In Default and Left Behind

Table of Contents

- Introduction and Overview

- Key Finding 1: Before Borrowers Entered Default, They Did Not Receive the Benefits Promised by Higher Education

- Key Finding 2: Before Borrowers Entered Default, They Struggled to Access Affordable Payments amid Financial Insecurity

- Key Finding 3: When Borrowers Entered the Default System, They Got Trapped

- The Default System Needs Reform on Many Levels

- Methods

Abstract

In the summer of 2022, New America managed focus groups with almost 50 borrowers from across the country who reported holding federal student debt and defaulting on their loans before the COVID-19 pandemic. Focus group participants felt hopeless about their student loans, and they had good reason to feel this way. They entered the default system, which damaged their finances and eroded their economic security. Before they defaulted, many did not receive the benefits promised by higher education and were poorly served by a complex student loan repayment system, experiences that contributed to ongoing financial instability.

Even though defaulting on a student loan is a worst-case scenario for borrowers, there is much we do not know about outcomes for those who default, and even less is known about borrowers’ experiences in and perceptions of default. This report seeks to fill some of these knowledge gaps by providing a narrative about why borrowers defaulted, the barriers they faced while in default, and how they attempted to bring their loans back into good standing. Current and historic failures in the default system continue to damage vulnerable families’ finances, and this analysis also underscores the need for additional relief for those who have been trapped in default.

Acknowledgments

The authors would like to thank Rachel Fishman, Wesley Whistle, and Stephen Burd for editing this brief, Sabrina Detlef for her copyediting support, and Riker Pasterkiewicz, Fabio Murgia, and Rocio Montoya-Pereyra for their communication and data visualization support. The authors would also like to thank Deanne Loonin, student loan borrower advocate; Michele Shepard, The Institute for College Access & Success; Scott Miller, consultant; and Clare McCann, Arnold Ventures for their assistance and reviewing earlier drafts.

This analysis was funded by The Joyce Foundation and the Bill & Melinda Gates Foundation. New America thanks the foundations for their support. The findings and conclusions contained within are those of the authors and do not reflect positions or policies of the reviewers or funders.

Downloads

Introduction and Overview

In the summer of 2022, New America managed focus groups with almost 50 borrowers from across the country who reported holding federal student debt and defaulting on their loans before the COVID-19 pandemic.1 The focus groups included borrowers with a wide range of experiences. Some reported defaulting 20 years ago and communicating about their loans through the mail, and some borrowed and defaulted more recently and checked on the status of their loans online.

But whether focus group participants had been repaying for five or 25 years, most felt similarly about their student loans: hopeless. And they had good reason to feel this way. They entered the default system, which damaged their finances and eroded their economic security. Before they defaulted, many did not receive the benefits promised by higher education and were poorly served by a complex student loan repayment system, experiences that contributed to ongoing financial instability.

The focus group participants reported trying a host of strategies to keep up with their payments. They took on second jobs and worked side hustles. Some reluctantly took whatever financial help family members could offer. Many sought relief from the federal student loan system but were met with a confusing maze of policies and programs, received inadequate or incorrect information along the way, and were not initially aware of how the default system worked or its consequences. These experiences—in addition to their economic instability and the fact that some had spent decades in repayment with no end in sight—chipped away at borrowers’ capacity to manage their student debt while balancing other needs and obligations. As they became more and more overwhelmed, they searched for, but did not find, easily accessible repayment solutions.

These borrowers had options and choices on paper but, in reality, many needed higher education to access a career or move up the economic ladder and needed to take on debt to pay for it. One borrower explained, “it's not like I just don't want to pay this [loan]. I literally cannot afford to.” Focus group participants were often at the mercy of systems and actors not designed for, incentivized around, or held accountable for meeting their needs.

Default was not an active choice made by these borrowers. Rather, by the time they reached default, they had been failed by multiple systems. In the end, many participants internalized these system failures. They felt like they had personally fallen short and expressed embarrassment for not being able to repay. One borrower said that he felt “ashamed and also…like a failure, because I don't have the financial capabilities to pay my loan.” Another had not spoken to his family about defaulting on his student loan and frustration with his higher education experience because he did not “want them to know.”

Many participants also described feeling regretful, and as a result of their own experiences, borrowers reported telling friends and family that education, and borrowing for education, is not always a good deal. These conversations may unfortunately have even dissuaded their loved ones from pursuing college and its potential economic benefits.

As of March 2022, 7.5 million borrowers—close to one in five—were in default on their federal student loans.2 Borrowers default when they miss at least 270 days’ worth of payments,3 and default not only causes family financial insecurity, but it also contributes to the racial wealth gap and related economic disparities. Those most likely to default on their loans—including borrowers of color, particularly Black borrowers; low-income, low-wealth, and low-resource students; those who do not complete a degree or credential; older borrowers; and those that attend for-profit schools, among others—are often least able to afford the severe financial consequences that come with default due to structural racism and discrimination that limit access to wealth-building, educational opportunities, and good jobs.4

Even though defaulting on a student loan is a worst-case scenario for borrowers, there is much we do not know about outcomes for those who default due to the complexity of the system itself, an absence of publicly available data, and a general lack of transparency by the Department of Education (the Department) and its contractors.5 And even less is known about borrowers’ experiences in and perceptions of default.

This report seeks to fill some of these knowledge gaps through an analysis of the six online focus groups mentioned above. It provides a narrative about why borrowers defaulted, the barriers they faced while in default, and how they attempted to bring their loans back into good standing.6 This analysis is focused on student loan default, but in order to fully understand the barriers borrowers face in default and how the higher education and student loan systems can better serve them, stakeholders—including researchers, practitioners, advocates, and policymakers—must better understand borrowers’ pathways to and through it. This paper’s key findings include:

- Key Finding 1: Before borrowers entered default, they did not receive the benefits promised by higher education. They reported going to schools that provided little support, often leaving without a degree or credential, and not being able to find the stable employment they had been promised.

- Key Finding 2: Before borrowers entered default, they struggled to access affordable payments amid financial insecurity. They faced challenges navigating a complex repayment system and accessing all of the safeguards available to keep them out of default. And these tools—and the assistance available to them from the Department and its contractors—were often inadequate and unresponsive to their financial situations. As they struggled to afford their car payments, rent, and child care, they fell farther and farther behind on their student loans.

- Key Finding 3: When borrowers entered the default system, its severe consequences further eroded their financial security. Participants lost track of their loans as they were transferred among different entities, their paychecks turned up short, and their tax refunds were unexpectedly garnished. When it was time to move, credit score damage often meant they could not live in the neighborhoods they wanted to or easily access funds to buy a more reliable car. Many struggled to identify and use available loan discharge options and other pathways to exit default, and others got stuck because they had no affordable way out. Interactions with student loan servicers, collectors, and the Department left many borrowers confused and without adequate aid or information.

In response to the pandemic, the government paused student loan payments and interest for most borrowers and collections for those in default starting in March 2020, and the Biden administration recently extended that pause through no later than June 30, 2023.7 In addition, the administration announced that it would cancel up to $10,000 in student loans for most borrowers—and up to $20,000 for those who received Pell Grants—an action with the potential to wipe out the debt of more than half of those in default and reduce repayment challenges for many others.8 (At the time of publication of this report, court orders had blocked this cancellation. The Biden administration is pursuing appeals and seeking to overturn those decisions.)

The administration, through its Fresh Start program, is also providing temporary relief to defaulted borrowers and a pathway back to repayment for those who are able to make arrangements to access it. These efforts complement a host of additional actions taken by the administration that will provide much-needed and long-overdue protections and benefits for students and borrowers. (See “Recent Initiatives that Benefit Borrowers in Default” for more information about these efforts.)

