Virtual Currency Donations

Table of Contents

- Executive Summary

- Introduction

- About Our Organizations

- Methodology and Terminology

- First Principles of Civil Society

- Blockchain and Digital Currency

- Use Cases

- Key Findings

- Other Findings

- Conclusion

- Appendix 1: Virtual Currency Terminology

- Appendix 2: International Highlights

- Appendix 3: Australia

- Appendix 4: Bermuda

- Appendix 5: Canada

- Appendix 6: Denmark

- Appendix 7: Malta

- Appendix 8: Singapore

- Appendix 9: South Africa

- Appendix 10: Switzerland

- Appendix 11: United Kingdom

- Appendix 12: United States

Abstract

This report, assembled by the Blockchain Trust Accelerator at New America with the support of the International Center for Not-for-Profit Law, assesses opportunities and obstacles in charitable donations of virtual currencies, and aims to bring civil society organizations, would-be virtual currency donors, and policymakers up to speed on the emerging trends across a number of different countries. In approaching this topic, we sought to answer a fundamental question: Can a civil society organization accept donations in virtual currencies—and, if so, how? We brought together an interdisciplinary team of public policy scholars, nonprofit experts, and attorneys to create an international survey of how different jurisdictions are regulating virtual currency donations. The results span 10 countries across five different continents: Australia, Bermuda, Canada, Denmark, Malta, Singapore, South Africa, Switzerland, United Kingdom, and the United States.

Acknowledgments

Contributors

Allison Price, Senior Advisor, Digital Impact and Governance Initiative and Blockchain Trust Accelerator

Ben Gregori, Policy Analyst, Digital Impact and Governance Initiative and Blockchain Trust Accelerator

John Miller, Legal Researcher, Blockchain Trust Accelerator

Jordan Sandman, Program Assistant, Digital Impact and Governance Initiative and Blockchain Trust Accelerator

Technical Support

Joe Wilkes, Media Relations Assistant, New America

Naomi Morduch Toubman, Data Visualization Developer/Designer, New America

This report is made possible by the generous support of the International Center for Not-for-Profit Law (ICNL). We are grateful for their support, and for the opportunity to work with Doug Rutzen, Julie Hunter, and the ICNL team.

The contents are the responsibility of the authors and do not necessarily reflect the views of ICNL.

Downloads

Executive Summary

In the wake of the 2020 Coronavirus outbreak, the Italian Red Cross (IRC) launched a virtual-currency fundraising campaign with a goal of raising at least €10,000 to purchase and set up an advanced medical post for pre-triage of COVID-19 cases.1 Virtual currency donations poured in. In three days, the IRC met its fundraising goal; in a week the organization nearly doubled it, receiving 50 different bitcoin donations—nearly all from anonymous or pseudonymous sources.2 Ten days later, the IRC launched a second fundraising initiative.3 This and other examples of virtual-currency charitable giving are emblematic of how donations in virtual currencies like bitcoin can impact civil society organizations (CSOs).4

On the other hand, virtual currency donations create new legal challenges around how charities, donors, and regulators should receive, solicit, report, and appraise these donations. Not all of these questions have clear answers; multiple bodies of law often overlap, and the novelty and complexity of some of these technologies has led lawmakers and regulators to take a wait-and-see approach, which has further accentuated existing gray areas.

This report, assembled by the Blockchain Trust Accelerator at New America with the support of the International Center for Not-For-Profit Law, assesses opportunities and obstacles in charitable donations of virtual currencies, and aims to bring CSOs, would-be virtual currency donors, and policymakers up to speed on the emerging trends across a number of different countries. In approaching this topic, we sought to answer a fundamental question: Can a civil society organization accept donations in virtual currencies—and, if so, how? We brought together an interdisciplinary team of public policy scholars, nonprofit experts, and attorneys to create an international survey of how different jurisdictions are regulating virtual currency donations. The results span 10 countries across five different continents: Australia, Bermuda, Canada, Denmark, Malta, Singapore, South Africa, Switzerland, United Kingdom, and the United States.

In approaching this topic, we sought to answer a fundamental question: Can a civil society organization accept donations in virtual currencies—and, if so, how?

Key Findings

As of May 2020, regulators worldwide are still relatively early on in their efforts to develop frameworks around virtual currencies. In the specific context of charities, the legal implications and practical applications are even more nascent. But even at this juncture, we see charities accepting virtual currencies in ways that advance their missions, adhere to best practices, and comply with the law. In many instances, virtual currency donations can be squared with existing laws—be they tax, charitable regulations, anti-money laundering measures, or complex combinations thereof. In some areas, charities and donors would benefit from further adaptation or clarification of the law. But under all circumstances, regulators should continue to allow for the reasonable application of law to virtual currency donations and consider the potential benefits they may have on civil society expansion, innovation, and the advancement of the public interest.

More broadly, while there has not been a concerted effort to catalog those donations—in part because they are frequently pseudonymous and challenging to track—our research found over USD $200 million in publicly-recorded donations of virtual currency. This $200 million is both a significant figure on its own and yet still a relatively small figure compared to total annual charitable donations, which are estimated to reach over $400 billion in the United States alone.5

In our research across ten countries, we also observed several broad regulatory trends:

- A wait-and-see approach has led to few or no regulations specific to virtual currency charitable donations, and little momentum towards banning them.

- Overlapping and sometimes conflicting bodies of virtual currency regulation or guidance, which complicates matters for charities and donors alike.

- The bulk of regulators’ attention in the virtual currency space has been focused on protecting consumers, investigating the issuance, sale, and promotion of digital tokens via “initial coin offerings” (ICOs), and prosecuting related scams.

- Some jurisdictions, such as Malta and Singapore, have attempted to position themselves as especially friendly to virtual currency activities and innovation; other bodies, such as the EU, have increasingly tightened regulations for virtual currency companies in a manner that could impede entrepreneurship and drive innovation elsewhere.

- To the extent charitable organizations can accept anonymous donations consistent with existing “know your customer” (KYC) or anti-money laundering (AML) guidelines, we found they should generally be able to continue to accept anonymous donations made using virtual currencies. In some countries, such as South Africa, is it not clear that AML/KYC rules apply to virtual currencies at all.

- A number of countries are exploring the issuance of their own sovereign virtual currency, often known as a Central Bank Digital Currency (CBDC). Depending on how they are designed and where they are launched, CBDCs could be given to a charity (anonymously or not), much like cash or a check today, and may eventually become as attractive a medium of donation as alternative virtual currencies.

Best Practices

Charities and CSOs interested in collecting virtual currency donations should generally adhere to guidelines for the acceptance of other non-cash donations. When in doubt, document (the value and means of donation), disclose (to tax authorities and regulators in compliance with appropriate laws, erring on the side of more disclosure rather than less), or decline the contribution (if there are serious concerns about a conflict of interest or donor motives). Charities starting to accept virtual currencies may also consider partnering with domestic, regulated virtual currency exchanges and/or custodians, in order to streamline processes around asset acceptance, custody, and liquidation.

For donors of virtual currency, best practices are similar to those applicable to donations of equity or property. If donors wish their donations to be tax-benefited, that usually requires giving to a tax-exempt domestic civil society organization (located in the same country as the donor), documenting the donation with a receipt from the charity, and claiming a tax benefit for the donor that year (often in the form of a deduction or a tax credit). As a rule of thumb, donors of higher amounts of virtual currencies hoping to receive tax benefits should obtain at least one independent, written appraisal of the value of their virtual currency donations and retain receipts of the donations.

For policymakers and regulators, putting forth consistent virtual-currency-specific tax and donation-compliance guidance could ease uncertainty and encourage more virtual currency donations. Direct engagement among regulators, industry, civil society, and consumers is often fruitful as well. In addition to less formal regulatory tools—like issuing non-binding guidance, conferring with virtual currency businesses, civil society, and consumers, and improving policy coordination—policymakers should continue to advance black letter law, like regulations, statutes, and case law, that would help both donors and recipient organizations alike in facilitating donations that are compliant with existing law and appropriately tax-benefited, where applicable.

Looking Forward

Charities, policymakers, and the citizenry they serve should continue to proactively engage one another and assess where and how the adoption or acceptance of virtual currency can, in fact, advance the public interest. We believe there is ample opportunity for additional research and public consultation on these topics. Among the questions for further inquiry: How should charities accept and custody virtual currency donations—and more generally, should policymakers develop regulations for virtual currency custodians and exchanges that more closely adhere to requirements placed on traditional banks, such as asset reserve requirements, deposit assurances, and regular audits of their holdings? Could regulators, policymakers, and/or researchers play a role in advising charities on these questions, including through the circulation of more detailed best practices, demonstrations, and explanations of security measurements and trade-offs?

