Sabiha Zainulbhai

Deputy Director, Domestic Housing

This brief was produced for The Chicago Community Trust by the Future of Land and Housing Program at New America. It was written by Sabiha Zainulbhai, with research assistance from Ellis O’brien.

Introduction

Barriers to Homeownership in Low- and Moderate-Income Communities of Color

Increasing Homeownership Affordability

Access to Capital to Increase Affordable Homeownership

Leveraging Capital to Scale Affordable Homeownership

Key Considerations for Increasing Access to Affordable Homeownership

The Chicago Community Trust (the Trust) seeks to address the racial homeownership gap in the City of Chicago by increasing access to financing for Black and Hispanic buyers in low- and moderate-income (LMI) communities. In 2019, 72 percent of white households in Chicago owned homes, compared to 48 percent of Hispanic households, and 42 percent of Black households. This is in large part because Black and Hispanic buyers have historically been excluded from traditional credit markets, and this lack of access, combined with rising housing prices and the low supply of affordable housing, has locked an untold amount of buyers out of the homeownership market.

Facilitating access to predictable and safe loans, as opposed to the risky, non-traditional, and unregulated subprime loans that were so common in the run up to the 2008 financial crisis, is critical for sustainable homeownership. When LMI buyers have access to safe and affordable financing, homeownership offers a way to build wealth and economic stability that can be passed down to future generations.

To inform the Trust’s homeownership goals, New America’s Future of Land and Housing (FLH) program conducted a national scan of innovative financing programs and products designed to address the barriers that LMI buyers in communities of color commonly face. This scan is illustrative of the kinds of affordable homeownership products and programs available, and is not exhaustive or representative of the full range of financing options. To produce this scan, FLH conducted background research on mortgage products and other financing mechanisms designed for Black and Hispanic buyers, and interviewed leaders of several affordable homeownership programs, in Chicago and across the United States. The goal of this work was to better understand the structure and innovation of existing products, as well as the most pressing challenges to increasing access to financing.

This brief outlines some key insights gained through the financial scan and the interviews, and organizes them into three broad areas:

It is important to note that while this brief focuses on programs targeted to LMI buyers in Black and Hispanic communities, many affordable homeownership programs or products are not racially explicit, and instead use proxies to channel financing to intended buyers. These proxies include eligibility criteria that limits financing to a specified income (typically below 80 percent or 120 percent area median income), requiring that buyers be first-time homeowners, or targeting products to specific zip codes or neighborhoods. Throughout the brief, we refer to the intended population of affordable homeownership products as "Black and Hispanic buyers in LMI communities" or "LMI buyers in communities of color", to encompass the range of target buyers of various programs while still focusing on the racial homeownership gap. However, the financing options in this brief could also be useful for increasing LMI homeownership even in areas where there is not a substantial Black or Hispanic population.

We also use affordable homeownership “products” and “programs” interchangeably throughout the brief, as some financing options are a singular product offered by a bank or non-bank lender while others are robust homeownership programs embedded within local community-based organizations.

