The Systemic Shifts Needed for a Just Energy Transition

At a Glance

In today’s 1.5°C reality, emerging economies disproportionately suffer from the climate effects of emissions historically generated by wealthy nations. Shifting to a renewable-driven economy will exacerbate inequalities unless wealthy nations and global institutions center justice and equity in the energy transition.

Three critical issues shape this inequity: the international financing of climate efforts, the ways companies and countries extract critical resources for renewable energy, and the ownership of crucial clean energy technology.

- Climate finance. Global institutions and wealthy nations must dismantle the political and economic barriers that block initiatives to reform international financial systems that underlie climate finance.

- Critical resources. The path to a net zero economy will see skyrocketing demand for critical resources, many of which exist in developing and climate-vulnerable countries. How resources are mined and who controls access to them will shape this century.

- Clean energy technology. Wealthy nations hold the lion’s share of clean energy technologies and need to lower the trade and technology transfer barriers hindering developing countries from adopting and benefiting from them.

Setting the Scene

Unmooring the power and transportation sectors from fossil fuels is essential to meet the climate challenge. But doing so will increase inequities around the world unless the transition is pursued with local and vulnerable communities in mind. A just energy transition addresses the inequities surrounding climate impacts while harnessing the economic opportunities of this third energy revolution. Coal powered the first energy age, fossils powered the last century, renewables will power the future. How renewables are tapped and the approaches taken will shape this century and determine whether or not we globally address the climate crisis.

Without an agreed definition of a just energy transition, opportunities for action and alignment are being missed across sectors and between nations. This brief uses this working definition, just energy transition: Ensuring climate and energy responses create a regenerative society, untethered to exploitive processes, that prioritizes equity, includes Indigenous and front-line communities, and expands energy access in concert with climate and sustainable development.

Failing on the just energy transition will mean a more unequal world between and within nations, between those able to adapt and those suffering the consequences. This is an intersectional challenge that will require breaking silos. Still, a just energy transition can be achieved based on the success of actions taken in concert with climate finance, critical resources, and technology transfers.

In Our 1.5°C World

- The last 14 months (July 2023 to August 2024) were at or above 1.5°C.

- The World Meteorological Organization estimates up to $1.2 quadrillion in global damages by 2100 if fossils remain the dominant energy source.

- More than 774 million people lacked access to electricity in 2022.

- Demand for electricity will increase by 62 percent by 2050.

- The global population, now 7.6 billion, is expected to reach 9.8 billion by 2050 and 11.2 billion by 2100.

