Table of Contents

- Introduction

- The Case for Crafting a Millennial Public Policy Agenda

- Part I: Millennial Public Policy Symposium

- Part II: Policy Research Papers

- Independent, Not Alone: Breaking the Poverty Cycle through Transition-Age Foster Care Reform

- Data Sharing as Social Justice: How an Improved Reentry Process Can Smooth the Transition for Formerly Justice-Involved People

- Making the Case for Culturally Responsive Teaching and Supportive Teaching Standards

- The Context of Tradition: Evolving Challenges in Federal Indian Policy

- Public Policy and the Poor People’s Campaign: Reducing Inequality through Political Action

- A Public Interest Test in Merger Review

- Beyond Access: The Future of Voting Rights in the United States

- Solutions for the Health Care Cybersecurity Workforce of the Digital Age

- Taking Down Terrorism: Strategies for Evaluating the Moderation and Removal of Extremist Content and Accounts

- Gridlock: Enhancing Disaster Response Efforts Through Data Transparency in the Electric Utility Sector

- Part III: The Millennial Public Policy Fellows

- Selected Pieces from the Direct Message Blog

A Public Interest Test in Merger Review

by Becky Chao

Concern over the effects of increasing corporate consolidation on competition, inequality, and labor has led to calls for U.S. antitrust law and competition policy to do more.1 The movement to reinvigorate antitrust enforcement includes potential new antitrust laws, including a package of bills introduced in April 2018 that addresses employment-related issues in mergers.2 Among other things, the bills seek to prohibit the consideration of so-called “spurious” economic efficiencies—namely, corporate layoffs—to justify anti-competitive mergers,3 and to provide clarification that the antitrust laws apply not just to monopolies but also to monopsonies.4 These bills could be interpreted as part of the broader call for antitrust to move toward a public interest standard that would be, proponents argue, better equipped to address the effects of consolidation beyond competition.5

But, what does the “public interest” mean? The term is used in different settings by government officials, politicians, and advocates alike. It appears almost interchangeable with concepts like the “common good” and “general will,” alluding to the conflicting interests between a group, community, or society and an individual—or, in the case of mergers, the interests of corporations and the interests of the general public.6 In any case, the meaning of the “public interest” remains unclear.7

This uncertainty permeates the merger review process at the Federal Communications Commission (FCC), which, unlike the antitrust authorities, is charged with a public interest mandate in its review of telecommunications mergers. But while some are calling for antitrust to move toward a public interest standard, the Commission appears to be moving away from one.

In its approval of CenturyLink’s acquisition of Level 3 with conditions in October 2017—the first major transaction approval under Ajit Pai’s tenure as chairman—the Commission signaled three major changes: First, it suggested that the inherent ability to transfer licenses is itself a public interest benefit.8 Second, it stated that the Commission “will not impose conditions to remedy pre-existing harms or harms that are unrelated to the transaction.”9 Third, it suggested a revision to the “balancing test”—the weighing of public interest benefits against public interest harms—it had employed in its merger review up to this point, saying “if the Commission is able to find that narrowly tailored, transaction-specific conditions are able to ameliorate any public interest harms and the transaction is in the public interest, it may approve the transaction as so conditioned.”10 This last statement signaled a departure from the Commission’s record of imposing transaction-related conditions on transaction parties. Together, these three statements suggested a narrowing of the Commission’s public interest test to focus on competitive effects analysis and to avoid addressing issues related to its broader policy objectives, as it had done in previous proceedings. The CenturyLink/Level 3 Order, and the response to it, is indicative of the tensions and disagreements in the Commission’s implementation of its public interest standard.

While some are calling for antitrust to move toward a public interest standard, the Commission appears to be moving away from one.

The debate at the FCC over its public interest standard may be seen as part of a larger trend in U.S. antitrust toward a focus on competitive effects in the last three decades.11 The FCC, however, does not have antitrust authority; as a regulatory agency, its authority is broader than of the antitrust enforcement agencies.12

A public interest standard in merger review has also been discussed and tested in some international domains. Notably, public interest factors are given considerable weight by competition authorities in South Africa, China, and Canada. While competition policies abroad do not solely encompass antitrust laws (just as the FCC’s merger review process does not solely encompass competition nor antitrust), recognizing the international landscape of merger review provides additional context to understanding the implications of a public interest test in merger review generally. In the first section of this report, an examination of public interest approaches to merger review internationally reveals differences in how each country defines the public interest in merger review, and possible mechanisms for preventing the influence of politics on the merger review process.

Next, this report provides an overview of U.S. merger enforcement primarily through antitrust law and explores the application of the public interest standard in the Federal Communications Commission’s merger review. An examination of 31 major transactions reviewed by the Commission under two administrations led by chairmen from different political parties, Democratic Chairman Tom Wheeler from 2013 to 2016 and Republican Chairman Kevin Martin from 2005 to 2009, and the noteworthy Comcast/NBCU merger in 2011 reveals the wide range of non-competition factors that the Commission has considered under its public interest mandate. Through case studies demonstrating how the Commission has addressed three such factors—diversity, universal access, and employment—this paper explores how the evaluation of these factors has led the Commission to exercise significant discretion in its review. Its inconsistent determinations of whether concerns are merger specific and its discretion in imposing conditions on the transaction parties have created much ambiguity in the factors it considers and how it considers them in making decisions.

The FCC does not have antitrust authority; as a regulatory agency, its authority is broader than of the antitrust enforcement agencies.

Finally, this report provides recommendations for how to implement a robust public interest standard in FCC merger review by standardizing its test. Recommendations include identifying factors that should be considered in merger review and codifying the evaluation process. The process can then be institutionalized through guidelines similar to the Department of Justice and Federal Trade Commission’s Horizontal Merger Guidelines, or statutory guidance from Congress.

The Public Interest Debate Abroad

Antitrust scholars Harry First and Eleanor Fox have called the United States “somewhat of an outlier in the international community” because of its rejection of public interest factors in antitrust merger policy.13 A survey of the international landscape, however, calls into question the degree to which this statement holds true. For one, not every country employs a public interest test, and the ones that do tailor their tests to country-specific social, cultural, and political factors. Competition—with its goals of consumer welfare and efficiency—remains the central goal in most jurisdictions, but public interest tests may be carved out to address non-competition factors in specific sectors. Ultimately, the idea of a public interest test in merger control is not standardized in international jurisprudence, and there are significant concerns regarding the susceptibility of a public interest test to political influence.

A Competition Test May Capture Some Public Interest Factors

In some jurisdictions, public interest factors may already be captured in efficiency analysis under a competition framework. South Korea acknowledges the possibility of examining public interest factors as part of efficiency enhancing effects: an increase in employment, regional economy, development of downstream and upstream markets, stable supply of energy, and improvement of environmental pollution.14 Canada, on the other hand, does not specify any public interest factors in its Competition Act or Merger Enforcement Guidelines.15 Its courts, however, have provided guidance on how to treat income redistribution in efficiency analysis.16 The Federal Court of Appeal in Canada (Commissioner of Competition) v. Superior Propane Inc., stated that a “balancing weights” approach that assigns a particular weight to the loss in consumer surplus relative to the gain in producer surplus was better equipped than a total surplus standard to account for income redistribution effects.17 In 2012, the Competition Tribunal stated in Canada (Commissioner of Competition) v. Tervita Corp that it must also “determine whether there are likely to be any socially adverse effects associated with a merger” if the Commissioner puts forth arguments in this vein.18

South Korea and Canada are therefore two examples of efficiency-centered competition regimes that can account for certain public interest factors. In the absence of an explicit public interest framework, competition regimes may think creatively to argue for the consideration of certain factors to be included in merger review under an efficiencies defense.