We look forward to continuing engagement on these issues by key stakeholders. We hope this research can bring us closer to a world in which virtual currencies best help charities promote the public good.

Citations

- See COVID-19 Advanced Medical Post for Pre-Triage in Italy, Helperbit (started Mar. 12, 2020), source; See also, Felipe Erazo, Italian Red Cross Launches Bitcoin Fundraiser to Combat Coronavirus, CoinTelegraph (Mar. 14, 2020), source

- A Bitcoin transaction “is ‘pseudonymous’ (or partially anonymous) in that an individual is identified by an alpha-numeric public key/address[.]” Commodity Futures Trading Commission, A CFTC Primer on Virtual Currencies, LabCFTC (Oct 17, 2017) source at 5; See also generally, Assistant Professor Abhishek Jain, Lecture 9: Anonymity in Cryptocurrencies, John Hopkins University Computer Science Department CS 601.641/441: Blockchains and Cryptocurrencies (Spring 2018) source

- Samuel Haig, Italian Red Cross Coronavirus Bitcoin Fundraiser Smashes Goal, Issues New Initiative, Cointelegraph (Mar. 22, 2020), source

- While we use the umbrella term “CSOs,” we are referring mainly to organizations commonly called “charities,” encompassing organizations that are typically eligible for tax-benefited donations, although we recognize that in many countries the term “charity” has a specific legal meaning. Charities are often considered a subset of CSOs, but not all CSOs are charities. See, e.g., Marion R. Fremont-Smith, The Legal Meaning of Charity, Urban Institute Center on Nonprofits and Philanthropy (Apr. 2013) source (describing the legal meaning of “charity” in the United States); Charity Commission for England and Wales, What makes a charity (CC4) (Sept. 2013) source (outlining “what the law in England and Wales says a charity is”).

- Giving USA, Giving USA 2019: Americans gave $427.71 billion to charity in 2018 amid complex year fro charitable giving (June 18, 2019) source

Introduction

The report is conveyed as an analysis of public policy and international trends and does not offer or constitute legal advice. Do not rely solely upon this report for making or receiving donations or for any other purpose. Please confer with a local attorney, tax specialist, financial advisor, and/or other licensed professionals before making an individualized decision about virtual currencies, donations, or other matters.

In December 2017, the New York Times reported on an unusual act of generosity: A single pseudonymous donor going by the name “Pine” announced that they were an early adopter of Bitcoin, now looking to contribute millions of dollars' worth of Bitcoin to charities. Pine received almost 10,000 applications appealing to various charitable causes and listed the recipients and amounts of their donations in a transparent and timely fashion. By the time they were done, Pine had given over $55 million worth of Bitcoin to approximately 60 different charities.1

The example of Pine’s charitable Bitcoin giving is emblematic of how Bitcoin and other virtual currencies will impact civil society organizations. On one hand, there is a great opportunity: Charities could attract more resources through tax-benefited donations, they may be able to more easily receive donations with high speed, low transaction costs, easy auditability, and from pseudonymous or anonymous donors. Virtual currencies could allow civil society organizations to develop new models for distributing resources directly and quickly to beneficiaries. At a higher level, the meteoric rise of virtual currencies is also intertwined with matters of public interest such as financial inclusion, censorship resistance, privacy, and decentralization of power. Simultaneously, central banks are increasingly exploring state-created, and potentially more value-stable, forms of virtual currency.

Virtual currencies could allow civil society organizations to develop new models for distributing resources directly and quickly to beneficiaries.

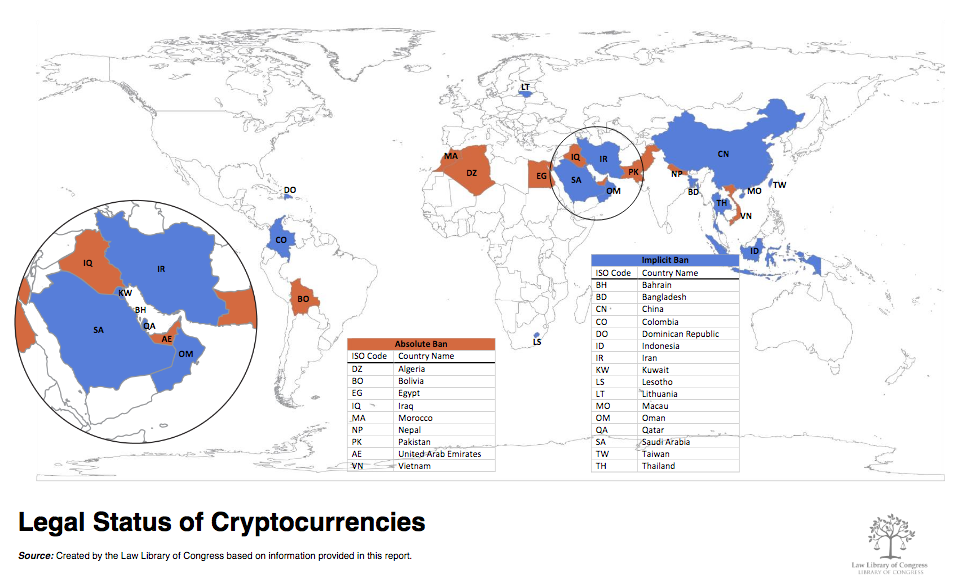

On the other hand, charitable donations of virtual currencies also present challenges: Legally speaking, there are questions about how and whether charities and donors should make, receive, solicit, report, and appraise virtual currency donations. Not all of these questions have clear answers. Multiple bodies of law apply in oft-overlapping ways in each country (and in some instances, within states or provinces). The novelty and complexity of these technologies have led many lawmakers and regulators to take a wait-and-see approach to rulemaking, which further accentuates existing gray areas. More generally, virtual currencies can also raise public policy questions around consumer protection, money laundering, tax evasion, and terrorist financing. In the absence of clear guidance, some jurisdictions—such as Algeria, Egypt, Nepal, and Pakistan—have explicitly banned the use of virtual currencies by private citizens and civil society organizations.2 Another challenge virtual currency donations have faced is steep declines in value among swaths of the virtual currency market since 2017, and, in some cases, extreme price volatility and allegations of market manipulation.3

As an overarching approach, we sought to answer a fundamental question: can a civil society organization accept donations in virtual currencies—and, if so, how?

This report assesses core opportunities and obstacles in charitable donations of virtual currencies, and aims to bring charities, would-be virtual currency donors, and policymakers alike up to speed on the emerging trends across a number of different countries surveyed. Just as the laws in many countries surrounding virtual currencies are still evolving, this report and accompanying appendices are offered as a living document. At the same time, we hope this research provides some clarity on accepting virtual currency donations and balancing various regulatory priorities. We view comparative analysis as a first and necessary step in helping regulators revisit, revise, and develop legal and regulatory frameworks that will leverage the strengths of virtual currencies and distributed ledger technology.

As of early 2020, countries worldwide are still in a relatively early phase for virtual currencies—whether it is Bitcoin, alternative forms of tokens, or central bank digital currencies. In the specific context of charities, the legal implications and practical applications are even more nascent. But even at this juncture, we see charities accepting virtual currencies in ways that advance their missions, adhere to best practices, and comply with the law. In many instances, virtual currency donations can be squared with existing laws—be it tax, charitable regulation, or anti-money laundering, or complex combinations thereof. In some areas, charities and donors would benefit from further adaptation or clarification of the law. But under all circumstances, regulators should continue to allow for the reasonable application of law to virtual currency donations and consider the potential benefits they may have on civil society expansion, innovation, and the advancement of the public interest.

Citations

- See Kevin Roose, Some Things About Tech Were Good in 2017. No, Really, The New York Times (Dec. 27, 2017), source ; Pineapple Fund, source (last accessed Jan. 23, 2020).

- See The Law Library of Congress, Global Legal Research Center, Regulation of Cryptocurrency Around the World (June 2018), source (listing the following nine countries as having an “Absolute Ban” on cryptocurrencies: Algeria, Bolivia, Egypt, Iraq, Morocco, Nepal, Pakistan, United Arab Emirates, Vietnam; another sixteen countries are listed as having an “Implicit Ban” on cryptocurrencies: Bahrain, Bangladesh, China, Colombia, Dominican Republican, Indonesia, Iran, Kuwait, Lesotho, Lithuania, Macau, Oman, Qatar, Saudi Arabia, Taiwan, Thailand.).