Climate Finance: Facing the Need for Reform

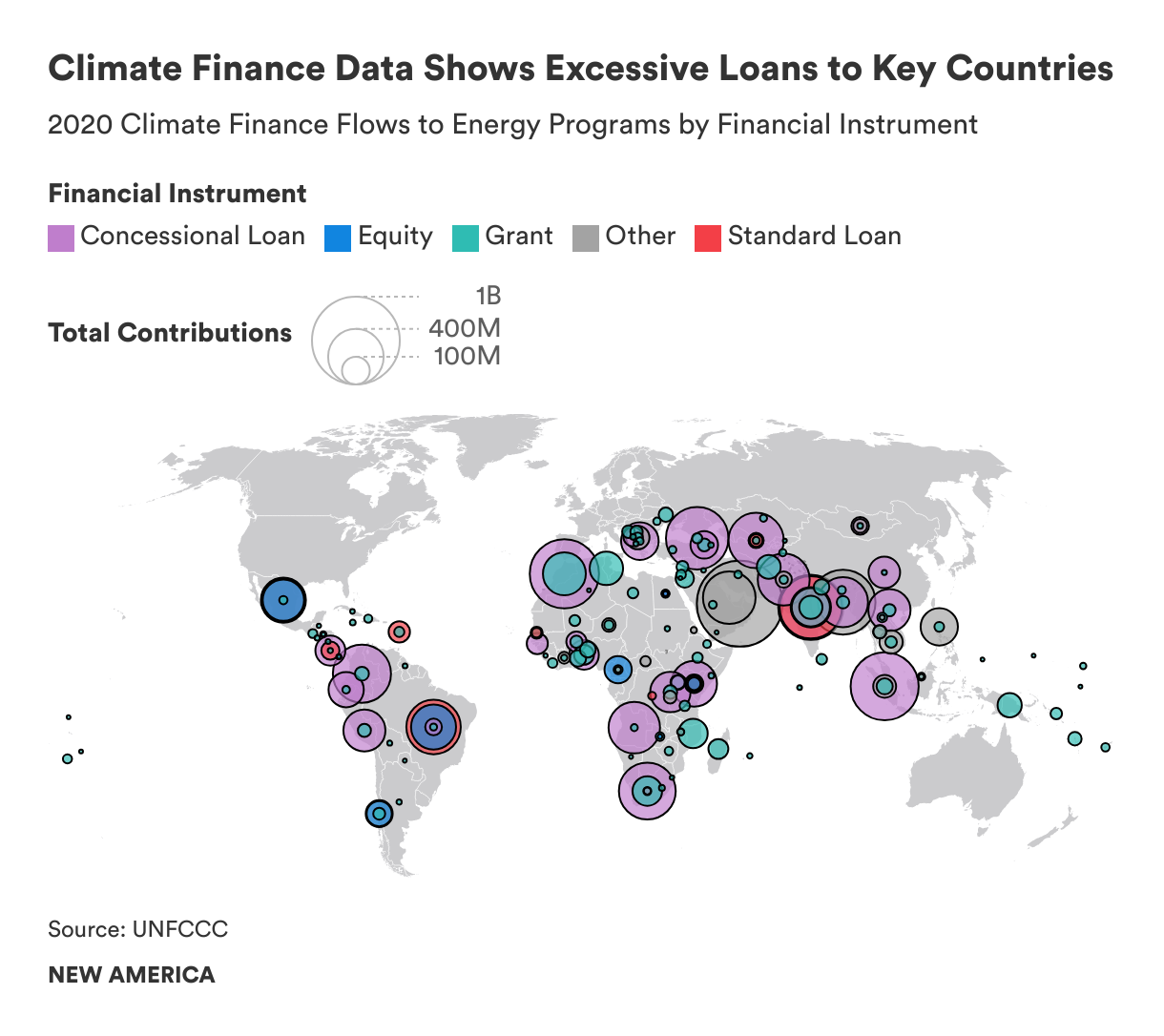

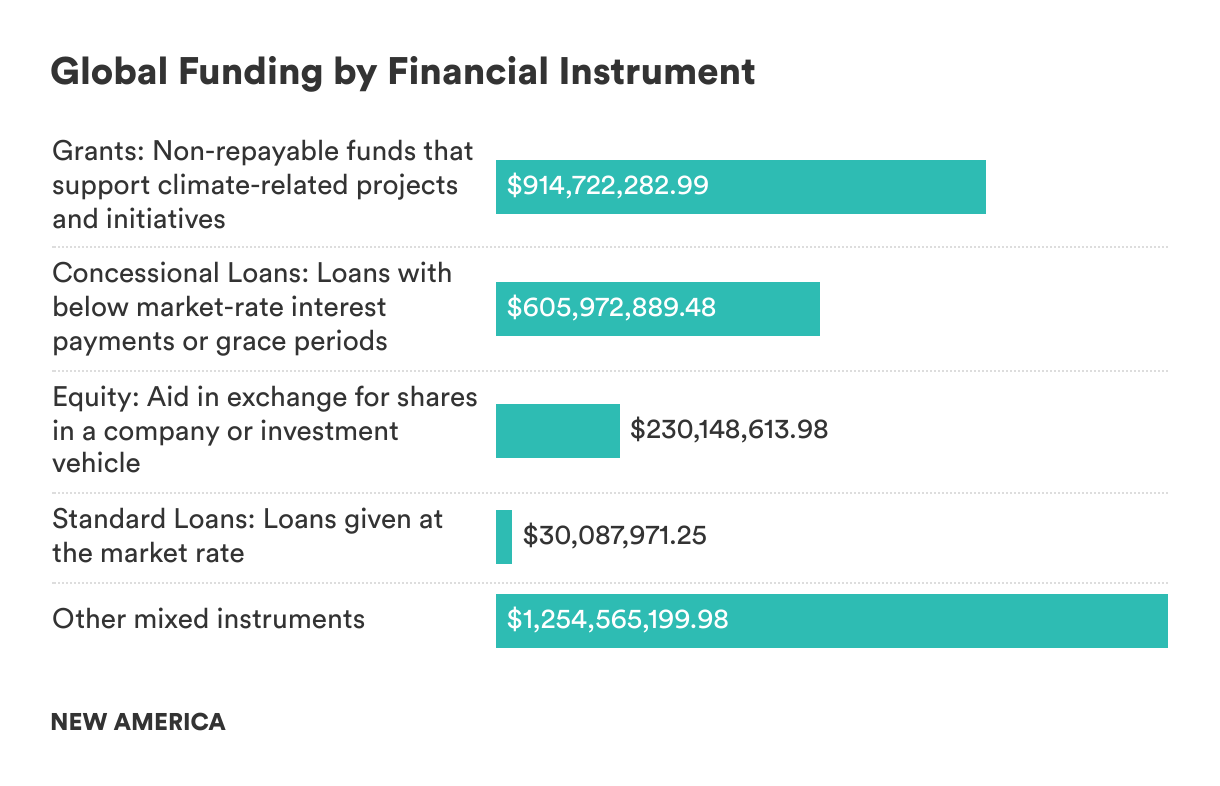

Our 1.5°C world is experiencing unprecedented heat waves, flooding, and other climate disasters. The cause is clear. Fossil fuels have produced 75 percent of all greenhouse gas emissions, which are driving climate change. To transition to renewable energy and keep temperatures within the Paris Agreement’s 1.5°C, global climate finance needs an estimated $8.5 trillion per year until 2030, then more than $10 trillion per year between 2030 and 2050.

Climate financing is insufficient, and the disparities between financing for wealthier and developing countries are stark and growing. Over 2021 and 2022, average annual climate finance reached $1.3 trillion, up from $653 billion in 2019 and 2020, but far below the $35 trillion needed by 2030. Less than 3 percent of global climate finance went to least developed countries; 15 percent went to emerging markets and developing economies excluding China; and less than 2 percent went to the 10 countries most affected by climate change in 2000–2019.

Funding is growing, and financing of renewable technologies is more visible. However, unequal access to these funds and resources, particularly in the Global South, will continue and likely grow unless governments, international financial institutions, and private sector investors address systemic issues to ensure fair distribution and impactful use of funds.

Regions that contribute least to global emissions often suffer most from the climate crisis and lack the resources to mitigate its effects. Countries in Africa contribute less than 4 percent of global greenhouse gas emissions but are the most vulnerable to climate change impacts, facing severe droughts, floods, and food insecurity. Existing financial structures fail to provide sufficient support to these vulnerable regions, exacerbating their struggles with debt and unfavorable lending conditions. In 2020, low-income countries spent over $40 billion on debt repayments, money that could have been used for climate adaptation and mitigation. Addressing this imbalance should be a priority, ensuring that those most affected by climate change receive adequate funding and support.

Countries like Nigeria and Sierra Leone are developing green growth plans and launching investment packages focused on renewables and climate-resilient infrastructure. Nigeria is expanding renewable energy sources like solar power, reducing carbon emissions, and enhancing infrastructure resilience. Sierra Leone is focusing on climate-resilient agriculture and renewable energy projects, such as rural access to solar power, to protect natural resources and improve livelihoods. Many climate-vulnerable nations are proactive in resilience, adaptation, and climate policy and diplomacy. However, financial innovations, such as green bonds and sustainability-linked loans, have not advanced at the necessary pace or scale to meet global climate challenges.

