Ill-gotten Gains: Predatory Lending and the Racial Wealth Gap in Chicago

Abstract

Illinois opened the door to high-cost lending in the 1980s. Since then, payday, short-term installment, car title loans, pawn loans, and other consumer loans often charged annual percentage rates (APRs) up to 400 percent. Many high-cost, short-term loans are targeted to communities of color, draining wealth from both Black and Latino/a residents. To help combat this trend, the 2021 Predatory Loan Prevention Act (PLPA) capped annual rates on most consumer loans at 36 percent, ostensibly putting an end to these predatory loans in Illinois. This report examines how predatory loans have impacted Chicago’s Black and Latino/a communities financially and what policy changes are needed next to ensure Black and Latino/a communities have access to affordable options that will help them build wealth. The paper focuses on two types of payday loans due to the availability of data.

Updated on February 16, 2024: The digital version of this report has been revised to more accurately capture what makes the loans referred to within so expensive for borrowers: both interest rates and the fees associated with annual percentage rates (APRs), not simply interest rates alone.

Acknowledgments

Special thanks for helping prepare this report to: Brent Adams, Tommie Robinson III, Sabiha Zainulbhai, Naomi Johnson, Joe Wilkes, Naomi Morduch Toubman, and Samantha Webster.

Downloads

Executive Summary

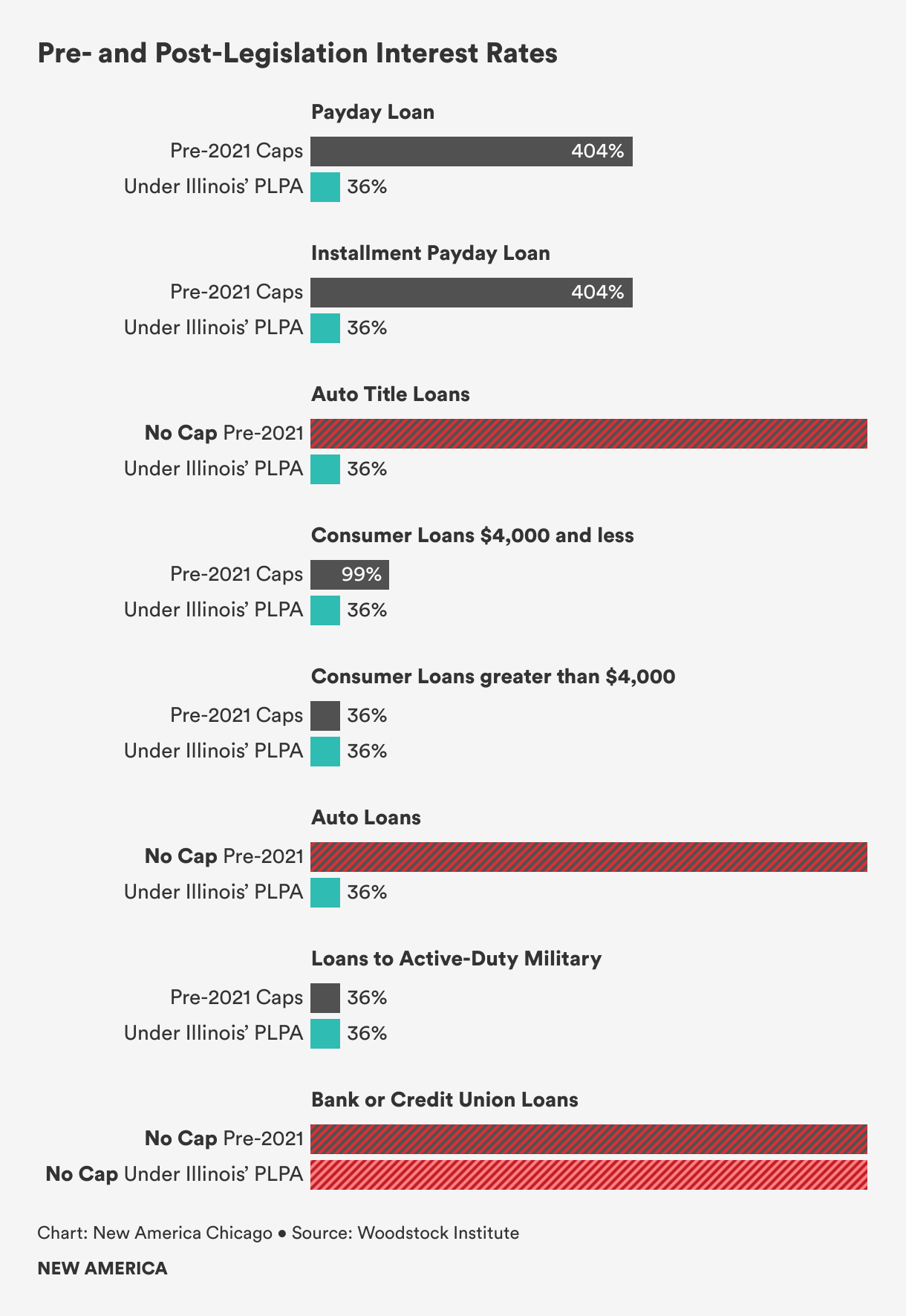

Since the 1980s, lenders have stripped billions of dollars from Black and Latino/a communities in Chicago through high-cost loans. These loans, including but not limited to payday, installment payday, auto title, and car loans, make consumers pay double, triple, or quadruple their original loan amount in fees and interest. By 2019, Illinois borrowers were taking out $1 billion per year in four types of small loans, before taking into account double- or triple-digit annual percentage rates (APRs).1 Prior to passage of the Predatory Loan Prevention Act (PLPA) in 2021, tacking on excessive fees and inflated interest was entirely legal. Lenders could charge up to 404 percent APRs legally for some loans, with no cap on auto title loans.

