The Cash Assistance Implementation Playbook

Table of Contents

Abstract

The purpose of this doc is to outline possible technical approaches to supporting a cash assistance program. These findings were gleaned from 10 organizations from the nonprofit sector that participated in a design sprint on cash assistance with Google.org in September 2020.

The playbook is intended to help organizations (nonprofits or civic entities) that are considering developing their own cash assistance platform.

As opposed to presenting a single definitive approach on how to set up a Cash Assistance Program, the document presents a series of “plays” that different organizations have executed to provide funds to their applicants. Each organization’s play acts as an example of a nonprofit scenario that the audience might be able to identify with. For example, the National Domestic Workers Alliance’s Cities Program would exemplify a civic fund that other civic funds might be able to model.

The doc aims to both capture individual approaches as well as overarching insights taken from across the approaches taken by different organizations.

Acknowledgments

Thank you to the many contributors to this playbook including:

The New America team for laying the foundation with your state of cash assistance work previously published and for your interest in amplifying these technical best practices.

- New America’s New Practice Lab: Vivian Graubard, Nikki Zeichner, Cassandra Lyn Robertson

The Google.org Cash Design Sprint Participants and Contributors of this playbook for the important work you do everyday and for your willingness to sharing your expertise and insights across sectors including:

- One Fair Wage: Saru Jayaraman and Nika Soon-Shiong

- The American Red Cross: Barb Larkin, Julia Dailey, Joy Stanton

- Colorado Left Behind Workers: Mark Newhouse, Katrina Van Gasse, Ben Newhouse

- National Domestic Workers Alliance: Palak Shah, Tommy Tseng, Matthew Hogains

- Fund for Guaranteed Income: Nika Soon-Shiong, Nick Salazar, and Daphne Sigala

- Accelerator for America: Phil Chambers, Paige Sterling, Justin Yoshimaru

- GiveDirectly: Hans Sheng, Ashley Beale

- Family Independence Initiative: Jesús Gerena, Aaron Smith, David Henderson, Rae Oglesby

- Jain Family Institute: Steven Lee, Stephen Nuñez, Sidhya Balakrishnan, Alexander Jacobs

The pro bono Google.org Fellows who spent six months working full-time with NDWA resulting in the open source cash assistance platform and for the many Google.org teammates who contributed to the design sprint that resulted in these learnings:

- Google.org Fellows: Saj Reshamwala, Jonathan Cham, Ali Stanfield, Alan Blanco, Kevin Arthur, Richard Wu, Lirong Liu

- Google.org: Erin Hattersley, Rasmi Elasmar, Jen Carter, Hector Mujica, Alex Diaz

Editorial disclosure: This report discusses the contributions by various organizations from a co-hosted sprint with Google, which are funders of work at New America but they did not contribute funds directly to the research or writing of this piece. View our full list of donors at www.newamerica.org/our-funding.

Downloads

Introduction

[Building an open source Cash Assistance Platform] Domestic workers are the ones who take care of our children, our eldery, the disabled, they keep our homes and our offices safe and clean. And when the pandemic hit, domestic workers were particularly hard hit as they are excluded from the formal social safety net and government economic relief.

The National Domestic Workers Alliance (NDWA) has been focused on improving the conditions of domestic workers across the United States for the last 14 years which enabled them to see the outsized impact of the pandemic on this community and the need for immediate relief. In response, NDWA quickly formed a coalition of organizations, Open Society Foundation, Google.org, and local governments like Philadelphia to provide emergency cash relief to workers via their platform, Alia Cares.

To get this relief to vulnerable workers there were two needs: to raise more money and a technical platform to get it into the hands of workers. The Open Society Foundations provided catalytic philanthropic capital both to get into the hands of workers and to help establish the platform, Alia, for vulnerable and left behind community members.

The Open Society Foundations provided catalytic philanthropic capital to fund both emergency cash relief and financial support for NDWA to build a solution for vulnerable and “left behind” populations. Google.org provided grant funding to NDWA to support the Alia Benefits platform in 2017, so when NDWA needed immediate design, product management and engineering resources Google.org was ready to quickly step in. They deployed a team of seven pro bono Google.org Fellows, who worked full-time for six months on building Alia Cares (the cash assistance platform) and open sourcing the solution so that it can be more easily replicated.

In total, NDWA raised more than $30M, 7x their original goal, and used this platform to get cash to 50K individuals who’ve used it for food, rent, medicine, and other essentials. The platform is already having an impact beyond NDWA, in cities like Tucson and Philadelphia where community based organizations are distributing their own relief funds through the platform.

Addressing complex issues such as providing emergency financial relief to marginalized workers requires innovative solutions that leverage the expertise of multiple organizations and sectors, as we saw here.

[The Design Sprint] As the Covid pandemic continued, there was a growing gap in benefits for those most affected by the outbreak. City, state, and community-based organizations have filled this gap by raising and distributing emergency cash and providing a much-needed lift across the country. While many of the questions about what to consider while setting up a cash assistance program have been answered, the effectiveness of programs often relies on the technical implementation of a platform especially since nonprofits and civic entities often have limited access to technical resources. Google.org, Google’s philanthropy, heard from many of their grantees like NDWA, that there were shared technical needs across the sector and that programs like the Google.org Fellowship could help advance those shared solutions. In the case of NDWA, providing technical expertise meant NDWA could get cash to domestic workers quickly, thoughtfully, responsibly, and securely, and that local governments could do the same.

In September 2020, New America’s New Practice Lab, National Domestic Workers Alliance, and Google.org ran a five-day virtual design sprint workshop with 10 nonprofit organizations to identify if there were shared technical solutions that could benefit the sector and to capture technical best practices and opportunities to get relief quickly to those in need.

This is what participants set out to achieve during the design sprint and what they focused on each day:

This document presents different approaches taken by the participating organizations so that nonprofits, governments, and policymakers can learn from existing cash assistance programs. This document isn't meant to capture all the possible solutions or to make recommendations as to a single preferred approach, but rather to capture the learnings of ten organizations that have developed expertise through experience with providing cash assistance programs.

Editorial disclosure: This report discusses the contributions by various organizations from a co-hosted sprint with Google, which are funders of work at New America but they did not contribute funds directly to the research or writing of this piece. View our full list of donors at www.newamerica.org/our-funding.

Overview

Successful cash assistance programs can be broken into four key areas: applicant intake & approval, the application, payment integration, and ongoing support. In addition, many organizations documented how their program would interact with other civic entities with the hopes that their programs could act as case studies for cash assistance programs implemented at a larger scale by government organizations.

Intake & Approval

Intake, or the process of how you find, qualify, and verify applicants, has a downstream impact on both the applicant experience and how you can manage your organization’s data. When designing their intake process, organizations often took advantage of previously established relationships with both their direct clients and community-based organizations.

Automation vs. Speed in Implementation

- When designing for speed, it’s worth considering the impact intake might have on the effectiveness of your verification process and protection against fraud. Many organizations allowed for an acceptable amount of fraud risk in order to get cash assistance out to their applicants quickly to provide emergency relief.

- Investing in the automation of your participant intake can impact how quickly you get assistance to applicants. It can be tempting to introduce automated applicant approval from the start but waiting until a fully automated application is implemented before distributing funds can unnecessarily delay getting funds to those in need.

- To allow for a faster rollout, it was often helpful for organizations to include a manual step, or a gate, in the intake process. For example, in the National Domestic Workers Alliance Cash Assistance Platform, a human must manually click on a button that approves a batch of applicants at one time. This manual step allows the team to mitigate risk and catch unknown bugs within the platform without holding up deployment.

- Because you may not have direct contact with your potential applicants, identifying fraudulent applications in a digital cash assistance program can be difficult. Working with community-based organizations and allowing applicants to apply in smaller batches helped to keep the risk of fraud low for many organizations and allowed them to catch vulnerabilities quickly.

Application

Building an effective application extends beyond the interface and requires intentionality around how people will find the application, how the status of applications will be tracked, where the application will be deployed, make architectural decisions, and assure applicant security and privacy.

Interface Design and Respecting Applicants Privacy

- Because the payoff for completing a cash assistance application is high, it can be tempting to underinvest in the user experience of the application. However, these users are often in complicated or challenging circumstances so reducing friction for them is key to their success. For example, when the National Domestic Workers Alliance improved the look and feel of their phone number and access code entry fields, they saw an immediate increase in the number of applicants that were able to successfully complete their applications.

- Many seemingly necessary steps of an application are often redundant and should be removed to ensure that applicants can receive assistance securely and safely. For example, organizations often found that, with the help of their legal teams, multiple consent and agreement forms could be combined to reduce the number of steps to complete an application. While this change might sound trivial, these reductions in steps reduced the perceived difficulty of completing the application and improved applicants’ perceptions of the programs and supporting organizations.

- Organizations should avoid using complicated applications to reduce the number of qualified applicants as it’s an imprecise method for reaching applicants that are most in need. Instead, organizations should focus on identifying the fewest number of questions possible to quickly identify applicants that could best be served by their program.

- In order to garner trust in the community, it is critical to consider the dignity of the applicant throughout the process. For example, offering multiple languages and highlighting relationships with trusted CBOs consistently increased the rate of application completion.

Building Trust

- Some organizations saw drop-offs of 30-50 percent because applicants thought the cash assistance program might be a scam. Organizations found that reaching out to applicants via community-based organizations (CBOs) with established relationships with their clients was an effective way to get more potential applicants to trust the program.

Support and Documentation

- Regardless of how automated the application was, it was consistently helpful to have customer support available to answer questions throughout the process. Organizations often used a combination of chat and phone support, prioritizing chat support when possible and reserving phone support for more critical issues.

- Applicant-facing documentation on your platform should clearly state how data will be used and abide by state-level privacy laws including making it clear who is administering the fund.

