Table of Contents

- The Lending Hole at the Bottom of the Market: Small Dollar Mortgages

- A Roadmap to this Report: Methodology, Data Sources, and Definitions

- It’s Expensive to be Poor: Small Dollar Homes are Inaccessible to Low- and Moderate-income Families

- A Microcosm of the Problem: The City of Winston-Salem, North Carolina

- Increasing Access to Small Dollar Mortgages: Potential Solutions

- Conclusion

It’s Expensive to be Poor: Small Dollar Homes are Inaccessible to Low- and Moderate-income Families

Nationwide, low- and moderate-income homebuyers face a host of challenges in accessing small dollar homes. We explore three major barriers that come into play at different stages in the home purchasing process: 1) the unavailability of financing for small dollar mortgages, 2) the catch-22 of mortgage standards, and 3) competition with all-cash buyers.

Small Dollar Mortgages are Unavailable Nationwide

Many homeownership assistance programs focus on building credit, increasing financial literacy, and providing down payment support for purchasing a home. While these are important, this focus misses a critical constraint that locks out low- and moderate-income homebuyers, even those with good credit and a secured down payment: the unavailability of small dollar mortgages for relatively affordable homes.

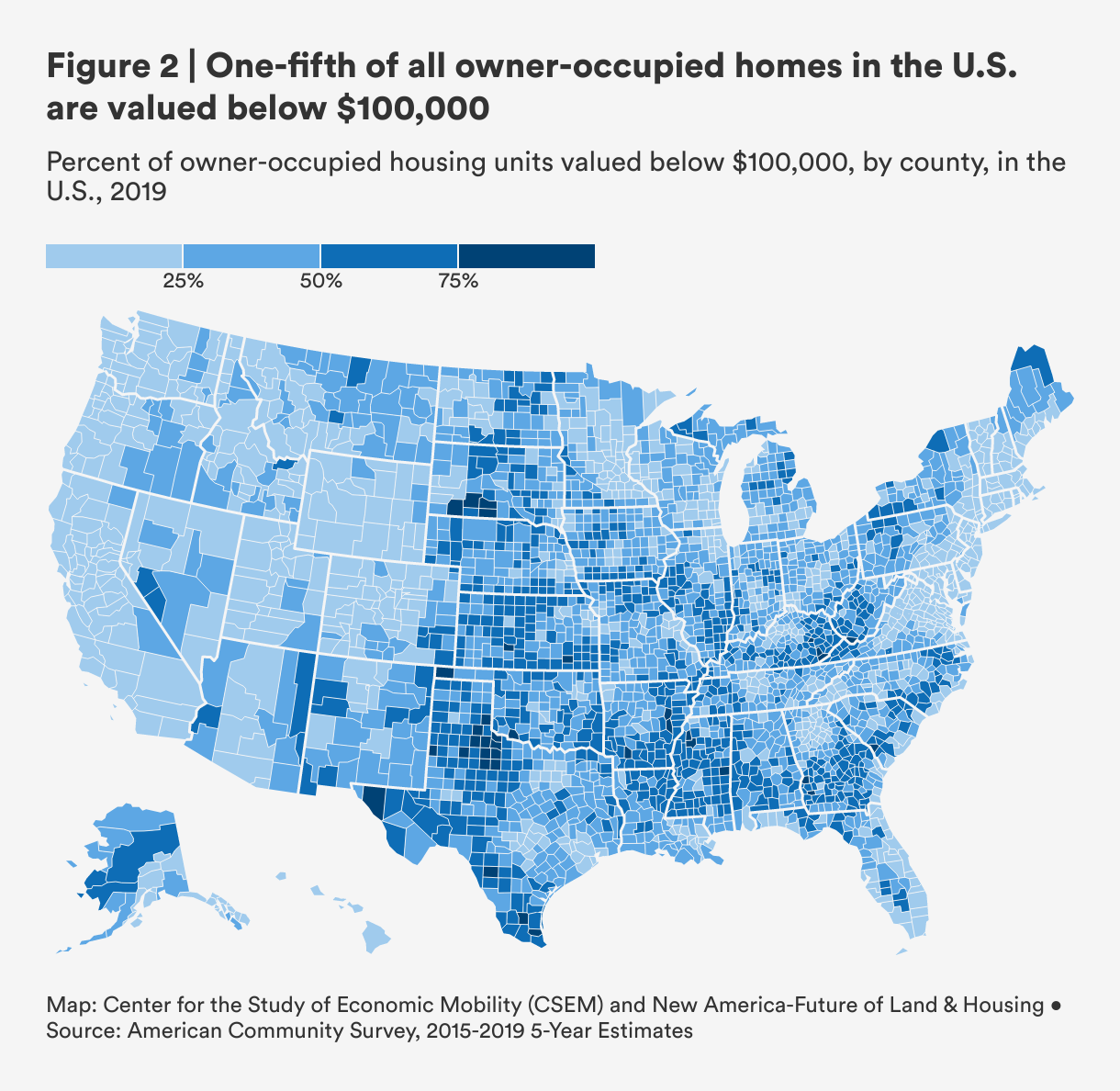

Nearly 20 percent of all owner-occupied homes are valued at $100,000 or less, according to U.S. Census data, and as shown in Figure 2, these homes are prevalent in counties all across the United States, though there are especially high concentrations of small dollar homes in the South and in the Midwest.

Access to small dollar homes is impacted by two different lending trends: first, lenders are opting out of extending small dollar loans altogether, and second, lenders are denying small dollar loans at higher rates than larger loans even when potential buyers do apply.

Despite the existence of these homes, in the decade following the 2008 financial crisis, originations for loans between $10,000 and $70,000 dropped by 38 percent, and originations for loans between $70,000 and $150,000 dropped by 26 percent. By contrast, originations for loans exceeding $150,000 rose by a staggering 65 percent. Another analysis documenting mortgage credit redistribution in the post-crisis period finds that since 2011, U.S. lenders have cut back on originating small and medium-sized loans, and that loans sized $200,000 and above have been increasing.