- See, e.g., Colin Wilhelm, New York AG raises flags over cryptocurrency manipulation, Politico (Sept. 18, 2018) source.

About Our Organizations

New America is committed to renewing American politics, prosperity, and purpose in the Digital Age. We generate big ideas, bridge the gap between technology and policy, and curate broad public conversation. We combine the best of a policy research institute, technology laboratory, public forum, media platform, and a venture capital fund for ideas. We are a distinctive community of thinkers, writers, researchers, technologists, and community activists who believe deeply in the possibility of American renewal.

The Blockchain Trust Accelerator (BTA) at New America is the world’s leading platform for harnessing blockchain technology to solve social impact and governance challenges. Established in 2016, BTA brings together governments, technologists, civil society organizations, and philanthropists to develop blockchain solutions that benefit society. BTA projects and research help organizations and institutions increase accountability, ensure transparency, create opportunity, and build trust in core institutions.

This report was made possible by a grant from the International Center for Not-for-Profit Law (ICNL). The International Center for Not-for-Profit Law works to improve the legal environment for civil society, philanthropy, and public participation in over 100 countries. ICNL works with partners from civil society, government, and the international community, developing long-term relationships to advance reforms. As the only global organization focused on the laws affecting civil society, philanthropy, and public participation, ICNL provides unique expertise.

Methodology and Terminology

The creation of this report involved a variety of methods. We brought together an interdisciplinary team of public policy scholars, nonprofit experts, and attorneys to create an international survey on how 10 countries across five different continents regulate virtual currency donations: Australia, Bermuda, Canada, Denmark, Malta, Singapore, South Africa, Switzerland, United Kingdom, and the United States.1 We engaged outside legal counsel and examined a wide range of primary and secondary sources, including regulation, scholarship, and legal commentary. Specifically, we consistently examined a series of detailed research questions across seven categories:

- Use cases

- Acceptance of donations of virtual currency

- Asset class, valuation, and tax issues

- Anti-money laundering (AML) and combating the financing of terrorism (CFT) measures

- Holding/liquidation

- Risks

- Other relevant (or emerging) legal issues, questions, or regulatory measures

Additionally, we researched and quantified existing use cases of virtual currency donations, namely through public sources of reporting and financial documents. New America drew upon its existing expertise, staff, and resources in areas such as blockchain, nonprofit regulation, tax law, and civil society, including past interactions with policymakers in foreign ministries, tax authorities, and securities agencies across a number of countries. We also conferred with select outside experts and showed them earlier drafts of our findings.2

This report assumes a fair degree of familiarity with terminology around taxation and virtual currencies. We generally use the term "tax-benefited" to mean the organization, and/or donations to it, offers some advantage to tax liability, such as tax exemption or an allowable donation deduction or credit on a tax return for the donor.3 Consistent with the European Union’s Fifth Anti-Money Laundering Directive (AMLD5), we use the term “virtual currency” (e.g. in lieu of “digital currency,” “cryptocurrency,” or “token”), broadly defined as “a digital representation of value that is not issued or guaranteed by a central bank or a public authority, is not necessarily attached to a legally established currency but is accepted by natural or legal persons as a means of exchange, and which can be transferred, stored or traded electronically.”4 Appendix 1 contains a list of key terminology pertaining to virtual currency technology. Throughout, we use the term civil society organizations (CSOs) expansively, consistent with the U.N. Development Program as including “all non-market and non-state organizations outside of the family in which people organize themselves to pursue shared interests in the public domain,"5 but our primary research focus is on organizations that are tax-exempt and offer some tax benefit to donors. While we refer to "CSOs" and "charities" often interchangeably in this report, we recognize that the term "CSOs" also includes some organizations for which donations might not normally be tax benefited, such as labor unions and professional or trade associations. The precise definition, regulation, and tax benefits of CSOs differ among nations.6

Citations

- These nations were selected to encompass various geographies, sizes of countries, and involvement with charitable giving, while still having a fairly developed set of laws that is generally translated and freely published.

- Special thanks to Joe Waltman, who reviewed earlier drafts of this document and provided critical expertise on local regulations and developments.

- See, e.g., Julia Kagan, What is a Tax Benefit?, Investopedia (May 8, 2018)

- Directive (EU) 2018/843 of the European Parliament and of the Council of 30 May 2018 amending Directive (EU) 2015/849 on the prevention of the use of the financial system for the purposes of money laundering or terrorist financing, and amending Directives 2009/138/EC and 2013/36/EU, Article I(d), source

- See, e.g., United Nations Development Programme, Annex 1: NGOs and CSOs: A Note on Terminology, 123 source (quoting the definition put forward by the 2007-2008 Advisory Group on CSOs and Aid Effectiveness, now adopted by OECD DAC).

- See infra at n.__[4].

First Principles of Civil Society

To achieve the right balance between encouraging private support for public problem-solving and ensuring that organizations—and the funds they raise and spend—are indeed serving the public interest, vibrant democracies regulate civil society organizations through tax exemption and beyond. Civil society is also subject to a variety of generally applicable regulations and specific laws, for example, about the registration of new corporate entities or the strictures of employment law. Across the world, many legislatures have gone beyond simply encouraging charitable donations: most effectively subsidize them, for example by allowing donors to receive a tax benefit and exempting CSOs from taxation. In return, lawmakers typically require CSOs to follow certain practices of transparency, accountability, AML compliance, and reporting. We conclude that policymakers can develop regulatory frameworks that maintain each of these principles without halting the growth of virtual currencies and associated donations.

In modern charitable giving, the vast majority of private capital that has been donated in support of public interest issues has been in the form of cash donations (fiat donations via checks, wire transfers, online donations, etc.). In addition, donations of non-cash assets—stocks, land, art, etc.—also can be a source of funding for some CSOs. In addition, new philanthropic models have developed, such as fiscal sponsorship arrangements, that permit support of a broader array of charitable projects, including those housed in non-charities or in foreign entities, in a tax advantageous way.

Against that backdrop, this project is designed to help regulators and donors better understand how best to apply existing rules governing charitable giving amid the new wealth and opportunities presented by virtual currencies and emerging technologies.1

Citations

- See, e.g., David Lehr & Paul Lamb, Digital Currencies and Blockchain in the Social Sector, Stanford Social Innovation Review (Jan. 18, 2018), source ; Stanford Graduate School of Business Center for Social Innovation and Rippleworks et al., Blockchain For Social Impact: Moving Beyond The Hype, source

Blockchain and Digital Currency

Digital assets and digital currency are based on blockchain technology. Blockchain is a record-keeping system with two important attributes: First, information stored via blockchain is distributed, with copies spread across multiple computers. This redundancy helps safeguard the accuracy and authenticity of the record and makes it extremely difficult to manipulate information stored in the system. Second, blockchain-based records are designed to be permanent. They are easy to update, but exceptionally hard to erase. Beginning with the advent of Bitcoin in 2008, technologists have been using blockchain to create highly secure digital ledgers as a mechanism for tracking and verifying ownership of digital assets such as virtual currency.

Blockchain and digital assets remain frontier technologies, but they provide the foundation for a rapidly growing number of applications related to philanthropy and social impact. Readers looking for additional background on the use of blockchain in public interest applications may want to consult the Blueprint for Blockchain and Social Innovation and the Blockchain Impact Ledger. These resources address a broad range of questions surrounding the technology and its current use in the social and public sectors.