- Effective management of the platforms and operational processes were critical to each organization’s ability to scale its assistance. For example, the National Domestic Workers Alliance developed internal-facing applications that would allow their customer service representatives to easily update applicant records during support calls.

Hosting and Data Management

- To reduce the amount of infrastructure you need to manage, the best place to host your application is in the cloud with a managed service. For example, NDWA’s cash assistance platform was built with Elastic Beanstalk on AWS, but this type of application can be deployed similarly with other infrastructure providers.

- No single platform was deemed best for tracking the status of applications and organizations sized their databases based on the size of their applicant base. For example, organizations with a smaller number of applicants often used simple spreadsheet-like databases while organizations with a large number of applicants would use larger databases with advanced features such as free text search.

- When determining a data management tool to use, it’s important to balance the accessibility of the interface with the ability to find specific data points or trends. For example, Airtable is an incredible tool to keep data structured and accessible, but is not great at complex queries.

Privacy & Security and Fraud

- Unfortunately, many professional hackers will target non-technical organizations because they believe it will increase their chances of finding vulnerabilities. This tendency means that data security is especially important for cash assistance programs.

- There are three generic types of fraud to be aware of:

- (A) Recipient fraud

- (B) Professional fraudsters/ hackers

- (C) Staff fraud

- Collecting more data increases both the risk of being a target of a cyber-attack and the cost of a successful cyber-attack. To minimize risk, only ask for the data that you need, and automate the deletion of data that is no longer needed (e.g. after applications have been processed)

- For example, different services you may be using in the cloud (payments, text messaging, analytics, etc) will likely be logging and keeping the data for a certain period of time.

- As much as possible, keep names and sensitive data within surfaces that you control.

- For example, you may be using a shared database with other teams/groups to store sensitive data. Realize that this data can be accessed by unknown individuals if you don’t have complete control over the service. As a precaution, managed cloud service providers will expose audit logs for data access (or similar), if properly configured.

- You may be able to implement certain types of access control on surfaces you control. These access limitations can help ensure sensitive data is only shared within your organization to those who actually need it. For example, someone on a customer support team might need to see name and payment status, but they don't need to see other stuff (e.g. physical location). If you’re using Google Docs, this can be done by curating the list of accounts information is shared with. If you’re using a more advanced backend, this can be done through the software’s setup or configuration.

- Regardless, simple reminders to staff about data security (e.g. erasing downloaded participant data, putting screen locks and passwords on devices with access) are always helpful.

- For extra-sensitive data, tools can be used to remove certain abuse vectors, like human misuse and access to data. For example, using a chatbot as an initial interface removes the human element and prevents unnecessary access to information.

- If you’re able, creating a “data inventory” early in the development process can be extremely helpful. By mapping out what data is collected from whom, and noting where that data is stored (and who holds access to that data), it’s easier to understand any potential threats or gotchas.

Payment Integration

Implementing payment includes making decisions as to how you’re going to distribute payment as well as what payment technologies you’re going to use. Each organization implemented a payment process that was different and was heavily influenced by the makeup of their applicant base and their preferred approach to receiving cash.

Meeting Recipients Where They Are

- Given that many applicants may be under or unbanked it’s useful to offer flexible payment options when possible.

- Regardless of the form of payment chosen, fund distribution must be discrete because of the potential for government audits.

- It was generally agreed upon that providing funds via no-fee debit cards is more secure than cash. Additionally, for unbanked residents, cashing checks sometimes involves payment of predatory fees.

- Some common payment platforms that were deemed successful are:

- ACH Transfers for the banked

- Money Orders that allow immediate access to cash

- Mastercard Akimbo

- Hyperwallet

- Prepaid debit cards

Ongoing Support

Ongoing support includes both an organization’s ability to ensure that applicants are able to make use of their cash assistance as well as helping the applicants engage with your organization in an ongoing way.

- Cash assistance programs can provide an opportunity to start a relationship with new clients while showing them your ability to meet their needs and ultimately build trust. For example, One Fair Wage uses initial interactions as an opportunity to see if applicants are interested in getting involved in organizing and advocacy while also offering them assistance.

Research Design and Policy Considerations

When thoughtfully implemented, cash assistance programs can serve as case studies for government and non-government organizations interested in running cash assistance programs at a greater scale.

- Pilots and guaranteed income experiments are acting as a crucial model for government organizations interested in offering cash assistance. Each additional well-documented cash assistance program provides insight into what does and doesn’t work when working to get assistance to those in need.

Additional Considerations and Opportunities

It was hard for organizations to measure demand, both generally and by specific location. This lack of clarity can make it hard for organizations to know if they’re distributing funds equitably or who they might be missing.

- Participating organizations agreed that they could benefit from a shared solution with a strong governance model to help each organization more effectively identify and verify applicants. A shared solution would help organizations identify potential applicants and also provide the data necessary to understand the impact of cash assistance programs at scale.

- Many organizations noted that, while providing cash assistance, there is a missed opportunity to refer applicants to other services, benefits, and funds they may qualify for. One nuance is that, if not done well, applicants can be off-put if they’re referred to programs that aren’t a good match for them. For example, an applicant that would benefit from cash assistance may not want or need help with financial literacy, and offering an applicant financial literacy classes could seem patronizing.

Conclusion

Cash assistance allows people to rebuild their lives on their own terms when distributed through effective, secure, and trustworthy technology. By understanding how organizations put cash in the hands of families who needed it at the beginning of the pandemic, we ensure that we are better prepared for future crises. The same technology can be used for new services, such as rental assistance, and adapted to the needs of both organizations and recipients.

Approaches

One Fair Wage’s Emergency Fund for Workers

Context

In 2-3 sentences, briefly describe your organization. What prompted you to start this cash assistance program?

We are a national service workers’ association, campaign, and organization seeking to lift millions of subminimum wage workers out of poverty. The workers who receive a subminimum wage today are disproportionately women of color and often ineligible for government benefits due to citizenship status. Since March 13, 2020, over 9 million restaurant and other service workers have lost their jobs; most are ineligible for unemployment benefits. In response, One Fair Wage launched the One Fair Wage Emergency Fund.

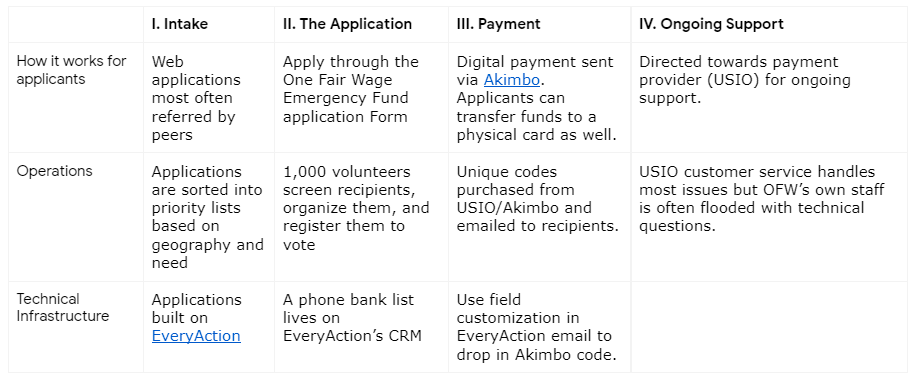

I. Intake

Qualifying Applicants + Verifying Applicants

How do you find, qualify and verify recipients?

Workers apply through the online Emergency Fund application form on our website. Our website has been shared in countless resource lists, and we have gotten hundreds of thousands of applicants. We distribute to those in more dire need, like parents, people who are facing a housing crisis, people who do not qualify for government assistance, etc. We verify applicants by asking for their Manager information, and a pay stub that shows their previous employment.

Why did you choose this approach?

We wanted to make sure that we weren’t creating high barriers that made applying to our fund difficult for workers who are faced with an unprecedented economic situation.

II. The Application

Application Experience

How do people find the application?

Predominantly they learn about Fund through peer referral (and initially through media coverage).

What information is needed?

No information is needed to receive funds, except for a mailing address and screening survey. We verify applicants by asking for their Manager information, and a pay stub that shows their previous employment.

How do they get approved?

1,000 volunteers screen recipients.

How, if at all, do they track their application status?

We track and screen applicants through EveryAction.

Why did you choose this approach?

Because our staff is familiar with EveryAction and it’s the database we use.

Hosting and Deployment

Where do you host your application? (AWS, GCP, Heroku, etc)

N/A

How are you tracking the success of the program? Are you using any tools, technologies to support this?

N/A

Security and Privacy

What are the considerations and tradeoffs related to security and privacy?

N/A

Customer Service

How do you support applicants and help answer their questions?

USIO customer service, our payments provider handles most issues.

III. Payment Integration

Payment Integration

How do you disperse funds to recipients?

We disburse funds through USIO Akimbo Now Mastercard prepaid debit cards.

What payment technologies do you use and why? (Paypal, Stripe, Square, Hyperwallet, etc.).

OFW uses USIO prepaid debit cards because they do not require ITIN or SSN, and give recipients the option to have a digital or physical card. We are able to administer the program through the USIO FIncentive portal.

What type of funds do you provide? (debit cards, cash, gift cards)

We provide prepaid debit cards.

IV. Ongoing Support

Are you providing additional or ongoing support to recipients? If so, in what way?

Yes, we organize workers and register them to vote. We are building an integrated platform to deliver services, build the movement, engage voters, and change the industry.

