Table of Contents

- Executive Summary

- I. Introduction

- II. Major Recent Precedents for “Use-it-or-Share-it”

- III. Major Benefits of a Use-it-or-Share-it Policy

- IV. The First Amendment Imposes Limitations on the Government’s Power to Limit Non-Interfering Use of Spectrum

- V. Operationalizing Harmful Interference: The FCC’s Balancing Approach

- VI. Scarcity to Abundance: Opportunities to Expand Shared Access

- VII. Conclusion

III. Major Benefits of a Use-it-or-Share-it Policy

A default policy that seeks systematically to open fallow and underutilized frequency bands for opportunistic access on a non-interfering basis can yield many substantial benefits that advance the public interest goals of the FCC and other regulators. These include:

A. Expanding Spectrum Capacity and Efficiency to Meet Surging Demand

Like electricity, wireless connectivity has become central to personal communication and a critical input into the output of nearly every other industry.1 As the demand for both mobile and fixed wireless data continues to surge, there are few if any desirable spectrum bands not already in use for a wide variety of other private and public purposes. Industry studies have projected substantial deficits in the availability of both licensed and unlicensed spectrum. While recent FCC actions, such as the recent C-band auction of 280 megahertz and the authorization of unlicensed sharing across the 6 GHz band, have temporarily ameliorated the shortfall, additional bands will need to be identified for clearing or sharing. As the President’s Council of Advisors on Science and Technology (PCAST) report observed, it is increasingly difficult to relocate important services (whether government or commercial users) and, even when possible, in the United States clearing a band for reallocation has taken an average of over eight years (and 13 years for the reallocated spectrum to actually be deployed for mobile use).2

Opening more underutilized bands for at least opportunistic sharing is therefore critical to meeting both the growing and more diverse demand for spectrum as the nation’s 5G wireless ecosystem builds out. This demand will come not only from mobile carriers deploying both mobile and fixed 5G services, but from other high-capacity fixed wireless providers, and from a growing number of individual enterprises, venues, critical infrastructure providers, community institutions, and others seeking to deploy customized IoT networks to meet their needs.

Despite these trends, there continues to be many occupied but underutilized frequency bands—that is, the challenge is spectrum access and not spectrum capacity. Spectrum measurements studies have long documented that only a fraction of the overall data-carrying capacity of most bands are being used on a frequency, geographic, directional, or temporal basis.3 As a report by the Dynamic Spectrum Alliance observed, coordinated sharing and “leveraging AFC systems to unlock dormant capacity, while avoiding interference to incumbents, is the closest thing there is to a spectrum ‘free lunch’ for businesses and consumers seeking connectivity at low cost.”4 Freeing up additional bandwidth through spectrum sharing makes wireless connectivity more available and affordable, thereby increasing both consumer welfare directly and the productivity of businesses that rely on wireless data. An example is cloud-based services, “which for mobile applications require both near-ubiquitous connections and relatively inexpensive data allowances.”5

Freeing up these bands of spectrum for additional use also facilitates the broader access to broadband services that would assist communities stuck on the wrong side of the digital divide. Communities of color, rural and Tribal communities, and low-income Americans more generally are all disproportionately harmed by the digital divide and would benefit from a more diverse, competitive, and affordable wireless ecosystem that democratizes access to wireless services.

B. Diverse Spectrum Access Promotes Innovation, Competition, and Choice

The implementation of open access to more bandwidth in a growing number of underutilized bands benefits a very broad and diverse range of potential spectrum users, including small and rural ISPs, individual enterprises (e.g., for IoT), large venues, community networks, and individual consumers. Nearly all spectrum auctions to date have been structured to promote mobile carrier business models premised on very wide-area coverage and a quality of service that can be more readily guaranteed with exclusive control of a band. As a result, small wireless ISPs and other enterprises seeking to deploy a network on a more localized basis (such as covering a neighborhood, campus, factory, farm, or warehouse) have needed to either purchase a carrier-offered service or have opted to make do with unlicensed spectrum.

