Table of Contents

- About the LEO Policy Working Group

- Foreword

- Executive Summary

- A Brief Introduction to Low Earth Orbit (LEO) Satellites

- Chapter I. Fueling Connectivity from Space: Spectrum Sharing and Coexistence

- Chapter II. The Final Economic Frontier: Satellite Competition in Low Earth Orbit

- Chapter III. Connectivity from New Horizons: How LEO Satellites Help Bridge the Digital Divide

Chapter III. Connectivity from New Horizons: How LEO Satellites Help Bridge the Digital Divide

Introduction

Recent advancements in satellite technology have made Low Earth Orbit (LEO) satellite service a viable and, in some cases, cost-effective broadband connectivity solution. While the emerging technology is well-positioned to help bridge the digital divide, LEO service brings its own tradeoffs for deployment and use compared to terrestrial broadband solutions. These differences should be taken into account as policymakers craft regulations and programs designed to bring—and keep—everyone online. This chapter offers policymakers key considerations and recommendations for how to utilize LEO satellite service to expand broadband access across the country.

The Digital Divide Persists

Today’s world is increasingly online, and the inability to get or stay connected can severely impact a person’s education, health, economic, civic, and social opportunities. The digital divide—or the gap between those who are connected to the internet, as well as the devices and skills needed to access it, and those who are not—persists both in the United States and abroad.

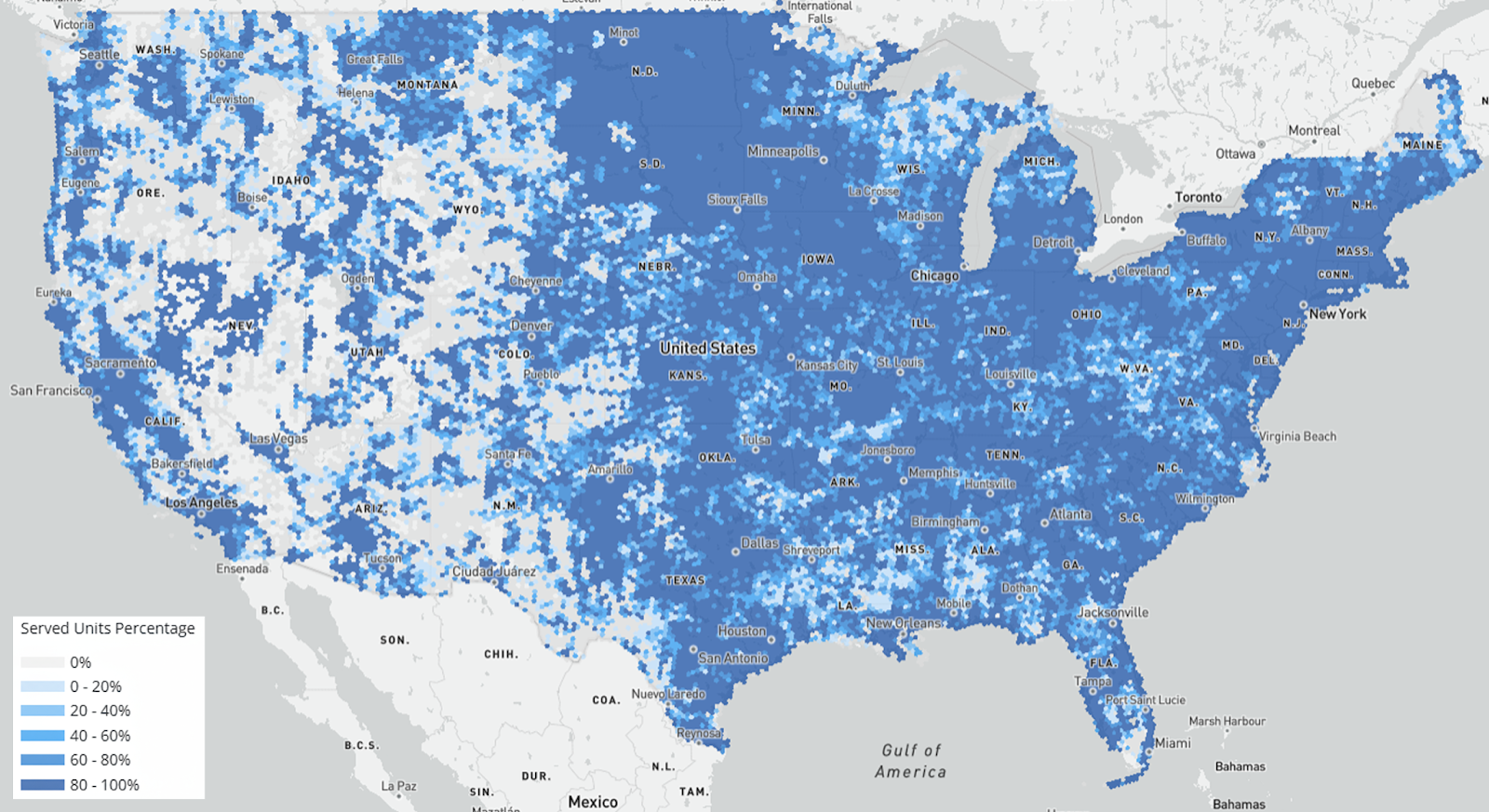

Barriers to universal service generally fall under the three overarching categories of access, affordability, and adoption. These factors are often interrelated and must all be comprehensively addressed to bring everyone online. In terms of access in the United States, the 2023 Internet Use Survey by the National Telecommunications and Information Administration (NTIA) found that 12 percent of people lived in households without any internet connection.1 In 2024, the Federal Communications Commission (FCC) found that 24 million Americans still lacked access to 100/20 Mbps fixed terrestrial broadband service—including 28 percent of people in rural areas and 23 percent of people on tribal lands.2 See Figure 5 for the FCC’s National Broadband Map (updated December 2024).

Screenshot from “FCC National Broadband Map,” Federal Communications Commission, December 31, 2024, broadbandmap.fcc.gov/home.

However, the availability of internet in an area does not guarantee quality of service, which is typically defined with respect to downlink and uplink throughput speeds. The Infrastructure Investment and Jobs Act of 2021 outlines requirements for “reliable broadband service,” categorizing areas as “unserved” if they have no broadband connectivity at all or have service less than 25/3 Mbps; and marked all areas with access to broadband service below 100/20 Mbps as “underserved.”3 These categories align with the FCC’s benchmark for broadband service at 100/20 Mbps with less than 100 milliseconds latency.4

Moreover, even when service is available, many users may still not subscribe to it. Cost of deployed service is consistently cited as a major driving factor inhibiting household connectivity, alongside lack of user interest and low digital skills.5 Despite recent gains in access and adoption, a small percentage of Americans still say that they do not use the internet at all—some because they are simply uninterested.6 This lack of interest can be associated with low digital skills, an area ripe for policy intervention where the United States is currently failing to act (for example, by instituting a framework for measuring digital skills rates or creating a federal digital upskilling program).7 While policy challenges remain to address all causes of the digital divide, technological advances embodied in LEO constellations have shrunk the scope of the problem by offering a new deployment method to reach the remaining unconnected.