Statewide, predatory lending has been concentrated primarily in Black Chicago neighborhoods and suburbs, with a considerable amount targeting Latino/a communities.2 These loans are just one of several common practices including high interest private student loans and bias in home appraisals that have stripped billions from Black and Latino/a communities over the last three decades.

Small Dollar Credit or a Cycle of Debt?

Most predatory loans end up being taken out again and again by the same lower income individuals, part of a cycle of endless debt. The majority of payday loans are borrowed by consumers who take out at least 10 loans in a row.3 In Illinois, from January 2012 to December 2020, 1,413,004 consumers took out 9,318,552 small-dollar loans—an average of 6.6 loans per person.4 In 2019, 48.3 percent of Illinois borrowers earned less than $30,000 per year and 78.6 percent earned less than $50,000 per year.5 Nationally, it has been found that increasing income reduces reliance on payday lending: A $1 increase in the state minimum wage has been associated with a 40 percent drop in payday borrowing.6

Predatory Loans Hit Chicago’s Black and Latino/a Communities Hard

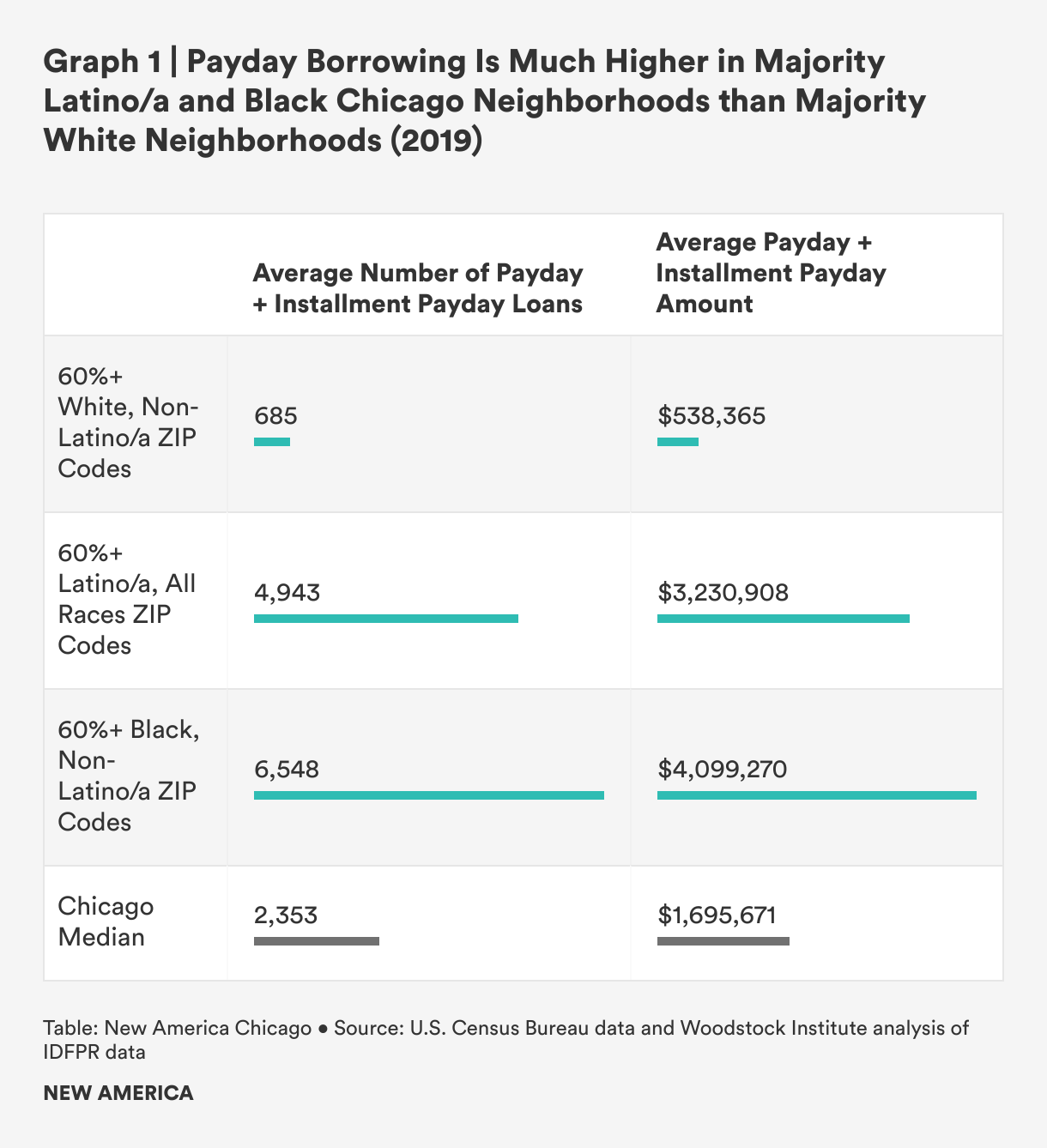

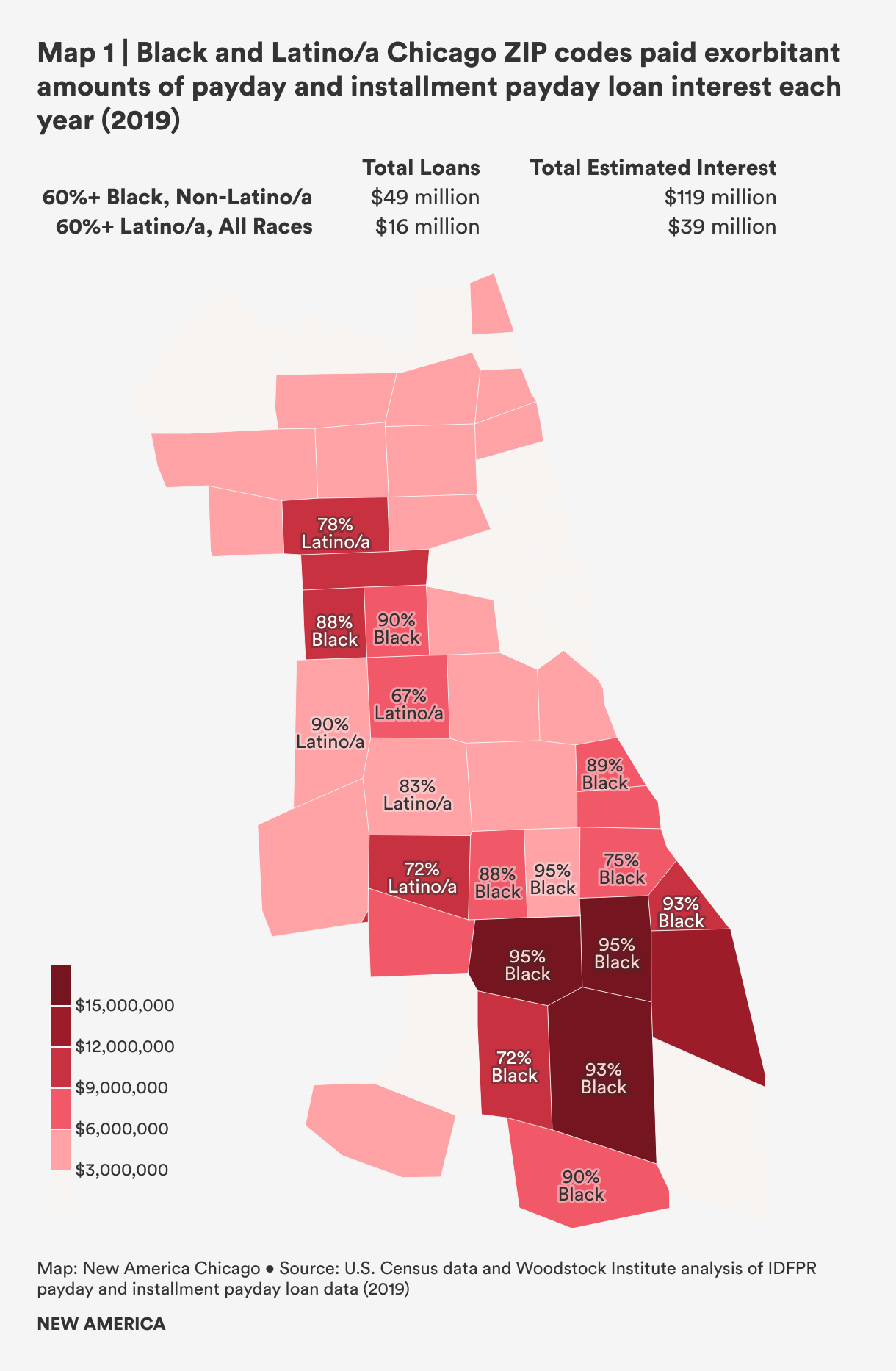

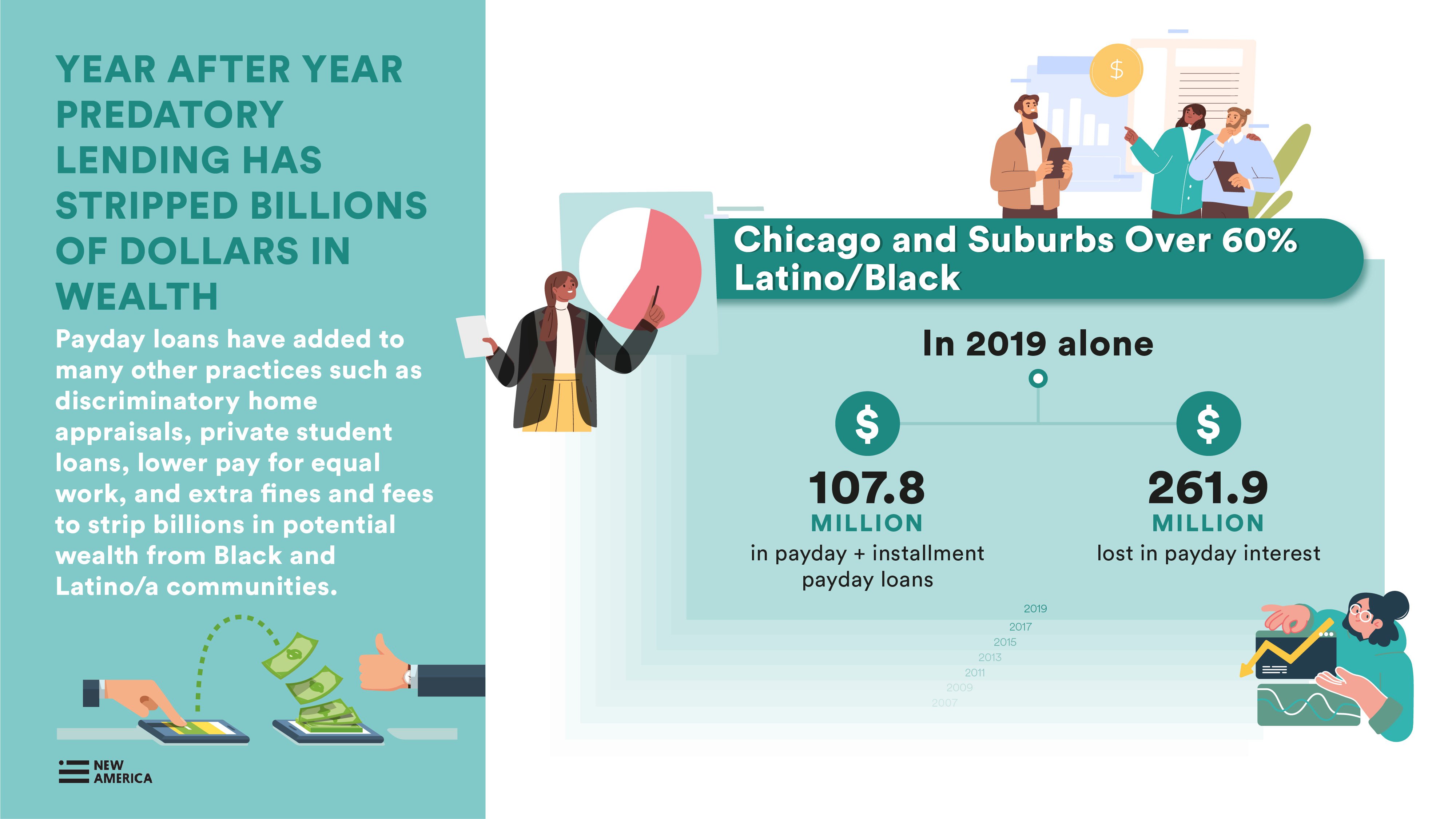

Over the years, predatory loans have taken a major financial toll in Black and Latino/a communities. In Chicago, payday and installment payday loans were almost ten times more common in majority Black ZIP codes and over seven times more common in majority Latino/a ZIP codes than in majority white ZIP codes.7 In just one year, 2019, people in majority Black and Latino/a city of Chicago ZIP codes paid over $158 million in exorbitant payday loan interest8 on $65 million in payday and installment payday loans.

