Evidence from Banks’ Entry-Level Checking Accounts

This report discusses findings from an investigation into the racialized costs of banking in entry-level checking accounts, including tests for evidence of banks’ discretionary practices in the delivery of account costs and fees. The findings are based on survey data collected from a stratified random sample of commercial banks in the United States, which asked banks about the costs and fees of entry-level checking accounts, as well as their strategies for serving consumers (e.g., whether branches operated extended hours during evenings and weekends, offered non-English language services, used ATMs, and offered online and/or mobile banking) and transaction processing (e.g., whether transactions were processed in chronological order). To analyze relationships between community racial demographics and banks’ checking account costs and fees, geocoded survey responses were combined with census tract and census place data from the 2011-2015 5-year sample of the American Community Survey (ACS), 2014 Federal Deposit Insurance Corporation (FDIC) summary of deposits, 2014 National Credit Union Administration (NCUA) call reports, and 2015 InfoGroup proprietary business listings. The results discussed here summarize key findings based on regression estimates in models with full controls, and a more detailed description of the data and methods is provided in the technical appendix.

Racial Disparities in Opening and Maintaining Accounts

Racial disparities are present in the costs and fees required to open and maintain basic, entry-level checking accounts. In other words, higher costs and fees charged by banks for these entry-level products are significantly associated with communities of color (see Figure 1). The minimum opening deposit is substantially higher in communities with majority black populations ($80.60), and in communities that are more racially diverse without a white, black, or Latinx majority ($97.00), when compared to majority white communities ($68.50). Opening deposit requirements are almost the same in majority Latinx ($68.60) as in white communities.