LEO Satellite’s Role in Reaching the Remaining Unconnected

LEO satellites can aid digital divide efforts by helping address remaining deployment gaps and reducing the number of unserved and underserved households. LEO satellite systems rely on three main components—the satellite constellation, ground stations, and user terminals—to deliver internet services. Once a satellite constellation is launched, it can be recruited to provide internet service to any equipped area or household along its orbital path. While mountainous areas, tree canopies, and other geographic conditions may disrupt the necessary line-of-sight from ground terminals to LEO constellations, LEO satellite service remains uniquely equipped to reach many of the remaining unserved areas in the United States, especially rural, remote, and other hard-to-reach locations that are difficult to service through traditional terrestrial means. In addition, LEO satellites can provide improved speeds for areas that are underserved, such as those relying on relatively slow DSL service. By operating in the closest orbital range to Earth, low altitudes grant LEO systems the ability to deliver high-speed, low-latency service where capacity is available.

LEO systems’ potential to close deployment gaps has spurred projects to deliver broadband to unserved and underserved households. For example, public school districts are tapping into satellite connectivity to bring students online.8 In October 2020, the Ector County Independent School District in Texas became the first school district to pilot LEO satellite technology to help connect students to the internet.9 North Carolina launched a pilot program in 2021 using LEO satellites to support remote learning opportunities for students and educators. Tribal lands have also used LEO satellites to bring broadband to their communities. The remote Hoh Indian Reservation in Washington began using Starlink beta services in 2020, and in 2025, the Navajo Nation announced its own pilot to better connect five chapters. Several states, such as Alaska,10 Arizona,11 Maine,12 and Washington,13 are increasingly looking to LEO satellite technology to bring connectivity to rural and remote communities.

Working Internet ASAP: A Closer Look at Maine’s LEO Satellite Program

In October 2024, Maine Connectivity Authority (MCA) announced its Working Internet ASAP (WIA) program to bring internet connections to the remaining 1.5 percent—approximately 9,000 remote and rural homes—that have no access to any type of broadband service.14 The program aimed to provide those households with Starlink’s LEO satellite service by the end of 2025.

Under WIA, Maine purchased LEO satellite hardware in bulk and reserved network capacity to provide eligible households a near-immediate option for internet service while areas await connectivity projects funded by the Broadband Equity, Access, and Deployment (BEAD) program. For enrolled households, the MCA subsidized LEO hardware and installation support (which proved key to deployment, but is not covered by BEAD, the current major federal broadband deployment program). MCA also provided digital skills materials and partner information to facilitate service adoption. Rather than excluding those locations from future subsidy programs, MCA ensured program locations remain eligible for future terrestrial deployments funded by the BEAD program or would receive the same service offered by these future programs.15 In addition, MCA established provisions for reserving additional tranches of LEO network capacity for future connectivity under BEAD.

While the program has quickly rolled out internet connections to households with no other technology available, enrollments have been slow despite vigorous outreach efforts. Affordability remains a key barrier, with some eligible households declining service due to the $120 monthly cost. For those who did activate service, a majority of Maine Starlink users experience upload and download speeds that meet or exceed the state program requirements.

Maine’s WIA program offers valuable insight into how other state and federal programs can integrate emerging satellite technology to bridge the digital divide. WIA was able to rapidly deploy an internet connection option to those without any access while leaving itself the flexibility to scale both satellite and fiber connections. At the same time, the program maximized available funds while remaining aligned with federal deployment efforts. Indeed, MCA’s approach has helped inform connectivity plans in numerous other states.

However, lagging uptake signals that adoption must be incentivized in order to meaningfully bring everyone online. Although uptake in other areas of the country may vary—particularly since Maine, which has many vacation and second homes, may not be representative of the country as a whole—the overall trend still suggests that affordability remains a key barrier in satellite service adoption.

Considerations for Bridging the Digital Divide with LEO Satellites

All broadband solutions come with their own tradeoffs—service performance, capacity, outages and disruptions, cost and speed of deployment, and service affordability—that should be considered when choosing a solution to meet a community’s needs. Users can connect to the internet through wired connections (fiber-optic, coaxial cable, and DSL) or wireless connections (satellite, fixed wireless, and cellular service).16 Traditionally, fiber internet is seen as the gold standard for connectivity given its reliability, equipment longevity, high capacity, and potential to scale with demand. These features have led government programs to generally prioritize fiber deployment. However, the cost of deploying fiber can be high, especially in rural, hard-to-reach, and remote areas. Other connectivity methods, such as cable and cellular services, can offer fast speeds, but users are more likely to experience higher latency, service disruptions, or degradations, particularly during peak usage times. Older technologies, like DSL or Geostationary Earth Orbit (GEO) satellite internet, lag behind other forms of connectivity but have sometimes been the only solution available in an area.17

Recent satellite and launch technology advances have lowered costs of LEO system development and deployment, making the technology a viable option for broadband delivery. For U.S. policymakers determining if and how to best incorporate LEO satellites into state and federal broadband programs, we offer several key considerations in the following sections.

A. Speedy Deployment

LEO satellites require less on-the-ground infrastructure buildout than existing methods, which can result in speedy deployment in certain areas. Once a satellite constellation is launched and approved for commercial operation, it can be tapped to provide internet access to any area with the appropriate receiving terminals in view of supporting ground gateways. This means that LEO satellites can bring new households online without extensive route-by-route infrastructure deployments in the area. Where LEO satellite capacity is already available, service can be deployed to households relatively quickly with the installation of a user terminal. However, increasing the number of users a LEO system can serve while maintaining performance standards requires adding capacity to the network. This can be done by adding more satellites to the constellation or through satellite technology improvements.

For hard-to-reach and rural areas that would traditionally require extensive (and expensive) terrestrial buildout, LEO satellite service can be a faster, more cost-effective alternative. Unlike the cost model of a fiber build, in which very high up-front costs are incurred in return for decades of reliable service, LEO satellite operates on the premise that the significant fixed costs to launch a constellation will be offset by low marginal costs to add subscribers until the network’s capacity is reached. Since LEO satellites function as a single network constellation, the benefits and costs of increasing capacity are shared across the entire network rather than being location specific.18 On the other hand, technology upgrades and ongoing network maintenance costs are relatively more expensive for LEO systems (such as repeated replacement of individual satellites at the end of their lifespan—for Starlink, approximately five years) than for terrestrial networks. The fact that LEO systems typically have low up-front marginal costs, but higher operating expenditures, over long periods has significant implications for pricing and affordability, as well as how government subsidies are structured (discussed below).

This deployment structure also means that satellite providers’ cost models—and likely, in turn, the amount and form of subsidized deployment support they require—vary based on the location of the area intended to be served and the available capacity within the constellation network. However, true cost comparisons can be obscured by existing subsidies, which historically prioritized wireline (and recently fiber), that help networks cover the cost of delivering service to expensive-to-serve areas in order to lower the cost to the consumer. These subsidies can be directed at fixed deployments with ongoing support for operating expenditures (for example, the FCC’s High Cost program) or implicitly through affordability subsidies to users (for example, the federal Lifeline and the now-defunded Affordable Connectivity Program).19 While Starlink’s technology development, vertical integration, and growth has benefited enormously from U.S. government contracts, it does not receive Universal Service Fund (USF) subsidies for either deployment or operating costs, which makes apples-to-apples comparisons difficult.