The countries and organizations of the Global South have offered significant proposals that specify achievable steps to enhance climate finance and address shortcomings in the global finance system. The Bridgetown Initiative 2.0 by Barbados’s Prime Minister Mia Mottley and the Accra-Marrakech Agenda by the Vulnerable 20 Group (V20) are key examples. Despite gaining some traction, these initiatives encountered resistance and dilution when incorporated into broader frameworks dominated by Global North interests. At the heart of the problem, development banks like the World Bank and the International Monetary Fund (IMF) impose high interest rates and onerous repayment terms on nations already historically disadvantaged by colonialist economic models. These financial burdens exacerbate existing inequalities, making it even more challenging for vulnerable nations to secure the funding they need for climate adaptation and development.

This dynamic continues to frustrate efforts by the V20 and other climate-vulnerable nations, as their needs for equitable financial support clash with the rigid and often punitive terms set by the global financial system.

Bridgetown Initiative 2.0

When Prime Minister Mottley first unveiled the Bridgetown Initiative at COP26 in 2021, it caught the attention of Global North leaders and struck a chord with the climate-vulnerable Global South. The 2.0 version, delivered in 2023 at the World Bank/IMF Spring Meetings, proposes a more comprehensive climate finance reform, aiming to:

- Mobilize $1.5 trillion annually in private sector investment for green projects;

- Expand IMF and development bank support with $100 billion per year in foreign exchange guarantees;

- Increase official development lending to $500 billion annually for sustainable development goals;

- Offer debt relief, with immediate liquidity support through special drawing rights for poverty reduction and temporary suspension of IMF surcharges;

- Restore debt sustainability via the Group of 20 framework reforms, IMF private debt restructuring, and funding for the Loss and Damage Fund; and

- Develop greater supply chain resilience, benefits for raw materials producers, and governance reforms to make international financial institutions more inclusive.

Despite its ambitious vision, the initiative failed to garner necessary support from advanced economies that benefit from the existing global financial order. The Paris Summit for the People and Planet (4P) in June 2023 appeared to advance equitable climate financing but significantly reduced the financial targets. While the Bridgetown Initiative initially sought to mobilize trillions of dollars per year, earmarking substantial portions for immediate debt relief and new funding mechanisms for developing countries, the Paris Summit discussed mobilizing only around $200 billion over the next decade from multilateral development institutions, leaning on private sector involvement rather than direct public funding. Issues around debt relief and new financing were also largely ignored. Critics argue that despite positive rhetoric, the commitments fell short of the transformative change needed.

While advocates of the Bridgetown Initiative presented it as more than just a model for climate reparations, the initiative still lacks the concrete incentives needed to appeal to Global North shareholders of multilateral development banks and the private sector, who sit at a favored place within the global financial architecture. To truly gain traction, such initiatives must develop specific and compelling incentives that align with the strategic interests of these influential stakeholders.

The Accra–Marrakech Agenda

The Accra–Marrakech Agenda emerged from the V20, a group of 20 climate-vulnerable nations that came together in 2015, determined to reshape global climate finance frameworks to better serve their needs. The agenda is their effort to enhance climate finance, risk reduction, and resilience, ensuring that the mechanisms developed at global summits genuinely address the needs of vulnerable nations. It focuses on transforming debt into sustainable finance, reforming international finance systems, upscaling carbon financing, and transforming risk management. It proposes detailed policies for making development finance climate-conscious and emphasizes national climate prosperity plans for setting development-positive and climate-aware financing targets. The agenda’s carbon financing proposals aim to strengthen emission targets, scale up emission exchanges, and foster public and private sector cooperation between high-emitting and low-emitting economies.

The Accra–Marrakech Agenda’s emphasis on detailed policy reforms and national climate plans is pragmatic, offering flexibility in implementation. However, its success hinges on the political will of both Global South and Global North countries to integrate these proposals into their national policies. One challenge is the lack of immediate debt relief focus, potentially making it less attractive to countries that urgently need financial reprieve. Another is the V20’s relatively limited political and economic clout, making global adoption of their agenda challenging without strong backing from more influential nations.

Navigating Political Will and Global Cooperation

While the energy around these proposals underscores the desire for transformative change, they will likely lose momentum unless we thoroughly examine the political will and incentive structures that can either impede or advance them. We must recognize that political will in climate finance is shaped by entrenched power dynamics, economic dependencies, and historical inequities. This is not only about increasing funding, but also about restructuring global cooperation and responsibility in climate action. The key is to frame climate finance as a shared pathway to sustainable development, where all stakeholders—governments, financial institutions, and the private sector—benefit from advancing solutions.

For the Global North, framing climate finance as a driver of economic growth—linked to trade benefits, job creation in green industries, and technology transfer—can shift political and economic priorities. Mobilizing private sector capital for renewable energy and climate-resilient infrastructure, especially in developing regions, can open up new markets and foster long-term economic partnerships.

For the Global South, climate finance must focus on reducing economic vulnerability and promoting resilience. This means implementing structural reforms that increase access to low-cost, long-term finance, while ensuring fair lending practices through international financial institutions like the IMF and World Bank. Expanding debt-for-climate swaps, which tie debt relief to investments in climate adaptation and mitigation, could provide much-needed liquidity for climate-vulnerable nations facing extreme debt distress.

The challenge remains in defining clear next steps and coordinating action. Robust data collection, analysis, and inclusive consultation with climate-affected nations and local stakeholders are essential as a first step. Still, the challenge remains in connecting the data to the interests of those who hold the reins of the financial systems.