A shortage of direct access to spectrum is a roadblock to innovation and competition now more than ever as an increasingly large share of individual businesses, community anchor institutions, office complexes, and even residential centers can benefit from an IoT network customized to their needs. The ability to quickly and inexpensively access (and aggregate) wide channels of spectrum on a local basis will be increasingly important to productivity and competition “in a 5G/IoT economy where wireless data connectivity will be associated with virtually every system, venue and device – and where many thousands of firms and service providers will have needs and demands for customized local networks.”6

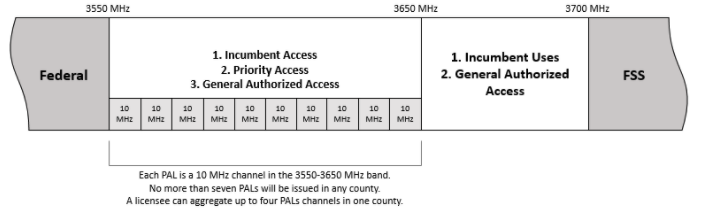

As the FCC stated in its 3.5 GHz Report & Order creating CBRS, “permitting opportunistic access to unused Priority Access channels would maximize the flexibility and utility of the 3.5 GHz Band for the widest range of potential users” and “ensure that the band will be in consistent and productive use.”7 The CBRS three-tier sharing framework makes both licensed and GAA spectrum available to smaller entities and enterprises that never or rarely bid in spectrum auctions. The combination of smaller-area licenses, dedicated GAA spectrum, and use-it-or-share-it access to unoccupied PAL spectrum provides direct spectrum access on a localized basis to a wide variety of rural WISPs, critical infrastructure, individual enterprises, and community anchors that cannot afford or justify buying exclusive licenses that cover large areas.

Providing more direct spectrum access with low coordination costs, which is what AFCs are designed to do, also lowers barriers to entry to new providers and types of services. Reducing barriers to entry thereby facilitates more competition, innovation, and consumer choice. Small and rural broadband providers, utilities, and other critical infrastructure, school districts, campuses, large venues, factories, and other individual enterprises are already taking advantage of GAA spectrum access, but will also require more capacity as use expands. More opportunistic access to spectrum (both GAA and unlicensed) would have the dual effect of encouraging these innovative local networks and increasing their benefits and chances of success.

C. Incumbent and Primary Services can be Fully Protected

The bedrock principle of spectrum sharing is that secondary users and the coordination process itself should have little, if any, impact on incumbent services. The focus of dynamic frequency coordination is the “prediction, and avoidance, of possible interference, rather than detecting and mitigating the condition.”8 When it unanimously authorized opportunistic GAA use of available PAL spectrum, both before and after its assignment by auction, the FCC recognized that licensees face no risk or loss of rights whatsoever from a use-it-or-share-it approach. This has been demonstrably true for geolocation database systems certified by the FCC. In the case of CBRS, the only burden on post-auction licensees is to use an online portal to notify the database (SAS) when the primary licensee is ready to commence service in a local area. The success of the 2020 CBRS auction for flexible-use PAL (raising $4.6 billion) demonstrates that licensees do not believe permitting opportunistic GAA access imposes significant burdens or in any way devalues their exclusive spectrum use rights.

As described in the previous section, a relatively static frequency coordination database can manage and automate the process. Examples include TVDBs (which have long been in operation); multiple SAS operators (which coordinate three tiers of sharing in the CBRS band); and the AFCs authorized to coordinate unlicensed sharing in 6 GHz, which are likely to be certified and operational later in 2021. Further, terminating the grant when the incumbent gives notice it will be commencing service in a specific area does not require anything as complex as the dynamic geolocation database (SAS) required to protect mobile U.S. Navy ships and other incumbents from interference.”9 Even a simple, static database can verify that a proposed deployment will not interfere with incumbent operations—as Comsearch has done for many years as the FCC-certified coordinator of the shared 70/80/90 GHz bands.10

D. Deters Warehousing and Promotes Secondary Market Transactions

Since the inception of spectrum auctions in 1994, with the partial exception of CBRS, the FCC’s policy to facilitate nationwide coverage has led to auctions for license areas that typically incorporate areas with disparate characteristics (urban, suburban, exurban, and rural) and span geographies far larger than are practical for small ISPs or for enterprise and institutional users (e.g., corporate and university campuses, ports, etc.). For example, the C-band auction that concluded in January 2021 offered only Partial Economic Areas (PEAs), which are so large that 416 cover the entire United States (the Los Angeles PEA extends to the Nevada border). The 10 largest PEAs are home to more than 100 million Americans.

