Rachel Fishman

Director, Higher Education

The Federal Government Continues Its Predatory Lending Program

Just over five years ago I published The Wealth Gap PLUS Debt: How Federal Loans Exacerbate Inequality for Black Families. That report detailed how the federal government has created a lending program—Parent PLUS loans—that allows parents to borrow nearly unlimited sums of money to send their children to college. These loans can be approved regardless of a family’s ability to repay. And when it does come time to repay there are very few flexible repayment options for parents. These debts can hound parents who are unable to repay. They can face harsh consequences including ruined credit reports, wage and social security garnishment, and tax return seizure.

Parent PLUS loans were established in the 1980s to give access to more affordable financing to middle-income students during a time of high interest rates. Multiple factors have led to the growth of the PLUS loan program over time: For decades, the cost of college has grown faster than the rate of inflation; the Pell Grant which is the cornerstone for need-based financial aid has not kept pace with inflation; states over the years have disinvested from their higher education institutions; and the need for a higher education degree, particularly bachelor’s degrees to secure middle-wage jobs, has increased sharply.

The result is that the Parent PLUS loan program is now burdening some of the neediest families with inescapable intergenerational debt that exacerbates the gap between the haves and have nots. Higher education, meant to be a catalyst out of poverty, makes poverty inescapable and permanent for some. No other demographic group feels this as acutely as Black families, who because of structural racism that has prevented wealth accumulation, tend to have the worst outcomes when it comes to both repaying loans and seeing strong labor market returns to their higher education. That the federal government enables low-income parents to borrow money that they will not be able to repay—and allows institutions to easily sign parents up for these loans—is part of the structurally racist harms inflicted upon this community.

Parent PLUS loans are also a part of the growing student debt crisis among older borrowers. We expect and hope that the loans made to low-income students will change their income trajectory—it’s why the federal government makes these loans and why there is a public interest to do so. But making a loan to a low-income parent will not change the parent’s income—instead parental income is likely to go down during repayment given that parents of college students are often nearing retirement age. Since 2004, the number of borrowers aged 60 and older grew six-fold, while their outstanding debt grew 19-fold. This translates to 3.5 million Americans 60 and older holding over $125 billion in student loans. While many older borrowers took out loans for their own education, many others have borrowed PLUS, and some are servicing their own debt for their own education while also taking on more loans for their child’s education.

While true that higher education policy alone has not led to this problem of intergenerational debt—segregated housing, k-12, and labor policies have all contributed—this should not absolve states and the federal government from taking an equity-centered approach when creating policies that enable pathways to affordable, high-quality credentials that lead to good jobs. The goal should be to maintain higher education as an engine of opportunity for students.

In this piece, I revisit the data from my original report and look at new data released in the intervening years to show that no progress has been made in preventing the harms of the Parent PLUS loan program. I conclude with policy recommendations for the Parent PLUS loan program, many of them unchanged since my original report.

A Snapshot of PLUS Loan Families from 2011-12 to 2019-20

In my original analysis, I used 2011-12 data from the U.S. Department of Education’s National Postsecondary Student Aid Study (NPSAS). NPSAS uses a nationally representative survey of undergraduates and pairs it with institution records, government databases, and other administrative sources to allow for researchers to understand how students and families finance their higher education. Since my report, there have been two other waves of NPSAS data in 2015-16, and 2019-20. My analysis looks at all three of these waves of data together.

It continues to be the case that overall, only a small percentage of students have parents who borrow PLUS loans. Only 5 percent of dependent students have parents who borrowed PLUS loans in 2011-12, which declined slightly to 4 percent in both 2015-16 and 2019-20. Yet interesting differences in who borrows the loans emerge once the data are analyzed by adjusted gross income (AGI), expected family contribution (EFC), and with a particular focus on Black families who often borrow more and face worse outcomes.

