The Lending Hole at the Bottom of the Homeownership Market

Table of Contents

- The Lending Hole at the Bottom of the Market: Small Dollar Mortgages

- A Roadmap to this Report: Methodology, Data Sources, and Definitions

- It’s Expensive to be Poor: Small Dollar Homes are Inaccessible to Low- and Moderate-income Families

- A Microcosm of the Problem: The City of Winston-Salem, North Carolina

- Increasing Access to Small Dollar Mortgages: Potential Solutions

- Conclusion

Abstract

While conventional wisdom maintains that high home prices are to blame for declining homeownership rates, there is another elusive barrier stopping millions of would-be homeowners: banks are increasingly unwilling to write small dollar mortgages. One fifth of owner-occupied homes in the United States cost less than $100,000, but due to unintended consequences of the Dodd-Frank Act, among other factors, banks are opting out of writing small dollar loans. Instead, more than three quarters of small dollar homes are purchased in cash, often by investors or well-off individuals. This lending gap locks millions of low-and-moderate income families out of homeownership, and exacerbates the racial homeownership gap as these small dollar homes are a critical source of homeownership for many first-time buyers in Black and Hispanic communities.

In this report, the Future of Land and Housing program at New America and the Center for the Study of Economic Mobility (CSEM) at Winston-Salem State University (WSSU) focus on three dimensions of this problem: 1) the unavailability of financing for small dollar loans; 2) the catch-22 of “mortgage standards”; and 3) competition with all-cash buyers at a national level and through a local case study of Winston-Salem and Forsyth County, North Carolina.

Acknowledgments

Contributing Authors

Jack Portman, Elaine Tsui, Leonardo Torres Beltran, and Joseph Sloop

We’d like to extend our gratitude to the reviewers of this report for offering their time and knowledge: Tara Roche, Tracy Maguze, and Rachel Siegel from the Consumer and Home Financing team at Pew Charitable Trusts; Jada Mclean, co-founder of Hurry Home; and Dan Kornelis, former Community and Economic Development Director at Forsyth County.

We’d also like to thank everyone we interviewed during this process: the real estate agents, the lenders and the housing leaders in Forsyth County, who generously shared their insights and expertise with us as we attempted to disentangle this complex issue.

Last, but certainly not least, we thank all of our former and current colleagues at New America that assisted with this report: Tim Robustelli, Alison Yost, Maria Elkin, Joanne Zalatoris, Naomi Morduch Toubman, Joe Wilkes, and Samantha Webster.

Downloads

The Lending Hole at the Bottom of the Market: Small Dollar Mortgages

“The U.S. financial system has built a well-oiled machine for extending credit to high-earning Americans with conventional finances. The machine sputters when confronted with borrowers on the margins, making it tougher to attain homeownership and its wealth-building potential.” — Ben Eisen, Wall Street Journal reporter

Homeownership is a key component of building wealth in the United States: The average homeowner boasts a net worth of $255,000, close to 40 times that of the average renter ($6,300). And yet, a critical constraint is locking out many low- and moderate-income homebuyers, even those with good credit and money for a down payment: the unavailability of small dollar mortgages for relatively affordable homes.

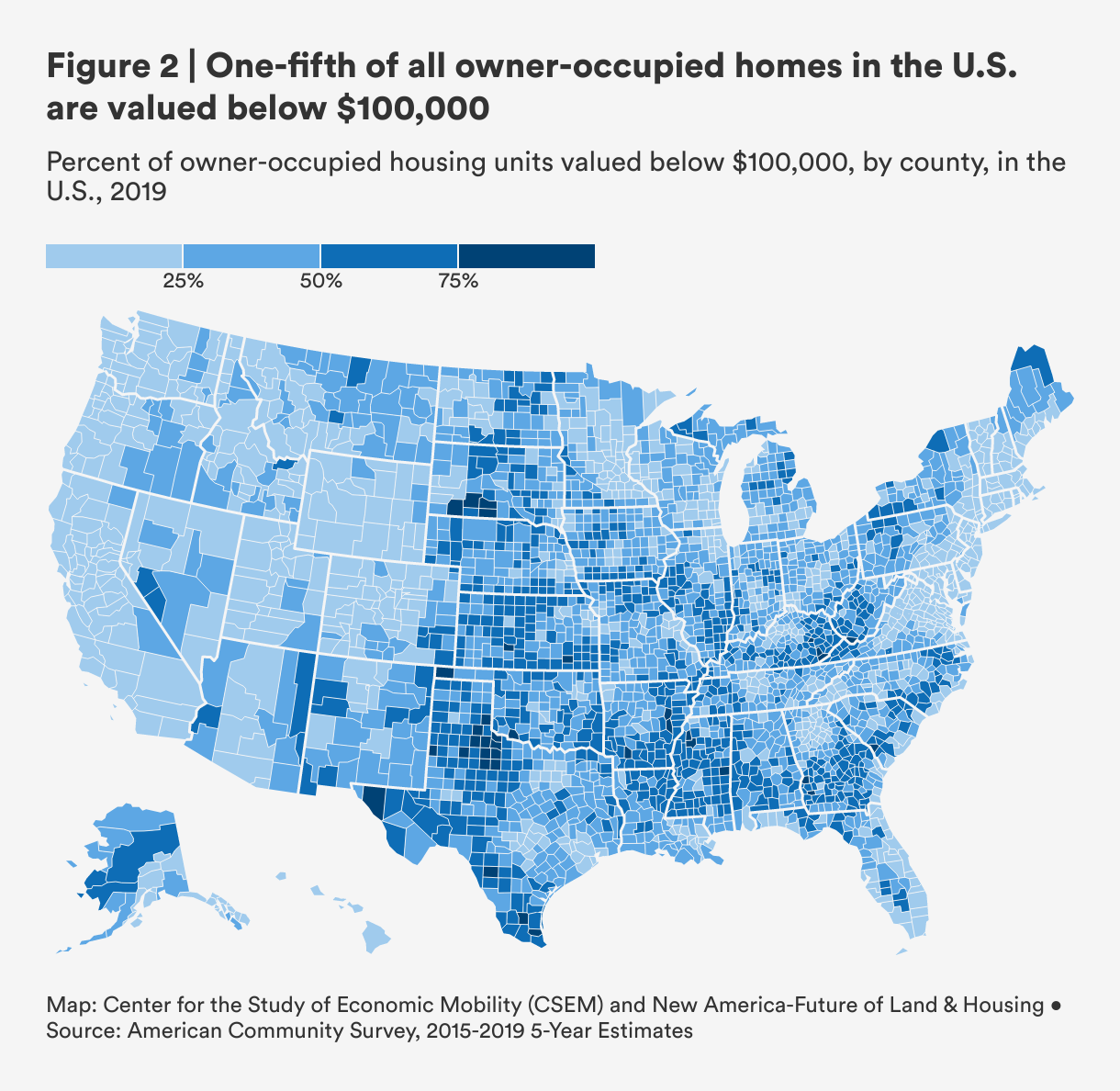

Nearly 20 percent of all owner-occupied homes in the United States are valued at less than $100,000, according to U.S. Census data. These “small dollar homes” provide a critical source of housing for low- and moderate-income families, often first-time homebuyers and people of color. Yet, for a host of reasons, including an unintended consequence of the post-2008 anti-predatory regulations in the Dodd-Frank Act, banks are increasingly unwilling to write mortgages on these homes. And without borrowing money, most Americans cannot afford to buy a home.

Yet, over the last decade, origination for mortgage loans between $10,000 and $70,000 and between $70,000 and $150,000 has dropped by 38 percent and 26 percent, respectively, while origination for loans exceeding $150,000 rose by a staggering 65 percent. At the same time, small dollar loans (defined in this report as $100,000 or below) are being denied nearly four times as often as larger loans nationwide, according to a 2019 Urban Institute analysis . While it is easy to attribute higher denial rates to weaker credit, a deeper look indicates that not only do borrowers of small dollar loans have similar credit profiles to those with midsize loans, but these loans also perform similarly.

Small dollar homes—intended to be the first rung on the ladder for building wealth—are becoming increasingly inaccessible to low- and moderate-income families reliant on borrowing money. Three quarters of homes costing more than $100,000 were purchased with the help of a mortgage loan in 2019, whereas only 23 percent of homes below $100,000 were purchased with a mortgage loan. Instead, investors and all cash buyers have largely purchased small dollar homes to flip and sell for a profit or for rental income.

Many homeownership assistance programs focus on improving a buyer’s finances through building credit, increasing financial literacy, and providing down payment support. While important, these appear to miss a critical piece of the puzzle for low- and moderate-income buyers: even when they have a down payment together, and even when they have good credit, they often are still unable to purchase a home because banks and other lenders won’t extend them a small dollar loan.

The Immediate Consequence: Homeownership Out of Reach for Millions

When banks and other lenders opt out of the small dollar housing market, and when denial rates are higher for small dollar loans when buyers do apply, homeownership becomes more difficult to access for low- and moderate-income families. Those locked out of the market are left with few choices; they either continue to rent, or enter into riskier alternatives, including rent-to-own agreements and contract-for-deed sales. These predatory housing arrangements, more prevalent in Black and Latinx communities, require buyers to pay off the price of the home without a proper title or rights to the home until the end of the term. Buyers become responsible for upkeep and insurance, but do not benefit from the same wealth-building benefits of homeownership.

This lack of access to homeownership is particularly pernicious for Black households. In the ten years since the Great Recession, the homeownership gap between Black and white households has reached its highest level in 50 years—even higher than when discrimination against Black homebuyers was legal. Today, the Black homeownership rate is 45 percent compared to a white homeownership rate of 74 percent. The huge disparity in Black and white homeownership rates has contributed to the racial wealth gap we see today: A typical white household has 10 times the wealth of a typical Black household. If current trends continue, it could take over 200 years for a Black family to accumulate the same amount of wealth as white families.

The ability to secure a mortgage lies at the heart of unlocking access to wealth-building opportunities and helping to close the racial homeownership gap. Access to small dollar or affordable homes, including the mortgage financing needed to afford these homes, is a complex issue, however, that encompasses a host of different players, acting according to their own incentives, across the housing system. In this report, the Future of Land and Housing program at New America and the Center for the Study of Economic Mobility (CSEM) at Winston-Salem State University (WSSU) focus on three dimensions of this problem: 1) the unavailability of financing for small dollar loans, 2) the catch-22 of mortgage standards, and 3) competition with all-cash buyers.

We explore nationwide lending trends, and ground our research in the City of Winston-Salem and Forsyth County, North Carolina to better understand the causes of the small dollar mortgage gap and in turn, develop effective solutions. We attempt to shed light on how some of the major challenges related to the inaccessibility of financing for small dollar mortgages interact with each other to perpetuate unequal access to homeownership for low- and moderate-income homebuyers, potentially contributing to the stagnation of neighborhoods that is ever-present in cities across the United States.

The Bigger Context: Stagnant Neighborhoods in Segregated US Cities

In the book The Divided City: Poverty and Prosperity in Urban America, author Alan Mallach describes how excitement over investment and development in certain parts of U.S. cities is “tarnished by the reality that in the process, these cities are turning into places of growing inequality, increasingly polarized between rich and poor, white and black, with unsettling implications for their present and future.”1 A 2014 study cited by Mallach of 1,100 high-poverty neighborhoods in fifty-one cities found that between 1970 and 2010, fewer than one in ten had “rebounded”- defined as having a poverty rate falling from above 30 percent to below 15 percent. In addition, there were nearly three times as many neighborhood areas with greater than 30 percent poverty in 2010 versus 1970.

Mallach’s unsettling conclusion is this: “Cities have largely stopped being places of opportunity where poor people come to change their lives, and today’s poor and their children remain poor, locked out of the opportunities that cities offer.”2

Small dollar homes in stagnant neighborhoods have previously served as starter homes for first-time homebuyers, who increase the tax base and contribute to neighborhood stability. We hypothesize that by restricting access to homes in neighborhoods with affordable housing stock, the unavailability of small dollar mortgages contributes substantially to segregation and stagnation.

But when would-be homebuyers are unable to get a mortgage loan, many of these homes are instead purchased by investors with cash on hand and converted into rental properties or flipped and sold for a profit. Unlike a growing family or individual hoping to build wealth and invest in their home and neighborhood, investors are less likely to fix up properties and contribute to neighborhood stability. At the neighborhood level, the result is that areas in cities with depressed home values become “locked in,” unable to rebound through new investment in the same way other neighborhoods can. And, individually, residents in these neighborhoods are unable to build wealth by becoming homeowners, contributing to continued stagnation and declining property values.

Winston-Salem, North Carolina: A Case Study

To better understand how small dollar loans impact a local housing market, we examine the City of Winston-Salem, in Forsyth County, N.C.—a place that typifies the growing economic and racial divide that Mallach writes about in The Divided City. Despite the rebound experienced in some parts of the city, a 2014 study by economist Raj Chetty, found that Forsyth County had the third worst economic mobility for the bottom quintile in the country, and another study found that it has one of the country’s fastest growth in concentrated poverty. According to 2019 American Community Survey data, Forsyth County is in the 93rd percentile for income inequality.

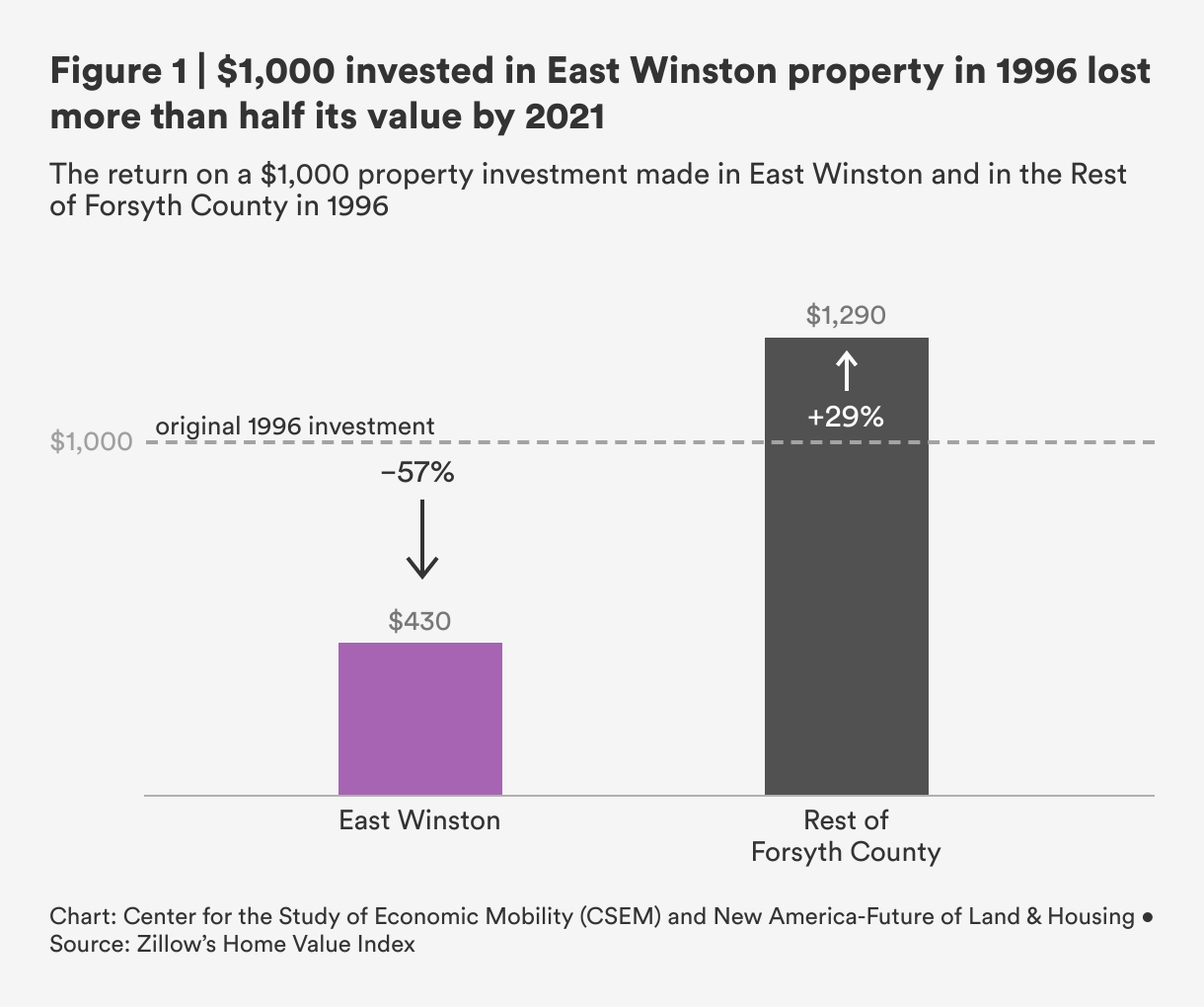

In East Winston, $1,000 invested in 1996 is now worth $430; elsewhere in Forsyth County, $1,000 is now worth $1,290.