A Public Interest Test Reflects Country-Specific Goals

The goals of competition policy are contingent on a country’s social, cultural, and political norms. A public interest test in merger review may be structured such that it captures a specific country’s broader policy goals. Generally, developed countries have antitrust laws that focus primarily on efficiency and consumer welfare, whereas developing countries have antitrust laws that also address issues of distribution and power.19

Competition policy in South Africa, for example, serves a dual role: it stimulates competition toward the goal of market efficiency, but it is also part of a broader suite of policy tools aimed at rectifying structural imbalances and past economic injustices.20 In this vein, public interest grounds considered by South African competition authorities include a merger’s potential effects on a particular industrial sector or region, employment, the ability of businesses controlled or owned by historically disadvantaged persons to become competitive, and the ability of national industries to compete in international markets.21

Similarly, China’s competition policy is structured such that it reflects the country’s broader social and economic goals. Article I of the country’s Anti-Monopoly Law (AML) specifies that the law exists “for the purpose of preventing and restricting monopolistic conduct, protecting fair competition in the market, enhancing economic efficiency, safeguarding the interests of consumers and social public interest, [and] promoting the healthy development of the socialist market economy.”22 Article 15 specifies a non-exhaustive list of public interests exemptions to monopolistic conduct that includes conserving energy, protecting the environment, and relieving disaster victims.23

Each nation faces the challenge of designing and implementing a competition regime that addresses both the market dynamics in their country and the unique aspects of broader policy objectives. That is to say, the variety of approaches seen across the international landscape today indicates continuing uncertainty over how best to achieve these goals.

A Public Interest Test Maybe Tailored to Address Non-Competition Factors in Specific Sectors

Where the primary goal of merger control may be competition, jurisdictions may implement a public interest test restricted to specific sectors. A sector-specific approach accounts for specific non-economic factors that are important to the functioning of a healthy market in the sector in question. For instance, a healthy democracy necessarily requires media pluralism, as without access to a diversity of viewpoints, individuals are less likely to come across ideas from multiple perspectives and make their own informed decisions.24 Sector-specific public interest interests have the advantage of limited reach; they do not apply broadly across industries in which these factors are irrelevant.

The variety of approaches seen across the international landscape today indicates continuing uncertainty over how best to achieve these goals.

In this vein, the European Commission considers the effect of a merger in the media space on the diversity of information sources for the purposes of preserving a plurality of opinion and multiplicity of views.25 Beyond the media sector, the European Union Merger Regulation also addresses security issues—such as the production of or trade in arms, munitions, and war material, the security of supply necessary for population health, and prudential rules relating to the financial sector in merger control.26

In Portugal, the Regulatory Authority for the Media may also overrule the competition-based assessment from the Portuguese Competition Authority on the grounds of protecting the freedom and pluralism of the media.27 The Competition Act in Canada specifies that while competition law focuses on a merger’s effects on economic welfare and efficiency, mergers in the finance, transportation, and telecommunications sectors are subject to a public interest test executed by their respective sector regulator.28 Regulators overseeing the finance, communications, and broadcasting industries may also consider public interest factors alongside competition elements in South Korea.29

Limiting the Susceptibility of a Public Interest Test to Political Influence

A public interest test may exacerbate the chances of undue political influence on regulators’ assessment of a deal, leading to unpredictability and inconsistency in merger control. This concern has driven reform of the merger review process in both Norway and the United Kingdom. Other jurisdictions, such as New Zealand and Germany, implement a public interest test secondary to a competition test, which may be a possible mechanism for curtailing the susceptibility of the merger review process to political influence.

From 2004 to 2016, the Norwegian government could overrule its Competition Authority’s decision to block a merger if it found that the merger involved “questions of principle or interests of major significance to society”—a public interest clause.30 These interests included concerns over job loss or competitive effects in local markets.31 Beginning in 2017, however, the Norwegian Parliament eliminated this public interest exception and established an independent competition complaints board. Policymakers justified the change by arguing that “[p]ublic interest considerations are better served by general regulations than political intervention in specific competition cases where the outcome is subject to the influence of the strongest lobbying interests.”32

Merger control in the United Kingdom has also moved away from a broad public interest test out of concerns over political influence. U.K. antitrust authorities previously reviewed mergers under the Fair Trading Act 1973, which implemented a broad public interest test that included employment and national competitiveness.33 The Enterprise Act of 2002, however, codified a competition-based test toward the goal of greater predictability and elimination of “substantial room for the exercise of political preferences.”34 Under current competition policy, the Competition and Markets Authority relies exclusively on economics in its analysis, but it may inform the secretary of state (SoS) when it believes that a merger raises material public interest factors.35 The SoS may then intervene in mergers on specified public interest grounds of national security, media plurality, and the stability of the financial system.36 Public interest considerations are carefully vetted by Parliament prior to SoS adoption.37

Similarly, other jurisdictions conduct a public interest test secondary to a competition test. In New Zealand, antitrust authorities will consider broader public benefits only if it finds that the merger would be likely to substantially lessen competition in a market.38 For the public benefit to be given weight in merger review, it must be transaction-specific.39 The Federal Cartel Office in Germany assesses mergers solely on the basis of competition, but the minister may permit mergers on non-competition grounds in exceptional cases if they outweigh anticompetitive harms, and if doing so does not jeopardize the market economy.40 This two-stage approach not only limits the ability to consider public interest factors in merger review, it also preserves the autonomy of the Federal Cartel Office and isolates any political pressures to the Ministry.41

A two-stage approach involving a competition test before a public interest test may thus be an effective mechanism for curtailing political influence on the merger review process. The current process in the United Kingdom may be the most effective example, as it ensures that public interest factors are properly vetted and specified prior to its adoption in the merger review process.

A two-stage approach involving a competition test before a public interest test may be an effective mechanism for curtailing political influence on the merger review process.

U.S. Sector Regulators Are Charged with a Public Interest Standard in Merger Review

Congress passed the first antitrust law, the Sherman Act, in 1890, followed by the Federal Trade Commission Act and the Clayton Act in 1914.42 These three core federal antitrust laws prescribe the general conditions under which a merger or certain business practices would be considered unlawful. Courts interpreted these statutes and applied them in decisions based on the merits of each case. The modern interpretation of these statutes is to protect and ensure fair competition and to maximize consumer welfare.43

Two federal government agencies enforce these antitrust laws: the Federal Trade Commission (FTC) and the U.S. Department of Justice (DOJ) Antitrust Division. The agencies will consult with each other before launching an investigation into a proposed merger to avoid duplicating efforts. In their investigations, the agencies focus exclusively on competitive factors. Beyond a public interest in the general sense in the enforcement of the antitrust laws,44 there are no public interest factors taken into account in the merger review process by the agencies.45

Mergers in certain sectors, however, may also be subject to a separate review by other federal agencies charged with a broader public interest mandate that goes beyond the scope of competition. The Committee on Foreign Investment in the United States (CFIUS) may block a merger on national security grounds.46 Two sector-specific regulators, the Federal Energy Regulatory Commission (FERC) and the Federal Communications Commission (FCC), review mergers in the electricity and telecommunications sectors, respectively, with a broader public interest mandate.