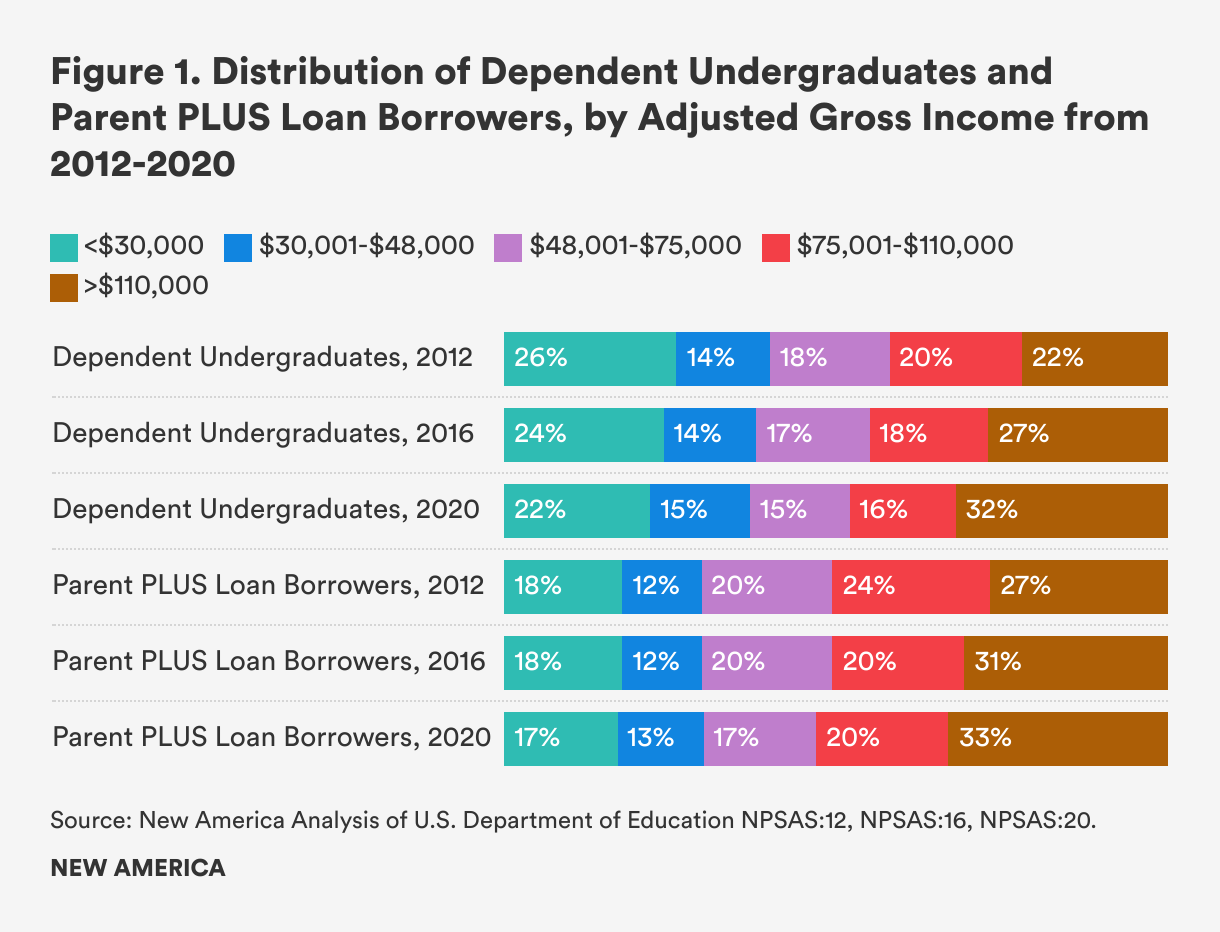

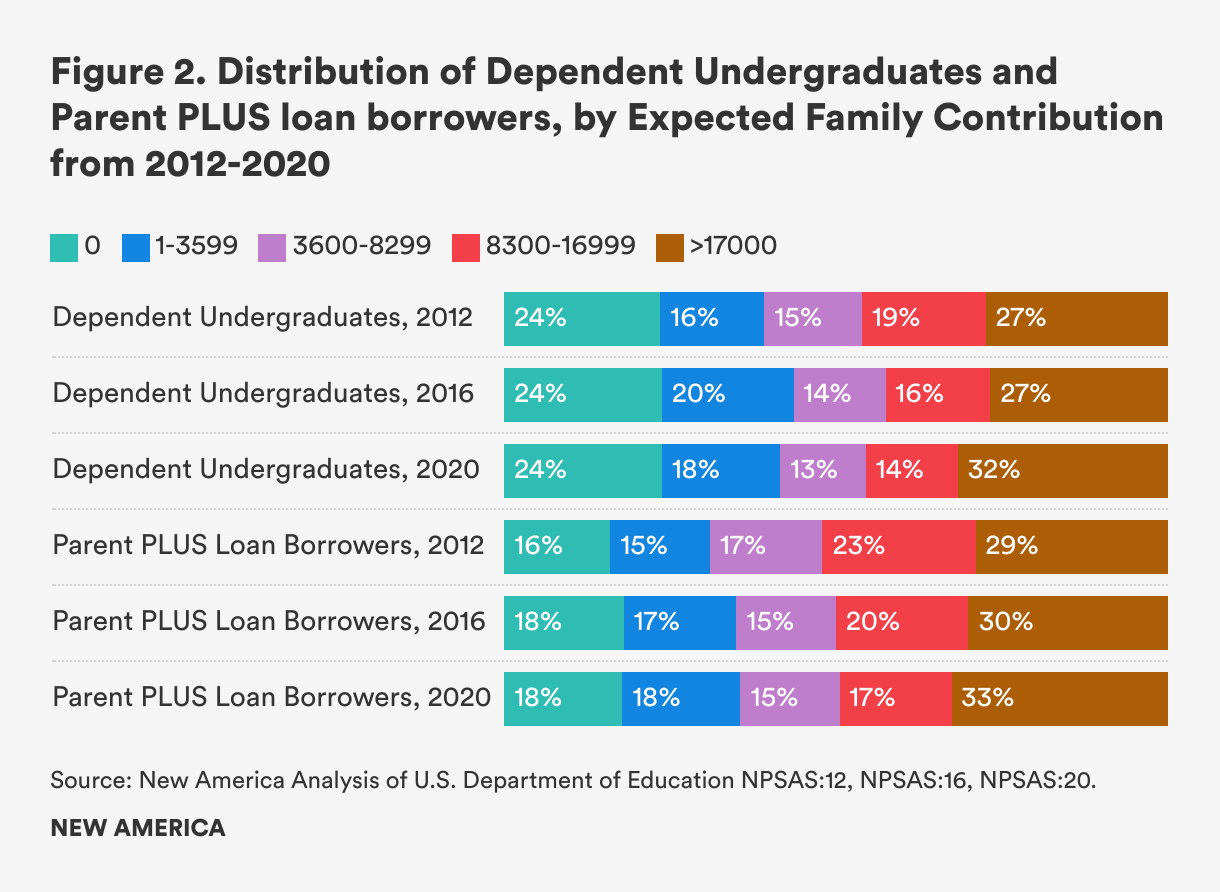

In Figure 1, I compare the distribution of dependent undergraduates to that of students whose parents borrowed PLUS by AGI. Parent PLUS borrowers tend to come from higher income families compared to the general population of dependent undergraduates overall. A majority of parent PLUS borrowers from 2012 to 2020 come from families with AGIs over $75,000. Looking at Expected Family Contribution (EFC), a measure established in law that tries to determine a family’s ability to pay for college and takes into account a variety of factors including number of children in college, the story is similar. (See Figure 2.)

One important factor to keep in mind as a rule for EFC is that a 0 EFC means that the federal government has determined that the student and their family should be contributing $0 towards their higher education, and that the federal government, state government, and institution should be picking up the tab. In actuality, low-income families face large gaps they must pay even when they maximize their grant and student loan aid.

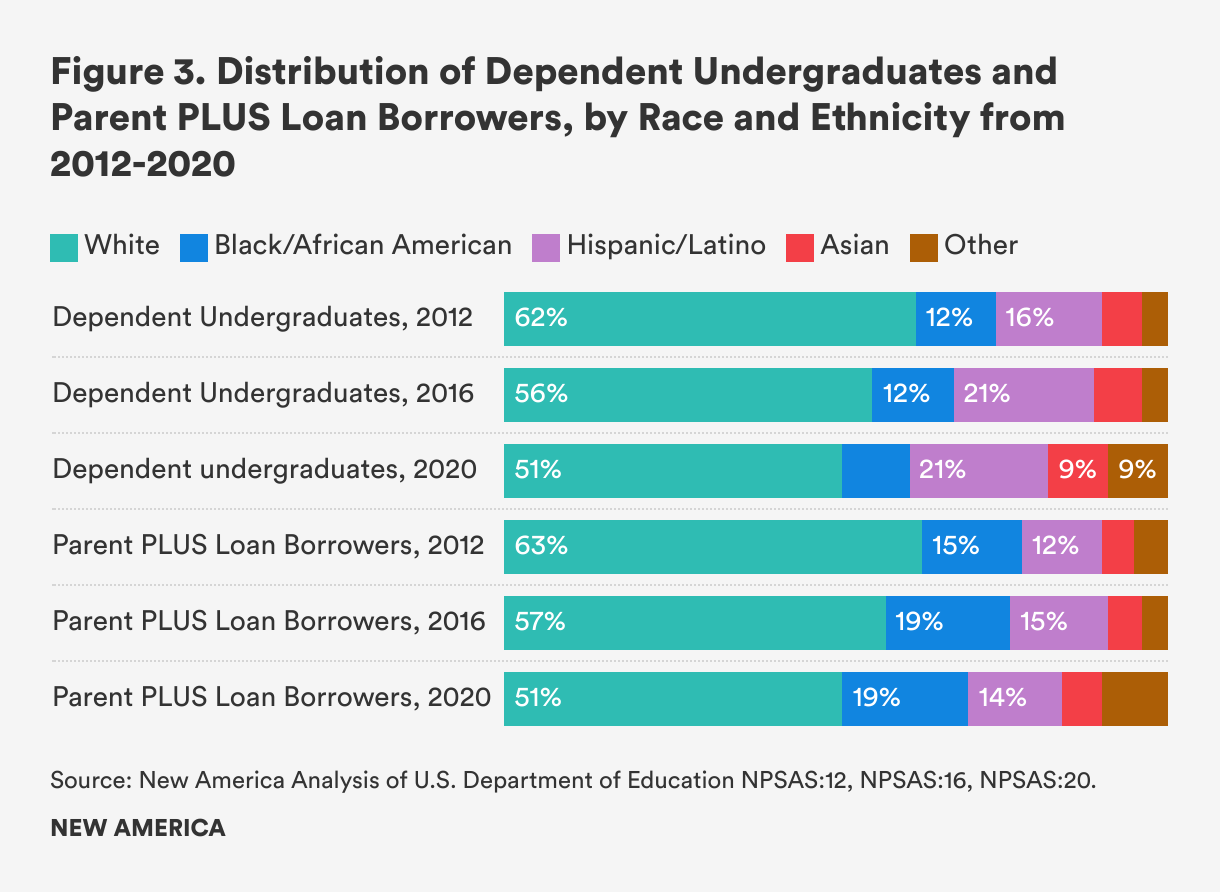

As in 2011-12, a majority of Parent PLUS loan borrowers are white, however there has been a fairly steep decline in white borrowers of PLUS as the share of white dependent undergraduate enrollment has also declined (See Figure 3). Black enrollment of dependent undergraduates has also been in decline, but the proportion of those borrowing PLUS has grown. Black students are the only racial demographic that is overrepresented in their borrowing rate compared to their enrollment.