But current and historic failures in the default system continue to damage vulnerable families’ finances, highlight the need to ensure that plans to support struggling borrowers can be implemented before repayment restarts, and underscore the need for additional relief for those who have been trapped in default. In addition, this analysis provides a framework for designing a more borrower-centered, and less piecemeal, system going forward, including pathways to help borrowers exit default and avoid redefaulting on their loans, protect borrowers’ financial security, and rethink the default system as a whole.

Recent Initiatives that Benefit Borrowers in Default

Over the last two years, the Biden administration has taken actions to provide repayment relief to student loan borrowers, including some that will provide long-overdue and much-needed protections and benefits to those who have defaulted on their loans. They include:

- Extending the Payment Pause: In response to the pandemic, the government paused student loan payments and interest for most borrowers and collections for those in default starting in March 2020. The Biden administration has extended that pause through no later than June 30, 2023 as it pursues appeals of court orders blocking its cancellation initiative.9

- Cancelling Debt: Borrowers with loans held by the Department of Education who made less than $125,000 as individuals or $250,000 as part of couples or households in 2020 or 2021 are eligible for $10,000 in student loan cancellation—and up to $20,000 if they received Pell Grants.10 (As noted earlier, at the time of publication of this report, court orders had blocked this cancellation. The Biden administration is pursuing appeals and seeking to overturn those decisions.)

- Providing Borrowers in Default a “Fresh Start”: The Fresh Start initiative eases the penalties of default for those with eligible loans in default, a benefit that will continue for one year after the payment pause ends.11 During that period, the Education Department will pause collections on most defaulted student loans and will allow most borrowers in default to temporarily regain eligibility for federal financial aid, including federal student loans. In addition, borrowers with defaulted loans will have the opportunity to exit default and reenter repayment in good standing if they are able to make repayment arrangements with the Education Department or the guaranty agency that manages the loans they borrowed in the now-defunct Federal Family Education Loan Program (but this will not happen automatically). Once back in good standing, these borrowers will regain access to income-driven repayment plans, Public Service Loan Forgiveness, and deferments and forbearances (tools that can be used to pause payments), and the default will be removed from their credit histories. If borrowers do not make payment arrangements during the Fresh Start period, they will again be subject to the consequences of default once the temporary program expires.

- Making Income-Driven Repayment (IDR) Plans Easier to Access: IDR plans calculate monthly payments based on a borrower’s income and family size.12 After making 20 or 25 years’ worth of payments, a borrower’s remaining balance is eligible to be forgiven. While time spent in default does not currently count toward forgiveness in any IDR plan, a forthcoming regulatory proposal from the Education Department may allow borrowers to access one of these plans, and its related forgiveness, while in default.13 For those with access to IDR, this proposal would also offer forgiveness after shorter periods for borrowers with low balances, decrease payments for many others, and help borrowers manage balance growth.14

The Department also recently took action to correct past failures in administration of IDR, which will make it easier for borrowers to access these plans and get credit toward loan forgiveness for previous time spent in repayment (but not default).15

- Making It Easier to Qualify for the Public Service Loan Forgiveness (PSLF) Program: PSLF forgives the remaining balances on qualifying loans for borrowers who make 10 years’ worth of payments in a qualifying plan while working for a nonprofit or government agency.16 Like IDR, time spent in default does not count toward PSLF forgiveness. Also like IDR, borrowers have struggled to access PSLF due to program administration failures from the Department and its contractors. Through recent administrative actions and the regulatory process, the Department has made it easier for some borrowers to access and get credit toward forgiveness for PSLF.17

- Making It Easier to Access Loan Discharges: Eligible borrowers—including those in default—who were defrauded by their schools, whose schools closed unexpectedly, or who are permanently disabled, among others, are eligible for loan discharges. Recent actions taken by the Department will make it easier for borrowers to access these discharge programs and make them automatic for more borrowers.18 In addition, the Departments of Education and Justice have developed a more streamlined and transparent process for borrowers seeking a discharge through bankruptcy.19

- Reforming Student Loan Servicing and Collections: When borrowers are in good standing on their loans, servicers, under contract with the Department, manage their accounts, help them access repayment plans and options, and collect payments. Once borrowers default, they are transferred to the Department and, until recently, many were assigned to a private collection agency (also under contract with the Department). The Department and its contractors have a history of providing inadequate information to borrowers, mishandling implementation of existing programs, and lacking strong oversight and standards that lead to borrower success.20 In 2021, the Department ended its contracts with collection agencies—entities that have been accused of misleading and aggressive practices—explaining that the decision was part of a strategy to improve collections, efficiency, and borrower support.21 It has also signaled an intent to reform pieces of the debt collection system through the regulatory process.22

In addition, the Department recently announced the first stages of a procurement that envisions a new role for and stronger oversight of contractors across the repayment and default systems.23 The Department has partnered with other government entities on enforcement actions, and as part of contract extensions until the new system is in place, it strengthened performance standards, transparency, and oversight for existing servicers.24

Even with these reforms, current and historic failures in the default system continue to damage vulnerable families’ finances, highlight the need to ensure that plans to support struggling borrowers can be implemented before repayment restarts, and underscore the need for additional relief for those who have been trapped in default.

Citations

- Participants reported holding federal student loans for their own educations at the time of the focus groups but were not necessarily still in default on those loans. Several participants also reported holding debt for someone else, and some held private student loans in addition to their federal loans.

- Federal Student Aid, “Federal Student Aid Posts Quarterly Portfolio Reports to FSA Data Center,” Electronic Announcement GENERAL-22-43, July 13, 2022, source. While some focus group borrowers may have had older loans from the Federal Family Education Loan Program, unless otherwise noted, this paper refers to and discusses elements of the default system relevant to federal Direct Loans.

- Federal Student Aid (website), “Student Loan Delinquency and Default,” source

- Sarah Sattelmeyer and Jon Remedios, “Race and Financial Security Play Central Roles in Student Loan Repayment,” Pew Charitable Trusts, December 15, 2020, source; Sarah Sattelmeyer, Trapped by Default (Washington, DC: New America, July 27, 2022), source; and Sarah Sattelmeyer, Trapped by Default, Appendices, source

- In addition, the current cohort default rate is an insufficient accountability mechanism, especially during the payment pause.

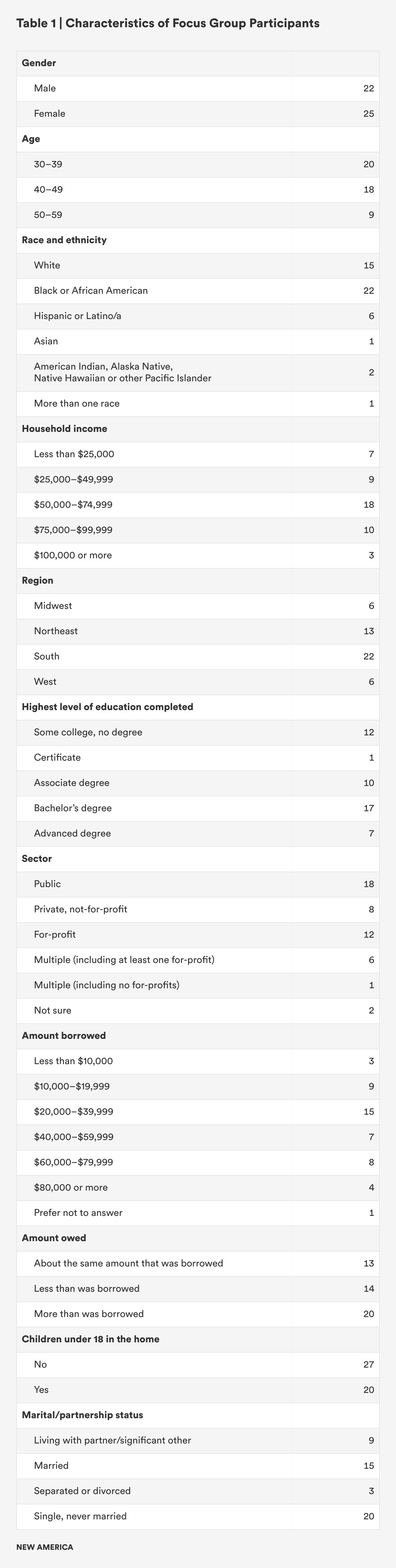

- While focus groups are not representative, these groups were recruited to ensure a mix of participants by gender, age, race and ethnicity, household income, region, level and sector of education, amount borrowed and owed, presence of children under 18 in the home, and marital/partnership status.