B. Improving Performance

LEO satellite service performance continues to improve. Starlink, which is at present the only residential LEO satellite internet provider in the United States, has seen substantial improvements in performance since its initial launch in 2019. The FCC’s current benchmark for broadband service is 100/20 Mbps with less than 100 milliseconds latency.20 Starlink currently offers download speeds between 25 and 220 Mbps, with the claim that most users experience speeds over 100 Mbps and some users experience speeds as fast as 300 Mbps.21 Upload speeds are advertised between 5 and 20 Mbps. Starlink latency is listed between 25 and 60 milliseconds on land, with some remote areas experiencing latency of 100 milliseconds or more. While this range can meet the FCC’s reliable broadband service requirements, it means that Starlink’s service may not meet the standard consistently, in all areas, or for both fixed and mobile service. Starlink has previously struggled to meet these requirements, leading in part to the FCC’s 2022 decision to revoke its application for funding from the Rural Digital Opportunity Fund (RDOF), part of the USF’s High Cost program.22 Recent analysis shows that while users receive fast download speeds and low latency, which meets most modern internet user needs, lagging upload speeds mean only 17.4 percent of Starlink users are consistently getting broadband that meets FCC requirements.23

Improvements in satellite technology and increased satellites in orbit can improve LEO systems’ performance. Starlink has an application pending to launch a new generation of satellites that promise to reach gigabit speeds. At the same time, Kuiper, which is set to be fully operational in two years, claims its service will deliver speeds up to 400 Mbps for residential customers and up to 1 Gbps for commercial customers.24 Pending FCC rulemakings with proposals to increase the spectrum and transmit power for NGSO systems are likely to substantially enhance LEO capacity; this is discussed in Chapter I.

C. Capacity Challenges

Despite LEO satellite performance improvements, capacity remains its greatest challenge. Several factors can contribute to capacity constraints. Due to their orbital speed, a constellation of hundreds or thousands of LEO satellites is typically needed to provide consistent service to an area, with users connecting to a different satellite in a constellation every few minutes. Similarly, heavy traffic or oversubscription in a particular area can be detrimental to performance. Starlink has attempted to offset this challenge by charging hundreds of dollars in “congestion fees” to subscribers in heavily subscribed areas.25 In addition, insufficient numbers or proximity of the ground terminals and gateways that backhaul data traffic to and from the internet can limit a LEO system’s available capacity in a particular area. While LEO satellites may be able to reach most households, a LEO system does not have the capacity to serve all the locations it can reach. Indeed, a recent Vernonburg Group analysis found that Starlink has the capacity to serve only 26 percent of BEAD-eligible locations with broadband that reliably meets FCC performance standards (100/20 Mbps), which equates to less than seven eligible locations per square mile.26

Advances in technology are likely to mitigate some of these concerns: For example, LEO satellite providers are already able to use steerable beams to direct capacity to areas on a network that may be serving more users or experiencing a surge. Technological advancements, further constellation buildout, and pending FCC proposals to increase spectrum access and power levels are likely to boost LEO system capacity substantially in the near future. But for the time being, guaranteeing reliable broadband at the benchmark performance goal of 100/20 Mbps and less than 100 milliseconds of latency, particularly for all users in an area at once, remains a challenge.

D. Subscription Costs and Competition

Current LEO satellite subscription costs, while comparable to other rural provider costs, are still higher than the national average and may deter adoption. Starlink’s standard residential plan is priced at $120/month with a $349 fee for the standard hardware kit for advertised speeds up to 350+ Mbps download and 10–20 Mbps upload.27 Depending on location, users may face a one-time congestion fee—which in some states can be several hundreds dollars.28 These high up-front fees and monthly subscription prices will deter financially constrained consumers from subscribing. While Starlink recently debuted an $80 “residential lite” plan meant to offer an affordable alternative, the service offers slower speeds (advertised as reaching 45–130 Mbps download speeds and 10–20 Mbps upload speeds) and are deprioritized in favor of the full-cost home service. Starlink has offered promotional plans offering free consumer equipment, and most recently announced a $59/month-for-one-year promotional deal for new customers in certain areas—the cheapest satellite service that has been offered to consumers to date.29 Meanwhile, surveys show the national average for internet service ranges from $75–$90/month for packages that generally offer at least 100Mbps download speeds.30 Of course, it is generally the case that for those in rural areas, the types of internet services available—such as GEO satellite service—tend to be more costly on average, and more likely subject to congestion and monthly download limits. These problems have been ameliorated to some degree with LEO service, which offers a higher-quality user experience, but pricing concerns remain.

Moreover, one of the benefits of LEO satellite’s provision of broadband services is increased intermodal competition, which may eventually drive down prices for consumers. While Starlink has increased availability and access to internet service in many areas, satellite’s overall share of the broadband market is not yet large enough to put competitive pressure on most other internet service providers. However, it is unclear how and if other broadband providers will adapt to compete as more reliable, faster, and possibly lower-priced LEO satellite service becomes available. In particular, smaller telecommunications providers may have a harder time adjusting pricing than larger providers such as Starlink and Kuiper.

E. Targeted Use of LEO Satellite Service

LEO satellite broadband is promising, but it should be considered part of the connectivity toolkit rather than a standalone solution. Current LEO satellite capacity constraints should inform decisions for how, when, and to what degree to rely on it as a solution today. While capacity is likely to improve, LEO service’s potential trajectory implies scalability, which will reach some natural stopping point, rather than an unlimited ability to expand. While LEO systems may never be able to fully meet the needs of high-density urban and suburban areas (many of which are served by fiber), other communities, like those in remote and hard-to-reach areas, may find LEO systems to be their best option available for the foreseeable future. In other cases, LEO satellite service can serve as a stopgap measure or augment available connectivity for unserved and underserved areas. With 85 percent of Starlink consumers residing in rural areas, LEO broadband performance may still be an improvement in internet access—especially for the 11 percent of Starlink users who report they are first-time internet subscribers.31 LEO systems can also provide alternative methods for connectivity in areas or situations where existing solutions face heavy traffic or outages, providing supplemental broadband to city centers and major events, or in cases of disaster response.

LEO-based connectivity solutions are an emerging and constantly developing field, where existing challenges—such as performance, capacity, and price—may be relatively short-lived. The field has grown exponentially since Starlink first launched satellites in 2019, and policymakers should be cognizant of how ongoing developments of the field will impact the overall calculus of determining the viability, reliability, and cost-effectiveness of LEO broadband service. In the United States, Starlink is the only available residential broadband provider, but as Amazon’s Kuiper comes online in the United States during 2026, competition could increase, lowering prices or improving plans available to consumers. (See also Chapter II.) In addition, spectrum management decisions can also improve the efficiency and capacity of LEO systems.

