Table of Contents

II. Applying: Application and Eligibility

Even when people are aware of tax credits, requesting support presents its own set of emotional and procedural barriers, and the ultimate filing action is intimidating and complex.

Many Fear an Honest Mistake on Their Tax Return Could Lead to Serious Consequences

For many people, filing taxes and claiming tax credits doesn’t just feel complicated; it feels risky.

“If you mess up, you can go to jail.”

—Survey respondent, <$10,000 annual household income; hadn’t filed taxes in three years

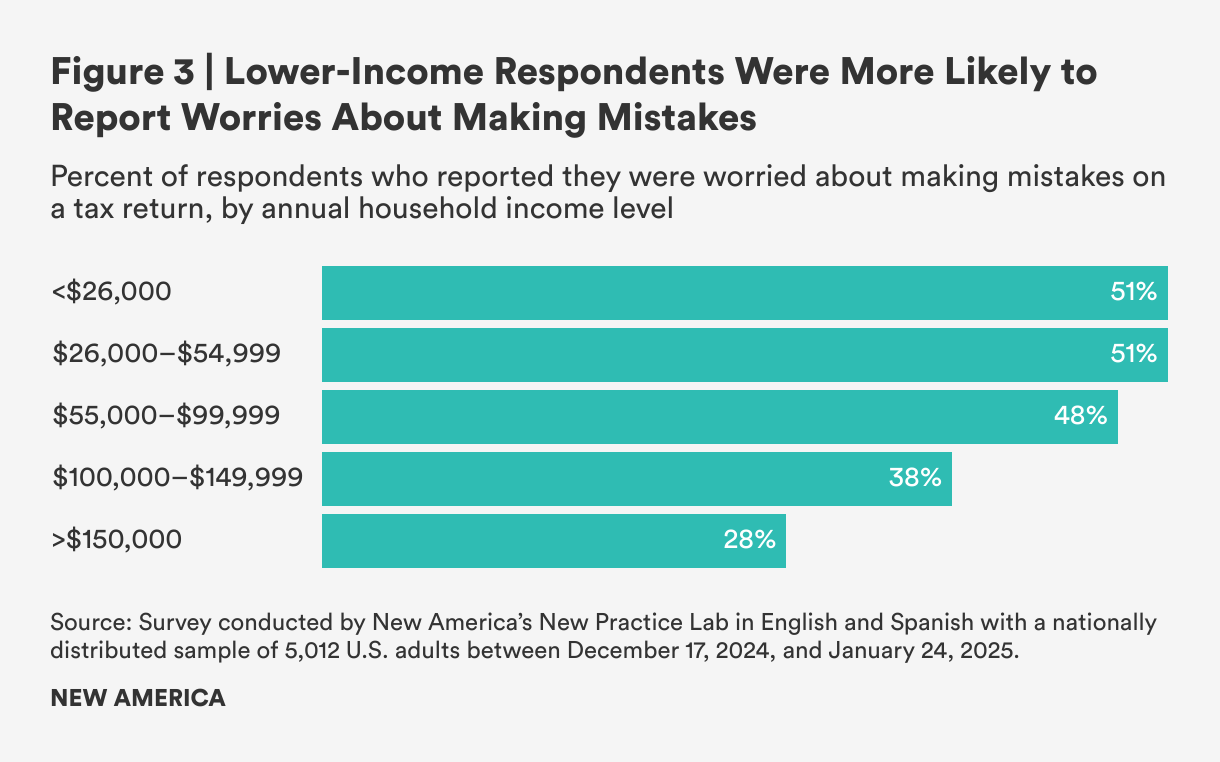

Across the country, people shared a common fear: that a simple mistake on their return could lead to penalties, audits, or even legal trouble. In our survey, more than half of the respondents identified the fear of making a mistake as a barrier to filing. This fear was especially acute among lower-income households: 51 percent of households earning under $26,000 cited it, compared to just 28 percent of those earning over $150,000 annually.

These fears have real consequences: 61 percent of respondents who were afraid of making mistakes had not filed taxes in the past three years. Even when they did file, they were more likely to miss out on tax credits (44 percent of people in this group said they had claimed tax credits before, compared to 55 percent of those who didn’t share this fear).

“I wasn’t properly taught how to do anything, and I don’t know where to begin. I’m scared I’ll do something wrong and be penalized for an honest mistake.”

“A friend I helped to file their taxes was afraid to claim any credits because he hadn’t filed since 2013.”

