Table of Contents

- The Lending Hole at the Bottom of the Market: Small Dollar Mortgages

- A Roadmap to this Report: Methodology, Data Sources, and Definitions

- It’s Expensive to be Poor: Small Dollar Homes are Inaccessible to Low- and Moderate-income Families

- A Microcosm of the Problem: The City of Winston-Salem, North Carolina

- Increasing Access to Small Dollar Mortgages: Potential Solutions

- Conclusion

A Microcosm of the Problem: The City of Winston-Salem, North Carolina

Winston-Salem, the county seat and largest city in Forsyth County, North Carolina, is an appealing place to live. It sits in the Central Piedmont region of North Carolina, and along with nearby Greensboro and High Point, Winston-Salem is part of the Triad, a significant regional metropolitan area.

According to a 2020 report on where Americans move, Winston-Salem ranked high among U.S. cities on inbound net migration, primarily attracting those with higher incomes and older movers relocating to less expensive housing markets where taxes are lower. At the same time, the area is one of the least economically mobile with one of the highest growths in concentrated poverty and highest eviction rates in the country.

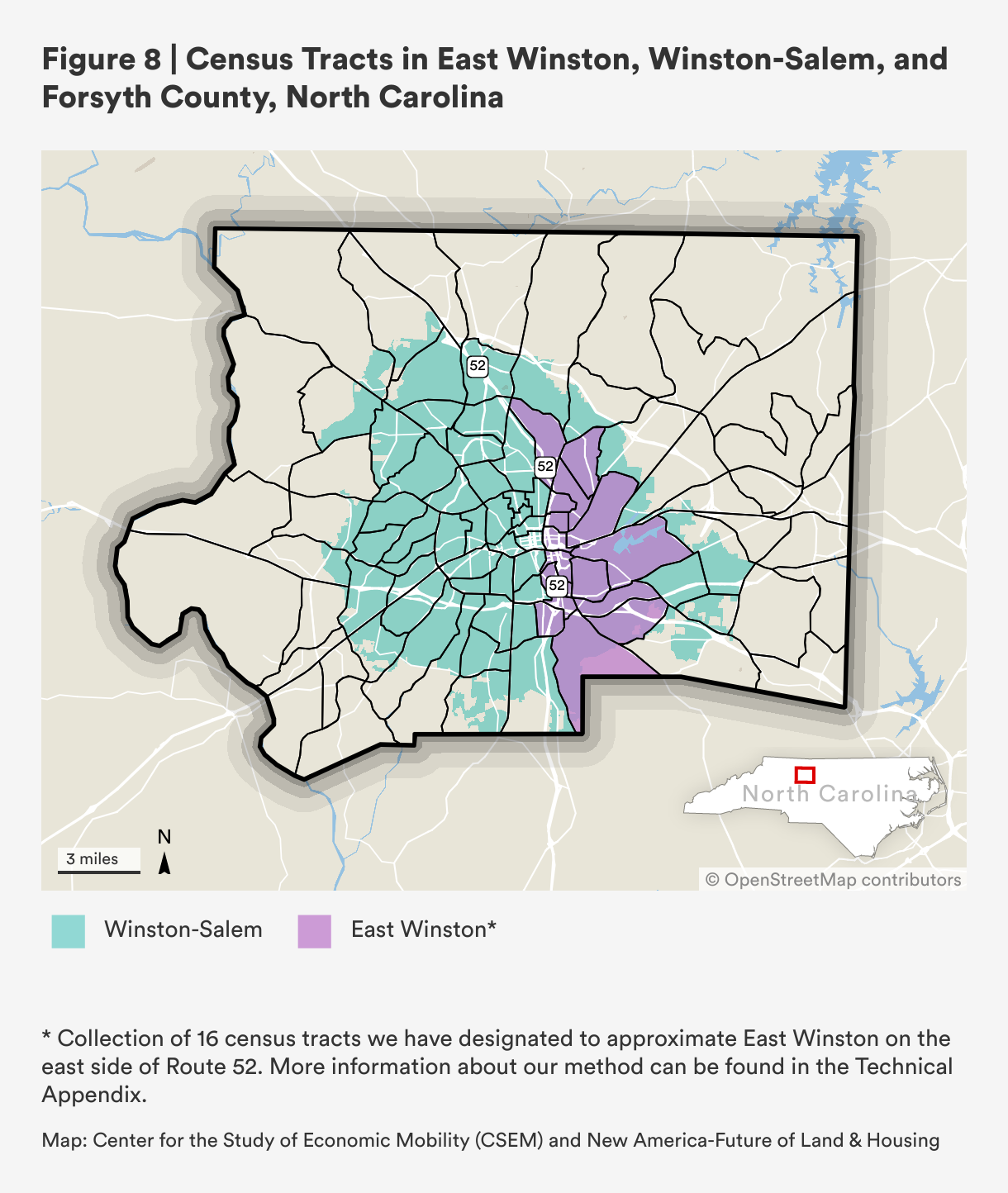

As seen in Figure 8, U.S. Route 52 runs through the City of Winston-Salem, dividing lower-income and predominantly Black and Hispanic communities in the east side from predominantly white neighborhoods in and to the west of the city center. This design was not an accident; in the early 1900s, the implementation of block-by-block segregation and racist ordinances advanced by the city’s all-white board of aldermen left Black laborers working in the city’s rapidly expanding tobacco industry little choice in where they lived.

The result was burgeoning Black communities in the east side of Winston-Salem, an area that has come to be known as East Winston. East Winston continued to expand until the 1960s, when urban renewal projects and highway construction led to the destruction of hundreds of Black homes. In 1950, the local union representing tobacco workers faced unprecedented resistance and were eventually forced to disband. When the city’s strong manufacturing presence began to dwindle in the 1980s, many workers in East Winston, reliant on the nearby factories, were left with a great deal of uncertainty. In addition, families lacking a vehicle for transportation had a difficult time accessing jobs, education, and health networks, as the city’s development sprawled outward to the suburbs on the west side of Route 52.

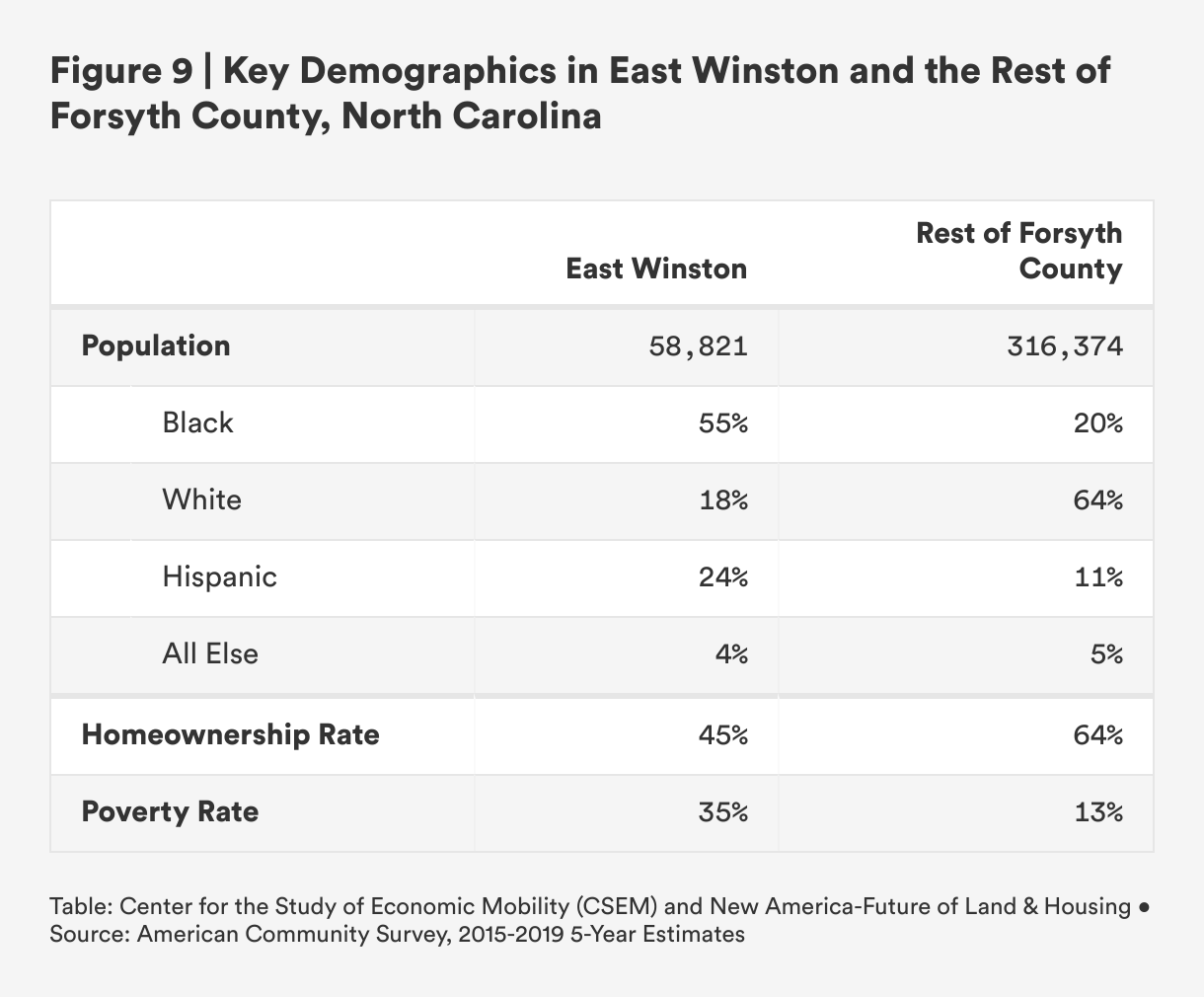

These disruptions help shed light on why homeownership and income may have remained markedly lower in East Winston than in the rest of Forsyth County. The large discrepancies between these regions, as shown in Figure 9, are in large part the result of these historical legacies.