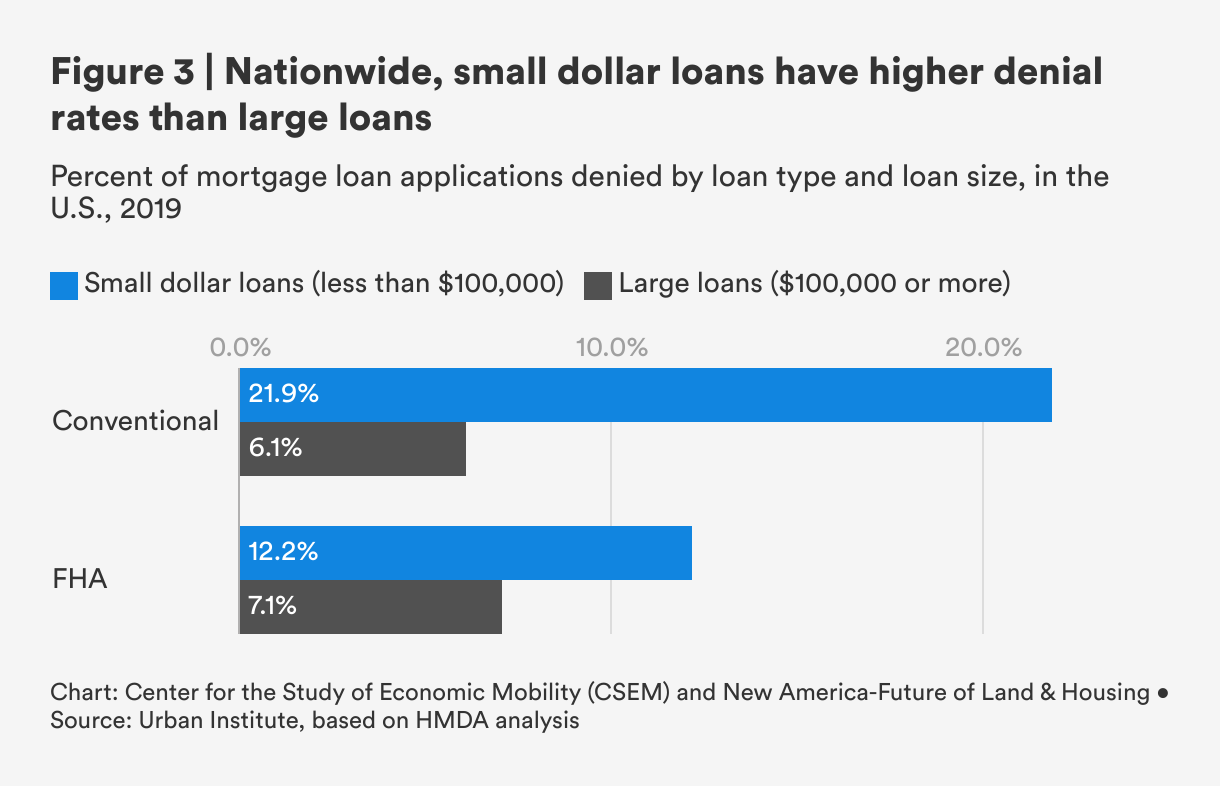

While origination for small dollar loans have been decreasing over time, denial rates for small dollar loans have consistently been high relative to large loans. As shown in Figure 3, a 2019 Urban Institute analysis finds that nationwide, denial rates for conventional small dollar loans (less than $100,000) are nearly four times as high as denial rates for conventional large loans ($100,000 or more). Denial rates for small dollar loans issued by the Federal Housing Administration (FHA)—an agency intended to serve low- to moderate-income buyers with lower credit scores and smaller down payments—were also notably higher than large FHA loans.

A deeper dive into the credit profiles of mortgage applicants debunks the myth that higher denial rates for small dollar loans are linked to the inherent risk level to lenders for extending these loans. This research, also conducted by the Urban Institute, finds that applicants of small dollar loans have similar credit profiles to applicants of larger loans, and that gaps in the denial rates persist even after accounting for applicants’ credit scores.

So what accounts for lower small dollar originations compared to large loans in the United States? Existing research ties the unavailability of small dollar loans to regulatory and structural changes in the real estate industry in the wake of the Great Recession.

Dodd-Frank regulations disincentivize small loans by lowering banks' profit relative to large loans. In the 2000s, a lack of federal oversight over the nation’s largest banks resulted in predatory lending practices that seduced many people into obtaining mortgage loans with low monthly payments. The sudden upswings in interest rates or large and unexpected balloon payments that came down the line led millions of homeowners into foreclosure as a result of the housing bubble burst beginning in 2007, leading to a near collapse of the U.S. banking system.

Soon after the financial crash, Congress implemented anti-predatory regulations in the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 (the Dodd-Frank Act). These regulations, designed to protect borrowers from this kind of predatory lending, also increased the fixed costs and the per-loan costs of extending a mortgage.

Dodd-Frank is intended to protect consumers from negligent lending practices, but some regulations have inadvertently stifled small dollar loans.

These regulations increased the fixed costs of originating a loan, regardless of the loan’s size.1 As a result, banks oriented towards originating larger loans and put less focus on small and medium-sized loans.