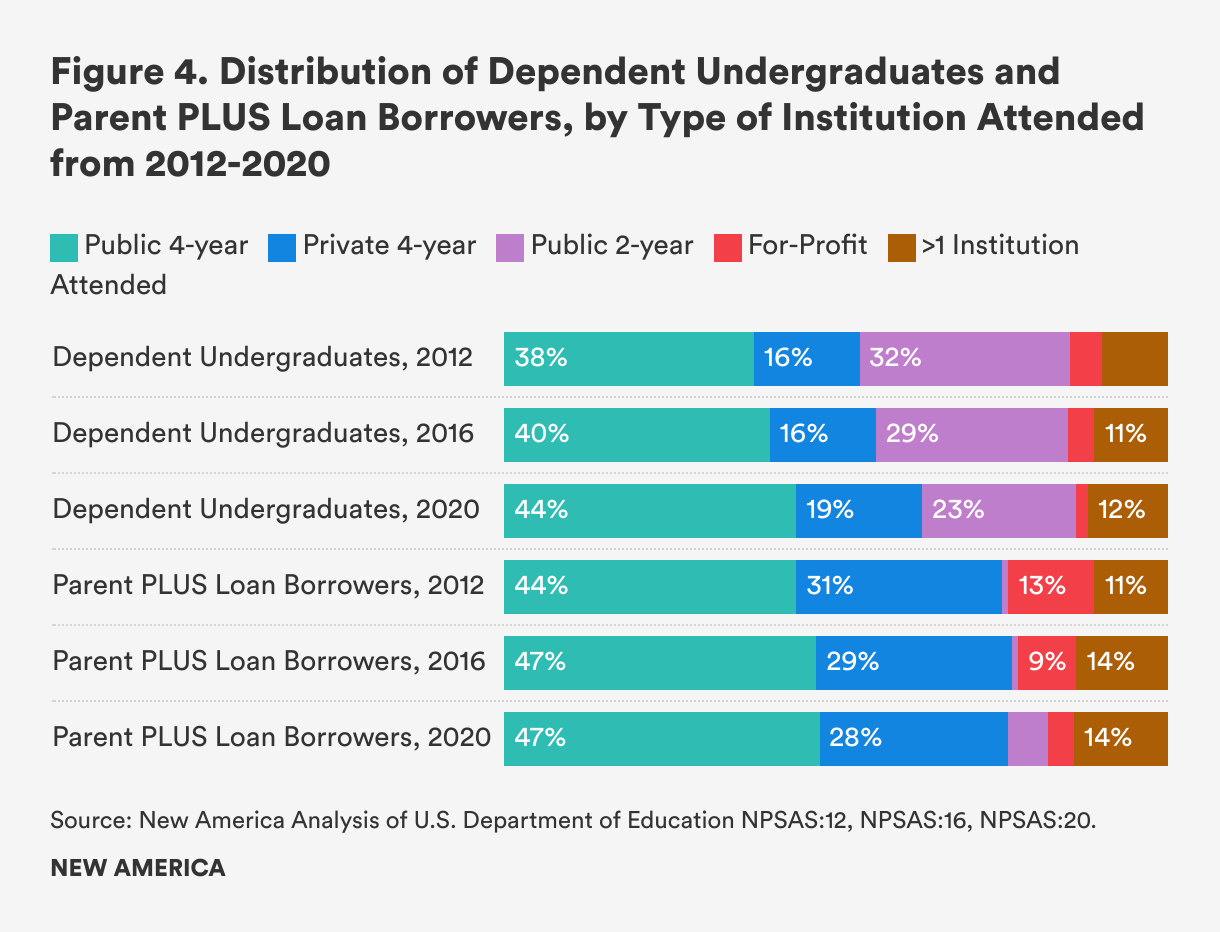

Most students whose parents borrowed PLUS continue to be enrolled in the public 4-year sector—only slightly overrepresented compared to the overall undergraduate population (See Figure 4). Private, four-year institutions and for-profit institutions both continue to be overrepresented in the proportion of families who borrow parent PLUS—although both have seen declines in the percentage of parents borrowing PLUS since 2012. Interestingly, while public 2-year colleges are underrepresented in their PLUS loan borrowing, there was a stark increase in the percentage of students who had parents borrow in 2019-20. This may be due to the pandemic and the particular hardships community college students and their families suddenly faced. This should be a trend researchers keep an eye on to determine whether the community college borrowing was indeed a pandemic blip.