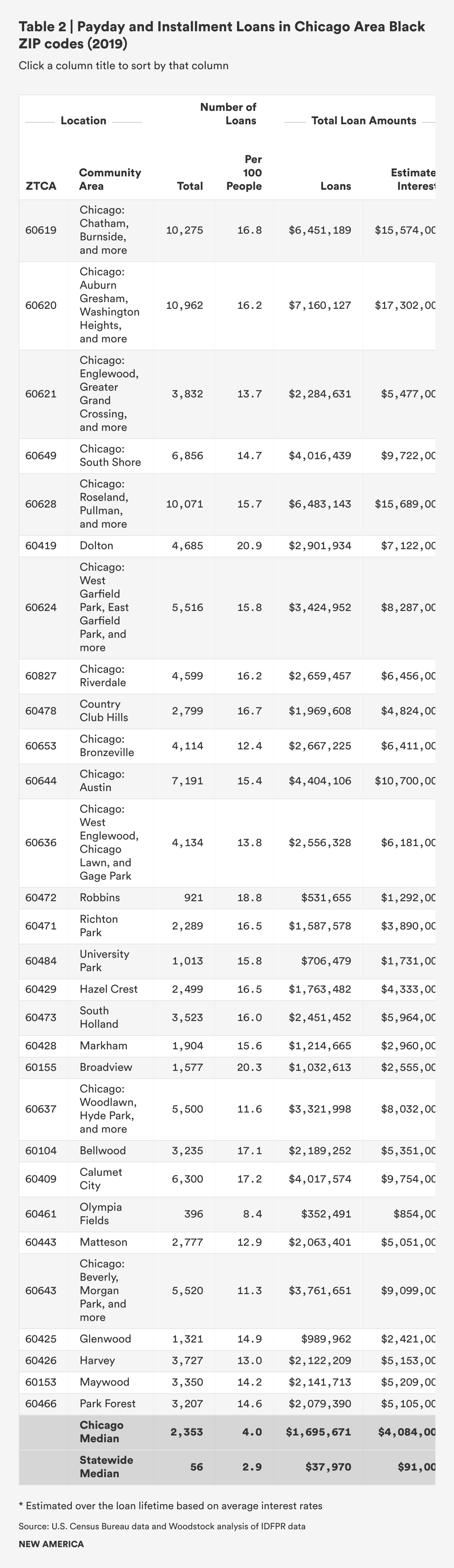

Six out of the seven Chicago ZIP codes with the highest number of payday loans per person were all over 87 percent Black. The highest number of payday loans per capita were found in 60619 which also has the highest percentage of Black residents in the city, followed closely by 60620, which is also over 95 percent Black. These two Southside ZIP codes alone paid over $30 million in interest on just the payday loans made in one year. In 60620, the interest paid would have consumed the average mortgage payments for an entire year for 1,300 families.