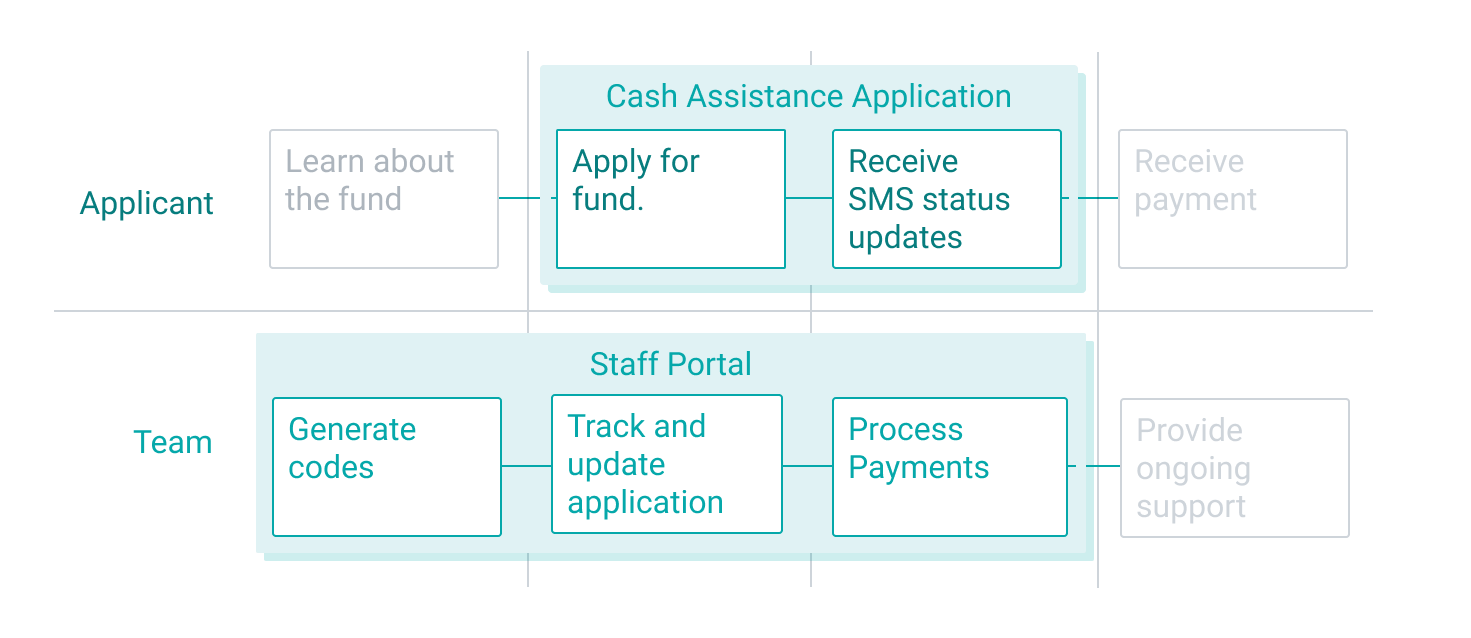

Summary Diagram

The diagram below was copied from the diagram you created for the Cash Assistance Design Sprint. Please feel free to make any updates or add more details where necessary.

Civic + Policy Consideration

[If applicable] What considerations did you make in the setup of this cash assistance program to involve government organizations or to impact policy?

Over a thousand volunteers have mobilized to call applicants, understand the policy issues which matter to them, and ask them to enlist five of their peers to vote. Distinct from other emergency relief or voter engagement efforts, we talk to our cash transfer recipients about the bigger picture, and how they can change the status quo. Less than a quarter of all applicants have never voted in an election. A pilot of our voter engagement program increased turnout by over 300 percent. With the right resources, our mobilization efforts have the unprecedented opportunity to address two urgent demands: economic security and electoral change.

Research Design

[If applicable] What considerations if any did you make so that others could learn from the project? If so, how?

We would emphasize the link to campaigns, and voter engagement.

Learnings

What might you do differently if you were to set up a similar assistant program knowing what you know now?

SPEED AND QUALITY OF VERIFICATION: We need faster ways for vetting workers that don't require documentation/proof that discriminates against or discourages undocumented workers. We need a way to confirm that people who they say they are do not rely on the word of owners and people who have denied workers decent pay.

ORGANIZING: People are coming to OFW for the Emergency fund, and we want to move them up a ladder of engagement in terms of organizing and advocacy, even if they are not selected for payment.

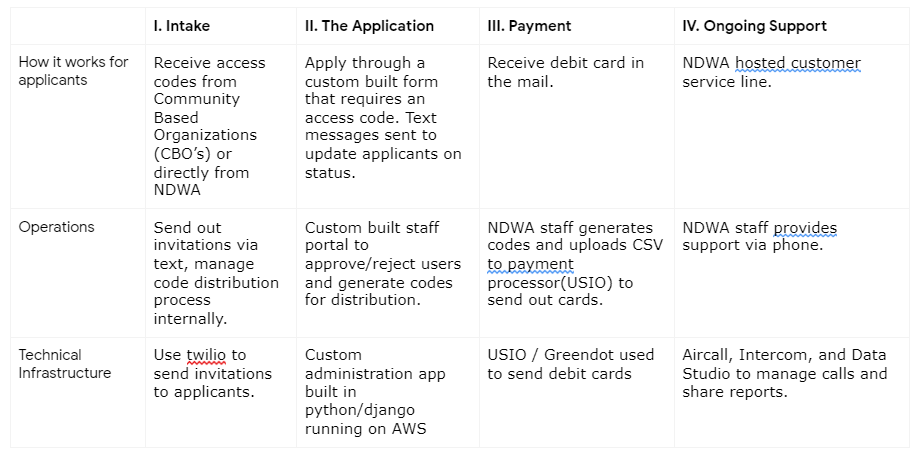

National Domestic Workers Alliance’s (NDWA) City Fund

Context

In 2-3 sentences, briefly describe your organization. What prompted you to start this cash assistance program?

NDWA is the nation’s leading organization fighting for the respect and dignity of domestic workers, who are the nannies, house cleaners and home care workers who work in our homes. Early in the pandemic we announced the Coronavirus Care Fund to provide emergency cash to domestic workers impacted by the pandemic, and raised more than $30m.

NDWA Labs, the innovation arm of NDWA, pivoted Alia, our benefits platform for domestic workers to distribute the Coronavirus Cares Fund. We were quickly contacted by cities across the United States who had raised their own funds and partnered with us to distribute their funds.

I. Intake

Qualifying Applicants + Verifying Applicants

How do you find, qualify and verify recipients?

Recipients of the Coronavirus Care Fund were found and qualified through our own membership, and the membership of our affiliates (NDWA is an alliance of more than 60 affiliates). Members were given an access code which verified their application in the system.

Recipients of the city funds were found and qualified by the cities themselves, which used their own intake processes and policies to decide on qualification requirements These recipients were also given an access code to verify their application.

Why did you choose this approach?

The success of this program relied on trust between organizations. NDWA has trusted relationships with our affiliates and their organizers, and cities relied on trusted relationships with organizations who found recipients and distributed access codes. The access code system enabled us to leverage those trusted relationships, while maintaining a verification system that we could confirm before distributing funds.

II. The Application

Application Experience

How do people find the application?

Through local outreach. Local organizations conducted their own outreach to community members, and applicants were given the application link with an access code to proceed through the form.

What information is needed?

Each city determined the information required for their fund, and the forms were customized according to the requirements of each.

How do they get approved?

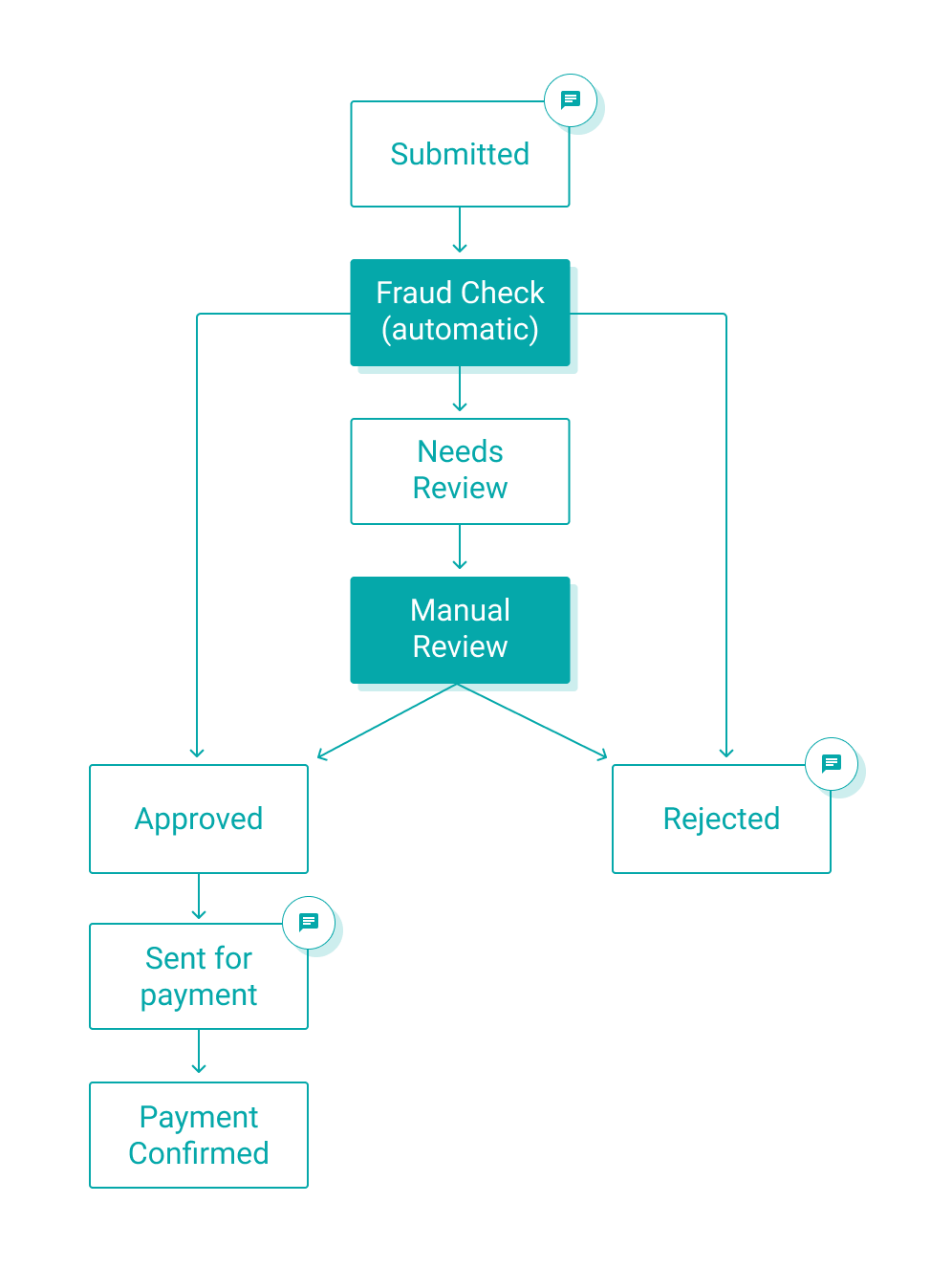

Approval takes place at the point of providing the access code to the individual. Once an application is received, the access code is verified and we run a fraud check before processing the application.