FERC regulates the interstate transmission of electricity, and both FERC and DOJ review mergers in the electricity sector.47 In accordance with Section 203 of the Federal Power Act, FERC assesses a merger’s effects on competition, rates, and regulation and will approve a merger if it will be “consistent with the public interest.”48

In the telecommunications sector, the FCC and DOJ generally share concurrent jurisdiction over mergers. The FCC is required to review the transfer of telecommunications licenses and authorizations. In accordance with the Communications Act of 1934, as amended, the agency assesses whether a transaction will serve “the public interest, convenience, and necessity.”49 This determination includes an assessment of competitive factors, but whereas the antitrust agencies’ standard, set forth by Section 7 of the Clayton Act, is whether the proposed transaction would “substantially lessen competition,” the FCC must assess whether approving the transaction would preserve and enhance competition.50 In addition, the FCC’s public interest standard encompasses the “broad aims of the Communications Act,”51 which include “examin[ing] the likely effects of the transfer on the private sector deployment of advanced services, the diversity of license holders, and the diversity of information sources and services available to the public.”52 The difference in statutory authority and relevant standards has, at times, led to different outcomes in the merger review process when both agencies review a transaction.53

After reviewing the evidence and public input, the Commission issues its decision.54 It may approve the transaction parties’ application to transfer licenses as submitted, or with conditions to ensure that the transaction serves the public interest.55 If the Commission is unable to approve a transaction, it will refer it to an administrative law judge for a hearing.56

The Public Interest Debate at the Federal Communications Commission

The specter of political influence has loomed over the Federal Communications Commission not only because of the revolving door between the Commission and the companies they regulate57 but also because of its broad public interest standard in merger review.58 The wide scope of this public interest standard has led some to conclude that the agency is more susceptible to political lobbying in its merger review, especially in comparison to the merger review process at the antitrust authorities that looks at competition exclusively.59

An examination of recent major transactions reviewed by the Commission reveals several practices that should be clarified and codified to avoid the appearance of arbitrariness and political influence on its merger review process. These practices relate to whether the Commission’s purview is limited to merger-specific or merger-related public interest factors, its discretion in imposing conditions even when pre-existing rules and regulations require similar actions from the transaction parties already, and its balancing of public interest factors against public interest harms. What follows is a discussion of several case studies exploring these issues in the Commission’s assessment of three commonly cited non-competition public interest factors—diversity, universal access, and employment—in its merger review process. Ultimately, these case studies demonstrate the need for clear and consistent standards in implementing a public interest test in merger review.

