative interpretation of the law. IRS did not make clear to taxpayers that this part of the guidance is not authoritative and is subject to change. Information reporting by third parties, such as financial institutions, on virtual currency is limited, making it difficult for taxpayers to comply and for IRS to address tax compliance risks. Many virtual currency transactions likely go unreported to IRS on information returns, due in part to unclear requirements and reporting thresholds that limit the number of virtual currency users subject to third-party reporting. Taking steps to increase reporting could help IRS provide taxpayers useful information for completing tax returns and give IRS an additional tool to address noncompliance.”).

- The IRS scrubbed its website of a reference to “Fortnite V-Bucks” as an example of a virtual currency. See, e.g., BrianFung, IRS quietly deletes guideline that Fortnite virtual currency must be reported on tax returns, CNN Business (Feb. 13, 2020), source

- See, e.g., Selva Ozelli, Qatar bans cryptocurrencies after updating its AML Laws, The FCPA Blog (Feb. 12, 2020), source

- Campbell Kwan, India’s highest court overturns cryptocurrency trading ban, ZDNet (March 5, 2020), source

- The Law Library of Congress, Regulatory Approaches to Cryptoassets in Selected Jurisdictions: Denmark (Apr. 2019), source at 74 (referring to Bitcoins, ikke erhvervsmæssig begrundet, anset for særkilt virksomhed [Bitcoins, Not CommerciallyJustified, Considered Special Activity], SKAT (Apr. 1, 2014), source at source).

- We discuss further some examples of overlapping and sometimes conflicting virtual currency regulations, infra at § “Asset Class, Valuation, and Tax Issues.”

- See, e.g., Peter J. Henning, Should Congress Create a Crypto-Cop?, The New York Times (Feb. 14, 2018), source

- See, e.g. Statement of Rebecca M. Nelson (Specialist in International Trade and Finance) before the U.S. Senate Committee on Banking, Housing, and Urban Affairs, Examining Regulatory Frameworks for Digital Currencies and Blockchain (July 30, 2019) at 9 source (“The Need for International Regulatory Harmonization? . . . Then-Managing Director of the International Monetary Fund (IMF) Christine Lagarde argued that international regulation and supervision of cryptocurrencies is “inevitable.” Additionally, the editorial board of the Financial Times argues that a coordinated international regulatory framework for the “wild west” of cryptocurrencies is long overdue. Some initial international efforts at harmonization of cryptocurrency regulations are proceeding [], although more systematic coordination remains elusive. A more aggressive adoption of a one-size-fits all international regulatory structure for cryptocurrencies could have costs, however. It could create distortions, have unintended consequences, and impede innovation, a particular concern in the fast-changing cryptocurrency market.”).

- Initial Coin Offering (ICO): A process by which a portion of a particular protocol’s cryptocurrency or tokens are sold publicly (in many cases following earlier distribution or reservation to venture capitalists, founders or other supporters) in exchange for either fiat currency or other virtual currencies. These funds can be used for a variety of purposes. ICOs have come under heavy regulatory scrutiny, especially where they can be said to resemble unregistered IPOs that fail to deliver buyers equity or other shareholder rights typical of registered securities. Some regulators view ICOs as rough equivalents of Initial Public Offerings (IPOs), and tokens issued in conjunction with an ICO may be governed under securities law.

- See, e.g., SEC Chairman Jay Clayton, Statement on Cryptocurrencies and Initial Coin Offerings (Dec. 11, 2017) source (“By and large, the structures of initial coin offerings that I have seen promoted involve the offer and sale of securities and directly implicate the securities registration requirements and other investor protection provisions of our federal securities laws.”).

- See, e.g., Malta Financial Services Authority, Virtual Financial Assets Framework Frequently Asked Questions (Jan 25, 2019), source

- See Monetary Authority of Singapore, Fintech Regulatory Sandbox Guidelines (Nov. 16, 2016), source at 2.4 (“[Applicants] can apply to enter a regulatory sandbox (the ‘sandbox’) to experiment with innovative financial services in the production environment but within a well-defined space and duration. The sandbox shall include[] appropriate safeguards to contain the consequences of failure and maintain the overall safety and soundness of the financial system. . . . Upon approval, the applicant becomes the entity responsible for deploying and operating the sandbox (the ‘sandbox entity’), with MAS providing the appropriate regulatory support by relaxing specific legal and regulatory requirements prescribed by MAS, which the sandbox entity will otherwise be subject to, for the duration of the sandbox.”).