Like so many other cities across the United States, Winston-Salem is truly a tale of two cities, split down the middle by U.S. Route 52, a four-lane highway dividing the city into east and west. While the city has seen recent growth and investment to the west side of Route 52, the east side of the city—a collection of historically Black neighborhoods referred to as East Winston—remains disconnected from access to high-quality jobs, housing, and public transit.

Home values in East Winston have plummeted over the last 25 years. Figure 1 illustrates the return on a $1,000 property investment in 1996, the first year Zillow began collecting market data, in East Winston compared to the rest of Forsyth County. We calculated that in real terms, every $1,000 invested in property in East Winston in 1996 is now worth $430; by comparison, every $1,000 invested elsewhere in the county is now worth $1,290.3

Despite the fact that homes in East Winston have fallen dramatically in value and despite the existence of robust homeownership assistance programs in Forsyth County that help cover the cost of homeownership,4 many would-be homeowners are still unable to purchase otherwise affordable homes in these neighborhoods.

Not only does the unavailability of small dollar mortgage loans lock out potential homeowners: We hypothesize that the lack of access to mortgage credit that removes potential buyers from the housing market may be one important reason why we have seen falling property values in East Winston over the past 15 years. Indeed, one clue is that in the past twenty years, East Winston has seen a change in the type of buyers who purchase its inexpensive homes—from a majority of homes sold to buyers relying on mortgage loans, to the majority of homes sold to buyers paying all cash.

The Structure of this Report

This report is organized in the following sections: the next section, titled “A Roadmap to this Report,” provides an overview of our quantitative and qualitative methods, as well as key terms and definitions. This is followed by “It’s Expensive to Be Poor,” an investigation into why it has become increasingly difficult for low- and moderate-income families across the county to obtain small dollar mortgages, drawing on existing research and reporting. The next section titled, “A Microcosm of a Problem” delves into the case study of Winston-Salem, N.C., showcasing our quantitative data and qualitative findings from a local housing market. Then we discuss some potential solutions before concluding this report.

Citations

- Alan Mallach, The Divided City: Poverty and Prosperity in America (Washington, DC: Island Press, 2018), p. 2.

- Mallach, The Divided City, pg. 10.

- The methodology for this analysis is detailed in the source">Technical Appendix.

- Forsyth County runs a highly successful program for low-income and largely Black participants who are interested in becoming first-time homeowners, as reported in severalsource"> CSEM Working papers. However, there are generally only about 10-20 participants a year.

A Roadmap to this Report: Methodology, Data Sources, and Definitions

To better understand the challenges of small dollar mortgages at the local level, this report presents findings from quantitative and qualitative research in Forsyth County, N.C. conducted from March 2021 through October 2021. Below we provide an overview of our data sources, methods, and key terms definitions, though a more detailed description of our methods and data sources can be found in the Technical Appendix.

Quantitative Methods

Our quantitative analysis relies on four main data sources. We provide a brief description of each data source, including the analysis conducted using each source, and any caveats or assumptions that are essential for understanding the analysis.

Home Mortgage Disclosure Act (HMDA) data: HMDA requires that eligible lending institutions report loan-level characteristics about mortgage applications, including applicant demographics, loan amounts, and application outcomes (e.g., whether a mortgage application resulted in an origination, denial, incomplete, etc.). We downloaded publicly-available HMDA data for Forsyth County, N.C. from 2007 to 2019. Though available, we excluded 2020 HMDA data to explore pre-COVID trends. We used this data to explore trends and geospatial patterns in mortgage loan application origination and denial rates, across small dollar and large dollar loans, as well as different loan types. The HMDA data we analyzed includes all mortgage loan applications related to a home purchase for a principal dwelling place, regardless of loan size, loan type, property type (manufactured, single-family, multi-family), or lien status.

ATTOM data: ATTOM Data Solutions is a for-profit database management company that provides detailed real estate data, including transaction and property-related data. We purchased property transaction data for the State of North Carolina going back to 1996 in May 2021. We used ATTOM data to investigate trends in residential market transactions, specifically trends in cash purchases vs. purchases involving a mortgage over time. The ATTOM data we analyzed included transaction data on single-family detached houses, townhomes, condos, mobile homes, and manufactured homes.

U.S. Census Bureau American Community Survey (ACS) data: The American Community Survey (ACS) is a demographics survey administered by the U.S. Census Bureau that collects data related to educational, income, migration, disability, employment, and family characteristics. We use ACS data to understand trends related to key housing and socio-demographic variables and geospatial trends across Forsyth County. We use ACS’s five-year estimates in the years between 2010 and 2019.

Zillow's Home Value Index: We used Zillow’s Home Value Index (ZHVI), a publicly-available resource on property value estimates. The data we analyzed includes the ZHVI for all home types, from years 1996 to 2021. The ZHVI is an estimate of a typical home’s value in a given region. We used this estimate to compare the area comprising East Winston and comprising the rest of Forsyth County.

We cleaned each data source, and created new variables based on existing data to assess mortgage loan application originations, denial rates, and trends in method of payment over time. We also visualized key metrics in Forsyth County to explore geospatial patterns based on findings from our qualitative and quantitative research. Maps in this report generally include data for multiple years to account for small sample sizes, and so while maps produced in this report do not show trends over time or even a present-day snapshot, they do illustrate spatial patterns that take into account multiple years of data.

Qualitative Methods

To better understand how issues related to small dollar mortgages interact within a local housing market, we conducted key informant interviews with three groups of housing stakeholders in Forsyth County: real estate agents, mortgage lenders, and local housing leaders. To identify potential interviewees, we filtered MLS real estate listings for homes in Forsyth County under $100,000. We reached out to real estate agents, and from there, we asked interviewees to identify other agents, lenders, and housing leaders who work with small dollar homes and/or loans in Forsyth County and asked that they provide contact information or introduce us directly.

From April 2021 to September 2021, we conducted interviews with:

- Fourteen real estate agents or realtors in Forsyth County

- Seven mortgage lenders operating in Forsyth County

- Ten housing leaders in Forsyth County, from non-profit housing organizations, homeownership assistance service providers, and local developers

We used semi-structured interview guides for each type of stakeholders, broadly focused on:

- Role as an agent, lender, or housing leader in working with low- and moderate-income homebuyers, including the payment structure of their organization

- Experience working with small dollar homes and mortgages, including challenges in selling homes or providing financing for loans under $100,000

- Experiences working with other actors in the home purchasing process (agents, lenders, city and county government officials, etc.)

- Other avenues for homeownership for low- and moderate-income buyers

All interviewees were provided assurance about confidentiality, and each interview was recorded and transcribed. We analyzed qualitative interview data for each type of stakeholder-based on the major causes and consequences laid out in existing research and reporting, and used data from our findings to validate, complicate, and deepen our understanding of small dollar loans, especially within the context of a specific housing market. We also used these findings to conduct additional quantitative inquiries.

Terms and Definitions

Here we define terms we commonly use in this report.

We define “small dollar mortgages” (or “small dollar loans”) as loan applications for $100,000 and below. We use $100,000 as a cutoff for loans and home values in Forsyth County for the following reasons:

- First, $100,000 is commonly used as a cutoff to indicate small dollar loan sizes and home values in existing research.

- Second, the median value of homes associated with small dollar loans (less than $100,000) in 2019 HMDA data is $105,000. Further, the share of homes valued at less than $100,000 associated with originated loans for under $100,000 is around 49 percent.

- Third, the overall median home value in Forsyth, according to 2019 ACS data, is $170,200, so higher small dollar cutoffs used in other research are high for Forsyth County, even if appropriate nationwide. It is important to note, however, that many lender costs are fixed regardless of the location of the home and potential homebuyer.

We use small dollar home as a proxy for what a buyer is able to purchase with a small dollar loan. As such, we define “small dollar homes” as those that sold for or cost the buyer $100,000 or less. It is important to note, however, that the amount a buyer pays to purchase a home typically differs from the size of the mortgage loan needed to finance that home due to down payments. However, we believe this difference is likely negligible, especially for low- to moderate-income buyers who typically put less down.

We define an “owner-occupant” as an individual who purchases a home with an intent to live in it, whereas an “investor” is a person or company that purchases homes to either rent out or flip and sell for a profit. We use the term “all-cash buyer” or “cash buyer” to refer to anyone who can afford to purchase a home without financing (either through a mortgage loan or an alternative financing arrangement). An all-cash buyer can be an investor or an owner-occupant, as this term refers only to the means used to purchase a home, and not the buyer’s intent once a home has been purchased.

We use the term “low- to moderate-income homebuyer” to refer to those most likely to be impacted by the lack of small dollar loans. We do not define an income cutoff for this group, as the ability to purchase a home is dependent on several factors beyond income. However, in Forsyth County, N.C., the eligibility cutoff for most homeownership assistance programs is 80 percent of average median income, or $55,100 for a family of four, and the North Carolina Housing Financing Agency (NCFHA) uses income cutoffs ranging from $71,000 to $99,000 depending on loan products and family size.

While government-backed loans are issued by the Federal Housing Administration (FHA), the U.S. Department of Veterans Affairs (VA), and the U.S. Department of Agriculture (USDA), this report only focuses on FHA loans as they are intended to make homeownership accessible for low- and moderate-income buyers, by extending mortgage financing to families with lower minimum down payments and credit scores than conventional loans. Conventional loans, on the other hand, are not backed by the federal government and are available through banks, mortgage companies, credit unions, or two government-sponsored entities, Fannie Mae and Freddie Mac.

We use the term "lenders" to refer to any institution or financial organization that extends mortgage loans to individuals, including banks, mortgage lenders, credit unions, and community development financial institutions.

Lenders can deny a mortgage loan application for a number of reasons, including an applicant having insufficient cash on hand, a high debt-to-income ratio, poor credit history, lack of verification of financial information, among other reasons. There is a lot of variation in the way that denial rates are calculated, but we calculate “denial rates” as the percentage of total loan applications that end in a denial by a lender. Lastly, we define “origination” as an extension of a mortgage loan to an applicant, presumably resulting in homeownership.

It’s Expensive to be Poor: Small Dollar Homes are Inaccessible to Low- and Moderate-income Families

Nationwide, low- and moderate-income homebuyers face a host of challenges in accessing small dollar homes. We explore three major barriers that come into play at different stages in the home purchasing process: 1) the unavailability of financing for small dollar mortgages, 2) the catch-22 of mortgage standards, and 3) competition with all-cash buyers.

Small Dollar Mortgages are Unavailable Nationwide

Many homeownership assistance programs focus on building credit, increasing financial literacy, and providing down payment support for purchasing a home. While these are important, this focus misses a critical constraint that locks out low- and moderate-income homebuyers, even those with good credit and a secured down payment: the unavailability of small dollar mortgages for relatively affordable homes.

Nearly 20 percent of all owner-occupied homes are valued at $100,000 or less, according to U.S. Census data, and as shown in Figure 2, these homes are prevalent in counties all across the United States, though there are especially high concentrations of small dollar homes in the South and in the Midwest.

Access to small dollar homes is impacted by two different lending trends: first, lenders are opting out of extending small dollar loans altogether, and second, lenders are denying small dollar loans at higher rates than larger loans even when potential buyers do apply.

Despite the existence of these homes, in the decade following the 2008 financial crisis, originations for loans between $10,000 and $70,000 dropped by 38 percent, and originations for loans between $70,000 and $150,000 dropped by 26 percent. By contrast, originations for loans exceeding $150,000 rose by a staggering 65 percent. Another analysis documenting mortgage credit redistribution in the post-crisis period finds that since 2011, U.S. lenders have cut back on originating small and medium-sized loans, and that loans sized $200,000 and above have been increasing.

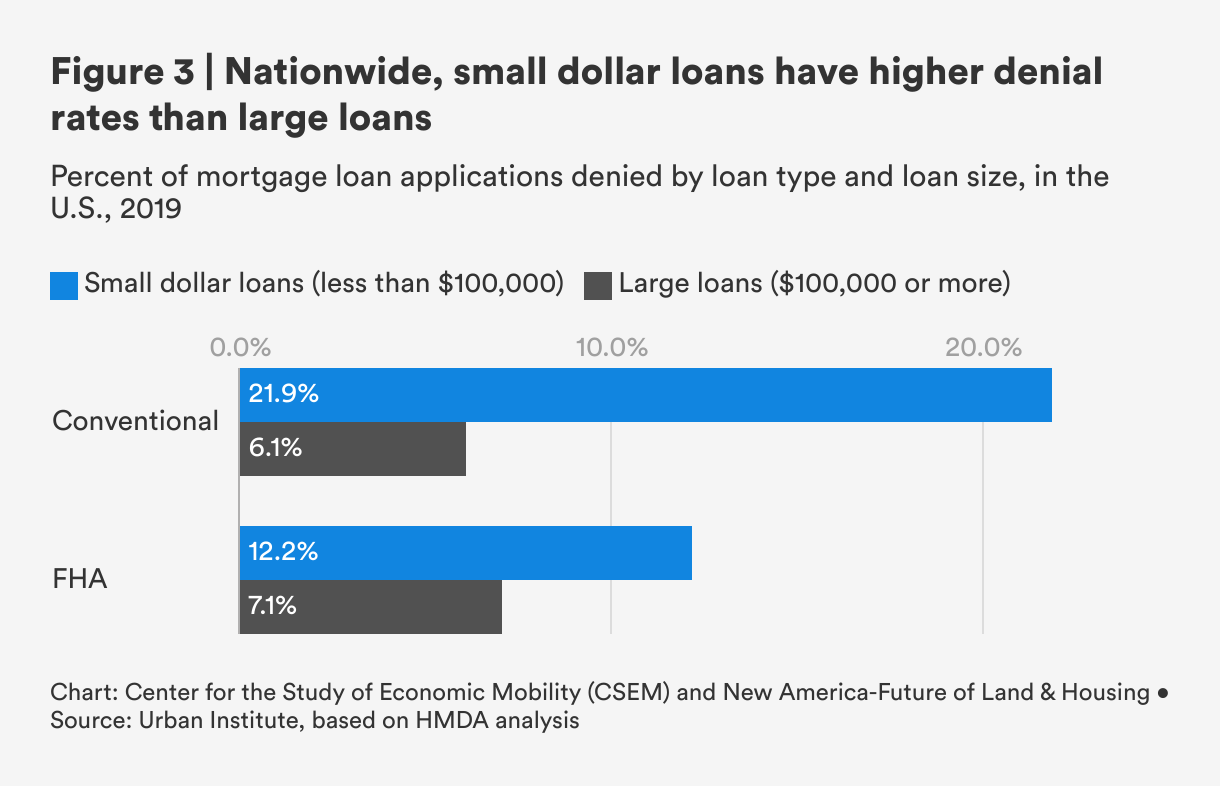

While origination for small dollar loans have been decreasing over time, denial rates for small dollar loans have consistently been high relative to large loans. As shown in Figure 3, a 2019 Urban Institute analysis finds that nationwide, denial rates for conventional small dollar loans (less than $100,000) are nearly four times as high as denial rates for conventional large loans ($100,000 or more). Denial rates for small dollar loans issued by the Federal Housing Administration (FHA)—an agency intended to serve low- to moderate-income buyers with lower credit scores and smaller down payments—were also notably higher than large FHA loans.

A deeper dive into the credit profiles of mortgage applicants debunks the myth that higher denial rates for small dollar loans are linked to the inherent risk level to lenders for extending these loans. This research, also conducted by the Urban Institute, finds that applicants of small dollar loans have similar credit profiles to applicants of larger loans, and that gaps in the denial rates persist even after accounting for applicants’ credit scores.

So what accounts for lower small dollar originations compared to large loans in the United States? Existing research ties the unavailability of small dollar loans to regulatory and structural changes in the real estate industry in the wake of the Great Recession.

Dodd-Frank regulations disincentivize small loans by lowering banks' profit relative to large loans. In the 2000s, a lack of federal oversight over the nation’s largest banks resulted in predatory lending practices that seduced many people into obtaining mortgage loans with low monthly payments. The sudden upswings in interest rates or large and unexpected balloon payments that came down the line led millions of homeowners into foreclosure as a result of the housing bubble burst beginning in 2007, leading to a near collapse of the U.S. banking system.

Soon after the financial crash, Congress implemented anti-predatory regulations in the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 (the Dodd-Frank Act). These regulations, designed to protect borrowers from this kind of predatory lending, also increased the fixed costs and the per-loan costs of extending a mortgage.

Dodd-Frank is intended to protect consumers from negligent lending practices, but some regulations have inadvertently stifled small dollar loans.

These regulations increased the fixed costs of originating a loan, regardless of the loan’s size.1 As a result, banks oriented towards originating larger loans and put less focus on small and medium-sized loans.