- U.S. Department of Education, “Biden-Harris Administration Continues Fight for Student Debt Relief for Millions of Borrowers, Extends Student Loan Repayment Pause,” Press release, November 22, 2022, source; U.S. Department of Education, “Biden-Harris Administration Announces Final Student Loan Pause Extension through December 31 and Targeted Debt Cancellation to Smooth Transition to Repayment,” Press release, August 24, 2022, source; Federal Student Aid (website), “COVID-19 Emergency Relief and Federal Student Aid,” source; and U.S. Department of Education, “Department of Education Announces Expansion of COVID-19 Emergency Flexibilities to Additional Federal Student Loans in Default,” press release, March 30, 2021, source. According to the Department, "payments will resume 60 days after the Department is permitted to implement the [debt cancellation] program or the litigation [currently blocking this program] is resolved, which will give the Supreme Court an opportunity to resolve the case during its current Term. If the program has not been implemented and the litigation has not been resolved by June 30, 2023—payments will resume 60 days after that."

- U.S. Department of Education, “Biden-Harris Administration Continues Fight for Student Debt Relief"; The White House, “President Biden Announces Student Loan Relief for Borrowers Who Need It Most,” fact sheet, August 24, 2022, source; Ben Miller, Who Are Student Loan Defaulters? (Washington, DC: Center for American Progress, December 14, 2017), source; and Thomas Conkling and Christa Gibbs, “Office of Research blog: Update on student loan borrowers during payment suspension,” Consumer Financial Protection Bureau blog post, November 2, 2022, source. The administration intends for the most recent payment pause extension to "alleviate uncertainty for borrowers as the Biden-Harris Administration asks the Supreme Court to review the lower-court orders that are preventing the Department from providing debt relief for tens of millions of Americans."

- U.S. Department of Education, “Biden-Harris Administration Continues Fight for Student Debt Relief"; and Federal Student Aid (website), “COVID-19 Emergency Relief and Federal Student Aid.”

- Danielle Douglas-Gabriel, “Appeals Court Grants Injunction Against Biden’s Student Loan Forgiveness,” Washington Post, November 14, 2022, source

- Federal Student Aid (website), “A Fresh Start for Federal Student Loan Borrowers in Default,” source; and Federal Student Aid, “A Fresh Start for Borrowers with Federal Student Loans in Default,” fact sheet, source

- Federal Student Aid (website), “If Your Federal Student Loan Payments Are High Compared to Your Income, You May Want to Repay Your Loans Under an Income-Driven Repayment Plan,” source

- U.S. Department of Education, “Proposed Regulatory Text for Issue Paper #10: Income-driven Repayment Plans,” Negotiated Rulemaking for Higher Education, Affordability and Student Loans Committee, 2021, source

- The White House, “President Biden Announces Student Loan Relief.”

- Federal Student Aid (website), “Income-Driven Repayment and Public Service Loan Forgiveness Program Account Adjustment,” source

- Federal Student Aid (website), “Public Service Loan Forgiveness (PSLF),” source

- Federal Student Aid (website), “Income-Driven Repayment and Public Service Loan Forgiveness Program”; U.S. Department of Education, “Education Department Announces Permanent Improvements to the Public Service Loan Forgiveness Program and One-time payment Count Adjustment to Bring Borrowers Closer to Forgiveness,” press release, October 25, 2022, source; and 87 FR 65904, source

- In addition, in November 2022, a judge gave final approval to a settlement with the Department granting cancellation to roughly 200,000 borrowers with outstanding borrower defense applications, among other benefits. Project on Predatory Student Lending, “Student Borrowers Win Final Approval of Settlement to Cancel Over $6 Billion in Loans for 200,000 Borrowers,” press release, November 16, 2022, source; and 87 FR 65904.

- U.S. Department of Justice, “Justice Department and Department of Education Announce a Fairer and More Accessible Bankruptcy Discharge Process for Student Loan Borrowers,” press release, November 17, 2022, source

- Sattelmeyer, Trapped by Default; and Sarah Sattelmeyer, “The Department of Education Seeks Bids for a Fifth Iteration of the Student Loan Servicing System Since 2016. How Did We Get Here?” EdCentral (blog), New America, May 20, 2022, source

- Michael Stratford, “Biden Administration to Cut Ties with Student Debt Collection Firms,” Politico, November 5, 2021, source; and David Harrison, “Biden Administration to Cut Ties With Debt Collectors for Student Loans,” Wall Street Journal, November 5, 2021, source

- Office of Information and Regulatory Affairs, U.S. Office of Management and Budget, Spring 2022 Unified Agenda of Regulatory and Deregulatory Actions, source

- U.S. Department of Education, “Unified Servicing and Data Solution (USDS) Solicitation,” May 19, 2022, source; and Sattelmeyer, “The Department of Education Seeks Bids for a Fifth Iteration.”

- U.S. Department of Education, “U.S. Department of Education Increases Servicer Performance, Transparency, and Accountability Before Loan Payments Restart,” press release, October 15, 2021, source; and Sattelmeyer, “The Department of Education Seeks Bids for a Fifth Iteration.”

Key Finding 1: Before Borrowers Entered Default, They Did Not Receive the Benefits Promised by Higher Education

Focus group participants reported going to schools that provided little support, often leaving without a degree or credential, and not being able to find stable employment, which contributed to their financial insecurity. But even among those who graduated and reported other benefits from a degree—such as the ability to have more control over work schedules and an expanded professional network—almost no one felt like their degrees or higher education experiences, especially given debt that they took on to get there, ultimately paid off.

Many participants did not receive a degree or credential

Those who do not complete a program of study are more likely to default on their loans, and many focus group participants reported leaving school without a degree or credential.1 While borrowers who do not graduate tend to hold relatively small amounts of debt—often less than $10,000—due to shorter periods spent in school, even smaller debt loads can be difficult to manage without the financial returns that can come from a college degree.2

Focus group participants also explained how their small balances grew and became more of a burden as interest accrued when they fell behind on their loans. One participant said that he had taken out “$5,000 or $10,000…30 years ago and I'm still paying on that…I know [my debt] is not astronomical, but I didn't get the degree out of it either.”

Focus group attendees noted that obstacles outside of their control prevented them from graduating. For example, many participants fell ill during college, struggled with a chronic illness, or had to drop out to care for a sick family member. One participant “went to school…over about a period of about 15 years or so” since he had to “keep dropping out and taking breaks…due to health issues.” Several of these borrowers were frustrated that their schools were not more accommodating, and others mentioned being frustrated by difficulties transferring credits and completing remedial classes.

Some borrowers cycled in and out of school for years, accruing debt along the way but never graduating. A number eventually hit limits on the amount of federal loans they could borrow or they defaulted on their existing student loans, preventing them from borrowing more to complete their degree.3 “It's the constant circle of couldn't finish, still have to pay back the loan,” said one borrower. “You need to go back to school to get a skill [but you] can't go back to school because you can't afford it and can't get a loan because you have this one.”