A survey by the Wireless Internet Service Providers Association (WISPA) of its members found that 90 percent seeking to lease vacant spectrum from carriers were unable to do so. WISPs reported that carriers either were unwilling to negotiate or imposed unacceptable conditions on potential transactions. WISPA told the FCC that “historically, large carriers acquire licenses for large areas, build out in the urban core where the population is more dense, and warehouse spectrum in rural areas that could be used for broadband deployment.”11

A Mobile Future study found that over a 10-year period (2003-2013) only 8.6 percent of the MHz/POPs leased among carriers represented leases from nationwide to non-nationwide providers.12 The largest carriers have a history of warehousing spectrum and leaving it fallow rather than making it available for use to catalyze broadband deployment or other services.13 Relying solely on secondary markets to make unused spectrum available through leasing or the partitioning of license areas, particularly to smaller providers, is a demonstrated market failure.14

For licensees, particularly those with exclusive (flexible use) rights, there are no obvious incentives to lease or partition vacant spectrum. Transaction costs are high and prime spectrum has proven to have an option value that deters the sort of long-term commitments that another ISP typically wants. In contrast, authorizing opportunistic, shared access to the fallow spectrum creates a general incentive for licensees to build out services more quickly, or to engage in secondary market transactions such as leasing unused spectrum or partitioning a license. Opportunistic access to unused spectrum demonstrates that other (typically smaller) operators are finding value in the unused portions of their license area. This “demand discovery” puts market-based pressure on licensees to partition and/or lease.15 With use-it-or-share-it rules in place, licensees will more readily identify small carriers as prospects for longer-term and more secure partitioning or leasing arrangements.

On the buy side, opportunistic access creates a market for interference protection and serves as an intermediate step between non-use and paying the licensee for partitioning or leasing spectrum. Opportunistic access can also serve as a form of price discovery. A small operator can do initial and test deployments to see if paying for interference protection would actually be worth the cost. Some small ISPs will determine that opportunistic use—temporary and without protection from interference—is all they can afford or justify (especially if they are primarily augmenting capacity), while others will trade up to negotiate and purchase a partitioned license or leasehold as a means of ensuring continued and exclusive use for a set period of years.

These options will particularly benefit very small, rural, and other local operators that do not have the funds to pay for (or do not need) interference protection, or where the transaction costs are simply too high to make it worthwhile for a licensee. For example, a rural ISP, school, or enterprise may decide it could make opportunistic use of a band to enhance the capacity of its network without relying on it. As a value-added service, an AFC database could help ISPs find unused spectrum and facilitate (possibly even automate) leasing and other secondary market transactions. Blockchain functionality could be incorporated to coordinate these databases, as a report from the Dynamic Spectrum Alliance articulated: “Blockchain may have the potential to enhance frequency coordination and secondary market transactions, particularly in shared bands that will need (or benefit from) an AFC database.”16

A use-it-or-share-it licensing condition is also an affirmative addition or alternative to more draconian use-it-or-lose-it rules that require licensees to relinquish spectrum licenses in areas where they have failed to meet build-out requirements.17 As part of a use-it-or-share-it policy, licensees could receive credits toward meeting construction or performance requirements without actually transferring the spectrum. The FCC could decide to allow licensees to attribute all or a portion of the buildout and coverage by opportunistic users at the end of the licensing period to the licensee for purposes of renewal, a significant incentive if it helps a licensee satisfy interim or final performance requirements. In turn, another provider gains the opportunity to put that spectrum to use until the actual licensee is ready to deploy and commence service in that area.

While a “keep-what-you-use” condition has been suggested as an alternative, it is suboptimal compared to a use-it-or-share-it policy. The licensee’s incentive is limited to losing the least profitable holes in its license area and only after the spectrum lies fallow for 10 years (coupled with a lengthy process that the commission has been reluctant to enforce). Since performance requirements are met as a share of population, milestones are satisfied by serving mainly the cities, suburbs, and other high-traffic areas that generate a higher return on investment, while leaving a disproportionate amount of licensed spectrum fallow in small town or rural areas. And because there is no database of available spectrum by geographic area, the FCC itself has no ongoing visibility into what areas are actually built out and serving customers. A far better alternative would be to combine use-or-share and keep-what-you-use conditions, so that after a certain number of years, areas that are not built out are permanently available for shared use by any provider.

E. Promotes Service in Rural and Underserved Areas, Narrowing the Digital Divide

It is, of course, well established that rural, tribal, and small town America lacks access to high-speed broadband at much higher rates than their counterparts in urban and suburban areas. Even in rural areas where high-speed broadband has been deployed, consumers are less likely to have a choice among competing providers and more likely to pay higher prices for worse service. Efficient farming in the digital era also depends increasingly on fast, reliable broadband connectivity.