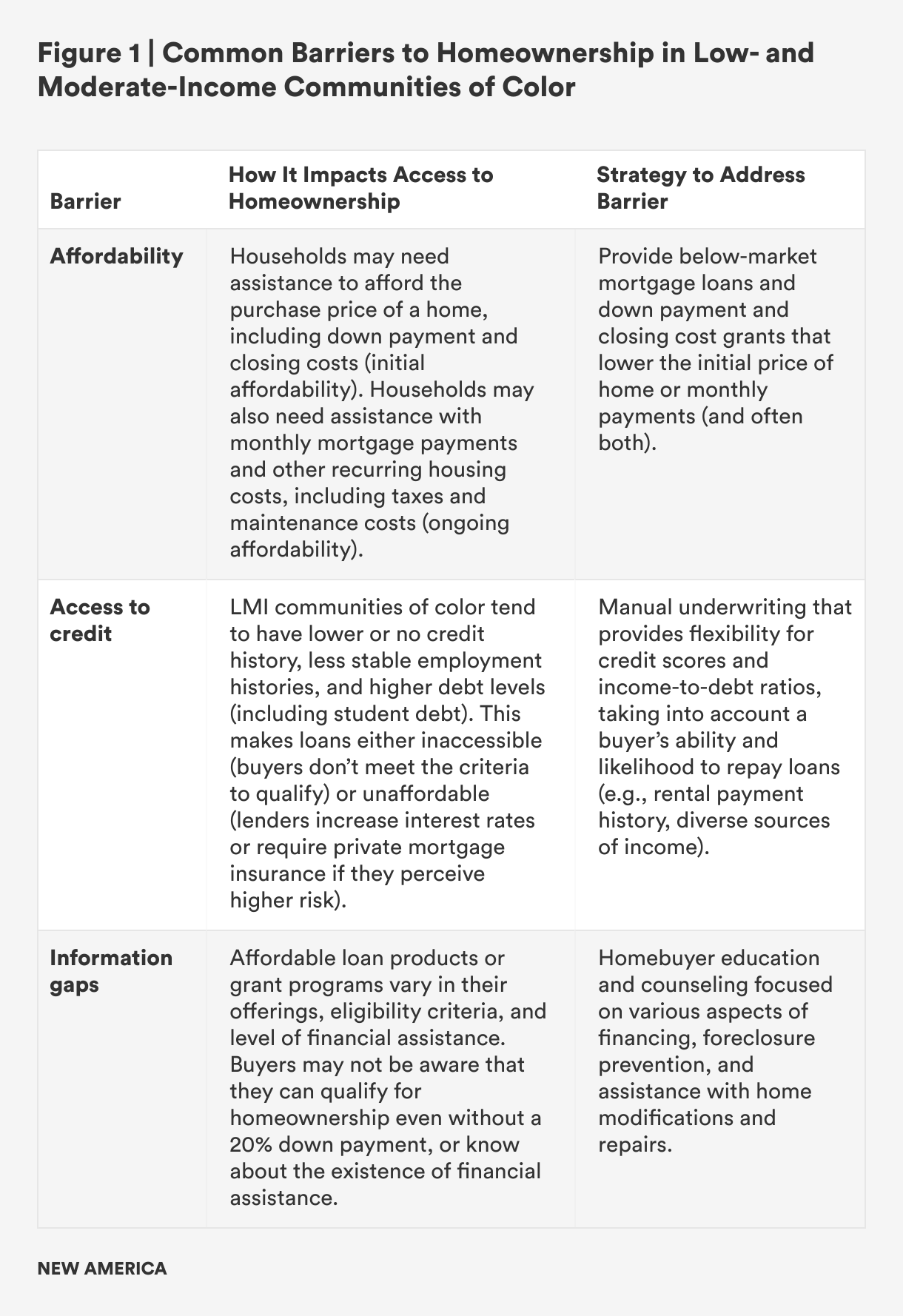

Barriers to homeownership in LMI communities of color fall into three broad categories: affordability, access to credit, and information gaps. As shown in Figure 1, there is a set of strategies that homeownership programs commonly use to address each barrier. These include subsidizing the cost of a home (to address affordability), ensuring flexible underwriting (to address access to credit), and requiring robust homeownership counseling and education (to address information gaps).

Each barrier is fueled in large part by the legacy of racist practices and policies that have dominated homeownership in the United States, and is now entrenched within the existing homeownership financing system. An in-depth WBEZ analysis between 2012 and 2018 found that for every $1 invested in white neighborhoods, mortgage lenders in Chicago lent 12 cents in Black neighborhoods and 13 cents in Hispanic neighborhoods. This disparity in lending was starkest among the biggest lenders; JPMorganChase, the second largest mortgage lender in Chicago, invested 41 times more dollars in white neighborhoods than in Black neighborhoods.

The racial disparity in lending not only impacts buyer’s access to financing to purchase a home on the private market, but also the cost of homeownership over time. According to one study, Black homeowners pay $67,320 more on average than white homeowners over the life of a loan due to higher mortgage rates, insurance premiums, and property taxes.

Ensuring access to predictable and safe loans, as opposed to the risky non-traditional and unregulated subprime loans that were so common in the run up to the 2008 financial crisis, is critical for sustainable homeownership. Given how deeply embedded these structural barriers are in the homeownership financing system, affordable homeownership programs typically increase access to the gold standard of safe and affordable financing: a 30-year, fully amortizing, fixed-rate mortgage, with below market interest rates and fair terms.

Programs typically pair a version of this mortgage loan with other services, such as high-touch loan origination and servicing, and robust homeownership education and counseling to prevent defaults and foreclosures. While these components of affordable homeownership programs are critical for accessing and sustaining homeownership in LMI communities, we focused on the ways that lending products the structure of mortgage loan and other innovative homeownership financing products increase affordability for LMI buyers in Black and Hispanic communities.

Structure of Affordable Homeownership Lending Programs

Given the variation in credit access and other services in financial markets across the United States, affordable homeownership programs serve different roles, based in part on the existing financial offerings in the market and how these offerings address the needs of communities being served. Some affordable homeownership programs (notably banks or credit unions offering affordable loan products, but local governments and community-based organizations as well) serve as a lender or grant administrator, and take an active role in the entirety of the mortgage lending process, from processing applications and conducting underwriting to originating or extending the loan or grant. Other programs serve as brokers, forming partnerships with existing lenders in the market, and referring buyers to their products instead. This is common for programs that only offer down payment and closing cost assistance, where eligibility for this assistance relies on securing a 30-year, fixed-rate first mortgage from an existing lender. Another role is that of financial intermediary, where an entity purchases loans from lenders or offers some form of credit enhancement, so that loans can be sold to secondary market investors, increasing liquidity for additional lending.