The Existing Broadband Subsidy Landscape

Federal subsidy programs that help lower the cost of broadband are one important tool to help bring all households online. The FCC’s USF, which originally supported access to affordable phone service, has expanded to support the deployment of broadband infrastructure and provide subsidized services for low-income households, schools, libraries, and rural health care providers.32 In response to the COVID-19 pandemic, Congress established the Affordable Connectivity Program (ACP), a broadband subsidy program that defrayed the monthly cost of a broadband subscription for over 20 million households.33 Despite the program’s success and improved outcomes for participating households, ACP officially ended in May 2024 after Congress failed to renew funding, resulting in 23 million households losing support.34

Congress also dedicated $42.45 billion to the Broadband Equity, Access, and Deployment (BEAD) program.35 BEAD is the largest one-time federal investment in broadband infrastructure deployment to date, intended to finally close the infrastructure deployment gap to help bring remaining unconnected households online.

Of the programs working to address the digital divide in the United States, the vast majority of funding focuses on deployment of the necessary infrastructure to provide all households with access to broadband service. Today’s unserved and underserved households are largely those in hard-to-reach, rural, remote areas, and tribal lands. These “high-cost” areas often lack access because the necessary infrastructure for service is too expensive to build out or maintain.36 Cost challenges can result from geographic complexities, such as difficult terrains or long distances to households that require more materials and labor for deployment. If an area is sparsely populated, providers may determine there are not enough potential consumers to cover the cost of operating in the area, nor enough expected ongoing revenue to generate an adequate return. As a result, broadband access in these high-cost areas is often heavily subsidized, with government programs supporting both deployment and operating expenses.

Historically, these programs have prioritized terrestrial wireline technologies—most recently, fiber-optic cable—as the most reliable long-term technology. This can be seen in satellite’s general exclusion from the federal USF High Cost program that has long been the cornerstone for subsidizing access to broadband in the United States. Through much of these programs’ lifespan, the only commercially available satellite service relied on GEO satellites and was generally incapable of meeting many programmatic guidelines.37 More recently, LEO satellite providers have been allowed to participate in some universal service programs but have still faced concerns over the service’s ability to reliably meet programmatic performance benchmarks.38

LEO satellites were also initially deprioritized within BEAD. Following the congressional directive to subsidize technologies able to easily scale with growing needs, NTIA’s initial guidance prioritized mainly fiber-optic cable technology and lumped LEO service together with unlicensed fixed wireless as an “alternative” technology that could only be funded in areas where no other, more reliable technology was feasible.39 Early state bid results under the original program’s rules suggested that satellite service made up a fraction of many states’ final selections.40 Until very recently, LEO satellite service has been resoundingly passed over by a broadband policy landscape with an appetite for fiber.

A. The Turn Toward Tech Neutrality

In June 2025, with many states on the cusp of starting BEAD deployment through their selected providers, the Trump administration released new programmatic guidelines that required states to reopen the selection process and evaluate new bids on a more tech-neutral basis. In the guidelines, the Department of Commerce removed the end-to-end fiber preference and redirected the program to prioritize minimizing BEAD outlays per project so long as applicants meet some baseline quality standards.41 Many states have now revised their BEAD plans to incorporate LEO to varying degrees. Although NTIA approval is still pending, it appears that while some states have still found fiber-to-the-home to be the best solution in many locations, some are projecting significant reliance on satellite coverage (sometimes upward of 40 or 50 percent).42

The shift comes as satellite service quality and capacity have markedly improved since the RDOF era. The LEO satellite service offered (and ultimately rejected) as part of the 2020 RDOF reverse auction is not the same service that is offered today. Satellite technology has improved both in quality and in capacity. Starlink has upwards of 8,000 satellites already in orbit,43 and Amazon’s Kuiper has begun launching its own constellation.44 While LEO satellite service cannot match the performance of a fiber connection, it can typically meet or exceed the average consumer’s current daily needs.45 It also has some qualities—like resilience in the face of disasters and speed to deployment—that allow it to outperform terrestrial broadband in some head-to-head comparisons.46 In a handful of years, satellite technology has grown up, and it is now robust enough to compete as a home broadband provider in the traditionally fixed arena.

Setting priorities and acknowledging budgetary tradeoffs is even more necessary if the resources saved on deployment can be turned toward broadband adoption and affordability instead—each of which today is a comparatively larger cause of the digital divide.47 While satellite’s current capacity and quality constraints mean that it cannot serve as a stand-in for fiber or serve every area lacking broadband, the FCC has several proceedings pending to increase the amount of spectrum available and raise allowable power levels, intended to significantly increase satellite’s capacity and performance.48

The idea of a “tech neutral” broadband policy also becomes more relevant as we near the upward sweep of the broadband deployment cost curve. Infrastructure now covers much of the United States. Unserved areas are generally disproportionately expensive and difficult to reach, and even areas with gains in broadband infrastructure deployment may be confronted with a lack of competitive and affordable service options. Broadband deployment policies must take into account existing geographic, budgetary, and logistical constraints. And subsidy programs must evolve with the broadband landscape to incorporate new technologies as they emerge.

B. Fully Incorporating LEO Technology into the Current Subsidy Landscape

Given improvements in quality, the policy question has shifted from whether LEOs can play a role in bridging the digital divide to how that role should be structured. The current system incorporates LEO satellites and other technologies in some programs but not others. It counts satellite service as broadband in some circumstances but deems it insufficient in others. This patchwork of approaches is imbalanced, inefficient, and unsustainable.

If U.S. broadband policy requires the complex balancing of short-term results with long-term benefits—all done within the constraints of a budget—all viable technologies must be utilized where appropriate. As a general matter, so long as LEO satellite service normally meets the minimum 100/20 Mbps performance standard and provides generally functional broadband service to users, it should be eligible for all existing broadband subsidy programs. This would mark a true shift toward tech neutrality in both federal and state broadband policy by gating participation based on quality of service, not kind of technology.

Of course, such a shift would not entail using LEOs to fill in every remaining deployment gap. Instead, LEO satellite service should be eligible for all programs under fair programmatic guidelines that assess it (and other competing technologies) on the merits. This means that in cases where the highest and most reliable level of performance is key, or where the marginal cost of extending an existing wireline network is low, a fiber connection may win out over satellite. In scenarios where the cost of laying fiber would exceed the likely expected value of the investment relative to the performance and cost of satellite service, satellite service may be tapped to fill the gaps. A smart, forward-looking, and tech-neutral approach would mean remaining open to all viable forms of broadband and making choices based on the totality of circumstances (and being transparent in cases where certain criteria are prioritized above the rest).49

Like other kinds of broadband deployment, both the quality and price of service and efficiency of a satellite deployment should be considered when choosing among contenders for a subsidy program. Some of the most meaningful metrics to be assessed up front include the requested subsidy amount, the quality and longevity of proposed service, how well the service meets consumers’ needs, and the speed and cost to deployment. These metrics can be incorporated to varying degrees depending on the context of each individual deployment.