How, if at all, do they track their application status?

We update applicants when we have received their application, when it has been approved or rejected, and when the payment has been sent.

Why did you choose this approach?

Keeping applicants updated on their application status created a better customer experience. We also found that many of the applicants depend on text messaging as their primary communication channel. Our studies found many of our applicants don’t use email.

Hosting and Deployment

Where do you host your application? (AWS, GCP, Heroku, etc)

AWS.

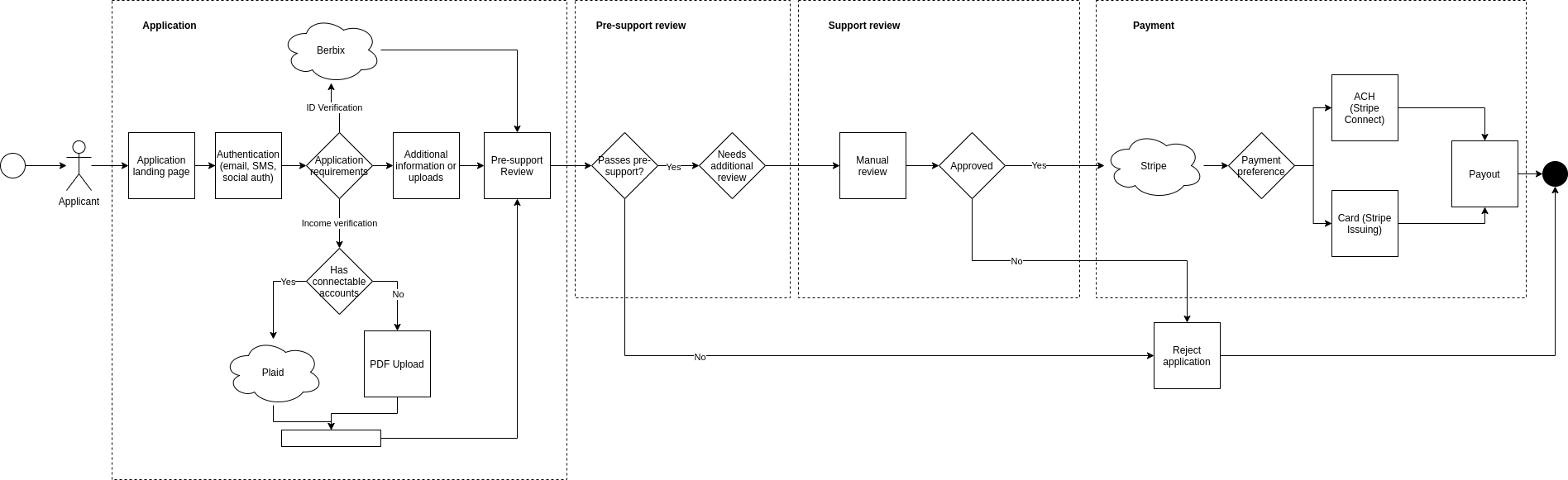

Do you have an architecture diagram for your application? (insert please)

Features of the application form include:

- Localization: The application is available in both English & Spanish.

- USPS address verification: Address issues such as missing apartments or unrecognizable addresses are detected and corrected on the front end, ensuring applicants’ funds make it to the right place.

- Real-time access code verification: A valid access code is required in order to submit the form; an access code can only be used once.

- Pre-filled access codes: Custom URLs can be used to prepopulate codes for the applicant, mitigating typo errors (e.g. ccf.myalia.org/abc-def-ghi will auto-populate the code abc-def-ghi).

- Text message confirmation: The applicant receives a text message upon successful form submission (see Text Messaging section for details on SMS communication).

See below:

How are you tracking the success of the program? Are you using any tools, technologies to support this?

We used Google Data Studio as a dashboard to track progress of the programs, including total funds distributed and applicant details.

Security and Privacy

What are the considerations and tradeoffs related to security and privacy?

All data at rest and in transit was encrypted. Data in the databases had a contractual lifetime that would be deleted at the end of the program to protect privacy.

The staff portal is a secure site for fund administrators to view and edit application data, generate access codes, and process payments. Two-factor authentication is enforced to provide an additional level of security.

Customer Service

How do you support applicants and help answer their questions?

Applicants could reach our bilingual (English and Spanish) customer service team by phone or email.

III. Payment Integration

Payment Integration

How do you disperse funds to recipients?

We mailed debit cards to applicants via USPS.

What payment technologies do you use and why? (Paypal, Stripe, Square, Hyperwallet, etc.).

Usio/Akimbo.

What type of funds do you provide? (debit cards, cash, gift cards)

Prepaid debit cards.

IV. Ongoing Support

Are you providing additional or ongoing support to recipients? If so, in what way?

We provide limited ongoing support to recipients who had any trouble using their cards.

Summary Diagram

The diagram below was copied from the diagram you created for the Cash Assistance Design Sprint. Please feel free to make any updates or add more details where necessary.

Civic + Policy Consideration

[If applicable] What considerations did you make in the setup of this cash assistance program to involve government organizations or to impact policy?

We worked with Google.org Fellows to design the core software to be modular and adaptable so that government organizations can quickly use this platform to distribute emergency cash to their applicants. In addition, we made data easily accessible and usable via tools such as Google Data Studio so that agencies can securely and easily access the data they need to implement the program and analyze the data for policy-related purposes.

Research Design

[If applicable] What considerations, if any, did you make so that others could learn from the project? If so, how?

One of the core hypotheses is that trust is necessary for eligible applicants to even apply for the fund at all, and that trust can be gained through partners who are community-based organizations that the applicant already knows. Our programs thus far have demonstrated that partner organizations have been absolutely essential in bridging the trust gap.

Learnings

What might you do differently if you were to set up a similar assistant program knowing what you know now?

There are two areas we would make adjustments to: customer service and theft prevention.

Customer Service

- Our assumption that using a prepaid debit card would be intuitive was not accurate for many recipients. When we included bilingual instructions on basic use of the card, recipient experiences improved greatly.

- Text messaging is the preferred communication for many of our recipients, however our initial customer service options only included email and phone. We added a text option, but if we were to set up a similar program we would have text as a customer service option from the start.

- We offered customer service in English and Spanish, but this was not the preferred language for many recipients. If we were to set up a similar program we would offer customer service in additional languages to foster more trust.

- Providing customer support was often challenged by the multiple tools we used to carry an application through to payment. Improved reporting processes would have made our customer service team’s job easier.

Theft Prevention

- Our fraud prevention didn’t factor in mail theft, which we had no control over. However, we could have controlled access to the funds even after the card had been mailed by adding an additional verification step, which would ensure the funds were accessible only once the card recipient had been verified.

Family Independence Initiative (FII)

Context

In 2-3 sentences, briefly describe your organization. What prompted you to start this cash assistance program?

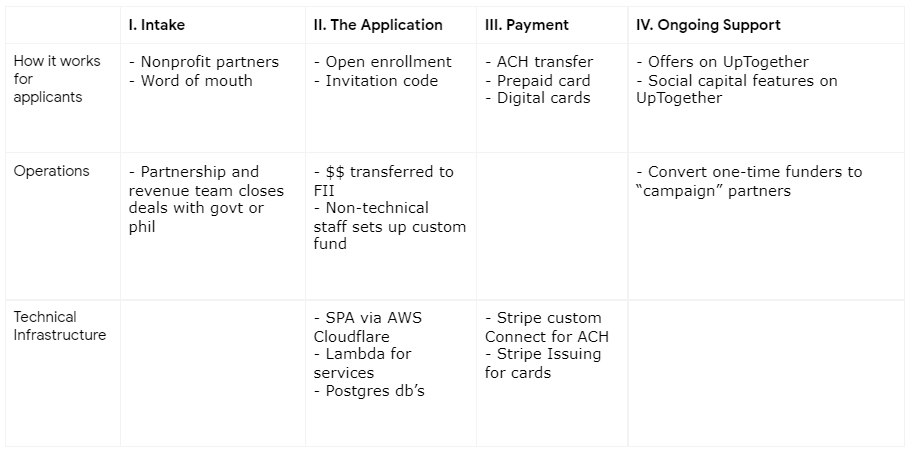

FII trusts and invests in families living with low-incomes across the country. We empower government and philanthropic institutions to make cash transfers directly to people through our online platform, UpTogether.org.

I. Intake

Qualifying Applicants + Verifying Applicants

How do you find, qualify and verify recipients?