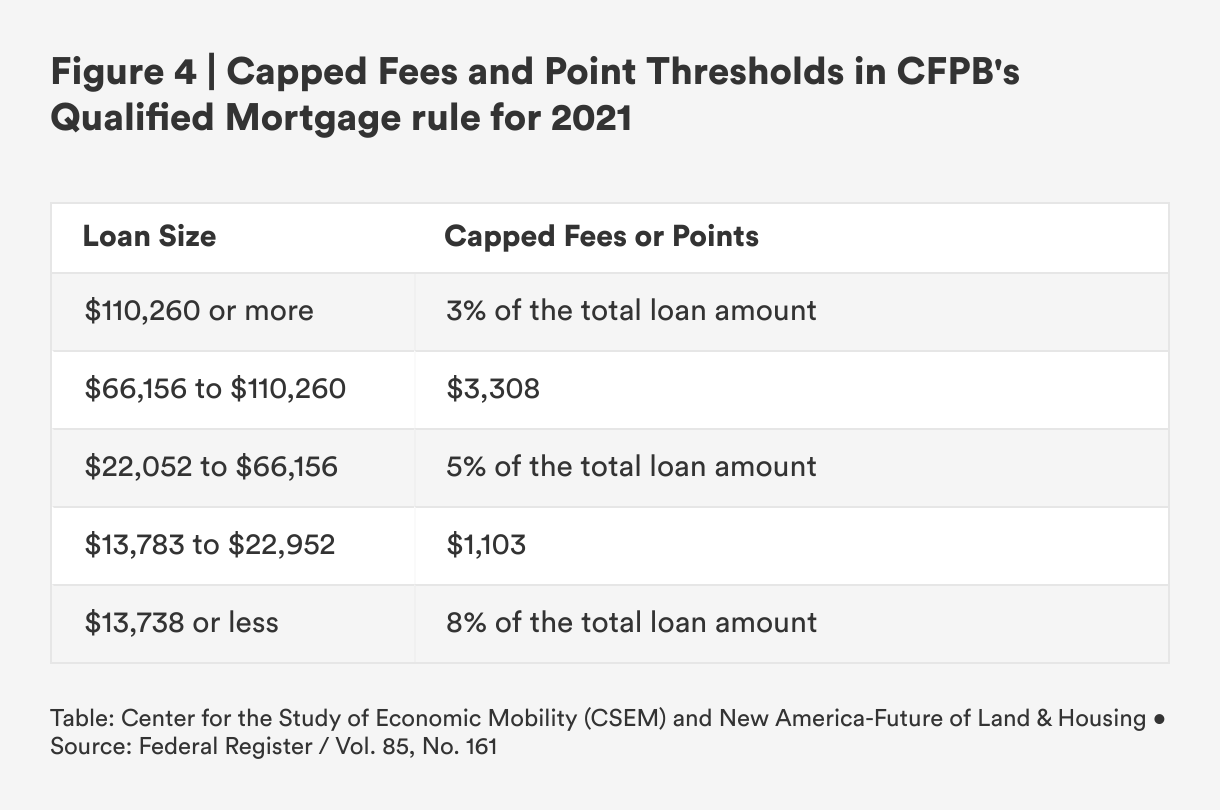

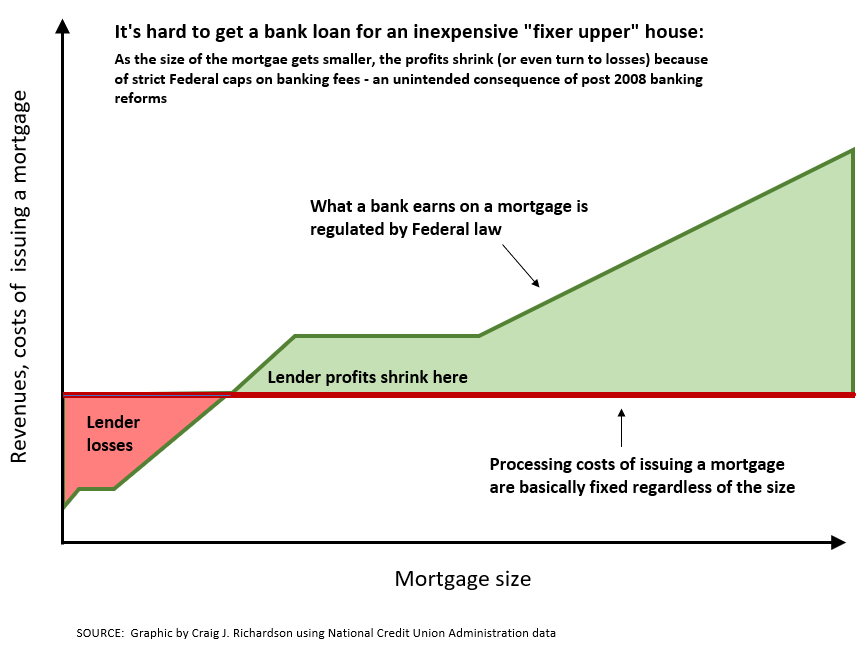

At the same time, the Qualified Mortgage rule, implemented by the Consumer Protection Financial Bureau (CFPB), capped the fees and points that lenders can charge for processing a loan on a sliding scale, based on the size of a loan (as shown in Figure 4). As a result, the smaller the loan, the less profit a bank can make, creating an additional disincentive for banks to originate small loans, even as the intent is to protect buyers from excessive fees.2

As a result of these regulations, depending upon the bank’s internal processing costs, shown by a horizontal line in Figure 5, banks could easily find it unprofitable to originate small loans. They may even refuse to write small dollar loans under a certain amount because profits shrink and can actually turn negative depending on the costs, since it takes the same amount of work to extend a loan regardless of the size.

National Credit Administration. Updated Ability-To-Repay and Qualified Mortgage Requirements from the Consumer Financial Protection Bureau(CFPB), 14-RA-09 / March 2014.

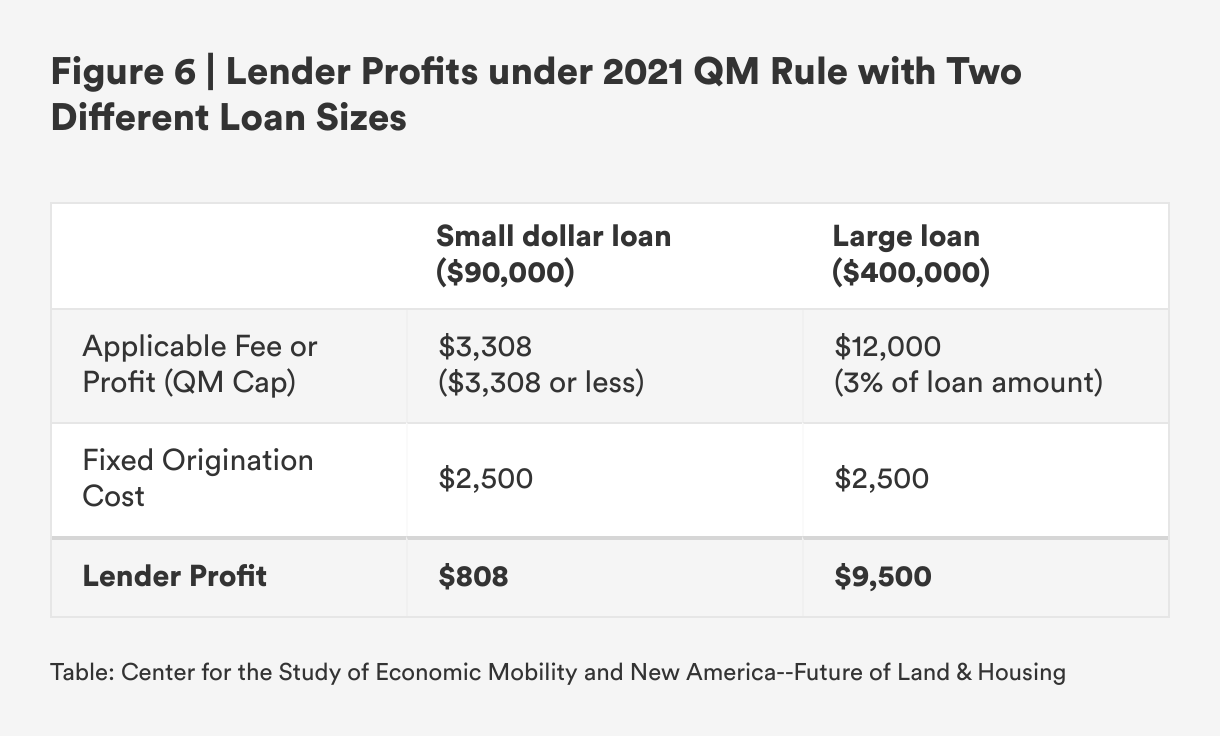

We provide a concrete example in Figure 6: Let’s say the bank faces approximately $2,500 in processing costs to originate a mortgage loan, regardless of the cost of the home. Based on Table 1 above, a lender could charge a $3,308 fee for a house costing $90,000, making a profit of $808 on that house. By contrast, a lender could charge a $12,000 fee for a $400,000 house (3 percent of the loan size per QM rules), making a profit of $9,500.

It is obvious in what direction this incentivizes the banks. While Dodd-Frank regulations were intended to protect consumers from the negligent lending practices that predated the financial crisis, they have inadvertently stifled the market for small dollar loans.

An additional impediment to lenders extending small dollar loans is the commission-based compensation structure under which lenders and many real estate agents operate. If operating under a commission-based payment structure, lenders stand to make more from larger loan amounts, further disincentivizing the desire to extend smaller loans.

The Low Supply of Housing in the United States

The United States is facing a low supply of housing decades in the making. And this lack of inventory has been most acute among starter homes, typically intended for first-time homebuyers and low- and moderate-income families. While the low supply of housing does not directly impact banks and other mortgage lenders' extension of small dollar loans, the composition and condition of the housing stock do impact the degree to which small dollar homes are accessible for mortgage financing.

This is especially true in times of unprecedented demand, like the one the U.S. housing market is currently facing. Across the country, this demand for housing is only expected to intensify in coming years, due in large part to historically low mortgage rates and the arrival of the millennial generation into their peak homebuying years.

This low supply and high demand drive up housing prices as buyers compete for available homes. This can be seen in the intense bidding wars on homes in competitive markets, where homes are selling for double their list price. It can also help explain why, according to Zillow.com, 37 percent of homes currently sell over the asking price, up from 13 percent just two years ago.

While we do not examine the lack of inventory in Forsyth County in this report, we do note that it is a large part of the problem, disrupting the traditional home purchasing process and exacerbating all other challenges homebuyers relying on small dollar loans face.

The Catch-22 of Mortgage Standards

Beyond assessing the individual finances and creditworthiness of a mortgage applicant, lenders also assess the condition of a home to protect themselves from taking on too much risk and to protect buyers from having to make repairs they cannot afford. As such, criteria on the condition of a home is a key factor in determining a home’s eligibility for financing—what some lenders refer to as “mortgage standards.”

Mortgage standards differ based on the type of loan, and loan products designed for low- and moderate-income buyers have stricter standards around the condition of the home. Loans insured by the FHA, which are intended for buyers that have been denied opportunities to build credit or save for a down payment, will not be approved by a lender unless the home meets minimum property standards for “safety, security and soundness.” Common violations include peeling paint, lead paint, openable windows without screens, a leaking roof, and damaged flooring.

As a result, these strict mortgage standards tied to FHA loans prevent these same buyers from obtaining financing on homes within their price range—often small dollar homes that are in relatively worse condition or require some degree of repair. Conventional loans, on the other hand, have much more lenient standards.

“Before you even get to the question of ‘how am I going to finance this [home]?’, you have to think, ‘can this property even be financed?’” — Forsyth County real estate agent

According to one real estate agent in Forsyth County, conventional loans are not typically concerned with the condition of a home unless it is determined to be unlivable. Discussing the differences between FHA and conventional loan standards, one real estate agent painted this picture: “Say there’s a beautiful house, and someone stole the heat pump. That is not going to stop someone with a conventional loan from buying the house, but it could with an FHA [loan].”3

These mortgage standards create a catch-22: Homes that are more likely to be affordable for low- and moderate-income buyers who are relying on FHA loan products are more likely to be older and in disrepair, and therefore less likely to meet the strict eligibility criteria of FHA loans. While the poor condition of a small dollar home alone is not necessarily causing loan denials, it is the combination of the home condition and the reliance on loan products with higher eligibility standards that creates a situation that locks many low- and moderate-income buyers out of the market. And because these buyers are often unable to obtain financing for homes within their price range, these homes instead go to buyers using cash or buyers relying on loan products with more lenient eligibility standards.

Cash (and Conventional Mortgages) are King in the U.S. Housing Market

The phrase “cash is king” refers to the considerable advantages that buyers who use cash to purchase a home bestow upon a seller, relative to buyers relying on conventional or FHA loans. Whether a cash offer is made by an investor or by a cash-flush individual who understands the inherent power of this form of payment, buyers using cash are able to streamline the transaction process and offer sellers speed and certainty—two major advantages in a transaction characterized by unpredictability.

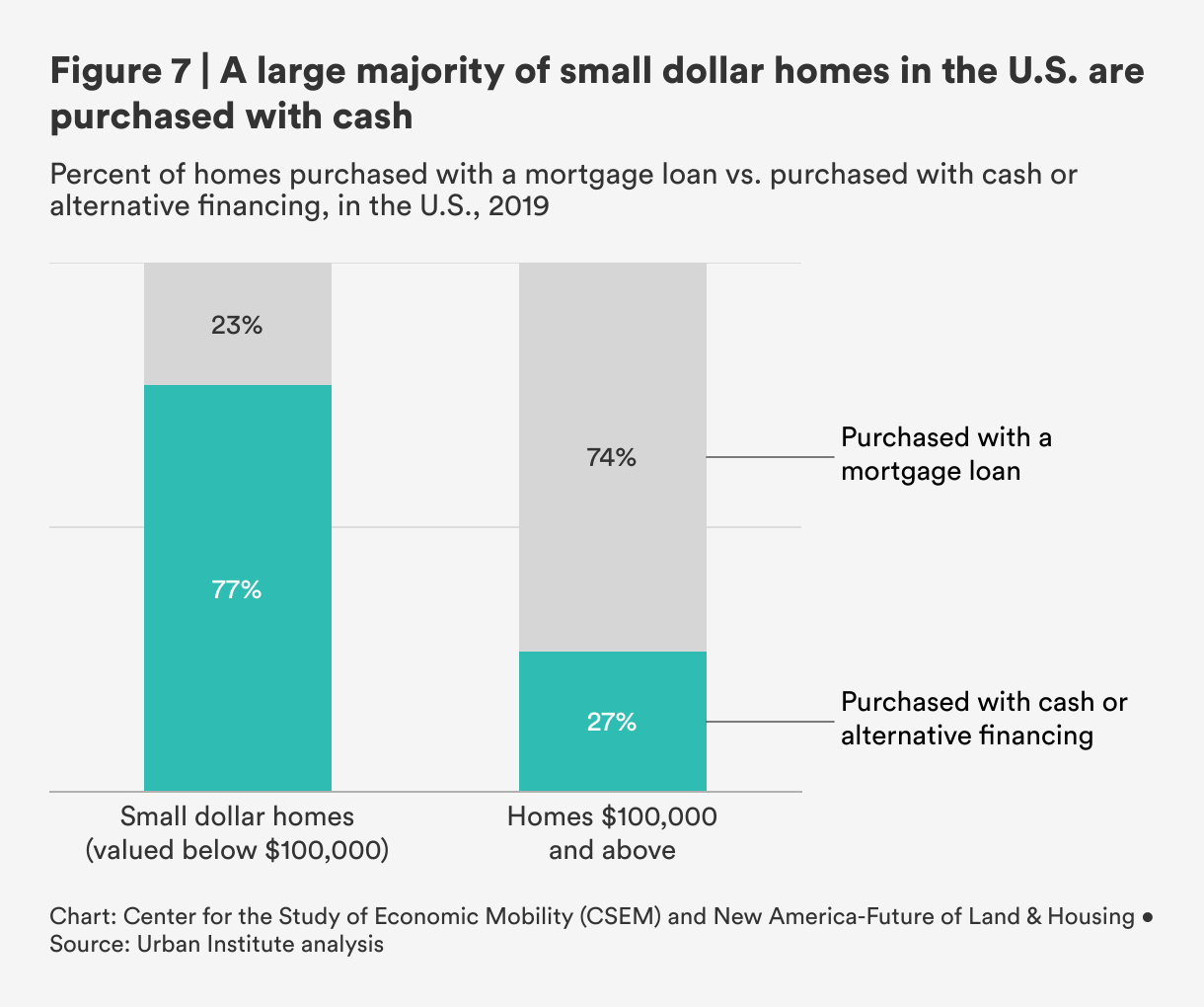

According to Zillow.com, closing time with an all-cash offer can be as little as two weeks, whereas the mortgage loan application process can take anywhere from 30 to 60 days. According to an Urban Institute analysis, cash purchases in the market for homes under $100,000 is more or less the inverse of cash purchases for homes above $100,000. As shown in Figure 7, roughly 74 percent of homes above $100,000 were financed with a mortgage in 2019, while 27 percent were purchased with cash. This was flipped in the market for small dollar homes: roughly 23 percent of single family homes below $100,000 in the United States were purchased with a mortgage loan, while roughly 77 percent were bought primarily with cash.