Homeownership programs also differ in the entities that comprise them; many programs are partnerships, often between banks, credit unions, state housing finance agencies, local housing departments, local non-profit organizations, and federal agencies. One of the most common entities increasing access to affordable homeownership are community development financial (CDFIs) which are public or private federally-designated organizations tasked with channeling financing to communities underserved by traditional credit markets. According to a LISC report, in 2017, there were 1,134 CDFIs that were certified through the CDFI Fund, and an estimated 1,000+ CDFIs that promote economic growth in LMI communities, but are not certified.

Regardless of the role programs play in the market or the entities that comprise them, the homeownership programs we assess all address one of the most common barriers to homeownership: affordability.

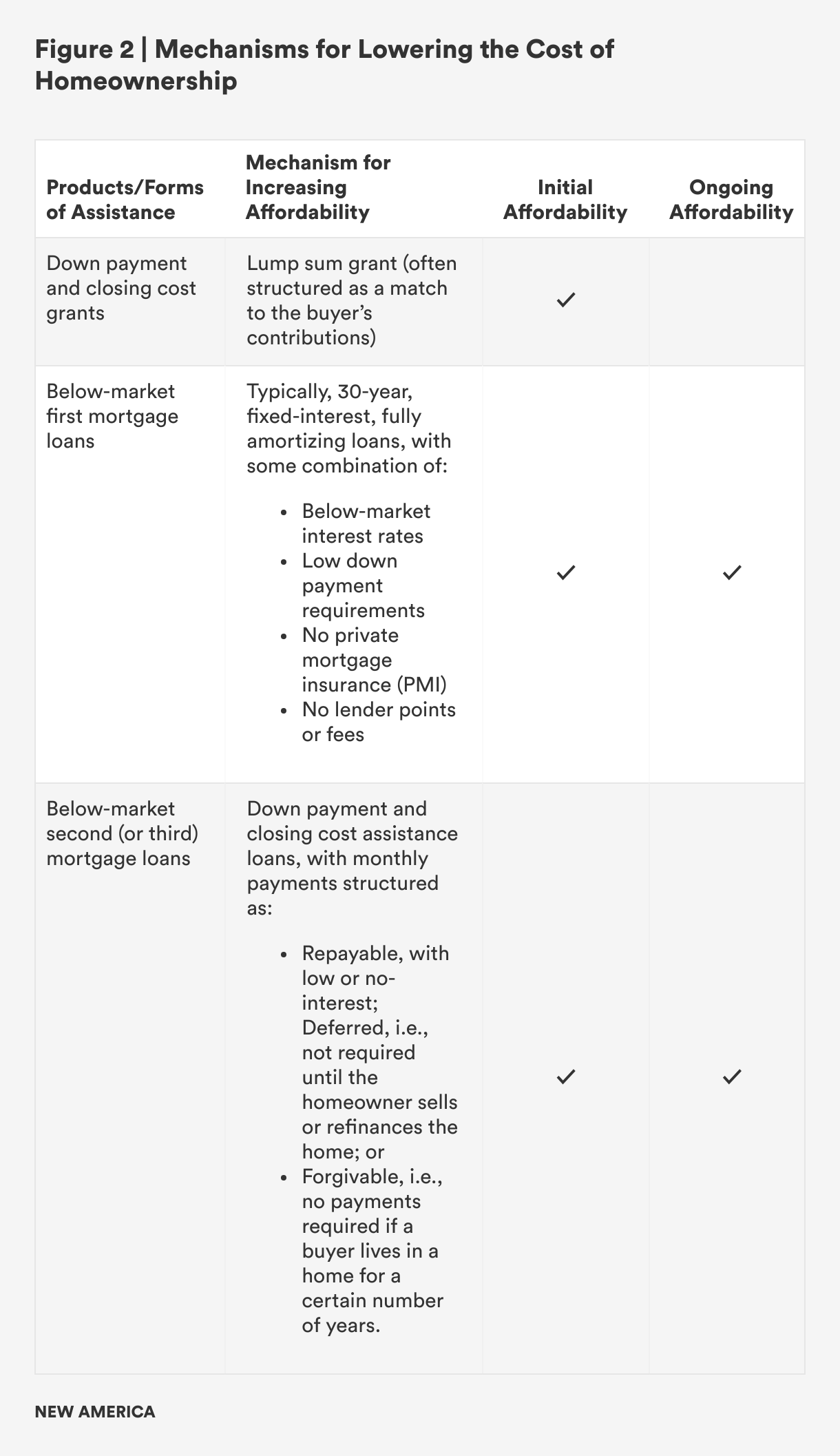

We assess two kinds of affordability relevant to homeownership—initial affordability and ongoing affordability. Initial affordability is intended to address the needs of buyers who lack the savings or intergenerational wealth to pay for a down payment, closing costs and other upfront fees to purchase a home on the private market, but may have the income to afford monthly payments. Ongoing affordability, on the other hand, addresses the needs of buyers who require additional financial assistance to afford both the purchase price of a home and the monthly costs of homeownership (e.g., mortgage principal, interest payments, property taxes, and maintenance costs).