East Winston’s Lack of Rebound After the Great Recession

During the Great Recession, and for some years afterward, East Winston was crushed by foreclosures. In 2009, the rate of foreclosures following the 2008 financial crisis in East Winston was 5.1 percent, which was nearly five times as high as the foreclosure rate in the rest of Forsyth County. By 2020, foreclosure rates in East Winston and the rest of Forsyth County dropped to under 0.3 percent, but East Winston’s foreclosure rate did not fall below 2 percent until 2015 and did not dip below 1 percent until 2017, while the rest of Forsyth County’s foreclosure rate never exceeded 2 percent, even during the height of the 2008 financial crisis.1

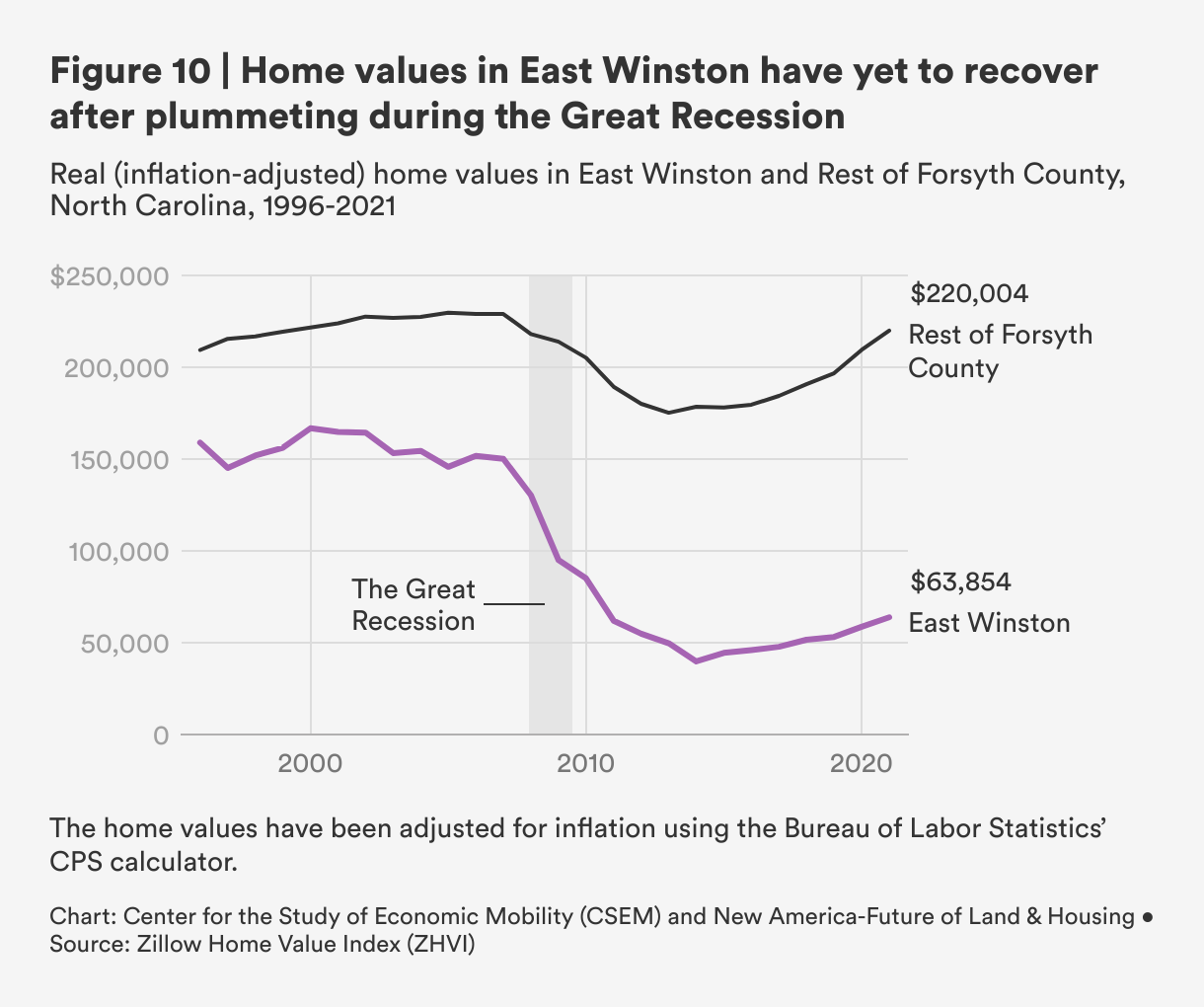

Figure 10 charts real (i.e. inflation-adjusted) home values in East Winston and the rest of Forsyth County from 1996 to 2021. Up until 2008, the value of a typical home in East Winston and the rest of Forsyth County were fairly stable, albeit values were lower in East Winston. After 2008, however, we see a distinct divergence in the two areas: the value of a typical East Winston home plummeted at a much faster rate than a typical home in the rest of the county, and has yet to recover from the 2008 collapse.

Though we see a gradual uptick in home values from 2014 until 2021 in both East Winston and the rest of Forsyth County, the value of a typical home in East Winston fell from $150,136 just before the crisis in 2007 to $39,825 at their lowest point post-crisis in 2014. By 2021, the real value of a typical home in East Winston was $63,854, down from $158,926 in 1996, meaning that over this 25 year period, the value of a typical home in these predominantly Black neighborhoods fell by nearly 60 percent.

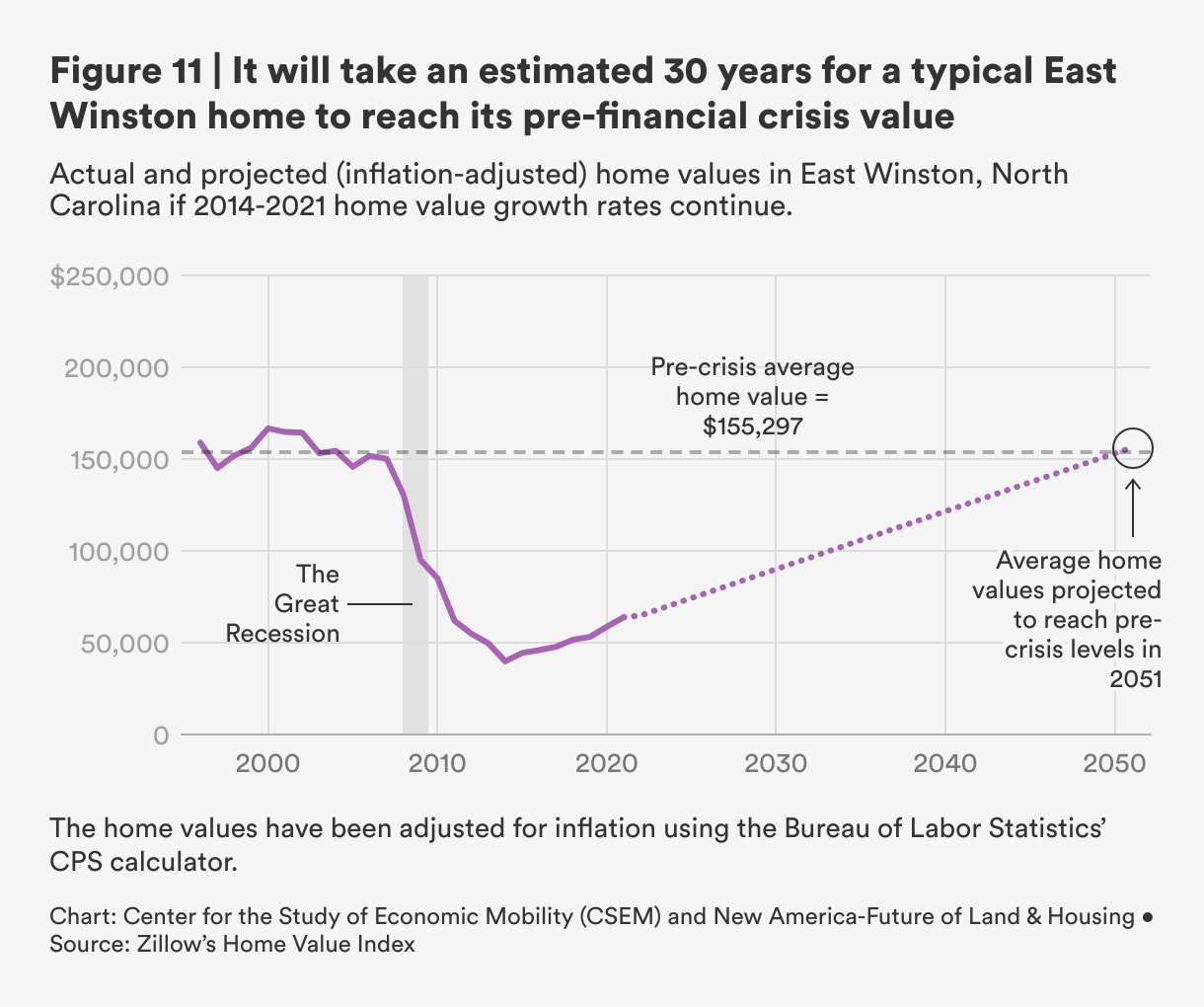

Figure 11 illustrates that, if the current trajectory of growth in home values in East Winston continues, it will take approximately 30 years for a typical home's value in East Winston to reach its pre-crisis level. We calculate that in East Winston, total real home values fell from $3.4 billion in 2007 to $1.1 billion in 2021, representing a 66 percent contraction of would-be home wealth. While today, the value of a typical home in East Winston are far from their pre-crisis levels, the value of a typical home in the rest of Forsyth County has reached and surpassed their pre-crisis levels. Instead of building long-term wealth, families who bought homes in East Winston may now owe more on their home than they will get back from selling it.