Challenges with Incorporating LEOs

There are also areas where satellite technology diverges from other technologies, and assessing them creates new challenges for policymakers grappling with LEO technology’s inclusion in existing programs.

A. Technical and Deployment-Related Challenges

Despite being relatively immune to some of the challenges faced by terrestrial broadband (such as geography and distance), LEO satellite providers do not enjoy an unfettered capacity to scale. Major restrictions on capacity include access to spectrum (and limitations on the use of that spectrum, such as coordination requirements and required power levels), topographical constraints (users must retain a clear view of the sky), permitting requirements and FCC restrictions on licensing ground infrastructure like earth station gateways, and the overall number of satellites in orbit, all of which are governed by various entities. Some of these restrictions mean that certain areas—such as crowded suburbs or urban canyons without a view of the sky—will likely never be able to rely on satellite service. Others, including spectrum access, power levels, and restrictions on earth station gateways used to backhaul data, will depend on a series of pending and future FCC rulemakings for a clear path forward.

These differences from traditional terrestrial networks also mean that the established method of subsidizing broadband deployment—which focuses on the marginal cost of location-specific infrastructure rather than the overall cost of adding capacity to an orbiting network—may need to be rethought. As noted above, reliance on satellite service must account for higher ongoing costs, including the regular replacement of satellites with more advanced capabilities, in return for a smaller marginal cost of deployment up front. For example, under USF, the FCC has historically relied on formulas that incorporate the up-front cost of deployment to determine High Cost funding awards. If satellite’s inclusion overly complicates this calculus, an alternative could be a general subsidy model that offers funding through installments contingent on outcomes (sustained service that meets minimum standards for a certain number of households) rather than being tied to specific kinds of expenditures, such as cost of deploying certain infrastructure.

In a similar vein, satellite deployment cannot be tracked through physical buildouts. While LEO networks have the potential to connect users almost anywhere, service is only actually transmitted to a location where a resident elects to subscribe. These differences in buildout and cost models complicate efforts to fit satellite connectivity into any subsidy program designed for terrestrial broadband, which is specifically place-based.

BEAD attempted to grapple with this by stipulating that grants to LEO providers be conditioned by requirements to maintain “reserved capacity” sufficient to ensure service to eligible (unserved) households for a period of time. The program rules also require that free consumer premises equipment (CPE) be included as part of the services and allow program administrators to reimburse satellite providers on the basis of adoption metrics.50 Since BEAD-funded deployments are only a slice of total satellite coverage, this has led to a paradoxical outcome in which only previously unserved households served by LEO providers funded through BEAD will be considered served. At the same time, only some LEO users receive free CPE, while others have to pay for it themselves, regardless of their relative income levels.

B. Market Structure Challenges

LEO satellite’s market structure diverges sharply from that of other providers (see Chapter II). While the emergence of satellite connectivity as a whole adds more robust competition to the total marketplace of broadband providers, there is a near-monopoly within the satellite connectivity space itself, with only one active residential provider and another still months away from offering service. This problem may be gradually solving itself: Kuiper has already won bids to serve a substantial number of locations in states’ proposed BEAD plans and will be in default if its residential service fails to materialize in those areas. However, the general lack of competition and adequate capacity is putting upward pressure on prices that threatens to raise the monthly cost of service and deter the very households that subsidy programs aim to help get online.

So long as network capacity remains constrained and demand exceeds supply in many areas, providers may charge higher monthly rates and use fees to control the flow of subscribers in particular areas. Put another way, LEO satellite service is nearly ubiquitous, but the number of subscribers that can be served in each local area is limited, leading providers to discourage uptake through their fee structure in areas that are already well-subscribed.51 Consumers in those areas with no other technology available may have no choice but to pay or to go without connectivity altogether.

The consumer market is fraught as well. Recipients of Starlink’s residential service have been paying $120/month for regular service in addition to hundreds in up-front fees and consumer equipment.52 These same consumers are excluded from consumer-side subsidy programs if their provider is ineligible for participation, and satellite providers have no real obligation to offer an affordable basic plan that still meets broadband benchmarks. Professional installation of CPE is not always included with the subscription, and the technically challenging installation can stymie consumers left to do it themselves.

Even addressing these financial barriers may not be enough. Maine’s pilot program saw relatively low participation despite offering Starlink to unserved households with free CPE and installation included.53 For a subsidy program to have any chance of success, widespread adoption needs to be reasonably guaranteed, and it remains at best unclear whether LEO satellite service providers can inspire widespread public interest and overcome adoption barriers to make that claim.

C. Policy Challenges

Like other wireless technologies, both LEO satellite’s sustainability and its improvement in capacity and overall performance are contingent on steady and increasing access to spectrum, permission to function at the necessary power levels, and a reasonably predictable trajectory for both. Indeed, Starlink’s application for a far larger constellation of new satellites with enhanced capabilities is pending approval at the FCC, as are multiple regulatory proceedings that would give them the access to the spectrum and higher transmit power levels they need. This means that LEO service’s ability to scale is somewhat out of the hands of service providers or NTIA. Instead, the FCC’s spectrum decisions will play a significant role in determining satellite’s future advances.

In addition to spectrum availability, satellite deployment comes with some necessary infrastructure buildouts that may face barriers of their own. For example, restrictions on building earth station gateways (which connect satellite constellations to terrestrial internet infrastructure) close to urban areas or even major roadways can limit or impede the expansion of satellite service capacity in certain zones. Satellite providers trying to expand service must navigate both federal licensing and local permitting restrictions.54

State broadband offices and similar local decision makers tasked with dispensing funding may be less versed in determining whether a satellite provider’s promises are feasible than those of a terrestrial provider, especially because some of those advances hinge on federal decision-making with an opaque or uncertain trajectory. Nevertheless, it remains important to verify up-front that bidders in deployment programs have the technical ability, finances, and capacity to pull off programmatic commitments. While the recent BEAD guidelines put the onus of verifying technical capacity on NTIA, expecting state broadband offices to navigate a world of LEO satellite-as-broadband service over the long term, without full ability to vet providers themselves, is an unsustainable solution.

This is not the only policy challenge satellite service faces. Mapping satellite deployment is also unexplored terrain since there are no fixed deployments to track: A satellite operator’s ability to service an area is dependent on whether consumer uptake in other regions justifies the capital expenditure to expand the constellation’s capacity, which is shared by the network as a whole. This is a problem that federal and state programs have largely ignored, resulting in an incoherent landscape where current maps classify households with LEO service as unserved, even as those very providers remain eligible to receive the BEAD funding meant to expand home broadband coverage. One option that could provide transparency and policy-relevant information is to map available capacity across geographic units that are, for example, roughly comparable to the coverage area of a LEO satellite transmission beam. This would highlight potential congestion and, in aggregate, illuminate the degree to which the operator needs to expand overall network capacity to meet both its obligations and growing demand.