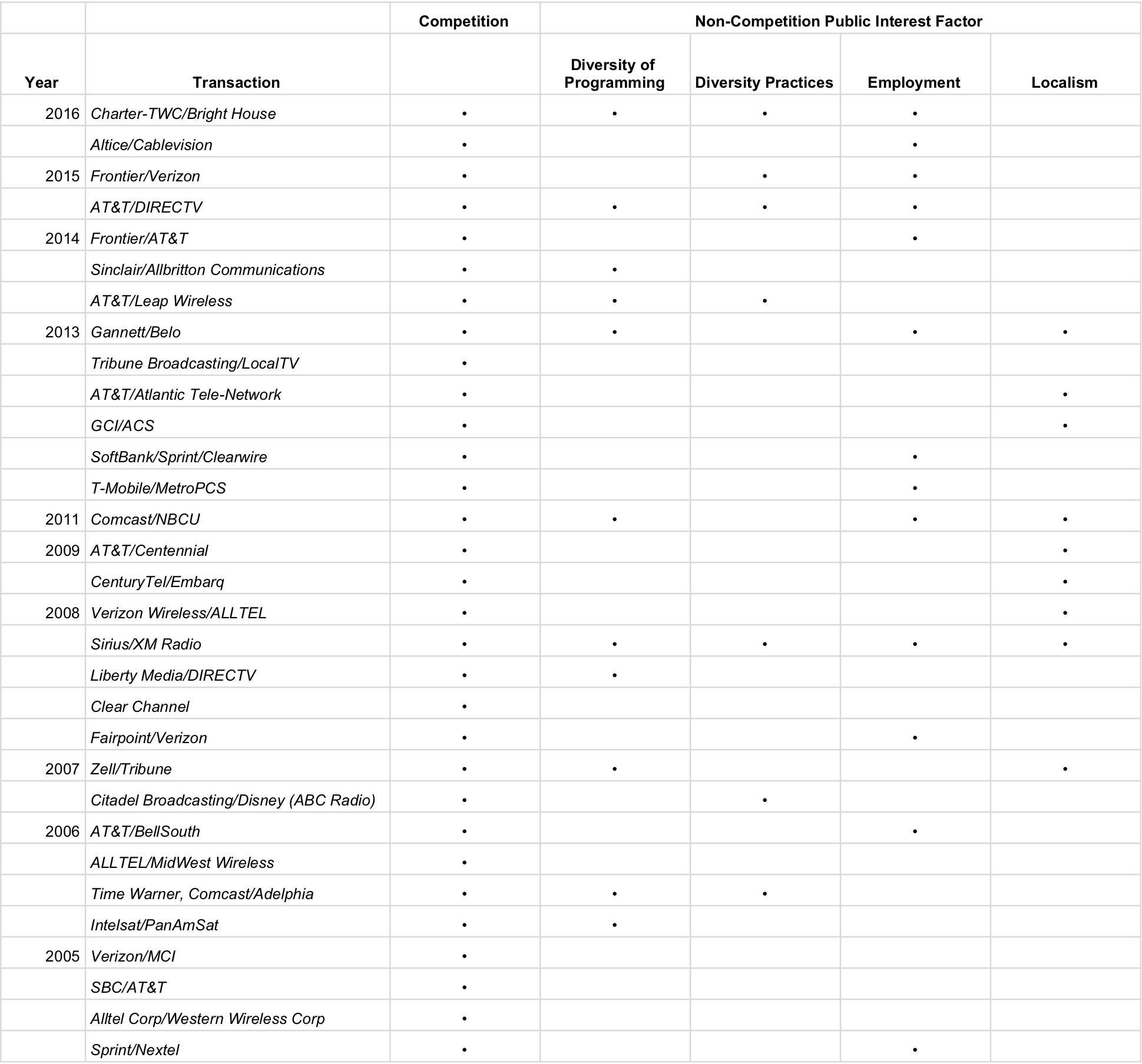

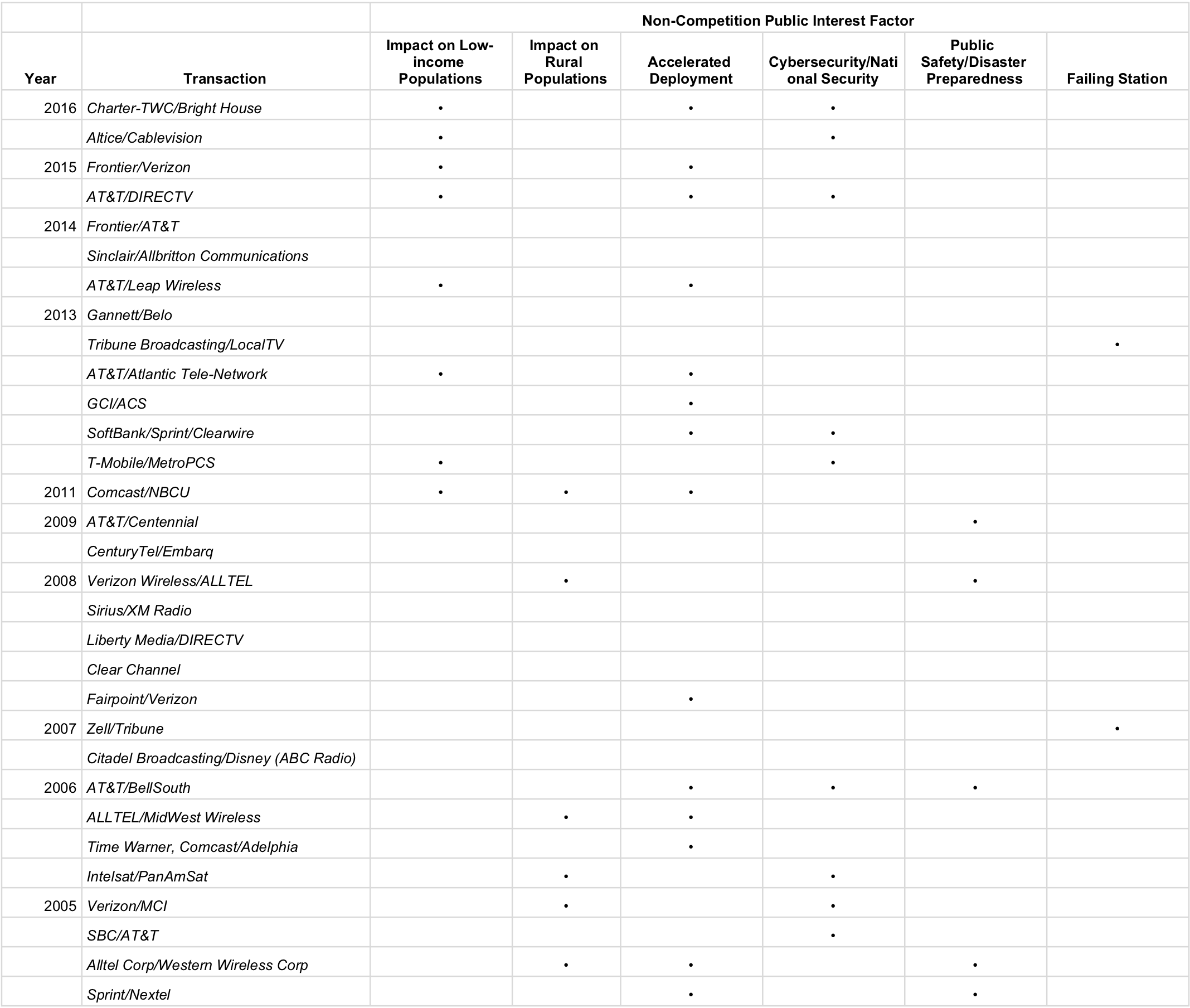

Table 1. Sampling of Public Interest Factors in FCC Merger Review

Source: Federal Communications Commission Major Transaction Decisions

The Commission Does Not Recognize Workforce Diversity as a Public Interest Factor

The Commission has not recognized workforce diversity as a public interest factor in its merger review for three general reasons: First, it finds that workforce diversity is not a merger-specific benefit—that is, the diversity practices in question do not require the parties to merge. Second, there is a question of jurisdiction; the Commission defers to other government agencies like the National Labor Board Relations and Equal Employment Opportunity Commission to address issues in this regard. Third, the Commission’s ability to consider workforce diversity as a public interest factor is limited by relevant case law.

Transaction parties sometimes argue that their diversity practices are a public interest benefit. In Charter-Time Warner Cable/Bright House, the transaction parties attempted to claim their commitment to diversity and inclusion with regards to supplier commitments and corporate governance as a public interest benefit.60 The companies in AT&T/DIRECTV claimed that the merged company would benefit from the application of AT&T’s “best-in-class diversity values.”61 The Commission, however, rejected this argument in both transactions on the basis that the diversity practices described in the parties’ application are not specific to the transaction; the parties could, in theory, implement the diversity practices independently as separate entities.62

Commenters have also raised concerns over a company’s employment practices with respect to workforce diversity. In Comcast/NBCU, commenters expressed concern over the transaction parties’ lack of diversity within management, drawing a connection between a media producer’s diversity in staff and diversity of programming.63 The Commission, however, deemed the issue to be both unrelated to the transaction and overseen by other government agencies like the National Labor Relations Board, Equal Employment Opportunity Commission, and relevant state authorities.64

In Comcast/NBCU, commenters expressed concern over the transaction parties’ lack of diversity within management, drawing a connection between a media producer’s diversity in staff and diversity of programming.

The efficacy of workforce diversity as a public interest factor, however, is limited by the courts. While the 1973 decision in TV 9, Inc. v. FCC found that the Commission’s public interest statutory mandate granted it discretion to expressly consider race and ethnicity in the adjudication of license applications,65 its ability to consider workforce diversity as a public interest factor, however, was restricted by Lutheran Church-Missouri Synod v. FCC in 1998. In the latter case, the court ruled that the Commission’s Equal Employment Opportunity requirements for hiring minorities and women were unconstitutional and found that the agency only has authority to pass anti-discriminatory measures in which the discrimination in question relates to programming.66 There are nuances in what diversity of programming precludes; namely, there is a difference between programming that serves the interests of minorities and programming created by minority-owned stations. Researchers nonetheless have suggested, at least, an imperfect correlation between the two, and—along with a handful of commissioners, including Michael Copps67—have called on the agency to “consider whether a marketplace model that has led to a demonstrable drop in the ownership percentages of minorities truly serves the public interest.”68 To fully account for diversity as a public interest factor in the merger review process at the Commission, then, it may be first necessary to undo the repercussions of Lutheran Church-Missouri Synod v. FCC. Whereas the Commission has discretion in interpreting its public interest mandate, its discretion is restricted by relevant legal factors, such as current case law.

The Commission’s Evaluation of Diversity of Programming as a Public Interest Factor Appears Ambiguous and Inconsistent

The Commission’s evaluation of diversity of programming as a public interest factor across transactions contributes to the perception that its review is inconsistent and ambiguous. First, the Commission exercises discretion in deferring to existing rules and regulations that require certain actions from companies in the industry or imposing conditions that require these actions from the specific transaction parties in response to concerns raised by commenters relating to diversity of programming. This discretion, combined with the Commission’s inconsistent determinations of whether diversity in programming concerns are merger-specific, has created ambiguity in its merger review process. This ambiguity is further exacerbated when the Commission fails to demonstrate that it has verified the weight of these factors in its analysis and the cost-benefit analysis indicating that the merger as approved is clearly in the public interest.

In Charter-Time Warner/Bright House, the Commission found that many of the concerns raised by commenters relating to program carriage decisions—specifically that these decisions would disproportionately affect diverse, minority-owned, or minority-focused video programmers—lacked merger specificity and supporting evidence.69 Instead, the Commission found that the concerns dealt more with industry-wide issues, and relied on economic analysis submitted by the parties that showed a lack of incentive for the merged company to discriminate against these programmers.70 It therefore deferred to existing program carriage rules to address any allegations of discriminatory conduct that may arise instead of imposing conditions on the transaction parties.71

The Commission found that many of the concerns relating to program carriage decisions—that these decisions would disproportionately affect diverse, minority-owned, or minority-focused video programmers—lacked merger specificity and supporting evidence.

In Comcast/NBCU, however, the Commission imposed conditions on the transaction parties to enhance its Spanish language programming in response to “legitimate concerns expressed in the record by commenters concerning the potential impact of the proposed transaction on localism” within Spanish-language-speaking communities.72 The Commission’s diverging decisions to address diversity of programming concerns raised by commenters in Comcast/NBCU and to reject similar concerns on lack of merger-specificity grounds in Charter-Time Warner/Bright House may give rise to the impression that its merger review process is inconsistent.

But there is one critical difference between the two cases: the concerns raised by commenters in Charter-Time Warner Cable/Bright House alleging New Charter’s ability to foreclose or discriminate in program carriage decisions were general and not based on any specific evidence or analysis.73 In Comcast/NBCU, on the other hand, the Commission relied on evidence submitted by commenters demonstrating harm to Spanish-language viewers when NBC acquired Telemundo in 2002 to preempt similar issues of potential harm to diversity of programming in this transaction.74

Nonetheless, the Commission did not address whether the concern of potential harm to diversity of programming was merger-specific in the Comcast-NBCU Order.75 While the imposed conditions would create public interest benefits by protecting what researchers have called “preference externalities,”76 then-Commissioners Robert M. McDowell and Meredith Attwell Baker objected to weighing these commitments in the Commission’s public interest test on grounds that they were not related to the underlying transaction.77 The different responses of the Commission to diversity in programming concerns in Comcast/NBCU and Charter-Time Warner/Bright House contribute to the appearance that the Commission is inconsistent in its merger review. These case studies also raise the question of whether the Commission has the authority to evaluate transactions with broader policy goals in mind and address merger-related public interest concerns toward these goals.