Why are cash purchases so much more prevalent in the market for small dollar homes? While we have not explored these causes directly, the hole left in the market opens the door for speculative non-owner occupants and other cash buyers.4 Regardless of the causes, the consequences remain the same: it is incredibly difficult for low- and moderate-income buyers, many of whom are first-time buyers in Black and Hispanic communities, to purchase and own their own homes.

FHA Loans Are Not Serving Their Intended Purpose

While the use of cash in real estate markets receives a lot of attention, the overall decline in FHA lending nationwide is also locking out many low- and moderate-income buyers. As discussed previously, FHA loans have more lenient eligibility requirements, like lower credit scores and less money required for down payments, than conventional loans and are intended for historically underserved homebuyers, many of whom are first-time buyers.

However, recent analysis shows that conventional loans are still much more prevalent than FHA loans among buyers with lower incomes. And while FHA loans decrease as income increases across both the small dollar and large loan market, this is more pronounced in the market for small dollar loans.

One reason why we may be seeing FHA lending declining nationwide is the increased federal enforcement levied against FHA lenders after the 2008 financial crisis. The Department of Justice (DOJ) during the Obama administration leveraged the False Claims Act to penalize FHA lenders for errors in their underwriting of FHA-insured loans, often bringing multi-million dollar lawsuits against FHA lenders. The lack of consistency and predictability in DOJ enforcement caused many lenders to pull back from offering FHA loans altogether.

Not only is the FHA undeserving its intended market, but FHA loans are also less competitive than cash or conventional loans with sellers choosing among several offers. The increased inspection and appraisal requirements for FHA loans, especially in competitive housing markets, can lower a buyer's odds of being chosen by a seller. In these instances, sellers are likely choosing the path of least resistance: If a home requires costly structural repairs before it can be sold to a buyer relying on an FHA loan, choosing a buyer with a conventional loan allows a seller to avoid expensive and time-consuming maintenance.

In the next section, we examine Winston-Salem, N.C. to understand the causes and consequences of a dearth of small dollar mortgages within a local housing market.

Owner-occupants Now Use Cash Too

There are a few different kinds of buyers in the market, differentiated by their method of payment and their intent once a property has been purchased. Whereas previously most buyers using cash could be considered investors, in today’s competitive market, a growing number of owner-occupants (or those purchasing homes with an intent to live in it) are using cash to win bidding wars.

Some buyers are borrowing from other assets or lines of credit instead of borrowing against the home itself. Others are utilizing companies like HomeLight Inc., Ribbon, and Opendoor Technologies Inc., that allow buyers to use cash up front while ultimately securing financing.

Even buyers using mortgage loans are increasingly leveraging the power of cash to sweeten their offers. Some buyers are including larger due diligence fees or deposits to signal their commitment to sellers, and others are waiving appraisal contingencies from their contracts with a seller, essentially ceding their right to walk away if the appraisal comes back below the sale price. This is a huge risk for buyers, as it removes a seller’s incentive to negotiate the price, meaning they would likely need to bridge the appraisal gap themselves.

Citations

- For more detail, see Regressive Mortgage Credit Redistribution in the Post-crisis Era (with A.G. Rossi), Review of Financial Studies, forthcoming, source

- Lenders can still extend non-qualified mortgages, but these have fewer legal protections and are more difficult to resell in the secondary market, which banks rely on to free up capital to make more loans.

- Recognizing the barriers that FHA mortgage standards can impose, the U.S. House of Representatives passed thesource"> Improving FHA Support for Small-Dollar Mortgages Act of 2021 in March 2021, which calls for a review of the FHA’s practices related to small dollar lending.

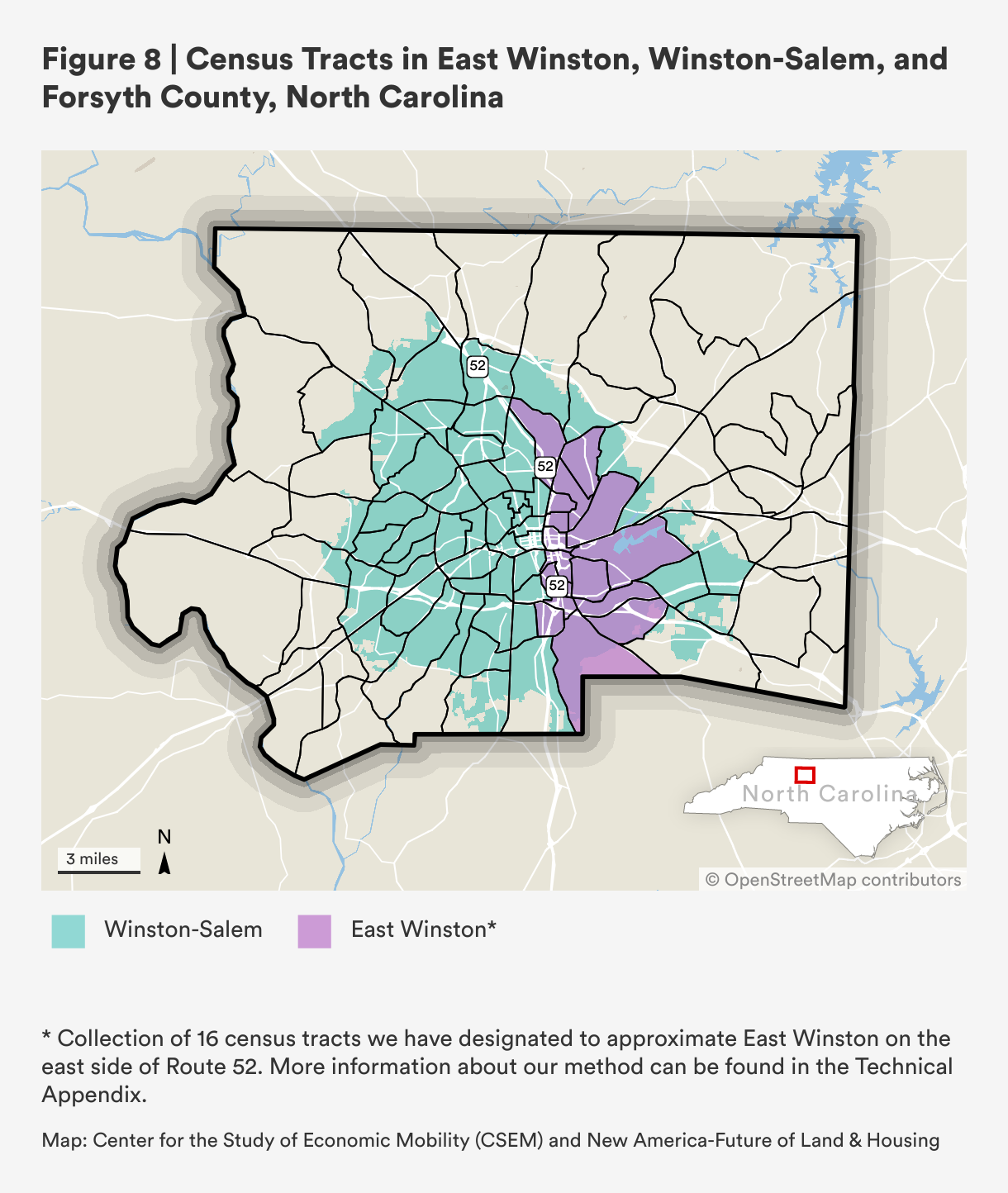

- We define East-Winston as a collection of 16 census tracts that are located near the city center of Winston-Salem on the east side of U.S. Route 52. More information about these tracts and our method can be found in the source">Technical Appendix.

A Microcosm of the Problem: The City of Winston-Salem, North Carolina

Winston-Salem, the county seat and largest city in Forsyth County, North Carolina, is an appealing place to live. It sits in the Central Piedmont region of North Carolina, and along with nearby Greensboro and High Point, Winston-Salem is part of the Triad, a significant regional metropolitan area.

According to a 2020 report on where Americans move, Winston-Salem ranked high among U.S. cities on inbound net migration, primarily attracting those with higher incomes and older movers relocating to less expensive housing markets where taxes are lower. At the same time, the area is one of the least economically mobile with one of the highest growths in concentrated poverty and highest eviction rates in the country.

As seen in Figure 8, U.S. Route 52 runs through the City of Winston-Salem, dividing lower-income and predominantly Black and Hispanic communities in the east side from predominantly white neighborhoods in and to the west of the city center. This design was not an accident; in the early 1900s, the implementation of block-by-block segregation and racist ordinances advanced by the city’s all-white board of aldermen left Black laborers working in the city’s rapidly expanding tobacco industry little choice in where they lived.

The result was burgeoning Black communities in the east side of Winston-Salem, an area that has come to be known as East Winston. East Winston continued to expand until the 1960s, when urban renewal projects and highway construction led to the destruction of hundreds of Black homes. In 1950, the local union representing tobacco workers faced unprecedented resistance and were eventually forced to disband. When the city’s strong manufacturing presence began to dwindle in the 1980s, many workers in East Winston, reliant on the nearby factories, were left with a great deal of uncertainty. In addition, families lacking a vehicle for transportation had a difficult time accessing jobs, education, and health networks, as the city’s development sprawled outward to the suburbs on the west side of Route 52.

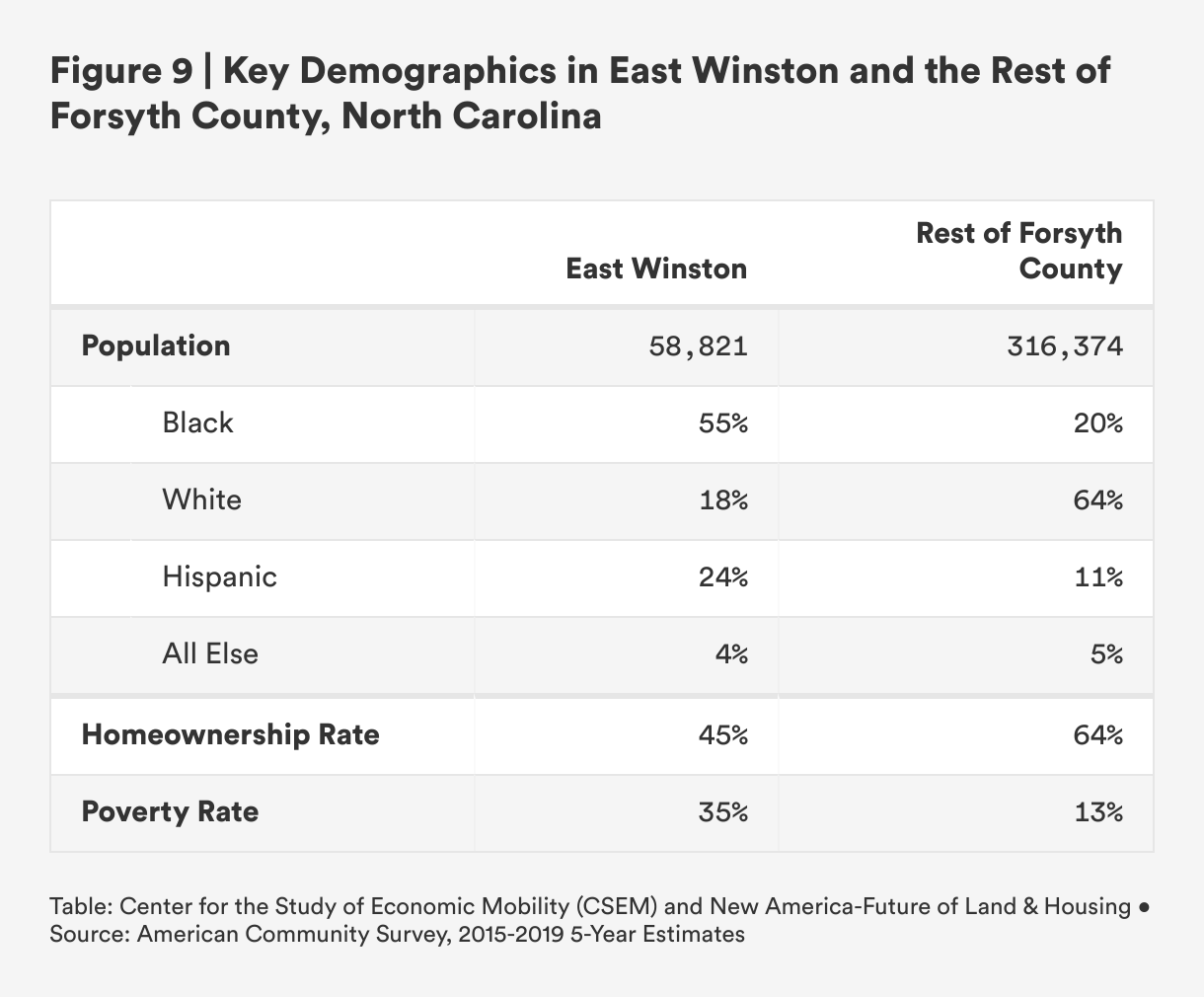

These disruptions help shed light on why homeownership and income may have remained markedly lower in East Winston than in the rest of Forsyth County. The large discrepancies between these regions, as shown in Figure 9, are in large part the result of these historical legacies.

East Winston’s Lack of Rebound After the Great Recession

During the Great Recession, and for some years afterward, East Winston was crushed by foreclosures. In 2009, the rate of foreclosures following the 2008 financial crisis in East Winston was 5.1 percent, which was nearly five times as high as the foreclosure rate in the rest of Forsyth County. By 2020, foreclosure rates in East Winston and the rest of Forsyth County dropped to under 0.3 percent, but East Winston’s foreclosure rate did not fall below 2 percent until 2015 and did not dip below 1 percent until 2017, while the rest of Forsyth County’s foreclosure rate never exceeded 2 percent, even during the height of the 2008 financial crisis.1

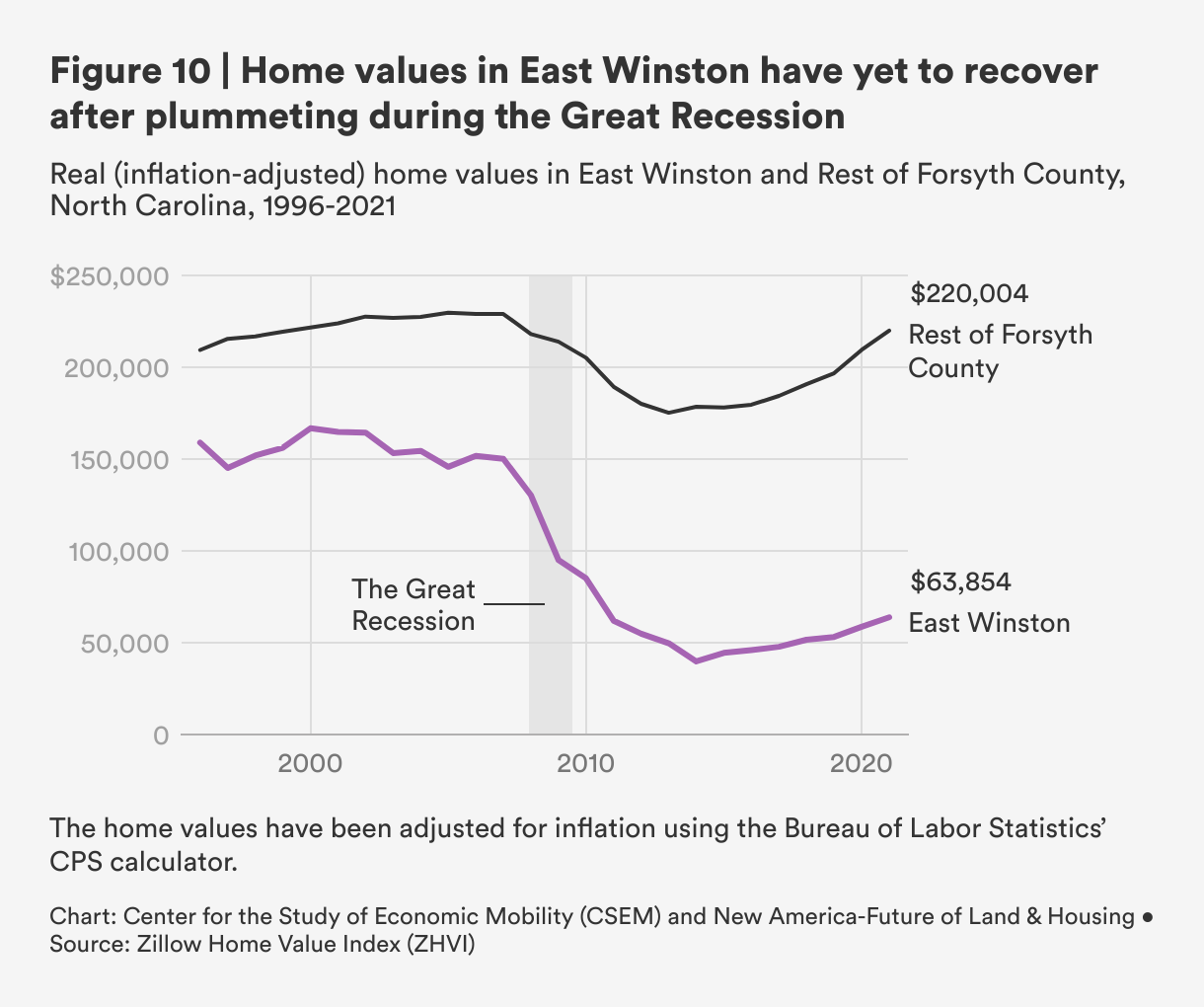

Figure 10 charts real (i.e. inflation-adjusted) home values in East Winston and the rest of Forsyth County from 1996 to 2021. Up until 2008, the value of a typical home in East Winston and the rest of Forsyth County were fairly stable, albeit values were lower in East Winston. After 2008, however, we see a distinct divergence in the two areas: the value of a typical East Winston home plummeted at a much faster rate than a typical home in the rest of the county, and has yet to recover from the 2008 collapse.