While we differentiate between these two types of affordability, it is often the case that addressing initial affordability lowers the monthly costs of housing, and vice versa. For example, a down payment grant may eliminate the need for private mortgage insurance by limiting the loan-to-value ratios as a percent of income, thereby reducing monthly housing costs; similarly, a second mortgage loan that covers the cost of a home between the first mortgage and what the buyer can afford to contribute, can lower the interest rate on the first mortgage, and also lower monthly payments.

Figure 2 provides a high-level overview of the ways that programs’ typically lower the cost of homeownership, and whether these forms of assistance address initial affordability, ongoing affordability, or both. It is important to note that the products in Figure 2 are commonly layered to deepen levels of affordability.

Ideally, financing for homeownership bridges the gap between what buyers can afford to pay—both initially and on a monthly basis–and the cost of home, while not placing excessive risk on the lender. This is true regardless of the level of financial assistance required by the buyer, and as such, the gold standard for first mortgages, and what most programs tend to offer or require, is a 30-year, fixed-rate, fully-amortizing loan with fair terms.

To increase the affordability of first mortgages without jeopardizing their soundness for the buyer (through features such as high up front fees, risk-based pricing, prepayment penalties, balloon payments, and negative amortization), programs offer lower interest rates, eliminate the requirement for private mortgage insurance (PMI), and/or limit or eliminate the points and fees that lenders can charge. PMI can add hundreds of dollars to monthly payments, and is typically required when buyers put down less than 20 percent of the purchase price. Programs often also lower the down payment required on a home.

An important consideration when designing affordable financing products is that what lenders perceive as higher risk is not ultimately borne by the buyer through higher costs. Conventionally, buyers perceived as higher risk, due to a lower down payment or lower credit score, for example, are met with higher interest rates, higher fees, or through a requirement for private mortgage insurance. These increased costs are essentially risk premiums embedded in the loan in ways that can make loans unaffordable or unsustainable over time. Further, passing along these costs in ways that are ultimately borne by a buyer limits the affordability goals these products are intended to advance.

Down payment and closing cost assistance can be offered in the form of a second or third mortgage loan or as a lump sum grant. Second or third mortgage loans, often referred to as “junior” loans, cover the amount between the purchase price, the first mortgage, and the down payment amount. In case of a default, junior loans are paid after the first mortgage, and as a result, typically have higher interest rates than first mortgages. However, to ensure second mortgage loans remain affordable, programs often structure these loans as no- or low-interest loans; forgivable loans in which all or some of the loan is forgiven after the buyer has lived in the home for a defined period of time; or as deferred loans, where payments are not required until the home is sold or refinanced.

Down payment and closing cost assistance provided in the form of a lump sum grant is often structured as a match to a buyer’s contributions or to other forms of assistance. Offering this assistance through a grant versus a second mortgage loan has pros and cons from an operational and administrative standpoint. Notably, grants are typically one-time in nature, and administratively less complex than loans since mortgage payments do not need to be tracked and monitored over time. At the same time, grants do not recapture capital from ongoing payments, which is key to financing a higher volume of loans for LMI buyers. However, deferred or forgivable second mortgages, given the stalled or complete lack of loan payments, also are limited in their ability to generate additional capital.

While these loans do not neatly fall within a form of assistance or kind of product, shared appreciation mortgage loans allow LMI buyers to take equity out of their homes before it is sold or refinanced, in exchange for paying a share of future price appreciation. Shared appreciation mortgages can be private or public, and are typically structured as deferred, no-interest second mortgage loans, although they can also take the place of a first mortgage, where a buyer takes a lower interest rate in exchange for a share of future home price appreciation.

The shared equity model of homeownership promotes long-term affordability for current and future buyers outside of the speculative homeownership financing system. Shared equity models—including community land trusts, deed-restricted housing, and limited-equity cooperatives—subsidizes home or land purchases via a grant or a loan, and then retains that subsidy for future buyers through resale restrictions. Unlike other kinds of financial assistance discussed in this brief, shared equity models tie financial assistance to the housing unit or the land, and not the buyer, locking in affordability for future buyers. While we do not assess shared-equity models in this brief or the financial scan, their potential to provide permanent affordability for LMI buyers outside the speculative housing market makes them worthy of further investigation.