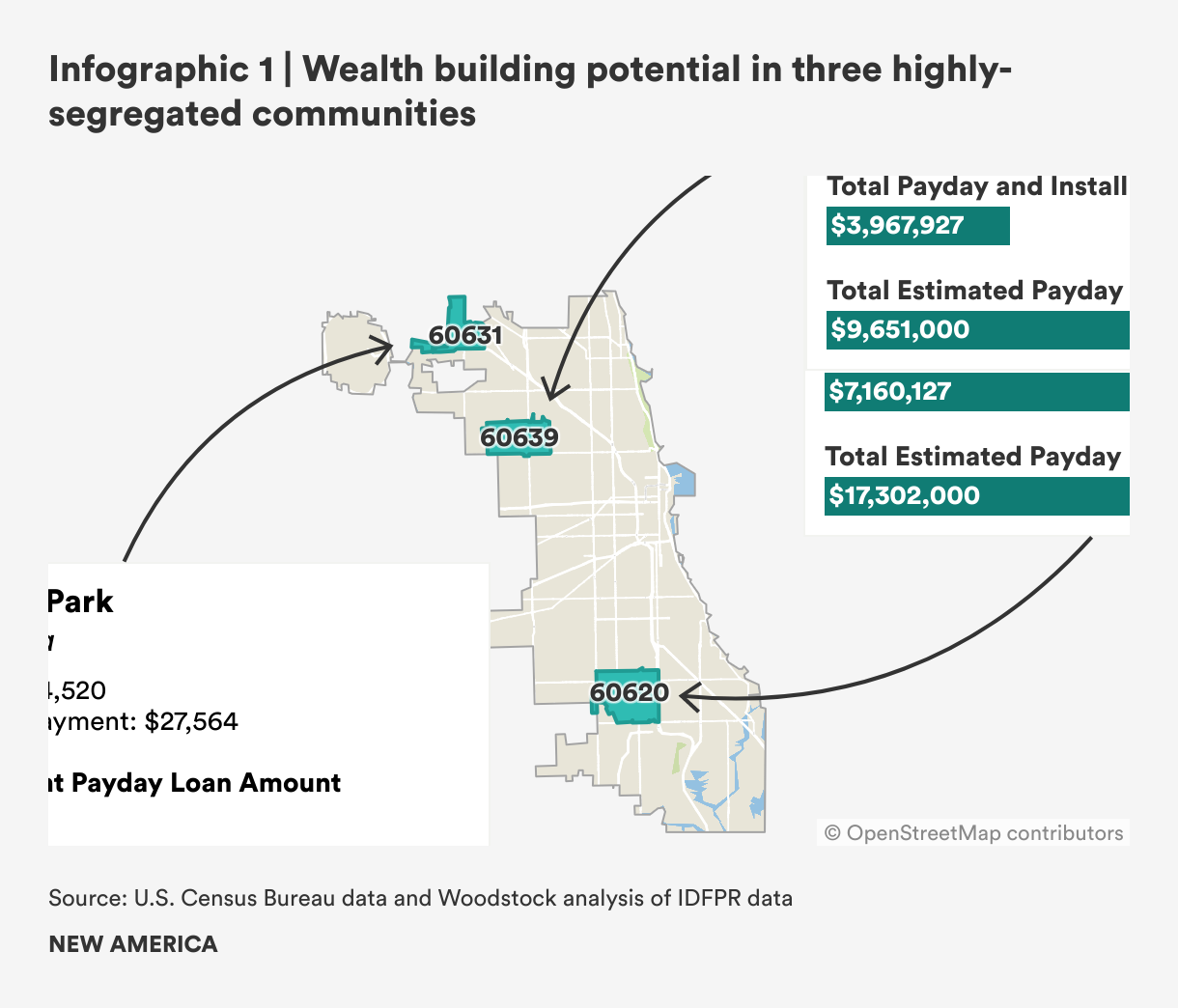

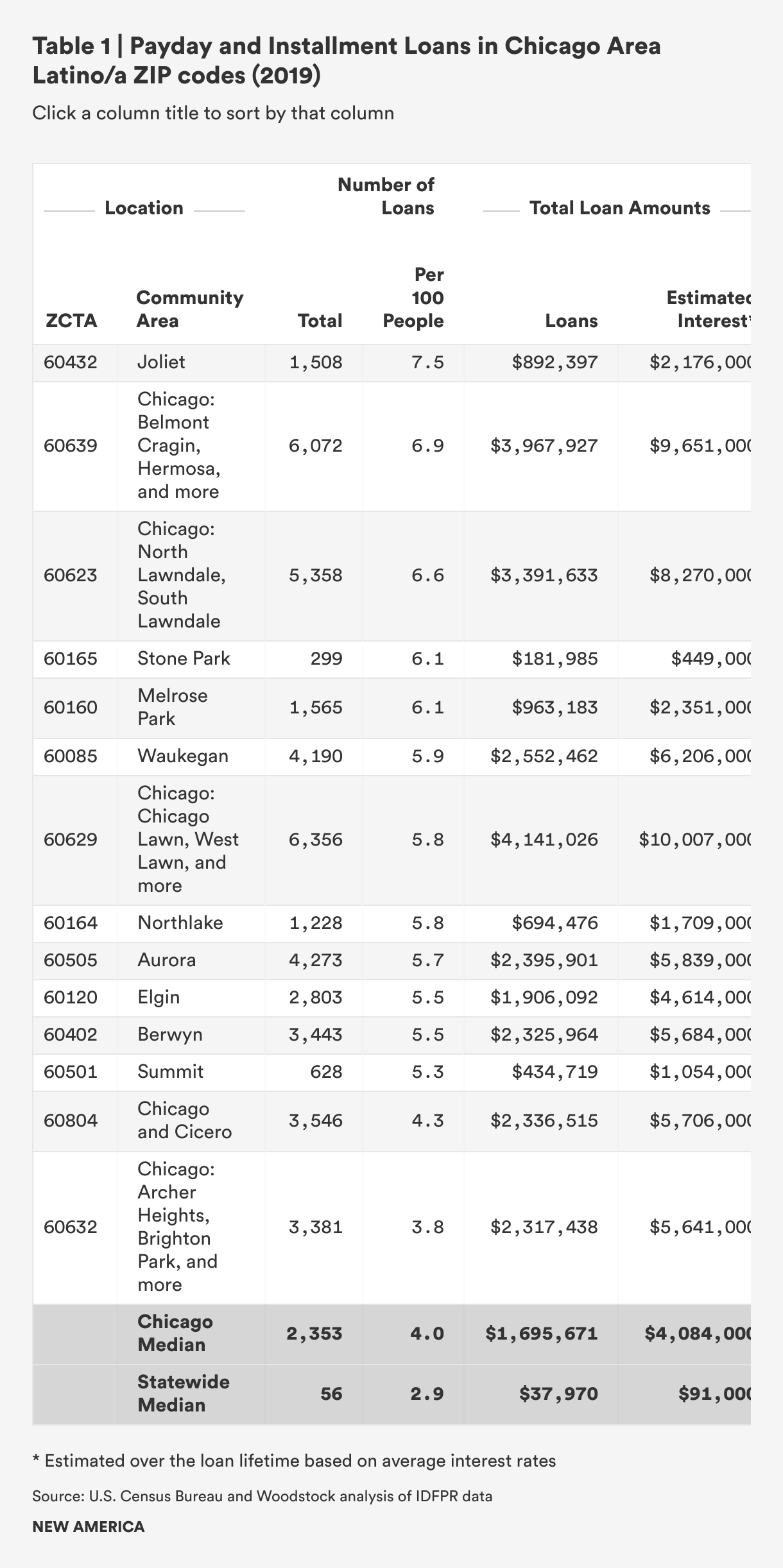

While there are fewer majority Latino/a areas than Black areas, across Latino/a city and suburban areas, the highest amount owed in payday loans was found in the city in 60629 (Chicago Lawn and West Lawn) which is 72 percent Latino/a. This was followed by 60639 (Belmont-Cragin and Hermosa) and 60623 (North and South Lawndale). In 2019, individuals in 60639, which is 78 percent Latino/a, paid over $9.6 million in payday and installment payday interest on over $3.9 million in loans.

Including suburban areas with high concentrations of Black and Latino/a residents, borrowers paid over $261 million in high interest on nearly $108 million in 2019 payday and installment payday loans. Majority Black suburbs, particularly Dolton, Broadview, and Robbins, have some of the highest rates of payday and installment payday loan usage in the entire state. In majority Latino/a metro areas, the highest number of payday loans per 100 people in majority metro areas was in 60432 (Joliet) despite a lower dollar amount than city ZIP codes. Two other suburban areas, 60165 (Stone Park) and 60160 (Melrose Park), also had some of the highest numbers of payday loans per 100 people in majority Latino/a ZIP codes.