Resources of the Future: Critical Resources

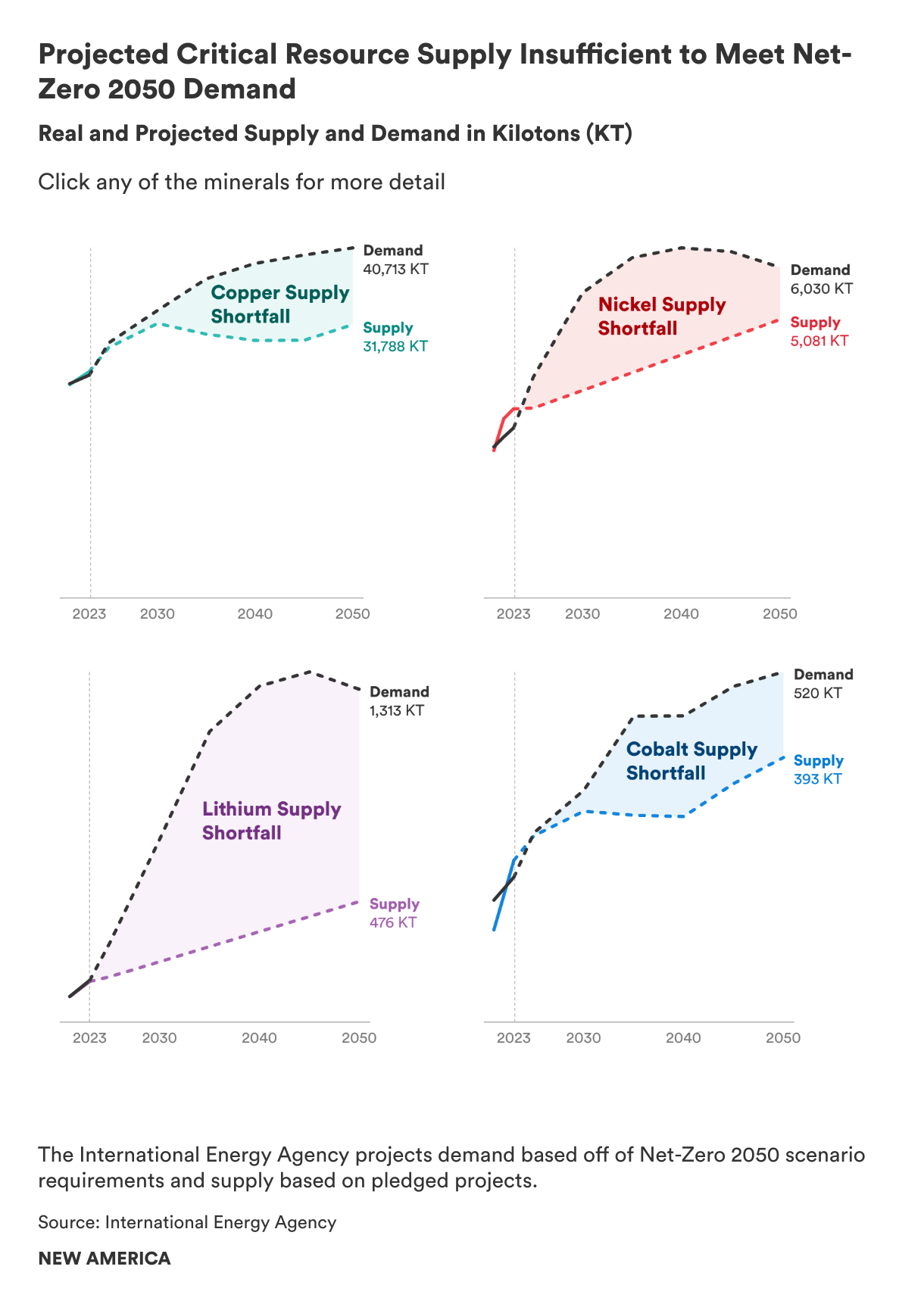

Achieving net zero emissions goals by 2050 will create an eightfold increase in demand for lithium and a two to fourfold demand increase in critical minerals like copper and nickel, outpacing projected supplies. In response to political signals at global climate conferences, the critical minerals market is booming, reaching $320 billion in 2022, with renewables like solar and wind powering 28 percent of electricity generation in 2023.

Minerals like lithium, copper, nickel, and rare earth elements are essential for electric vehicle batteries, solar cells, and storing renewable energy. Access to critical resources will make or break the COP28 Dubai goal to triple renewable energy by 2030, the science-backed path to reach net zero emissions by 2050. Achieving these goals will require an $800 billion investment in mining by 2040 to keep the Paris Agreement’s 1.5°C goal within reach and avoid the worst consequences of a climate-changed future.

Once mined, critical resources can be recycled and reused, provided that infrastructure for recycling is present. With such infrastructure, the world will need to mine far less to transition than the amount of coal mined in a single year. It is currently estimated that the world will need under 30 million tons of critical minerals to power renewables by 2040. To get to circularity, technologies will need to advance to ensure recycling is possible. Today, only 5 percent of lithium batteries are recycled globally, including electric vehicle batteries. It is possible to recycle 95 percent of the component minerals used to make a lithium-ion battery, but recycling technologies and plants need to increase. China alone plans to build 10,000 recycling facilities nationally.