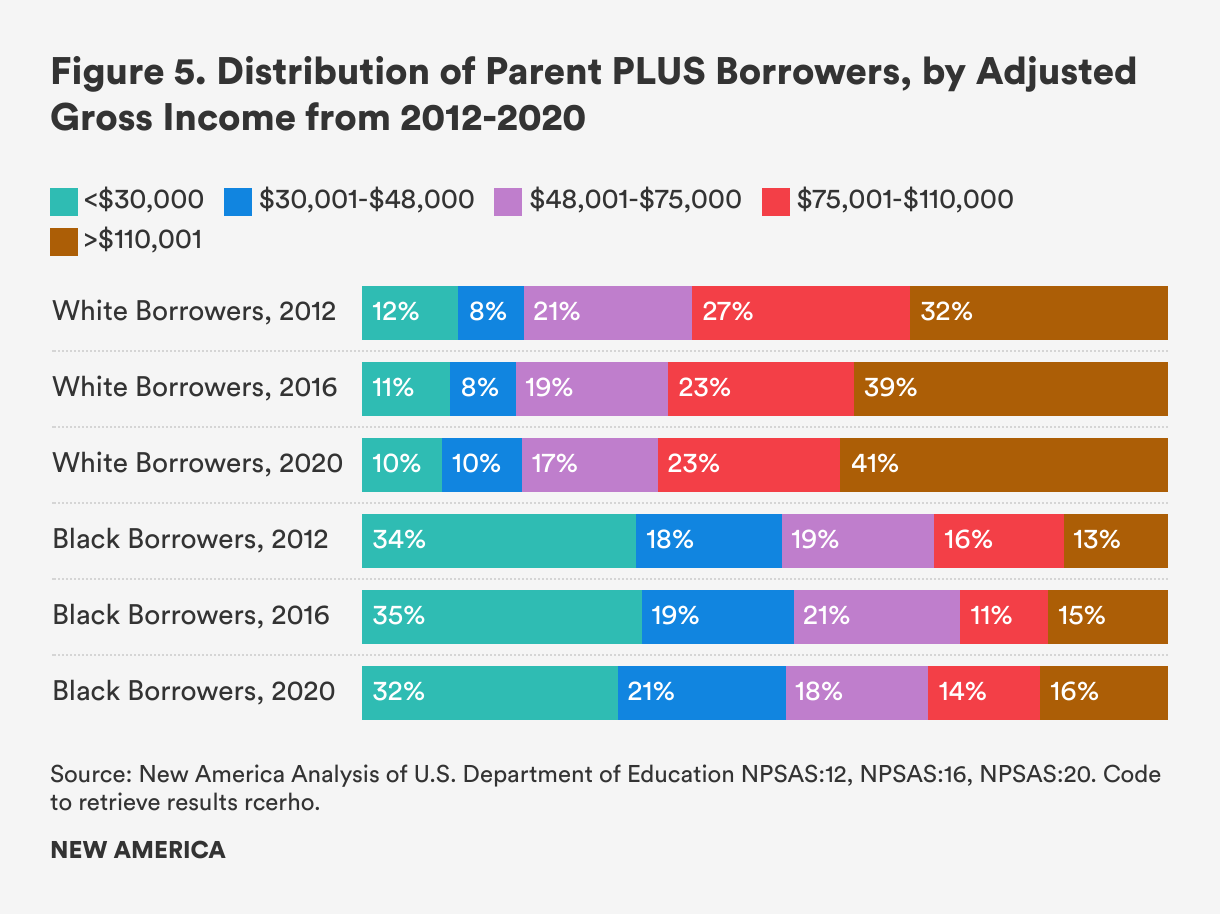

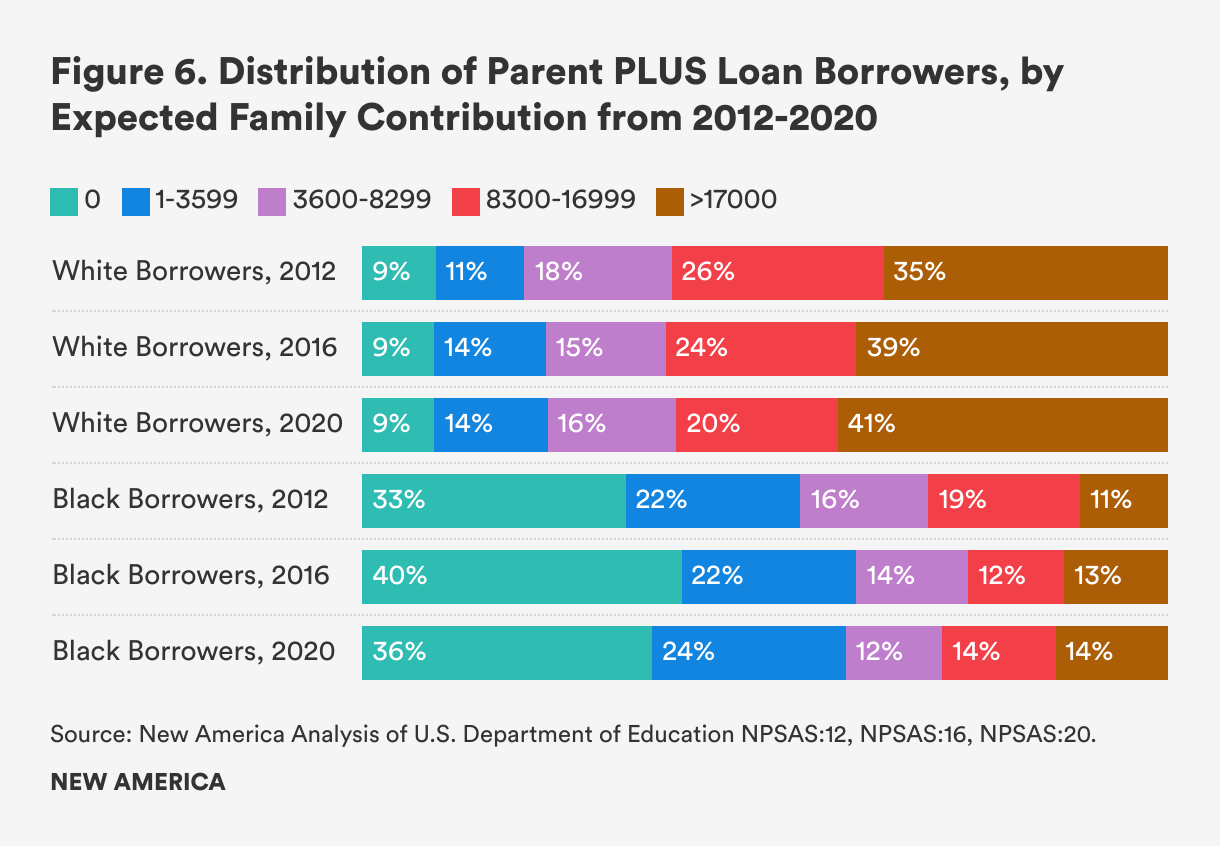

Given that Black borrowers are overrepresented as PLUS borrowers and that they tend to have worse outcomes with federal student loans, I also compared the share of Black PLUS loan borrowers with white borrowers by AGI and EFC (See Figures 5 and 6). Here we see not much has changed for Black students whose parents borrowed PLUS—nearly a third have AGI’s less than $30,000. White students whose parents borrowed PLUS, however, have seen the proportion of the wealthiest borrowers grow. In 2012, about a third of white borrowers had incomes over $110,000. In 2020, that proportion grew to 41 percent. When looking at differences in borrowing by EFC, a similar pattern emerges.

For white families, the PLUS loan works exactly as designed—middle- and higher-income families use it for liquidity, and likely given their higher incomes and EFCs, they’ll be able to afford repayment. Meanwhile a significant proportion of Black families who the government has determined cannot afford to contribute any money towards their higher education (0 EFC families) are relying on the program to fund their child’s education. This is after the student has likely exhausted Pell Grants and their own student loans.