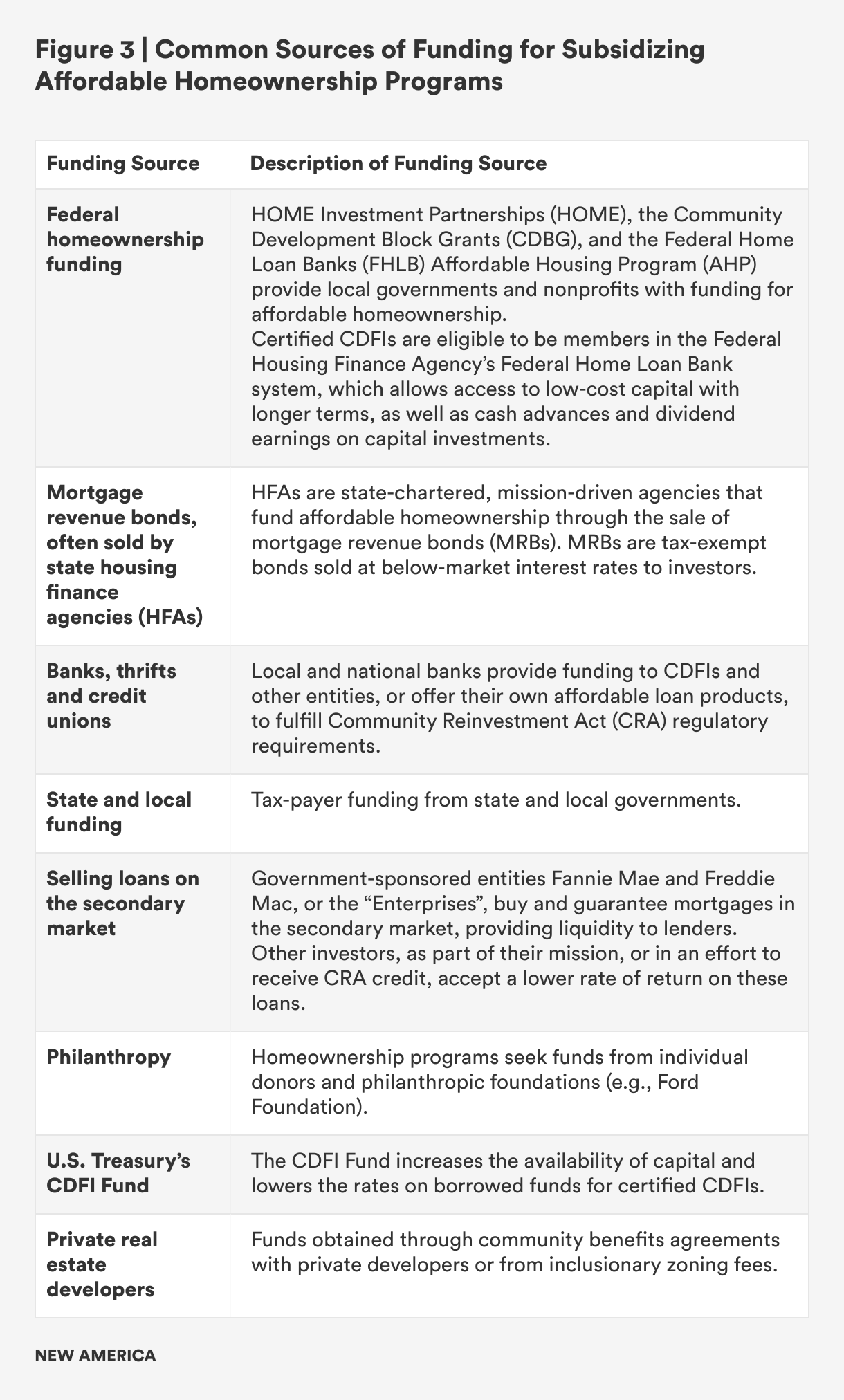

Despite its critical importance, access to reliable funding and securing sufficient capital for homeownership financing is one of the biggest challenges that CDFIs and other entities filling the gaps created by the traditional banking system face. While the federal government provides a large tax subsidy to homeowners through the mortgage interest deduction, allowing buyers to deduct mortgage interest from taxable income on their annual taxes, this deduction is primarily an incentive to borrow using more mortgage debt rather than an incentive for LMI families to become homeowners.

To cover the cost of subsidizing homeownership, programs often pool funding from different sources, the most common of which are listed in Figure 3.

While securing sufficient capital to subsidize and support homeownership is the main funding goal for affordable homeownership programs, there are trade-offs that come with funding from certain sources. Government funding sources, for example, can have burdensome regulatory requirements that can overwhelm the administrative capacity of local organizations, and funding from private sources, can be inconsistent and hard to attract. One of the biggest challenges, however, is covering risk in ways that lead to additional financing.

