Table of Contents

- Introduction: Problems with IRS Benefit Delivery and Goals of Reform

- 1. Immediate Technical Fixes

- 2. Create A Modern, Government-Run Tax Filing Option, Starting With “The Portal”

- 3. Statutory Simplification: Restructure EITC/CTC and Redefine Child

- 4. Advance Periodic Payments: A Critical Step that Requires Careful Implementation

- Conclusion

3. Statutory Simplification: Restructure EITC/CTC and Redefine Child

The structure of the EITC and CTC today is arguably more the product of historical flukes and path dependence than reasoned policy design. Both credits have been periodically and independently expanded over the decades, while remaining grounded in the basic and unchanging framework of IRS tax filing. The result is a confusing tangle of different rates and phaseouts, and an arcane and dense set of family and income rules that is hard enough for policymakers to wrap their minds around, let alone average families.1 This submerged state hides government policy from its own citizens, drives families scared of making mistakes to use predatory tax preparation services, leads families to commit unintentional fraud and become subjected to invasive audits (which themselves discourage families from claiming credits in future years), and sometimes even fails to allocate benefits to the right recipients.

The complexity of the rules also makes it difficult to take popular steps to improve administration. Advocates of late have made a particular priority of advancing periodic payments of the CTC (and, to a lesser degree, the EITC) throughout the year, a pilot version of which is in the American Rescue Plan. But advance periodic payments require either a daunting amount of paperwork from overburdened low-income families, or a reliable process to automatically detect eligibility levels throughout the year—and the latter is significantly stymied by the rules’ complexity. The first step towards an automated and timely benefit disbursement system is a simplified code.

This section only gestures to two of the major changes that would be required, both of which have long been endorsed by scholars and advocates. Further research is needed to solidify the details of these proposals. Moreover, these fixes require significant and complex legislation. But the effort would pay dividends in clarifying the tax code and streamlining the data required to disburse payments, thus making possible aggressive implementation measures.