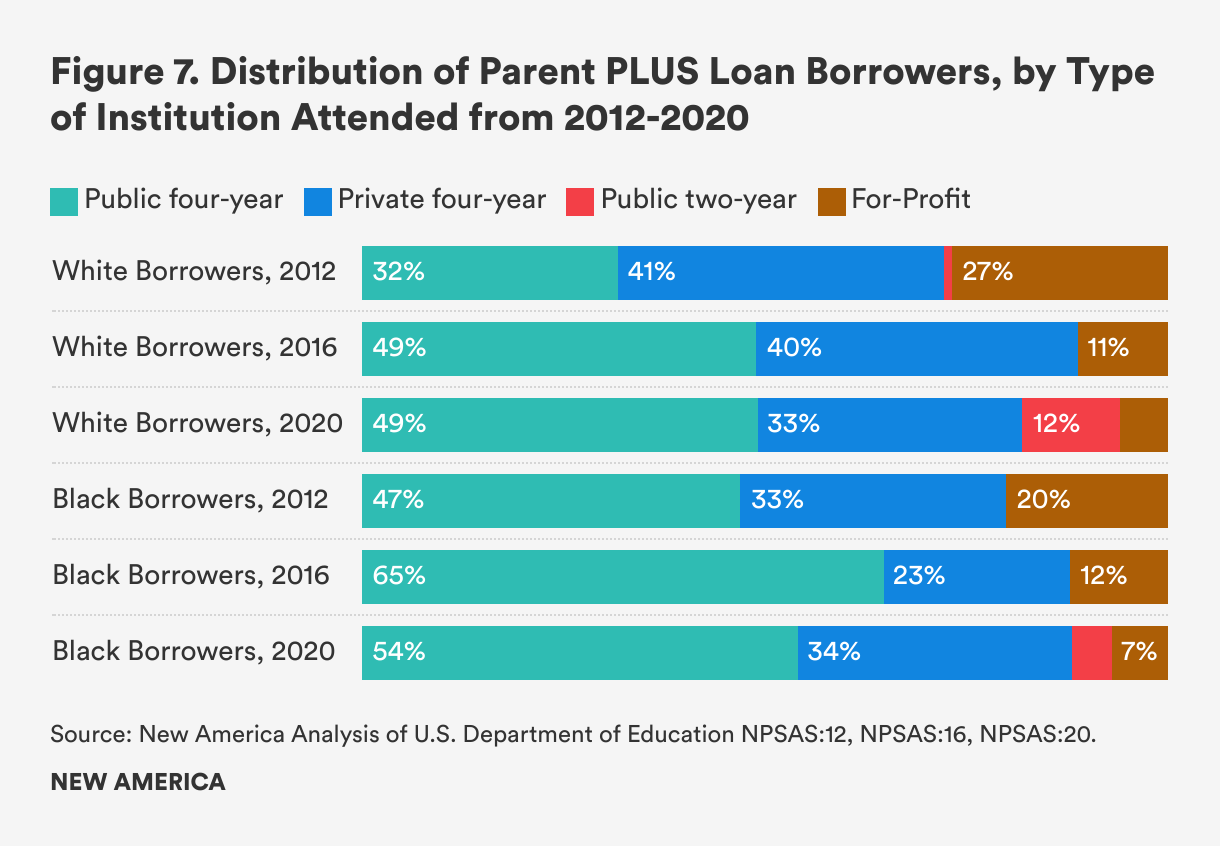

The types of colleges and universities where Black and white students enroll does not easily explain the disparate patterns we see by race and income (See Figure 7). Black PLUS loan borrowers are mostly borrowing to attend public institutions, and since 2012 the share of Black PLUS borrowers has declined at for-profit institutions, likely due in part to the large enrollment decline of that sector as many predatory institutions collapsed and closed and the labor market improved in the wake of the Great Recession.

Total Intergenerational Debt Accumulation Between 2011-12 and 2016-17

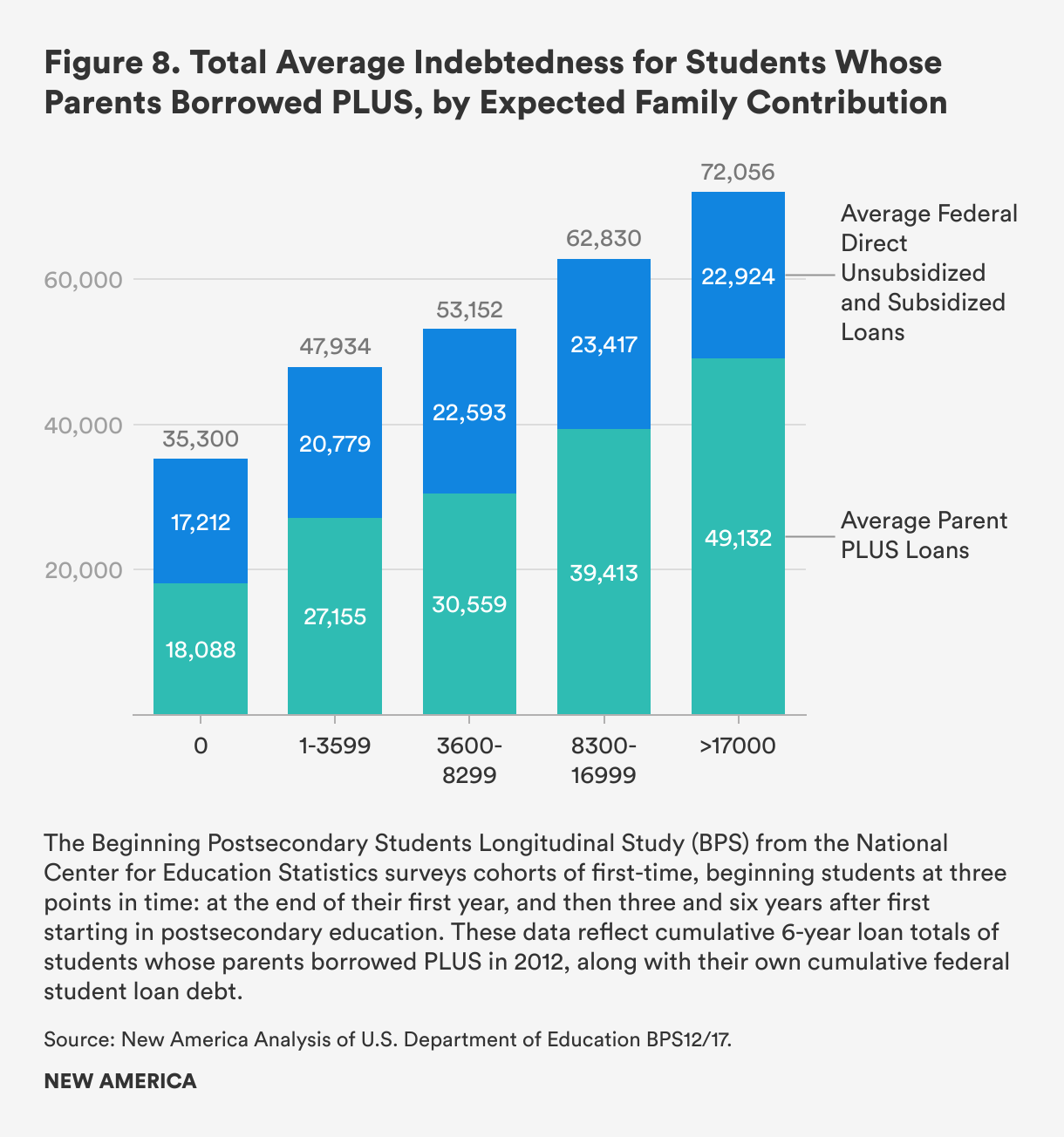

Using a different data set, the Beginning Postsecondary Students Longitudinal Study (BPS), I am able to gauge total average indebtedness for students whose parent borrowed a PLUS loan and their own average federal student loan debt. BPS surveys cohorts of first-time, beginning students at three points in time: at the end of their first year, and then three and six years after. This helps give a picture of how much intergenerational debt families are on the hook to repay for a child’s higher education. As seen in figure 8, for students who entered higher education in 2011-12 and had parents who borrowed PLUS, significant levels of debt were accumulated by both students and parents over six years. For 0 EFC families, the average family accumulated approximately $35,000 of intergenerational debt. For families with EFCs greater than 17000, the average intergenerational debt load was about $72,000.