Though we see a gradual uptick in home values from 2014 until 2021 in both East Winston and the rest of Forsyth County, the value of a typical home in East Winston fell from $150,136 just before the crisis in 2007 to $39,825 at their lowest point post-crisis in 2014. By 2021, the real value of a typical home in East Winston was $63,854, down from $158,926 in 1996, meaning that over this 25 year period, the value of a typical home in these predominantly Black neighborhoods fell by nearly 60 percent.

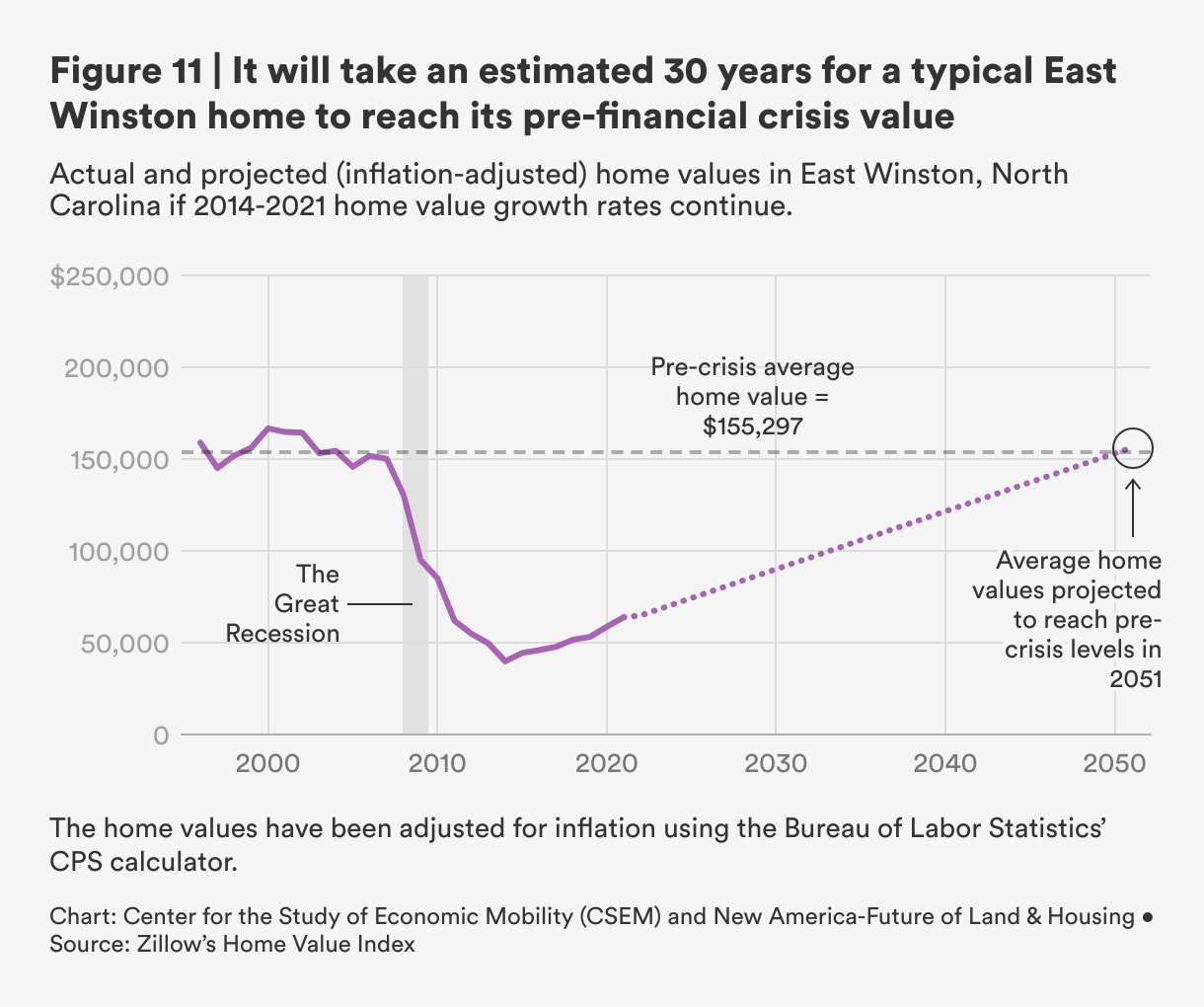

Figure 11 illustrates that, if the current trajectory of growth in home values in East Winston continues, it will take approximately 30 years for a typical home's value in East Winston to reach its pre-crisis level. We calculate that in East Winston, total real home values fell from $3.4 billion in 2007 to $1.1 billion in 2021, representing a 66 percent contraction of would-be home wealth. While today, the value of a typical home in East Winston are far from their pre-crisis levels, the value of a typical home in the rest of Forsyth County has reached and surpassed their pre-crisis levels. Instead of building long-term wealth, families who bought homes in East Winston may now owe more on their home than they will get back from selling it.

What does East Winston’s foreclosure crisis have to do with small dollar homes? The precipitous decline in home values and lack of rebound in East Winston is likely the result of the high volume of predatory loans pre-crisis resulting in a high number of foreclosures. At the same time, changes in banking regulations since 2009 may have prohibited the kind of rebound seen in other parts of Forsyth County.

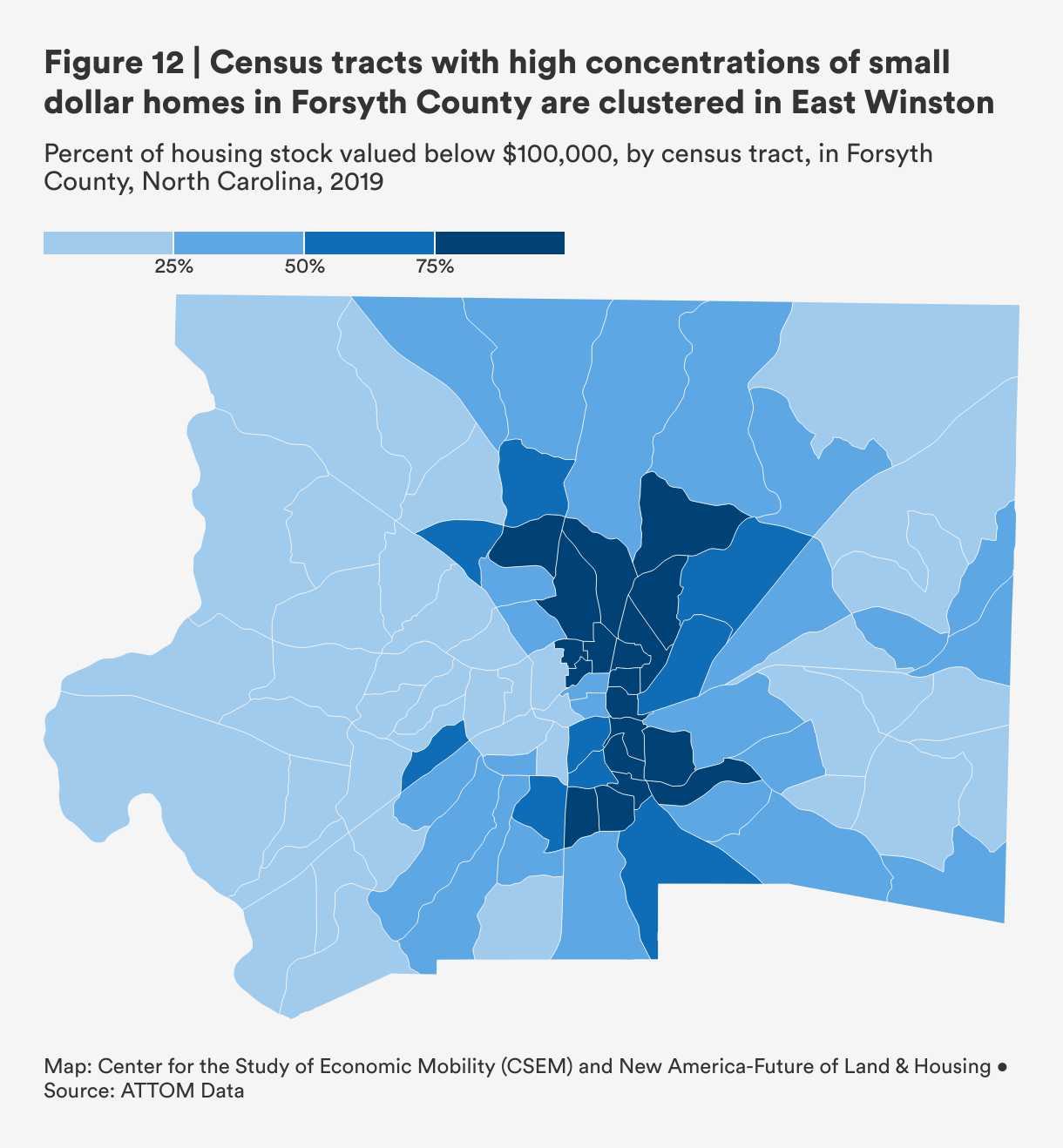

In the Figure 12, we see that neighborhoods in and around East Winston have a higher concentration of small dollar homes (below $100,000) as part of their overall housing stock than other parts of the city and county. While not visualized, this map also contains information on the share of housing stock owned by an LLC, which we use as a proxy for investor-owned properties, homeownership rate, and a host of other housing and economic indicators (by hovering over each census tract).

We can see that census tracts near the city center tend to have higher shares of investor-owned properties compared to tracts further away from the downtown area. The same holds true for East Winston, where in some tracts, a quarter of housing stock is owned by an investor. Moreover, the homeownership rates among East Winston neighborhoods are much lower than those in the rest of the county, suggesting that not only is investor activity higher in East Winston, but communities living in these neighborhoods are also less likely to own their homes.

While it is critical that communities are protected from the kind of predatory lending that led to the immediate collapse in home values in 2008, regulations keeping families from obtaining reasonable mortgage loans may be going too far in the other direction.

The Unavailability of Small Dollar Loans in Forsyth County

Roughly 34 percent of all tax-assessed homes in Forsyth County are valued at less than $100,000. Access to small dollar loans is impacted both by lenders opting out of this market, and through higher denial rates for smaller loans relative to larger loans once families do apply for financing.

Most real estate agents and lenders we interviewed acknowledged the presence of a lending floor, below which most lenders are unlikely to extend mortgages. While exact dollar amounts ranged from $45,000 to $85,000, most cited a floor of $50,000 in Forsyth County. Several lenders shared that fixed costs and maximum allowable closing costs meant that low loan amounts can quickly become expensive. One lender explained, “We stay at $50,000 or above primarily because of laws that govern fees and costs. Attorneys and appraisers also have to charge a certain amount. So when you add all this together, it exceeds what is allowed by the government.”

For lenders operating under a commission-based payment structure, individual lender profits can also be a powerful disincentive for extending smaller loans. And most lenders we spoke with in Forsyth County worked on commission, save for those whose organization’s mission included working with low- and moderate-income buyers, in which case, they earned both a salary and a commission.

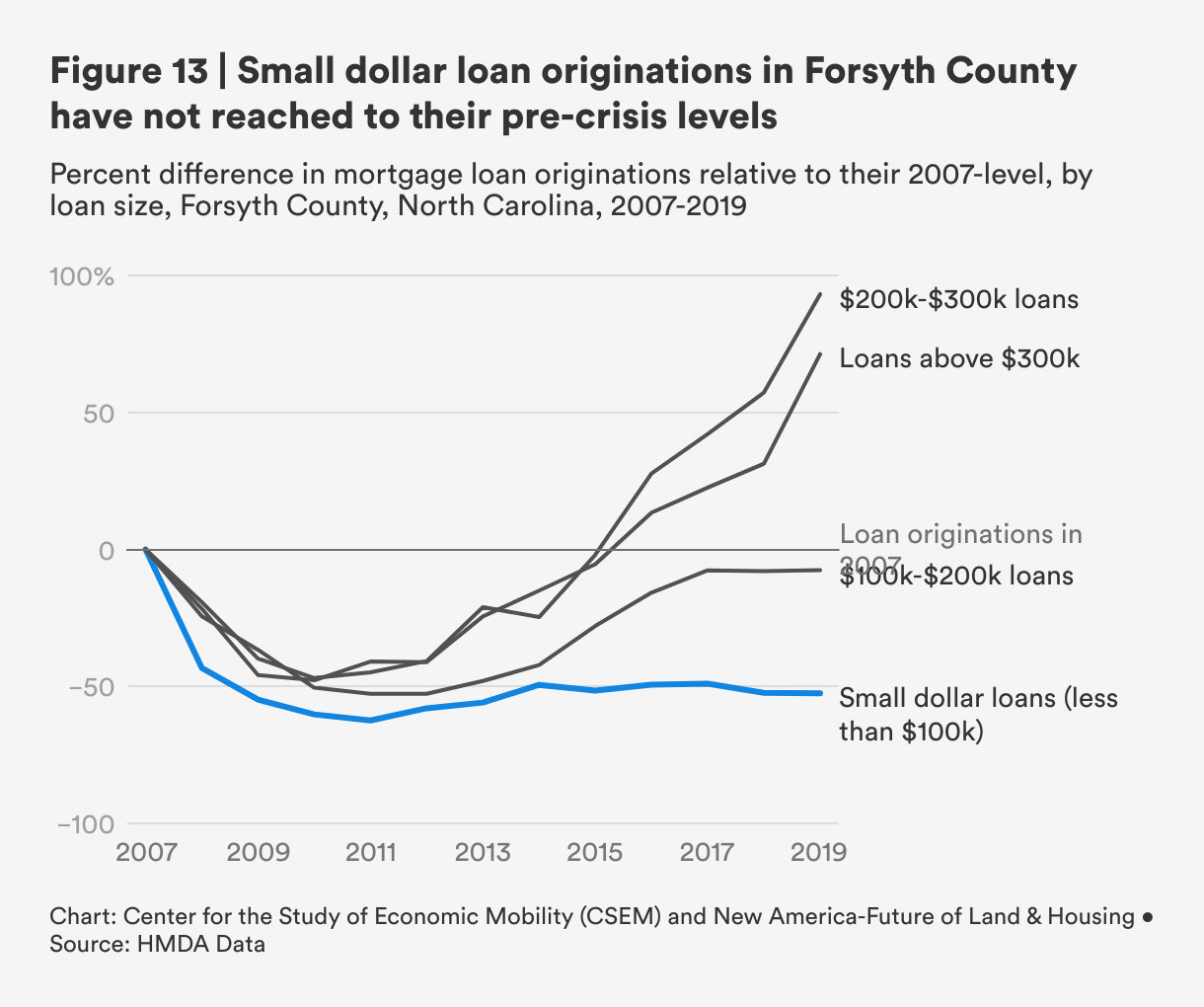

The presence of lending floors and other disincentives likely result in the lower originations we see of small dollar loans in Forsyth County. Figure 13 shows the percent difference in originations for mortgage loans of differing amounts relative to their pre-crisis level in 2007 in Forsyth County. By 2019, loan originations for small dollar loans (those less than $100,000) and for loans between $100,000 and $200,000 were 52.5 percent and 7.5 percent below their 2007-level, respectively. While originations for loans above $200,000 have recovered to their pre-crisis levels, small dollar loans have yet to see the same kind of rebound after the Great Recession.

