Table of Contents

- The Lending Hole at the Bottom of the Market: Small Dollar Mortgages

- A Roadmap to this Report: Methodology, Data Sources, and Definitions

- It’s Expensive to be Poor: Small Dollar Homes are Inaccessible to Low- and Moderate-income Families

- A Microcosm of the Problem: The City of Winston-Salem, North Carolina

- Increasing Access to Small Dollar Mortgages: Potential Solutions

- Conclusion

The Lending Hole at the Bottom of the Market: Small Dollar Mortgages

“The U.S. financial system has built a well-oiled machine for extending credit to high-earning Americans with conventional finances. The machine sputters when confronted with borrowers on the margins, making it tougher to attain homeownership and its wealth-building potential.” — Ben Eisen, Wall Street Journal reporter

Homeownership is a key component of building wealth in the United States: The average homeowner boasts a net worth of $255,000, close to 40 times that of the average renter ($6,300). And yet, a critical constraint is locking out many low- and moderate-income homebuyers, even those with good credit and money for a down payment: the unavailability of small dollar mortgages for relatively affordable homes.

Nearly 20 percent of all owner-occupied homes in the United States are valued at less than $100,000, according to U.S. Census data. These “small dollar homes” provide a critical source of housing for low- and moderate-income families, often first-time homebuyers and people of color. Yet, for a host of reasons, including an unintended consequence of the post-2008 anti-predatory regulations in the Dodd-Frank Act, banks are increasingly unwilling to write mortgages on these homes. And without borrowing money, most Americans cannot afford to buy a home.

Yet, over the last decade, origination for mortgage loans between $10,000 and $70,000 and between $70,000 and $150,000 has dropped by 38 percent and 26 percent, respectively, while origination for loans exceeding $150,000 rose by a staggering 65 percent. At the same time, small dollar loans (defined in this report as $100,000 or below) are being denied nearly four times as often as larger loans nationwide, according to a 2019 Urban Institute analysis . While it is easy to attribute higher denial rates to weaker credit, a deeper look indicates that not only do borrowers of small dollar loans have similar credit profiles to those with midsize loans, but these loans also perform similarly.

Small dollar homes—intended to be the first rung on the ladder for building wealth—are becoming increasingly inaccessible to low- and moderate-income families reliant on borrowing money. Three quarters of homes costing more than $100,000 were purchased with the help of a mortgage loan in 2019, whereas only 23 percent of homes below $100,000 were purchased with a mortgage loan. Instead, investors and all cash buyers have largely purchased small dollar homes to flip and sell for a profit or for rental income.

Many homeownership assistance programs focus on improving a buyer’s finances through building credit, increasing financial literacy, and providing down payment support. While important, these appear to miss a critical piece of the puzzle for low- and moderate-income buyers: even when they have a down payment together, and even when they have good credit, they often are still unable to purchase a home because banks and other lenders won’t extend them a small dollar loan.

The Immediate Consequence: Homeownership Out of Reach for Millions

When banks and other lenders opt out of the small dollar housing market, and when denial rates are higher for small dollar loans when buyers do apply, homeownership becomes more difficult to access for low- and moderate-income families. Those locked out of the market are left with few choices; they either continue to rent, or enter into riskier alternatives, including rent-to-own agreements and contract-for-deed sales. These predatory housing arrangements, more prevalent in Black and Latinx communities, require buyers to pay off the price of the home without a proper title or rights to the home until the end of the term. Buyers become responsible for upkeep and insurance, but do not benefit from the same wealth-building benefits of homeownership.

This lack of access to homeownership is particularly pernicious for Black households. In the ten years since the Great Recession, the homeownership gap between Black and white households has reached its highest level in 50 years—even higher than when discrimination against Black homebuyers was legal. Today, the Black homeownership rate is 45 percent compared to a white homeownership rate of 74 percent. The huge disparity in Black and white homeownership rates has contributed to the racial wealth gap we see today: A typical white household has 10 times the wealth of a typical Black household. If current trends continue, it could take over 200 years for a Black family to accumulate the same amount of wealth as white families.

The ability to secure a mortgage lies at the heart of unlocking access to wealth-building opportunities and helping to close the racial homeownership gap. Access to small dollar or affordable homes, including the mortgage financing needed to afford these homes, is a complex issue, however, that encompasses a host of different players, acting according to their own incentives, across the housing system. In this report, the Future of Land and Housing program at New America and the Center for the Study of Economic Mobility (CSEM) at Winston-Salem State University (WSSU) focus on three dimensions of this problem: 1) the unavailability of financing for small dollar loans, 2) the catch-22 of mortgage standards, and 3) competition with all-cash buyers.