3.1 Harmonize and Improve the Definition of Child across Tax Code Provisions

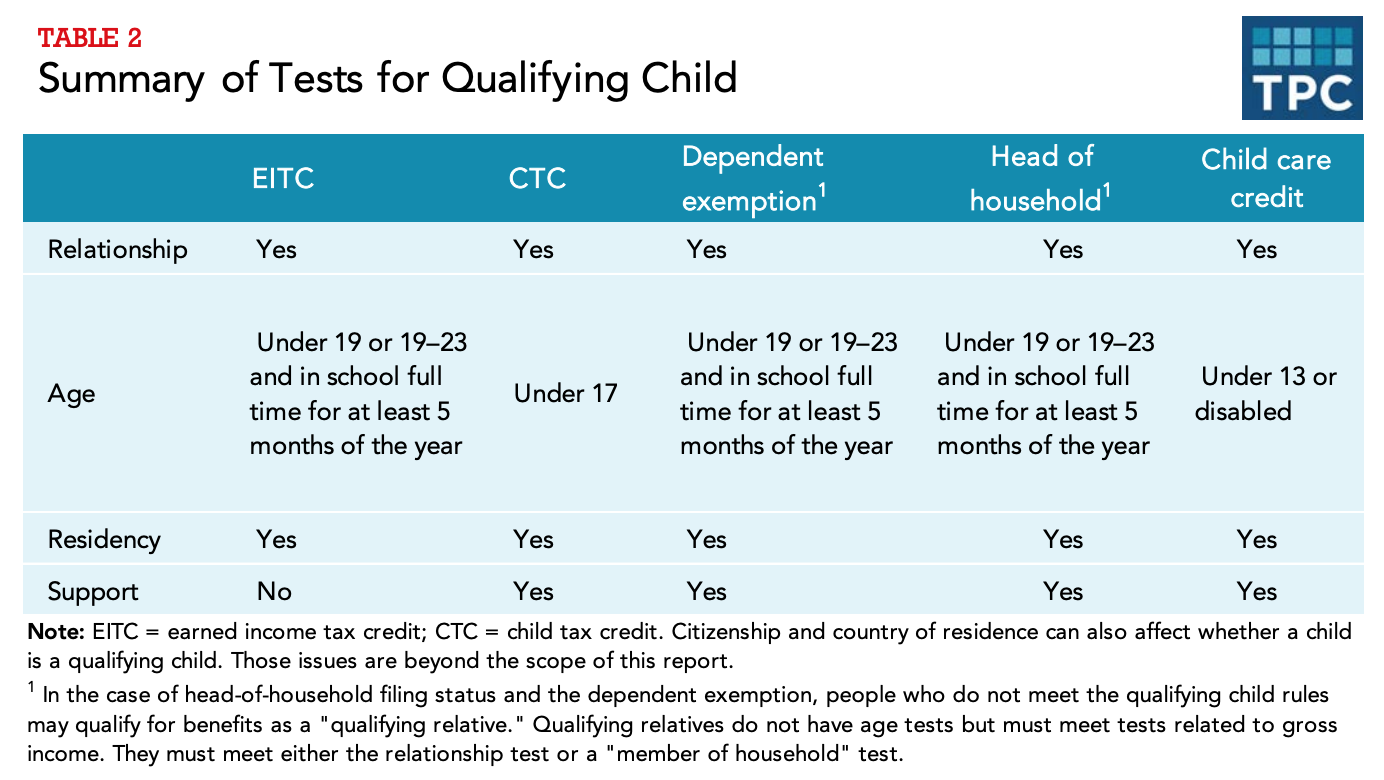

Currently, different tax provisions use slightly different definitions of child, needlessly complicating the code and allowing taxpayers to accidentally claim one credit and not another. Elaine Maag et al (2016) summarize the current status quo in the below table. Because of the misaligned definitions, taxpayers must separately claim each relevant credit, and read all the associated instructions, rather than defining once and for all which children they have.

Still worse, though, these complex and opaque definitions tend to fall apart when faced with the realities of non-traditional modern family structures, with the vagaries of the law denying taxpayers EITC eligibility for minors who are, for all intents and purposes, their children. This misalignment was illustrated by Cowan v Commissioner. Jean Cowan, the plaintiff, had effectively claimed her son’s son—her grandson, who lived in her home and whom she supported—as a qualifying child for EITC purposes. But Cowan had never legally adopted her son, whose guardian and de facto parent she had been from the time he was six weeks old. As such, the grandson was technically not her blood relative, and the IRS disallowed the credit. The court agreed. (See Leslie Book’s 2015 article in Procedurally Taxing for further detail on the case.)

Zooming out, it is clear that American families have a clear common understanding of whose children are whose; only around half of 1 percent of dependents are actually doubly claimed under EITC.2 But the IRS estimates that 15 percent of all EITC claims improperly claim a child3—that is, the IRS frequently purports to know that a given child does not belong to a given taxpayer, when real families rarely dispute whose child is whose. The program’s byzantine rules essentially manage to invent custody disputes where none actually exist.

The best solution is to move to a commonsense “primary caregiver” standard, in which families are given latitude to determine who claims a given child, and the IRS investigates only when multiple taxpayers claim the same child (or there is some other clear indication of fraud). (See the National Taxpayer Advocate’s 2016 report for details on the primary carer proposal.) The benefit should, in effect, follow the child, with the government needing no particular role in determining whose child it is except to resolve disputes. This international best practice4 would simplify the code and better reflect the lived experiences of taxpayers. Moreover, it would greatly reduce alleged fraud, thus easing alarm from the Government Accountability Office (GAO) and the Treasury Inspector General, reducing low-income families’ subjection to costly and invasive audits, and eliminating those audits’ follow-on impact in dissuading future tax filing and credit claiming.

This change would also set the stage for greater automatic detection of tax credit eligibility from other data sources. Unlike the current arcane set of rules, a primary caregiver test would bring the tax programs roughly in line with the definition used by other anti-poverty programs like Supplemental Nutrition Assistance Program (SNAP) and Medicaid, raising the possibility that the IRS could solicit data from state social service agencies to determine child relationships, saving families from doing such paperwork. Such data sharing could prove especially critical if efforts move forward to automate advance periodic payments of the CTC.