Use Cases

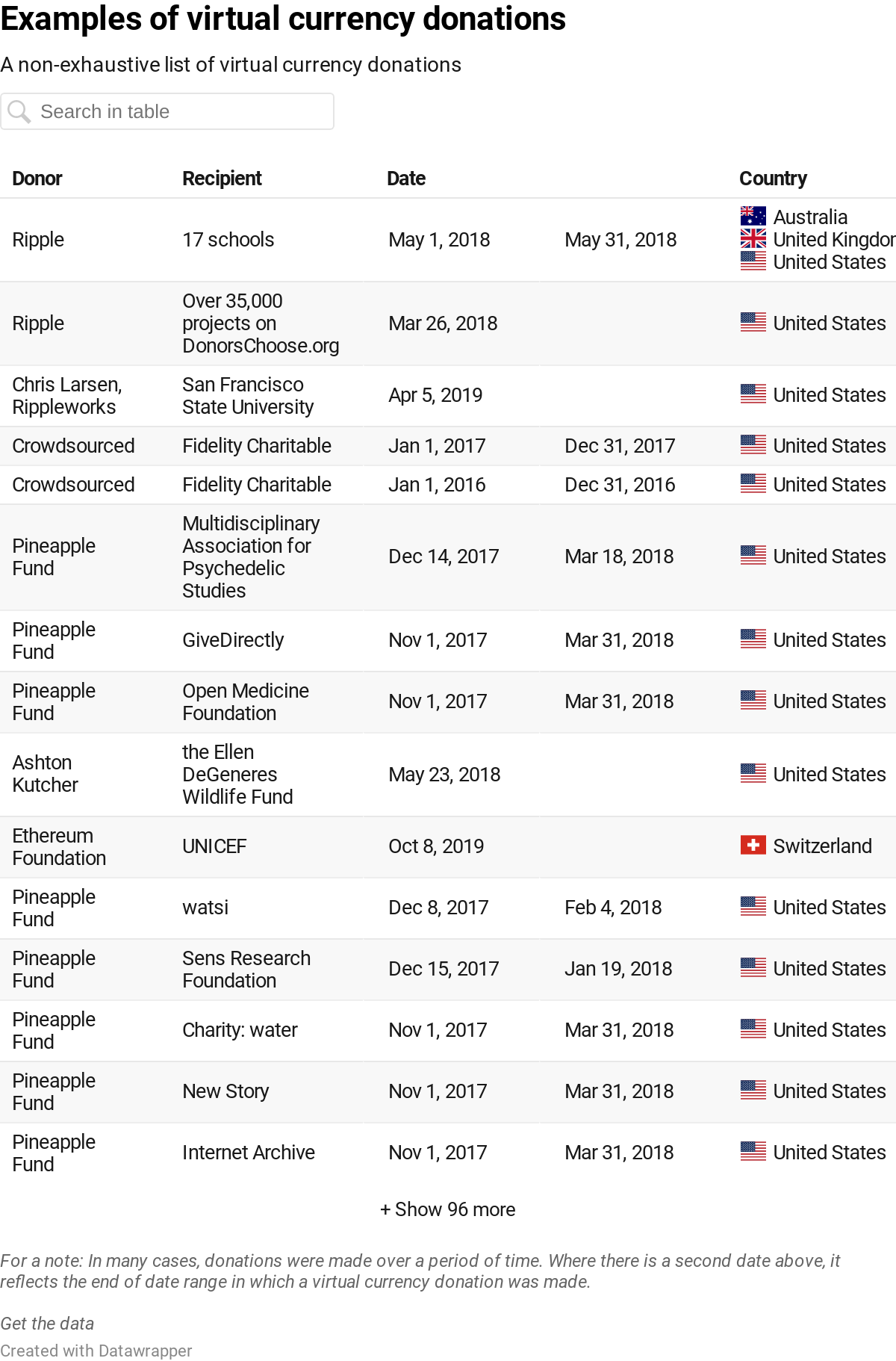

Individuals and companies that have profited from new asset classes can often make donations of these assets to CSOs. In the case of virtual currency, donors are occasionally embracing novel approaches in their gifts. In addition to the previously mentioned gifts to 60 charities from Pine, whose “Pineapple Fund” donated over $50 million worth of bitcoins,1 a virtual currency company donated the equivalent of $29 million to fund classroom projects listed on the education crowdfunding platform, DonorsChoose.2 These strategies are both intriguing and unconventional.

Smaller virtual currency donations from either individuals or organizations to their charities of choice are more common. For example, Fidelity Charitable reported $106 million in virtual currency donations since it started accepting these donations in 2015, including $30 million in 2018.3 All told, Fidelity Charitable estimates that in 2018 the United States saw over $1.3 billion in charitable donations of non-publicly traded assets, including virtual currencies, nearly three times more value than similar donations in 2014.4 Overall, however, virtual currency donations remain quite low relative to other forms of donation. One report estimates that only 2 percent of U.S. and Canadian charities accept Bitcoin.5 And the $30 million in virtual currency donations to Fidelity Charitable accounted for less than 1 percent of the over $9 billion donated to Fidelity Charitable in 2017.6

All told, Fidelity Charitable estimates that in 2018 the United States saw over $1.3 billion in charitable donations of non-publicly traded assets, including virtual currencies, nearly three times more value than similar donations in 2014

More broadly, while there has not been a concerted effort to catalog those donations—in part because they are frequently pseudonymous and challenging to track—our research has found over $200 million in publicly-recorded donations of virtual currency to charities across the world. This $200 million is both a significant figure on its own and yet still a relatively small figure compared to total annual charitable donations, which are estimated to reach over $400 billion in the United States alone.7

Virtual currency donations to charities could be transacted in a number of ways. But the most common mode we observe at the moment is a simple donation to an existing nonprofit through a website where the method of payment is from and to a virtual currency wallet—as opposed to a credit card or wire transfer.

For instance, during the recent wave of fires in Australia, the Australian Rural Fire Service raised over USD $1,500 in Bitcoin donations.8 In addition, we found a wide variety of organizations that have received donations made in virtual currencies: online knowledge communities such as the Wikimedia Foundation,9 journalistic organizations like the Freedom of the Press Foundation,10 houses of worship like a mosque in the United Kingdom11 and several churches in the United States,12 the Seattle Children’s Hospital,13 and the United Nations Children’s Fund (UNICEF).14

New America created and maintains the Blockchain Impact Ledger, a database of projects that harness virtual currencies and blockchains for social impact, and which demonstrate ways in which these technologies are being used around the world to address the United Nations Sustainable Development Goals.15 While virtual currencies currently play a small role in the overall work of civil society, the extant use cases and growth of virtual currencies in both civil society and other sectors suggests that increased future activity is likely.

The trajectory of virtual currency donations will be affected by the evolution of laws and regulations—including potential tax benefits—applied to those donations. Emerging laws or regulations that restrict movements of virtual currency, donations, or treat virtual currencies differently from fiat for donation purposes could have a chilling effect on donations.

Citations

- Helen Partz, Pineapple Fund Writes Farewell Post, Reports That All Funds Have Been Donated, Cointelegraph (May 11, 2018) (source

- Niraj Chokshi, How to Get $29 Million for Classroom Projects? Just Ask, The New York Times (Mar. 30, 2018), source

- Fidelity Charitable, 2019 Giving Report, source at 15.

- Id.

- The Giving Block, Cryptocurrency Fundraising: Key Findings from the Global NGO Technology Report 2019 (Oct. 14, 2019), source ; see also, Nonprofit Tech for Good, Global NGO Technology Report 2019 source

- Michael Theis, 10 Largest Donor-Advised Funds Grew Sharply in 2018, The Chronicle of Philanthropy (Dec. 10, 2019), source

- National Philanthropic Trust, Charitable Giving Statistics (accessed Feb. 14, 2020), source

- Christine Vasileva, Bitcoin for Charity: BTC Donations are on for Australian Bush Fires, Bitcoinist (Jan. 4, 2020), source

- Lisa Gruell, Wikimedia Foundation Now Accepts Bitcoin, Wikimedia Blog (July 30, 2014), source ; see also Sydney Ember, Wikipedia Begins Taking Donations in Bitcoin, The New York Times (July 30, 2014), source

- Freedom of the Press Foundation, You can now support Freedom of the Press Foundation Using Cryptocurrency (June 18, 2018), source

- Reuters, Looking for new way to Donate During Ramadan? London mosque now Accepts Bitcoin (May 28, 2018), source

- See, e.g., Daniel Cawrey, St. John’s is ‘world’s first Catholic church to accept bitcoin’, CoinDesk (Apr. 15, 2014), source ; Fern Creek United Methodist Church, Bitcoin Donations (last accessed Apr. 8, 2020), source

- Nikhilesh De, CryptoKitties Charity Auction Raises $15K for Children’s Hospital, CoinDesk (May 25, 2018), source

- United Nations Children’s Fund, UNICEF launches Cryptocurrency Fund (Oct. 8, 2019), source

- New America, Blockchain Impact Ledger, source (last accessed Jan. 22, 2020).

Key Findings

In approaching this topic, we sought to answer a fundamental question: Can a civil society organization accept donations in virtual currency—and, if so, how?