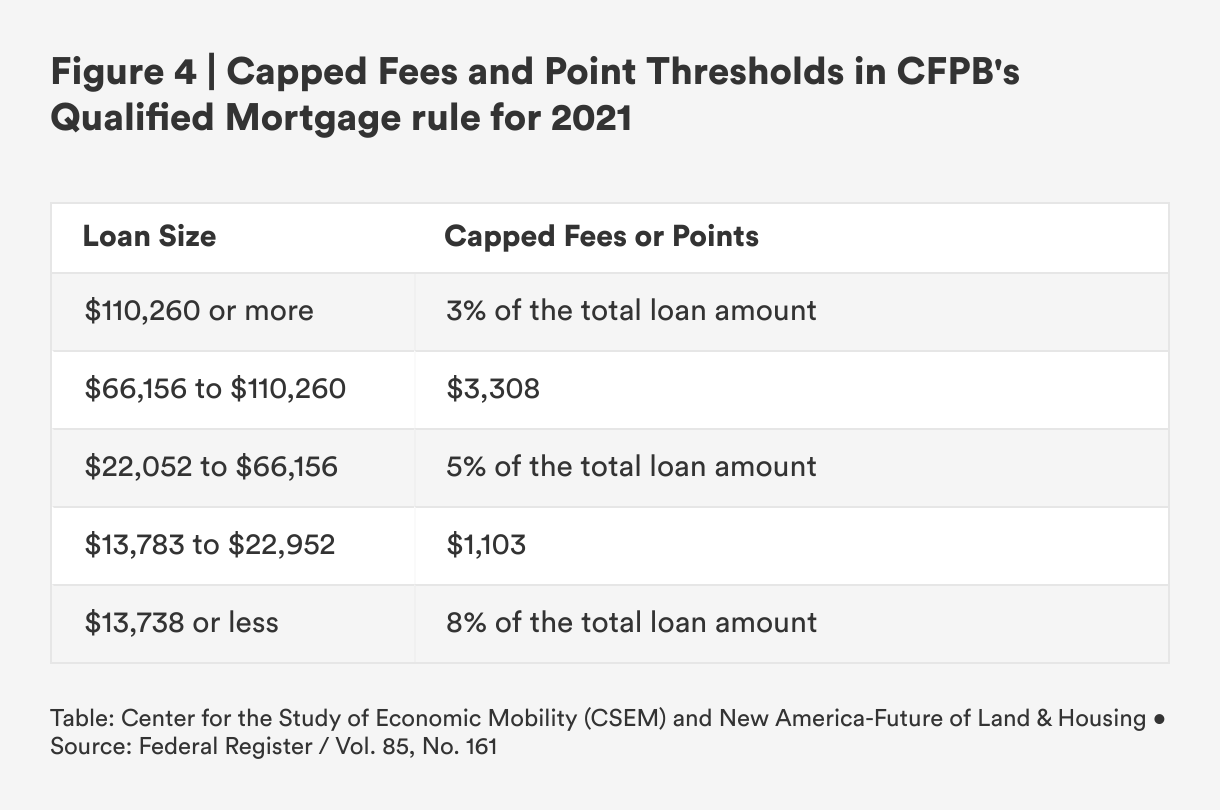

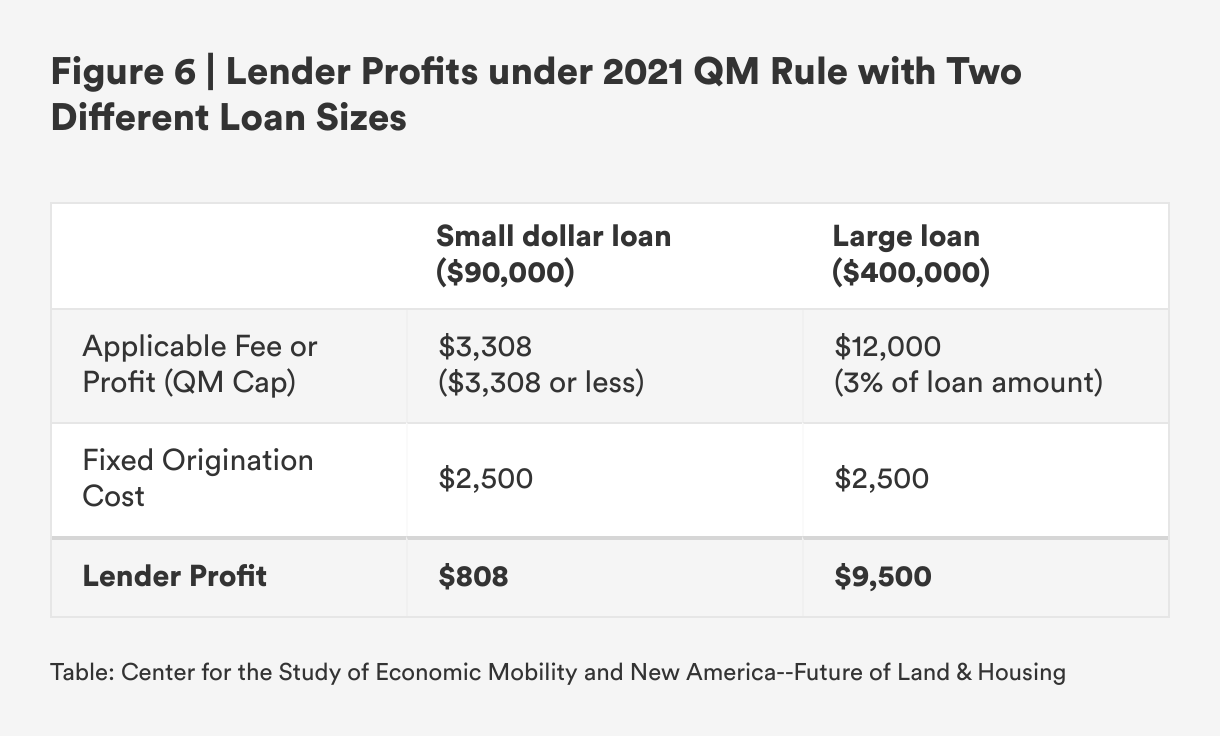

At the same time, the Qualified Mortgage rule, implemented by the Consumer Protection Financial Bureau (CFPB), capped the fees and points that lenders can charge for processing a loan on a sliding scale, based on the size of a loan (as shown in Figure 4). As a result, the smaller the loan, the less profit a bank can make, creating an additional disincentive for banks to originate small loans, even as the intent is to protect buyers from excessive fees.2

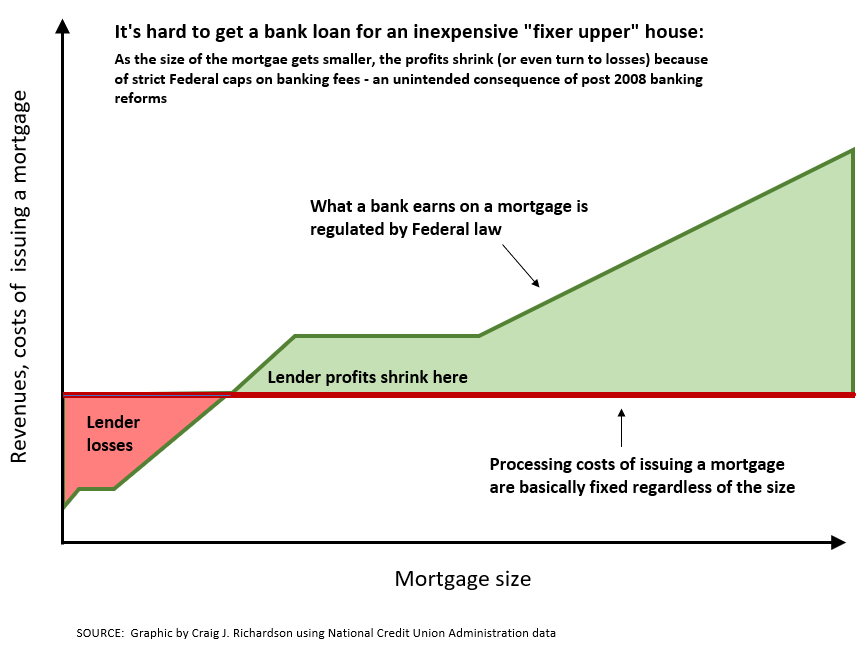

As a result of these regulations, depending upon the bank’s internal processing costs, shown by a horizontal line in Figure 5, banks could easily find it unprofitable to originate small loans. They may even refuse to write small dollar loans under a certain amount because profits shrink and can actually turn negative depending on the costs, since it takes the same amount of work to extend a loan regardless of the size.

National Credit Administration. Updated Ability-To-Repay and Qualified Mortgage Requirements from the Consumer Financial Protection Bureau(CFPB), 14-RA-09 / March 2014.

We provide a concrete example in Figure 6: Let’s say the bank faces approximately $2,500 in processing costs to originate a mortgage loan, regardless of the cost of the home. Based on Table 1 above, a lender could charge a $3,308 fee for a house costing $90,000, making a profit of $808 on that house. By contrast, a lender could charge a $12,000 fee for a $400,000 house (3 percent of the loan size per QM rules), making a profit of $9,500.