A sizable portion attended schools that did not pay off for them

While defaults are not limited to students in one sector, research indicates that a large portion of those who attended for-profit schools—roughly half—default on their loans.4 A Brookings analysis found that for-profit enrollees are 10 percentage points more likely to default, even after accounting for student characteristics and background.5

Multiple participants reported going to for-profit schools that closed or lost accreditation, which made it difficult to transfer credits elsewhere. While participants often questioned the value of their education, they were only sometimes aware that their schools misrepresented educational opportunities, the quality of their programs, and job placement rates. One borrower reported going to ITT Technical Institute, a for-profit college that ceased operations in 2016 amid evidence that it misled and defrauded students.6 He said, “I'm regretful that I took the loans, because I went to ITT and that school closed…it was a joke…I got straight A's in one semester, and I didn't even turn in the workbook of the assignments at the end of the year.”

Some participants experienced a compounding of setbacks, and they did not complete low-quality programs. One participant reported feeling “robbed” and not having anything to show for the debt he accumulated at a school that lost its accreditation. He noted that he had “spent the better part of 10 years working to get the experience that I would've gotten” if he had been able to complete a program at an accredited school.

Even some borrowers who got bachelor’s and graduate degrees defaulted

Those who complete bachelor’s degrees and attend graduate school are often left out of critical conversations about student loan repayment because they make up a small portion of those who default. But in the focus groups, borrowers indicated that the higher levels of student debt that come with such degrees—in all sectors of higher education—could be devastating when they did not see the income growth they expected.

While these focus groups do not allow disaggregation of the findings by race, research indicates that student of color, and particularly Black students, are more likely to have fewer resources to pay for college, attend historically underfunded institutions, be targeted by and enroll in for-profit schools, have student debt and borrow more, and see their student loan balances grow after leaving school than white students and borrowers.7 For some of these borrowers, even earning a college degree is not necessarily protective against default: Black graduates with bachelor's degrees default at higher rates than white students who do not complete a credential.8

Discrimination and credentialization in the job market also mean that women and students of color often need more education to earn amounts similar to their male and white peers.9 Many focus group participants described feeling like they kept losing out in a race for degrees and credentials. One noted that “you get a degree and it's not worth what you think it is…so now you're having to go back to school again, to get another degree on top…. You're in a constant quicksand of just reaching for something higher.”

Citations

- Rajashri Chakrabarti, Nicole Gorton, Michelle Jiang, and Wilbert van der Klaauw, “Who Is More Likely to Default on Student Loans?” Liberty Street Economics, Federal Reserve Bank of New York, November 20, 2017, source; Judith Scott-Clayton, The Looming Student Loan Default Crisis Is Worse Than We Thought (Washington, DC: Brookings, January 11, 2018), source; and Neha Dalal and Jessica Thompson, “The Self-Defeating Consequences of Student Loan Default,” (Washington, DC: The Institute for College Access & Success, October 2018), source

- Scott-Clayton, The Looming Student Loan Default Crisis; Miller, Who Are Student Loan Defaulters?; and Colleen Campbell and Nicholas Hillman, A Closer Look at the Trillion: Borrowing, Repayment, and Default at Iowa’s Community Colleges (Washington, DC: The Association of Community College Trustees, September 2015), source

- For more information about federal student loan limits, see Federal Student Aid (website), “The U.S. Department of Education Offers Low-Interest Loans to Eligible Students to Help Cover the Cost of College or Career School,” source. For more information about the consequences of default, including loss of eligibility for federal financial aid, see Federal Student Aid (website), “Student Loan Delinquency and Default,” source

- Scott-Clayton, The Looming Student Loan Default Crisis; and The Institute for College Access & Success, “Students at Greatest Risk of Loan Default,” April 2018, source

- Judith Scott-Clayton, What Accounts for Gaps in Student Loan Default, and What Happens After (Washington, DC: Brookings, June 21, 2018), source

- Danielle Douglas-Gabriel, “ITT Technical Institutes Shut Down after 50 Years in Operation,” Washington Post, September 6, 2016, source; and Project on Predatory Student Lending, Dreams Destroyed: How ITT Technical Institute Defrauded a Generation of Students (Cambridge, MA: Harvard University, February 2022), source

- Ben Miller, The Continued Student Loan Crisis for Black Borrowers (Washington, DC: Center for American Progress, December 2, 2019), source; Judith Scott-Clayton and Jing Li, Black-White Disparity in Student Loan Debt More Than Triples after Graduation (Washington, DC: Brookings, October 20, 2016), source; Krystal L. Williams and BreAnna L. Davis, “Public and Private Investments and Divestments in Historically Black Colleges and Universities,” issue brief, American Council on Education, January 2019, source; CJ Libassi, The Neglected College Race Gap: Racial Disparities Among College Completers (Washington, DC: Center for American Progress, May 23, 2018), source; Genevieve Bonadies, Joshua Rovenger, Eileen Connor, Brenda Shum, and Toby Merrill, “For-Profit Schools’ Predatory Practices and Students of Color: A Mission to Enroll Rather than Educate,” Harvard Law Review blog, July 30, 2018, source; and Diana Farrell, Fiona Greig, and Daniel M. Sullivan, “Student Loan Debt: Who is Paying it Down?,” JPMorgan Chase Institute, October 2020, source

- Scott-Clayton, The Looming Student Loan Default Crisis.

- Scott-Clayton and Li, Black-White Disparity in Student Loan Debt; Dorothy A. Brown, “College Isn’t the Solution for the Racial Wealth Gap. It’s Part of the Problem,” Washington Post, April 9, 2021, source; and Anthony P. Carnevale, Nicole Smith, and Artem Gulish, Women Can’t Win: Despite Making Educational Gains and Pursuing High-Wage Majors, Women Still Earn Less than Men (Washington, DC: Georgetown University Center on Education and the Workforce, 2018), source

Key Finding 2: Before Borrowers Entered Default, They Struggled to Access Affordable Payments amid Financial Insecurity

Even before the pandemic, borrowers who had defaulted were financially insecure, and the experience of attending low-quality programs without a financial return on investment and struggling to repay loans over months and years contributed to this insecurity. While focus group participants welcomed the respite from the ongoing pandemic pause in payments and collections, they had long faced economic instability, and most expected to continue to experience insecurity when repayment and collections resume.

A few borrowers defaulted soon after they entered repayment. But most took a winding path to default as they searched for solutions to their repayment difficulties. Some looked outside the student loan system, trying to increase their earnings by returning to school or by taking on another job. A few borrowers reluctantly turned to family members for help. And most participants tried to access repayment relief through the student loan repayment system but faced challenges navigating a complex repayment system and accessing all of the safeguards available to keep them out of default. These tools—and the assistance available to them from the Department and its contractors—were often inadequate and unresponsive to their financial situations. As they struggled to afford their car payments, rent, and child care, they fell farther and farther behind on their student loans.

Participants missed student loan payments, and eventually defaulted, because they were financially insecure

Borrowers’ financial insecurity was often caused by unemployment, injury, or illness. One borrower explained that he “couldn't make payments. [I] lost my car and my apartment, had to move back with my mom…and I got sick too…. I was struggling.” Another borrower reported that she “had [pregnancy] complications, so I had to quit working…[and] could barely take care of myself, let alone pay a student loan bill.” Multiple participants reported receiving public benefits from Medicaid and Medicare, the Supplemental Nutrition Assistance Program (SNAP), and the Temporary Assistance to Needy Families (TANF) program, among others.

Borrowers got behind on their payments when they had to choose between essentials and their loans.

“No one's going to pick paying their [student loans] over fixing their car.”

In a 2021 survey, most borrowers who defaulted reported doing so because they were not able to afford their payments (67 percent) or had other debt they needed to take care of first (71 percent).1 Participants in these focus groups paid other bills—including rent, transportation, groceries, utilities, and child care expenses—first, not because they did not want to pay down their loans, but because they had limited resources and put family well-being first. For example, one borrower said, “I was making consistent payments. And of course my car broke down… and I need my car to work or take my kids to sports. So you’ve got to choose, ‘Do I fix my car or do I pick my payments?’ No one's going to pick paying their [student loan] payments over fixing their car.”