Overall, we found that the regulatory frameworks within the scope of our study were generally amenable toward virtual currency donations. In every country surveyed, the answer to whether charities could receive tax-benefited contributions of virtual currencies is at least a qualified “yes.” As we explain in further detail, CSOs interested in collecting virtual currency donations are usually advised to adhere to existing guidelines for the acceptance of other non-cash donations: when in doubt, document the value and means of donation; disclose to tax authorities and regulators in compliance with appropriate laws, erring on the side of more disclosure, rather than less; or decline the contribution if there are serious concerns about conflicts of interest, regulatory considerations, asset management expertise, donation valuation, or any other reason a charity might typically decline a donation.

In every country surveyed, the answer to whether charities could receive tax-benefited contributions of virtual currencies is at least a qualified “yes.”

The policy landscape is still unfolding, and details, including regulatory development and risk management, are uncertain. For example, in the United States, the Internal Revenue Service (IRS) added a new clarification in December 2019 to its informal guidance on virtual currency, requiring virtual currency donors to receive appraisal for donations worth $5,000 or more—presumably after a majority of 2019 virtual currency donations were already made and accepted.1 Just a few weeks later, without public notice or explanation, the IRS deleted significant examples from that informal guidance.2

We also find that frameworks to regulate virtual currency donations can be guided by previous efforts to regulate other forms of in-kind donations. Sometimes virtual currency donations are seen as a novel undertaking due to unique technical features (such as wallets, digital custody, encryption, and key management), forms of traceability (via public blockchains or other shared database designs), and methods of valuation (i.e. assessing the worth of virtual currencies traded on just a few, highly volatile, markets). But in reality, this phenomenon may not be unique: Charities have long been able to accept donations in the form of cash, securities/commodities, real property, and art. The various rules that govern those scenarios apply with equal measure here. Though art and diamonds can be hard to value or are sometimes subject to theft or money laundering concerns, countries have not banned charities from accepting them.

Moreover, many of the policy values underlying virtual currency donations are timeless: balancing recordkeeping requirements with donor privacy, fostering technological innovation while still ensuring consumer protection, allowing for efficient and quick donations while also guarding against money laundering, and protecting the public interest in promoting CSOs. Officials in different countries may have found different ways to balance these numerous values, but they have each struck a balance nonetheless.

Regulatory Trends

In many countries surveyed, there were few or no regulations that apply specifically or in much detail to charitable organizations with regards to virtual currencies. Nations we examined tended to take a hesitant approach to regulatory action in the space, typically extending and applying existing charity and tax laws to the donation and receipt of virtual currency donations. Six other trends are worth highlighting up front:

- We did not observe regulatory momentum towards banning virtual currency donations or treating them as categorically exceptional. The nations that have expressly or implicitly banned virtual currencies (pictured below, as of June 2018) are outside of the set of countries examined for this report.3 In fact, some large countries that banned virtual currency trading, such as India, have recently overturned those prohibitions.4 Worldwide, however, there is little public data to illuminate whether or how often individuals or entities are actually reporting virtual currency donations to local tax authorities. Nor is there comprehensive and publicly-available information about the incidence of tax authorities or other regulators using other enforcement mechanisms, such as investigations, audits, fines, warning letters, or rejected tax applications in response to virtual currency donations. While Denmark does not ban virtual currencies, their practical use is somewhat limited by law: In 2014 the Danish Tax Authority issued a binding opinion stating that invoices cannot be denominated in virtual currency but must instead be issued in the official Danish currency (Kroner) or another recognized currency.5

2. We found overlapping and sometimes conflicting bodies of regulation or guidance regarding virtual currencies, which complicates matters for charities and donors alike. Such examples speak to the need, both within and across governments, to engage in greater inter-agency coordination and public-facing clarification.6 Despite some proposals that certain countries form a new agency to coordinate virtual currency regulation within each jurisdiction,7 countries have not yet created these bodies and we expect that a number of existing agencies will continue to concurrently engage in regulation and oversight absent clearer guidance. Moreover, international harmonization of virtual currency regulations at this early stage could carry both benefits and costs, and there may be advantages from a comparative policy perspective to, at this stage, letting different international regulatory approaches continue to evolve.8

3. The bulk of regulators’ attention in the virtual currency space has been focused on protecting consumers and investigating the issuance, sale, and promotion of digital tokens, sometimes referred to as initial coin offerings (ICOs), and prosecuting virtual-currency-related scams.9 For example, we found ICO-specific statements and guidance across nearly all countries surveyed, including Australia, Bermuda, Denmark, Malta, Singapore, Switzerland, and the United States. The overarching concern here is the use of misleading or downright fraudulent ICOs to entice retail investors, skirt securities law, and engage in capital formation by another name.10 Regulators’ focus on ICOs suggests comparatively less attention and, at this point, scrutiny, have been focused on donations of virtual currency.

4. Some jurisdictions, such as Malta and Singapore, have attempted to position themselves as especially friendly to virtual currency activities and innovation as a means of attracting investment and commerce. Malta uses a hybrid regulatory regime, the Virtual Financial Assets Framework, that is still technically operating under the European Union (EU) umbrella.11 Singapore has created a regulatory sandbox (and a “sandbox express”), that invites firms to apply to experiment with innovative financial services under a relaxed legal and regulatory regime.12 Singapore’s aim is to encourage financial technology experimentation, innovation, market testing, and wide adoption.13 The Monetary Authority of Singapore also announced in January 2020 that it had received 21 applications for new digital bank licenses.14 By contrast, the EU’s recent passage of the Fifth Anti-Money Laundering Directive (AMLD5) created stringent new requirements for providers of virtual currency transfers.15 It also led several companies, including one that had recently received a multimillion-dollar round of venture capital funding, to shut down entirely, while others announced plans to relocate out of the EU in favor of more virtual-currency-friendly jurisdictions.16 We did not observe similar relocation efforts by international charities to avoid or avail themselves of such regulations.

5. We did not observe additional requirements for civil society organizations receiving donations of virtual currencies beyond existing best practices regarding anti-money laundering (AML) and countering the financing of terrorism (CFT) guidelines. To the extent charitable organizations accept anonymous donations and follow existing AML/CFT guidelines, they should continue to do so with regard to virtual currencies.17 In some countries, such as South Africa, is it not clear that AML/CFT rules apply to virtual currencies at all.18

6. A number of countries are exploring the issuance of their own sovereign virtual currency, often known as a Central Bank Digital Currency (CBDC). This fast-moving space has recently garnered serious attention from a wide range of monetary policymakers. In January 2020, several major central banks—the Bank of Canada, the Bank of England, the Bank of Japan, Sveriges Riksbank (in Sweden), and the Swiss National Bank, along with the Bank for International Settlements—announced they had formed a group to assess potential use cases for CBDCs.19 While the legal status of CBDCs is beyond the scope of this report, it is reasonable to assume that they would be treated as legal tender in a given country, could be given to a charity, much like cash or a check today, and may become just as attractive a medium of donation as alternative virtual currencies.

Best Practices

For Civil Society

CSOs interested in collecting virtual currency donations should generally adhere to guidelines for the acceptance of other non-cash donations: When in doubt, document (the value and means of donation), disclose (to tax authorities and regulators in compliance with appropriate laws, erring on the side of more disclosure, rather than less), or decline the contribution (if there are serious concerns about a conflict of interest or donor motives). Charities just beginning to accept virtual currencies may also consider partnering with domestic, regulated virtual currency exchanges and/or custodians, in order to streamline processes around asset acceptance, custody, and liquidation.

For Donors

For donors of virtual currency, best practices are similar to those applicable to donations of equity or property. If donors wish their donations to be tax-benefited, that usually requires giving to a tax-exempt domestic CSO (located in the same country as the donor) and documenting the donation with a receipt from the charity. As a rule of thumb, donors of higher amounts of virtual currencies hoping to receive tax benefits should obtain at least one independent, written appraisal of the value of their virtual currency donations and retain receipts of the donations.

For donors of virtual currency, best practices are similar to those applicable to donations of equity or property.