A major obstacle to better access and more competition in the high-speed broadband market in rural areas is the cost of deployment, as fiber and other wireline technologies can be five-to-seven times or more expensive and far slower to deploy in less densely-populated or topographically-challenging areas. Prohibitive costs are a major obstacle to high-speed broadband adoption in rural and less densely-populated communities, even when and where it is available.18 Fixed wireless providers (point-to-multipoint, or PtMP) offer a more cost-effective method of bringing high-speed broadband to targeted, hard-to-serve rural areas, which should in turn make the actual service more affordable. As one report noted, “Fixed wireless has a much lower upfront cost to build than fiber. This lower cost makes reaching certain locations more economically feasible.”19

The areas with more unused spectrum tend to be the same communities that are underserved because deployment costs are highest relative to revenues per user. However, small and rural ISPs cannot afford to buy exclusive, large-area licenses and rely on unlicensed or opportunistically-shared spectrum (CBRS) to provide service. As described in the previous section, in response to the pandemic-induced surge in home bandwidth consumption, the FCC was able to help WISPs quickly and affordably increase the capacity of their fixed wireless service in many underserved areas by granting STA to licensed but unused spectrum in the lower 5.9 GHz band. More generally, use-it-or-share-it rules, implemented in bands with equipment readily available, can empower aggregation with other bands to expand capacity and improve quality of service even if use is only temporary.

F. No Permanent Assignments, No Stranded Users

One objection to opportunistic use has been that the primary incumbent user (e.g., the military) or the FCC may want to repurpose the band at a later date. However, opening underutilized bands for opportunistic access need not be permanent, or even long-term, if users must periodically renew their grant to operate (as in TVWS and CBRS) and especially if devices are capable of switching to other frequencies. In the TVWS rules, the Commission reserved the option to license additional TV stations, to grant stations channel reassignments, or even to reallocate a portion of the TV band (as it did by auctioning the channels in 600 MHz). In all cases the TVBDs denied unlicensed users continued use of newly-occupied channels. With multiple AFCs now in operation, it should be relatively straightforward for channels or new shared bands to be added, withdrawn, or limited for opportunistic use to a particular geographic area or a particular time of day.

Further, opportunistic access presumes—and in some bands requires—that devices certified to operate on a shared, secondary basis are multi-band and capable of accessing alternative spectrum. CBRS is an example: Because roughly half the 3.5 GHz band is reserved for GAA use (see below), if all the PAL spectrum in a market is in use, the SAS can require GAA users to make due with available GAA channels. In the future, given AFC/SAS capabilities, bands can be opened or closed for sharing—nationally, regionally, or locally—and even on short notice, without stranding any users, legacy devices, or infrastructure. With a geo-location database in place, any fallow band could be listed for opportunistic access on a temporary basis—and then de-listed (or restricted in additional ways) if and when a new licensee is selected and built out.

G. Regulators Benefit from an Automated, Scalable, Transparent Enforcement Tool

By leveraging the capabilities of certified but privately-operated AFC systems, regulators have been able to greatly increase available spectrum capacity with little or no increase in agency resources. As the Dynamic Spectrum Alliance report on the evolution of AFCs noted:

Dynamic database management can give regulators more control over band sharing, better enforcement tools, a greater ability to monitor usage, and the option to outsource technical developments and operations to stakeholders—and all while retaining ultimate authority, regulatory flexibility and even the ability to collect fees.20

While frequency bands allocated for purely fixed services (such as point-to-point links and the FSS) have long been authorized for shared use based on manual coordination, the transaction costs are high, the coordination process slow, and the regulator typically has to devote personnel to reviewing and approving new entrants or changes in siting or power levels. AFCs scale and automate that process, allowing—for example—the millions of new unlicensed uses that will rapidly populate the 6 GHz band. Whereas manual or even database-assisted coordination is relatively expensive, slow, limited in granularity, and prone to inconsistent results, “AFCs can produce near-real-time and consistent outcomes at very low marginal cost.”21

In addition, AFCs also create capabilities for monitoring spectrum use (and non-use) and for assisting enforcement of the rules that avoid or mitigate interference. For example, when the United Kingdom adopted its version of unlicensed access to TVWS, its telecommunications regulator (Ofcom) required database coordinators to incorporate an information system that allowed the agency to “see the locations and channels used by WS devices at any point in time,” as well as a “kill switch” function that allows Ofcom to “turn down any WS device within a short period of time” if there is an interference problem.22 These features, along with others, offer regulators a high level of visibility and control of a shared spectrum environment compared to what they have now in relation to unlicensed or even licensed bands.