A related issue concerns the Commission’s process of measuring public interest factors and the role that quantifying these factors plays in imposing conditions on transactions. In Sirius/XM Radio, commenters raised concerns that the merger would lead to reduced competition that “would diminish the incentive to innovate and provide diverse programming,” and that the reduced channel capacity would harm diversity of programming.78 The Commission did not address whether these concerns were merger specific in this transaction either, and ultimately found that Sirius/XM Radio’s voluntary commitments to set aside eight percent of channels on both platforms to qualified entities and non-commercial educational use would mitigate the potential harm from a decrease in diversity.79

These case studies raise the question of whether the Commission has the authority to evaluate transactions with broader policy goals in mind and address merger-related public interest concerns toward these goals.

What is noticeably absent, however, is an explanation as to why these commitments would offset the potential public interest harms to diversity in programming created by this transaction. Indeed, in his dissent, then-Commissioner Jonathan S. Adelstein noted that,

Granting the merger under this [‘worst-case’ scenario] approach [of assuming that the proposed transaction represents a merger to monopoly] should require significant conditions, proportional to the significant public interest harm assumed, in order to mitigate the extreme concentration of market power. Regrettably, the majority’s acceptance of the Applicants’ ‘voluntary commitments’ fails to meet this professed prophylactic public interest standard because of gaping loopholes in them.80

One of Adelstein’s underlying points is that public interest factors should be measurable. When the Commission fails to verify the weight of these public interest factors in its analysis and demonstrate that the cost-benefit analysis tilts clearly in the public interest, it contributes to the perception that its merger review process is inconsistent.

The Commission Exercises Significant Discretion over Merger-Related Conditions Addressing Universal Access

The Commission exercises significant discretion in assessing—and modifying—transaction parties’ proposed broadband offerings for low-income consumers in line with its larger policy objective of promoting universal access by ensuring that “all Americans have access to robust, affordable broadband and voice services.”81 The Commission’s assessment of whether this aspect of a merger is merger-specific, however, varies. The Commission also holds significant discretion in imposing conditions around the merging parties’ low-income broadband offerings as part of its public interest test, such that it might impose conditions that are deemed to be merger-related.82 Where it draws the line between merger-specificity and merger-relatedness, however, is a question of its regulatory purview; while the Commission sometimes rejects applicants’ proposed broadband offerings for low-income consumers because the transaction parties can independently offer the services without the merger already, it has, at times, modified these services and specified plan requirements in order to deem it a public interest benefit. Whether the Commission can promote the larger goal of universal access in the merger review process insofar as the item is transaction-specific, as opposed to transaction-related, is unclear.

These conditions vary from merger to merger, and have included requirements around plan specifics, including price, program duration, enrollment benchmarks, and enforcement mechanisms;83 standalone broadband offerings;84 and eligibility.85 The variation in plan requirements raises questions about how this public interest benefit is quantified. The Commission’s overall discretion over items that relate to its goal of universal access contributes to the perception that its merger review process is inconsistent.

The Commission sometimes accepts discount offerings for low-income consumers as a public interest benefit arising from the transaction, but it also rejects them in other transactions. In Altice/Cablevision, the Commission accepted Altice’s low-income broadband package proposal as “firm and definite commitments from Altice and, accordingly, credit[ed] them as a benefit to support a finding that the transaction is in the public interest.”86 The same year, however, in Charter-Time Warner/Bright House, the Commission found Charter’s proposed plan to offer standalone broadband service to low-income households to be a benefit that is not transaction-specific, as “any of the Applicants could offer a low-income broadband program absent the transaction.”87 Instead, the Commission imposed enrollment benchmarks at regular intervals and enforcement mechanisms around the program88 to “ensure that the public benefits of the transaction outweigh the potential harms.”89 Commissioner Michael P. O’Rielly objected to this specific condition in his statement, saying that “These changes don’t make the program any more relevant to the transaction than it was when the applicants made the initial offer, nor does the item even attempt to justify this as a remedy to any transaction-specific ‘harm.’”90

The Commission’s overall discretion over items that relate to its goal of universal access contributes to the perception that its merger review process is inconsistent.

Similarly, in Comcast/NBCU, the Commission relied on imposed conditions and voluntary commitments made by the merging parties to “ensure that the transaction serves the public interest.”91 These conditions included broadband adoption and deployment commitments targeted toward serving low-income households made by Comcast.92 These commitments toward removing barriers that keep low-income consumers from accessing the internet were in part why then-Commissioner Mignon Clyburn ultimately voted to approve the deal,93 but they are also among those singled out by McDowell and Baker for lacking merger specificity.94

These examples demonstrate the flexibility that the public interest standard grants the Commission so that it may fulfill its policy objectives to ensure that low-income consumers have access to affordable broadband. Whether the Commission can address this larger goal in the merger review process insofar as the item is transaction-specific, as opposed to transaction-related, is unclear. This difference in priorities may be distinguished along party lines, with Democratic commissioners like Clyburn more inclined to prioritize broader policy objectives in fulfilling the Commission’s public interest standard in merger review, and Republican commissioners like McDowell and Baker, on the other hand, more inclined to ensure that the Commission’s review is limited to merger-specific public interest factors.

The Commission Is Unclear on Whether Employment Is a Public Interest Factor

The Commission has historically considered employment-related issues in its public interest analysis.95 These issues include job creation, commitments to honor union bargaining contracts, and efficiencies resulting from workforce reduction. The extent to which employment factors into its public interest analysis, however, is ambiguous. While the Commission has generally found that employment-related issues are often not verifiable, it has signaled support for these factors in its merger review. For example, the Commission has not recognized commitments toward job repatriation as public interest benefits, but it has sometimes accepted them as evidence that a public interest harm from employment-related issues is unlikely to arise. The agency’s different approaches to evaluating employment under the contexts of potential benefits and harm to the public interest may be attributed to an issue of evidence. Nonetheless, the extent to which it counts employment as a public interest factor remains ambiguous.

Perhaps the most noteworthy example of an employment-related issue in FCC merger review is the transaction parties’ voluntary commitment toward job repatriation in AT&T/BellSouth. Though the Order did not evaluate the public interest merits of this commitment—and it clearly noted that while the commitment was enforceable, it was not a “general statement of Commission policy and [did] not alter Commission precedent or bind future Commission policy or rules”—it was well-received by at least one commissioner.96 In his concurring statement to the Order, then-Commissioner Copps praised this voluntary commitment from the transaction parties:

Because the loss of jobs is so often the first cost-cutting move of any merger, I am pleased at the company’s willingness to repatriate approximately 3,000 jobs from overseas back to the United States, with at least 200 jobs being created in the hurricane-ravaged area of New Orleans. I believe this commitment is the first such job repatriation ever to accompany a telecom merger. While I fear other jobs will be lost, this provides at least some job comfort for the company’s employees.97