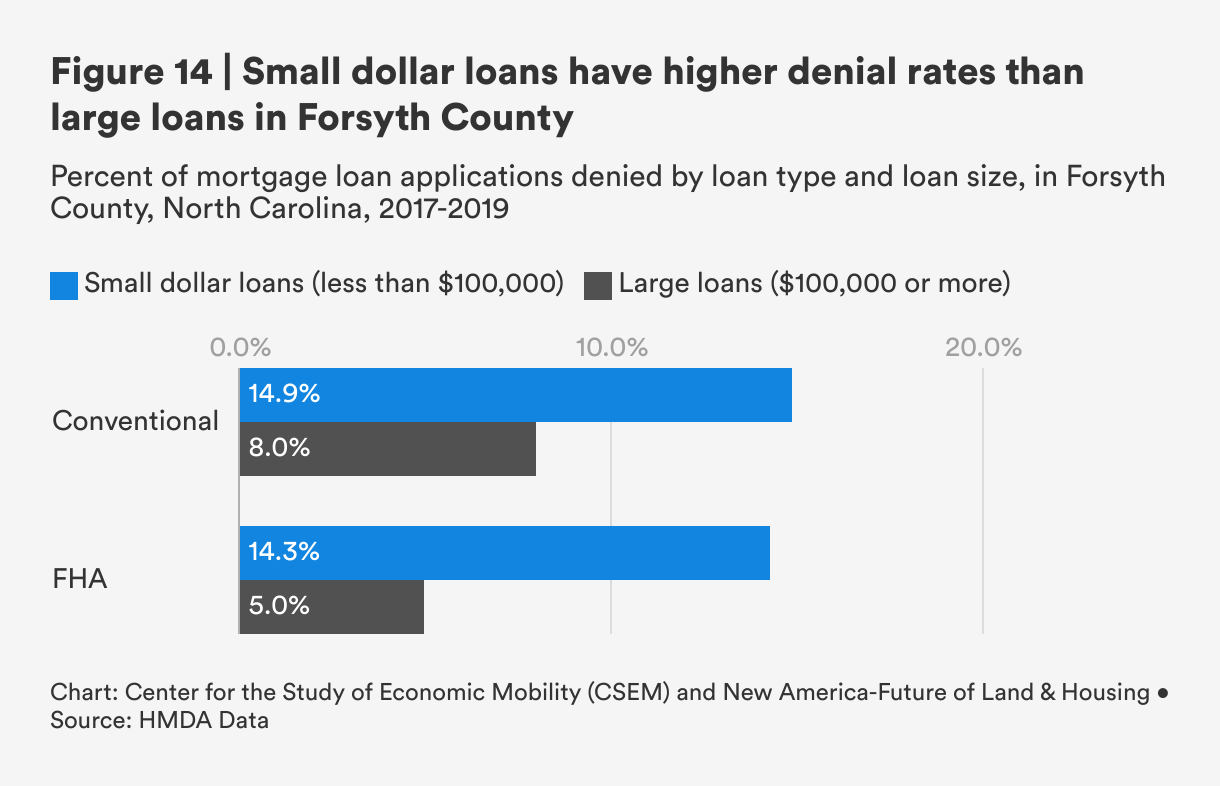

At the same time, small dollar loans are also being denied at higher rates in Forsyth County. Using pre-COVID data from 2017 to 2019, Figure 14 shows that small dollar loans are denied at nearly two and three times the rate of large loans, across conventional and FHA markets in Forsyth County, respectively. The combination of lower levels of small dollar originations and higher denial rates results in increasingly less mortgage financing for homes under $100,000.

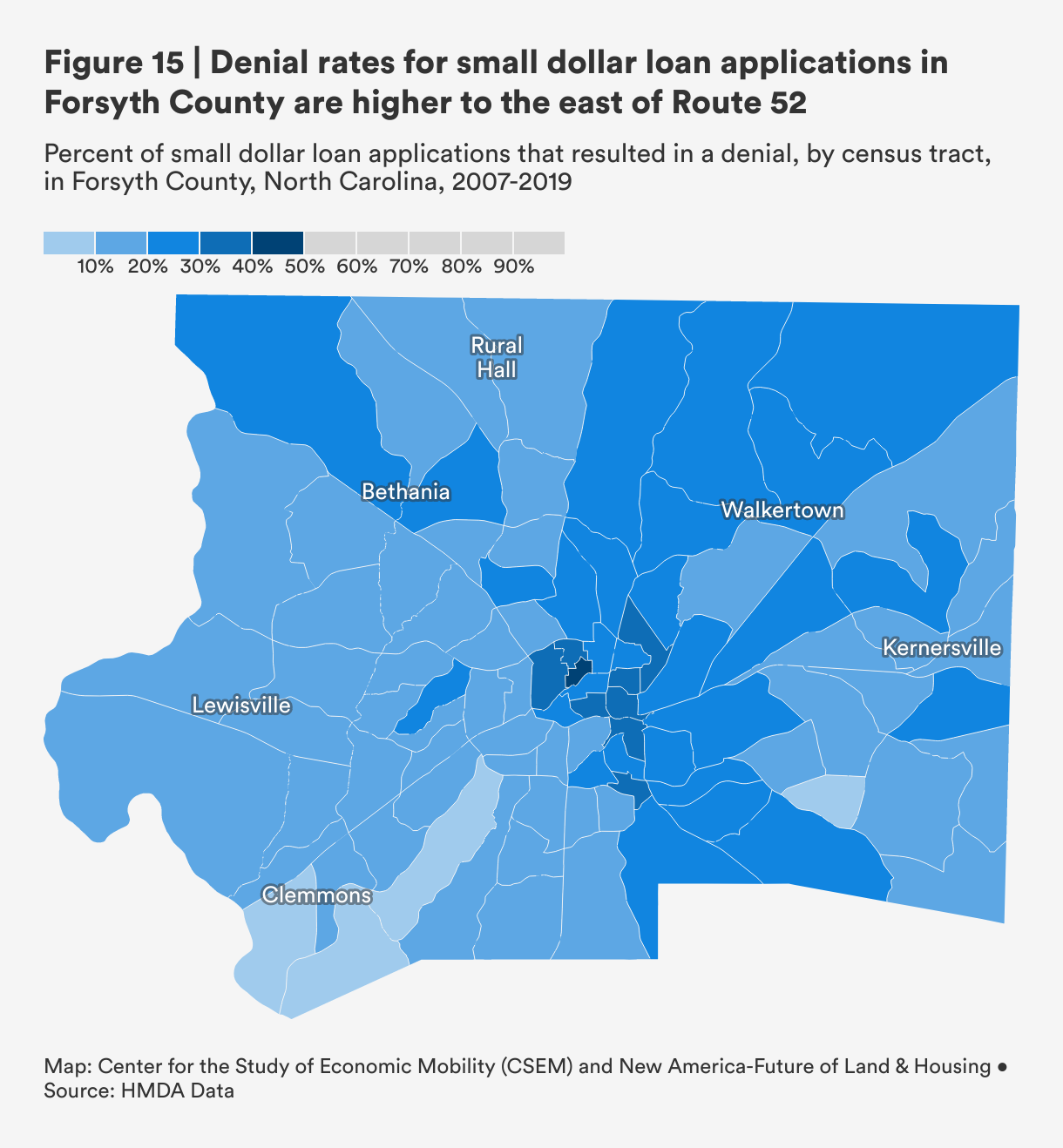

To understand any spatial patterns in denial rates, we mapped small dollar denial rates at the census tract level in Forsyth County, using data from 2007 through 2019. Figure 15 shows that neighborhoods near the city center and in East Winston tend to experience higher small dollar loan denial rates than the rest of the county. While the average small dollar denial rate in Forsyth County across all loan markets from 2007 to 2019 is around 20 percent, some census tracts, notably those in and around East Winston, have denial rates ranging from 30 to 40 percent.

In Forsyth County, small dollar originations are low relative to originations of larger loans and small dollar denial rates are high relative to large loans. Further, we see that neighborhoods in and around East Winston have both a higher concentration of small dollar housing stock (see Figure 12) and higher small dollar denial rates (Figure 15 above). It's not surprising that we also observe that these areas also have higher shares of investor-owned housing stock and lower homeownership rates in these neighborhoods as well.

While it is critical that communities are protected from the kind of predatory lending that led to the immediate collapse in home values in 2008, regulations keeping families from obtaining reasonable mortgage loans may be going too far in the other direction.

Small Dollar Loan Applicants: "High Touch, High Need"

Several Forsyth County lenders discussed how processing loans for low- to moderate-income applicants often requires high-touch, high-need engagement. Relative to higher-income applicants, lenders and real estate agents reflected on how low- and moderate-income applicants are more likely to experience changes in employment or financial circumstances. And these shocks, even if slight, could jeopardize the likelihood of an application ending in origination, as any financial change in an applicant’s life, whether to employment status or student loan payments, impacts an applicant’s debt-to-income ratio.

One local lender who focuses exclusively on low- and moderate-income buyers explained that many of these applicants are purchasing homes at the maximum amount they qualify for; if they go any lower, the available housing stock shrinks to the point where finding viable housing in good condition may become impossible. As a result, their debt-to-income ratios are already near or at the maximum permitted level by the lender, and “little things like [changes to the taxes or homeowner’s insurance] can be hard stops” for an already-sensitive loan application.

The possibility that a buyer’s financial circumstances could forestall closing could also contribute to some agents and lenders' hesitancy to work with low- and moderate-income buyers. According to one Forsyth County real estate broker, “[Agents] get discouraged [from selling homes under $100,000] because the lower income borrowers are more difficult to close. They have more nuances in their finances because they are more reliant on credit in their day to day lives.”

Mortgage Standards for Local Homeownership Assistance Programs in Forsyth County

Similar to the misalignment between FHA standards and small dollar homes discussed in the previous section, agents and lenders expressed concern over the misalignment between the existing housing stock in Forsyth County and the eligibility criteria for state, county, and city homeownership assistance programs.

The state, county and city governments in North Carolina, Forsyth County and Winston-Salem offer homeownership assistance with differing eligibility criteria and levels of assistance. These programs can be layered on top of each other and paired with FHA or conventional loan products to make financing more viable for low- and moderate-income buyers. Agents, lenders and housing leaders all noted that the need for repairs on small dollar homes and homes that are more likely to be affordable for low- to moderate-income buyers disincentivizes sellers from accepting buyers relying on FHA loans or local down payment assistance programs, pushing them towards conventional loans or cash offers instead.

The Affordable Homeownership Opportunity Program (AHOP) and the North Carolina Housing Financing Agency (NCHFA) Community Partners Loan Pool (CPLP) both offer down payment and closing cost assistance for low- and moderate-income Forsyth County residents. These programs offer generous funding, with maximum loan amounts often qualifying eligible buyers for homes up to $200,000. However, these programs also include rigorous home inspections, requiring that every item detailed in an inspection report be addressed by the seller before closing.

Some affordable home ownership programs have a recommended 10 year age cutoff to ensure a home is in good condition, but only 7.3 percent of homes in Forsyth County were built after 2010.

To increase the likelihood that homes pass inspection, CPLP recommends that a home must either be newly-constructed or in like new condition, using a 10 year age cutoff as guidance. According to 2019 Census data, only 7.3 percent of homes in Forsyth County were built after 2010. In effect, this eligibility criteria further constrains the supply of homes that buyers using local affordable homeownership programs can purchase. Many developers and housing leaders we spoke with also noted that new construction in Forsyth County is unlikely to be affordable for low- and moderate-income families, suggesting that existing housing stock is currently the only viable option for homeownership.

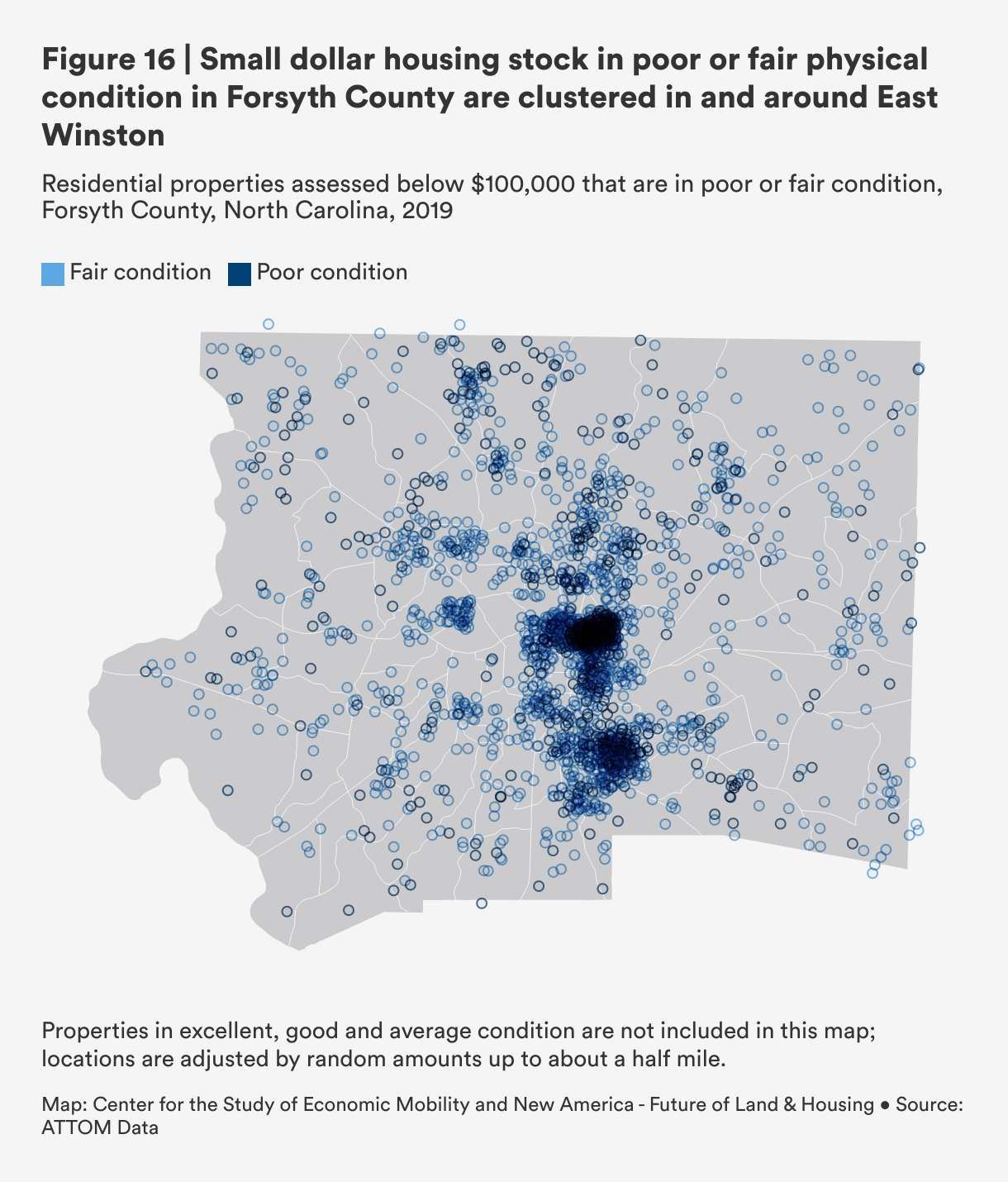

To better understand how small dollar housing stock in relatively worse off condition is concentrated, we map small dollar homes assessed as having below-average (either fair or poor) physical condition in Forsyth County, using 2019 data.2 Figure 16 shows that Forsyth’s stock of small dollar homes that are assessed as having below average condition are most frequently found in and around East Winston.

Agents, lenders, and housing leaders all emphasized that most homes that are affordable for low- and moderate-income residents are typically not move-in-ready, and generally require some level of repairs, anything from minor fixes to major structural rehabilitation. Of these homes, interviewees emphasized that homes under $100,000 are in the worst condition. A Winston-Salem realtor who works with bank-owned properties noted, “If a house is sitting on the market, and it’s coming in at $80,000, and that’s what it’s worth, you’ll typically have $25,000 to $30,000 worth of repairs.”

These local mortgage standards—designed to protect both the lender and the buyer—are instead disincentivizing sellers from selecting buyers relying on local loan products and assistance programs. Describing how Forsyth County’s highly competitive housing market intensifies this dynamic, one agent added, “This is an especially important problem in this market, because sellers can always find another buyer.”

Cash (and Conventional Loans) are King in Forsyth County

Intense competition over homes in Forsyth County equates to what is known as a seller's market, in which sellers have the power to select the offer on their home that best fits their needs. For most sellers, this means balancing the bid price with an offer that allows them to close quickly with as much certainty as possible.

Real estate agents, mortgage lenders, and housing leaders we spoke with in Forsyth County emphasized that the lack of affordable housing in decent condition is one of the biggest barriers low- and moderate-income buyers face. While the supply of homes in good condition is more constrained at the bottom of the market—acutely so for homes below $100,000, they said—the lack of housing impacts buyers with budgets up to $200,000.