We explore nationwide lending trends, and ground our research in the City of Winston-Salem and Forsyth County, North Carolina to better understand the causes of the small dollar mortgage gap and in turn, develop effective solutions. We attempt to shed light on how some of the major challenges related to the inaccessibility of financing for small dollar mortgages interact with each other to perpetuate unequal access to homeownership for low- and moderate-income homebuyers, potentially contributing to the stagnation of neighborhoods that is ever-present in cities across the United States.

The Bigger Context: Stagnant Neighborhoods in Segregated US Cities

In the book The Divided City: Poverty and Prosperity in Urban America, author Alan Mallach describes how excitement over investment and development in certain parts of U.S. cities is “tarnished by the reality that in the process, these cities are turning into places of growing inequality, increasingly polarized between rich and poor, white and black, with unsettling implications for their present and future.”1 A 2014 study cited by Mallach of 1,100 high-poverty neighborhoods in fifty-one cities found that between 1970 and 2010, fewer than one in ten had “rebounded”- defined as having a poverty rate falling from above 30 percent to below 15 percent. In addition, there were nearly three times as many neighborhood areas with greater than 30 percent poverty in 2010 versus 1970.

Mallach’s unsettling conclusion is this: “Cities have largely stopped being places of opportunity where poor people come to change their lives, and today’s poor and their children remain poor, locked out of the opportunities that cities offer.”2

Small dollar homes in stagnant neighborhoods have previously served as starter homes for first-time homebuyers, who increase the tax base and contribute to neighborhood stability. We hypothesize that by restricting access to homes in neighborhoods with affordable housing stock, the unavailability of small dollar mortgages contributes substantially to segregation and stagnation.

But when would-be homebuyers are unable to get a mortgage loan, many of these homes are instead purchased by investors with cash on hand and converted into rental properties or flipped and sold for a profit. Unlike a growing family or individual hoping to build wealth and invest in their home and neighborhood, investors are less likely to fix up properties and contribute to neighborhood stability. At the neighborhood level, the result is that areas in cities with depressed home values become “locked in,” unable to rebound through new investment in the same way other neighborhoods can. And, individually, residents in these neighborhoods are unable to build wealth by becoming homeowners, contributing to continued stagnation and declining property values.

Winston-Salem, North Carolina: A Case Study

To better understand how small dollar loans impact a local housing market, we examine the City of Winston-Salem, in Forsyth County, N.C.—a place that typifies the growing economic and racial divide that Mallach writes about in The Divided City. Despite the rebound experienced in some parts of the city, a 2014 study by economist Raj Chetty, found that Forsyth County had the third worst economic mobility for the bottom quintile in the country, and another study found that it has one of the country’s fastest growth in concentrated poverty. According to 2019 American Community Survey data, Forsyth County is in the 93rd percentile for income inequality.