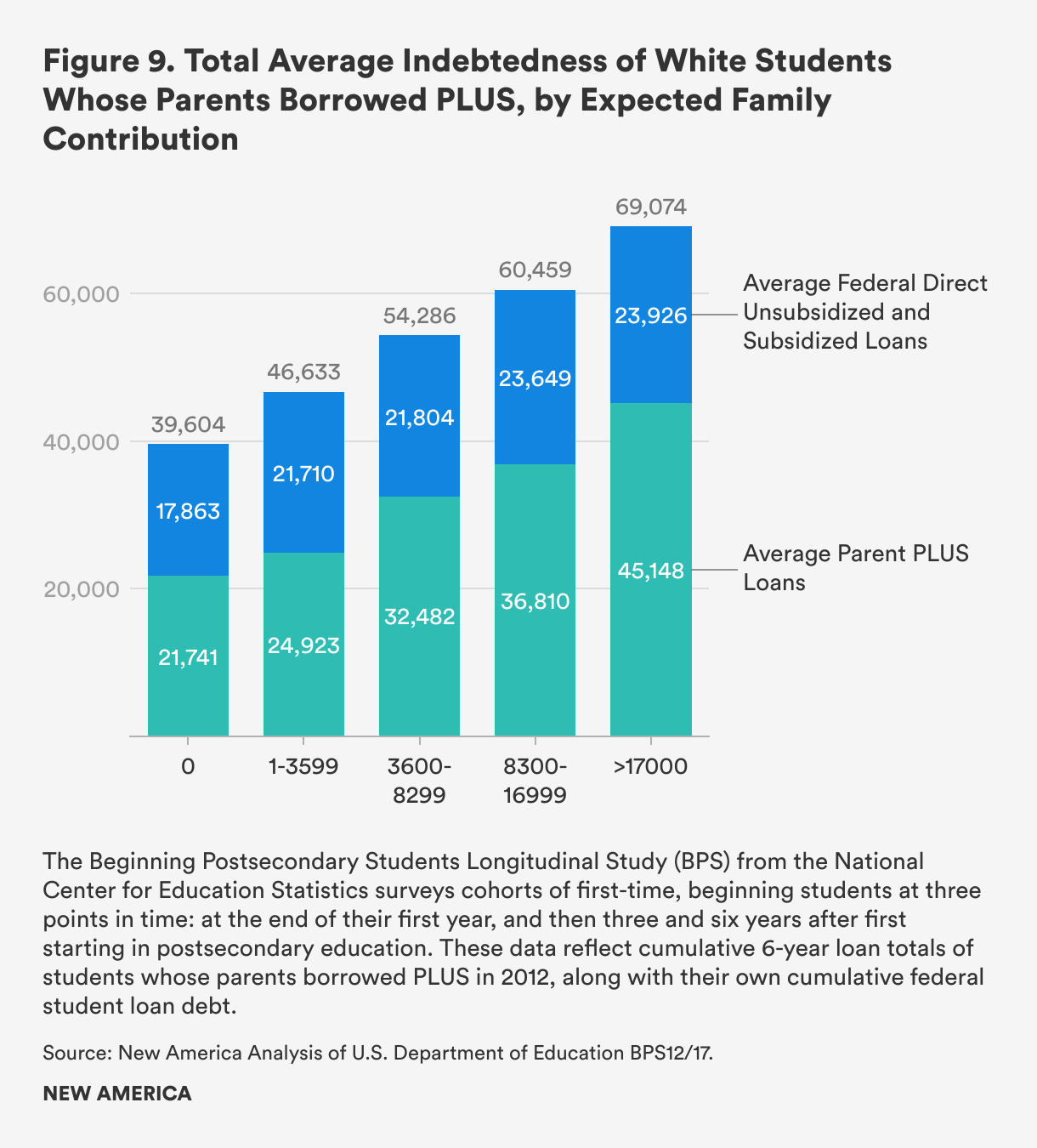

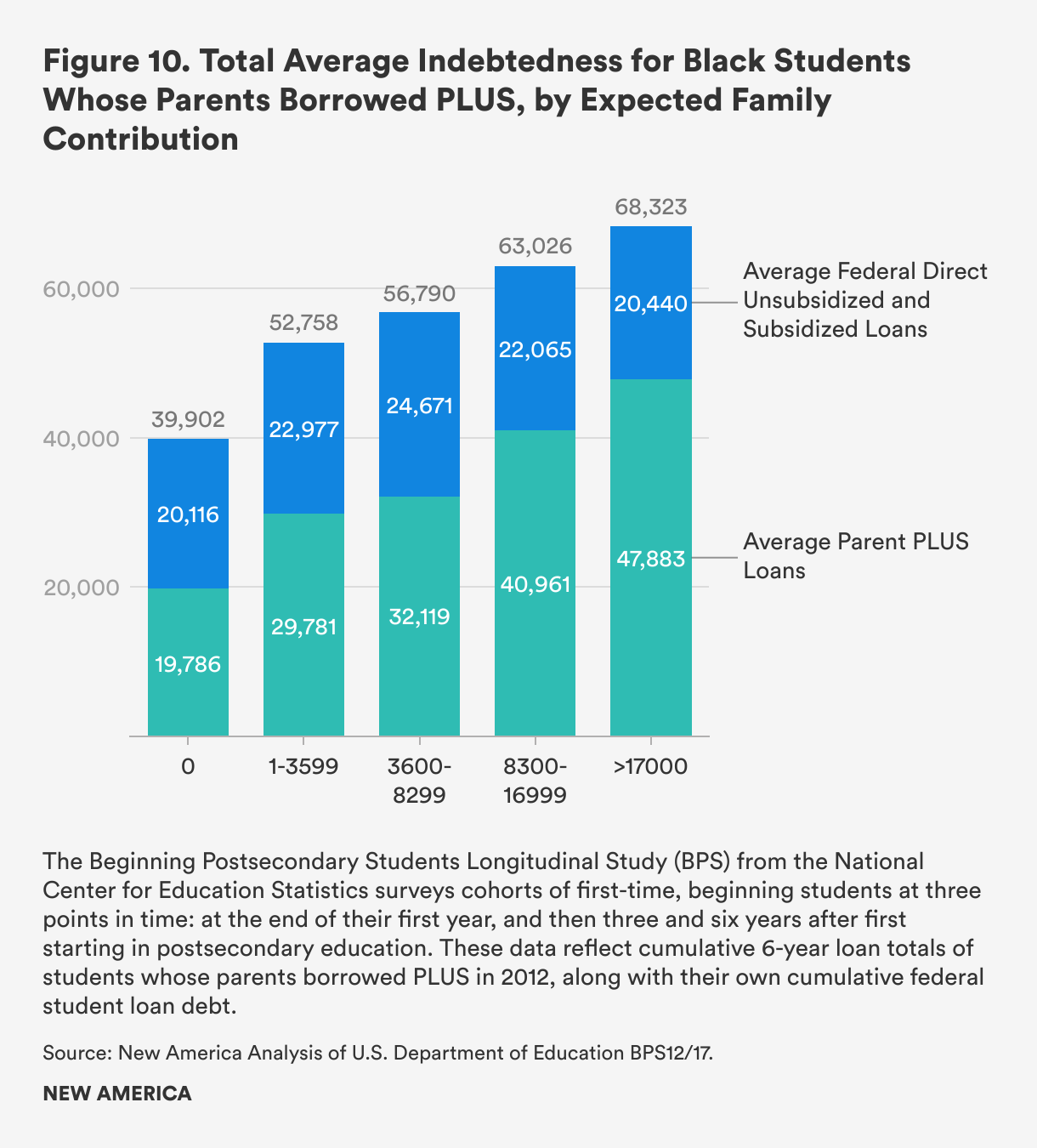

Figures 9 and 10 show what total average indebtedness looks like by white and Black borrowers. There are not large differences between the amounts borrowed by white and Black families, but it is still important to keep in mind that Black families are overrepresented as PLUS borrowers and a much higher proportion of Black PLUS borrowers come from 0 EFC families.