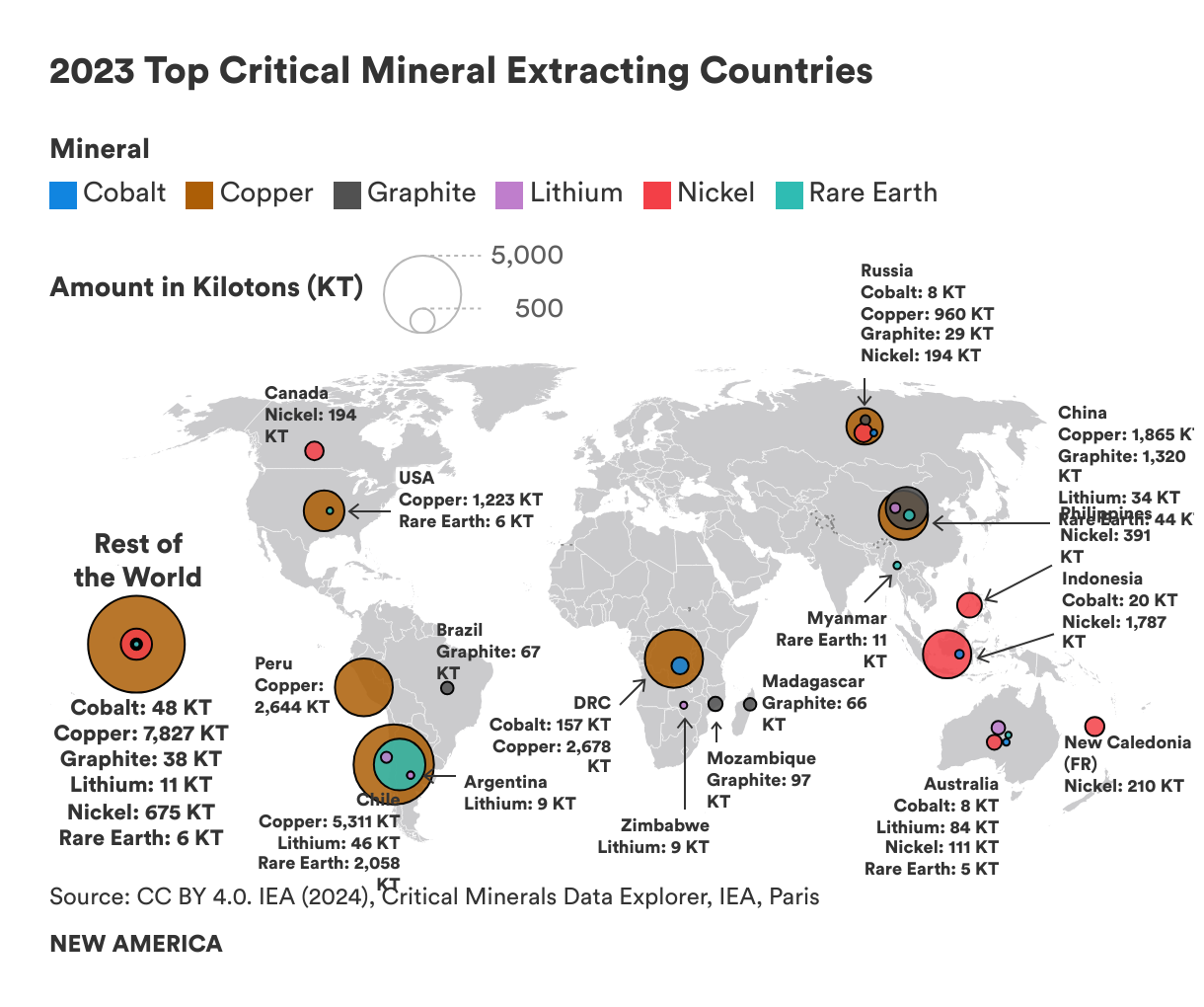

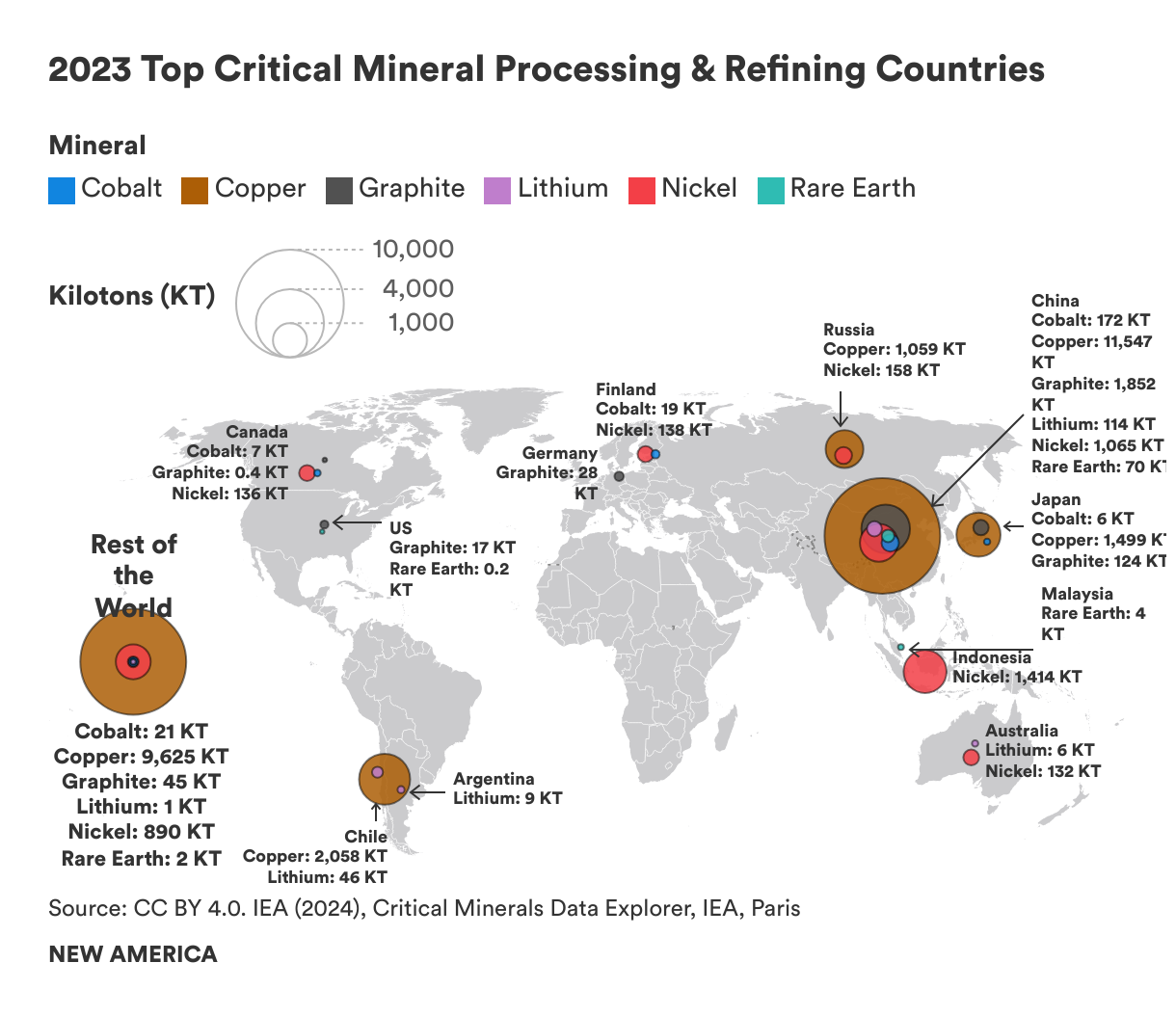

Transitioning entire energy systems and the global economy away from fossils will be determined by who controls access to the extraction and production of critical minerals. Whether or not justice and equity are considered will be predicated on these supply-side dynamics. Today, China controls the majority of production and extraction of the critical minerals that will fuel the future.