3.2 Transfer the Child-based Portion of the EITC to the CTC

At present, the IRS administers one program based on the number of children you have (CTC), and one program based both on the number of children you have and the amount you earn (EITC). This makes the EITC a conceptually confusing composite. A better approach would move the child-based portion of the EITC to the CTC, yielding one worker credit (what is currently roughly the childless worker EITC, based solely on income) and one child credit (an expanded version of what is currently the CTC, based solely—or primarily—on family size). Under this new regime, each credit would serve one purpose, clearly and transparently. Note that harmonizing the child definition across the two credits, as discussed above, is a necessary prerequisite for this reform.

This reform has been regularly advocated for years, appearing annually as a highlighted recommendation of the National Taxpayer Advocate (see for example 2016, 2019, and 2020 reports). There has historically been one major barrier to its implementation: holding all families harmless under such a restructuring would be challenging, and advocates are loath to leave poor households worse off after the change.5 The current political moment offers a reprieve from this bind: The Biden administration seeks to greatly expand the generosity of all of these credits, regardless. The American Rescue Plan will, for one year, increase the maximum childless worker EITC to $1,502 from $343, and the maximum CTC to $3,000 (or $3,600 for children under six) from $2,000.6 With all that extra funding in the mix, it is significantly easier to move some funds around without hurting any particular group compared to what they would have received last year.

The change would pay dividends in a simpler and more rational tax code, which achieves clear purposes and which taxpayers can understand, and which does not, for example, impose astronomical effective marginal tax rates on middle-income families due to the confluence of multiple different phase-outs. More importantly, however, it would facilitate easier delivery of the now greatly streamlined worker credit, and could simplify periodic payments. In the new regime, the worker credit (formerly childless EITC) would be based exclusively on income, with no need to collect more complex household structure data. As the IRS has detailed income data already, the realignment would free the agency to make payments based on information it already has on hand. And it would mean that, to the degree the IRS has to wait until later in the filing season to reconcile child claims under the new child definition, the worker credit would not be subject to any such delay, and could be paid as soon as wage data are confirmed.

Finally, the realignment would enshrine the family credit more clearly as what many advocates believe it should be: a true child allowance, not one of two tax arcane credits geared towards making it more affordable to raise children. Congress may even consider transferring administration of this new family credit from the IRS to the SSA, making explicit the program’s role as a (nearly) universal entitlement. The IRS, meanwhile, would continue administering the worker credit, given that credit’s more precise reliance on income data.

Lawmakers and advocates rightly tend to focus on program expansion rather than restructuring when there is political will to make changes. But, confusing programs exact costs over time, and, as multiple programs seek to serve the same population, poor design can diminish their reach and impact. If policymakers agree that the current EITC/CTC structure is misaligned and outdated, and is not one that anyone would choose if starting from scratch—then perhaps it is an opportune moment to right that wrong.

Citations

- Robert Greenstein, John Wancheck, and Chuck Marr at the Center on Budget and Policy Priorities write that the “EITC is one of the most complex elements of the tax code that individual taxpayers face,” source , while the Tax Foundation writes that it is “bogged down with some of the most complicated eligibility requirements in the tax code” source. Mark Mazur, then at the Tax Policy Center, testified to Congress in 2017 that: “There is a sense among taxpayers and tax policy observers that the tax code is too complex for ordinary Americans to understand their tax obligations and comply with them. This sense of extreme complexity is evidenced by the robust tax preparation and tax software industries, as well as a belief among taxpayers that they are missing out on benefits being claimed by others… Congress…is complicit in this sense of growing complexity; over the past three decades,increasing amounts of social policy have been run through the tax code. While this can be an efficient way to deliver benefits to particular taxpayers, every one of these provisions carries with it eligibility rules and benefit calculations that can overwhelm taxpayers. This proliferation of tax expenditures itself fosters complexity.” source

- See NTA (2019), p. 18, Footnote 82: source

- The 2014 IRS EITC Compliance Report, which is based on audits of a representative sample of returns, concludes that 50.2% of EITC returns (11.9 out of 23.7 million) have an overpayment (Table 1), and that 30% of EITC returns with known errors have a qualifying child error (Table 4): source

- Both Canada, source , and Australia, source , among others, use this type of standard.

- Specifically, any reasonable level of the new worker credit would be higher than the current childless worker EITC, and would thus require taking money from somewhere else—presumably from single parents with one child, whose benefits are comparatively generous under the existing regime.

- source