Subsidy programs—and the federal, state, and local governments that dispense funding—may also be charged with assessing the benefits of their programs beyond infrastructural buildout. For any form of connectivity including satellite service, these benefits can include improved access to services like health care and education, as well as job creation related to the deployment itself.55 Though the deployment of a satellite network does not generally directly create local jobs to the same degree as a fiber network, the existence of ground infrastructure such as points of presence (earth station gateways for fiber backhaul) means that there are some direct workforce benefits to satellite deployment as well. These benefits may just be less uniformly localized. To the degree policy programs seek to ensure these ancillary benefits of broadband buildouts as well, satellite’s return on investment can be harder to track.

Recommendations

Rather than the current piecemeal approach that gates satellite’s participation in some programs but not others, U.S. broadband subsidy programs need an overhaul that equips program administrators to rigorously evaluate technologies on the merits, allows LEO satellite service to compete, and maximizes the service quality for consumers. This can be achieved through both short-term and long-term changes.

Short-Term Recommendations

Since satellite inclusion across subsidy programs is not standardized, the most immediate issue at hand is to ensure satellite broadband service is integrated and standardized as an option in all relevant federal and state broadband access and affordability programs, including any future USF High Cost program. This means standardizing service quality expectations and broadband performance benchmarks across all programs and data collection (such as through the FCC’s regular data collecting and reporting). Subsidy programs will also need to be adjusted to accommodate the differences in LEO satellite service’s underlying cost and deployment models.

1. Adjust Programs to Require and Track Satellite Service Commitments

First, policymakers should determine the necessary metrics and reporting required to ascertain whether satellite providers are satisfying the terms of their bid agreements without harming existing customers. This can be done by verifying reserved capacity for a period of time, but policymakers must be cognizant of the fact that requiring operators to hold too much capacity in reserve—in effect, leaving it fallow—may ultimately lead to other customers being denied service or charged higher prices. At the same time, satellite service quality may be variable depending on a network’s overall capacity, the number of customers in a given area, and other factors, leading to consumers of the same service potentially encountering a significantly different user experience. While all technologies suffer quality dips at times, the risk is significant with satellite, and program managers funding LEO providers to serve an area should vet its quality over time accordingly. More generally, policymakers should also collect data to better understand satellite’s viability as a high-speed broadband solution, including practical considerations and potential constraints.

As long as a LEO operator can provide evidence that it will follow through on its commitments—and, for example, has a history and technical expertise that suggest it will be able to perform—program administrators should require a sufficient, but not excessive, amount of capacity in reserve. It should be the responsibility of the provider to ensure compliance with deployment commitments. These agreements should provide for enforcement actions in cases where operators fail to follow through. These kinds of metrics should be standardized and applied uniformly across programs, and program administrators should be given the tools to verify them. NTIA should offer some basic instruction on vetting and verifying satellite providers’ capacity to serve an area to interested state offices.

2. Subsidize All the Necessary Infrastructure

Second, programs should ensure the necessary consumer education, free or subsidized CPE, and optional professional installation of household equipment. These steps of a satellite deployment are just as critical as the final stages of a terrestrial deployment and are particularly important for satellite service, since the terminal (receiver) is mounted outdoors. Traditional programs subsidize wireline fiber or cable up until the point where the consumer plugs in their home Wi-Fi router. Similarly, for satellite deployments, professional installation of the terminal and necessary wiring—which can be particularly technically challenging given the need for the terminal to maintain line of sight to the sky—should be included in the bidding process for any subsidy program. Basic customer service and technical support are particularly important for new satellite subscribers, but they should be considered as technology-neutral conditions that apply to all subsidized providers.

3. Adjust the Application Process to Accommodate LEO Providers

The application process should be adjusted to better facilitate LEO participation. As global providers that offer nationwide service, LEO providers are disadvantaged by application processes that involve duplicative submissions for small geographic areas, and stakeholders are often not well-positioned to evaluate the many facets of their applications through a process designed for terrestrial providers with discrete deployment zones. Policymakers should determine the specific information that LEO providers must offer as part of their applications, which may include the projected uptake of the service by eligible users, current and planned capacity, and policies concerning any guarantees or prioritization of the basic level of service being subsidized. In addition, policymakers should standardize a format that allows bidders to easily provide all the necessary application information relevant to satellite service. For example, this may include aggregating bids for individual geographic areas. At the same time, program administrators should be given the opportunity to assess a provider’s claims based on its total capacity and planned service across the country, since service continues across county and state lines.

Long-Term Recommendations

The broadband policy landscape no longer reflects either the causes or the potential solutions to the digital divide. This needs to change.

1. Use LEO Connectivity Where Appropriate as a Broadband Solution and Assess Its Potential Across Other Sectors

LEO connectivity is one tool out of many to close the digital divide. Incorporating LEO satellite service into the existing broadband landscape means using it where it makes sense—in otherwise high-cost, low-density areas—rather than attempting to shoehorn it in as the solution in every scenario. While policymakers should give it a fair shot, the end goal should be to create a competitively neutral process that matches consumers with the technologies that make sense for them. At the same time, policy decisions should enable satellite’s growth and ability to serve locations. For example, since a limiting factor in LEO satellite providers’ capacity to serve customers is access to spectrum, the FCC should make opening up more spectrum or creating additional sharing frameworks in existing bands a priority (see Chapter II).

In addition to broadband coverage, the FCC should study and seek to promote, where appropriate, the integration of satellite connectivity into other areas, such as direct-to-device services (see Chapter I), community networks using hotspots, backhaul (which is complicated by restrictions around earth stations in urban areas), and facilities-based VoIP (which would include adhering to the FCC’s stringent public safety requirements, such as offering enhanced 911 emergency calling capabilities, direct PSAP access, and automated dispatchable location requirements). As direct-to-cell services, such as those offered through the Starlink and T-Mobile partnership, proliferate and in some contexts replace standard telephone services, satellite providers will need to provide the same degree of public safety and certainty as their terrestrial precursors.

2. Ensure LEO Service Is Eligible for Any Future Deployment Programs

On the deployment side, any future High Cost programs that fund buildouts or operational expenses in high-cost areas should include LEO satellite service alongside any other technologies that reliably meet minimum performance standards. This is the only way to enact a truly balanced approach to deployment policy that treats all technologies as potentially viable tools. Additional support for satellite technology could help defray the high costs faced by consumers today and ensure future upgrades to the service. As satellite service becomes more common as a connectivity solution, subsidy programs may also need to adjust to match its unique cost structure. With advances in satellite technology and BEAD’s promise to finish deployment across the country, there is good reason to anticipate that high up-front deployment costs may become a thing of the past and future High Cost and any similar deployment programs should shift significantly to funding operational expenses instead (or otherwise defraying ongoing costs that are passed to consumers through subscription prices).

3. Include LEO Satellite Service in All Current and Future Affordability Programs

LEO satellite service generally imposes higher prices on consumers (particularly through its additional up-front fees) in return for widely available service, and it is not currently eligible for consumer-side subsidies.56 At least for the time being, even Starlink’s low-cost option ($80) is pricier than the low-cost options offered by many other national providers.57 Nor does it account for the one-time equipment and potential congestion fees.