Given this positive reception, transaction parties have attempted to argue that similar intentions to repatriate jobs to the United States were a public interest benefit in subsequent mergers. In Charter-Time Warner Cable/Bright House, the parties held that their commitment to increase customer care through domestic investment and insourced jobs (i.e., by bringing thousands of overseas Time Warner Cable jobs back to the United States) was a public interest benefit.98 However, the Commission found that the transaction parties failed to articulate precise actions in this regard.99 These promises were also unverifiable, given the parties’ claims that the merger would bring significant cost-savings efficiencies, specifically by eliminating redundant positions.100 The Commission therefore concluded that the transaction parties failed to demonstrate the verifiability of their proposed labor practices as a public interest benefit, suggesting that job repatriation under certain contexts could be considered a public interest benefit.101

While the Commission has not explicitly recognized commitments toward job repatriation as public interest benefits, it has sometimes accepted them as evidence that a public interest harm from employment-related issues is unlikely to arise. Commenters have argued that a public interest harm exists with the potential loss of employment resulting from a transaction. While the Commission dismissed these concerns as speculative in Altice/Cablevision102 and T-Mobile/MetroPCS,103 the Commission took a different approach to similar concerns raised by Communications Workers of America (CWA) in Frontier/Verizon.104 In separate discussions between Frontier and CWA, Frontier committed to “employment security protections, the addition of 150 jobs in California and 60 jobs in Texas, a commitment to a 100 percent U.S. based workforce, operational flexibility to enhance the service experience for customers, and two-year extension of the collective bargaining agreements.”105 The Commission then accepted these commitments as assurances that the transaction would be unlikely to result in public interest harms related to the loss of employment.106

Conclusion and Recommendations

Many competition authorities around the world have adopted a public interest framework in merger review to address non-competition public interest factors, such as preserving employment, protecting national security and defense, and promoting opportunities for populations that have been historically disadvantaged. Each of these competition regimes account for country-specific social, economic, and political goals, and the variety of approaches seen across the international landscape today indicates continuing uncertainty over how best to achieve these goals.

There are also legitimate concerns around the use of a public interest test. Because of its amorphous nature, the public interest test may also be susceptible to political influence. Indeed, the prevalence of this concern in Norway and the U.K. led to the elimination and curtailment of their respective public interest tests. Countries like Germany and New Zealand also have grappled with how to balance competition concerns against public interest ones—after all, without proper checks, public interest factors may easily be used to justify competitively harmful mergers.

Each of these competition regimes account for country-specific social, economic, and political goals, and the variety of approaches seen across the international landscape today indicates continuing uncertainty over how best to achieve these goals.

This concern relates to the Federal Communications Commission’s use of its public interest standard. Its statutory mandate is broad and undefined; the Supreme Court has said that it “no doubt leaves wide discretion, and calls for imaginative interpretation.”107 The courts have provided some clarification into how the Commission may apply its public interest mandate toward the interrelated goals of enriching diversity of programming and workforce diversity. The Commission has been less clear, however, on how it considers other public interest factors, such as universal access and employment. The Commission’s standard is further complicated by its ad hoc treatment of universal access and employment issues—especially when these factors manifest as voluntary commitments or imposed conditions against the context of anti-competitive concerns or public interest harms.

The Commission should aim to standardize its public interest test. The Commission should first identify the values that are critical to preserving a healthy media sector, including localism and diversity, from the outset. In deciding whether to adopt a public interest factor in merger review, the intended goals of these factors should be weighed against the goals of competition. The Commission should establish whether the specific factor aligns with national social, cultural, and economic objectives relative to the media sector and therefore made a priority in merger review. To minimize the risk of approving competitively harmful mergers, the Commission should perform a competitive analysis prior to performing a public interest test. These public interest factors should be verified, quantified, and weighed to the best of the regulator’s ability. The process for evaluating these factors should be transparent, with clear indication that the Commission has confirmed and evaluated the public interest factors and conducted a cost-benefits analysis to indicate that the transaction is in the public interest, in order to minimize the suggestion that its review is inconsistent.

To achieve these goals, the Commission could create a set of guidelines for its public interest test that specifies these factors and the process for weighing them against competition, similar to the Horizontal Merger Guidelines adopted by the Department of Justice Antitrust Division and the Federal Trade Commission, for example. Alternatively, Congress may provide statutory guidance by passing clarifying legislation or enacting a national media policy.

This does not mean, however, that a public interest test should be applied uniformly across all merger review in the United States. Each sector is unique, and, therefore, merger review requires greater scrutiny to identify the non-competition values that are critical to that particular sector. As mentioned briefly in this paper, FERC also employs a public interest standard in its review of electricity mergers.108 But the public interest factors that matter in telecommunications mergers do not necessarily translate to electricity mergers. There may also be other statutes or procedural mechanisms that ensure that its merger review process is clear and consistent. These are areas of potential further research into how a public interest test works in merger review. As the examples from the international landscape of competition policy and the FCC’s merger review demonstrate, regulators must exercise caution in implementing a public interest test in merger review.

Becky Chao is a 2017-18 Millennial Fellow with the Open Technology Institute at New America. She gives many thanks to Sarah Morris, Josh Stager, Sean P. Sullivan, Janet Kim, Caroline Holland, and Matthew Gessesse for their thoughtful and insightful comments on her paper; Open Technology Institute, Melody Frierson, Reid Cramer, and the Millennial Public Policy Fellows for their constant encouragement and support; and Maria Elkin, Angela Spidalette, and the rest of the Communications and Events team for communications and programming support.

Citations

- See Eric Posner and Glen Weyl, “The Real Villain Behind Our New Gilded Age,” New York Times, May 1, 2018, source; The Editorial Board, “How Mergers Damage the Economy,” New York Times, November 1, 2015, source.

- “House Democrats Unveil Legislation to Protect American Workers Against Anti-Competitive Employment Practices,” Congressman David Cicilline, April 26, 2018, available at source.

- Restoring and Improving Merger Enforcement Act of 2018, HR 5642, 115th Cong., 2d sess., (April 26, 2018).

- Economic Freedom and Financial Security for Working People Act of 2018, HR 5630, 115th Cong., 2d sess., (April 26, 2018). Monopsony refers to a market situation in which there is only one buyer.

- K. Sabeel Rahman and Lina Khan, “Restoring Competition in the U.S. Economy” in Untamed: How to Check Corporate, Financial, and Monopoly Power, (Washington, DC: Roosevelt Institute, June 2016), source.

- Anthony Downs, “The Public Interest: Its Meaning in a Democracy,” Social Research 29, no. 1 (1962): 1-36, source; Norman P. Barry, “The Public Interest and Democracy,” in An Introduction to Modern Political Theory, (London: Palgrave, 1995), 260-297.

- Anthony Downs, “The Public Interest: Its Meaning in a Democracy,” Social Research 29, no. 1 (1962): 1-36, source.

- In re Applications of Level 3 Communications, Inc. and CenturyLink, Inc. for Consent to Transfer Control of Licenses and Authorizations, Memorandum Opinion and Order, WC Docket No. 16-403, FCC 17-142 (2017) (“CenturyLink-Level 3 Order”), ¶ 10.

- Ibid., ¶ 9.

- Ibid., ¶ 11. In a footnote, the Commission suggests that it has not allowed “potential competitive harms to go unremedied nor allowed them to be offset by benefits that are not transaction-specific, i.e., benefits that do not naturally arise from the transaction at issue” in an ostensible contradiction of its balancing test. Then-Commissioner Mignon Clyburn disagreed with this characterization of the Commission’s balancing test in practice.

- The antitrust statutes may in fact cover broader policy goals than modern antitrust law considers. Earlier Supreme Court cases suggest a more expansive standard (see, e.g., Brown Shoe Co., Inc. v. United States, in which the Clayton Act is interpreted to protect small competitors against more efficient rivals, and Appalachian Coals, Inc. v. United States, in which the Court permitted price fixing as a way to avoid excessive competition; the latter is almost certainly bad law today), but these older cases do not represent how U.S. antitrust law works today.