It is obvious in what direction this incentivizes the banks. While Dodd-Frank regulations were intended to protect consumers from the negligent lending practices that predated the financial crisis, they have inadvertently stifled the market for small dollar loans.

An additional impediment to lenders extending small dollar loans is the commission-based compensation structure under which lenders and many real estate agents operate. If operating under a commission-based payment structure, lenders stand to make more from larger loan amounts, further disincentivizing the desire to extend smaller loans.

The Low Supply of Housing in the United States

The United States is facing a low supply of housing decades in the making. And this lack of inventory has been most acute among starter homes, typically intended for first-time homebuyers and low- and moderate-income families. While the low supply of housing does not directly impact banks and other mortgage lenders' extension of small dollar loans, the composition and condition of the housing stock do impact the degree to which small dollar homes are accessible for mortgage financing.

This is especially true in times of unprecedented demand, like the one the U.S. housing market is currently facing. Across the country, this demand for housing is only expected to intensify in coming years, due in large part to historically low mortgage rates and the arrival of the millennial generation into their peak homebuying years.

This low supply and high demand drive up housing prices as buyers compete for available homes. This can be seen in the intense bidding wars on homes in competitive markets, where homes are selling for double their list price. It can also help explain why, according to Zillow.com, 37 percent of homes currently sell over the asking price, up from 13 percent just two years ago.

While we do not examine the lack of inventory in Forsyth County in this report, we do note that it is a large part of the problem, disrupting the traditional home purchasing process and exacerbating all other challenges homebuyers relying on small dollar loans face.

The Catch-22 of Mortgage Standards

Beyond assessing the individual finances and creditworthiness of a mortgage applicant, lenders also assess the condition of a home to protect themselves from taking on too much risk and to protect buyers from having to make repairs they cannot afford. As such, criteria on the condition of a home is a key factor in determining a home’s eligibility for financing—what some lenders refer to as “mortgage standards.”

Mortgage standards differ based on the type of loan, and loan products designed for low- and moderate-income buyers have stricter standards around the condition of the home. Loans insured by the FHA, which are intended for buyers that have been denied opportunities to build credit or save for a down payment, will not be approved by a lender unless the home meets minimum property standards for “safety, security and soundness.” Common violations include peeling paint, lead paint, openable windows without screens, a leaking roof, and damaged flooring.

As a result, these strict mortgage standards tied to FHA loans prevent these same buyers from obtaining financing on homes within their price range—often small dollar homes that are in relatively worse condition or require some degree of repair. Conventional loans, on the other hand, have much more lenient standards.

“Before you even get to the question of ‘how am I going to finance this [home]?’, you have to think, ‘can this property even be financed?’” — Forsyth County real estate agent

According to one real estate agent in Forsyth County, conventional loans are not typically concerned with the condition of a home unless it is determined to be unlivable. Discussing the differences between FHA and conventional loan standards, one real estate agent painted this picture: “Say there’s a beautiful house, and someone stole the heat pump. That is not going to stop someone with a conventional loan from buying the house, but it could with an FHA [loan].”3

These mortgage standards create a catch-22: Homes that are more likely to be affordable for low- and moderate-income buyers who are relying on FHA loan products are more likely to be older and in disrepair, and therefore less likely to meet the strict eligibility criteria of FHA loans. While the poor condition of a small dollar home alone is not necessarily causing loan denials, it is the combination of the home condition and the reliance on loan products with higher eligibility standards that creates a situation that locks many low- and moderate-income buyers out of the market. And because these buyers are often unable to obtain financing for homes within their price range, these homes instead go to buyers using cash or buyers relying on loan products with more lenient eligibility standards.

Cash (and Conventional Mortgages) are King in the U.S. Housing Market

The phrase “cash is king” refers to the considerable advantages that buyers who use cash to purchase a home bestow upon a seller, relative to buyers relying on conventional or FHA loans. Whether a cash offer is made by an investor or by a cash-flush individual who understands the inherent power of this form of payment, buyers using cash are able to streamline the transaction process and offer sellers speed and certainty—two major advantages in a transaction characterized by unpredictability.