Too often, extraction means exploitation, with extractive industries perpetrating resource curse dynamics around the world. Companies like Glencore—the world’s largest mining company—are enmeshed in legal battles over corruption in mining operations. In 2023, Glencore was fined $700 million by U.S. regulators for bribing officials across several nations to turn a blind eye to mining practices or approve leases. Others, like Australia’s multinational mining company BHP, damage not only the environment but also cultural sites; an Australian state government granted BHP permission to destroy over 40 Aboriginal sites as part of a mining operation in Western Australia. Of critical mineral projects globally underway, 54 percent are on Indigenous and First Nations lands. Business and human rights groups have identified over 100 incidents of abuse tied to Chinese mining companies domestically and globally, directly connecting human rights concerns to Chinese-made electric vehicles and renewables.

The environmental and social costs of mining lithium and copper will increase as water stress increases. Producing one ton of lithium requires 2.2 million liters of fresh water, which later becomes polluted mining waste. Many lithium and copper deposits are in arid places, like the Atacama Desert in Chile and the deserts of Western Australia, areas already under considerable water stress due to climate impacts.

While Chile and Australia dominate the lithium market today, Chinese and Australian mining companies are setting their sights on Africa. The Democratic Republic of Congo (DRC) possesses the highest volume of known lithium reserves in the world at 6.9 million tons but produces zero tons annually. Projects to develop lithium in the DRC, like the Manono Project, have been delayed due to governance and transparency issues. Lithium and other mining can potentially bring opportunities to communities, but communities must be involved from the start.

Leading the production of critical minerals, China controls 90 percent of all rare earth elements processing and mining globally. Global Witness reported that China is dominating rare earth element processing and mining in neighboring Myanmar, with operations in 2023 valued at $1.4 billion—mainly in the Kachin state, where ethnic minorities have been fighting for autonomy for decades. In its wake, this mining is harming a biodiverse ecosystem, and likely contributing to conflicts through livelihood insecurities, in addition to the toll on human health caused by polluted air, soil, and water.

Five Largest Global Mining Companies in 2024

- Glencore (UK)

- Jiangxi Copper Co. Ltd (China)

- BHP Group (Australia/UK)

- Rio Tinto (Australia/UK)

- Vale SA (Brazil)

Avoiding resource curse dynamics will be predicated on government regulations and requirements. The largest struggle is for governments and the United Nations to set a path where communities that possess critical resources benefit from them developmentally and economically, while protecting local environments from mining pollution. These actions would also help emerging economies tap into more restrictive markets for minerals, as the European Union and United States increase trade requirements that include supply chain traceability, environmental best practices, and human rights.

Sustainable Supply Chains and Best Practices

As the extraction of critical resources plays out across the globe, the process of ensuring human rights, transparency, and sustainability will require both voluntary and regulatory efforts from governments, civil society, and international institutions.

New regional, bilateral, and global trade agreements on critical resources should include a social license to operate, setting minimum requirements and standards for sustainable practices with a triple bottom line approach: the environment, society, and the economy. Voluntary efforts, like the Energy Resource Governance Initiative’s social license to operate toolkit, provide valuable examples, reinforcing social responsibility and benefits and setting benchmarks like earning local support for mining projects. The Extractive Industries Transparency Initiative and the Natural Resource Governance Institute have set other transparency and governance-focused benchmarks to ensure best practices, so that resource wealth can benefit local communities more directly. Many First Nations have called for free and prior informed consent to occur before resource development, a right enshrined in the United Nations Declaration on the Rights of Indigenous Peoples. In 2024, the United Nations Secretary General’s Panel on Critical Energy Minerals explored the human rights and environmental impacts of critical resources, unpacking the core equity and justice principles mining operations should consider. Combining these examples into future supply chain requirements can help ensure communities benefit from their resource wealth.

China’s solar photovoltaic market has driven the price of renewables down. However, Chinese firms are not held to the same sustainability and justice-centered standards as European or American counterparts. In an effort to protect domestic production and foster sustainable supply chain practices, the European Union and United States have placed protectionist trade limits on both raw minerals and component parts for semiconductors and batteries. While this will raise the price of transition for developed countries, these measures will help encourage better practices that deter resource curse dynamics and human rights abuses. It will also make cheaper Chinese renewables more financially accessible to emerging and developing economies.

To support traceability, sustainability, and supply chain tracking, CDP runs the world’s largest environmental disclosure system. In 2023, 24,000 companies representing $67 trillion in market capitalization reported on their environmental and social impacts, particularly on their supply chains and climate impacts. While many voluntarily report, the European Union now requires it as part of doing business in the EU: The Corporate Sustainability Reporting Directive requires domestic and international businesses with dealings in Europe to report on their supply chains, climate risk, and human rights impacts.

Who controls critical resources will shape this century. As the demand for critical resources explodes, a global agreement on extractive industries’ best practices would be a gold standard. Voluntary efforts can only go so far, but new sustainability requirements show what is possible within supply chain requirements and the means of including sustainability, equity considerations, and climate. It is in the interest of governments to create regulations and incentives for best mining practices, while it is in the interest of mining companies to conform to the most stringent requirements to ensure they can tap into renewable markets in the European Union and United States.

Technology Transfers

Eighty percent of technologies that will achieve global net zero emissions by 2050 already exist. Renewables are now cheaper to install and maintain compared to fossil energy generation, while creating more jobs and fostering local energy security.

However, developing economies are not getting the investments or technology transfers they need to transition to renewables. Only 15 percent of the $1.8 trillion in renewable energy investments in 2023 went to emerging and developing economies. Patents and tariffs may make technology transfers akin to Covid vaccines: available for some, but not all. But without knowledge and technology sharing, there will be no global energy transition: developing economies will lack essential resources to install and build solar systems and turbines for wind and hydropower, train workforces, and build battery storage.

Technology transfers can involve trade, knowledge sharing, and skill and jobs training, taking place through direct investments, joint ventures, or partnerships. Accessibility to technology transfers relies on foreign direct investments, licensing agreements, joint ventures and partnerships, technical assistance and training, and research and development collaborations.