Covering Perceived Risk of Mortgage Loan Defaults

Lenders providing conventional mortgages, and even government-insured mortgage loans through the Federal Housing Administration (FHA) and Department of Veterans Affairs (VA), cover what they perceive as higher risk (e.g., lower down payments, higher credit scores, higher loan-to-value ratios, etc.) by passing on higher costs to buyers through private or FHA mortgage insurance, higher lender fees, or higher interest rates. As discussed earlier, these increased costs are embedded in the loan structure, in what are known as loan-level price adjustments (LLPAs), which can make loans unaffordable or unsustainable over time.

Restructuring loan terms to cover higher perceived risk is counterproductive when the goal of a is to increase affordability, and as such, affordable homeownership programs must look for other ways to cover higher perceived risk. One such way is a loan loss reserve fund. A loan loss reserve fund is a pool of funds established to cover a specified amount of loan losses, thereby minimizing the risk to lenders from possible defaults. Many programs use these loss reserves as a guaranty or credit enhancement in lieu of a sufficient amount of collateral, to improve the risk profiles of mortgage loans, and thus incentivizing more investors to purchase these loans. A common form of credit enhancement is recourse, or an agreement between a lender, GSE or secondary market investor, and the seller of the loans that the seller will repurchase or replace the lost funds in the case of a default.

One of the most robust examples of an effective loan loss reserve fund is Self-Help’s Community Advantage Program (CAP), which was established in 1998 and provided over $4.5 billion in financing to over 50,000 lower-income homebuyers nationwide—mainly to women and buyers of color. CAP did not originate loans, but instead served as a financial intermediary between lenders and investors, thereby increasing liquidity for affordable homeownership. With a $50 million grant from the Ford Foundation, CAP established a loan loss reserve fund to provide recourse to Fannie Mae in case of a buyer defaulting on their loan. This meant that Self-Help retained the credit risk for the loans it sold and agreed to purchase them back in case of a default. Because the perceived higher risk of these loans was sufficiently covered by the reserve fund, Fannie Mae felt confident pooling loans from LMI buyers and selling them to investors on the secondary market.

While not traditionally thought of as a risk mitigation strategy, some programs service their loans in house, instead of transferring them to a secondary market buyer. This allows a lender or local organization to establish a close relationship with the buyer over the life of the loan, intervening early and aggressively at the first sign of repayment difficulties. Homewise, a longstanding and successful CDFI in Santa Fe, N.M., attributes their ability to maintain affordability through low interest rates and no PMI requirements to “really know[ing] the customer” from the beginning of the home buying process through the life of the loan.

The ability to scale affordable lending for LMI buyers of color is limited when capital cannot be recycled or recaptured. In addition to generating capital through monthly loan payments, capital is recycled by selling mortgage loans on the secondary market instead of holding these loans on a lender or program’s balance sheets (also referred to as in portfolio). Lenders sell loans to investors, GSEs, thrift institutions, banks (for their own portfolios or trust accounts), pension funds, life insurance companies, socially-motivated impact investors, and others, who either hold these loans as investments, or securitize and sell to other investors. The funds from selling these loans can be used to make more loans without taking on additional debt, creating liquidity that can exponentially increase the impact of even a limited amount of funding.

While increasing additional funds for lending via the secondary market is critical, it can also come at a cost, as secondary market investors typically have their own underwriting guidelines and criteria that must be met in order for them to purchase loans (e.g., specified mortgage amounts, loan-to-value ratios, types and amount of insurance required, and loan terms). One organizational leader we interviewed described the secondary market as a “completely faceless third party system that tells you, ‘I'm only going to buy this’, and then everyone needs to figure out how to fit what [they’re doing] into what [the secondary market] says they will buy.”

The ability to determine eligibility and use flexible underwriting criteria to increase access to meet the needs of an LMI Black or Hispanic buyer is a huge advantage of some homeownership programs. Doing so allows programs to tailor or bypass some of the strict criteria that can automatically Selling loans to GSEs or other investors on the secondary market can jeopardize this flexibility, often forcing a choice between attracting private investment (and thus scaling to additional buyers) and increasing credit access to those underserved by the traditional market.

Scalability vs. Flexibility: Two Differing Approaches to Increasing Access to Financing

We contrast the structure and financing model of two local lenders–Transform Capital and the Indiana Neighborhood Housing Partnership–to illustrate the tradeoffs that they each made between increasing access through underwriting flexibility and increasing access through prioritizing ability to sell on the secondary market.