Government and philanthropic partners can establish “funds” on UpTogether.org. Members can either directly apply for or receive offers (based on provided data) for one-time or on-going cash transfers. Qualifications vary by fund.

Why did you choose this approach?

Our focus is creating a platform for experimentation around cash transfers and a marketplace where government and philanthropy can shift their approach to investing in people’s strengths instead of deficits. This approach allows us to deploy funds across the country that match local contexts.

II. The Application

Application Experience

How do people find the application?

Funds are advertised by our government and philanthropic partners when first launched. After members receive cash offers we often see information then spread through natural networks.

What information is needed?

While different funds have different requirements, common verifications are identify verification with a government issued ID (does not have to be current nor does it have to be us), address verification (can be done by stripping meta-data off government ID), income verification (can do via connected checking/savings accounts or via PDF upload of various forms of documents proving income).

How do they get approved?

We use a two-step process. The first step is an automated system that verifies what it can without additional human intervention. Where necessary we have a support team that can manually verify uploaded evidence.

How, if at all, do they track their application status?

Application status is available in a user’s dashboard on UpTogether.org. We also send transactional messages (email or SMS) as a member’s application moves through various stages.

Why did you choose this approach?

We believe in being communicative and transparent. Having both transactional messages as well as dashboard status allows our members various ways of accessing application status information.

Hosting and Deployment

Where do you host your application? (AWS, GCP, Heroku, etc)

AWS.

Do you have an architecture diagram for your application? (insert please)

How are you tracking the success of the program? Are you using any tools, technologies to support this?

Two randomized control trials in partnership with a team based out of Harvard Business School. Additionally, periodic surveys to recipients and frequent focus groups.

Security and Privacy

What are the considerations and tradeoffs related to security and privacy?

Hackers can’t get what you don’t collect. We don’t collect Social Security or checking account information (we do pass that through to third party processors). Identification uploads are purged after 30 days. We also hired a security firm to conduct a white-hat attack on our systems to identify holes and harden systems.

Customer Service

How do you support applicants and help answer their questions?

Internally housed support team that provides support via email tickets, SMS, live chat, and phone or screen share where helpful.

III. Payment Integration

Payment Integration

How do you disperse funds to recipients?

Recipients can choose to receive funds via ACH transfer, prepaid physical card, or digital card. We will soon add fulfillment via Venmo and Paypal as well, and look to continue adding more options to meet the range of choices recipients prefer for their funds.

What payment technologies do you use and why? (Paypal, Stripe, Square, Hyperwallet, etc.).

Stripe.

What type of funds do you provide? (debit cards, cash, gift cards)

Direct deposit, physical card that can be remotely topped up, digital card.

IV. Ongoing Support

Ongoing Support

Are you providing additional or ongoing support to recipients? If so, in what way?

All applicants can join UpTogether.org where members support each other and they may be eligible for additional cash offers.

Summary Diagram

The diagram below was copied from the diagram you created for the Cash Assistance Design Sprint. Please feel free to make any updates or add more details where necessary.

Civic + Policy Consideration

[If applicable] What considerations did you make in the setup of this cash assistance program to involve government organizations or to impact policy?

About half of the $100+ million we have disbursed in 2020 is government money. Government entities across the country are seeing the value in direct investment. Our long-term vision is for government and philanthropy to shift the ~$300 billion annual spending in deficit based anti-poverty programs to direct investment in the initiatives of the ~50 million people experiencing poverty.

Research Design

[If applicable] What considerations if any did you make so that others could learn from the project? If so, how?

We presently have two RCTs in progress, one focusing on one-time payments and another focused on ongoing payments. In both studies participants are split into four groups: 1. No-treatment control 2. Cash transfer only 3. Social capital only (participation in small cohort groups facilitated on UpTogether) 4. Cash and social capital together.

While we believe cash is good, we think the pathway out of poverty is when people are both invested in and empowered to turn to and support one another. This experimental design allows us to learn about the individual and joint effect of cash and social capital augmentation in the form of peer groups.

Learnings

What might you do differently if you were to set up a similar assistant program knowing what you know now?

Invested in support staff sooner. Support is such an important and underrated part of doing this well. A good, integrated support team can quickly translate user issues to engineering to fix before problems magnify.

Accelerator for America

Context

In 2-3 sentences, briefly describe your organization. What prompted you to start this cash assistance program?

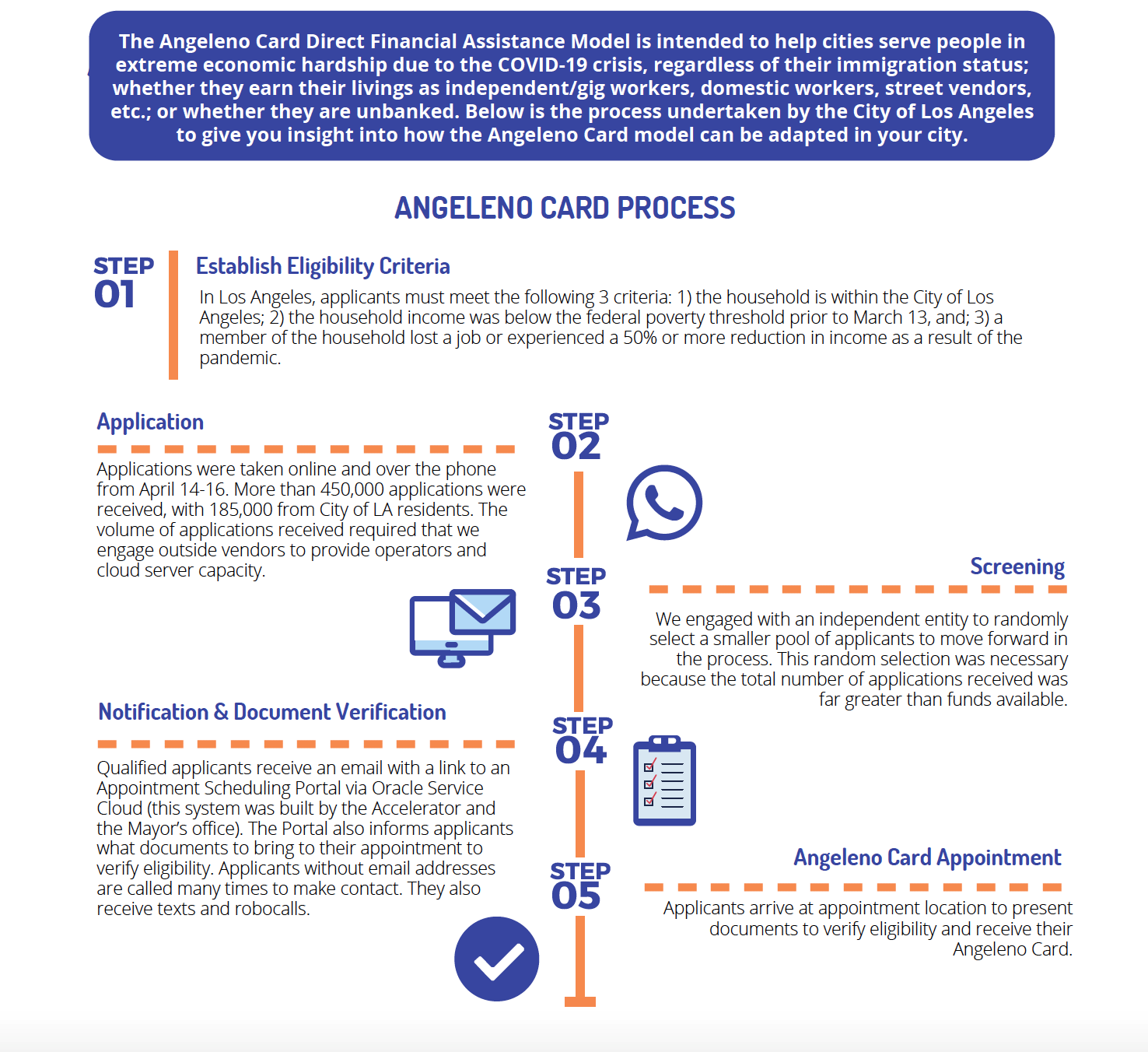

Accelerator for America is a national nonprofit co-founded by Los Angeles Mayor Eric Garcetti in 2017. Guided by a network of mayors, labor leaders, corporate CEOs and nonprofit executives from across the country, the Accelerator’s mission is to find and develop solutions to economic insecurity and share them with cities to create national change from the ground up. With 20 percent of Angelenos living below the poverty level prior to the COVID-19 crisis, we knew that there would be widespread need for financial assistance. In partnership with the Mayor Garcetti and the City of Los Angeles, Mastercard’s City Possible team, and the Mayor’s Fund for Los Angeles, Accelerator for America created a privately-funded direct financial assistance program in Los Angeles to serve those experiencing extreme economic hardship due to the COVID-19 pandemic, including undocumented Angelenos who would be excluded from federal assistance programs.

I. Intake

Qualifying Applicants + Verifying Applicants

How do you find, qualify, and verify recipients?

Applications were available online at hcidla.lacity.org. Those without internet access were able to call 213-252-3040. Households were required to meet the following criteria to be eligible for assistance: (1) Households in the City of Los Angeles; (2) Households with total annual incomes that fell below the federal poverty level prior to the COVID-19 crisis (March 13); and (3) Households that have fallen into deeper economic hardship during the crisis because at least one household member has lost a job or experienced a reduction in income of at least 50 percent. Recipients were given $700, $1,100, or $1,500 prepaid, no-fee “Angeleno Cards” (Mastercard debit cards) based on household size and income. News of the program was shared widely by the LA media and by Mayor Garcetti during his nightly coronavirus briefings. Once the three day application period was over, we received more than 450,000 applications (far more than we anticipated).