If nations have tariffs or higher fees to develop one technology over another, the energy transition will not reach everyone. The creditworthiness of countries depends on ratings such as those from Standard & Poor’s, with developing nations often receiving lower ratings, requiring higher interest rates on loans and a higher return on investment for foreign direct investments in renewable projects. For instance, in Namibia, with a rating of BB–, the required return on a solar project is 21 percent; in the United States, with a AAA rating, the required return is only 7 percent. Comparably, fossil projects have a lower required return. Companies need incentives to participate in foreign direct investment endeavors and support skill training, technical assistance, and public-private partnerships.

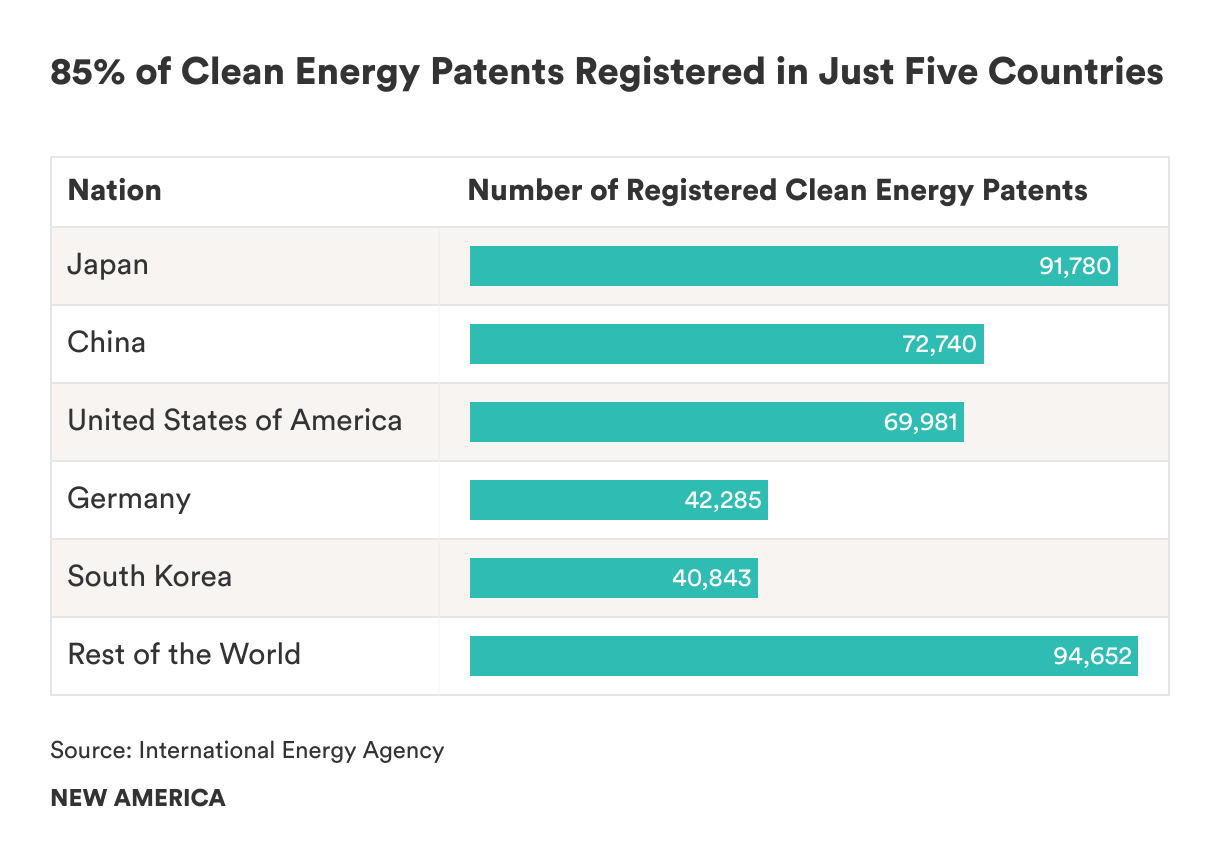

About 85 percent of all adaptation-oriented trade occurred among wealthy nations, largely excluding developing economies from key transition technologies. Developing countries need roughly $1.7 trillion annually in clean energy investments, a steep climb from $544 billion in 2022. Meanwhile, steeper requirements for returns on investment make renewable energy investments harder to harness. Eighty-five percent of all clean energy technology patents are registered in five countries: China, Japan, United States, South Korea, and Germany, with only 2 percent owned by developing countries. In 2022, private companies—including state-owned or supported companies—held 79 percent of all climate-oriented technology patents, with the public sector holding 5 percent and individuals and universities holding the remainder.

Technologies like solar panels and lithium-ion batteries were created by U.S.-based research institutes and oil companies, often with government funding. As the United States pivoted towards cheaper shale gas at the end of last century, European countries, Japan, and China expanded on clean energy and transport technologies to scale up domestic production, promote national energy security, and reduce costs. Through state-owned and heavily subsidized enterprises, China is the largest manufacturer of renewable energy systems and electric vehicles today.

Who owns technologies ultimately determines who can access them. Issues surrounding intellectual property rights and licensing mean developing countries can access renewable energy, but are unlikely to be given the tools, skill training, and capacity to manufacture renewables themselves, even though they possess many raw materials that will fuel the green economy. Protecting intellectual property and setting up barriers to technology transfers has been a hallmark of the U.S. Trade Representative, particularly regarding China, though there are efforts to reduce tariffs on clean energy and adaptation technologies among the U.S. and other nations via the Environmental Goods Agreement.

Companies Leading on Renewable Power and Electric Vehicles

- Top five renewable energy companies by production in 2024: China Three Gorges Corp, Enel SpA (Italy), Centrais Eletricas Brasileiras SA (Brazil), China Huaneng Group Co Ltd, and Iberdrola SA (Spain).

- Top five electric vehicle manufacturers in 2024: BYD (China), Tesla (US), Volkswagen (Germany), General Motors (US), and Stellantis (Netherlands).