- See United States v. FCC, 652 F.2d 72, 88 (D.C. Cir. 1980), in which the Court states that the FCC is “entrusted with the responsibility to determine when and to what extent the public interest would be served by competition in the industry.”

- Harry First and Eleanor M. Fox, “Philadelphia National Bank, Globalization, and the Public Interest,” Antitrust Law Journal 80, no. 2, (2015), source.

- “Note by Korea,” Public Interest Considerations in Merger Control (123rd Meeting of Organisation for Economic Co-operation and Development Working Party No 3 on Co-operation and Enforcement, June 14-15 2016), source.

- Canada Competition Act, and “Merger Review Process Guidelines,” September 8, 2015, source.

- “Note by Canada,” Public Interest Considerations in Merger Control (123rd Meeting of Organisation for Economic Co-operation and Development Working Party No 3 on Co-operation and Enforcement, June 14-15 2016), source.

- Ibid. In Canada (Commissioner of Competition) v. Superior Propane Inc. (2001), after the Federal Court of Appeal sent the matter back for redetermination, the Tribunal once again permitted the merger to proceed on the basis of a successful efficiencies defense, but noted that “the Tribunal must accept that redistribution effects can legitimately be considered neutral in some instances, but not in others. Fairness and equity require complete data on socio-economic profiles on consumers and shareholders of producers to know whether the redistributive effects are socially neutral, positive or adverse.”

- Ibid.

- Eleanor M. Fox, “Economic Development, Poverty, and Antitrust: The Other Path,” Southwestern Journal of Law and Trade in the Americas 13 (2007), source.

- “Note by South Africa,” Public Interest Considerations in Merger Control (123rd Meeting of Organisation for Economic Co-operation and Development Working Party No 3 on Co-operation and Enforcement, June 14-15 2016), source.

- South Africa Competition Act 89 of 1998, Section 12(A)(3).

- China Anti-Monopoly Law, Article I.

- Ibid., Article 15.

- See Petra Bárd and Judit Bayer, A Comparative Analysis of Media Freedom and Pluralism in the EU Member States (Brussels: Policy Department for Citizens’ Rights and Constitutional Affairs, 2016), source.

- European Union Merger Regulation, Article 21.

- Ibid.

- “Note by Portugal,” Public Interest Considerations in Merger Control (123rd Meeting of Organisation for Economic Co-operation and Development Working Party No 3 on Co-operation and Enforcement, June 14-15 2016), source.

- Canada Competition Act.

- “Note by Korea,” Public Interest Considerations in Merger Control (123rd Meeting of Organisation for Economic Co-operation and Development Working Party No 3 on Co-operation and Enforcement, June 14-15 2016), source.

- Norway Competition Act in 2004, Section 21.

- “Note by Norway,” Public Interest Considerations in Merger Control (123rd Meeting of Organisation for Economic Co-operation and Development Working Party No 3 on Co-operation and Enforcement, June 14-15 2016), source.

- Ibid.

- Federico Mor, Contested mergers and takeovers (London: House of Commons Library, 2018), source.

- “Note by the United Kingdom,” Public Interest Considerations in Merger Control (123rd Meeting of Organisation for Economic Co-operation and Development Working Party No 3 on Co-operation and Enforcement, June 14-15 2016), source.

- Ibid.

- Ibid.

- Ibid.

- “Note by New Zealand,” Public Interest Considerations in Merger Control (123rd Meeting of Organisation for Economic Co-operation and Development Working Party No 3 on Co-operation and Enforcement, June 14-15 2016), source.

- Ibid.

- “Note by Germany,” Public Interest Considerations in Merger Control (123rd Meeting of Organisation for Economic Co-operation and Development Working Party No 3 on Co-operation and Enforcement, June 14-15 2016), source The Minister has previously considered non-competition factors such as technological progress, international competitiveness, employment (including safeguarding jobs and protecting workers’ rights), energy supply, and healthcare access.

- Ibid.

- “Guide to Antitrust Laws: The Antitrust Laws,” Federal Trade Commission, source.

- See Barak Orbach, “How Antitrust Lost Its Goal,” Fordham Law Review 81, no. 5 (2013), source, and Steven C. Salop, “Question: What is the Real and Proper Antitrust Welfare Standard? Answer: The True Consumer Welfare Standard,” Loyola Consumer Law Review 22, no. 3 (2010), source.

- See, e.g., Swedish Match, 131 F. Supp. 2d at 173 (D.D.C. 2000) (“There is a strong public interest in effective enforcement of the antitrust laws.”); U.S. v. Ivaco, Inc., 704 F. Supp. 1409, 1430 (W.D. Mich. 1989) (“By enacting Section 7, Congress declared that the preservation of competition is always in the public interest.”).

- “Note by the United States,” Public Interest Considerations in Merger Control (123rd Meeting of Organisation for Economic Co-operation and Development Working Party No 3 on Co-operation and Enforcement, June 14-15 2016), source.

- 50 U.S.C. §4565.

- Stuart Chemtob, “The Role of Competition Agencies in Regulated Sectors,” (remarks, 5th International Symposium on Competition Policy and Law, Beijing, China, May 11, 2007).

- 16 U.S.C. §824(b).

- Communications Act of 1934, 47 U.S.C. §214(a), §310(d). The FCC is also authorized to analyze telecommunications mergers under Section 7 of the Clayton Act. 15 U.S.C. §21.

- “Overview of the FCC’s Review of Significant Transactions,” Federal Communications Commission, source.

- See In re Applications of AT&T and DIRECTV for Consent to Assign or Transfer Control of Licenses and Authorizations, Memorandum Opinion and Order, 30 FCC Rcd 9131 (2015) (“AT&T-DIRECTV Order”), ¶ 19.

- “Overview of the FCC’s Review of Significant Transactions,” Federal Communications Commission, source.

- See In re Applications for Consent to the Transfer of Control of Licenses, XM Satellite Holdings Inc., Transferor, to Sirius Satellite Radio Inc., Transferee, Memorandum Opinion & Order, 23 F.C.C.R. 12348, 12349 (2008) (“Sirius/XM Radio Order”), ¶ 7 (stating that the Commission approves the Sirius/XM Radio transaction with voluntary commitments and imposed conditions), 29 (stating that the Department of Justice closed its investigation of the transaction without taking any enforcement actions).

- “Overview of the FCC’s Review of Significant Transactions,” Federal Communications Commission, source.

- Ibid.

- Ibid.

- Hayley Tsukayama, “FCC commissioner Meredith Baker to join Comcast-NBC,” Washington Post, May 12, 2011, source.

- See, e.g., In re Applications of Comcast Corporation, General Electric Company, and NBC Universal, Inc. for Consent to Assign Licenses and Transfer Control of Licenses, Memorandum Opinion and Order , 26 FCC Rcd 4238, 4247 (2011) (“Comcast-NBCU Order”), Dissenting Statement of Commissioner Ajit Pai (Pai calls the current merger review process at the Commission, “fact-free, dilatory, politically motivated, non-transparent decision-making”), and Comcast-NBCU Order, Joint Concurring Statement of Commissioners Robert M. McDowell and Meredith Attwell Baker.

- Jonathan Baker, “Antitrust Enforcement and Sectoral Regulation: The Competition Policy Benefits of Concurrent Enforcement in the Communications Sector,” Articles in Law Reviews & Other Academic Journal, (2013), source.

- In re Applications of Charter Communications, Inc., Time Warner Cable Inc., and Advance/Newhouse Partnership for Consent to Assign or Transfer Control of Licenses and Authorizations, Memorandum Opinion and Order, 31 FCC Rcd 6327, 6479 (2016) (“CharterTWC-Bright House Order”), ¶ 433-436.