What does East Winston’s foreclosure crisis have to do with small dollar homes? The precipitous decline in home values and lack of rebound in East Winston is likely the result of the high volume of predatory loans pre-crisis resulting in a high number of foreclosures. At the same time, changes in banking regulations since 2009 may have prohibited the kind of rebound seen in other parts of Forsyth County.

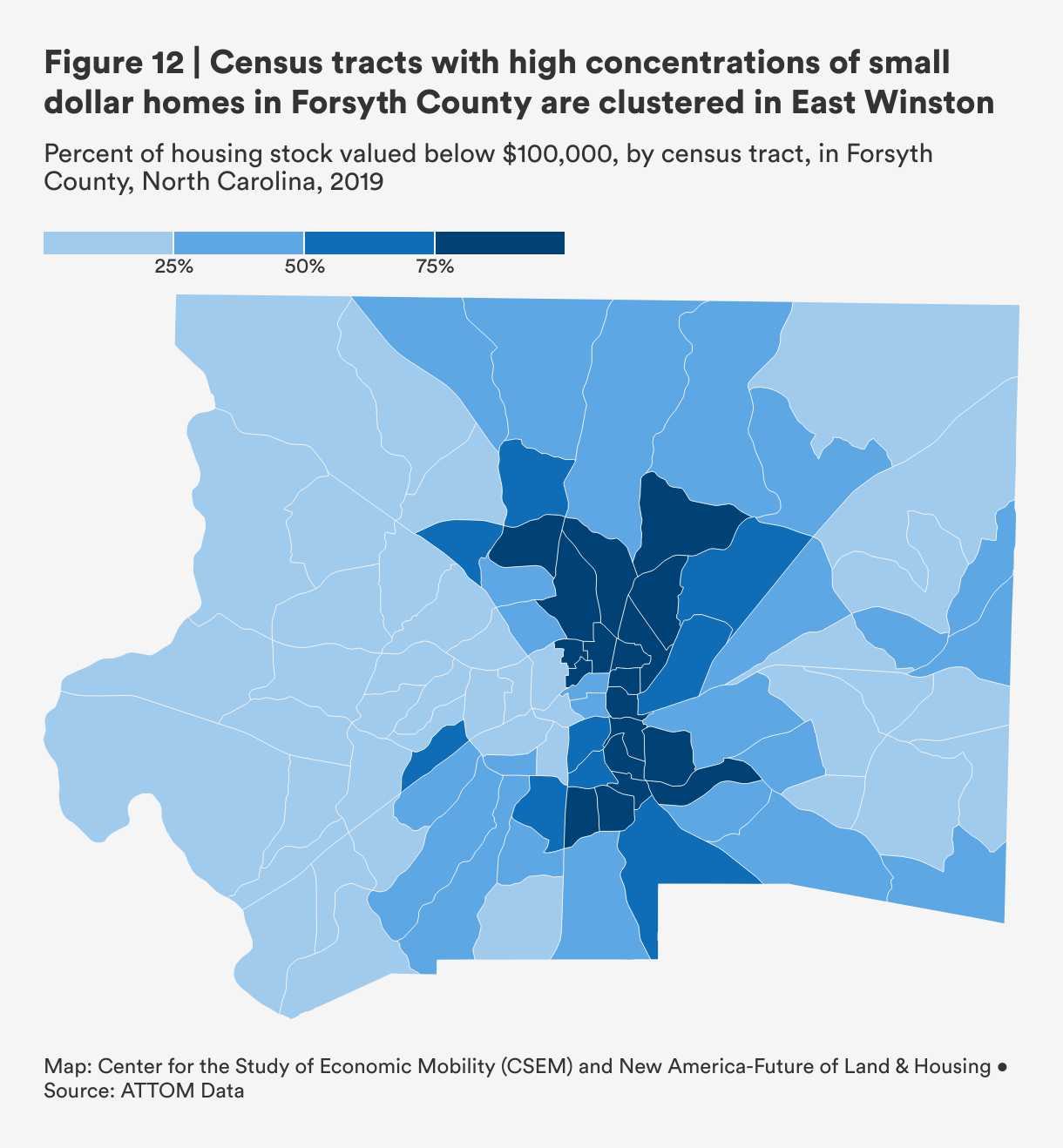

In the Figure 12, we see that neighborhoods in and around East Winston have a higher concentration of small dollar homes (below $100,000) as part of their overall housing stock than other parts of the city and county. While not visualized, this map also contains information on the share of housing stock owned by an LLC, which we use as a proxy for investor-owned properties, homeownership rate, and a host of other housing and economic indicators (by hovering over each census tract).

We can see that census tracts near the city center tend to have higher shares of investor-owned properties compared to tracts further away from the downtown area. The same holds true for East Winston, where in some tracts, a quarter of housing stock is owned by an investor. Moreover, the homeownership rates among East Winston neighborhoods are much lower than those in the rest of the county, suggesting that not only is investor activity higher in East Winston, but communities living in these neighborhoods are also less likely to own their homes.

While it is critical that communities are protected from the kind of predatory lending that led to the immediate collapse in home values in 2008, regulations keeping families from obtaining reasonable mortgage loans may be going too far in the other direction.

The Unavailability of Small Dollar Loans in Forsyth County

Roughly 34 percent of all tax-assessed homes in Forsyth County are valued at less than $100,000. Access to small dollar loans is impacted both by lenders opting out of this market, and through higher denial rates for smaller loans relative to larger loans once families do apply for financing.

Most real estate agents and lenders we interviewed acknowledged the presence of a lending floor, below which most lenders are unlikely to extend mortgages. While exact dollar amounts ranged from $45,000 to $85,000, most cited a floor of $50,000 in Forsyth County. Several lenders shared that fixed costs and maximum allowable closing costs meant that low loan amounts can quickly become expensive. One lender explained, “We stay at $50,000 or above primarily because of laws that govern fees and costs. Attorneys and appraisers also have to charge a certain amount. So when you add all this together, it exceeds what is allowed by the government.”

For lenders operating under a commission-based payment structure, individual lender profits can also be a powerful disincentive for extending smaller loans. And most lenders we spoke with in Forsyth County worked on commission, save for those whose organization’s mission included working with low- and moderate-income buyers, in which case, they earned both a salary and a commission.