Those who pre-qualified based on their applications were given an in-person appointment at one of the LA Housing and Community Investment Department’s (HCID) 16 “FamilySource” Centers and asked to provide documentation. A few weeks into the process, we ended up implementing an online appointment scheduling, verification, and documentation program via Oracle and TimeTrade to make the process more efficient. When the Angeleno Card program first launched, we were using a phone banking system to call and verify recipients as well as schedule their appointments at one of the FamilySource Centers.

Why did you choose this approach?

We chose this approach in order to reach the most number of Angelenos possible. Unfortunately, due to the media promoting this program and Mayor Garcetti speaking about it during his nightly coronavirus briefings, the application website crashed due to the sheer number of people applying for assistance. Ultimately, we were happy we chose to open up this program to all LA residents because we were able to help more than 100,000 Angelenos.

II. The Application

Application Experience

How do people find the application?

The application was available online at hcidla.lacity.org. Those without internet access were able to call 213-252-3040. The program information including how to apply was widely publicized by the local LA media, and Mayor Garcetti spoke about the program (including how to apply) during his nightly coronavirus briefings. All 16 HCIDLA FamilySource Centers also shared the program information with the individuals and families they served.

What information is needed?

We never asked for immigration status, nor was it considered in determining eligibility. This initiative was entirely funded by private donations and was not a City program. Applicants were asked to provide the following documentation for each of the aforementioned requirements, though they could also self-certify:

(1) Households in the City of Los Angeles: A valid California Driver’s License or Identification Card with the applicant’s name and an address in the City of Los Angeles; A tenant lease agreement with the applicant’s name for a home, apartment, room, etc. within the City of Los Angeles; A utility bill with the applicant’s name for an address within the City of Los Angeles; or Postmarked mail addressed to the applicant at an address within the City of Los Angeles.

(2) Households with total annual incomes that fell below the federal poverty level prior to the COVID-19 crisis (March 13): A copy of the applicant’s 2018 or 2019 tax return; OR information about all wages and public benefits within the household. (Proof of wages within the household could include: W2s, 1099s, paychecks (annualized), or self-declarations. Proof of public benefits within the household could include: Notice of Public Benefit from CalWorks, General Relief, Unemployment Insurance, Social Security, SSI, or SSDI. Again, applicants with no documents were able to go through a self-certification process).

(3) Households that have fallen into deeper economic hardship during the crisis because at least one household member has lost a job or experienced a reduction in income of at least 50 percent: A layoff letter from an employer; Contact information for an employer to allow a case manager to make contact and verify a job loss or a reduction in income of at least 50 percent; A denial letter for unemployment insurance or other public benefits; or a referral letter from a nonprofit organization such as a day laborer center or domestic worker association stating that the organization knows the applicant has recently lost employment or suffered a reduction in income of at least 50 percent.

How do they get approved?

Applicants were approved if they are able to provide the required documentation detailed above (though we had a self-certification process for those without documentation). Through the oracle system that was implemented a few weeks into the program, applicants were able to upload documents to ensure they had everything they needed for their appointment (which they were also able to schedule via this system).

How, if at all, do they track their application status?

N/A

Why did you choose this approach?

We implemented an online verification and scheduling system in order to efficiently process all of the applications received. We had no idea that we would receive so many applications for this program (which only speaks to the need for assistance), so we needed to streamline our ability to help the 104,000+ Angelenos we were able to serve by the program’s end.

Hosting and Deployment

Where do you host your application? (AWS, GCP, Heroku, etc)

AWS via the HCIDLA website

Do you have an architecture diagram for your application? (insert please)

N/A

How are you tracking the success of the program? Are you using any tools, technologies to support this?

What started as an idea on March 15 had by June 30 distributed $36,753,800 to provide assistance to 104,156 Los Angeles residents via 37,841 Angeleno Cards. Mayor Garcetti’s office worked with HCIDLA leadership to track every person served, the number of Angeleno Cards distributed, and the amount of money distributed via an excel mastersheet (Managers of all 16 FamilySource Centers would report their numbers at the end of each day).

Security and Privacy

What are the considerations and tradeoffs related to security and privacy?

N/A

Customer Service

How do you support applicants and help answer their questions?

Applicants were provided a number to call if they had any questions about the application.

III. Payment Integration

How do you disperse funds to recipients?

Funds were dispersed via prepaid, no-fee Angeleno Cards (Mastercard debit cards) in the amounts of $700, $1,100, or $1,500 based on household size and income. Once an applicant uploaded their documentation and schdelied their appointment via the online system, they received their Angeleno Card at their closest HCIDLA FamilySource Center (all COVID public health guidelines were followed).

What payment technologies do you use and why? (Paypal, Stripe, Square, Hyperwallet, etc.).

Mastercard debit cards/ Prepaid Technologies (program manager)

What type of funds do you provide? (debit cards, cash, gift cards)

Debit cards.

IV. Ongoing Support

Are you providing additional or ongoing support to recipients? If so, in what way?

The City of LA is currently exploring ways to add a number of public benefits to the 37,000+ Angelenos Cards in circulation in the city (with the hopes of expanding the number of cards to more Angelenos). The City wants to be able to continue to provide support to this population via an efficient, effective way.

Summary Diagram

Civic + Policy Consideration

[If applicable] What considerations did you make in the setup of this cash assistance program to involve government organizations or to impact policy?

Based on information from a number of local organizations and departments, we knew that so many Angelenos would be struggling to make ends meet as people continued to lose jobs because of the pandemic. Additionally, while we never asked for immigration status, we knew that we would be serving a large number of undocumentred Angelenos based on the areas we were serving. Due to the scale and success of the Angeleno Card program in LA, the Open Society Foundations granted Accelerator for America $750,000 to help an additional two states and eight cities nationwide set up similar direct financial assistance programs. The impact of these ten programs has been remarkable, distributing millions in financial assistance (again showing how desperately people across the country need financial support during this time). Alongside the Open Society Foundations and the mayors/governors of these ten jurisdictions (plus LA), we are exploring different advocacy efforts for cash-based policies at the local, state, and federal levels.

Research Design

[If applicable] What considerations if any did you make so that others could learn from the project? If so, how?

N/A

Learnings

What might you do differently if you were to set up a similar assistant program knowing what you know now?

If we could start over, we would definitely make sure we had an online system established to verify and schedule appointments from the start. We had no idea that we would receive more than 450,000 applications, and there is no way to efficiently manage this number of applicants without a streamlined system.

GiveDirectly

Context

In 2-3 sentences, briefly describe your organization. What prompted you to start this cash assistance program?

GiveDirectly (GD) is the first, and largest, nonprofit that lets donors send money directly to the poor, no strings attached. We believe people living in poverty deserve the dignity to choose for themselves how best to improve their lives, cash enables that choice. To date, we have delivered $400M+ to over 900K recipients across nine countries.

When COVID-19 began devastating the United States in early 2020, we saw the need for a fast, remote method of getting emergency relief to Americans in need. In April 2020, we stood up our U.S. COVID response program. To date, we’ve delivered $150M to 158K families experiencing financial hardship due to the pandemic across 51 U.S. states and territories.

I. Intake

Qualifying Applicants + Verifying Applicants

How do you find, qualify and verify recipients?

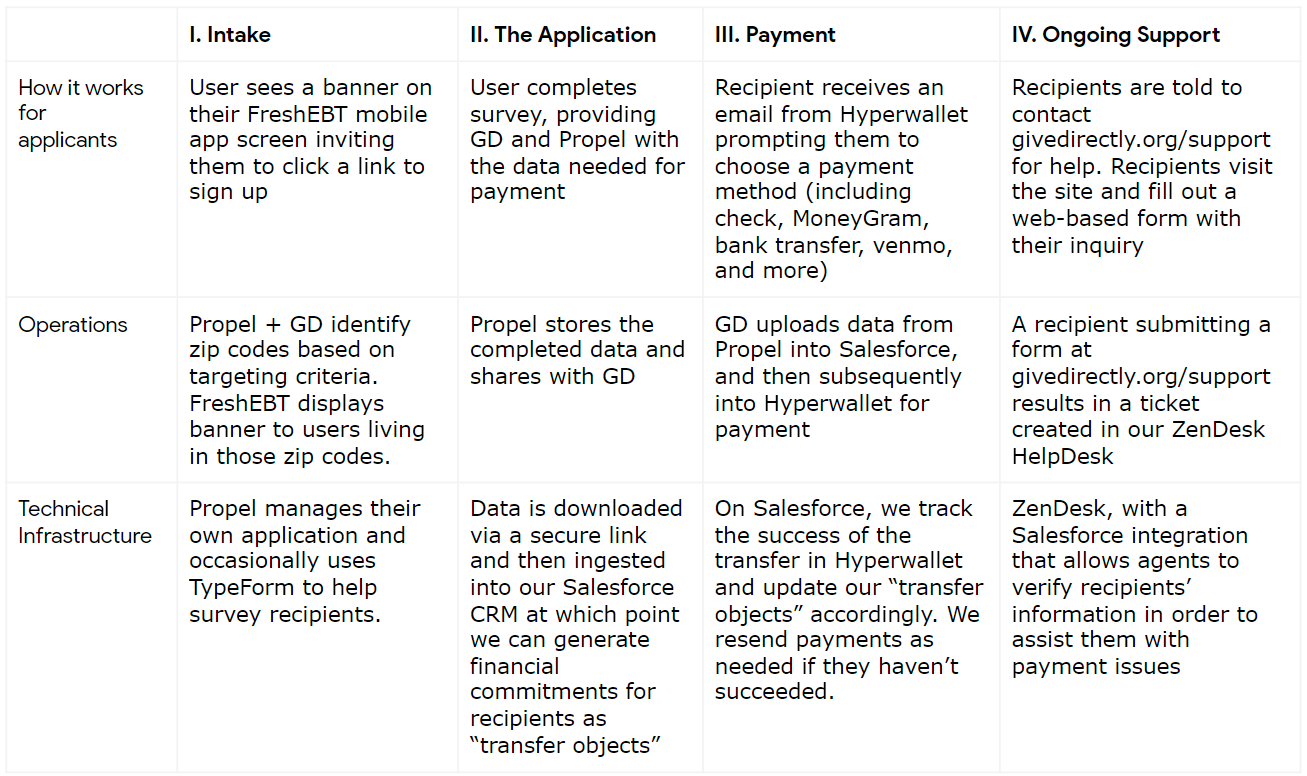

Primary program model (90 percent+ of recipients): FreshEBT, owned by Propel, is an app that allows U.S. SNAP beneficiaries to manage their benefits, all registered users are verified U.S. SNAP beneficiaries. We work with Propel to identify users living in the highest poverty zip codes across the United States (e.g., 35 percent+ poverty rate). Users living in these zip codes are randomly selected to enroll in our program, and once verified (i.e. to ensure they are not duplicates) are then able to receive payment. Note: our targeting and exclusion criteria have evolved, and may continue to, over time. The remainder of this document will describe the elements of our most recent program design.