Potential Threats to Consumer Protections in Illinois

While the PLPA is an essential piece of protective legislation for Illinois’s Black and Latino/a communities, the effectiveness of the law is threatened by constant opposition from the high-interest lending lobby. Potential loopholes that have been introduced or could be introduced in Illinois include:

- Reversing the PLPA’s “all-in” annual percentage rate (APR) definition to allow lenders to charge exorbitant fees and interest rates, similar to the Truth in Lending Act (TILA).

- Introducing a regulatory sandbox that could open the door to exclusions on interest caps.

- Allowing partnerships between predatory lenders and rogue “rent-a-banks,” or Native American tribes, which don’t have the same regulatory requirements, to skirt caps on interest.

- Creating carve-outs to redefine loans or exclude specific lenders, such as pawnbrokers.

To protect the integrity of the PLPA and prevent consumers from being exploited through hidden costs and excessive interest rates, lawmakers should be wary of similar bills in future years.

Policy Recommendations

Caps on interest rates put guardrails on the industry and are a good start. However, consumers aren’t always aware of affordable options and more action is required to ensure Black and Latino/a communities can protect and build wealth.

Protect Consumers from Further Predatory Practices

- Ensure consumers can access credit without paying exorbitant interest by protecting the 36 percent cap in Illinois and expanding the national Military Lending Act (MLA) to all consumers.

- Stop rent-a-bank predatory lending with monitoring by the Illinois Attorney General.

Improve Access to Banking and Lower-cost Alternatives to Predatory Loans

- Develop a state fund to increase access to low-cost loans in underserved cities and towns similar to the Ag Invest program, with banks, credit unions, fintech, and nonprofits.

- Pilot an individual and/or small business state emergency fund program for low-bank access areas through fintech and credit unions using targeted marketing.

- Establish and enforce robust affirmative obligations through the Illinois Community Reinvestment Act for banks, credit unions, and mortgage companies to lend to and invest in communities of color.

- Bring public banking to the post office, partnered with fintech to provide low-cost credit.

- Invest in nonprofit financial institutions to establish affordable small-dollar loan programs through the federal Community Development Financial Institutions (CDFI) Fund or other new sources.

- Pass the Overdraft Protection Act and limit high-to-low bank processing to protect low-income consumers from excessive banking fees.

- Address credit algorithm bias in regulations.9

Give Consumers New Tools to Manage Credit

- Ensure the accuracy of credit scores by amending the Fair Credit Reporting Act.

- Create transparency around consumer credit scores or create a public scoring agency to address institutionalized bias in home mortgages.10

Citations

- “Illinois Trends Report: Select Consumer Loan Products Through 2019” Illinois Department of Financial and Professional Regulation. 2020.

- For this analysis, we chose to do both racial and ethnic analysis. Unless otherwise stated, White refers to people who identified themselves as White, Not Hispanic. Black refers to those who identified themselves as Black, Not Hispanic. Latino/a numbers include anyone of any race who considers themselves ethnically Hispanic.

- CFPB Finds Four Out Of Five Payday Loans Are Rolled Over Or Renewed | Consumer Financial Protection Bureau. Consumer Financial Protection Bureau. 2014.

- “Illinois Trends Report: Select Consumer Loan Products Through 2020” Illinois Department of Financial and Professional Regulation. 2021.

- “Illinois Trends Report: Select Consumer Loan Products Through 2020” Illinois Department of Financial and Professional Regulation. 2021.

- Eisenberg-Guyot, J. et al. “From Payday Loans To Pawnshops: Fringe Banking, The Unbanked, And Health” Health Affairs 2018 37:3, 429-437

- Our analysis uses ZIP Code Tabulation Areas (ZCTAs) from the Census Bureau an approximation of ZIP codes from the USPS. We use the term ZIP code for readers who aren’t familiar with ZCTAs.

- Includes interest on both payday loans and longer-term installment payday loans.

- Bruckner, M. “The Promise and Perils of Algorithmic Lenders’ Use of Big Data” Chicago-Kent Law Review. Volume 92, Issue 1. 2018.

- Peterson, D. and D. Mann. Closing the Racial Inequality Gaps: The Economic Cost of Black Inequality in the U.S. CitiGPS. 2020

Introduction

Since the 1980s, lenders have stripped billions of dollars from Black and Latino/a communities in Chicago through high-cost, short-term loans. These loans, including but not limited to payday, installment payday, auto title, and car loans, often come with incredibly high interest rates and fees that make consumers pay double, triple, or quadruple their original loan amount. Sadly, many predatory lenders have targeted these loans to Black and Latino/a communities where access to bank branches and other financial services has been limited. Statewide, predatory lending has been concentrated primarily in Black low- and moderate-income Chicago neighborhoods and suburbs, although a considerable amount of predatory lending also targeted Latino/a communities.

Over the last four decades, this access to small-dollar credit has come at an incredibly high cost for Illinois families. Prior to the passage of the Predatory Loan Prevention Act (PLPA) in early 2021, charging inflated interest rates and tacking on high fees and draconian late payment penalties was an entirely legal, very lucrative scheme in Illinois. By 2019, the total annual loan principal on four types of predatory loans had gone up to over $1 billion per year in Illinois.1 Across different types of consumer loans, caps on rates varied widely. Lenders could charge families taking out a payday loan or short-term installment loan up to 404 percent legally. With the fourth-highest payday and auto title loan fee drain in the nation, Illinois families lost incredible amounts of money to the high-interest and fees on auto title loans, which had no caps prior to the PLPA.2 With incredibly high-interest and fees, small-dollar credit became an instrument for stripping billions of dollars from low- and moderate-income Illinois communities.