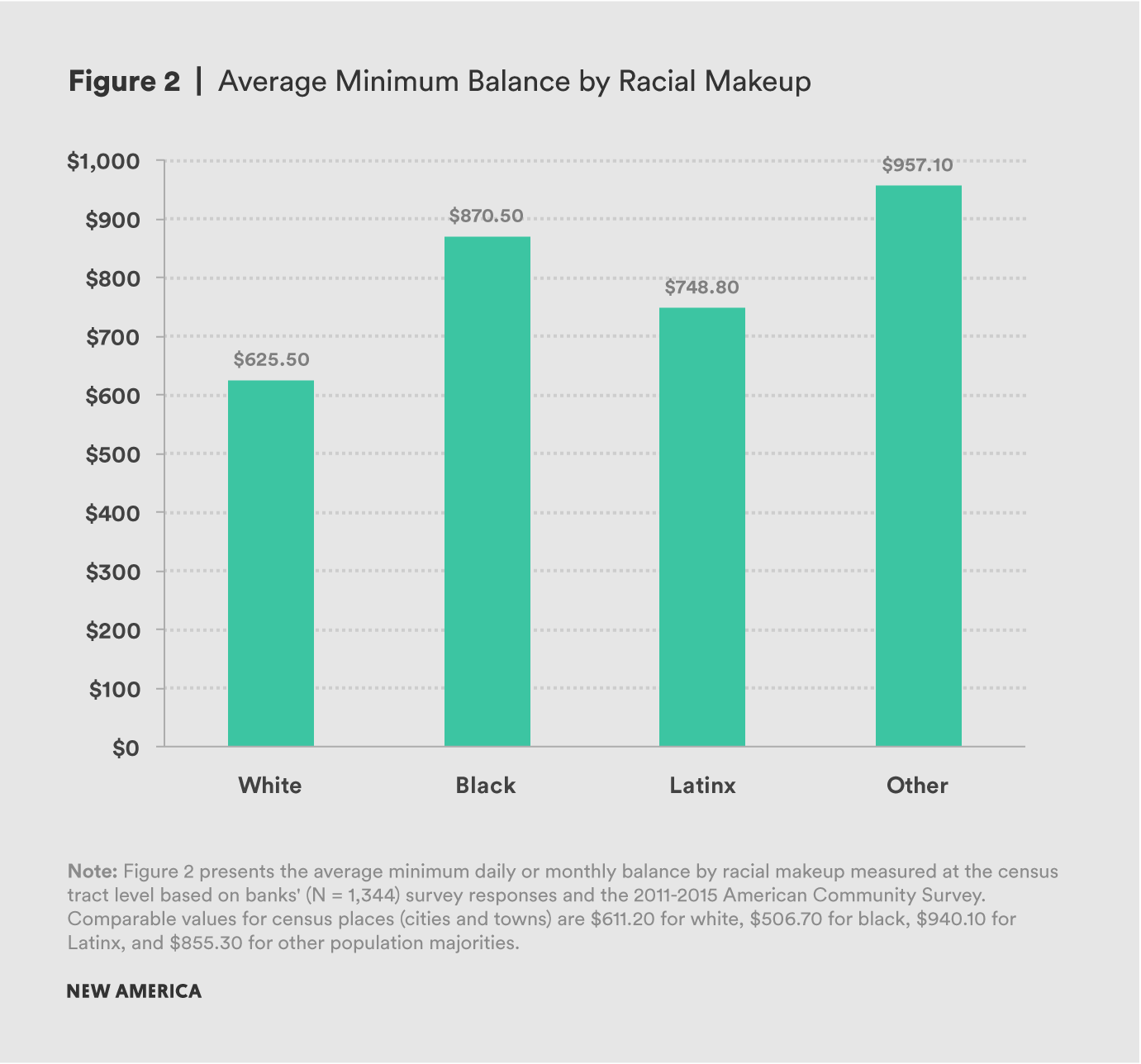

It is cheaper to maintain a checking account opened in a white neighborhood (see Figure 2). A minimum balance of only $625.50 is required to avoid fees or closure in a majority white tract, compared to $748.80 in majority Latinx tracts, $870.50 in majority black tracts, and $957.10 in other tracts.

The Extra Costs of Segregation

Segregation at the national level also shapes the cost of banking. In other words, in addition to the racial disparities across communities described above, white, black, Asian, or Latinx individuals can expect to pay different costs and fees based on their neighborhood-level exposure to other racial groups shaped by national patterns of segregation.1

For example, the extra costs of segregation are apparent in the maintenance fee amounts on banks’ entry-level checking accounts. The average maintenance fee amount of $2.83 varies widely by race and provides evidence of the extra costs of segregation (see Figure 3). Based on their neighborhood-level exposures to other racial groups, the average individual white person can expect to pay a maintenance fee of $6.09 while average black, Latinx, and Asian individuals pay nearly $1 more for the same fee. Despite the fact that these fees appear to be relatively small on average, the extra costs of segregation are disproportionately large. These fees add up over time, contributing to the extra costs that black, Latinx, and Asian individuals pay to maintain entry-level checking accounts.