For Charities

Virtual currency donations also raise considerations for charities receiving them. Like a receipt of equity, a crucial initial question for the CSO will be determining what portion, if any, to immediately liquidate, and what portion to hold on for short-, medium-, or long-term appreciation. Moreover, like a receipt of equity, CSOs should take care to avoid the appearance of conflicts of interest—e.g., where a board member has substantial existing interest in a virtual currency or affiliated entity. Regulatory risk is greater in cases where the classification of the virtual currency donated is unclear (we found this to be the case for many virtual currencies, with the exception of Bitcoin and in some cases Ether), and CSOs should take care to establish with a reasonable basis that the virtual currencies are legal to possess and sell within their jurisdiction. CSOs that may not feel technologically savvy enough to self-custody (see Appendix 1: Virtual Currency Terminology) may also consider accepting virtual currency donations through a third-party custodian with expertise in securing and handling these assets. As a matter of board governance, it may also be prudent to adopt policies or pass resolutions documenting why and how the board is accepting virtual currency donations and how its investment strategy would apply to them.20

For Policymakers

For policymakers and regulators, putting forth consistent virtual-currency-specific tax and donation-compliance guidance, such as FAQs and other communications from the IRS in the United States,21 could ease uncertainty and encourage more virtual currency donations. Direct engagement among regulators, industry, and consumers, whether in public hearings or private consultations, is often fruitful. In addition to less formal regulatory tools—like issuing non-binding guidance, conferring with virtual currency businesses and consumers, and improving policy coordination—policymakers should continue to advance black letter law, like regulations, statutes, and case law, that would help both donors and recipient organizations alike in facilitating charitable contributions that are fully compliant with existing law and appropriately tax-benefited.

Open Questions

In light of the widespread lack of virtual-currency-specific charity guidance, it may be necessary in some cases for CSOs and donors to engage the democratic process, asking regulators to provide a no-action letter or encouraging lawmakers to draft new legislation that clearly establishes these rules and ameliorates these inter-agency disagreements. Despite the rise in virtual currency value and interest, most countries have passed little new virtual-currency-specific black letter law. The U.S. Congress’s quiescence on new virtual-currency-specific legislation, in particular, may contribute to the consistent reluctance of other countries to take first steps.

Achieving greater regulatory clarity may be especially important for CSOs interested in holding onto virtual currency donations rather than converting the donations immediately to a fiat currency. This may occur in cases where the CSO believes the donations might appreciate in value. For example, CSOs that several years ago received numerous donations in Bitcoin and immediately converted them into fiat currency likely lost out on millions of dollars in potential gains due to Bitcoin’s subsequent appreciation. Although immediate liquidation is simpler from a tax, technology, and investment standpoint, we should expect interest in saving particular virtual currencies to persist so long as these virtual currencies continue to hold and/or appreciate in value. In these and similar cases of saving virtual currency donations, regulatory considerations tend to follow similar considerations as charities accepting and saving donations of securities, including guarding against possible conflicts of interest with regard to the board of directors and ensuring the equities are properly registered with authorities.

For regulators and policymakers, tools like questionnaires and account auditing may be more effective than outright bans or hard to meet licensure requirements that could curb the total number of donations or move more donation transactions off the books. In some contexts, the public and private sectors could benefit from the creation of regulatory sandboxes that facilitate transparent experimentation at relatively modest scale. The insights derived from these efforts can help shape adaptation of future regulatory regimes as the space continues to evolve.

…the public and private sectors could benefit from the creation of regulatory sandboxes that facilitate transparent experimentation at relatively modest scale.

Tax evasion, money laundering, and terrorist financing are all legitimate areas of government concern regarding for-profit and tax-exempt organizations alike. For example, the recent growth in tax-exempt donor advised funds (DAFs) in the United States may create both useful new tax savings for individual donors and also, in some circumstances, the potential for misuse.22 Concerns about DAFs may also extend to donations of virtual currencies, insofar as they could conceivably allow a donor to receive a multi-year tax deduction for an illiquid virtual currency donation at a high valuation (even momentarily), without requiring or ensuring those funds are ultimately distributed or put towards charitable causes.23 Other potential public interest concerns may arise in evaluating tax-exempt status for virtual-currency-specific foundations—philanthropic organizations directly affiliated with the companies or organizations that created or manage a given virtual currency—both in the United States and abroad, including monitoring for conflicts of interest, for-profit motives, and distributions to affiliated entities. There are a number of virtual currency entities abroad, often styled as scientific foundations, that contribute to the development, distribution, and/or marketing of a given virtual currency, and hold large sums of it. Separately, there have also been several high-profile instances of individuals pledging sizable virtual currency donations—garnering significant attention (to their companies and currencies) in so doing—but never following through with a donation. While the problem of unfulfilled pledges may or may not be a legal problem, per se, it dovetails with concerns about potential profit-oriented motives, ICO issuances, and evaluating how much CSOs are benefiting from certain virtual currencies.24

Technical familiarity is another key question for charities considering accepting and custodying virtual currencies. How equipped are charities to securely custody these assets, manage their price volatility and regulatory risk, and properly account for them on all tax documents? Charities and regulators alike may benefit from more hands-on training and question and answer opportunities with industry professionals. Lawmakers may consider taking Canada’s lead and require asset managers and virtual currency custodians to meet particular expertise or certification requirements before allowing them to custody virtual currencies on behalf of charity clients.25

Charities and regulators alike may benefit from more hands-on training and question and answer opportunities with industry professionals.

Citations

- Internal Revenue Service, Frequently Asked Questions on Virtual Currency Transactions (Dec. 2019), source ; see also United States Government Accountability Office, Virtual Currencies: Additional Information Reporting and Clarified Guidance Could Improve Tax Compliance (Feb. 2020), source at 2 (“However, part of the 2019 guidance is not authoritative because it was not published in the Internal Revenue Bulletin (IRB). IRS has stated that only guidance published in the IRB is IRS’s authoritative interpretation of the law. IRS did not make clear to taxpayers that this part of the guidance is not authoritative and is subject to change. Information reporting by third parties, such as financial institutions, on virtual currency is limited, making it difficult for taxpayers to comply and for IRS to address tax compliance risks. Many virtual currency transactions likely go unreported to IRS on information returns, due in part to unclear requirements and reporting thresholds that limit the number of virtual currency users subject to third-party reporting. Taking steps to increase reporting could help IRS provide taxpayers useful information for completing tax returns and give IRS an additional tool to address noncompliance.”).

- The IRS scrubbed its website of a reference to “Fortnite V-Bucks” as an example of a virtual currency. See, e.g., BrianFung, IRS quietly deletes guideline that Fortnite virtual currency must be reported on tax returns, CNN Business (Feb. 13, 2020), source

- See, e.g., Selva Ozelli, Qatar bans cryptocurrencies after updating its AML Laws, The FCPA Blog (Feb. 12, 2020), source

- Campbell Kwan, India’s highest court overturns cryptocurrency trading ban, ZDNet (March 5, 2020), source

- The Law Library of Congress, Regulatory Approaches to Cryptoassets in Selected Jurisdictions: Denmark (Apr. 2019), source at 74 (referring to Bitcoins, ikke erhvervsmæssig begrundet, anset for særkilt virksomhed [Bitcoins, Not CommerciallyJustified, Considered Special Activity], SKAT (Apr. 1, 2014), source at source).

- We discuss further some examples of overlapping and sometimes conflicting virtual currency regulations, infra at § “Asset Class, Valuation, and Tax Issues.”

- See, e.g., Peter J. Henning, Should Congress Create a Crypto-Cop?, The New York Times (Feb. 14, 2018), source

- See, e.g. Statement of Rebecca M. Nelson (Specialist in International Trade and Finance) before the U.S. Senate Committee on Banking, Housing, and Urban Affairs, Examining Regulatory Frameworks for Digital Currencies and Blockchain (July 30, 2019) at 9 source (“The Need for International Regulatory Harmonization? . . . Then-Managing Director of the International Monetary Fund (IMF) Christine Lagarde argued that international regulation and supervision of cryptocurrencies is “inevitable.” Additionally, the editorial board of the Financial Times argues that a coordinated international regulatory framework for the “wild west” of cryptocurrencies is long overdue. Some initial international efforts at harmonization of cryptocurrency regulations are proceeding [], although more systematic coordination remains elusive. A more aggressive adoption of a one-size-fits all international regulatory structure for cryptocurrencies could have costs, however. It could create distortions, have unintended consequences, and impede innovation, a particular concern in the fast-changing cryptocurrency market.”).

- Initial Coin Offering (ICO): A process by which a portion of a particular protocol’s cryptocurrency or tokens are sold publicly (in many cases following earlier distribution or reservation to venture capitalists, founders or other supporters) in exchange for either fiat currency or other virtual currencies. These funds can be used for a variety of purposes. ICOs have come under heavy regulatory scrutiny, especially where they can be said to resemble unregistered IPOs that fail to deliver buyers equity or other shareholder rights typical of registered securities. Some regulators view ICOs as rough equivalents of Initial Public Offerings (IPOs), and tokens issued in conjunction with an ICO may be governed under securities law.