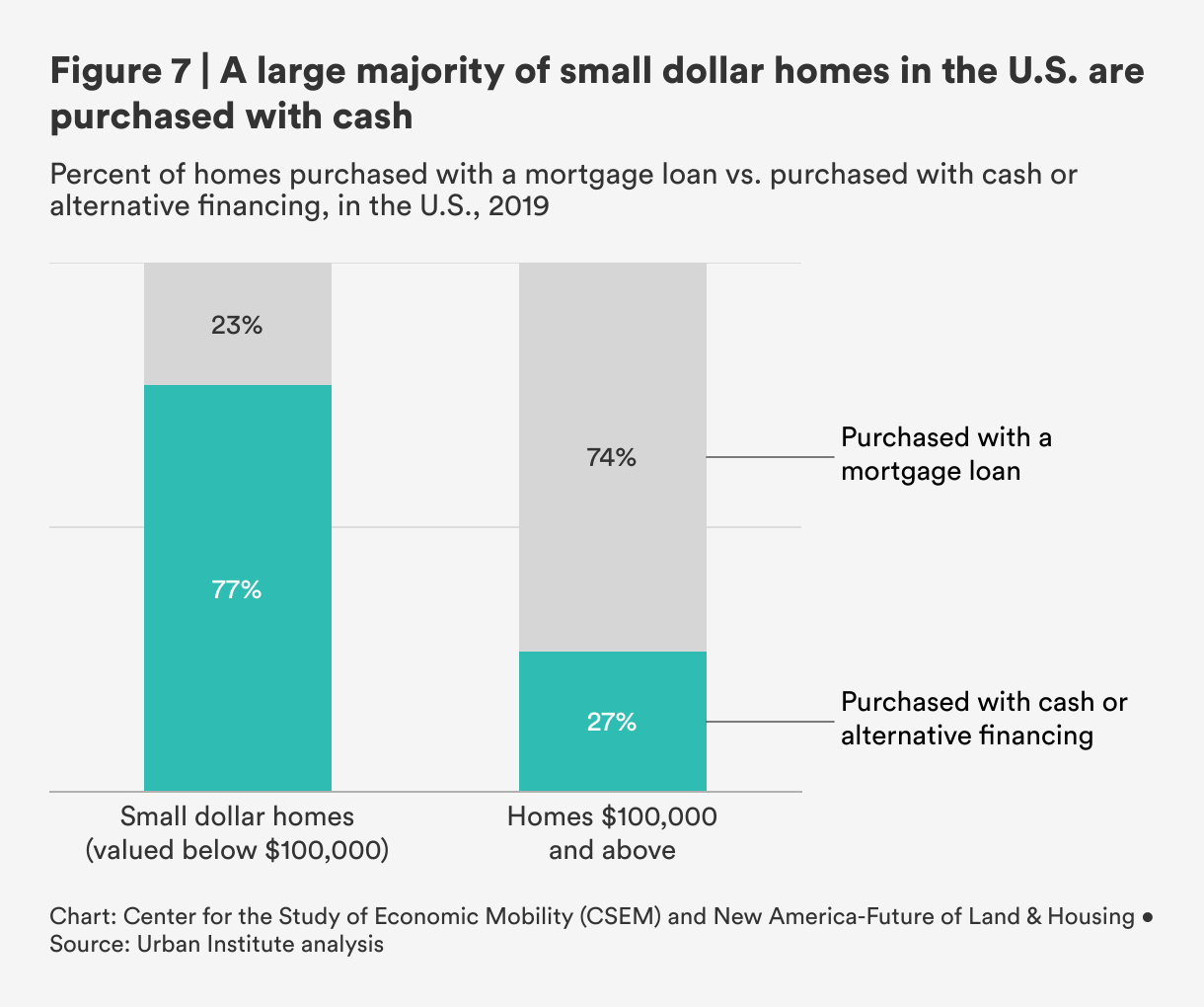

According to Zillow.com, closing time with an all-cash offer can be as little as two weeks, whereas the mortgage loan application process can take anywhere from 30 to 60 days. According to an Urban Institute analysis, cash purchases in the market for homes under $100,000 is more or less the inverse of cash purchases for homes above $100,000. As shown in Figure 7, roughly 74 percent of homes above $100,000 were financed with a mortgage in 2019, while 27 percent were purchased with cash. This was flipped in the market for small dollar homes: roughly 23 percent of single family homes below $100,000 in the United States were purchased with a mortgage loan, while roughly 77 percent were bought primarily with cash.