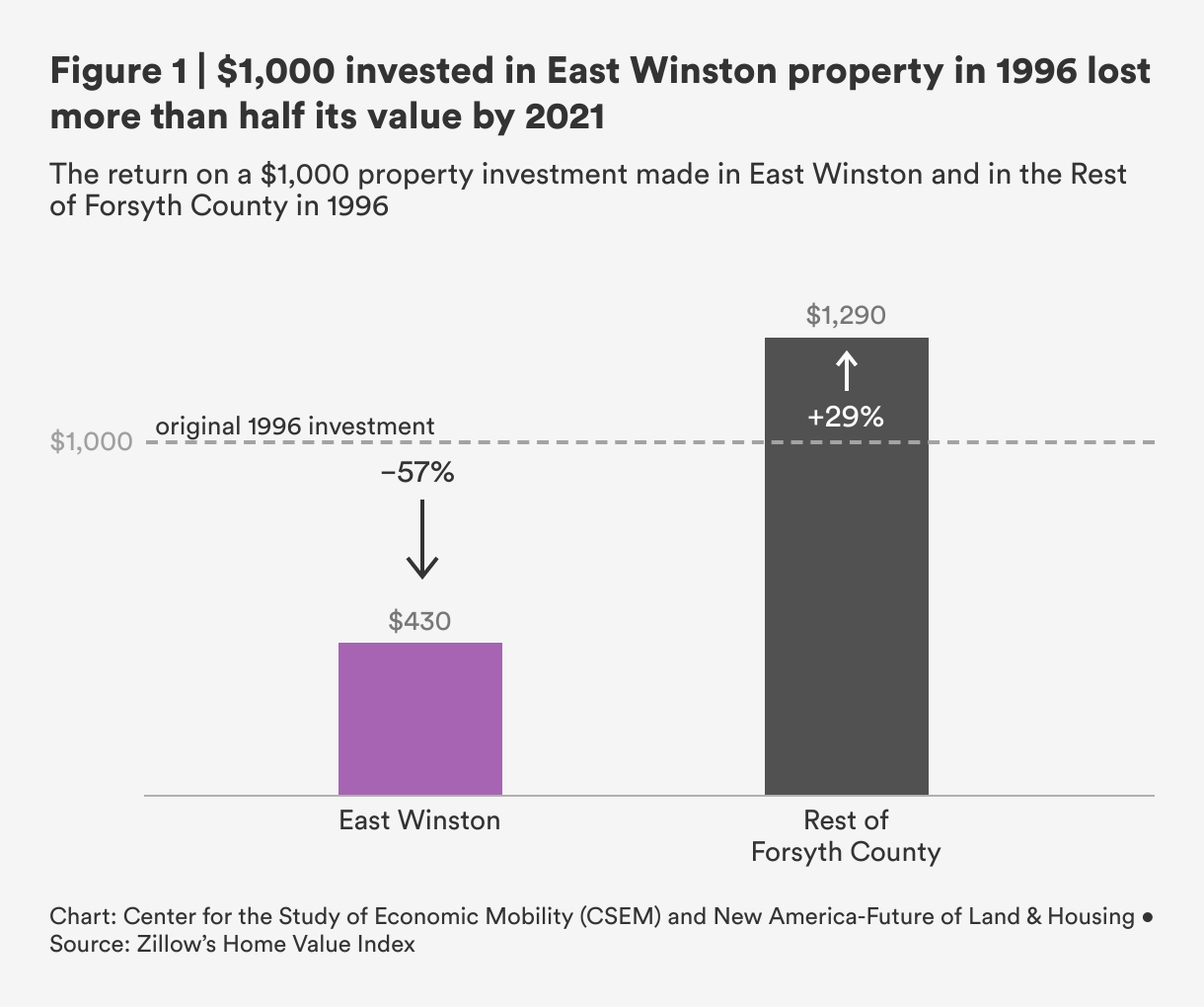

In East Winston, $1,000 invested in 1996 is now worth $430; elsewhere in Forsyth County, $1,000 is now worth $1,290.

Like so many other cities across the United States, Winston-Salem is truly a tale of two cities, split down the middle by U.S. Route 52, a four-lane highway dividing the city into east and west. While the city has seen recent growth and investment to the west side of Route 52, the east side of the city—a collection of historically Black neighborhoods referred to as East Winston—remains disconnected from access to high-quality jobs, housing, and public transit.

Home values in East Winston have plummeted over the last 25 years. Figure 1 illustrates the return on a $1,000 property investment in 1996, the first year Zillow began collecting market data, in East Winston compared to the rest of Forsyth County. We calculated that in real terms, every $1,000 invested in property in East Winston in 1996 is now worth $430; by comparison, every $1,000 invested elsewhere in the county is now worth $1,290.3

Despite the fact that homes in East Winston have fallen dramatically in value and despite the existence of robust homeownership assistance programs in Forsyth County that help cover the cost of homeownership,4 many would-be homeowners are still unable to purchase otherwise affordable homes in these neighborhoods.

Not only does the unavailability of small dollar mortgage loans lock out potential homeowners: We hypothesize that the lack of access to mortgage credit that removes potential buyers from the housing market may be one important reason why we have seen falling property values in East Winston over the past 15 years. Indeed, one clue is that in the past twenty years, East Winston has seen a change in the type of buyers who purchase its inexpensive homes—from a majority of homes sold to buyers relying on mortgage loans, to the majority of homes sold to buyers paying all cash.

The Structure of this Report

This report is organized in the following sections: the next section, titled “A Roadmap to this Report,” provides an overview of our quantitative and qualitative methods, as well as key terms and definitions. This is followed by “It’s Expensive to Be Poor,” an investigation into why it has become increasingly difficult for low- and moderate-income families across the county to obtain small dollar mortgages, drawing on existing research and reporting. The next section titled, “A Microcosm of a Problem” delves into the case study of Winston-Salem, N.C., showcasing our quantitative data and qualitative findings from a local housing market. Then we discuss some potential solutions before concluding this report.

Citations

- Alan Mallach, The Divided City: Poverty and Prosperity in America (Washington, DC: Island Press, 2018), p. 2.

- Mallach, The Divided City, pg. 10.

- The methodology for this analysis is detailed in the source">Technical Appendix.

- Forsyth County runs a highly successful program for low-income and largely Black participants who are interested in becoming first-time homeowners, as reported in severalsource"> CSEM Working papers. However, there are generally only about 10-20 participants a year.