- See, e.g., SEC Chairman Jay Clayton, Statement on Cryptocurrencies and Initial Coin Offerings (Dec. 11, 2017) source (“By and large, the structures of initial coin offerings that I have seen promoted involve the offer and sale of securities and directly implicate the securities registration requirements and other investor protection provisions of our federal securities laws.”).

- See, e.g., Malta Financial Services Authority, Virtual Financial Assets Framework Frequently Asked Questions (Jan 25, 2019), source

- See Monetary Authority of Singapore, Fintech Regulatory Sandbox Guidelines (Nov. 16, 2016), source at 2.4 (“[Applicants] can apply to enter a regulatory sandbox (the ‘sandbox’) to experiment with innovative financial services in the production environment but within a well-defined space and duration. The sandbox shall include[] appropriate safeguards to contain the consequences of failure and maintain the overall safety and soundness of the financial system. . . . Upon approval, the applicant becomes the entity responsible for deploying and operating the sandbox (the ‘sandbox entity’), with MAS providing the appropriate regulatory support by relaxing specific legal and regulatory requirements prescribed by MAS, which the sandbox entity will otherwise be subject to, for the duration of the sandbox.”).

- Monetary Authority of Singapore, Sandbox Express, Consultation Paper P015-2018 (Nov. 14, 2018), source

- Monetary Authority of Singapore, MAS Receives 21 Applications for Digital Bank Licences (Jan. 7, 2020), source

- See, e.g., Jenny Gesley, European Union: 5th Anti-Money Laundering Directive Enters into Force, The Law Library of Congress (July 16, 2018), source

- See, e.g., Yogita Khatri, Two more crypto firms shutting down over impending EU money-laundering rules, The Block (Dec. 16, 2019), source ; Deribit, Deribit Moving to Panama + KYC Feb. 2020 (Jan. 9, 2020), source (“Currently, Deribit is operating in the Netherlands. However, the Netherlands will most likely adopt a very strict implementation of new EU regulations that also apply to crypto companies (5AMLD). . . . Therefore, we have decided to operate the Platform from Panama.”).

- We reiterate that this report is conveyed as an analysis of public policy and international trends and does not offer or constitute legal advice. Do not rely upon this report for making or receiving donations or for any other purpose. Please confer with a local attorney, tax specialist, financial advisor, and/or other licensed professionals before making an individualized decision about virtual currencies, donations, or other matters. See supra, n1.

- The Law Library of Congress, Regulatory Approaches to Cryptoassets in Selected Jurisdictions: South Africa (April 2019), source at 221 (“It does not appear that South Africa’s anti-money laundering laws are currently applicable to cryptoassets.”); South Africa Intergovernmental FinTech Working Group (Crypto Assets Regulatory Working Group), Consultation Paper on Policy Proposals for Crypto Assets (Jan. 2019) at 22.

- Bank of England, Central Bank group to assess potential cases for central bank digital currencies (Jan. 21, 2020), source?

- See, e.g., Lawrence J. Trautman & Janet Ford, Nonprofit Governance: The Basics, 52 Akron L. Rev. 971, 1035–36 (2018), available at source (“Serving competently on a board requires understanding of a considerable body of enterprise (corporate) governance knowledge. Novel and disruptive technological innovations create a constant challenge to those seeking to govern any enterprise.”); id. at n.164 (referencing bitcoin and virtual currency).

- Internal Revenue Service, Frequently Asked Questions on Virtual Currency Transactions (Dec. 2019), source

- See, e.g., David Gelles, How Tech Billionaires Hack Their Taxes With a Philanthropic Loophole, The New York Times (Aug. 3, 2018), source (“D.A.F.s have become one of the most controversial issues in the charitable world. . . . Unlike family foundations, which are required to distribute 5 percent of their assets each year and have historically been the way wealthy donors disbursed their philanthropic firepower, D.A.F.s have no distribution requirements, meaning that billions of dollars earmarked for charity can sit idle for decades. And because organizations that manage D.A.F.s are not required to report which funds give money to which causes, it is impossible to know how much money individual donors are giving away to nonprofit organizations.”); Theodore Schleifer, How a lawsuit could reveal secrets about Silicon Valley’s favorite philanthropic loophole, Vox Recode (July 2, 2019), source

- See, e.g., Laura Mahoney, California Looks Into Billions Held in Funds Intended for Charities, Bloomberg Tax (Jan. 14, 2020), source ; See also, Theodore Schleifer, Why Jack Dorsey (and you) should pay attention to this proposed charity law in California, Vox (Jan. 14, 2020), source (noting that “[t]he amount of money stored in DAFs has tripled over the last decade.”). In some cases, particularly with regard to highly illiquid virtual currencies where donation valuation would be difficult to ascertain, regulators and charities may consider asking donors to first liquidate the assets to conventional currencies.

- Compare Laura Shin, Former Child Actor Brock Pierce Vows To Give Away $1B From His Crypto Fortune, Forbes (Feb. 28, 2018), source , with Neil Strauss, Brock Pierce: The Hippie King of Cryptocurrency, Rolling Stone (July 26, 2018), source (“As of this writing, it has been nine months since Pierce first mentioned giving away $1 billion, and there still hasn’t been a white paper released or a penny given.”).

- Canada Securities Administrators, CSA Staff Notice 46-307 (Aug. 24, 2017), source (“Custody: Securities legislation of the jurisdictions of Canada generally require that all portfolio assets of an investment fund be held by one custodian that meets certain prescribed requirements. We expect a custodian to have expertise that is relevant to holding cryptocurrencies. For example, it should have experience with hot and cold storage, security measures to keep cryptocurrencies protected from theft and the ability to segregate the cryptocurrencies from other holdings as needed.”).

Other Findings

Acceptance of Donations of Virtual Currency

Given the technical complexities that can be involved in accepting virtual currency donations—including setting up a wallet, self-custodying the funds with proper distribution of “private keys,” transferring and converting donations into fiat currencies, and so on—charities accepting virtual currencies have typically opted to partner with exchanges or payment processors in their local jurisdictions to manage many of these issues on their behalf. For example, when the Wikimedia Foundation, which curates Wikipedia, started accepting Bitcoin donations in 2014, the organization partnered with a U.S.-based Bitcoin exchange that accepted donations on Wikimedia’s behalf and immediately converted them into U.S. dollars.1 The Tor Project, which started accepting Bitcoin donations in 2013, partnered with a U.S.-based payment processor that similarly converted all donations into dollars.2 Nonetheless, charities are not required to utilize a third-party virtual currency processor, and when the Tor Project hosted a Bitcoin fundraiser again in 2019, they directly accepted payments via BTCPayServer—a self-hosted payment technology.3

As charities consider accepting virtual currency donations, it is reasonable for regulators to expect that charities’ chosen means of acceptance will mirror their own familiarity with the underlying assets. Those charities for whom virtual currencies are new and unfamiliar will likely lean heavily on third-party solutions. As they grow in familiarity, the charities may choose to self-host and self-custody donations instead (in some cases, saving money on processing fees or improving donor privacy as a result). Perhaps in recognition of the emerging innovation in this area, and perhaps also because so little virtual-currency-specific legislation has been enacted, no jurisdictions surveyed required charities to use a particular technology for accepting virtual currency donations, though Canada did require virtual currency custodians to meet certain expertise requirements.4

As over one thousand virtual currencies have been issued, the laws governing charitable donations have tended to treat them in broad strokes and do not facially distinguish between specific currencies. But beyond the milieu of CSOs, there are some de facto differences in how virtual currencies are treated. In general, virtual currencies with larger market capitalization and daily circulation, like Bitcoin and Ether, tend to have somewhat clearer regulatory treatment than alternative tokens or newer currencies. For example, in the United States, the Securities and Exchange Commission (SEC) and Commodities and Futures Trading Commission (CFTC) have essentially signalled through public speeches and media interviews that Bitcoin and Ether will not be treated as securities—notwithstanding unresolved questions about Ether’s original issuance and the lack of formal enforcement orders or case law—while leaving open the regulatory classification of other virtual currencies, such as XRP.5 Likewise, larger jurisdictions such as the United States and the EU can serve as bellwethers for how smaller countries are likely to regulate a given virtual currency.6 In a number of countries, there are ongoing debates about when a virtual currency should be classified as a security and whether it is prudent to essentially assume any given tokens are securities, given their common issuance as capital formation devices and often low utility value other than as a means of investment. Even under the securities rubric, charities are generally able to accept donations of stock and other non-cash financial instruments, although in the United States, for example, there may be some residual risk associated with anyone, including a charity, reselling (liquidating) an instrument that may constitute an unregistered security.