Why are cash purchases so much more prevalent in the market for small dollar homes? While we have not explored these causes directly, the hole left in the market opens the door for speculative non-owner occupants and other cash buyers.4 Regardless of the causes, the consequences remain the same: it is incredibly difficult for low- and moderate-income buyers, many of whom are first-time buyers in Black and Hispanic communities, to purchase and own their own homes.

FHA Loans Are Not Serving Their Intended Purpose

While the use of cash in real estate markets receives a lot of attention, the overall decline in FHA lending nationwide is also locking out many low- and moderate-income buyers. As discussed previously, FHA loans have more lenient eligibility requirements, like lower credit scores and less money required for down payments, than conventional loans and are intended for historically underserved homebuyers, many of whom are first-time buyers.

However, recent analysis shows that conventional loans are still much more prevalent than FHA loans among buyers with lower incomes. And while FHA loans decrease as income increases across both the small dollar and large loan market, this is more pronounced in the market for small dollar loans.

One reason why we may be seeing FHA lending declining nationwide is the increased federal enforcement levied against FHA lenders after the 2008 financial crisis. The Department of Justice (DOJ) during the Obama administration leveraged the False Claims Act to penalize FHA lenders for errors in their underwriting of FHA-insured loans, often bringing multi-million dollar lawsuits against FHA lenders. The lack of consistency and predictability in DOJ enforcement caused many lenders to pull back from offering FHA loans altogether.

Not only is the FHA undeserving its intended market, but FHA loans are also less competitive than cash or conventional loans with sellers choosing among several offers. The increased inspection and appraisal requirements for FHA loans, especially in competitive housing markets, can lower a buyer's odds of being chosen by a seller. In these instances, sellers are likely choosing the path of least resistance: If a home requires costly structural repairs before it can be sold to a buyer relying on an FHA loan, choosing a buyer with a conventional loan allows a seller to avoid expensive and time-consuming maintenance.

In the next section, we examine Winston-Salem, N.C. to understand the causes and consequences of a dearth of small dollar mortgages within a local housing market.

Owner-occupants Now Use Cash Too

There are a few different kinds of buyers in the market, differentiated by their method of payment and their intent once a property has been purchased. Whereas previously most buyers using cash could be considered investors, in today’s competitive market, a growing number of owner-occupants (or those purchasing homes with an intent to live in it) are using cash to win bidding wars.

Some buyers are borrowing from other assets or lines of credit instead of borrowing against the home itself. Others are utilizing companies like HomeLight Inc., Ribbon, and Opendoor Technologies Inc., that allow buyers to use cash up front while ultimately securing financing.

Even buyers using mortgage loans are increasingly leveraging the power of cash to sweeten their offers. Some buyers are including larger due diligence fees or deposits to signal their commitment to sellers, and others are waiving appraisal contingencies from their contracts with a seller, essentially ceding their right to walk away if the appraisal comes back below the sale price. This is a huge risk for buyers, as it removes a seller’s incentive to negotiate the price, meaning they would likely need to bridge the appraisal gap themselves.

Citations

- For more detail, see Regressive Mortgage Credit Redistribution in the Post-crisis Era (with A.G. Rossi), Review of Financial Studies, forthcoming, source

- Lenders can still extend non-qualified mortgages, but these have fewer legal protections and are more difficult to resell in the secondary market, which banks rely on to free up capital to make more loans.

- Recognizing the barriers that FHA mortgage standards can impose, the U.S. House of Representatives passed thesource"> Improving FHA Support for Small-Dollar Mortgages Act of 2021 in March 2021, which calls for a review of the FHA’s practices related to small dollar lending.

- We define East-Winston as a collection of 16 census tracts that are located near the city center of Winston-Salem on the east side of U.S. Route 52. More information about these tracts and our method can be found in the source">Technical Appendix.