Most borrowers were not able to enroll in an affordable repayment plan when they first struggled to repay

Throughout repayment, borrowers must make a host of complex decisions among a variety of repayment plans and options, including IDR plans, forbearances, and deferments. While the complexity of the repayment system affects most borrowers, achieving success can be particularly difficult for those with the fewest resources.2 Research from other fields, such as behavioral economics, and stories from recent focus groups and interviews highlighting borrowers’ experiences in repayment, underscore the fact that economic instability can chip away at the bandwidth that families have to manage complicated systems, especially when many are also using safety net programs, which have their own complex application processes and program requirements.3

For example, income-driven repayment plans calculate monthly payments based on a borrower’s income and family size, which must be recertified annually.4 Enrolling in these plans results in lower payments for many borrowers, and bills can be as little as $0 for those with earnings close to the poverty line, making them ideal for those struggling to repay their loans. In fact, borrowers in income-driven plans have lower rates of default.5 But despite IDR being the best option for many low-income and low-resource borrowers, it can be difficult to enroll and remain in these plans because of confusing annual paperwork requirements. Many who might benefit may not be able to access these programs and the forgiveness promised at the end of a lengthy 20 to 25 years’ worth of payments.6 And for some, these payments are still unaffordable.

In addition, the Department and its contractors have a history of providing inadequate information about IDR.7 The Department has reported ongoing concerns regarding borrowers' awareness of IDR plans, and the Department and its servicers have not consistently notified borrowers about these repayment options.8 And government oversight entities have turned up evidence of servicers directing borrowers to pause payments using forbearances even when they might qualify for an affordable IDR plan.9

As a result, most participants reported using forbearances to pause payments when they first struggled. When payments are paused, borrowers have a sure $0 monthly commitment, and the process for pausing payments using a forbearance can be quick, simple, and not require extensive paperwork. However, when their payments are paused, borrowers may see their balances grow due to interest accrual, and they can therefore pay more over the life of their loans.10

When borrowers’ payments are less than the interest that accrues on their loans in an IDR plan, their balances can also grow over time.11 However, unlike with IDR, while their payments are paused, borrowers are typically not making progress toward forgiveness. Rising balances—regardless of whether they occur through time spent in deferments and forbearances, IDR plans, delinquency, or default—also come with psychological consequences, as borrowers feel like they cannot make a dent in their debt and there is no end in sight.12 One borrower said that balance growth “feels like impending doom. You make payments, [but] it just feels like you're not getting anywhere because of the interest.” Another said that a growing balance “makes me feel like it'll never go away. Like I'm married to it. And it feels like no matter what I do, how hard I work to pay them off, they'll never go down because you're still accruing interest.”

Some borrowers described not knowing about IDR plans or being advised to try loan pauses when they first struggled to repay. While some participants may have been in repayment prior to widespread IDR eligibility, one borrower said that he “was just happy [to receive] the little three-month stall out. I was just doing that because that was the only option presented to me at the time.” This spring, the Department outlined new efforts to address inaccuracies in how payments were being counted toward IDR plans and to hold student loan servicers accountable for practices that “put borrowers into forbearance in violation of Department rules.”13

Balance growth “feels like impending doom. You make payments, [but] it just feels like you're not getting anywhere because of the interest.”

Other participants had been told about IDR but chose to pause their payments. Some were reluctant to enroll in IDR when their servicer could not promise an immediate, zero-dollar monthly payment. As one borrower said, “there were a couple other options [besides pausing], but it all involved money. So the only way to have no payment, which is the only thing I could afford at the time, was to go into forbearance.”

Participants used forbearances frequently, transitioning in and out of pauses or extending their pauses continuously. Generally, forbearances can be used for 12 months at a time and for a total of three years.14 Many borrowers reported “maxing out” these periods, and a recent New America analysis showed that a third of those who defaulted said they entered default because they had exhausted their ability to pause payments.15 While some participants knew that their forbearances were time-limited, others said that they were surprised when they hit the cap. Either way, most did not have a plan for other accommodations when their pauses ran out. One said, “I did so many forbearances that I maxed out. And at the time, what are you supposed to do? I couldn't afford it. So I just didn't pay.”

Some borrowers reported enrolling in IDR only after defaulting. Many participants built their knowledge of IDR plans over time through trial and error, interactions with the Department and its contractors, and their experiences in default. Those who were able to enroll—often after defaulting—noted that the plans were helpful in reducing monthly bills. (IDR usage may be higher for some borrowers after they default, given that one way to exit default, as described below, involves borrowers consolidating their loans and enrolling in an IDR plan.)

Many of these borrowers would likely have been eligible for a $0 payment on an IDR plan before defaulting.16 Even though more borrowers are enrolling in IDR plans today—and the Department will soon release proposed regulations and is implementing systems that address some of the challenges with IDR plans—focus group participants were still suffering from the consequences of their preventable defaults.

Citations

- Sattelmeyer, Trapped by Default.

- Sattelmeyer, Trapped by Default; Lindsay Ahlman, Casualties of College Debt: What Data Show and Experts Say About Who Defaults and Why (Washington, DC: The Institute for College Access & Success, June 2019), source; Scott-Clayton, What Accounts for Gaps in Student Loan Default; Miller, Who Are Student Loan Defaulters?; and Campbell and Hillman, A Closer Look at the Trillion.

- Sattelmeyer, Trapped by Default; Borrowers Discuss the Challenges of Student Loan Repayment (Washington, DC: The Pew Charitable Trusts, May 20, 2020), source; Jalil B. Mustaffa and Jonathan Davis, “Jim Crow Debt,” The Education Trust, October 20, 2021, source; Ernst-Jan de Bruijn and Gerrit Antonides, “Poverty and Economic Decision Making: A Review of Scarcity Theory,” Theory and Decision 92 (2022): 5–37, source; and Ahlman, Casualties of College Debt.

- Federal Student Aid (website), “If Your Federal Student Loan Payments Are High Compared to Your Income, You May Want to Repay your Loans under an Income-Driven Repayment Plan.”

- Income-Driven Repayment Plans for Student Loans: Budgetary Costs and Policy Options (Washington, DC: Congressional Budget Office, February 2020), source

- Borrowers Discuss the Challenges of Student Loan Repayment.

- Sattelmeyer, “The Department of Education Seeks Bids for a Fifth Iteration”; U.S. Department of Education, “Department of Education Announces Actions to Fix Longstanding Failures in the Student Loan Programs,” press release, April 19, 2022, source; Annual Report of the CFPB Student Loan Ombudsman: Transitioning from Default to an Income-Driven Repayment Plan (Washington, DC: Consumer Financial Protection Bureau, October 2016), source; Sattelmeyer, Trapped by Default; Federal Student Aid: Education Needs to Take Steps to Ensure Eligible Loans Receive Income-Driven Repayment Forgiveness (Washington, DC: U.S. Government Accountability Office, March 21, 2022), source

- Federal Student Aid: Education Could Do More to Help Ensure Borrowers Are Aware of Repayment and Forgiveness Options (Washington, DC: U.S. Government Accountability Office, August 25, 2015), source; and Education Needs to Take Steps.

- See, for example, Federal Student Aid: Additional Actions Needed to Mitigate the Risk of Servicer Noncompliance with Requirements for Servicing Federally Held Student Loans (Washington, DC: U.S. Department of Education, Office of Inspector General, March 5, 2019), source

- Borrowers’ balances may also grow due to interest capitalization. Once implemented, new regulations will eliminate most instances of capitalization going forward. Sarah Sattelmeyer, “Borrowers’ Student Loan Balances Are Growing Over Time. And It's Not Just Because of the Interest Rate,” EdCentral (blog), New America, May 12, 2022, source; and 87 FR 65904.

- Sattelmeyer, “Borrowers’ Student Loan Balances Are Growing Over Time.”

- Victoria Jackson and Jalil B. Mustaffa, “Student Debt is Harming the Mental Health of Black Borrowers,” The Education Trust, June 2022, source; and Sattelmeyer, Trapped by Default.