Transform Capital (TC), a volunteer-run, non-profit lender in the City of North Chicago, attributes its ability to extend loans to non-traditional LMI buyers with its flexible funding source (currently all private donations) and lack of involvement with the secondary market. Similar to a traditional lender, TC conducts robust credit analysis to ensure that monthly payments are within reach, but are able to look beyond metrics that typically disqualify LMI buyers, including low credit scores, high loan-to-value ratios, or ineligibility based on citizenship status. Established in early 2022, TC has since extended almost $1 million in funding lending assets to seven LMI families, many of whom would not be able to access credit otherwise (one buyer had a credit score of 490, for example). By not selling loans on the secondary market, TC is not beholden to structuring their loans so GSEs or other investors will purchase them, and can employ the underwriting flexibility and risk mitigation strategies that work well for their buyers, while still keeping loans affordable. While TC’s model ensures that its loan products are as accessible as possible, it may present challenges for scaling both the model and the volume of lending, however.

The Indiana Neighborhood Housing Partnership (INHP), a non-profit lender and CDFI in Marion County, Indiana, pairs extensive data analysis of LMI buyers with product experimentation. INHP offers two innovative loan products—the Mortgage Accelerator and the Mortgage Expander. The Mortgage Accelerator offers a 20-year loan with the same low interest rates from a typical 30-year loan; the shorter amortization period allows LMI buyers to accumulate equity at a faster pace, while still keeping monthly payments affordable. The Mortgage Expander bridges the gap between the below-market first mortgage accessed through the Mortgage Accelerator program and the purchase price, with a no-interest, second mortgage loan with deferred payments. This ability to be innovative with mortgage loan structure and financing can in part be attributed to consulting with secondary market investors throughout the mortgage loan design process, and embedding feedback to ensure that these products will attract private investment. Because the Mortgage Accelerator is sold on the secondary market, INHP does not maintain a relationship with the buyer over the life of a loan. But at the same time, INHP views the recycled capital from selling loans on the secondary market as essential to achieving the goal of serving as many potential buyers in the Indianapolis region as possible.

Increasing Liquidity for Affordable Homeownership: Case Studies from Other Sectors

Since the 2008 financial crisis, the private secondary market has remained more or less stagnant, resulting in a secondary market dominated by Fannie Mae and Freddie Mac. As such, it is useful to look at ways that liquidity can be increased for lending in LMI communities beyond the role of GSEs.

Exploring a Flexible, Tranched Secondary Market Structure. An idea that holds promise for increasing liquidity and unlocking more lending for affordable homeownership is creating a secondary market specifically for CDFIs and other lenders. An in-depth case study of The New York Forward Loan Fund (NYFLF)—a $104 million fund established to help small businesses in New York impacted by COVID-19—details how a similar structure could be applied to mortgage lending from CDFIs. NYFLF acts as an intermediary between five CDFIs and investors; NYFLF purchases loans originated by these CDFIs and securitizes and sells them to investors, utilizing a tranched structure with waterfall payments designed to attract investors with different risk tolerance and return levels: an A-Class tranche provided by banks, a B-Class tranche provided by foundations and impact investors, and a $20 million guarantee provided by New York State as a loan loss reserve. At its core, the NYFLF provides a model for a large-scale acquisition for what is perceived as a risky class of uncollateralized assets, and an innovative way to structure risk for different kinds of investors. One reason this idea holds promise is because it increases lending capacity without increasing indebtedness, whereas many existing solutions rely on lowering the cost of debt for CDFIs, without reducing their need for debt.

Exploring the Creation of State-Chartered Public Banks. Another potential avenue for increasing liquidity for a higher volume of lending in LMI communities is through the development of public banks. The concept itself is simple: a public bank is a depository institution owned by one or more levels of government that holds and leverages government deposits for the public good. While only one public bank currently exists in the United States (the Bank of North Dakota), there is proposed legislation in several states, with a bill in Philadelphia which passed earlier this year. Most legislation envisions that public banks would work with existing lenders through loan participations, which is a form of risk mitigation involving one lender originating loans and one or more providing the borrowed funding, with all participating lenders sharing the interest earned on the loan. Indeed, the Bank of North Dakota, which was established in 1919, bought 788 participation loans (albeit small business and agriculture loans) accounting for $1.6 billion in borrowed funds in 2021 alone.

This section reflects on some of the common themes reflected in interviews and in assessing affordable homeownership programs via the scan, and provide additional context for increasing accessing to financing for homeownership in LMI communities of color.

Closing the racial homeownership gap will always be limited within our existing homeownership financing system. CDFIs, banks and other entities have found innovative ways to increase access to affordable and safe mortgage products through flexible underwriting, robust homeownership counseling, and by increasing liquidity on the secondary market. However, innovation in financing for homeownership has a ceiling, due to constraints from the homeownership financing system and the housing supply and affordability crisis. Indeed, the most common first mortgage is still a 30-year, fixed rate, fully amortizing loan with fair terms, and what many programs are really investing their time and resources in is ensuring that these sound products are offered in neighborhoods and to buyers that are currently underserved by the traditional credit market. While there are homeownership models that exist outside the speculative housing market, such as shared equity models, these are not in wide use across the United States. And further, recent research shows that Black communities do not accrue the same equity gains from homeownership as white communities, pointing to the need for solutions that exist outside the current the homeownership financing system.