A Decade of Federal Loan Disbursements and Recipients

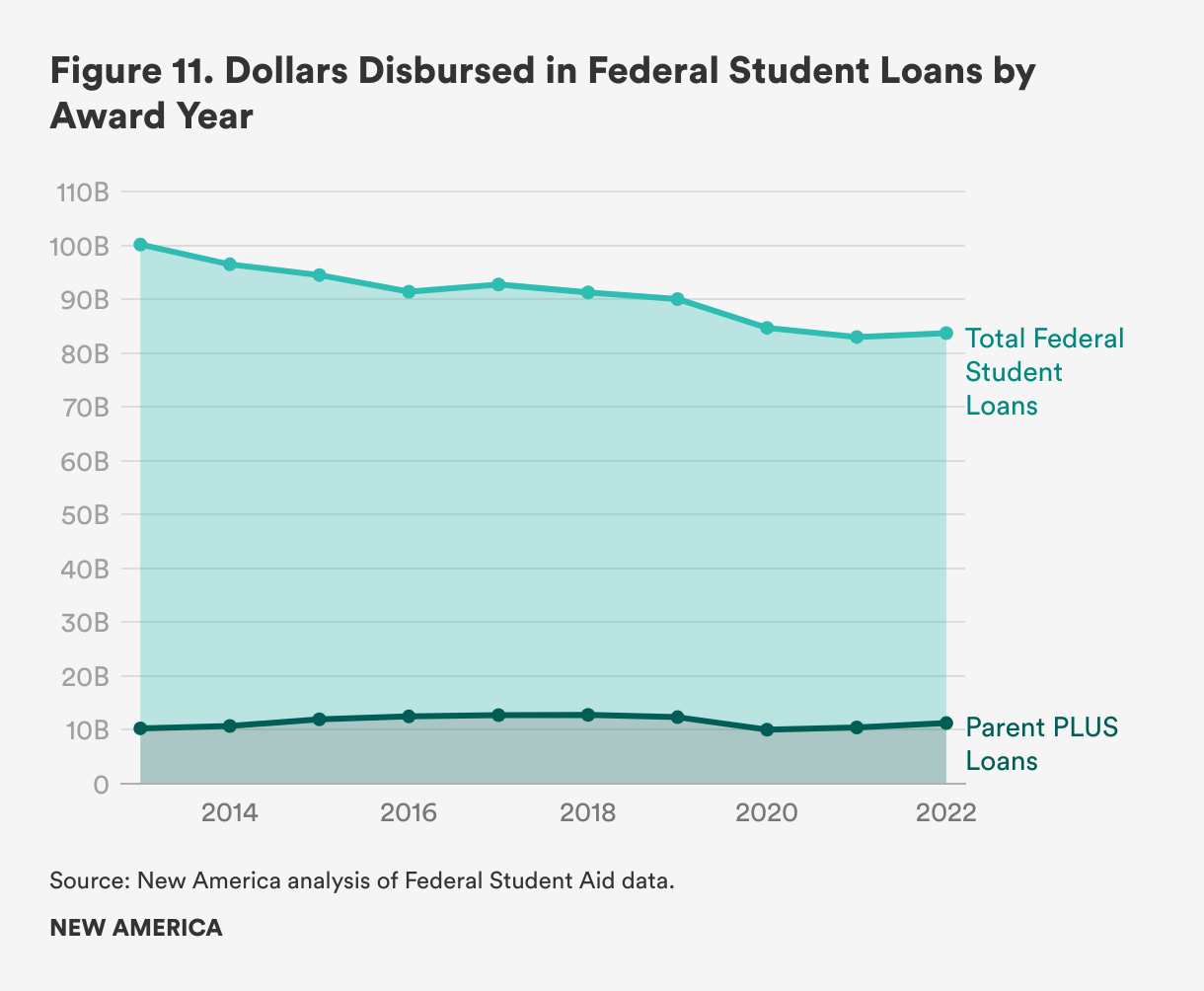

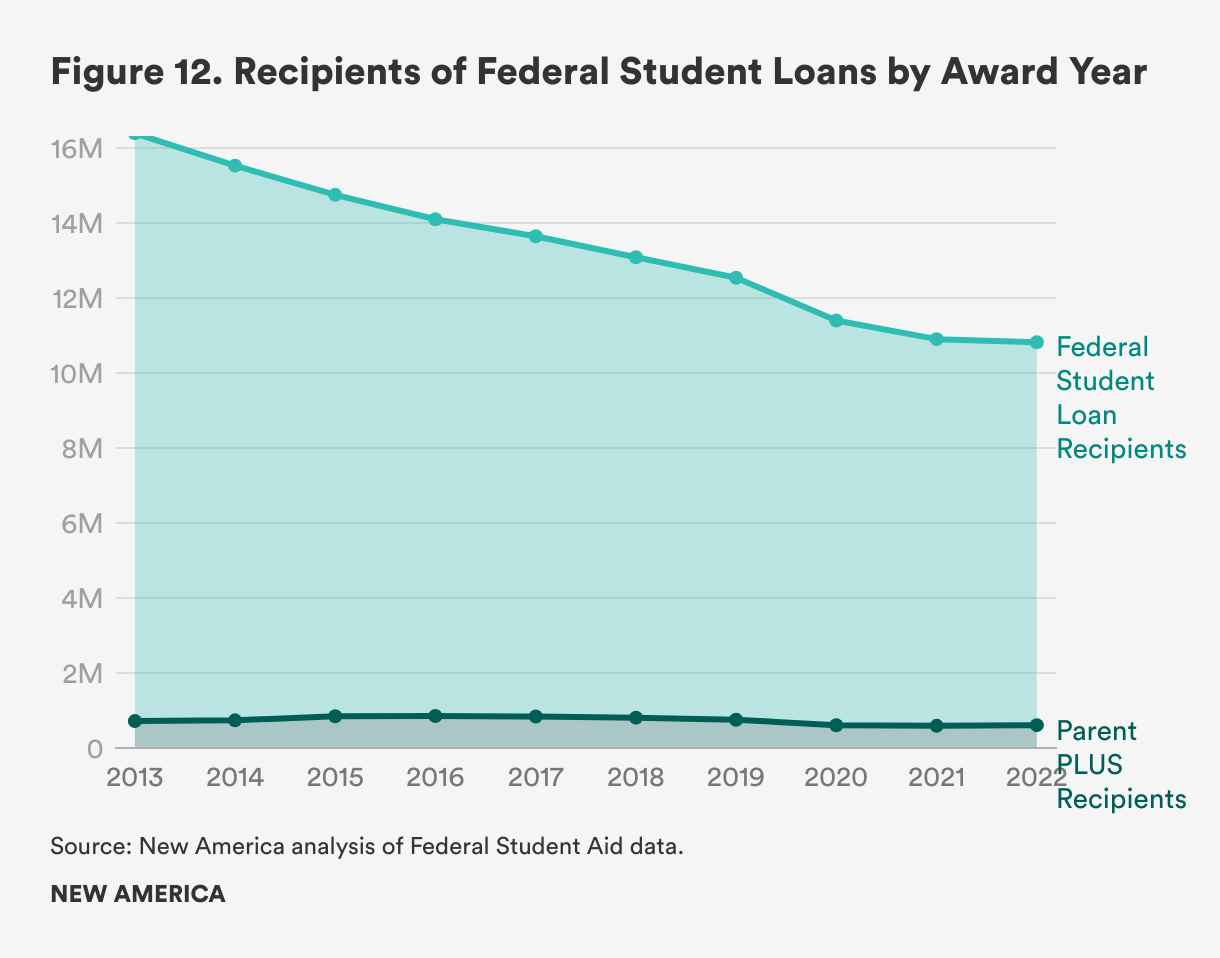

The data show concerning racial differences of who borrows PLUS loans and who can afford to pay them back, and just how much intergenerational debt families take on for higher education. Another trend to watch is that according to Federal Student Aid disbursement data, while federal student lending has decreased overall, Parent PLUS lending has remained fairly steady. This indicates reliance on this loan continues to be strong despite declining enrollments. The yearly disbursements of the federal student loans have declined by almost $10 billion from 2013 to 2022. Meanwhile Parent PLUS loan disbursements have remained fairly steady by comparison, which has resulted in a $1 billion dollar increase in 2022 compared to 2013 (see Figure 11).

Over the years, as the economy has recovered from the Great Recession and entered a pandemic recession and recovery, enrollments in higher education have declined. With that decline has come a decline in federal student loans overall. We would have this expectation—the less students who enroll in higher education, the greater the decline in those borrowing loans. Federal student loan recipients have declined overall by nearly 6 million borrowers between 2013 and 2022. PLUS loan borrowers have also decreased over that same time frame, but not as precipitously (see Figure 12). Importantly, the decline in recipients and the increase of dollars disbursed means that parents are likely taking out larger amounts of loans.

Ending Federal Predatory Lending for Higher Education

Unfortunately, the landscape of Parent PLUS loans remains largely the same as it did in 2018. I wrote then, “The federal government provides ‘access’ to higher education, via PLUS loans, to any college or university as long as a parent is approved. But if the parent is low-wealth, then a PLUS loan does not provide true access because it will ultimately result in harm and erasure of wealth when the bill is due. The switch to intergenerational debt-financing for higher education has worsened the racial wealth divide.” No policy has been put in place—or has been legitimately considered in any Congress since—that truly gets at what needs to change to ensure families aren’t actively harmed in pursuit of a higher education.

Because little has changed since 2018, many of my recommendations for reforming the program remain the same. But several key analyses from places such as the Urban Institute, the Century Foundation, Georgetown’s Center on Poverty and Inequality, and from my own colleague Stephen Burd have helped strengthen some of them.

The Parent PLUS loan program highlights broader affordability and accountability problems in our system of higher education. There needs to be fixes to the program itself and broader reform beyond Parent PLUS.

Parent PLUS Loan Fixes

Adding an ability-to-repay measure to the Parent PLUS credit check would be a fair standard, ensuring parents are able to access a loan that is capped to prevent borrowing beyond their means. The government collects information to calculate a family’s Student Aid Index (formerly known as EFC before the advent of the new FAFSA). This same information could be used to determine a family’s loan limit. If a family has a negative or zero SAI, the parent applying for a PLUS loan would not be extended one. Instead the student would be offered additional loans up to the independent lending limit, automating a process that currently happens when parents are rejected for PLUS loans based on adverse history alone. This equates to an additional $4,000 to $5,000 in federal student loans a year.

On the flipside, if a family is higher-income and has a 17000 SAI, the parents could take out up to $17,000 in a PLUS loan or the full cost of attendance of the school, whichever is lower. In both situations, students would still be able to borrow up to the loan limits for which they’re eligible.

While giving more loans to low-income dependent students is not the ideal situation, given our current reliance on debt-financing for many students and families, it’s important that the loans that are taken on come with more protections than Parent PLUS loans, like access to income-driven repayment plans and lower interest rates. This also ensures the neediest of parents do not end up with non-dischargeable debt they cannot afford as they close in on retirement. Students should also be required to exhaust their own loan eligibility before their parents turn to PLUS, since federal student loans have much more flexible repayment options.