LEO satellite should be incorporated into a broader affordability program that accounts for both and brings subscription prices down to the level that households can afford. If a technology provides service that qualifies for participation in deployment programs for unserved and underserved communities, it should be eligible for affordability support as well—if not as a fully designated eligible telecommunications carrier, then at least through a limited process that allows it to participate in affordability programs, which is what the government did for ACP. More widespread use of LEO satellite service may warrant higher monthly affordability subsidies, as the current amount given to households through the Lifeline program—approximately $10—would not, if applied to satellite providers, bring the service to a level comparable to other offerings.

In a truly tech-neutral landscape—one with a diverse set of technologies with varying cost models—the most competitively neutral and efficient means of subsidizing technologies long-term may be to defray costs on the user side with vouchers or credits. These subsidies could be determined on the basis of need, with amounts calculated based on consumer income and the cost of serving a location. Participating providers could then recoup ongoing costs by acquiring and retaining users based on service quality and competitive subscription prices. The subsidies could be portable to allow consumers to switch if another provider could better meet their needs.

4. Develop a New Mapping Process That Incorporates Satellite Coverage

The FCC should also look to modernize mapping and data collection to be more inclusive of satellite’s reach. Right now, LEO satellite service is available almost everywhere, but not everywhere all at once. There are no current, comprehensive broadband maps that accurately show its true availability, particularly with respect to the capacity available in particular communities. As states create and refine individual maps of their territories based on BEAD bids—indeed, the most accurate and granular maps yet—NTIA and the FCC should plan to reintegrate those maps into one nationwide picture. But these maps as well fail to accurately capture the full coverage of satellite service.

At a certain point, policymakers should consider moving beyond static mapping altogether in favor of another method that better captures all forms of broadband coverage and correctly identifies gaps. For example, a form of mapping that incorporates wireless signal propagation and reflects the impact of terrain and other physical obstructions (e.g., heavy tree cover) could better show a satellite service’s true availability and performance level. A mapping technique that accounted for a constellation’s overall capacity and showed how many households in an area could be served would depict satellite’s actual availability rather than marking it as feasible almost anywhere, as the current FCC maps do. An overlay that incorporated satellite service and other less easily tracked services, such as fixed wireless, could be used to verify unserved areas and indicate whether those areas were in need of a fixed broadband deployment or whether another form of broadband was available.

Citations

- Rafi Goldberg, “New NTIA Data Show 13 Million More Internet Users in the U.S. in 2023 than 2021,” National Telecommunications and Information Administration, June 6, 2024, source.

- “FCC Increases Broadband Speed Benchmark,” Federal Communications Commission, March 14, 2024, source; Federal Communications Commission, Inquiry Concerning the Deployment of Advanced Telecommunications Capability to All Americans in a Reasonable and Timely Fashion, 2024 Section 706 Report, GN Docket No. 22-270 (rel. March 14, 2024), source.

- Infrastructure Investment and Jobs Act, H.R. 3684, 117th Cong. (2021), source. In the original BEAD guidance released in January 2024, BEAD did not include LEO satellite broadband as a “reliable broadband service” but instead as an alternative technology. The latest guidance eliminated distinctions between fiber, other reliable broadband services, and alternative technologies. See “Reliable Broadband Service & Alternative Technologies Guidance,” National Telecommunications and Information Administration, January 2024, source; see also “BEAD Restructuring Policy Notice,” National Telecommunication and Information Administration, June 6, 2025, source.

- “FCC Increases Broadband Speed Benchmark,” Federal Communications Commission, source.

- Anna Read, “How Can the United States Address Broadband Affordability?,” Pew, April 29, 2022, source; Michelle Cao and Rafi Goldberg, “New Analysis Shows Offline Households Are Willing to Pay $10-a-Month on Average for Home Internet Service, Though Three in Four Say Any Cost Is Too Much,” National Telecommunications and information Administration, October 6, 2022, source; Jessica Dine, The Digital Inclusion Outlook: What It Looks Like and Where It’s Lacking (Information Technology and Innovation Foundation, 2023), source; NTIA Data Explorer, “Main Reason Not Online at Home: Too Expensive,” National Telecommunications and Information Administration, June 6, 2024, source; NTIA Data Explorer, “Main Reason Not Online at Home: Don’t Need or Not Interested,” National Telecommunications and Information Administration, June 6, 2024, source.

- Rafi Goldberg, “New NTIA Data Show 13 Million More Internet Users in the U.S. in 2023 than 2021,” source; Andrew Perrin and Sara Atske, “7% of Americans Don’t Use the Internet. Who Are They?,” Pew Research Center, April 2, 2021, source.

- Jessica Dine, Exploring Paths to a U.S. Digital Skills Framework (and Why We Need One), 52nd Research Conference on Communications, Information, and Internet Policy (Open Technology Institute at New America, 2024), source.

- David Ingram, Kailani Koenig, and Cal Perry, “Elon Musk’s Satellite Internet Flies under the Radar at Public Schools Nationwide,” NBC News, February 2, 2022, source.

- Mike Adkins, “ECISD Becomes First School District to Utilize SpaceX Satellites to Provide Internet for Students,” Ector County Independent School System, October 20, 2020, source.

- “OneWeb Joins Connecting Alaska Consortium in Strategic Partnership to Connect Alaska’s Tribes and Villages,” Eutelsat OneWeb, June 7, 2023, source.

- Melissa Sevigny, “Tuba City Households Get Starlink Internet Pilot Program,” KNAU, June 14, 2021, source.

- Ari Bertenthal, “Maine to Hand Out Free Starlink Terminals to Unserved,” Broadband Breakfast, October 17, 2024, source.

- Low Earth Orbit (LEO) Satellite Feasibility Report (Washington State Department of Commerce, December 2023), source.

- “New State Program to Provide Internet Connectivity to Maine Homes and Businesses with No Current Option” Maine Connectivity Authority, October 14, 2024, source; “Working Internet ASAP (WIA),” Maine Connectivity Authority, source.

- “WIA FAQ External,” Maine Connectivity Authority, source.

- David Anders and Sean Jackson, “Home Internet 101: Which Internet Connection Is the Best?” CNET, July 12, 2025, source.

- Kate Fann, “DSL v Fiber v Cable: What’s the Best Wired Internet?” Broadband Now, August 1, 2025, source; “Exploring the Evolution of Satellite Communications–from GEO to LEO,” Reliasat, January 26, 2024, source.

- “Large Constellations of Low-Altitude Satellites: A Primer,” Congressional Budget Office, May 2023, source.

- “High Cost,” Universal Service Administrative Co., source; “Affordable Connectivity Program & Lifeline FAQ,” Federal Communications Commission, source.

- “FCC Increases Broadband Speed Benchmark,” Federal Communications Commission, source.

- “Starlink Specifications,” Starlink, source.

- “FCC Rejects Applications of LTD Broadband and Starlink for Rural Digital Opportunity Fund Subsidies,” Federal Communication Commission, August 10, 2022, source; Federal Communications Commission, Rural Digital Opportunity Fund Auction, Order on Reconsideration, WC Docket No. 19-126 (rel. Aug. 30, 2024).