Where patents are registered and where companies are based can play a major role in how or if technology transfers are possible. Often non-domestic Chinese renewable energy investments leave out local labor, preferring instead to import Chinese workers—while creating new debt hurdles and environmental impacts for developing economies. European and U.S. investments can create similar debt problems, but rely on social development efforts and local labor. They also face scrutiny by their citizens and an active civil society as a check on activities, unlike Chinese counterparts. Ultimately, the challenge of technology transfers and resource development hinge on the competition between wealthy nations with dynamically different world views and different accountability realities.

To date, UN bodies and global development banks continue to classify China as a developing economy. However, China is the world’s second-largest economy. China controls the majority of clean energy production, electric vehicle production, and supply chain resources; it possesses the largest domestic electric vehicle market. Continuing to exclude China among wealthy nations creates a distorted view of the global economy and the political weight of influence China exudes, both in its peripheries and via state-owned and state-sponsored companies operating internationally. Including China within the realm of developed nations would necessitate increased pressure on human rights considerations, potential intellectual property violations, and contributions toward development financing.

Framing technology transfers as a co-development of technology could be a way to highlight public-private collaborations that protect intellectual property rights, encourage financial resources, and split risks and benefits among partners. Co-developed technologies allow those in possession of technologies to retain intellectual rights, while gaining co-financing or other collaboration from nations not in possession of that intellectual property. This would make clean energy development endeavors partnerships rather than isolated state-led or company-led efforts in developing economies, and offers a way to get over the hurdles of intellectual property protections while meeting financial gaps through partnerships.

Signals for Technology Sharing

The Addis Ababa Action Agenda in 2015 called for closing technology gaps as key to implementing the Sustainable Development Goals. António Guterres, UN Secretary-General, has repeatedly called technology transfers integral to the necessary energy transition. The High Level Political Forum and planning agendas for COP29 prioritized technology transfers as essential to achieving the Sustainable Development Goals and key climate goals. Over 70 World Trade Organization member states are working to structure discussions on trade and sustainability, specifically technologies and environmental goods that would help achieve global climate agreements.

The UNFCCC’s Technology Framework is a platform for developing countries to assess technology needs and create technology action plans to implement their Nationally Determined Contributions (NDCs). These efforts take countries from identification to implementation, but access to climate adaptation and resilience tools relies on individual multi-stakeholder initiatives.

Dubai’s COP28 noted technology transfers as necessary to a net zero path, but left implementation to existing technology platforms and individual nations. Knowledge sharing and technology transfers will likely be an underpinning of the second round of NDCs, to be submitted in 2025 before COP30. In November 2024, COP29 will focus on the role of technology transfers and how best to embed them in the second round of NDCs. While technology transfers are woven into the Paris Agreement and other global climate agreements, no mandate requires technology transfers: They are voluntary, which has not yielded dramatic drops to global emissions or spurred clean energy technological adoption. If COP29 provides a requirement for technology transfers, that would open the door to more clean energy endeavors for emerging and medium economies.

Uniquely successful in reducing harmful substances impacting the ozone, the Montreal Protocol continues to rely on technology transfers to help nations transition from ozone depleting chemicals and technologies towards more sustainable options. The Multilateral Fund channels financial and technical assistance to help implement the Montreal Protocol.

Knowledge sharing will need to be a part of future climate agreements at upcoming COPs, but also for the new Plastics Treaty, anticipated for November 2024. The UN’s Summit of the Future will center on synergy between the SDGs, and focus on necessary actions to achieve the SDGs by 2030. Today, the Montreal Protocol serves as the only global environmental agreement to put technology transfers at its core. COP29 will signal whether or not technology transfers will move from a voluntary measure to a requirement to achieve net zero goals.

Opportunities For Impact

International Energy Agency reports show that achieving net zero emissions by 2050 and a habitable future will mean no new oil, gas, or coal projects. Phasing out fossils means phasing in alternatives, like renewable energy.

It’s possible there will be an energy transition for some and not all. The challenges are many. Today, it is riskier to invest in clean energy than in fossil fuel projects in developing economies. Many developing nations face a stark financial reality where they cannot provide essential social benefits, like roads and health care, making it virtually impossible to deal with climate impacts or provide incentives for new clean energy projects. In the background remain colonial paradigms on finance, critical resources, and technology transfers, even though many critical resources are mined in developing economies. Wealthy nations largely control development banks and private equity financing and are home to the largest mining companies and renewable energy companies in the world. They control access to how and where the energy transition will happen, and whether or not equity will be at its core.

The renewable energy transformation will cause shocks to fossil-dependent nations. These nations will need to diversify economies and use resource rents to support a transition to renewables. It is also likely that petrostates could fuel new or renewed conflicts to maintain the current status quo or exert other means of stalling progress on climate.

The systems that have governed in the past will need to adapt to be fit for purpose, or their inertia will compound the polycrisis linked to the just energy transition. Past best practices on technology transfers and resource alignment, like the Montreal Protocol, can serve as an example. The Summit of the Future represents an opportunity to link synergistic approaches to achieve the Sustainable Development Goals by 2030. Upcoming COP29 and COP30 represent opportunities to elevate financing, require technology transfers, and address supply chain challenges and justice considerations around critical resources. More needs to be done to lower trade barriers on renewable energy technologies and open opportunities for developing countries to mine, manufacture, and benefit from the resources they possess, while instituting best practices to protect local environments and support mining communities.

Taking these challenges into account with just energy transition framing can lead to better, holistic policy approaches that consider economic benefits and opportunities in conjunction with climate needs and responses.

Acknowledgments

We’d like to give a nod to these fine folks who helped us bring together our ideas, arguments, and data for this report: Candace Rondeaux, Narisara Murray, Aleksander Kostic, Rafael Swift, and Madison Harris.

Editorial disclosure: The views expressed in this report are solely those of the author(s) and do not reflect the views of New America, its staff, fellows, funders, or board of directors.

Downloads

More About the Authors

Martha Molfetas

Senior Non-Resident Scholar

Heela Rasool-Ayub

Director, Planetary Politics

Issues

Programs/Projects/Initiatives

Related