“Most sellers are looking for the best offer with the least amount of work.” — Forsyth County real estate agent

Several agents discussed how a seller’s market was evident in the intensity of the bidding wars in Forsyth County, notably on affordable homes in good condition. One agent shared that one home selling for $150,000 received 65 offers. While the number of offers typically decreases as the cost increases, agents noted that more expensive homes, $300,000 and above range, could still expect to choose among several offers, even if not quite as many as on small dollar homes.

Cash vs. Mortgage Transactions in Forsyth County

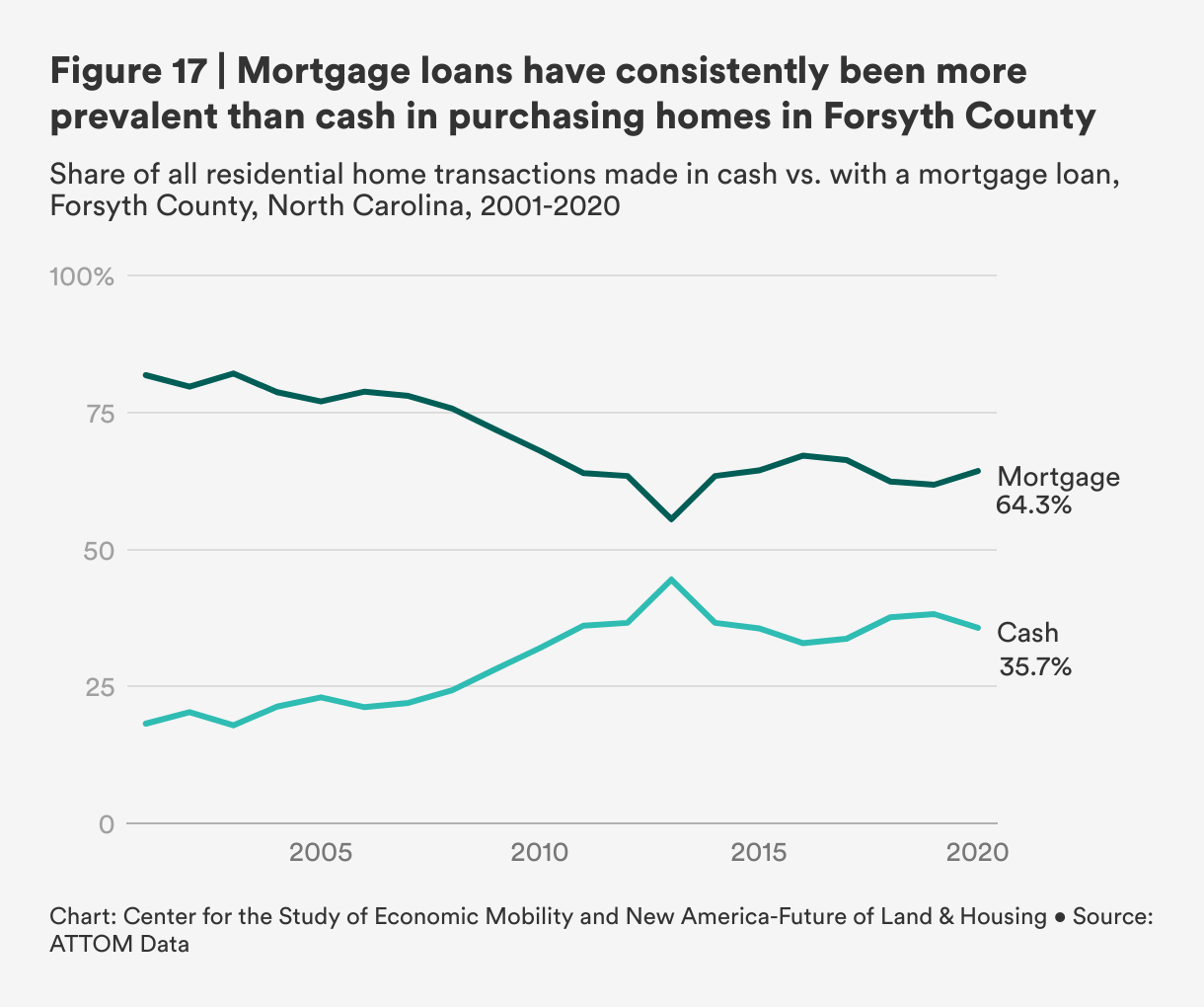

As discussed in the previous section, homes purchased with cash allow for the fastest and surest pathway from contract to close, and homes purchased with conventional loans tend to close more quickly than buyers relying on FHA loans. To understand trends in payment methods used in Forsyth County, we explore the share of residential home purchases made with cash versus with a mortgage over a 20 year time period in Figures 17 and 18 below. The share of homes purchased with cash is the inverse of the share of homes purchased with a mortgage (see the technical appendix for more details).

Figure 17 plots all residential homes purchased in Forsyth County from 2001 to 2020, by method of payment: cash or a mortgage loan. Over this time period, homes purchased with mortgage loans has decreased slightly and the use of cash has increased slightly, but at no point in the last 20 years have more homes been purchased with cash than with a mortgage in Forsyth County. In 2020, cash purchases accounted for 35.7 percent of all transactions, while the use of mortgage loans accounted for 64.3 percent.

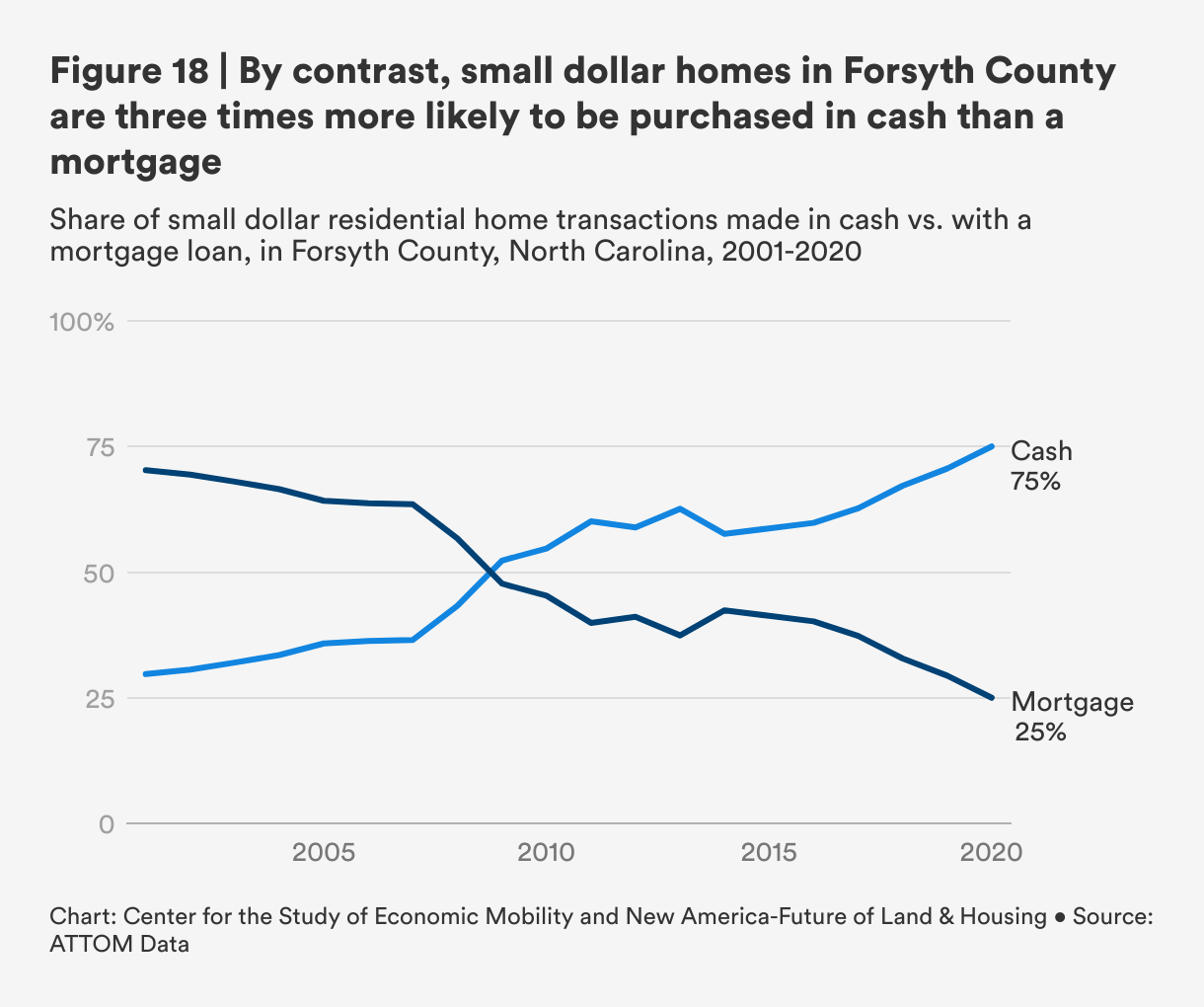

This payment story looks different among small dollar homes, however. Figure 18—which plots the same information as Figure 17, but only among homes below $100,000—shows that in 2001, only 30 percent of small dollar homes were purchased in cash, but the use of cash to purchase small dollar homes has steadily increased over the last two decades. Between 2008 and 2009, the share of homes purchased in cash overtook the share of homes purchased with a mortgage, and after steep increases between 2014 and 2020, cash purchases now account for 75 percent of the small dollar home market.

Seventy-five percent of small dollar homes in Forsyth County are now purchased with cash, up from 30 percent in 2001.

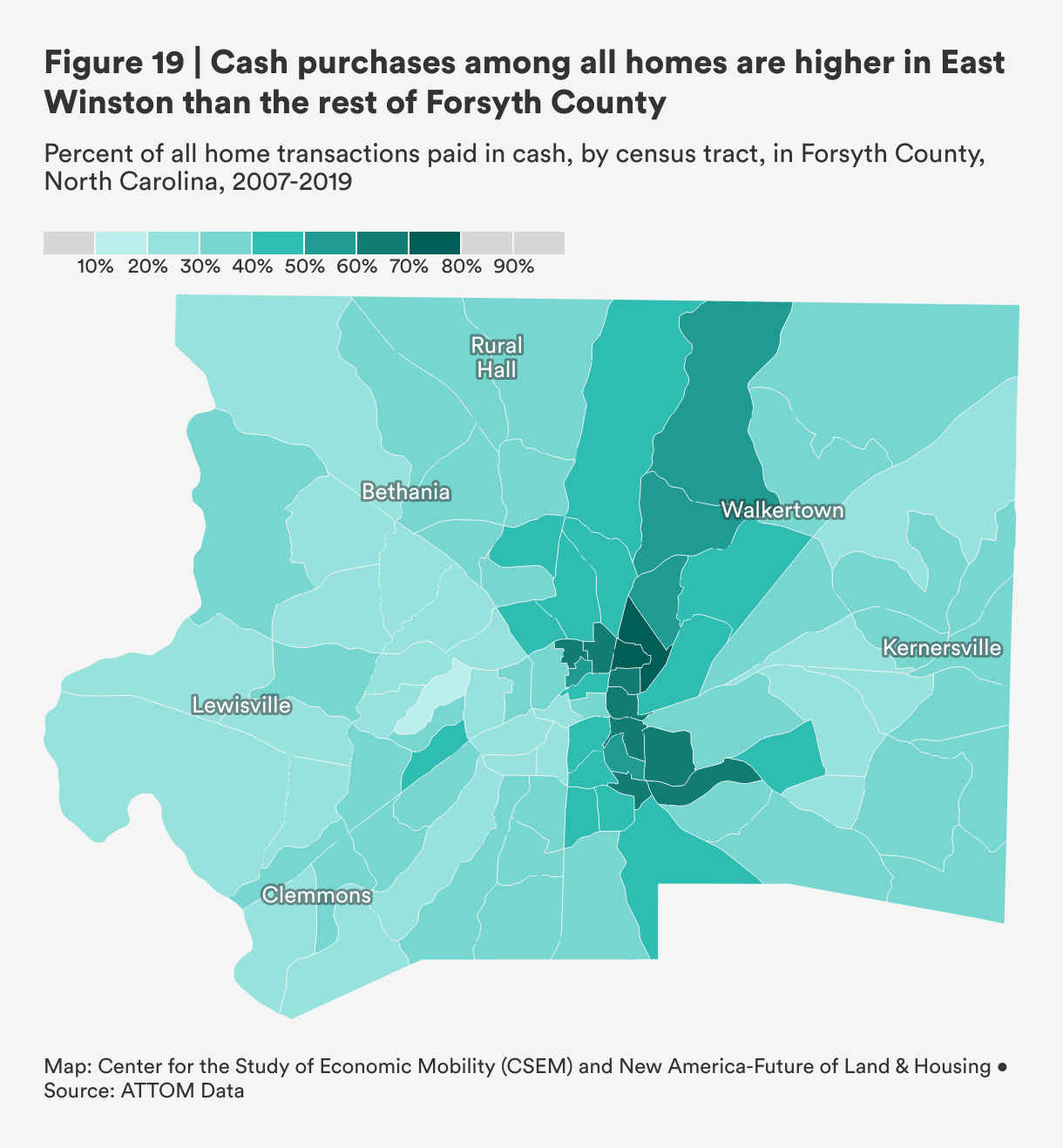

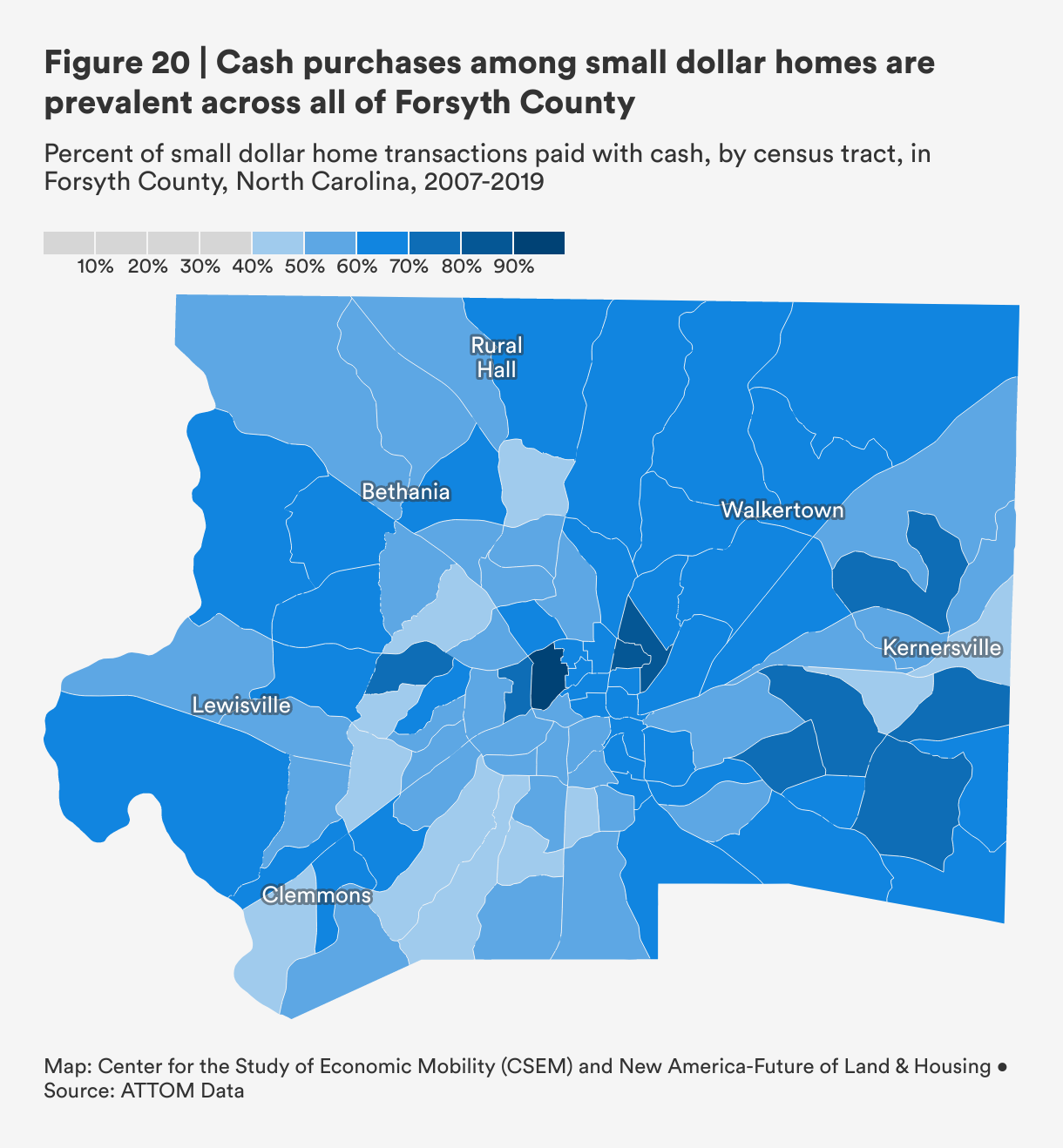

To understand where cash purchases are most prevalent in Forsyth County, we use data from 2007 through 2019 to visualize the distribution of all cash transactions at the census tract level (Figure 19) and the distribution of small dollar cash transactions (Figure 20). Among all transactions, we see that census tracts in East Winston, and tracts located along the eastern corridor of Route 52, have the highest share of cash payments. Indeed, real estate agents and lenders we interviewed suggested that cash purchases in Forsyth County, notably in recent years, were becoming common among homes well beyond those costing $100,000.