Overall, about one in four survey respondents (27 percent) said they found it difficult to file taxes because they had multiple income sources or jobs. While this number is not meant to represent all taxpayers, it signals a significant implementation barrier for credit access—especially as gig work and nontraditional income become more common. Sixty percent of gig workers and 54 percent of self-employed respondents reported being afraid of making mistakes. When asked about challenges they faced, gig or freelance workers shared that managing expenses and earnings was difficult:

“Complexity of gig work…tracking receipts, mileage, etc., makes taxes hard.”

“I’m not great at math.”

“When I work gigs or am self-employed, I have to report my earnings for taxes multiple times a year. It’s hard and confusing.”

Reducing perceived risk, especially for those with non-W-2 income, is essential to improving participation and ensuring that those who qualify for support can confidently claim it.

Others shared how disconnected they felt from the tax system altogether:

“I’ve never really done taxes because I’ve always worked in construction, and people get a better deal when they pay cash.”

“Honestly, it’s been a very long time since I filed because for a lot of my younger years, I was terrible at keeping a job.”

This isn’t just a technical issue; it’s an emotional one. In a system that often assumes individuals are tax experts, or requires them to navigate complex rules and jargon on their own, the fear of getting it wrong can quietly and powerfully shut people out from critical support.

Filing Feels Too Complex to Do Alone, but Help Is Too Expensive

Filing taxes is supposed to help people access the money they’re owed, but for many, it comes with a price: in time, energy, or dollars they can’t spare.

The cost of filing was another commonly cited barrier to claiming credits: 36 percent of survey respondents identified cost as a barrier. For many, the decision to pay for tax help was driven not just by convenience but also by the fear of making a mistake. The desire for professional support often reflected a lack of confidence in navigating the process alone.

“I would like to e-file without using TurboTax so I could do it totally for free and not spend part of my refund on it, but I’m scared I’ll get it wrong.”

—Survey respondent, living in a household with two children; $10,000–$25,999 annual household income; filed every year for past three years

For low-income families already navigating instability, even a $40 software fee or a few hundred dollars for a preparer can mean choosing between filing and meeting a basic need.

“I had to skip paying my January electric bill in order to buy tax software.”

—Survey respondent, married with two children and working as a gigworker/freelancer; $10,000–$25,999 annual household income

“It’s like a mortgage payment.”

—Illinois study participant, a veteran, describing the cost of a tax preparer

“Taxes have to be on pause…there were so many years during the pandemic when there was so little work. You know, people have to eat. So the debt got big, and we’re still paying it off.”

—Illinois study participant, a mother and unpaid caregiver

Despite the cost, most survey respondents used professional tax help at some point. Of those who had filed in the past, 70 percent reported using a preparer, 15 percent filed on their own, and 16 percent filed with help from friends or family. Of those who filed on their own or with help from family or friends, 22 percent mentioned that they had done so because they did not know that free or cheap tax preparation services were available.

Those who used services like TurboTax (58 percent), H&R Block (36 percent), or IRS Free File (17 percent) appreciated the convenience, and over 90 percent said they would use a tax preparation service again, even though affordability still came up again and again as a barrier.

“It was hard to find completely free filing anywhere.”

—Survey respondent, a single parent with one child under six; $10,000–$25,999 annual household income

“Certain websites I’ve tried…like Credit Karma where everything was completely free, but you did everything yourself. It wasn’t like doing TurboTax online, where they help you a little bit.”

—Illinois study participant, a father and warehouse worker who filed taxes inconsistently

And even though many relied on tax preparation services for their ease of use and built-in error detection, 21 percent still ran into problems. Among those who reported issues with their tax prep experience:

- 28 percent said they had been charged unexpected or high fees

- 15 percent could not access free filing support despite seeking it

- 15 percent were encouraged to open financial products (e.g., refund anticipation loans or advance refund loans) that reduced their refund

For some, it just didn’t feel worth it. Respondents described skipping tax filing altogether because the effort or cost didn’t seem justified by the refund they expected. When filing feels complicated, and the financial return is uncertain or minimal, some decide it’s not worth the trouble.

“I had a CPA do them three years ago…paid $200, got a $28 refund.”

“I would love some help in claiming my tax credits for EITC. Figuring out the details is not worth the time and effort against the small amount of tax credits I might be able to claim.”

“It’s not worth it to go through the trouble to pay someone to do it if you don’t get much back.”

A third of respondents (34 percent) said they struggled to understand tax instructions or found the language too technical. This difficulty wasn’t due to a language barrier: 98 percent of respondents said they had accessed tax materials in their preferred language, even among those who found the jargon hard to follow.