In general, virtual currencies with larger market capitalization and daily circulation, like Bitcoin and Ether, tend to have somewhat clearer regulatory treatment than alternative tokens or newer currencies.

Anonymous virtual currency donations fall more squarely under the regulation of AML and CFT for charities generally. But many countries, such as Australia, the U.K., the United States, and Switzerland, to name a few, do have a history of allowing anonymous and pseudonymous cash donations and non-cash donations alike. For example, the Australian Charities and Not-for-profits Commission (ACNC) both acknowledges that anonymous donations may create potential vulnerabilities for charities, but also offer and recommend mitigation strategies (record keeping, reporting suspicious activity, independent audits, and so on) that can help charities protect themselves without sacrificing the ability to accept these donations.7 In annual tax filings, some U.S. entities must disclose contributions above a certain monetary threshold, although “[a] tax-exempt organization is generally not required to disclose publicly the names or addresses of its contributors,”8 and some organizations simply list anonymous donations as “anonymous.” As of 2019, proposed IRS and Treasury rules would change disclosure requirements for tax-exempt organizations (other than 501(c)(3) entities).9 Moreover, the question of donor anonymity is also the subject of active litigation in the United States, where appeals are pending about when a state can compel a nonprofit to disclose the names of its major donors in annual filings.10

When charities accept virtual currency, they are not normally required to undertake a virtual-currency-specific registration for that particular donation. However, charities broadly do have to submit a variety of information upon their creation and for annual taxes, and the acceptance of virtual currencies in some countries surveyed creates additional reporting obligations for the receiving charities. For example, the IRS requires charities to file a Form 990-series annual return,11 but the acceptance of virtual currency (a “non-cash contribution”) may create additional reporting obligations in the form of Schedule M, which lists all non-cash contributions received during the year.12 Moreover, if a U.S.-based charity sells, exchanges, or otherwise disposes of non-cash charitable deduction property (including virtual currency) within three years after receiving the donation, IRS guidance also directs them to file Form 8282 and gives the original donor a copy of that form.13 These sorts of annual charity reporting of non-cash donations are typical across countries surveyed. For example, in Bermuda, charities are required to submit an annual financial and organizational report to the Registry General, and the “Know Your Donors” section contains questions that encompass reporting virtual currency donations received.14 In Canada, charities file Form T3010, which includes a schedule for documentation of all “non-cash gifts,” presumably including virtual currencies.15

Asset Class, Valuation, and Tax Issues

As a general rule of thumb, charitable contributions of virtual currency are classified as non-cash donations and valued for tax purposes like donations of property or equity. But, outside the tax context, exceptions and incongruity abound in the legal classification of digital assets.

Across a number of countries, we found overlapping and sometimes conflicting bodies of regulation or guidance regarding virtual currencies, which complicates matters for charities and donors alike. In the United States, a virtual currency can be many things at once: a security in the eyes of the SEC, a commodity for purposes of the CFTC, property as defined by the IRS, a transfer of value under the auspices of the U.S. Treasury’s Financial Crimes Enforcement Network (FinCEN), and money under state regulation of money services businesses (MSBs). By contrast, the U.K. identifies three different types of virtual currencies—exchange tokens, utility tokens, and security tokens—while clarifying that “the tax treatment of all types of tokens is dependent on the nature and use of the token and not the definition of the token,” which further complicates the provision of straightforward tax treatment guidance.16 Not to be outdone, Malta’s Virtual Financial Assets Act uses four possible categories for any given virtual currency (referred to in the bill as a “DLT asset”): a virtual token; a virtual financial asset; electronic money; or a financial instrument that is intrinsically dependent on, or utilizes, distributed ledger technology. Under the same Act, for a given asset to qualify as a “virtual financial asset,” it must not be electronic money, a financial instrument, or a virtual token, which complicates categorizations given the wide-ranging and overlapping uses of many virtual currencies.17

It is noteworthy that this considerable regulatory overlap—and associated inconsistencies—persists in the United States, a country with a comparatively well-developed regulatory regime. Such examples speak to the need, both within and across governments, to engage in greater inter-agency coordination and public messaging of regulatory intent. In many countries surveyed, including Bermuda, Singapore, South Africa, and the United States, regulatory guidance expressly states that virtual currencies are not equivalent to legal tender—but that, of course, does not affirmatively indicate their legal status.

Regarding appraisals, we identified few jurisdictions that promulgated binding rules specific to virtual currency donations. As of December 2019 in the United States, the IRS added a new clarification to its informal guidance on virtual currency that clarified that virtual currency donors, just as donors of most other types of property, are required to receive an appraisal for donations worth $5,000 or more. Under IRS guidance, this is already true for non-cash donations such as donations of art, property, land, or stocks.18 More broadly, countries such as Singapore and Canada normally require the donor to obtain a written, independent appraisal of significant non-cash donations like donations of art, land, and buildings.19 For donations of stock or other publicly-traded financial instruments, contemporaneous price quotes from relevant markets are usually sufficient in lieu of independent appraisal.20 In the case of virtual currencies that are regularly traded on public markets, it is unclear whether an appraisal is strictly required or whether a price quote will suffice for tax purposes. In most circumstances, appraisals are conducted by private parties, produced by the parties submitting tax forms, and subject to audit.

Once a virtual currency has been donated, donors can typically avail themselves of tax advantages. Namely, the amount donated can generate a tax benefit (usually in the form of a deduction or credit), although maximum allowable donation, applicable tax brackets, and the duration of the benefit vary considerably by country and individual circumstances.21 For recipient CSOs, the tax incentives are less pronounced, since many charitable organizations are already tax exempt. Fundamentally, the most basic requirement for receiving these tax incentives is that the donor (and donee) must submit appropriate annual tax paperwork. While documentation may sound obvious, under-reporting of virtual currency dispositions in tax filings is reportedly still common.22

Anti-Money Laundering and Measures to Combat the Financing of Terrorism

In many charitable donations, donors freely identify themselves to the charity as part of the giving process or paperwork. In some cases, however, donors may wish to give anonymously, without identifying themselves or to avoid publicizing their support to the general public. Both as a matter of practice and legally speaking, in our research we found that charities are able to accept such donations even where they do not know the identity of the donors—and we saw no indication that this principle would apply differently in cases where the anonymous donations are made in virtual currencies. As a general rule, charities should take care to follow the existing rules of their local jurisdictions regarding all AML/CFT compliance, including in donations of virtual currencies.

In the aftermath of the September 11, 2001 attacks, a number of governments worldwide expanded measures regarding AML and CFT, which generally increased surveillance over money flows and placed new KYC obligations on banks and other money-handling businesses.23 Additionally, in 2018, the U.S. Office of Foreign Asset Control (OFAC) designated specific virtual currency “addresses” as belonging to sanctioned individuals for the first time, prohibiting U.S. individuals and businesses from sending and receiving funds associated with these addresses.24 While recognizing the importance of combating money laundering and terrorist financing, organizations like ICNL have also pointed out these measures are sometimes enacted without proper consideration of their impact on human rights and civil society.25 For charities, these obligations raise important questions about preserving and protecting the privacy rights of donors who wish to remain anonymous, questions made even more pertinent amid the potential for accepting anonymous donations of virtual currencies.

Anonymous donations allow charities to facilitate donations from a wide swath of donors who might not otherwise wish to identify themselves or seek to support potentially controversial causes. For early adopters and generous donors of virtual currency like Pine, de-anonymizing themselves alongside their donations could put themselves at risk of harm, in terms of revealing the causes they support, the extent of their wealth, or other personal information.26 Virtual currencies generally better facilitate anonymous and pseudonymous donations than other forms of digital payment. As an example of distributed anonymous charitable giving in the virtual currency context, in July 2019, the Tor Project held a crowdfunding effort that raised nearly $20,000 worth in Bitcoin donations from over 500 donors.27 Because the donations were sent in Bitcoin and accepted directly by the Tor Foundation without going through a AML/CFT-compliant payment processor, the Tor Project did not have any means to certify the identity of their donors—and yet could still convert the funds to fiat currencies and use them to fund their efforts.

Virtual currencies generally better facilitate anonymous and pseudonymous donations than other forms of digital payment.