Community-partnership model: A community-based partner independently finds, qualifies, and verifies recipients using customized qualification criteria and application and verification methods. The vetted list of beneficiaries is sent to GD for payment. We partnered with OneFairWage and Stand for Children to deliver cash to vulnerable individuals through this model.

Why did you choose this approach?

Primary program model: We launched this program in April 2020. The effects of the pandemic made our priorities clear: getting out fast, remote financial support to as many people in need as possible. The FreshEBT model offered a highly scalable, fully remote method to find a large number of people in need.

Community-partnership model: We recognized specific groups of people in need would be systematically left out by the FreshEBT model (e.g., those who cannot register for SNAP). In order to extend emergency relief to those groups, we partnered with organizations who could identify and verify people in need from those populations.

Both approaches were lean and scalable, keeping all delivery costs at about 2 percent (98 percent efficiency).

II. The Application

Application Experience

How do people find the application?

Recipients living in targeted zip codes see a banner on their FreshEBT app that prompts them to click a link to a survey to enroll for payment.

What information is needed?

Information requested as part of the enrollment process includes: First and Last Name, Date of Birth, Email Address, Phone Number. Note: Other descriptive data is collected as well (e.g., gender, disability, race)

How do they get approved?

Any FreshEBT user who sees the banner on the app, completes the enrollment survey, and is verified by GiveDirectly gets a payment. We primarily verify individuals to ensure we are not paying duplicates (which is rare).

How, if at all, do they track their application status?

They do not track their status. Once they have successfully enrolled and been verified, users see a new banner on their app that tells them to look out for a payment email coming from GiveDirectly in the coming days.

Why did you choose this approach?

It allowed our systems and operations to be simpler, which allowed for a rapidly-scalable approach. It also leverages a trusted platform and brand for the target population.

Hosting and Deployment

Where do you host your application? (AWS, GCP, Heroku, etc)

AWS (both for GD Salesforce and Propel application/data).

Do you have an architecture diagram for your application? (insert please)

How are you tracking the success of the program? Are you using any tools, technologies to support this?

Percent of recipients successfully claiming payments and customer experience: Success of the program is being tracked in a combination of dashboards housed in google sheets and Salesforce. Data to inform the success of the program is pulled from a variety of sources including our payment provider (percent of recipients who claimed payment successfully), our ZenDesk customer service stats, and self-reported recipients data collected in periodic surveys (customer satisfaction ratings, adverse event frequency).

The impact of the program is also being assessed via a Randomized Control Trial conducted by the University of Michigan.

Security and Privacy

What are the considerations and tradeoffs related to security and privacy?

We collect the minimum amount of information to be able to 1) pay recipients 2) contact recipients and 3) verify identity of recipients for customer service requests. We collect self reported first and last name, date of birth, email address, and last four digits of phone number for these purposes. We restrict the access to recipient PII to those parties working on any of the three purposes listed above.

Trade-off between operational simplicity and data privacy/security: There are trade-offs in terms of staffing and workflow between operational simplicity and security. For example, allowing fewer people access to view PII means fewer people can respond to help desk tickets which decreases operational efficiency.

Customer Service

How do you support applicants and help answer their questions?

Since users enroll using the FreshEBT app, Propel handles most customer service needs of users before enrollment (before payment) via a help link in their app or email support. Once they enroll, recipients are given GiveDirectly’s HelpDesk contact information. We have a team of agents who monitors this help desk seven days a week, which is run on a Zendesk platform and allows us to provide ongoing support to recipients.

III. Payment Integration

How do you disperse funds to recipients?

Email, then chosen payment method: Some days after enrolling in the program via the FreshEBT app, GD pays the recipient via our payment provider (Hyperwallet). Hyperwallet then sends an email to each recipient with a link to their portal, in which the recipient registers for payment by selecting a payment method. The speed at which recipients receive their funds depends on the elected payment method (see below for list of payment method options)

What payment technologies do you use and why? (Paypal, Stripe, Square, Hyperwallet, etc.)

GD uses Hyperwallet for the U.S. COVID-19 program, its primary differentiating factor being the flexibility in payment options. Recipients can choose from eight different payment options that accommodate both banked and unbanked families.

What type of funds do you provide? (debit cards, cash, gift cards)

Direct deposit, deposit to ATM card, Paypal, Venmo, physical pre-paid Visa card, virtual pre-paid Visa card, Moneygram, and check.

IV. Ongoing Support

Are you providing additional or ongoing support to recipients? If so, in what way?

Yes, Online HelpDesk. Recipients can contact GiveDirectly’s online HelpDesk at givedirectly.org/support. Our HelpDesk is staffed by agents who respond via email to inbound recipient inquiries, which are received as tickets in ZenDesk (the platform is integrated with Salesforce to provide agents with some access to recipient information).

Summary Diagram

The diagram below was copied from the diagram you created for the Cash Assistance Design Sprint. Please feel free to make any updates or add more details where necessary.

Civic + Policy Consideration

[If applicable] What considerations did you make in the setup of this cash assistance program to involve government organizations or to impact policy?

RCT to contribute to U.S. Cash evidence base: Early in the program we began working with the Poverty Solutions Lab at the University of Michigan to run a Randomized Control Trial (RCT) of the impact of our U.S. COVID program. The RCT will contribute unique literature to the cash space in its study of the effectiveness of cash transfers as emergency relief in the United States, which we hope can be used in the future to inform policy around disaster/emergency relief in the United States.

Research Design

[If applicable] What considerations if any did you make so that others could learn from the project? If so, how?

Collection of demographic and self reported impact and spending data:

- The enrollment survey includes the collection of demographic and self-reported data on government benefits received (i.e. have you received a government stimulus check? Unemployment benefits?) from recipients which could be used for research and analysis in the future.

- We have also periodically collected larger amounts of data from recipients ( via a Typeform survey link that recipients see in a banner on their FreshEBT app), which includes self-reported data on spending, impact of COVID-19, impact of the received cash transfer, and preference for in-kind vs cash relief.

Learnings

What might you do differently if you were to set up a similar assistant program knowing what you know now?

Standardize data requirements upfront to ensure partners provide high quality data: Identifying and enrolling people digitally is hard so a 3rd party dataset to triangulate or onboarding CBOs in an efficient way can help ensure data quality is high and fraud risk is low.

Make a plan for revisiting what you deprioritized during design: Keep track of the areas you are consciously deprioritizing when designing a program. Create a timeline to come back to those deprioritized areas as they may become increasingly important as the program grows in scale, changes in design, or simply over time. This is especially true when sacrificing certain program components in favor of speed and scale.

Fund for Guaranteed Income: Compton Pledge

Context

In 2-3 sentences, briefly describe your organization. What prompted you to start this cash assistance program?

The Fund for Guaranteed Income is a registered public charity launched in August 2020 to redistribute wealth and create a society characterized by economic equity, beginning with efforts to raise funds and launch the Compton Pledge. The F4GI: Compton Pledge has begun providing direct payments to 800 low-income residents of Compton for a two-year period. It sets in motion an actionable policy approach, building new financial and technological infrastructure to reimagine community investment. This first-of-its-kind partnership between national advocacy groups and local community leaders can chart a template for how recurring cash transfers can fight poverty and racial inequality.

I. Intake

Qualifying Applicants + Verifying Applicants

How do you find, qualify and verify recipients?