“Don’t have all the correct W-2 forms or whatever they’re called…it’s too high-class, written for only college people, not for the blue-collar workers.”

“I don’t understand a lot of the questions being asked.”

“You have to learn the laws and the new rules and regulations each year.”

“I have a form of dyslexia with numbers. I don’t make enough money to pay someone to do them professionally.”

Of those surveyed, 27 percent of respondents mentioned that they found it difficult to file taxes because they had multiple income sources or jobs, and 25 percent did not know how to report self-employment or gig income. People shared how hard it was to know which documents were needed, what qualifies as income, or whether they’d done things correctly.

“This year is going to be difficult because I’m now self-employed, and I have no idea what I need or if I’ll even qualify for my child tax credits.”

—Survey respondent, living in a household with two children; $26,000–$54,999 annual household income; had filed every year for the past three years

Parents in the qualitative study in Illinois also mentioned that using online tax software like TurboTax helped them be more aware of tax credits. The platforms guided them through eligibility questions and clearly showed whether credits were applied.

But for those who filed on their own or with less-guided tax software, claiming credits required knowing exactly what to fill in, and many didn’t.

“I may not claim credits if I file without a professional…not sure whether or not I could get some sort of legal trouble for claiming something falsely—accidentally, of course.”

—Survey respondent, a single parent of three; unhoused; $10,000–$25,999 annual household income

Documentation and Identity Verification Challenges Block Filing

“I don’t know if I’m going to file that this year because I don’t really understand the 1099 form or know how or where to get it…it’s different from a W-2. Completely different.”

“I was homeless…my tent got flooded. I lost everything.”

For many, the filing process didn’t just feel expensive or difficult; it felt inaccessible. The act of filing breaks down not just because of technical tax forms or costs, but because people lack the documents, access to technology, or verification tools they need to even get started.