- AT&T-DIRECTV Order, ¶ 389.

- CharterTWC-Bright House Order, ¶ 438 and AT&T-DIRECTV Order, ¶ 389.

- Comcast-NBCU Order, ¶ 219.

- Ibid., ¶ 223.

- TV 9, Inc. v. FCC, 495 F.2d 929, 938 (D.C. Cir. 1973). The court stated: “To say that the Communications Act, like the Constitution, is color blind, does not fully describe the breadth of the public interest criterion embodied in the Act. Color blindness in the protection of the rights of individuals under the laws does not foreclose consideration of stock ownership by members of a Black minority where the Commission is comparing the qualifications of applicants for broadcasting rights in the Orlando community. The thrust of the public interest opens to the Commission a wise discretion to consider factors which do not find expression in constitutional law.”

- See Lutheran Church-Missouri Synod v. FCC, 141 F.3d 344 (D.C. Cir. 1998).

- Michael Copps, Transcript: Prepared Statement – FCC Meeting, PBS (Dec. 18, 2007), source.

- Jason Allen, “Disappearing Diversity? FCC Deregulation and the Effect on Minority Station Ownership,” Indiana Journal of Law and Social Equality 2, no. 1, Article 11 (2013), source.

- CharterTWC-Bright House Order, ¶ 273-275.

- Ibid.

- Ibid.

- Comcast-NBCU Order, ¶ 198-202. The Commission required Comcast-NBCU to air original, locally produced and locally oriented news programming to the Spanish language-speaking community for 1,000 hours per year for three years.

- CharterTWC-Bright House Order, ¶ 274.

- Comcast-NBCU Order, ¶ 196n514. The Commission cites comments from Free Press attesting to NBC’s “gutt[ing]” of local newscasts and jobs at Telemundo despite promises to improve the quality of Spanish language news when NBC acquired Telemundo in 2002.

- Ibid., ¶ 198-202.

- Peter Siegelman and Joel Waldfogel, “Race and radio: Preference externalities, minority ownership, and the provision of programming to minorities,” in Advertising and Differentiated Products (Advances in Applied Microeconomics, Volume 10), ed. Michael R. Baye and Jon P. Nelson (Emerald Group Publishing Limited, 2001), 73 – 107, source. Siegelman and Waldfogel calls “preference externalities” social benefits derived by minority consumers from being in the same market as others with similar preferences. They note the substantial differences in white and minority content preferences, concluding that inefficient under-provision may more likely be an issue for small minority populations.

- Comcast-NBCU Order, Joint Concurring Statement of Commissioners Robert M. McDowell and Meredith Attwell Baker.

- Sirius/XM Radio Order, ¶ 70,

- Ibid., ¶ 134, 134n437, 135, 141. The transaction parties voluntarily committed to lease four percent each of full-time audio channels on both the Sirius and XM platforms to Qualified Entities and another four percent of capacity for noncommercial educational use. A Qualified Entity is any entity that is “majority-owned by persons who are African American, not of Hispanic origin; Asian or Pacific Islanders; American Indians or Alaskan Natives; or Hispanics.”

- Ibid., Dissenting Statement of Commissioner Jonathan S. Adelstein.

- “Telecommunications Access Policy Division,” Federal Communications Commission, source.

- CharterTWC-Bright House Order, ¶ 452-453.

- Ibid.

- Ibid., Appendix B: “Conditions”, VI “Discounted Broadband Services Offer”. The Commission finds it “in the public interest to ensure that a bundle of video and broadband services is not the consumer’s only competitive choice, and this protection may be particularly important for low-income subscribers who may not be able to afford bundled services. Thus, we impose this Condition to ensure an affordable, low-price standalone broadband service is available to low-income consumers in the Company’s wireline footprint.”

- Ibid., specifying that “eligible enrollee[s]” are families with at least one child who participates in the National School Lunch Program or seniors age 65 or older receiving Supplemental Security Income (SSI) program benefits.

- In re Applications Filed by Altice N.V. and Cablevision Sys. Corp. to Transfer Control of Authorizations from Cablevision Sys. Corp. to Altice N.V., Memorandum Opinion and Order, 31 FCC Rcd 4365, 4372-75 (2016) (“Altice-Cablevision Order”), ¶ 47. Altice proposed to offer low-income consumers 30 Mbps for $14.99 a month throughout Cablevision’s service territory.

- CharterTWC-Bright House Order, ¶ 450-452. The standalone broadband plan was for 30/4 Mbps for $14.99 per month.

- Ibid., Appendix B: “Conditions”, VI “Discounted Broadband Services Offer”. The merged company must offer this reduced price broadband service within six months of closing the transaction for at least four years, though the company may increase the monthly fee for this product by maximum $3.00 after three years. It must provide this discounted broadband service to at least 25,000 households by the end of the first year of closing the transaction; 100,000 by the end of the one-year-and-a-half; 225,000 by the end of two years; 475,000 by the end of three years; and 525,000 by the end of four years.

- Ibid., ¶ 453.

- Ibid., Statement of Commissioner Michael P. O’Rielly, Approving in Part, Concurring in Part, and Dissenting in Part.

- Comcast-NBCU Order, ¶ 6, 233, Appendix A: “Conditions”, XVI. Conditions to Expand Broadband Deployment and Adoption.

- Ibid. Comcast committed to providing approximately 2.5 million low-income households with high-speed internet access for less than $10 per months for three school years. In addition, the combined company promised to expand its broadband network to reach an additional 400,000 homes in the three years after the transaction closes, provide broadband internet in six additional rural communities, and provide free high-speed internet to 600 new schools and libraries in underserved, low-income areas.

- Ibid., Statement of Commissioner Mignon L. Clyburn.

- Ibid., Joint Concurring Statement of Commissioners Robert M. McDowell and Meredith Attwell Baker.

- CharterTWC-Bright House Order ¶ 443; In re Applications of Nextel Comm., Inc. and Sprint Corp., for Consent to Transfer Control, Memorandum Opinion and Order, 20 FCC Rcd 13967, 13976 (2005) (“Sprint-Nextel Order”), ¶ 168-9; Comcast-NBCU Order, ¶ 224.

- AT&T Inc. and BellSouth Corporation Application for Transfer of Control, WC Docket No. 06-74, Memorandum Opinion and Order, 22 FCC Rcd 5662, 5672, (2007) (“AT&T-BellSouth Order”), ¶ 222.

- Ibid., Concurring Statement of Commissioner Michael J. Copps.

- CharterTWC-Bright House Order, ¶ 439.

- Ibid., ¶ 444.

- Ibid.

- Ibid.

- Altice-Cablevision Order, ¶ 26-7.

- In re Applications of Deutsche Telekom AG, T-Mobile USA, Inc., and MetroPCS Communications, Inc. for Consent to Transfer of Control of Licenses and Authorizations, WT Docket No. 12-301, Memorandum Opinion and Order and Declaratory Ruling, 28 FCC Rcd at 2333-34, 2334-5 (2013) (“T-Mobile-MetroPCS Order”), ¶ 76, 80.

- In re Applications Filed by Frontier Communications Corporation and Verizon Communications Inc. for Assignment or Transfer of Control, WC Docket 09-95, Memorandum Opinion and Order, 25 FCC Rcd 5972, 5980-81-83 (2010) (“Verizon/Frontier Order”), ¶ 29-30. CWA sought “concrete commitments […] to ensure that the transaction [would] not lead to any reduction in employment levels, workers’ living standards, and service to customers.”

- Ibid.

- Ibid.

- FCC v. RCA Communications, Inc., 346 U.S. 86, 90 (1953).

- 16 U.S.C. §824(b).