- Sue Marek, “Starlink’s U.S. Performance Is on the Rise, Making It a Viable Option for Broadband in Some States,” Ookla, June 10, 2025, source.

- Thomas Konstamm, “Everything You Need to Know About Project Kuiper, Amazon’s Broadband Network,” Amazon, June 3, 2025, source.

- Michael Kan, “Starlink Imposes Eye-Popping ‘Demand Surcharge’ for New Sign-Ups in this State,” PCMag, June 20, 2025, source.

- “What Percentage of BEAD Eligible Locations Can LEO Satellite Providers Serve at Scale?,” Vernonburg Group, August 7, 2025, source.

- “Starlink Residential,” Starlink, source.

- Michael Kan, “Starlink Imposes Eye-Popping ‘Demand Surcharge’ for New Sign-Ups in this State,” PCMag, June 20, 2025, source; Michael Kan, “SpaceX Increases Starlink Congestion Charge in Several U.S. Cities,” PCMag, April 22, 2025, source; Andreas Rivera, “Starlink Begins Charging an Extra $500 to $1000 in High Demand Areas,” SatelliteInternet.com, July 1, 2025, source.

- Michael Kan, “Starlink for Only $59 Per Month? SpaceX Offers Cheapest Satellite Deal Yet,” PCMag, September 12, 2025, source.

- Camryn Smith, “Internet Costs About $76 a month,” All Connect, September 8, 2025, source; Bobbi Dempsey, “Internet Service Provider Cost and Speed Report,” U.S. News & World Report, April 2, 2024, source.

- Masha Abrarinova, “Starlink Outshines Cable in Reliable Service with Mostly Rural Footprint,” Fierce Network, August 19, 2024, source.

- Sarah Forland and Raza Panjwani, What is the Universal Service Fund? (Open Technology Institute at New America, 2024), source.

- Infrastructure Investment and Jobs Act, H.R. 3684, 117th Cong. (2021) source; “Support for the Affordable Connectivity Program,” New America, September 6, 2023, source.

- Brian Fung, “FCC Ends Affordable Internet Program Due to Lack of Funds,” CNN, May 31, 2024, source; “FCC Brings Affordable Connectivity Program to a Close,” Federal Communications Commission, May 31, 2024, source.

- “Broadband Equity and Access Deployment Program,” National Telecommunications and Information Administration, source.

- “BEAD Allocation Methodology,” National Telecommunications and Information Administration, source. According to the NTIA, high-cost areas are “areas where at least 80 percent of the locations are unserved, and in which the cost of building out broadband service is higher than the average for all such unserved areas.” NTIA calculates the cost of serving an area by looking at factors such as (1) topography, (2) remoteness, (3) population density, and (4) poverty.”

- Nathan Smith, “Lessons from RDOF for BEAD,” Connected Nation, April 30, 2025, source.

- See, for example, Jason Rainbow, “FCC Upholds Denial of Starlink’s 900 Million Rural Broadband Subsidies,” SpaceNews, December 13, 2023, source. As noted above, LEO reliability in meeting the necessary benchmarks is impacted by multiple factors. As a consequence, the FCC reversed the awards to Starlink following post-auction review.

- “Final Guidance for BEAD Funding of Alternative Broadband Technology,” National Telecommunications and Information Administration, January 2, 2025, source.

- Kevin Taglang, “What Do We Know About LEO BEAD Bids,” Benton Institute for Broadband & Society, June 12, 2025, source.

- In addition to submitting the lowest bid, LEO satellite applicants are generally required to demonstrate that they have sufficient network capacity to deliver high-speed connectivity to all unserved and underserved locations within the proposed funding area, as well as a credible plan to scale capacity in line with future demand. Moreover, state broadband offices retain discretion to select among bidders when proposed costs are within 15 percent of each other. See “BEAD Restructuring Policy Notice,” National Telecommunication and Information Administration, June 6, 2025, source; see also Jessica Dine, “Thanks to New Guidance, We’re Pouring Billions into a Broadband Program That’s Doomed to Fail,” Newsweek, June 20, 2025, source.

- “Planned BEAD Awards,” Broadband Breakfast, September 4, 2025, source.

- Tereza Pultarova, “Starlink Satellites: Facts, Tracking, and Impact on Astronomy,” Space.com, August 1, 2025, source.

- “Kuiper Mission Updates,” Amazon, accessed on August 29, 2025, source.

- Proponents argue that fiber offers sufficient bandwidth to the home to make it “future proof” against any increase in consumer demand (such as increased reliance on video-streaming applications or telemedicine). This must be weighed against the much greater time and expense needed to deploy fiber, the continuing expense of supporting fiber-network operating expenses with a small and dispersed customer base, and the expectation that satellite capability will continue to improve over time.

- “Starlink for Emergency Response,” Starlink, source.

- Jessica Dine, The Digital Inclusion Outlook: What it Looks Like and Where It’s Lacking, source.

- See, for example, Federal Communications Commission, Satellite Spectrum Abundance, Further Notice of Proposed Rulemaking and Notice Of Proposed Rulemaking, SB Docket No. 25-180 (rel. May 27, 2025), source; Federal Communications Commission, Modernizing Spectrum Sharing for Satellite Broadband, Notice of Proposed Rulemaking, SB Docket No. 25-157 (rel. Apr. 29, 2025), source.

- Jessica Dine, “So You Want BEAD to Be Tech Neutral?,” Open Technology Institute at New America, March 21, 2025, source.

- “BEAD Restructuring Policy Notice,” National Telecommunication and Information Administration, 2025.

- Cameron Marx, “Starlink Imposes $750 Surcharge on New Customers in Major Northwestern Cities,” Broadband Breakfast, June 23, 2025, source.

- “Service Plans,” Starlink, source.

- “Working Internet ASAP (WIA),” source.

- “Overview of Earth Station Licensing and License Contents,” Federal Communications Commission, updated December 7, 2023, source.

- Wolfgang Briglauer, Jan Krämer, and Nicole Palan, “Socioeconomic Benefits of High-Speed Broadband Availability and Service Adoption: A Survey,” Telecommunications Policy 48 (August 2024), source; Jessica Dine, Enabling Equity: Why Universal Broadband Access Rates Matter, (Information Technology and Innovation Foundation, 2023), source.

- While LEO satellite plans are often cited as imposing comparatively higher costs on consumers, it is important to note that rural-broadband pricing more broadly tends to exceed suburban and urban benchmarks. Many smaller fiber and fixed wireless ISPs in rural markets charge rates at or above LEO entry points. See, for example, “Pricing & Service Offerings,” NEK Broadband, source (lowest residential tier $80/month, excluding fees); “Service Plans,” CVFiber, source. National surveys of broadband pricing frequently rely on plan data from large ISPs and may not capture the pricing practices of the 2,000–3,000 smaller ISPs serving rural areas.

- See, for example, “Internet Essentials,” Xfinity, source (“Internet Essentials provides affordable home Internet for qualifying households ($14.95/month for up to 75 Mbps, or $29.95/month for up to 100 Mbps)—as well as low-cost computers, free WiFi hotspots, and free Internet training.”).