- U.S. Department of Education, “Department of Education Announces Actions to Fix Longstanding Failures”; and U.S. Department of Education, “Education Department Announces Permanent Improvements.”

- Federal Student Aid (website), “Student Loan Forbearance Allows You to Temporarily Stop Making Payments,” source

- Sattelmeyer, Trapped by Default.

- Federal Student Loans: Education Could Do More; Seth Frotman and Rich Williams “New Data Documents a Disturbing Cycle of Defaults for Struggling Student Loan Borrowers,” Consumer Financial Protection Bureau blog post, May 15, 2017, source; and Annual Report of the CFPB Student Loan Ombudsman.

Key Finding 3: When Borrowers Entered the Default System, They Got Trapped

When they entered default, focus group participants lost track of their loans as their accounts changed hands multiple times, and they heard from a variety of entities charged with explaining a complicated system. For some, their paychecks turned up short, and their tax refunds were unexpectedly garnished. When it was time to move, credit score damage often meant they could not live in the neighborhoods they wanted to or easily access funds to buy a more reliable car. In effect, the default process was clawing back money from the same low-income families that government safety net programs were simultaneously working to lift out of poverty.

Many struggled to identify and use available loan discharge options and other pathways to exit default, and others got stuck because they had no affordable way out. Interactions with servicers, collectors, and the Department left many borrowers confused and without adequate aid and information.

Severe financial consequences of default can push economically insecure families into (or further into) poverty

For example, once in default:1

- Borrowers’ wages can be garnished and their federal tax refunds and benefits—even those meant to prevent poverty, including the Child Tax Credit, the Earned Income Tax Credit, and Social Security—can be withheld.2

- Borrowers can be charged high collection fees.

- Borrowers experience damage to their credit scores, which can make it difficult or more expensive to get a car loan, rent an apartment, find employment, and buy a house.

- Borrowers lose benefits and protections that exist in the pre-default repayment system, such as access to IDR plans and the ability to pause payments.

- Borrowers are not eligible for federal financial aid if they want to or need to return to school, which is a potential path toward upward economic mobility for those who have not completed a degree or credential or need an additional credential.

- Borrowers’ professional licenses, in some states, can be suspended or cancelled.

- Borrowers’ balances grow because interest continues to accrue, which is not common when borrowers default on other types of loans.

The government and its contractors can collect using multiple mechanisms at the same time, meaning that some borrowers, for example, may have their wages garnished while also having federal benefits withheld. As a result, borrowers can pay more, and more quickly, after they enter default than they are required to when they are current on their loans. And there is no statute of limitations for collecting federal student debt.3

The default process was clawing back money from the same low-income families that government safety net programs were simultaneously working to lift out of poverty.

Low credit scores prevented participants from buying homes, living in convenient and safe locations, affording reliable transportation, and accessing employment opportunities. Credit score drops were the most commonly mentioned consequence in the focus groups. Low credit scores can affect job opportunities and quality of life by limiting transportation and housing options. Credit scores can also interfere with employment in a more direct way. One participant explained that a potential employer turned him down for a job because of his low credit score, a practice which is legal in most states.4

The credit score damage is the worst. It affects every aspect of adulthood. Home ownership has been difficult because of my student loans, even though I'm repaying them.

As a direct result of a hit to the credit score, I've had trouble. There have been times when I've had to move in a pinch and not been able to find an apartment because of the low credit.

Wage and tax garnishment prevented borrowers from building a financial cushion or investing in the well-being of their families. Some participants described feeling crushed when they realized they no longer had funds to dedicate towards their children. Others noted that a garnishment ate into their already low pay and prevented them from being able to handle any unexpected expenses. A recent New America analysis found that almost all of those who reported experiencing garnishment while in default said the collections caused financial hardship.5

I wasn't expecting it, and I have kids. That big chunk that you get every year [in tax refunds] is a big help to take care of your household. And when I had $5,000 or $6,000 taken away from me… it hurt.

At that point you don't have the option of whether you're going to pay it this month or if something is more pressing, you need something at the house, or your car breaks down or whatever, it doesn't matter. They're taking it, regardless.

High collection fees slowed participants’ efforts to get out of default. One participant said, “the collection fees sometimes were the amount of my payments…[I was paying] nothing towards the actual loan. [I] was paying the collectors money instead.” According to a recent survey, almost half of those who defaulted said they had experienced collection fees, and over 80 percent of that group felt like the fees damaged their finances.6

“That big chunk that you get every year [in tax refunds] is a big help to take care of your household. And when I had $5,000 or $6,000 taken away from me… it hurt.”

The loss of access to federal financial aid closed off an important route to higher earnings—completing a degree or credential. For a few participants, losing access to student loans and federal financial aid was the end of a dream of upward mobility. (In a recent survey, about one-third of those who defaulted said they were unable to obtain more financial aid for school.7) These participants felt that the loss kept them locked out of the education they hoped would end their financial struggles.

I wanted to get a college degree. I wanted to become a sociologist…. So, when I wound up in default, it was basically the end of that dream.

While I was in default…I couldn't return to school and finish my degree that I was so close to getting because I wasn't able to receive further financial aid or loans at the time.

Many participants did not understand the consequences of default, which impeded their ability to avoid them or plan for the future. While a few did know about these penalties, most were surprised when they saw their wages or tax returns had been garnished. Many people also reported finding out that they were in default through a credit report.

They would take my whole income tax refund and put it towards my student loans…. Not knowing that the first time around was heartbreaking.

I wasn't aware of what was going on with my loan until I saw the drop in my credit score and how many payments I actually missed.

Many struggled to exit default

Borrowers have limited pathways out of default, some of which can be used only once, and borrowers face different processes and fees for each option.8

- Full loan payoff: Borrowers can exit default by paying their full outstanding principal, interest, and any related collection fees voluntarily. Borrowers can make these payments all at once or over time, including through involuntary payments like garnishments.

- Rehabilitation: Borrowers can enter into a rehabilitation agreement and make nine payments within a 10-month period to exit default. Payments can be as low as $5 per month. This option can typically be used only once, and it removes the default from a borrower’s credit history.

- Consolidation: Borrowers can also exit default by consolidating their loans into a new loan in good standing and enrolling in an IDR plan or making three payments. Borrowers can typically only consolidate their loans once and the default remains on their credit history.

- Settlement agreements: In some cases, borrowers may be able to negotiate terms to close out a loan.

- Discharge or cancellation: Borrowers in default may be eligible for existing loan discharge programs, as described below.

Participants were unsure about the pathways that were available to exit default. Given the complexity of the system, many borrowers reported being reliant on the options presented to them by those collecting the debt instead of having a whole picture. One borrower said, “I thought [exiting default] was just doing whatever they said.” In fact, a recent New America analysis found that almost one-third of those who exited default were not sure how it happened.9

Some participants did not know whether they were currently in default.10 Often, these participants had resigned themselves to being stuck in default because they did not have money and the process to exit was too confusing, complex, or overwhelming; as a result, they no longer checked in on the status of their loans. The pandemic pause also added to this uncertainty and confusion.11 “It's gotten to the point where I don't even know if I'm in default,” one borrower said. “My loans aren't even hitting my credit score, so it's kind of like I don't know what's happening anymore.”12

Often, participants resigned themselves to being stuck in default because they did not have money and the process to exit was too confusing, complex, or overwhelming.

Participants most commonly reported exiting default through rehabilitation. Federal data from 2018 show that far more dollars are typically collected through rehabilitation than consolidation.13 Previously, collectors may have been directing more borrowers to rehabilitation because their contracts compensated them more for rehabilitation than consolidation. They received a flat payment of $150 for a consolidated loan that entered an IDR plan and over 10 times as much for a rehabilitated loan.14 One borrower said, “the only way that I knew of [to exit default] was to make these small, scheduled payments every month on time and that was the plan I made and I agreed to.” While some borrowers were able to exit default via rehabilitation, at least one reported not being able to do so. And several borrowers noted being directed to make payments that did not lead to rehabilitation or exiting default.