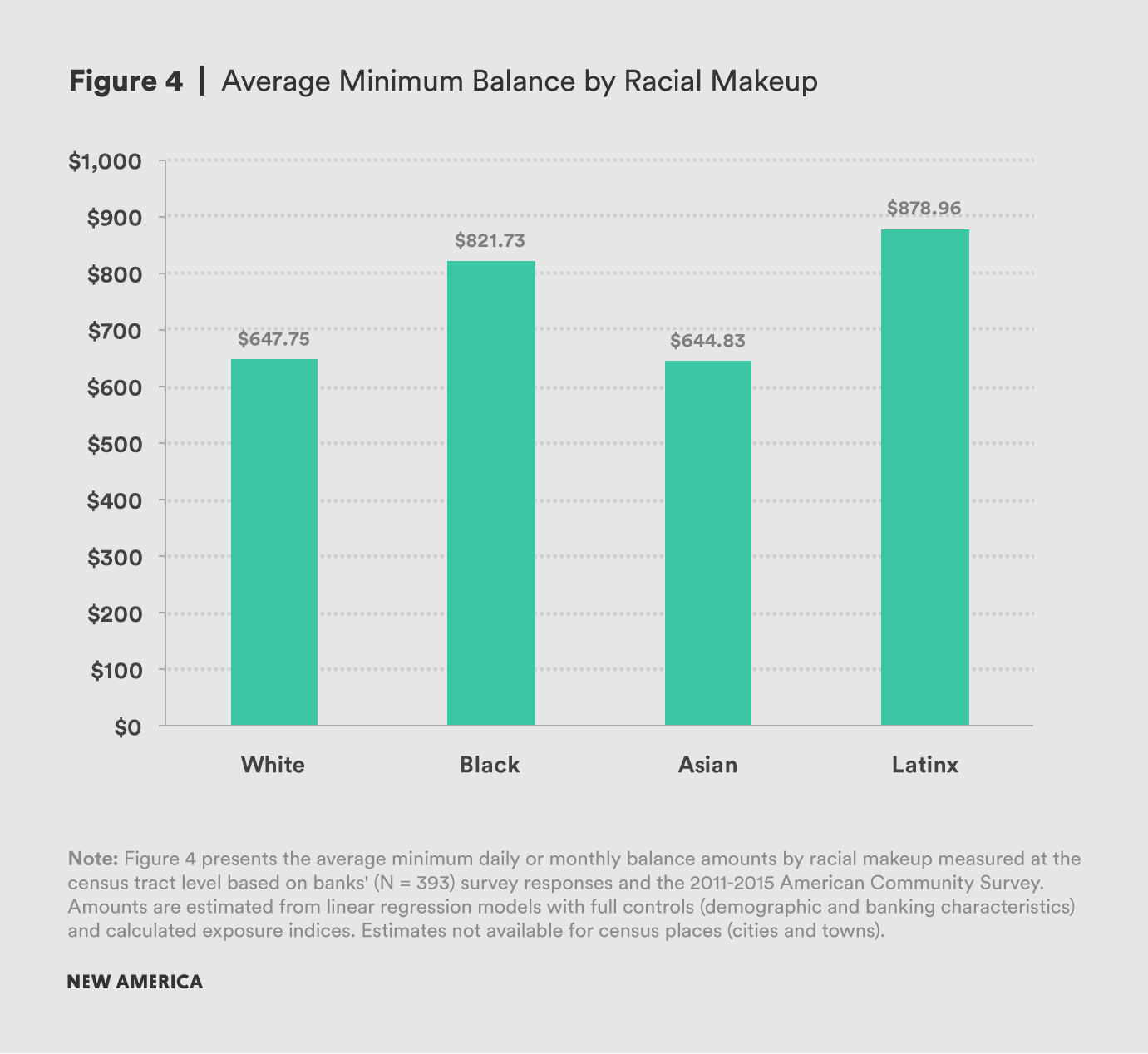

Disparities are also observed within the average minimum balance on entry-level checking accounts. While the average minimum balance is $676.55, based on average exposure to other racial groups, black and Latinx individuals can expect to maintain substantially higher minimum balance amounts (see Figure 4). The average individual white person can expect to maintain a minimum balance amount of $647.75 and the average individual Asian person can expect a balance amount of $644.83. By comparison, average black and Latinx individuals must maintain respective minimum balance amounts of $173.98 and $231.21 more than their white counterparts.

The total costs of segregation are staggering. The differences add up to hundreds of dollars after summing together all the costs and fees that average individuals can expect to pay based on their exposure to other racial groups.2 When compared to whites, the average checking account costs and fees are $190.09 higher for blacks, $25.53 higher for Asians, and $262.09 higher for Latinx.

The average individual white person can expect to maintain a minimum balance amount of $647.75, while the respective minimum balance amounts are $821.73 and $878.96 for the average Black and Latinx individuals.