While income-driven repayment makes less sense for parents whose income trajectory remains largely unchanged from the education their child received, an insurance policy is still needed for parents to prevent punitive consequences if they fall into hard times. Once an ability-to-pay measure is in place, parents should be able to access income-driven repayment. Giving access to income-driven repayment without an ability-to-pay measure in place creates a complicated back door grant program that institutions, particularly for-profit institutions who have a record of predatory behavior, will likely exploit.

Three-year institutional cohort default rates should be calculated for Parent PLUS. Just like with current cohort default rate policy, institutions should face sanctions if their Parent PLUS default rate is at least 30 percent (if not lower, since parents must pass a credit check), including loss of eligibility to offer PLUS loans if the rate remains high year over year.

Given the pandemic payment pause and improvements in sign up for income-driven repayment plans, cohort default rates are becoming less and less meaningful. As Congress considers other options, such as repayment rates, to hold institutions accountable for loan payments, Parent PLUS loans must be part of that conversation.

Broader Higher Education Reform

Parent PLUS loan reform cannot be thought of in a vacuum. The reliance of low-income families on PLUS loans is an indicator of an affordability crisis in higher education that goes beyond reforming one loan program alone. Below, I detail targets for broader reform.

There needs to be a new federal state partnership that will require states to fund their institutions in order to participate in federal aid programs. Importantly, this partnership must require that the under-resourced public institutions that serve the most disadvantaged populations—like community colleges, Historically Black Colleges and Universities, and minority serving institutions—get their fair share of funding compared to the state’s flagship institutions.

Accountability metrics, peer groups, and sanctions should be developed in consultation with relevant stakeholders including colleges and universities, their membership organizations, accreditors, federal and state policymakers, and student groups. At a minimum, these metrics must focus on the number and percentage of students who progress through their programs in a timely fashion, graduate or successfully transfer to the next step in an educational track, and secure employment that pays a family-sustaining wage after leaving college (or at the very least, more than what they would have made as a high school graduate). These data would need to be collected at the student level and would require Congress to authorize a Student Level Data Network. This would allow data to be disaggregated by various demographics at the institutional, programmatic, and student level.

Low-income students of color should have the opportunity to attend a prestigious college or university without going through a cumbersome and opaque admissions and financial aid process. For this reason, the most highly-resourced and highly-selective institutions should end legacy admissions and other preferential admissions treatment that overwhelmingly favor wealthy and white families, including early decision programs. Congress could require institutions to comply or risk losing access to federal student aid.

Institutions should also end so-called “merit” aid programs that siphon money away from needy families. These non-need-based aid programs often just reward wealthy students with a discount to entice them to enroll, helping to ensure the institution is able to cover their bottom line while potentially improving their rankings in the U.S. News and World Report. It comes right from the playbook of the private-equity backed enrollment management industry. Parent PLUS loans enable institutions to continue this trend, plugging any gaps that low-income students have with Parent PLUS loans, while giving non-need-based grants to students who don’t need them.

Because the incentives are so misaligned, Congress should investigate enrollment management firms—understanding just how they use algorithms to formulate financial aid packages. Federal policymakers have a right to know how federal student aid is being undermined by enrollment management tactics. This information will help Congress craft policy solutions that prevent institutions from leveraging federal aid in the future, contrary to the mission of the federal government’s student aid programs.

Director, Higher Education