Fewer participants described using consolidation, and historically, fewer borrowers have exited default through consolidation than rehabilitation.15 But borrowers who did use consolidation may have also been less aware of that process as it was happening. This could have been because borrowers can consolidate their loans when they are in good standing, consolidation is typically faster than rehabilitation, and consolidation may not involve making payments. One borrower who likely used consolidation to exit default described it as having “switched over to where they basically refinanced [my loans] somehow and it lowered the payments down tremendously.”

A few participants exited default by paying off their loans when they started making more money. Some believed that the only way to exit was by making enough—either through getting a better paying job or working multiple jobs—to pay down their loans. One participant said that he was able to get out of default because “I was doing really well business wise: I had a full time [job] and was just working my side hustle and just caught up and started paying [my loans].” These participants were rare; most continued to struggle with low incomes for years.

Many got stuck in default because they saw no affordable paths out. Research indicates that getting stuck in default is common. Among a cohort of students who entered school in 2003–04, the typical defaulter remained in that status for almost three years; 30 percent who defaulted had not exited default five years later.16 In the focus groups, borrowers reported that they got stuck for two main reasons: they did not know there were low-cost ways to leave default or they had previously defaulted and had no remaining low-cost paths available.

Some borrowers assumed that, without more money, there was nothing they could do to exit default. Some of these participants remained in default for years. One said, “I was just in distress with my life and…I noticed one of my checks got garnished and I couldn't really do a plan to pay that back, [because I had] this little meager job. It was months before I did anything about with it, because I didn't have any money.”

Some borrowers who defaulted multiple times may not have had any affordable way out of default. Borrowers can get stuck in default if they have already consolidated and rehabilitated their loans, as these options can typically be used only once. Borrowers can also exit through a settlement agreement (which is rare), discharges (many of which have historically been difficult to access), and by fully repaying (an option that is out of reach for many). The Consumer Financial Protection Bureau has warned that for some borrowers, “a subsequent default may be a permanent barrier to critical borrower protections.”17

There was probably some confidence that I could get back on track and do this and maintain it. But [I had] other student loans to pay, so I got behind again. And then I believe I defaulted on that same loan again….And that's been over the course of probably 10 or 15 years.

Eventually, I went back in default, and that's when they started taking my taxes. And I've been in default pretty much since then. So it's been rough, because when I do my taxes, I get paranoid, and I start dreading doing my taxes. I'm like, “They're going to end up taking them.”

For a few participants, staying in default felt easier than attempting to get out and make regular payments. A couple of borrowers mentioned deciding to use wage garnishment almost like an automatic payment for their loan debt. “I told them, ‘Just go ahead and garnish my paycheck.’ It just made it a lot easier than for me to have to keep remembering, set an alarm, or while I'm at work go make a payment,” one borrower said. This suggests both that these borrowers may not have fully understood the consequences of and ways out of default and that they valued automatic solutions to repaying their loans.

There were mixed outcomes on post-default trajectories. Some borrowers reported that their new payments were more manageable, including several who had entered an IDR plan. A few had taken on an extra job or experienced improved economic conditions that allowed them to make progress paying down their loans. But others said that their new payments continued to be unaffordable. These borrowers defaulted again after reentering a repayment system that had not served them well the first time around, without any new accommodations.

Forgiveness options were not advertised or accessible

A host of programs exist that provide access to loan discharges and forgiveness for federal student loan borrowers, as noted in the “Recent Initiatives that Benefit Borrowers in Default” section.18 Borrowers may also be eligible for other programs based on the types of loans they have, their occupations, and their experiences while in school, among other factors.

Borrowers reported learning about forgiveness and discharge programs primarily from friends, family, and their own research. A few people described outreach that may have been from the Department and its contractors or their schools, but this was not the norm. The Department does not always require this outreach, and large-scale promotional campaigns have typically not been conducted. The lack of official guidance is compounded by misinformation and scams related to loan discharge, which makes it challenging for borrowers to know whom to trust and how to understand their eligibility for various programs.19

As a result, many borrowers were unfamiliar with discharge programs or unsure about how to access them. Given recent actions and reforms made by the Biden administration, many of these borrowers may now be eligible for automatic discharges. But others still need to apply or file a claim.

Some reported being put off from applying for PSLF by the cumbersome and confusing processes, failures in program administration, and rarity of success stories, barriers that have received increasing attention in recent years.20 Time spent in default does not count toward PSLF. But many borrowers explained that PSLF was not an option for them because, when they were in good standing on their loans, they had tried and failed to access the program.

One borrower said, “I've heard so many horror stories about getting that to actually work that I never hedged my bets on it.” Recent actions by the Department have made this program easier to access and qualify for, and some borrowers can become eligible over time by consolidating their loans or working for longer periods or for different employers.21 But only one borrower said that she reapplied, since the program has “new qualifications…[and] people are saying it's easier to get the student loan forgiveness.”

Knowledge of IDR forgiveness was extremely low among focus group participants, even though knowledge of and experience with IDR was relatively high. While time spent in default does not currently count toward forgiveness in any IDR plan, borrowers in IDR plans in good standing on their loans often talked about expecting to pay back their student loans forever instead of working toward forgiveness. The Department recently took action to correct past failures in administration of IDR, which will make it easier for borrowers to access these plans and get credit toward loan forgiveness for previous time spent in repayment.22 However, a recent report by a government watchdog confirmed that much communication about IDR plans from servicers and the Department has historically failed to mention IDR forgiveness and that the Department’s guidance does not always require this disclosure.23

Participants who reported being defrauded by their schools expressed confusion and limited knowledge about discharge options, including borrower defense to repayment discharges. Not many participants understood this type of discharge. Among those that did, several mentioned barriers to applying or knowing how to access relief. Some of this confusion likely stems from the fact that, in recent years, the borrower defense policy has shifted considerably in terms of what borrowers need to do to access and be eligible for discharges. (For some, that relief may be automatic.) One borrower said that in “the news where student loans are going to be forgiven, I always hear my school…I see my school pop up. So it's like, all right, great. Do I need to do anything?”

Several borrowers went to schools that closed but did not know about or had not received a closed school discharge. While many borrowers can now receive a closed school discharge automatically, that has not always been the case. To access a closed school discharge, borrowers in the past, and some still today (once new regulations are implemented in 2023), are required to complete a short application about their enrollment histories. Some felt like the process as they understood it was too complex or they overestimated the complexity of what would be required. One participant said, “I had to prove that my school closed and all that…I feel like it was just too complicated to even try. Yeah. That's why I didn't even do anything, I think, at the time, because I was just like, ‘Oh, just more paperwork and stuff.’”

Despite a high level of reported medical and health issues, knowledge of disability discharges was also low among focus group participants. Many disabled borrowers also faced challenges accessing care, which, in addition to a lack of knowledge and information from the government and its contractors, could have been a barrier to getting a diagnosis that would have made them eligible for a discharge.

Interactions with servicers, collectors, and the Department left many borrowers confused and without adequate aid or information

When borrowers are in good standing on their loans, servicers manage their accounts, help borrowers access repayment plans and options, and collect payments. Once borrowers default, they are transferred to the Department and, until 2021, many were assigned to a private collection agency. Previously, these collectors were governed by different rules and incentives, received different types of compensation, and were subject to different types of oversight than servicers. If borrowers exit default, their accounts are transferred back to servicers.

Most participants experienced the repayment system as a continuum: they did not understand that the repayment and default systems were separate and run by different contractors.24 One borrower said, “I don't really know how it works anymore, or who is a collection agency, or who is just the student loan [servicer].” This caused borrowers to be confused—reasonably, because they were hearing from myriad organizations—about the rules governing their loans, and borrowers sometimes used the terms “servicer,” and “collector” interchangeably. Another borrower said he was “just kind of confused because I didn't know how it worked and I didn't know that they had collections for student loans.”