- Monetary Authority of Singapore, Sandbox Express, Consultation Paper P015-2018 (Nov. 14, 2018), source

- Monetary Authority of Singapore, MAS Receives 21 Applications for Digital Bank Licences (Jan. 7, 2020), source

- See, e.g., Jenny Gesley, European Union: 5th Anti-Money Laundering Directive Enters into Force, The Law Library of Congress (July 16, 2018), source

- See, e.g., Yogita Khatri, Two more crypto firms shutting down over impending EU money-laundering rules, The Block (Dec. 16, 2019), source ; Deribit, Deribit Moving to Panama + KYC Feb. 2020 (Jan. 9, 2020), source (“Currently, Deribit is operating in the Netherlands. However, the Netherlands will most likely adopt a very strict implementation of new EU regulations that also apply to crypto companies (5AMLD). . . . Therefore, we have decided to operate the Platform from Panama.”).

- We reiterate that this report is conveyed as an analysis of public policy and international trends and does not offer or constitute legal advice. Do not rely upon this report for making or receiving donations or for any other purpose. Please confer with a local attorney, tax specialist, financial advisor, and/or other licensed professionals before making an individualized decision about virtual currencies, donations, or other matters. See supra, n1.

- The Law Library of Congress, Regulatory Approaches to Cryptoassets in Selected Jurisdictions: South Africa (April 2019), source at 221 (“It does not appear that South Africa’s anti-money laundering laws are currently applicable to cryptoassets.”); South Africa Intergovernmental FinTech Working Group (Crypto Assets Regulatory Working Group), Consultation Paper on Policy Proposals for Crypto Assets (Jan. 2019) at 22.

- Bank of England, Central Bank group to assess potential cases for central bank digital currencies (Jan. 21, 2020), source?

- See, e.g., Lawrence J. Trautman & Janet Ford, Nonprofit Governance: The Basics, 52 Akron L. Rev. 971, 1035–36 (2018), available at source (“Serving competently on a board requires understanding of a considerable body of enterprise (corporate) governance knowledge. Novel and disruptive technological innovations create a constant challenge to those seeking to govern any enterprise.”); id. at n.164 (referencing bitcoin and virtual currency).

- Internal Revenue Service, Frequently Asked Questions on Virtual Currency Transactions (Dec. 2019), source

- See, e.g., David Gelles, How Tech Billionaires Hack Their Taxes With a Philanthropic Loophole, The New York Times (Aug. 3, 2018), source (“D.A.F.s have become one of the most controversial issues in the charitable world. . . . Unlike family foundations, which are required to distribute 5 percent of their assets each year and have historically been the way wealthy donors disbursed their philanthropic firepower, D.A.F.s have no distribution requirements, meaning that billions of dollars earmarked for charity can sit idle for decades. And because organizations that manage D.A.F.s are not required to report which funds give money to which causes, it is impossible to know how much money individual donors are giving away to nonprofit organizations.”); Theodore Schleifer, How a lawsuit could reveal secrets about Silicon Valley’s favorite philanthropic loophole, Vox Recode (July 2, 2019), source

- See, e.g., Laura Mahoney, California Looks Into Billions Held in Funds Intended for Charities, Bloomberg Tax (Jan. 14, 2020), source ; See also, Theodore Schleifer, Why Jack Dorsey (and you) should pay attention to this proposed charity law in California, Vox (Jan. 14, 2020), source (noting that “[t]he amount of money stored in DAFs has tripled over the last decade.”). In some cases, particularly with regard to highly illiquid virtual currencies where donation valuation would be difficult to ascertain, regulators and charities may consider asking donors to first liquidate the assets to conventional currencies.

- Compare Laura Shin, Former Child Actor Brock Pierce Vows To Give Away $1B From His Crypto Fortune, Forbes (Feb. 28, 2018), source , with Neil Strauss, Brock Pierce: The Hippie King of Cryptocurrency, Rolling Stone (July 26, 2018), source (“As of this writing, it has been nine months since Pierce first mentioned giving away $1 billion, and there still hasn’t been a white paper released or a penny given.”).

- Canada Securities Administrators, CSA Staff Notice 46-307 (Aug. 24, 2017), source (“Custody: Securities legislation of the jurisdictions of Canada generally require that all portfolio assets of an investment fund be held by one custodian that meets certain prescribed requirements. We expect a custodian to have expertise that is relevant to holding cryptocurrencies. For example, it should have experience with hot and cold storage, security measures to keep cryptocurrencies protected from theft and the ability to segregate the cryptocurrencies from other holdings as needed.”).