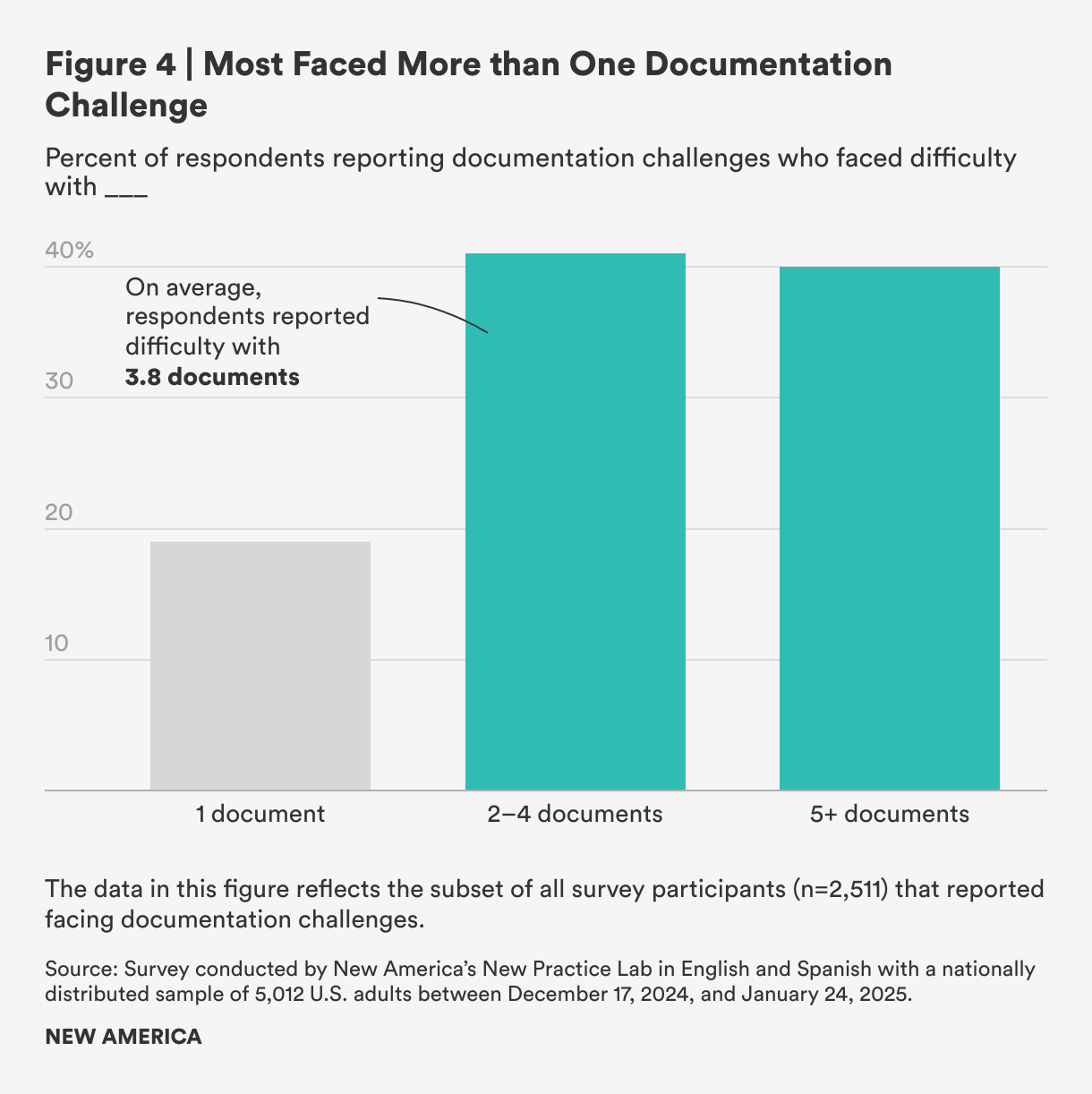

Fifty percent of respondents said they had trouble gathering documents. The most common challenges with documentation were missing wage documents (40 percent), missing proof of Social Security or Tax ID numbers (37 percent), difficulty documenting expenses (36 percent), missing or incomplete banking or financial information (33 percent), and difficulty documenting non-wage income, such as earnings reported on a 1099 (32 percent).

Crucially, of those who mentioned facing documentation challenges, 80 percent faced challenges with more than one document type (reporting challenges with 3.8 documents, on average), suggesting that these issues are layered rather than isolated incidents.

“Too much paperwork, too many questions. I don’t have any of my receipts from a couple of years back, and I don’t know how to file my taxes.”

—Survey respondent, living in a household with two children; hadn’t filed taxes in three years

Others told us about lost or expired IDs, difficulty obtaining or locating a spouse’s death certificate, or records destroyed in extreme circumstances—like the respondent who was living in a tent when a flood destroyed their paperwork.

Approximately 15 percent of survey respondents reported identity verification issues when trying to file. Among those who faced this challenge:

- 34 percent struggled with navigating ID.me

- 22 percent encountered mismatched records, such as outdated addresses, name changes, or incorrect Social Security numbers

- 20 percent couldn’t proceed because of errors on prior tax returns

- 20 percent said they simply did not have identity documents

“You have to wait to see if it’s accepted or rejected. I’ve been rejected about eight times! It was for something simple, like a wrong digit on my Social Security number. I didn’t understand what I was doing wrong…I called the IRS a few times and they finally explained it.”

—Illinois study participant, a mother and a part-time paid caregiver; had filed taxes inconsistently

Digital access was another limiting factor: 12 percent of respondents said they lacked access to a reliable computer or internet. People also mentioned that their phones had been stolen, their accounts were locked, or that they lacked a permanent address to receive or store tax documents.

“I couldn’t get my W-2—they were done digitally, and my phone was stolen. I’ve never been able to recover my account and don’t know how to proceed with filing my taxes.”

—Survey respondent, living in a multigenerational household with three children and one elderly dependent; $55,000–$64,999 annual household income; hadn’t filed taxes in three years

Recommendations for Implementation

Reframe Filing as Supportive—Not Punitive

“I want to be able to have that reassurance that I can come back to this…and say, “Hey, this wasn’t right,’ and they can double-check…and say, well, ‘Let's fix it together.’”

Perception matters. State Departments of Revenue (DORs) can help reduce fear and build confidence by shifting the tone of their communications and making it clear that trusted support is available.

Instead of focusing on enforcement, penalties, or compliance in outreach to economically vulnerable households, messaging should highlight the resources available to help along the way—like tax assistance centers, free filing tools, and clear sources of information—and focus on the real, tangible benefits of claiming tax credits, such as help with food, housing, or child care. While most state DORs may not have the capacity to coach people through their taxes directly, there are small, meaningful ways to ease anxiety and help people feel safer navigating the system.

How state DORs can reduce fear and build confidence:

- Emphasize financial support, not penalties. Make it clear that filing is an opportunity to access resources for low-income households, not just a legal obligation.

- Normalize mistakes. Communicate that the system allows for learning and correction. Filing shouldn’t feel like a one-shot test. Small missteps happen, and they can be fixed.