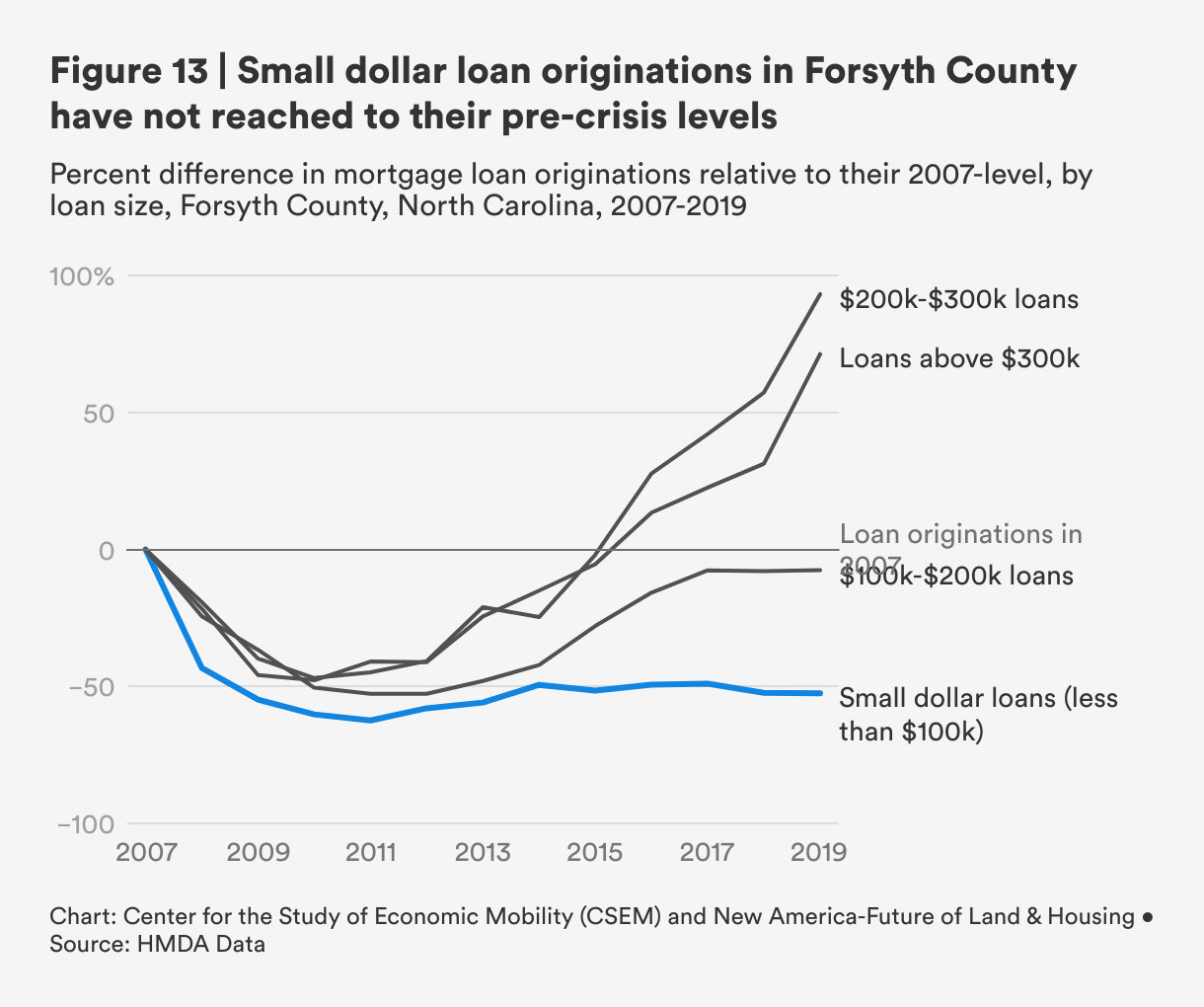

The presence of lending floors and other disincentives likely result in the lower originations we see of small dollar loans in Forsyth County. Figure 13 shows the percent difference in originations for mortgage loans of differing amounts relative to their pre-crisis level in 2007 in Forsyth County. By 2019, loan originations for small dollar loans (those less than $100,000) and for loans between $100,000 and $200,000 were 52.5 percent and 7.5 percent below their 2007-level, respectively. While originations for loans above $200,000 have recovered to their pre-crisis levels, small dollar loans have yet to see the same kind of rebound after the Great Recession.

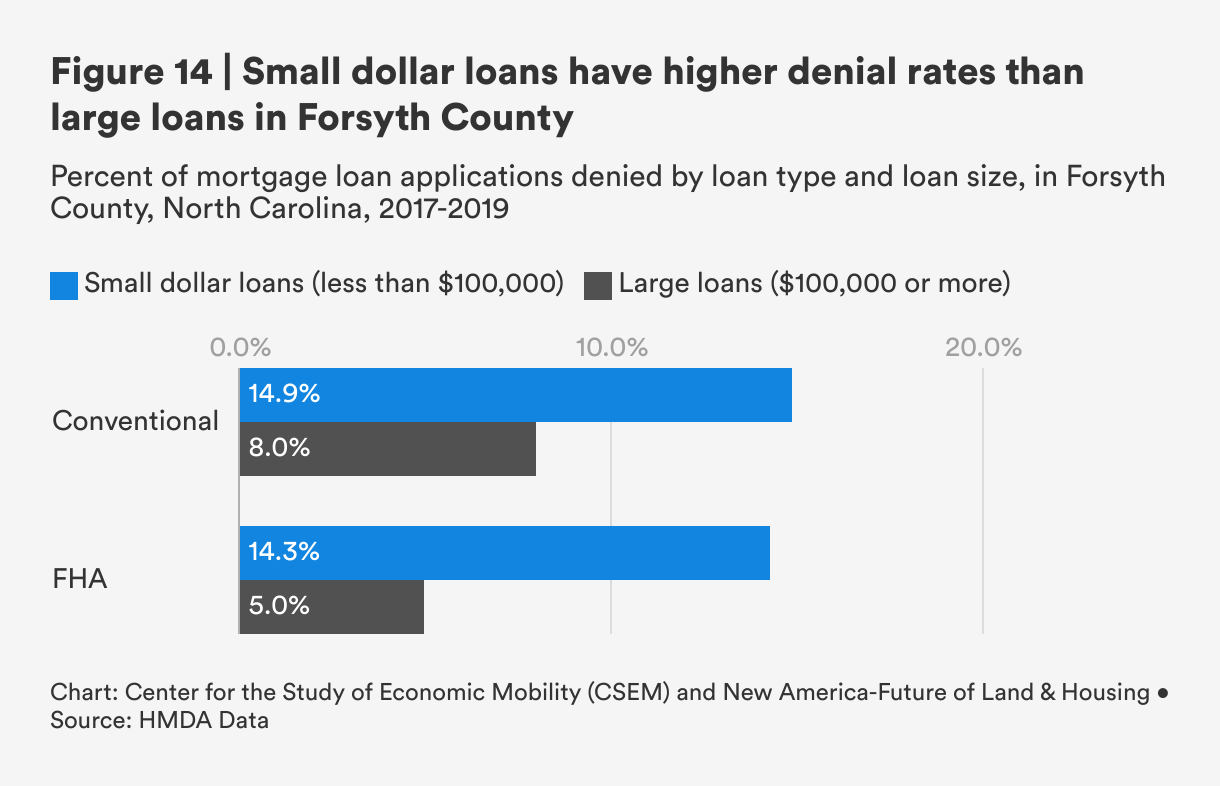

At the same time, small dollar loans are also being denied at higher rates in Forsyth County. Using pre-COVID data from 2017 to 2019, Figure 14 shows that small dollar loans are denied at nearly two and three times the rate of large loans, across conventional and FHA markets in Forsyth County, respectively. The combination of lower levels of small dollar originations and higher denial rates results in increasingly less mortgage financing for homes under $100,000.

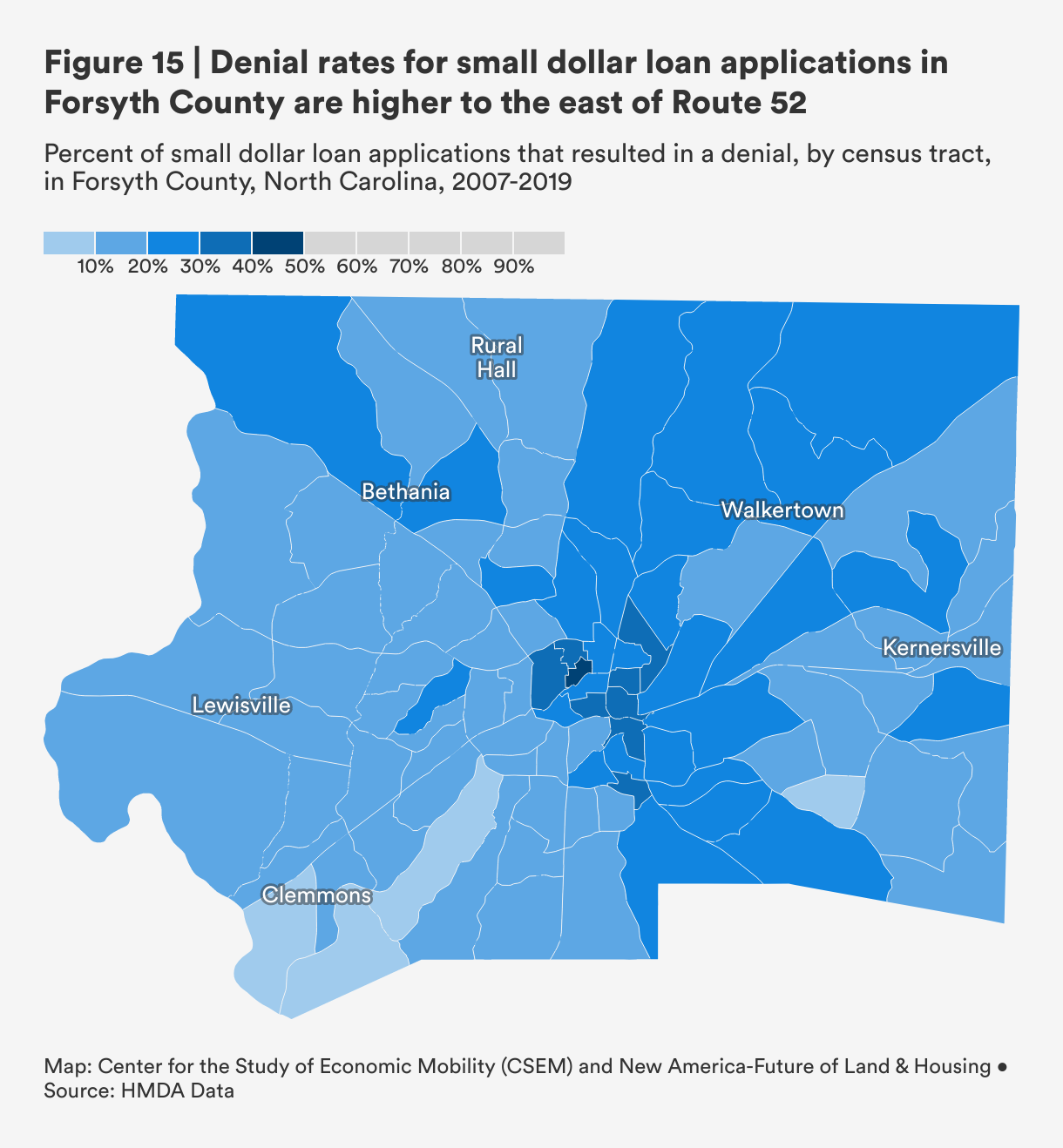

To understand any spatial patterns in denial rates, we mapped small dollar denial rates at the census tract level in Forsyth County, using data from 2007 through 2019. Figure 15 shows that neighborhoods near the city center and in East Winston tend to experience higher small dollar loan denial rates than the rest of the county. While the average small dollar denial rate in Forsyth County across all loan markets from 2007 to 2019 is around 20 percent, some census tracts, notably those in and around East Winston, have denial rates ranging from 30 to 40 percent.