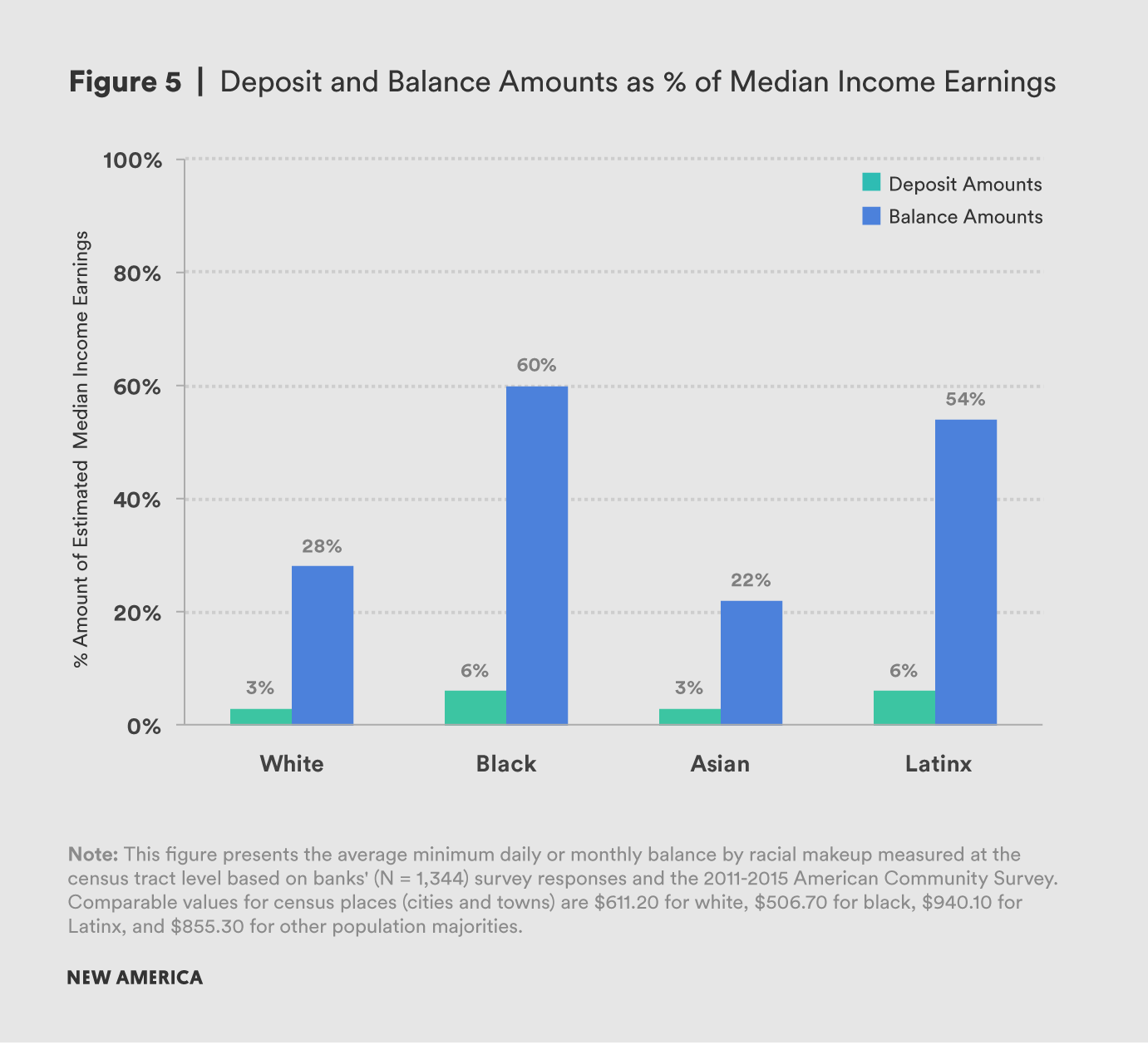

Banks’ costs and fees further limit the economic power of communities of color by requiring more earnings of black and Latinx individuals to be sequestered in checking accounts where they cannot be used (see Figure 5). For instance, based on median annual income earnings for households and assuming 26 paychecks per year, the average paycheck amounts are approximately $2,290 for whites, $1,373 for blacks, $1,640 for Latinx, and $2,856 for Asians. Based on these amounts, the average white individual needs to deposit approximately 3 percent of a paycheck in order to open a checking account in their community and keep 28 percent of a paycheck deposited to avoid a fee or account closure. For Blacks and Latinx, these amounts are more than double. Blacks need to initially deposit 6 percent of a paycheck and keep 60 percent unused in their account and the comparable values for Latinx are 6 percent and 54 percent.