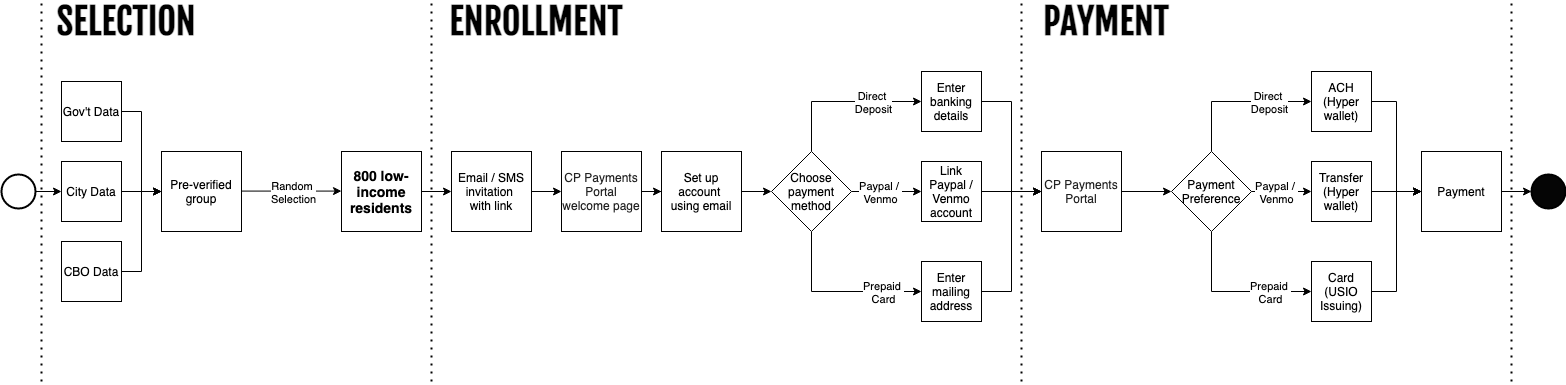

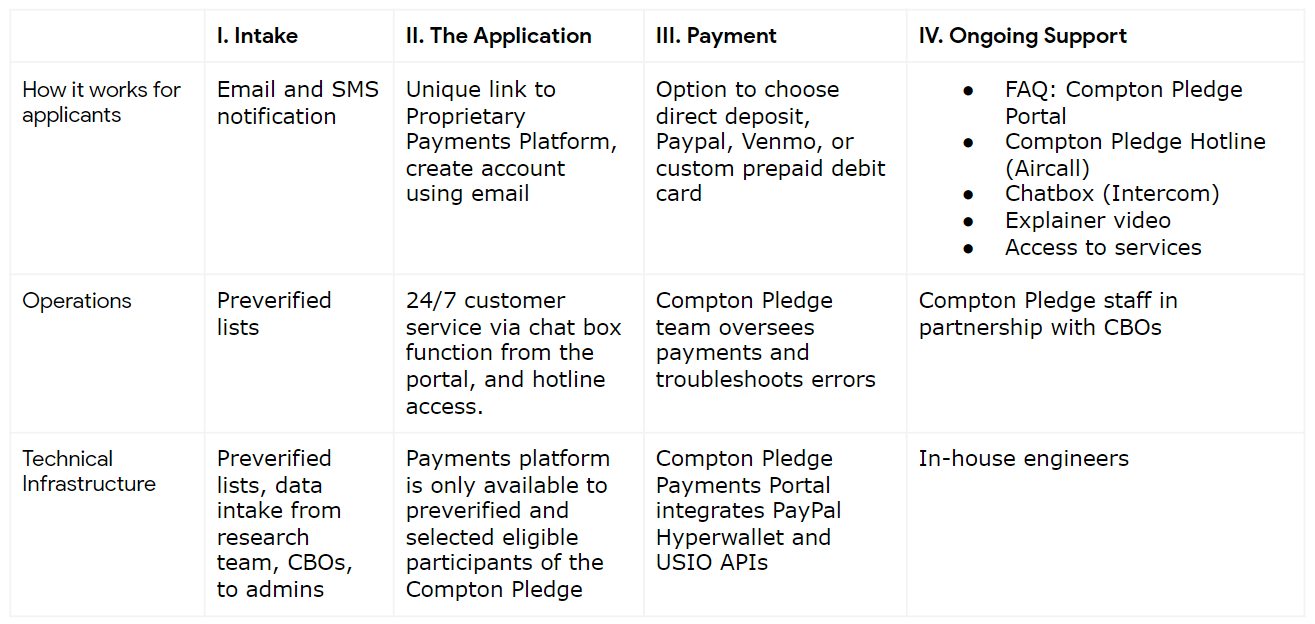

Participants are randomly chosen from a pre-verified group of low-income Comptonians, drawn from a combination of city data and member lists from national and local community-based organizations.

Why did you choose this approach?

We believe these sources of data ensure the lowest burden of documentation on participants, with the aim of making the program inclusive and truly representative. By using random selection, we deliberately draw from the widest possible range of Compton’s community, representing a cross-section of low-income populations, such as households with income less than 200 percent of the Supplemental Poverty Measure and those excluded from federal welfare programs.

The Compton Pledge is built on principles of individuals’ agency and rights. While philanthropy has supplemented gov’t investments in often paternalistic and bureaucratized programs, using the pre-verified list of eligible participants reduces the burden of proof placed on participants.

II. The Application

Application Experience

How do people find the application?

Recipients are sent an email and SMS notification informing them that they have been selected to receive a guaranteed income cash transfer for two years. The email is translated in multiple languages, and contains personal messages from Compton Pledge Community Advisory Council members. Messages contain a unique link to access the Compton Pledge Payments Portal, where participants create a profile and select their payment method. The unique link expires in two weeks, with reminder messages sent at the one week and one day mark.

What information is needed?

Participants are only required to create a unique password in order to access the payments portal.

How do they get approved?

Individuals are pre-verified, so there is no approval process.

How, if at all, do they track their application status?

Participants are officially enrolled after they set up a payments profile on the portal. Our backend administrative portal allows us to monitor whether a participant has created a password but not yet selected a payment method.

Why did you choose this approach?

Our approach provides a crucial alternative to the limitations of state-based welfare recipient databases and cumbersome approval processes. Partnerships with community based organizations were critical to raising awareness and credibility of the program, a key obstacle for take-up of existing programs. Towards the end of our enrollment process, our enrollment rate was 99 percent.

Hosting and Deployment

Where do you host your application? (AWS, GCP, Heroku, etc)

Vercel, website hosting. Heroku, server hosting.

Do you have an architecture diagram for your application? (insert please)

How are you tracking the success of the program? Are you using any tools, technologies to support this?

The success of the overall program will be evaluated via a two-year randomized control trial designed by the Jain Family Institute in collaboration with an Academic Advisory Board, the Fund for Guaranteed Income, and the Compton Community Development Corporation.

The success of the program’s implementation will be monitored by the Fund for Guaranteed Income, which built an administrative portal to notify team members when there is a payment failure or customer service request.

Security and Privacy

What are the considerations and tradeoffs related to security and privacy?

We collect minimal information in order to best protect users’ data privacy. The information which participants are required to provide depends on the payment method that they select. For example, prepaid cards only require a mailing address (no SSN or ITIN). We collect and securely store individual’s names, phone numbers, and email addresses, and do not store banking information or physical addresses.

Customer Service

How do you support applicants and help answer their questions?

We support participants in house through the customer service feature of our payments portal which includes a chatbox and hotline.

III. Payment Integration

How do you disperse funds to recipients?

The Compton Pledge Payments Portal automatically facilitates transactions on a biweekly or quarterly basis and sends emails and SMS notifications to the recipients when the funds are on their way and delivered. Carefully selected administrators address payment issues if they arise. The portal is accessible for under/unbanked users, offering multiple payment options including a prepaid card which does not require ITIN or SSN. The portal is currently available in English and Spanish.

What payment technologies do you use and why? (Paypal, Stripe, Square, Hyperwallet, etc.).

We use PayPal Hyperwallet and USIO APIs to provide participants a wide range of options.

What type of funds do you provide? (debit cards, cash, gift cards)

We provide the following options:

- Direct Deposit

- Venmo

- PayPal

- Prepaid debit card

IV. Ongoing Support

Are you providing additional or ongoing support to recipients? If so, in what way?

Access to Resources: We provide additional resources to cash transfer recipients including access to financial coaching, job training, and telehealth services.

Ongoing Support: Our Fund for Guaranteed Income team manages all customer service requests directly. In only five months we have had over 5000 conversations with an average waiting time of 90 seconds. We have found this to be an incredibly important way to build trust with participants and receive feedback around ways to improve our program.

Summary Diagram

The diagram below was copied from the diagram you created for the Cash Assistance Design Sprint. Please feel free to make any updates or add more details where necessary.

Civic + Policy Consideration

What changes if any did you make in the setup of this cash assistance program to involve government organizations or to impact policy?

Mayor Aja Brown launched the pilot as part of a local resolution of the BREATHE Act, the modern day civil rights act proposed by the Movement for Black Lives (M4BL). We are also linking the cash transfer as future equity in the One Fair Wage unemployed workers cooperative, which we hope to pilot in the city. A parallel effort is ongoing to design forms of municipal revenue to sustainably finance this effort and comparable policies.

Research Design

Did you set up the project so that you and others could learn from the project? If so, how?

An independent research evaluation will ensure the pilot’s meaningful contribution to the case for GI. The study is geared to answer the most pressing open questions about a long-term GI by testing transfers of varying frequency and identifying best practices in enrollment and disbursement. Our results, shared every six months, will build a roadmap for future policymakers.

Learnings

What might you do differently if you were to set up a similar assistant program now?

A. It is important to give recipients the option of different payment methods. Around 50 percent of our participants selected direct deposit, 18 percent selected Venmo/PayPal, and the remainder selected prepaid debit card.

B. An admin portal is crucial to support ongoing operations and troubleshooting, as well as leveraging analytics to directly improve the platform and related services.

C. Send reminder emails and clear communication with an established brand to selected recipients, especially given the rise in robo-calls and scams.

D. Allow for pop-up notifications to demonstrate how participants find information when they select their direct deposit, such as account number and routing numbers. When entered incorrectly it can cause delays.

E. Develop a mechanism for older recipients or those without technology to have access to their account, or a call system where they enter an ID number with automated details on their accounts.

F. A live chat feature and hotline have proven to be a great success at addressing problems and questions in real time.

G. We have coded a function in Slack that collects portal data, changes, and conversations from intercom. This has proven a very useful tool for internal collaboration and rapid problem solving.

More About the Authors

Erin Hattersley

Manager, Google.org

Saj Reshamwala

UX Designer & former Google.org Fellow

Jonathan Cham

Customer Engineering Leader & former Google.org Fellow

Cassandra Robertson

Alberto Rodríguez

Issues

Programs/Projects/Initiatives

Related