By contrast, Figure 20, which shows the distribution of cash purchases only among small dollar homes, we see that census tracts near the city center and on the east side of Forsyth tend to have higher concentrations of small dollar cash purchases, though cash transactions for small dollar homes appear to be prevalent all across Forsyth County.

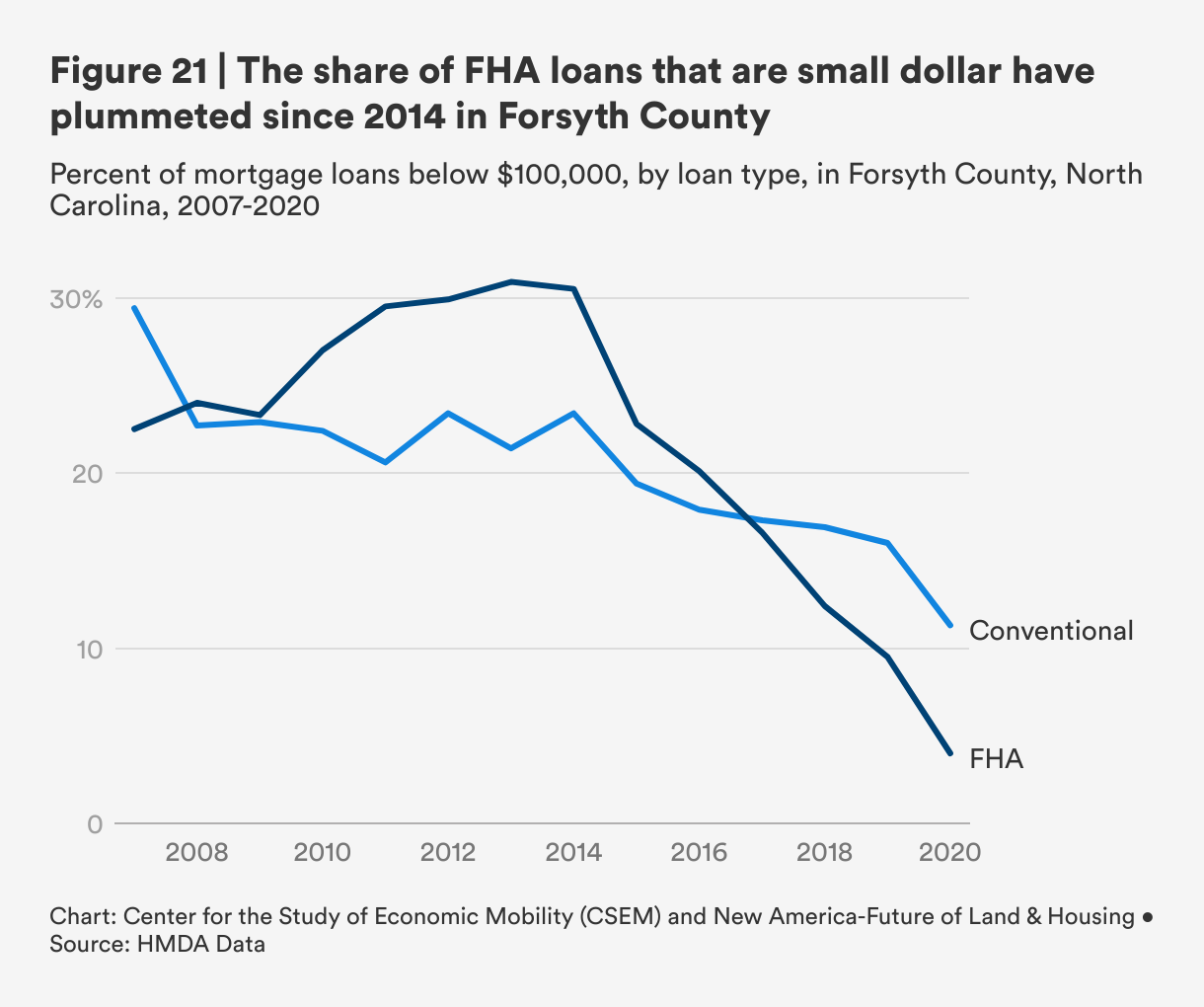

Conventional and FHA Small Dollar Loans in Forsyth County

After buyers with all-cash offers, sellers tend to favor offers that rely on conventional loans before FHA loans. We explore why this may be in subsequent sections, but explore the trends in these loan markets first.

Figure 21 plots the share of FHA and conventional loans that are below $100,000 from 2007 to 2020. Since 2014, the share of FHA loans and conventional loans has declined, albeit at different rates. Indeed, the share of small dollar mortgages secured with an FHA loan has plummeted since 2014. At their peak in 2013, 31 percent of all FHA loans in Forsyth were below $100,000; by 2020, this had dropped to around 4 percent.3 The rapid decline in FHA lending may be related to reliance on the False Claims Act, which sowed a level of uncertainty among FHA lenders (discussed in the previous section).

Describing changes to the FHA market, one Forsyth County real estate agent noted: “We call them the big box banks—SunTrust, Wells Fargo, Bank of America, Capital One, First Capital, First Citizens. All of those sorts of banks abandoned the FHA loan product [a number of years ago] because of the tightened regulations. Some of them have come back with altered products, but the FHA loan product… was pretty essential to the lower-income borrowers. A lot of banks just jumped ship.”

This rapid decline in small dollar FHA loans is particularly troubling given that these loans are explicitly designed to increase homeownership for first-time homebuyers, racial minorities who have faced discrimination, and low- to moderate-income buyers. Though the FHA is supposed to be a key lending channel for these groups, data shows that it underserves borrowers with small dollar loans. In addition to decreased FHA lending, in competitive markets where sellers have multiple bids, they may be increasingly disinterested in opting for buyers relying on FHA loans, which come with more requirements and take longer to close.

The Speed of Closing in Forsyth County: Home Purchases with a Mortgage Loan

Agents, lenders, and housing leaders we spoke with in Forsyth County estimated that the timeline from contract to close for purchasing a home could range anywhere from 30 days to four months. While the process for a buyer relying on a mortgage loan involves more steps than the process for a buyer using cash, the timeline is dependent on several additional factors, all of which can impact sellers’ decision-making. And given the competition among buyers for small dollar homes in Forsyth County, any extension to the timeline can hinder the strength of a buyer’s offer.

“It’s not just about whether [the timeline] works for my buyer. If you throw that to a seller, will they wait four months or will they reduce the price and sell to someone else?” – Forsyth County real estate agent

The main factors that agents and lenders discussed were: the type of loan, the type of lender, layering a mortgage loan with local homeownership assistance, and the condition of the home.

- The type of loan. Given the mortgage standards on FHA loans and stricter requirements for appraisals and home inspections, conventional loans were recognized as having faster turnaround times, typically around 30 to 45 days while FHA loans take closer to 45 to 60 days.

- The type of lender. All mortgage loans, regardless of whether they are conventional or FHA loans, are issued by approved lenders at banks, credit unions, mortgage companies or other financial institutions. While agents and lenders we spoke with noted that credit unions in Forsyth County offer flexible terms and alternate financing options, some also noted that they typically move slower than loans issued through banks or mortgage companies.

- Layering a mortgage loan with local homeownership assistance. As discussed earlier, the state, county, and city governments in North Carolina, Forsyth County, and the City of Winston-Salem offer homeownership assistance with differing eligibility criteria and levels of assistance. These programs can be layered on top of each other and paired with FHA or conventional loan products to make financing more viable for low- and moderate-income buyers. According to Forsyth County agents and lenders, utilizing these programs, and coordinating among the various departments that administer them, can extend the timeline substantially, taking anywhere from two to four months.

- Condition of the home. The condition of the home is the biggest factor for a delayed timeline. We explore this further in the next section.

Streamlining the Homebuying Process: Foregoing Inspections and Appraisals

Homes that are affordable for low- and moderate-income residents in Forsyth County are typically older, in worse condition, and have more structural or foundational issues than more expensive homes. If buyers are also relying on FHA loans or local homeownership assistance programs that have stricter standards for the condition of a home, this can cause significant delays in the loan approval process, notably during appraisals and inspections.

Forsyth County’s first-time homebuyer program, AHOP, requires that homes are inspected by a licensed home inspector, and any repairs needed must be performed by the seller before closing. After the required home inspection, buyers may have to bring in third-party specialists to assess any structural issues that came up, prolonging the timeline. Appraisals can also inject a great deal of uncertainty into a mortgage loan approval process as failure to appraise for the selling price can be grounds for a lender to deny a loan.

Cash buyers, on the other hand, face no requirements around home inspections or appraisals. Even when a cash buyer opts to commission a home inspection or appraisal, the ability of the transaction to move forward does not necessarily hinge on what is returned in an inspection or appraisal report as it would for a buyer relying on a mortgage loan, especially an FHA loan or a loan layered with a local affordable homeownership program.

Differing Home Preferences for Investors vs. Owner-occupants

Purchasing a home is an economic investment for any buyer, regardless of whether they use cash or a mortgage loan. However, Forsyth County interviewees did discuss some key differences in the criteria for choosing a home among owner-occupants and investors. For many owner-occupants, purchasing a home is an emotional decision that requires weighing competing priorities. For many investors, decisions about which home to purchase are based on economic calculations alone, and provide more freedom of choice. While none of this criteria is concrete, it can further narrow housing options among the already limited stock available for owner-occupants.

Condition of the home. Many low- and moderate-income owner-occupants have a preference for move-in ready homes that only require minimal repairs. For some owner-occupants, even minor repairs can wipe out a lifetime of savings, and that is to say nothing of needing to fix major structural damage. Investors, however, are more likely to purchase homes as-is and consider homes in poor or average condition to be ripe for investment. Investors tend to have the resources and knowledge to take on these repairs efficiently and at scale. However, preferences around the condition of the home depend to some degree on the financial resources of an owner-occupant or investor; ensuring that a home is safe and in good condition for one's family or future generations could translate to a willingness to invest as many resources as possible.

Location of home. Neighborhood characteristics, including access to high-quality schools and jobs, adequate public transit, and access to other resources matter a great deal to owner-occupants. Many homebuyers living in neighborhoods in Forsyth County that have experienced public and private disinvestment often hope to move out of these neighborhoods to ones that have greater access to opportunity. These considerations are less relevant to investors who intend to either sell the home or rent it and make a profit.

Citations

- See source">Technical Appendix for more information regarding foreclosure rates.

- The condition of a property is based on a rating system for a property’s overall physical condition, assessed at least every four years by Forsyth County. The rating system takes into account the maintenance level one would expect in a dwelling place of that property’s age. The ratings are: excellent, good, average, fair and poor. A property that is fair or poor is a property that has more than the typical “wear and tear” and shows more than the ordinary level of maintenance and upgrades based on the property’s age.

- To ensure these trends are not just the result of growth rates in large FHA loans outpacing growth rates in small dollar FHA loans, we also assessed the number of originations over time. This revealed that this is not the case, and in fact, the total number of small dollar FHA originations has been declining since 2015, while the total number of large FHA originations (more than $100,000) have remained fairly constant over this same time period. Small dollar originations of conventional loans, on the other hand, have been steadily growing since 2015, though the growth in larger conventional loan originations has been much faster, resulting in the declining overall share in small dollar conventional loans.

Increasing Access to Small Dollar Mortgages: Potential Solutions

Understanding the challenges facing potential buyers in need of small dollar loans, and how these challenges interact with one another, allows us to assess existing solutions and develop new ones that take into account the full scope of the issue. While this report does not include a comprehensive discussion on potential solutions, we raise ones that are particularly relevant to the challenges laid out in this report, at both a local and national level.

Before getting into the solutions, it is important to note that many of the challenges that buyers are facing do not stem from the small dollar mortgage market or even the housing system. In today’s highly competitive market, part of the challenge is that the playing field is stacked against low- and moderate-income buyers not only because of a lack of financing, but because these buyers do not have extra cash on hand to compete or conduct repairs, due in large part to stagnant wages and skyrocketing rents. If homeownership is becoming a game of how much a buyer is willing to risk, what happens to those who cannot afford to take such a risk? They are increasingly left behind.

Ultimately, it takes money to compete for a home, and thereby build wealth, which in turn leads to more money. When asked about the most promising solutions for low- and moderate-income buyers in Forsyth County, it is perhaps unsurprising that many responded with the same thing that has kept many low- and moderate-income buyers out of the market for homeownership in the first place: more money.

Developing Flexible and New Loan Products

As discussed, regulations implemented in the aftermath of the Great Recession may be disincentivizing lenders from writing small dollar mortgages. Streamlining the mortgage loan process and creating new loan products to accommodate small dollar loans would help ease the flow of mortgage credit and is an important component of a robust federal and local response. The existing mortgage system is long and prohibitively expensive. By automating the underwriting process and reducing the time it takes to review borrowers’ finances, costs may be reduced, allowing more lenders to offer smaller loan sizes.

Most mortgage loans issued in the United States are made by non-bank lenders, including credit unions, community development financial institutions (CDFIs), and other mortgage lending companies. The same is true in Forsyth County: according to 2019 HMDA data, nearly 75 percent of loans were issued by non-bank lenders. Whereas many lending institutions are unable or unwilling to write mortgage loans below a certain threshold, some financial institutions like credit unions offer flexible financing terms that make them more favorable to extending small dollar mortgages.

According to one Forsyth County lender, credit unions have greater flexibility in their lending practices, enabling them to offer more accessible products than banks, such as 100 percent financing home loans and portfolio loans. However, knowledge among real estate agents in Forsyth County that credit unions may offer products not offered by banks is not widespread, and the barriers to entry are higher for credit unions than for banks. Credit unions are one example, but there may be other sources of funding for local banks and CDFIs to support small dollar lending.

Alternative loan products may also be a viable avenue for redressing existing barriers to financing a mortgage. For example, the Neighborhood Assistance Corporation of America (NACA), which formed amid the fallout of the 2008 financial crash, disregards loan applicants’ credit scores and offers below market interest rates.

Some banks which initially shied away from small dollar lending after the passage of Dodd-Frank have since returned to the small dollar market with revised loan products. One agent discussed the Community Homeownership Incentive Program (CHIP) loan product offered by Truist Bank, designed for lower-income neighborhoods. If eligible, “they offer 100% financing which is actually better than what FHA is offering.”

And given the major decline in FHA small dollar loans and the important role they serve, revisiting FHA processes to ensure the agency is serving its intended purpose is critical. This includes ensuring a wider array of options for purchasing and renovating older homes and homes in need of repairs, both through FHA and other loan products.

Leveraging the Community Reinvestment Act

In direct response to redlining and other discriminatory practices, the 1977 Community Reinvestment Act (CRA), is intended to guide commercial banks towards serving the credit needs of low- and moderate-income communities. The CRA holds a lot of potential to leverage the role of banks and other financial institutions to ensure that the needs of homebuyers looking for small loans are met.

At the same time, agents, lenders, and housing experts in Forsyth County, reported that, in actuality, some “[banks] are doing what is required but they are not doing what the spirit of the CRA intended.” In some cases, financing new development in low- and moderate-income communities is sufficient to satisfy CRA requirements, even if it is unclear whether this development constitutes community reinvestment as outlined in the CRA. In other cases, banks can hold community events and other outreach initiatives, suggesting that there are several non-lending related ways that banks can meet CRA requirements that may not manifest in wealth-building opportunities.

Certain banks have offered programs for qualified borrowers in order to meet CRA requirements, such as a 100 percent financing home loan with no mortgage insurance or down payment, suggesting that leveraging the stipulations of the CRA could be an effective means of compelling banks to accommodate low- and moderate-income borrowers, but may not be utilized to its full extent.

Certain banks operating in Forsyth County have offered programs for qualified borrowers in order to meet CRA requirements, such as a 100 percent financing home loan with no mortgage insurance or down payment. This suggests that further leveraging the stipulations of the CRA could be an effective means of compelling banks to accommodate low- and moderate-income borrowers, though it may not be utilized to its full extent.

Addressing Misaligned Incentives for Lenders, Agents, Buyers, and Sellers