Design loan structure and repayment around the barriers that buyers in a specific community face. While there are common barriers to homeownership across LMI communities of color, the specific needs of buyers along income, race and ethnicity differ. This includes the level of financial assistance required to bring homeownership within reach, the underwriting flexibility needed to ensure access to credit, and the kind of pre- and post-purchase counseling and support necessary to afford and sustain homeownership over time. Yet, many affordable homeownership programs are designed specifically to impact the marginal buyer, or those on the brink of homeownership, whose only barrier is the lack of savings or intergenerational wealth for a down payment.

Even programs like Bank of America’s Community Loan Affordable Loan Solution that offer zero down payment loans and flexible underwriting that relies on timely rent or auto payments instead of credit scores may only address barriers for a specific kind of buyer (i.e., those with no credit as opposed to those who may have bad credit). This kind of loan offering is of course an improvement over the current financing system, but many loan and grant programs that are not explicitly targeted to the communities they intend to serve may find that they are only partially mitigating existing barriers. Deferred Action for Childhood Arrivals (DACA) recipients in Illinois, for example, would still struggle to find mortgage lenders who would qualify them for loans based on their immigration status, even if affordability is ultimately within reach. HomeSight in Washington State, for example, has loan offerings targeted to those without social security numbers, Muslims who require Sharia-compliant loans, among others.

The aging housing stock and need for deferred maintenance exacerbates existing inequities in homeownership financing and access. Even if the United States had a more accessible and equitable homeownership financing system, access to homeownership rests on the supply of homes available in a given housing market. Across the United States, there is not enough affordable housing to meet demand, and this mismatch disproportionately impacts Black and Hispanic buyers, who often have lower incomes and fewer assets to compete for an affordable home. As one leader of a homeownership program noted, “we could have $100 million dollars, but if we don’t have anything to buy, it won’t matter.” This lack of supply is compounded by decades of disinvestment in LMI communities of color that has resulted in a housing stock that requires a significant amount of repairs and deferred maintenance. Prior research (see “the catch-22 of mortgage standards” in Section 3) has shown that standards on the condition of homes, designed to protect buyers from purchasing homes that require repairs they cannot afford, can further lock LMI buyers from accessing financing.

Closing the racial homeownership gap will require a coordinated effort across all levels of government and the private sector. The patchwork of homeownership programs that blend public and private financing have impact, but singular efforts, even if far-reaching and scalable, are a poor substitute for a well-functioning lending market for LMI communities of color. Indeed, the federal government has had a hand in determining how markets work to provide credit and opportunity since the 1930s, and is in the strongest position to influence the homeownership market through its housing agencies (FHA, VA, and GSEs) as well as through the standards and policies it sets forth and enforces. For example, Fannie Mae and Freddie Mac recently announced the use of rental payment history in underwriting, which sets a precedent for private sector programs, to take this up as well.

Some innovations in homeownership financing are leveraging creative branding and marketing more so than addressing structural barriers to accessing homeownership. The application of new technologies to the mortgage lending market, or fintech, holds promise for creating efficiencies within the homeownership market, by automating manual functions like underwriting, loan processing, and servicing. Companies such as Landed, Point and OwnHome, for example, provide a tech platform to scale down payment assistance or shared appreciation mortgages to more buyers across the United States. While scaling innovative financing programs is important, an overemphasis on automating functions can come at the cost of the relationship-building and high-touch services that are often required to mitigate existing barriers among LMI buyers of color.

The existing system of homeownership in the United States is incredibly complex, and moving the needle on closing the racial homeownership gap will require coordinated efforts across the public and private sector, that focuses on systemic changes, such as grappling with how credit markets perceive risk, unlocking financing for entities providing credit access, and exploring permanent affordability that exists outside of the speculative housing market.

We would like to thank The Chicago Community Trust for their support and guidance, specifically Shandra Richardson, Ianna Kachoris and Lynnette McRae. We'd also like to thank Meegan Dugan Adell at New America Chicago and our colleagues at New America that assisted with the layout and design: Joe Wilkes, Jodi Narde, and Naomi Morduch Taubman. We’d also like to thank New America fellow Malcom Glenn for his careful review.

We would also like to extend our gratitude to leaders from the following organizations who took the time to speak with us and share their experiences with affordable homeownership financing: Transform Capital, Illinois Housing Development Agency, Indianapolis Neighborhood Housing Partnership, Neighborhood Housing Services of Chicago, Inc., Massachusetts Affordable Housing Alliance, and Woodstock Institute.

Deputy Director, Domestic Housing