Discretionary (a.k.a. Discriminatory) Banking

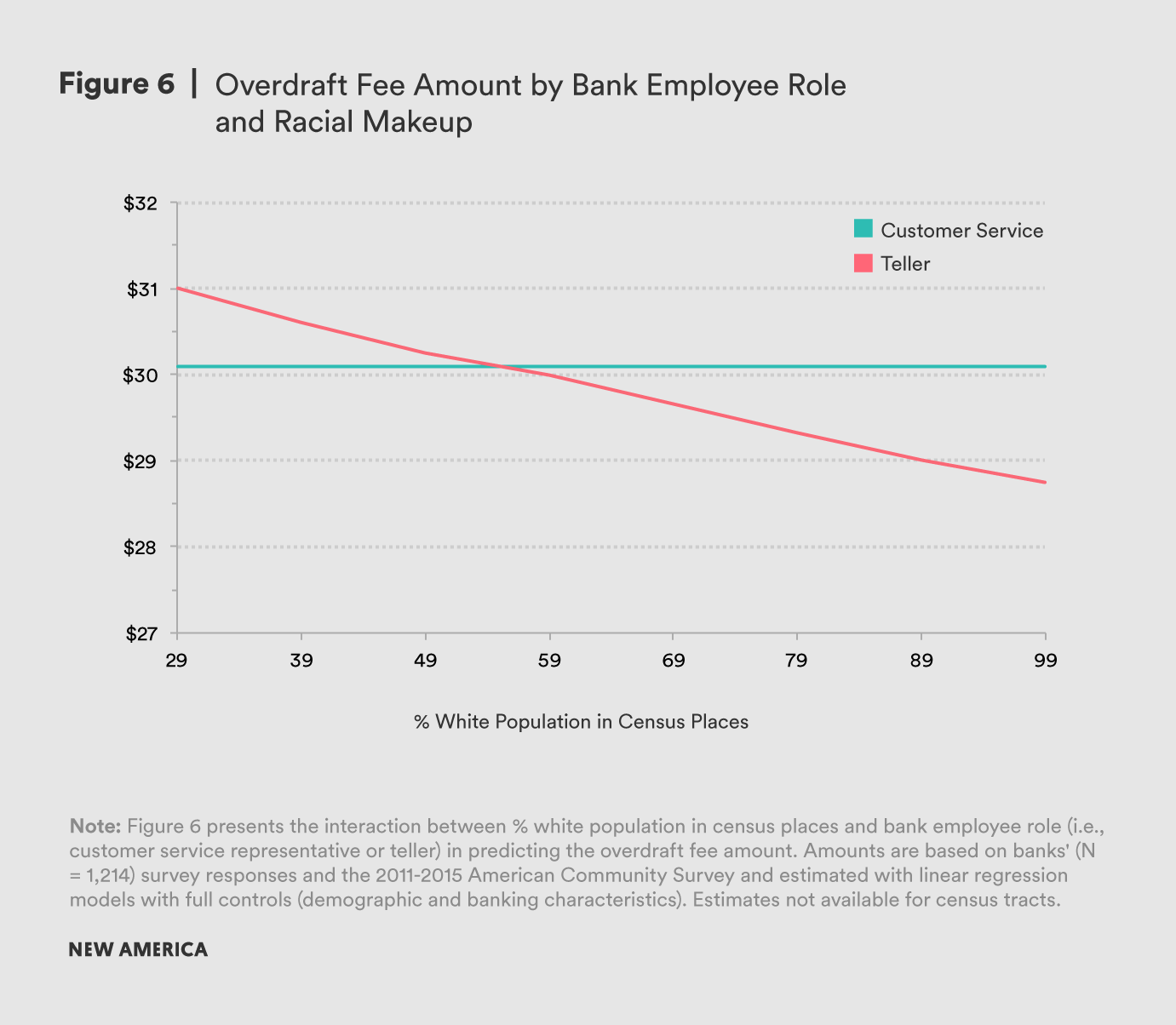

Discretionary banking practices amplify the racialized costs of banking, and evidence of racial bias among tellers suggests that checking account costs and fees depend on who consumers talk to at the bank. In particular, tellers in places with small white populations report significantly higher overdraft fees and greater likelihoods of using credit or screening agencies than tellers in places with large white populations (see Figure 6). The difference between the average overdraft fee amounts in places with the largest and smallest white populations is $2, which may seem like a small amount. However, these fees can accumulate over time and represent ways that banks may be siphoning money out of consumers of color.

Citations

- Please see the technical appendix and Reardon (2002) for more information about segregation and exposure indices. The results presented in this section are based on multivariate models with full controls.

- These costs and fees include the minimum opening balance, minimum balance, maintenance fee, and overdraft fee amounts.