In Forsyth County, small dollar originations are low relative to originations of larger loans and small dollar denial rates are high relative to large loans. Further, we see that neighborhoods in and around East Winston have both a higher concentration of small dollar housing stock (see Figure 12) and higher small dollar denial rates (Figure 15 above). It's not surprising that we also observe that these areas also have higher shares of investor-owned housing stock and lower homeownership rates in these neighborhoods as well.

While it is critical that communities are protected from the kind of predatory lending that led to the immediate collapse in home values in 2008, regulations keeping families from obtaining reasonable mortgage loans may be going too far in the other direction.

Small Dollar Loan Applicants: "High Touch, High Need"

Several Forsyth County lenders discussed how processing loans for low- to moderate-income applicants often requires high-touch, high-need engagement. Relative to higher-income applicants, lenders and real estate agents reflected on how low- and moderate-income applicants are more likely to experience changes in employment or financial circumstances. And these shocks, even if slight, could jeopardize the likelihood of an application ending in origination, as any financial change in an applicant’s life, whether to employment status or student loan payments, impacts an applicant’s debt-to-income ratio.

One local lender who focuses exclusively on low- and moderate-income buyers explained that many of these applicants are purchasing homes at the maximum amount they qualify for; if they go any lower, the available housing stock shrinks to the point where finding viable housing in good condition may become impossible. As a result, their debt-to-income ratios are already near or at the maximum permitted level by the lender, and “little things like [changes to the taxes or homeowner’s insurance] can be hard stops” for an already-sensitive loan application.

The possibility that a buyer’s financial circumstances could forestall closing could also contribute to some agents and lenders' hesitancy to work with low- and moderate-income buyers. According to one Forsyth County real estate broker, “[Agents] get discouraged [from selling homes under $100,000] because the lower income borrowers are more difficult to close. They have more nuances in their finances because they are more reliant on credit in their day to day lives.”

Mortgage Standards for Local Homeownership Assistance Programs in Forsyth County

Similar to the misalignment between FHA standards and small dollar homes discussed in the previous section, agents and lenders expressed concern over the misalignment between the existing housing stock in Forsyth County and the eligibility criteria for state, county, and city homeownership assistance programs.

The state, county and city governments in North Carolina, Forsyth County and Winston-Salem offer homeownership assistance with differing eligibility criteria and levels of assistance. These programs can be layered on top of each other and paired with FHA or conventional loan products to make financing more viable for low- and moderate-income buyers. Agents, lenders and housing leaders all noted that the need for repairs on small dollar homes and homes that are more likely to be affordable for low- to moderate-income buyers disincentivizes sellers from accepting buyers relying on FHA loans or local down payment assistance programs, pushing them towards conventional loans or cash offers instead.

The Affordable Homeownership Opportunity Program (AHOP) and the North Carolina Housing Financing Agency (NCHFA) Community Partners Loan Pool (CPLP) both offer down payment and closing cost assistance for low- and moderate-income Forsyth County residents. These programs offer generous funding, with maximum loan amounts often qualifying eligible buyers for homes up to $200,000. However, these programs also include rigorous home inspections, requiring that every item detailed in an inspection report be addressed by the seller before closing.

Some affordable home ownership programs have a recommended 10 year age cutoff to ensure a home is in good condition, but only 7.3 percent of homes in Forsyth County were built after 2010.

To increase the likelihood that homes pass inspection, CPLP recommends that a home must either be newly-constructed or in like new condition, using a 10 year age cutoff as guidance. According to 2019 Census data, only 7.3 percent of homes in Forsyth County were built after 2010. In effect, this eligibility criteria further constrains the supply of homes that buyers using local affordable homeownership programs can purchase. Many developers and housing leaders we spoke with also noted that new construction in Forsyth County is unlikely to be affordable for low- and moderate-income families, suggesting that existing housing stock is currently the only viable option for homeownership.

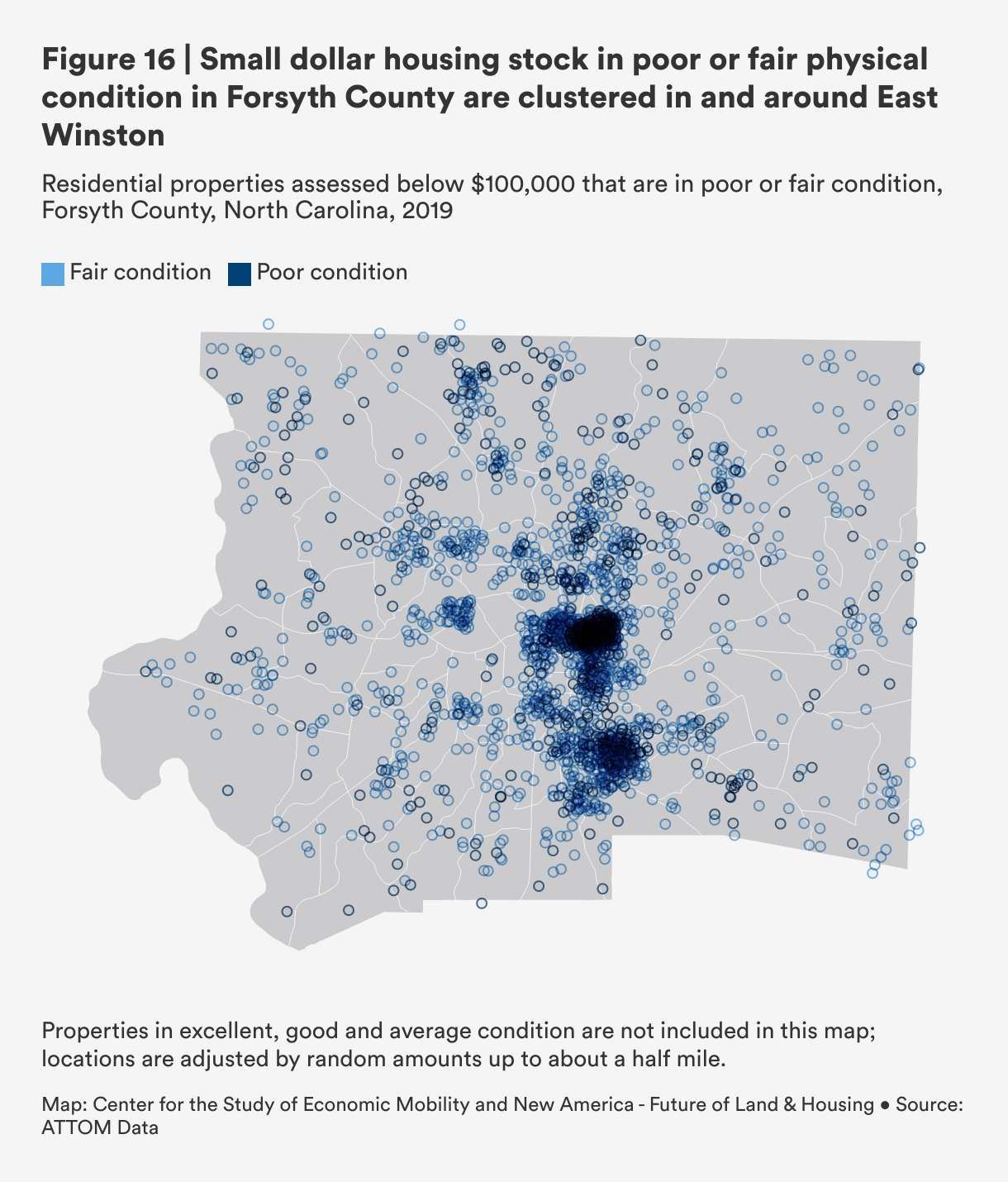

To better understand how small dollar housing stock in relatively worse off condition is concentrated, we map small dollar homes assessed as having below-average (either fair or poor) physical condition in Forsyth County, using 2019 data.2 Figure 16 shows that Forsyth’s stock of small dollar homes that are assessed as having below average condition are most frequently found in and around East Winston.

Agents, lenders, and housing leaders all emphasized that most homes that are affordable for low- and moderate-income residents are typically not move-in-ready, and generally require some level of repairs, anything from minor fixes to major structural rehabilitation. Of these homes, interviewees emphasized that homes under $100,000 are in the worst condition. A Winston-Salem realtor who works with bank-owned properties noted, “If a house is sitting on the market, and it’s coming in at $80,000, and that’s what it’s worth, you’ll typically have $25,000 to $30,000 worth of repairs.”

These local mortgage standards—designed to protect both the lender and the buyer—are instead disincentivizing sellers from selecting buyers relying on local loan products and assistance programs. Describing how Forsyth County’s highly competitive housing market intensifies this dynamic, one agent added, “This is an especially important problem in this market, because sellers can always find another buyer.”

Cash (and Conventional Loans) are King in Forsyth County

Intense competition over homes in Forsyth County equates to what is known as a seller's market, in which sellers have the power to select the offer on their home that best fits their needs. For most sellers, this means balancing the bid price with an offer that allows them to close quickly with as much certainty as possible.

Real estate agents, mortgage lenders, and housing leaders we spoke with in Forsyth County emphasized that the lack of affordable housing in decent condition is one of the biggest barriers low- and moderate-income buyers face. While the supply of homes in good condition is more constrained at the bottom of the market—acutely so for homes below $100,000, they said—the lack of housing impacts buyers with budgets up to $200,000.

“Most sellers are looking for the best offer with the least amount of work.” — Forsyth County real estate agent

Several agents discussed how a seller’s market was evident in the intensity of the bidding wars in Forsyth County, notably on affordable homes in good condition. One agent shared that one home selling for $150,000 received 65 offers. While the number of offers typically decreases as the cost increases, agents noted that more expensive homes, $300,000 and above range, could still expect to choose among several offers, even if not quite as many as on small dollar homes.