Citations

- Cisco’s most recent projection of global data traffic forecasted continued year-to-year growth of 30%, with nearly 80% of all internet data traffic flowing over mobile (22%) or Wi-Fi networks (57%) by 2022, and Wi-Fi offload traffic increasing to 71% of total mobile data traffic. Cisco Visual Networking Index: Global Mobile Data Traffic Forecast Update, 2017–2022, Cisco White Paper (Feb. 2019) (“Cisco 2019 VNI”), available at source.

- See Executive Office of the President, President’s Council of Advisers on Science and Technology, Realizing the Full Potential of Government-Held Spectrum to Spur Economic Growth, Report to the President (July 2012) (“PCAST Report”); Thomas K. Sawanobori & Dr. Robert Roche, “From Proposal to Deployment: The History of Spectrum Allocation Timelines” (July 20, 2015), source; Federal Communications Commission, Connecting America: The National Broadband Plan (2010), available at source.

- See Calabrese 2011 TPRC at 10-11.

- DSA, Automated Frequency Coordination, supra, at 29.

- Ibid.

- DSA, Automated Frequency Coordination, supra, at 32.

- 3.5 GHz Report & Order at ¶ 72.

- Preston Marshall, Three-Tier Shared Spectrum, Shared Infrastructure, and a Path to 5G (Cambridge Univ. Press, 2017), at 104. Ideally, coordination should be “invisible to the current users of the spectrum being shared.” Id. at 82.

- Comments of Open Technology Institute at New America and Public Knowledge, WT Docket No. 19-38 (June 3, 2019), at 12, source (“OTI and PK Secondary Market Comments”).

- See DSA, Automated Frequency Coordination, supra, at 17-20. Since 2004, the FCC has certified multiple commercial database operators, under delegated authority, to register, manage and coordinate point-to-point links in the 71-76 GHz, 81-86 GHz and 92-95 GHz bands shared with federal agencies, including an automated interface with a NTIA database that yields a “green light, yellow light, or red light” with respect to interference in a particular location with the government links. See FCC, “Order and Notice to Database Managers for the 70/80/90 GHz Link Registration System Under Subpart Q of Part 101,” WT Docket No. 13-291 (rel. Aug. 26, 2016).

- Comments of the Wireless Internet Service Providers Assn, GN Docket No. 12-354, at 25 (July 24, 2017), source. According to a 2017 survey of WISPA members, 25% of respondents said that they had made efforts to obtain licensed spectrum from AT&T, Verizon, Sprint or T-Mobile – and that less than 10 percent of the WISPs who tried to obtain spectrum successfully did so. See Comments of the Wireless Internet Service Providers Assn, GN Docket No. 17-258 at 43-44 (Dec. 28, 2017).

- Mobile Future, “FCC Spectrum Auctions and Secondary Market Policies: An Assessment of the Distribution of Spectrum Resources Under the Spectrum Screen,” at 18-19 (Nov. 2013), available at source. Similarly, only 11% of the spectrum licenses transferred went similarly from nationwide to non-nationwide carriers.

- Comments of Ruckus Wireless, GN Docket No. 12-354, at 5 (July 24, 2017) (shifting from license areas the size of census tracts to counties “would greatly impair the formation of a dynamic secondary trading market for PAL licenses or access, due to the concentration of a smaller number of PAL licenses into the hands of a few very large companies that are not well known for making fallow licensed spectrum available to others.”).

- See Comments of Google LLC, Partitioning, Disaggregation, and Leasing of Spectrum, WT Docket No. 19-38, at 7-10 (June 3, 2019) (describing evidence of market failure and recommending that “’use of share’ requirements for spectrum licensees would be warranted to align the obligations of spectrum holders with the interests of consumers”).

- OTI and PK Secondary Markets Comments at 13-14.

- DSA Report at 51.

- OTI and PK Secondary Markets Comments at 9.

- See Edward Carlson and Justin Goss, “The State of the Urban/Rural Digital Divide,” National Telecommunications and Information Administration Blog (Aug. 10, 2016),

- See “OVUM White Paper Reveals Growth in Fixed Wireless as an Alternative to Fiber for Enterprise-Class Services,” Business Wire (March 15, 2018), available at source.

- DSA, Automated Frequency Coordination, supra, at 33.

- Id at 12-13.

- European Conference of Postal and Telecommunications Administration (CEPT), Electronic Communications Committee, ECC Report 236 (May 2015).