- Improve tone and clarity. Review and revise common messages (like error alerts, follow-ups, or help prompts) to be plainspoken, clear, and reassuring rather than intimidating.

- Offer simple guidance on common errors. Even one-pagers and short FAQs on frequent mistakes can help people feel more confident, especially if these are available early in the filing process or shared proactively.

- Include actionable links to resources. Provide links to free state-verified filing tools, community organizations, nonprofits offering tax assistance services, or even maps showing nearby Volunteer Income Tax Assistance (VITA) center locations—reinforcing that help exists and no one is expected to do this alone.

- Train frontline staff, community partners, and adjacent benefits agencies to reinforce supportive messaging. Many people are more comfortable asking questions in familiar spaces. Equip trusted intermediaries with talking points that reflect this tone.

By treating mistakes as normal and solvable and framing filing as a gateway to critical support (not a trap), states can make tax filing feel safer, more approachable, and more worth it for the people who stand to gain the most.

Expand Access to Tax Credit Options

Even with free and simplified tax filing tools, many low-income households face steep barriers to accessing tax credits. For these low-income households, especially those below the federal threshold for filing, the process of claiming credits like the Earned Income Tax Credit (EITC) or Child Tax Credit (CTC) should not require completing a full tax return.

Instead, states can design streamlined pathways that meet people where they are, using only the minimum information needed to verify eligibility (e.g., income, household size, or dependent status). This approach can:

- lower the barrier for people who aren’t otherwise filing

- reduce the risk of incomplete or inaccurate filings just to access benefits

- create a stronger safety net for those with the least financial and administrative bandwidth

Some public benefits programs have used simplified application processes:

- In April 2020, the IRS launched a non-filer tool to provide Economic Impact Payments (EIP) more quickly to those who did not have a return filing obligation, including those with too little income to file.

- The Supplemental Nutrition Assistance Program (SNAP) has introduced the Elderly Simplified Application Project (ESAP), which helps adults 60+ and those with disabilities by removing barriers to recertification—waiving interviews and using data crossmatches to verify eligibility—making it easier for vulnerable participants to maintain access to food benefits.

- The temporary 2021 Advance Child Tax Credit also demonstrated how tax benefits can be delivered proactively: Most eligible families received monthly payments automatically if they had filed taxes in 2019 or 2020 or used the EIP non-filer tool. Others could enroll through a simplified online portal designed specifically to help previous non-filers access the credit with minimal paperwork.

States can look to other proactive models. For example, in 2019, the Illinois Department of Revenue (IDOR) piloted a proactive and simplified approach to help eligible households access tax credits. It identified residents who had claimed the federal EITC, but hadn’t filed a state return and likely qualified for the state EITC. Rather than requiring a full return, IDOR offered a simple, secure pathway for people to claim their credit. The pilot helped over 22,000 Illinoisans access refunds and has since been integrated into the state’s regular workflow.

When combined with free simplified tools such as Direct File, these delivery choices can reduce administrative burden and increase critical tax credit access among low-income households.

States don’t need to overhaul the entire system to make progress. They can start by building flexible, lower-friction alternatives for economically vulnerable households most likely to benefit.

Support Through Tax Credits Shouldn’t Depend on Perfect Paperwork

Simplified filing has gained much-needed momentum in recent years—particularly efforts to pre-fill income using employer-reported wage data. About 20 percent of our survey respondents said they had trouble accessing their W-2s or wage information, and for this group, prefilled income data could make a meaningful difference in helping them access tax credits.

But for most, income reporting wasn’t the only or biggest hurdle. Eighty percent of respondents who faced documentation challenges dealt with far more complex issues: expired or missing IDs, identity verification problems, locked accounts, trouble tracking expenses, or paperwork lost during housing instability. These barriers can prevent people from completing the filing process, even if their income is correctly prefilled.

Simplifying access to wage data is one important piece of the puzzle, but it is not a silver bullet. To truly expand access, we need filing pathways that work even when paperwork is incomplete or hard to retrieve.

These could include:

- Simplified forms for accessing credits that gather only critical items needed for credit determination for low-income households that are not required to file taxes

- Opt-in programs that use existing state data, such as health and human services information, to estimate eligibility and conduct outreach to the right individuals (see next section)

- Partnerships with trusted intermediaries (like local caseworkers) who can help verify information

- Additional ID verification options, such as using documents already submitted in the past or to state benefits programs, or enabling in-person or video-based verification through community organizations

These approaches aren’t intended to replace full tax returns for most taxpayers, but they can help low-income households currently locked out of the system even when they are eligible for support.