Cash vs. Mortgage Transactions in Forsyth County

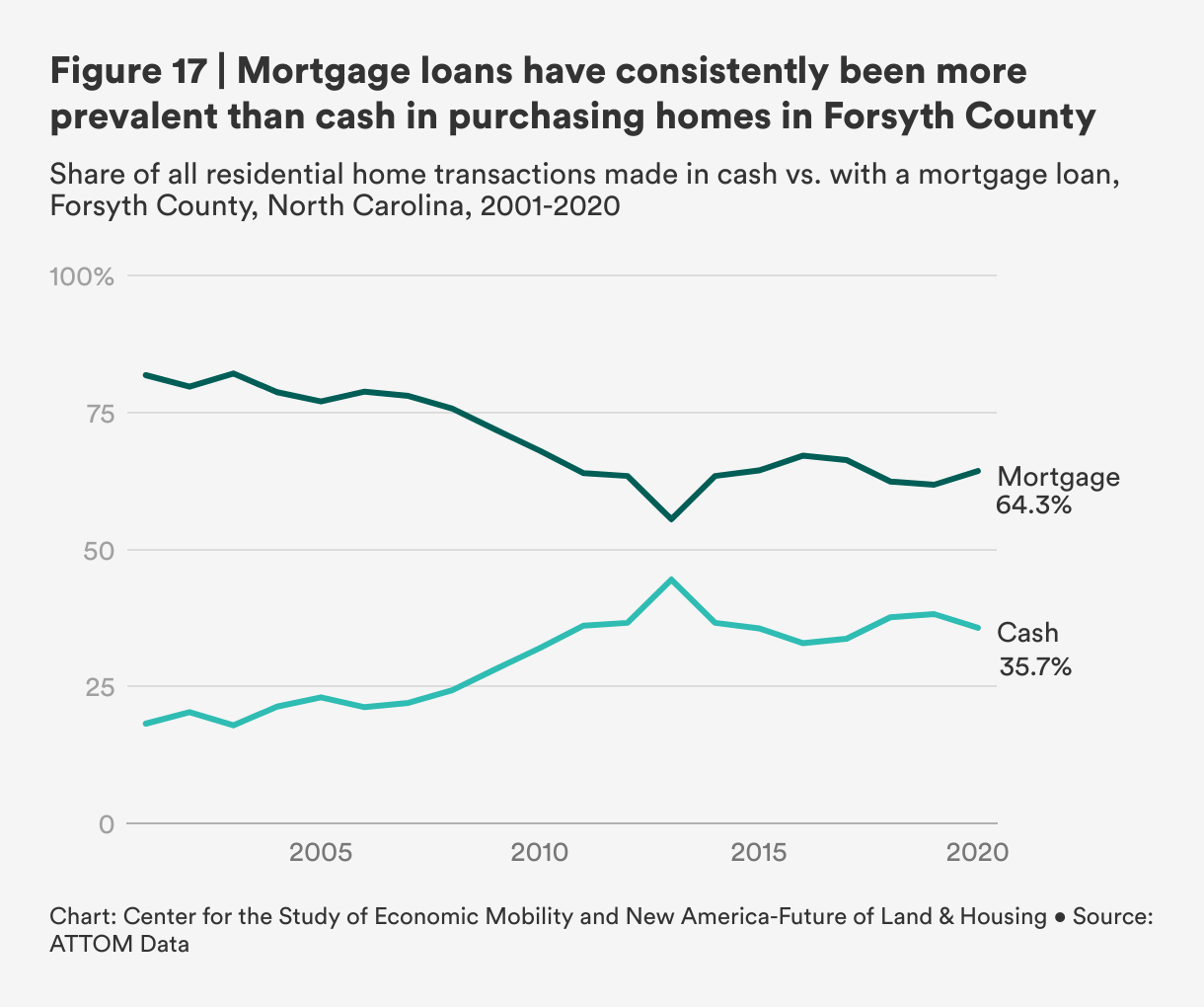

As discussed in the previous section, homes purchased with cash allow for the fastest and surest pathway from contract to close, and homes purchased with conventional loans tend to close more quickly than buyers relying on FHA loans. To understand trends in payment methods used in Forsyth County, we explore the share of residential home purchases made with cash versus with a mortgage over a 20 year time period in Figures 17 and 18 below. The share of homes purchased with cash is the inverse of the share of homes purchased with a mortgage (see the technical appendix for more details).

Figure 17 plots all residential homes purchased in Forsyth County from 2001 to 2020, by method of payment: cash or a mortgage loan. Over this time period, homes purchased with mortgage loans has decreased slightly and the use of cash has increased slightly, but at no point in the last 20 years have more homes been purchased with cash than with a mortgage in Forsyth County. In 2020, cash purchases accounted for 35.7 percent of all transactions, while the use of mortgage loans accounted for 64.3 percent.

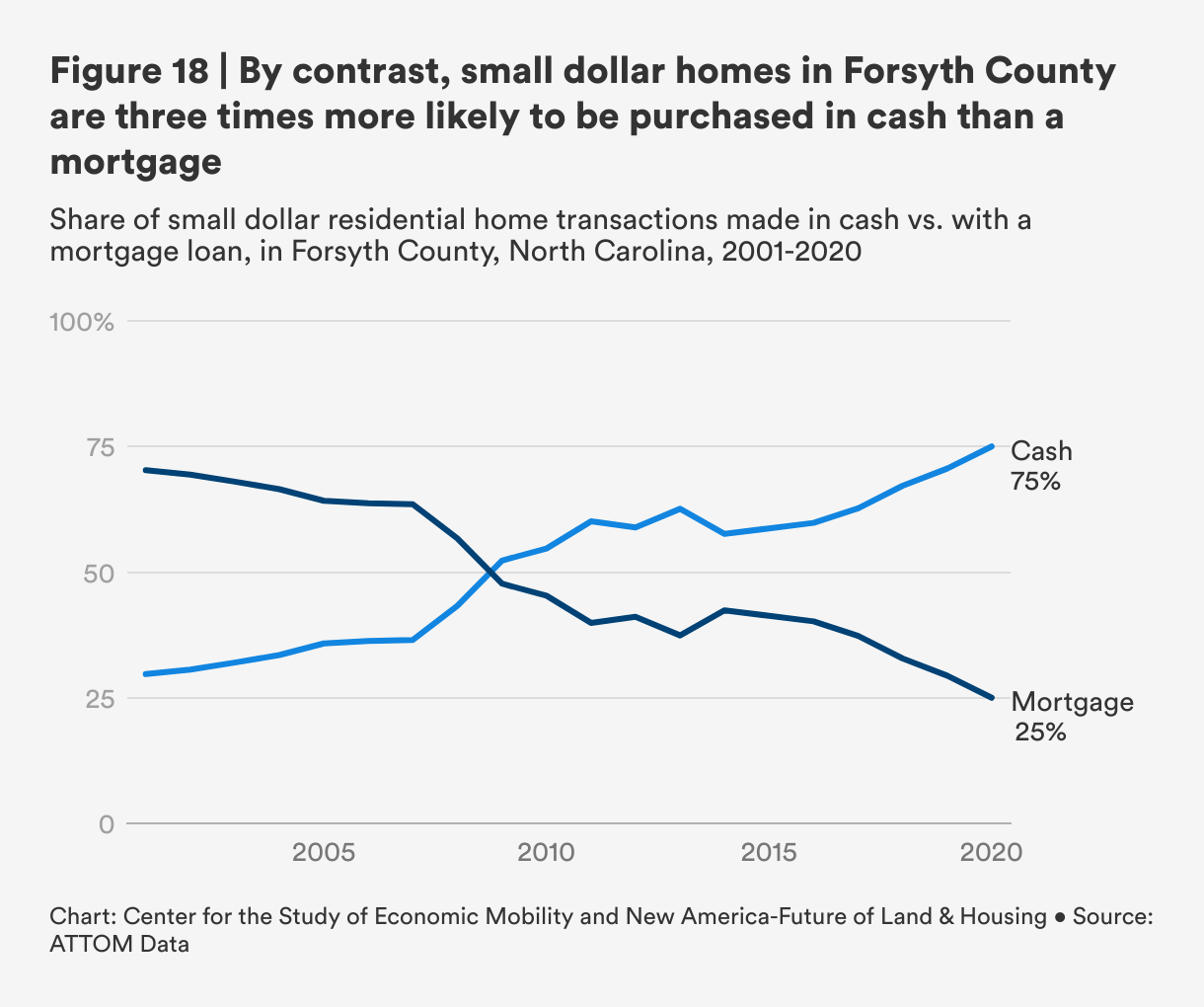

This payment story looks different among small dollar homes, however. Figure 18—which plots the same information as Figure 17, but only among homes below $100,000—shows that in 2001, only 30 percent of small dollar homes were purchased in cash, but the use of cash to purchase small dollar homes has steadily increased over the last two decades. Between 2008 and 2009, the share of homes purchased in cash overtook the share of homes purchased with a mortgage, and after steep increases between 2014 and 2020, cash purchases now account for 75 percent of the small dollar home market.

Seventy-five percent of small dollar homes in Forsyth County are now purchased with cash, up from 30 percent in 2001.