When loans were transferred between contractors, borrowers had trouble keeping track of their accounts. The Department and its contractors made these transfers as borrowers moved between the repayment and default systems, between and among servicers as servicers left the system, and away from collectors as the Department ended its contracts with them. Borrowers reported feeling confused and frustrated when they had to track down and establish a point of contact with yet another company. This system also made it difficult for borrowers to make sense of which rules applied to their loans and when, who was contacting them, and why.

I wasn't sure who I should…make payments to….I just didn't have faith in it, because I didn't even really understand the process of transferring.

I've had so many loans that have been transferred that it's hard to keep track of which ones went where.

People viewed their engagement with both servicers and collectors as a negotiation, which could have contributed to feelings of confusion and frustration. To borrowers, communicating with a debt collector to establish a payment as part of a rehabilitation plan to exit default, selecting a pathway to consolidate loans, or engaging with a servicer around different IDR plans could feel very much like a compromise or mediation instead of a discussion of options.25

I would have to negotiate after they called me. I pick up their phone [call]; we'd negotiate. "Okay. Well, I'm able to pay this price or I'll make payments."

I felt like they were just fishing for more information. They were trying to see what they could get out of me as far as maybe building their attack plan for getting money out of me, whatever they could do.

As a result of interactions with different entities, loan transfers, and general confusion, outreach from servicers and collectors often seemed like spam. This made it difficult for borrowers to know whether and when they were talking to legitimate entities, and it contributed to their not engaging with the system at all. Participants were right to be wary: student loan-related scam calls are rampant.26

One of the focus group participants reported that he got scammed and paid a company that was not his loan servicer or collector for years. “When I was paying a different company for three years straight, I just believed them…[but]I found that it was a scam,” he said. “I asked the attorney general to look into it. He says other people have problems with this company. So now, I may be part of a class action lawsuit against them.”

When borrowers missed payments, many reported hearing from servicers and collectors. This is often how struggling borrowers found out about their options for handling their loans, especially forbearance and deferment. Borrowers also reported that servicers checked in at other inflection points, like for IDR recertification, for example.

Right away when I missed a payment, they provided the options to me about going to deferment or forbearance. And so I was grateful because I didn't even know that I had the option. I just thought I was doomed….They [also] contact me when it's time for me to renew my IDR.

If I missed a payment on the due date, literally by the next day, or two days later, they would contact me and remind me or ask me, “is everything okay? We noticed you didn't make a payment or [we] didn't receive it on time,” stuff like that. So it was helpful in that part.

Many borrowers felt like servicers, collection agencies, and the Department did not provide all of the information they needed, options they should consider, or relief for which they were eligible.

However, even with perfect program implementation, some borrowers in default may be hard to reach—or have lost touch with or not received or acted on communication from the Department and its contractors—making it more likely that they had insufficient information. A government report released in January indicated that contact information is missing for one-quarter of borrowers in default.27 These borrowers, some of whom likely move frequently, may also not have known whom to reach out to about their loans.28 In addition, when borrowers got confusing information from their contacts or heard that no accommodations were available, they often believed that was final and stopped communicating. One borrower explained that “I know I'm in default and…after they told me that I could not do the income-based thing, I just stopped checking.”

But borrowers did report reaching out to their debt collectors in response to the consequences of default. While the consequences—or threat of those consequences via communications from the Department and its contractors—“motivated” participants to bring their loans back into good standing, this was motivation in the way that a fire is motivation to leave a burning house. The consequences made the student loan the biggest emergency in a life full of other crises.

I'm like, "What do I have to do…so I won't have my wages or income tax and things like that taken away?" And they were able to help me there, set me up on a temporary plan where they had my checking account number and they took out so much money a month so I could get out of default.

When they took my income tax away, I reached out to them because I'm like, "I don't want this to happen again." I think that's the only choice they gave me.

Once communication was established, results were mixed. Many participants had good things to say about their student loan contacts, especially that they were friendly and helpful and did a good job explaining certain processes. One borrower said, “nobody wants to hear from a collector…but they were very helpful in trying to make it work for me.” Some borrowers also reported noticing improvement in communication over time. For many, the online systems operated by the Department and its contractors felt convenient and effective. Borrowers said that “it's pretty easy to go on the website and pay” and the online system “gives you all kinds of information…[like] different plans that you can choose from.”

But many borrowers felt like servicers, collection agencies, and the Department did not provide all of the information they needed, options they should consider, or relief for which they were eligible. As noted above, few knew about IDR forgiveness and other options for discharges, many did not understand key aspects of forbearance and deferment, and few were prepared for the garnishments, tax withholding, and credit score drops that followed their loan defaults. Since borrowers did not have a comprehensive understanding of the system or the pros and cons of various options, they felt reliant on the options suggested to them by servicers and collectors.

As far as required communication, yeah, I'm sure they fit the bill, but as far as being overly communicative, I don't think they were. And…I remember it being just sort of confusing, and it didn't really lay out all the options.

I was never asked any questions based on what I can afford, or given any options.

And some participants felt harassed, especially by collection agencies, interactions that left participants feeling even more overwhelmed.

When I went into default…all the collectors…were rude and so I just got to the point where I wouldn't even—I'd just hang up on them.

[The collectors are] trying to get the most out of you because it's business. Again, [you are] treated as a number…[and] over time you start getting these phone calls and then you start taking it personally. Like, am I the only guy in America that's defaulted on my student loan? Give me a break.

Citations

- This information is pulled from: Federal Student Aid (website), “Collections on Defaulted Loans,” source; Sattelmeyer, Trapped by Default; and Sattelmeyer, Trapped by Default, Appendices.

- Carolyn Carter and April Kuehnhoff, “Starting July 15: Protecting the Monthly Child Tax Credit Payments from Creditors,” National Consumer Law Center, July 13, 2021, source; Persis Yu, “Voices of Despair: How Seizing the EITC is Leaving Student Loan Borrowers Homeless and Hopeless During a Pandemic,” National Consumer Law Center, November 10, 2020, source; and Social Security Offsets: Improvements to Program Design Could Better Assist Older Student Loan Borrowers with Obtaining Permitted Relief (Washington, DC: U.S. Government Accountability Office, December 19, 2016), source

- Sattelmeyer, Trapped by Default.

- Amy Traub and Sean McElwee, Bad Credit Shouldn't Block Employment: How to Make State Bans on Employment Credit Checks More Effective (New York: Demos, February 25, 2016), source

- Sattelmeyer, Trapped by Default.

- Sattelmeyer, Trapped by Default.

- Sattelmeyer, Trapped by Default.

- This information is pulled from: Sattelmeyer, Trapped by Default; and Sattelmeyer, Trapped by Default, Appendices.

- Sattelmeyer, Trapped by Default.

- Confusion among all defaulted borrowers is likely even greater than described in this report, given that these focus groups were conducted with borrowers who knew they had been in default or collections or knew they had experienced the consequences of default.

- Federal Student Aid (website), “COVID-19 Relief: Loans in Default,” source. Months that borrowers in default spend in the payment pause count as payments in a rehabilitation agreement.

- Federal Student Aid, “A Fresh Start for Borrowers with Federal Student Loans in Default.” After seven years of missed payments, defaulted loans fall off of borrowers’ credit reports.

- Federal Student Aid Data Center (website), “Default Rates,” source

- U.S. Senate Committee on Health, Education, Labor, and Pensions, “Questions Submitted by Senator Patty Murray,” source. Guarantors of loans made under the Federal Family Education Loan Program also had incentives to resolve defaults via rehabilitation.

- Update from the CFPB Student Loan Ombudsman: Transitioning from Default to an Income-Driven Repayment Plan (Washington, DC: Consumer Financial Protection Bureau, May 16, 2017), source