Jason Delisle

Director, Federal Education Budget Project

In the coming weeks, the Senate is expected to begin consideration of a companion bill to the Student Aid and Fiscal Responsibility Act adopted by the House of Representatives last month. In an effort to derail the legislation, which would expand the Direct Loan program and eliminate the Federal Family Education Loan program (FFEL), the student loan industry has been making some pretty outrageous arguments to Senators and staff. Consider our favorite example below from loan industry talking points — which Higher Ed Watch has obtained — that were provided to Senate staff.

MYTH: Forcing all students to borrow Direct Loans will save billions over the next 10 years by eliminating huge subsidies being paid to private lenders.

FACT: Lenders are not being paid subsidies. This year, lenders will pay the government $9 billion in interest that is passed on from borrowers and in fees. (Source: Budget Appendix, page 388)

It is easy to understand why anyone would be confused by such a statement. Why would private lenders care so much about the proposed elimination of FFEL if they weren’t getting any government subsidies under the program? If that were the case, lenders would stand to lose nothing when the program is eliminated — they would be able to continue to make loans to students at the same FFEL borrower terms as before. Nothing in law would prevent them from doing so.

The claim, of course, is absurd. Without a government subsidy, private lenders would not make loans with as favorable borrower terms as those under FFEL. The loans would be unprofitable.

Lenders do indeed receive government subsidies. They receive two separate subsidies that transfer virtually all of the risk and costs of making a FFEL loan to the federal government. The first subsidy is a default guarantee, which means that if a borrower does not repay his or her loan, the government reimburses the lender for 97 percent of the outstanding loan balance. It is a subsidy in the form of insurance.

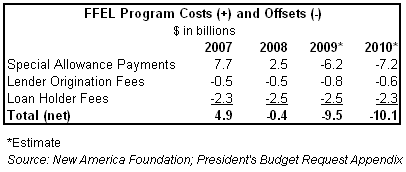

The other subsidy is less straightforward, and not surprisingly, is the subject of the misleading talking point above. This subsidy, called a Special Allowance Payment, sets in law the interest rate that lenders are guaranteed to receive on a FFEL loan. The rate adjusts automatically every three months to reflect short-term market interest rates plus an arbitrary 1.79 percentage points. The federal government pays this rate on the loan no matter how high (or low) short term interest might be. That guarantee, or insurance, is a significant subsidy. The Special Allowance Payment is intentionally designed so that it bears no relation to the interest rates that borrowers pay. Thus, lenders do not earn interest from the borrower; they earn it from the federal government.

Now, where do the lenders come up with the $9 billion figure above? The government uses borrower payments to cover the costs of the interest it guarantees the lender under the Special Allowance Payment. But because the Special Allowance Payment rate fluctuates and the borrower rate is fixed, sometimes the borrower rate is more than enough to cover the rate the government guarantees the lender and other times it is not. In 2007 and 2008 the borrower rate was not enough, so the federal government paid lenders $7.7 billion and $2.5 billion respectively. This year it is estimated that borrower interest payments will more than cover the rate guaranteed lenders, leaving some $6.2 billion left over. Add in other fees lenders pay the government and the total comes to $9.5 billion.

But, the cash value of these payments in any one year is not the value of the government subsidy lenders receive. Rather, the actual subsidy is the expected value of all the future payments associated with a loan. And it is also the value of the guarantees – the insurance against default risk and interest rate risk – that lenders receive from the federal government under FFEL.

This is one of the main reasons why loans are subject to accrual accounting in the federal budget rather than cash accounting. The student loan industry knows this of course… and budget analysts know it, too, but the student loan industry is hoping Senators and their staff do not.

So, Senator, when the loan industry hands you the talking point above, tell them that if government guarantees aren’t a subsidy, then FFEL lenders should have no problem with Congress eliminating these guarantees. Then, tell them that when FFEL is gone, they can continue to make loans to students at 20-year, fixed 6.8 percent interest rates just as they do today and they won’t even have to make those pesky $9 billion payments to the government anymore.

Director, Federal Education Budget Project