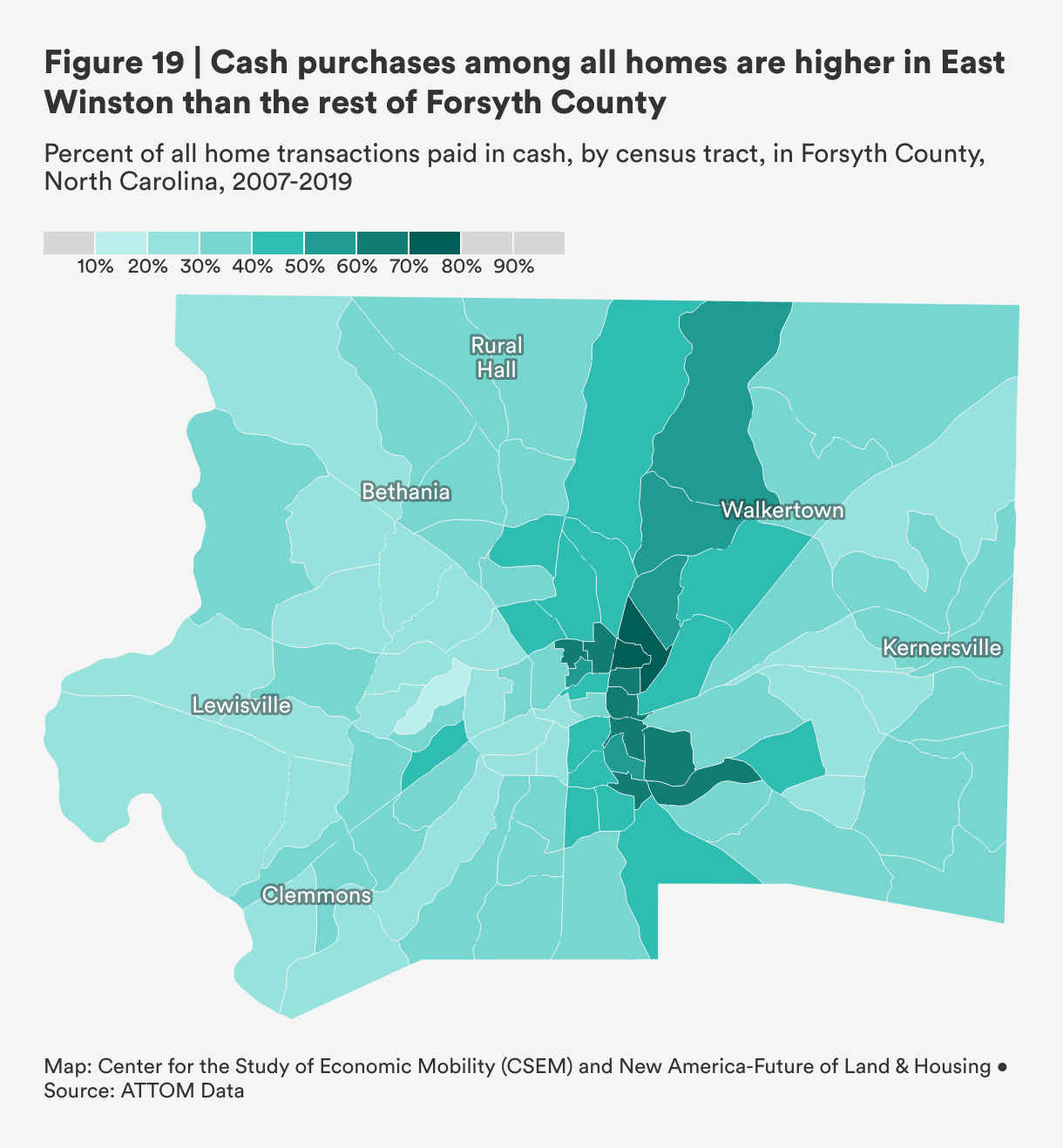

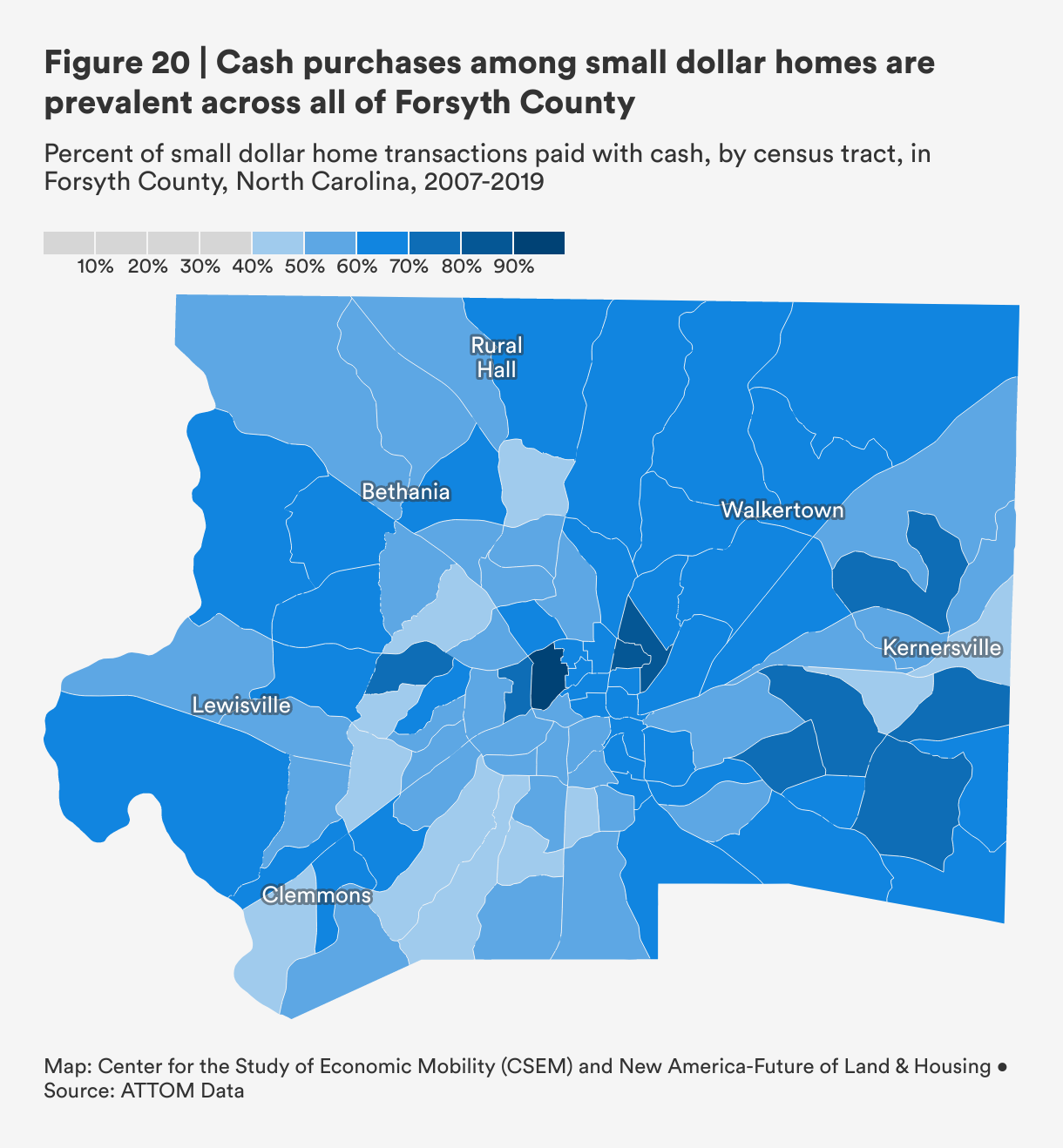

To understand where cash purchases are most prevalent in Forsyth County, we use data from 2007 through 2019 to visualize the distribution of all cash transactions at the census tract level (Figure 19) and the distribution of small dollar cash transactions (Figure 20). Among all transactions, we see that census tracts in East Winston, and tracts located along the eastern corridor of Route 52, have the highest share of cash payments. Indeed, real estate agents and lenders we interviewed suggested that cash purchases in Forsyth County, notably in recent years, were becoming common among homes well beyond those costing $100,000.

By contrast, Figure 20, which shows the distribution of cash purchases only among small dollar homes, we see that census tracts near the city center and on the east side of Forsyth tend to have higher concentrations of small dollar cash purchases, though cash transactions for small dollar homes appear to be prevalent all across Forsyth County.

Conventional and FHA Small Dollar Loans in Forsyth County

After buyers with all-cash offers, sellers tend to favor offers that rely on conventional loans before FHA loans. We explore why this may be in subsequent sections, but explore the trends in these loan markets first.

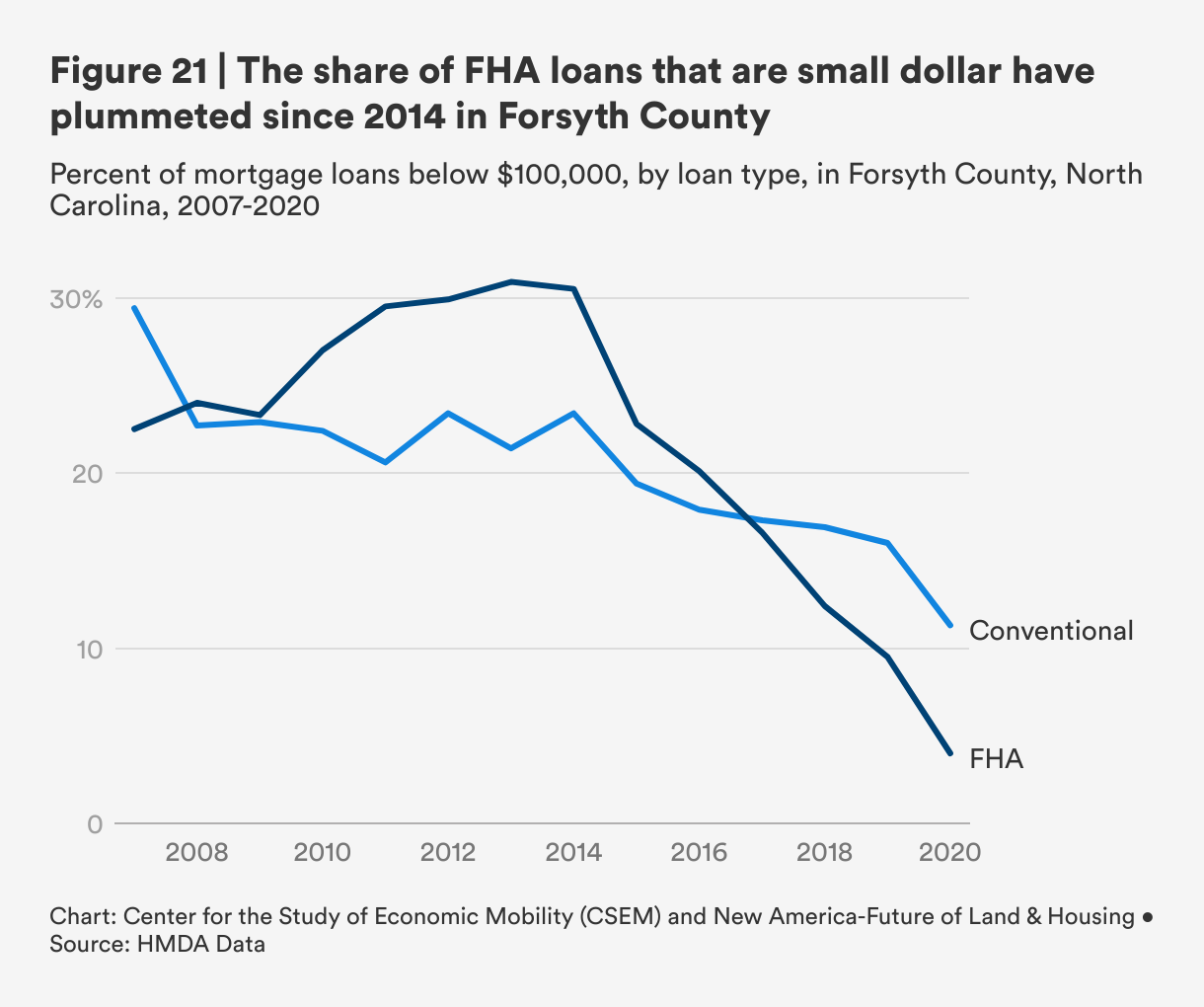

Figure 21 plots the share of FHA and conventional loans that are below $100,000 from 2007 to 2020. Since 2014, the share of FHA loans and conventional loans has declined, albeit at different rates. Indeed, the share of small dollar mortgages secured with an FHA loan has plummeted since 2014. At their peak in 2013, 31 percent of all FHA loans in Forsyth were below $100,000; by 2020, this had dropped to around 4 percent.3 The rapid decline in FHA lending may be related to reliance on the False Claims Act, which sowed a level of uncertainty among FHA lenders (discussed in the previous section).

Describing changes to the FHA market, one Forsyth County real estate agent noted: “We call them the big box banks—SunTrust, Wells Fargo, Bank of America, Capital One, First Capital, First Citizens. All of those sorts of banks abandoned the FHA loan product [a number of years ago] because of the tightened regulations. Some of them have come back with altered products, but the FHA loan product… was pretty essential to the lower-income borrowers. A lot of banks just jumped ship.”

This rapid decline in small dollar FHA loans is particularly troubling given that these loans are explicitly designed to increase homeownership for first-time homebuyers, racial minorities who have faced discrimination, and low- to moderate-income buyers. Though the FHA is supposed to be a key lending channel for these groups, data shows that it underserves borrowers with small dollar loans. In addition to decreased FHA lending, in competitive markets where sellers have multiple bids, they may be increasingly disinterested in opting for buyers relying on FHA loans, which come with more requirements and take longer to close.

The Speed of Closing in Forsyth County: Home Purchases with a Mortgage Loan

Agents, lenders, and housing leaders we spoke with in Forsyth County estimated that the timeline from contract to close for purchasing a home could range anywhere from 30 days to four months. While the process for a buyer relying on a mortgage loan involves more steps than the process for a buyer using cash, the timeline is dependent on several additional factors, all of which can impact sellers’ decision-making. And given the competition among buyers for small dollar homes in Forsyth County, any extension to the timeline can hinder the strength of a buyer’s offer.

“It’s not just about whether [the timeline] works for my buyer. If you throw that to a seller, will they wait four months or will they reduce the price and sell to someone else?” – Forsyth County real estate agent

The main factors that agents and lenders discussed were: the type of loan, the type of lender, layering a mortgage loan with local homeownership assistance, and the condition of the home.

- The type of loan. Given the mortgage standards on FHA loans and stricter requirements for appraisals and home inspections, conventional loans were recognized as having faster turnaround times, typically around 30 to 45 days while FHA loans take closer to 45 to 60 days.

- The type of lender. All mortgage loans, regardless of whether they are conventional or FHA loans, are issued by approved lenders at banks, credit unions, mortgage companies or other financial institutions. While agents and lenders we spoke with noted that credit unions in Forsyth County offer flexible terms and alternate financing options, some also noted that they typically move slower than loans issued through banks or mortgage companies.

- Layering a mortgage loan with local homeownership assistance. As discussed earlier, the state, county, and city governments in North Carolina, Forsyth County, and the City of Winston-Salem offer homeownership assistance with differing eligibility criteria and levels of assistance. These programs can be layered on top of each other and paired with FHA or conventional loan products to make financing more viable for low- and moderate-income buyers. According to Forsyth County agents and lenders, utilizing these programs, and coordinating among the various departments that administer them, can extend the timeline substantially, taking anywhere from two to four months.

- Condition of the home. The condition of the home is the biggest factor for a delayed timeline. We explore this further in the next section.

Streamlining the Homebuying Process: Foregoing Inspections and Appraisals

Homes that are affordable for low- and moderate-income residents in Forsyth County are typically older, in worse condition, and have more structural or foundational issues than more expensive homes. If buyers are also relying on FHA loans or local homeownership assistance programs that have stricter standards for the condition of a home, this can cause significant delays in the loan approval process, notably during appraisals and inspections.

Forsyth County’s first-time homebuyer program, AHOP, requires that homes are inspected by a licensed home inspector, and any repairs needed must be performed by the seller before closing. After the required home inspection, buyers may have to bring in third-party specialists to assess any structural issues that came up, prolonging the timeline. Appraisals can also inject a great deal of uncertainty into a mortgage loan approval process as failure to appraise for the selling price can be grounds for a lender to deny a loan.

Cash buyers, on the other hand, face no requirements around home inspections or appraisals. Even when a cash buyer opts to commission a home inspection or appraisal, the ability of the transaction to move forward does not necessarily hinge on what is returned in an inspection or appraisal report as it would for a buyer relying on a mortgage loan, especially an FHA loan or a loan layered with a local affordable homeownership program.

Differing Home Preferences for Investors vs. Owner-occupants

Purchasing a home is an economic investment for any buyer, regardless of whether they use cash or a mortgage loan. However, Forsyth County interviewees did discuss some key differences in the criteria for choosing a home among owner-occupants and investors. For many owner-occupants, purchasing a home is an emotional decision that requires weighing competing priorities. For many investors, decisions about which home to purchase are based on economic calculations alone, and provide more freedom of choice. While none of this criteria is concrete, it can further narrow housing options among the already limited stock available for owner-occupants.

Condition of the home. Many low- and moderate-income owner-occupants have a preference for move-in ready homes that only require minimal repairs. For some owner-occupants, even minor repairs can wipe out a lifetime of savings, and that is to say nothing of needing to fix major structural damage. Investors, however, are more likely to purchase homes as-is and consider homes in poor or average condition to be ripe for investment. Investors tend to have the resources and knowledge to take on these repairs efficiently and at scale. However, preferences around the condition of the home depend to some degree on the financial resources of an owner-occupant or investor; ensuring that a home is safe and in good condition for one's family or future generations could translate to a willingness to invest as many resources as possible.

Location of home. Neighborhood characteristics, including access to high-quality schools and jobs, adequate public transit, and access to other resources matter a great deal to owner-occupants. Many homebuyers living in neighborhoods in Forsyth County that have experienced public and private disinvestment often hope to move out of these neighborhoods to ones that have greater access to opportunity. These considerations are less relevant to investors who intend to either sell the home or rent it and make a profit.

Citations

- See source">Technical Appendix for more information regarding foreclosure rates.

- The condition of a property is based on a rating system for a property’s overall physical condition, assessed at least every four years by Forsyth County. The rating system takes into account the maintenance level one would expect in a dwelling place of that property’s age. The ratings are: excellent, good, average, fair and poor. A property that is fair or poor is a property that has more than the typical “wear and tear” and shows more than the ordinary level of maintenance and upgrades based on the property’s age.

- To ensure these trends are not just the result of growth rates in large FHA loans outpacing growth rates in small dollar FHA loans, we also assessed the number of originations over time. This revealed that this is not the case, and in fact, the total number of small dollar FHA originations has been declining since 2015, while the total number of large FHA originations (more than $100,000) have remained fairly constant over this same time period. Small dollar originations of conventional loans, on the other hand, have been steadily growing since 2015, though the growth in larger conventional loan originations has been much faster, resulting in the declining overall share in small dollar conventional loans.