In particular, predatory lending is one of several common practices that have stripped billions of dollars from hard-working Black and Latino/a communities where they have been heavily targeted.3 In 2019, people in 17 ZIP codes with high concentrations of Black and Latino/a residents in the city of Chicago paid over $158 million in exorbitant payday loan interest.4 Including suburban areas with high concentrations of Black and Latino/a residents, borrowers paid over $261 million in high-interest rates on payday loans in one year. Now imagine those losses multiplied over decades and combined with billions lost in interest and fees on auto title loans, higher mortgage interest, disproportionate use of collection lawsuits for small debts, high-interest student loans, and bias in home appraisals. The massive impact on Black and Latino/a asset building is undeniable.

“It was a $1,500 loan, but we ended up paying $3,000 because of late payments when my mom had triple bypass surgery. We were paying double trying to play catch up. With a payday loan it is almost impossible to catch up when you miss payments.” – Indyia, former installment payday loan borrower

Citations

- “Illinois Trends Report: Select Consumer Loan Products Through 2019” Illinois Department of Financial and Professional Regulation. 2020.

- Standaert, D. et al. “Payday and Car-Title Lenders Drain Nearly $8 Billion in Fees Every Year” Center for Responsible Lending. 2019.

- For this analysis, we chose to do both racial and ethnic analysis. Unless otherwise stated, White refers to people who identified themselves as White, Not Hispanic. Black refers to those who identified themselves as Black, Not Hispanic. Latino/a numbers include anyone of any race who considers themselves ethnically Hispanic.

- Includes interest on both payday loans and longer-term installment payday loans.

Small-dollar Credit or Wealth-Stripping

For many Illinoisans, when money is tight, short-term or small-dollar loans have been a go-to. High-interest, small-dollar loans often provide access to high-risk cash at an extra cost in Black and Latino/a neighborhoods where bank access is limited, and lending practices are still discriminatory.1 Sadly, many Black and other traditionally marginalized Illinois residents turned to these expensive loans to try to bridge the gap between wages and the actual cost of living. Corporate greed and sky-high interest rates have left many in worse situations than before.

Nationally, users of predatory lending fall into one of four categories, those with insufficient income who borrow frequently, those who borrow frequently because their checks come at a different time (and less frequently) than their bills, and those who have an unexpected or expected major expense (new water heater or computer).2 However, research has shown most predatory loans end up being taken out again and again by the same lower-income individuals, part of a cycle of endless debt. The Consumer Financial Protection Bureau found that more than four out of five payday loans are re-borrowed within a month, and the majority of payday loans are borrowed by consumers who take out at least 10 loans in a row.3 Around 40 percent of those with misaligned cash flow and those with insufficient income take out more than six loans a year.4 In Illinois, from January 2012 to December 2020, 1,413,004 consumers took out 9,318,552 loans—an average of 6.6 loans per person.5 About 55 percent of Illinois’s reported consumer loan requests in 2019 were denied because the borrower already had too many loans or had a loan for too many days.6

“You don’t want to end up paying $1,000 for some gas, because of all of the interest. It was even worse than worrying about the house. The loan felt like a drip, drip, drip of a faucet, never-ending.” – Angie, former payday loan borrower

Individuals who earn less annually are more likely to live paycheck-to-paycheck, and as a result, are more likely to take out predatory loans than people with higher incomes. According to a 2012 Pew study, households making under $40,000 comprise 72 percent of payday borrowers.7 In 2020, the Financial Health Network found that roughly 50 percent of payday borrowers fall into the category of “financially vulnerable,” those who struggle with all aspects of their financial lives. The remaining 50 percent comes from a category they label as “financially coping,” those who only struggle with some aspects.8 Less research is available about borrowers of the other types of predatory loans like auto title loans and installment loans. However, in Illinois, borrowers of all four types of small dollar loans tend to be lower-income. Between 2012 and 2020, the average income of all Illinois small dollar credit borrowers was $33,542 per year. In the year of our analysis, 2019, 48.3 percent earned less than $30,000 per year and 78.6 percent earned less than $50,000 per year.9 Nationally, increasing income decreases reliance on payday lending: a $1 increase in the state minimum wage has been associated with a 40 percent drop in payday borrowing.10

It may come as no surprise then that around two-thirds of short-term borrowers either borrowed to cover a bill that arrived before payday or earned too little to cover basic expenses. Of these two groups, both primarily used loans to pay for basic living expenses.11 One study found that 64 percent of online payday and installment borrowers used the loan to cover regular expenses.12 A Pew study similarly found that the majority of payday borrowers do not use the funds for unexpected emergencies, but for recurring expenses such as rent, groceries, and utilities.13 One study found that states that expanded their Medicare access saw a 15 percent drop in payday, pawn, and check cashing services compared to states that didn’t, suggesting that the high costs of medical care can push people towards paying bills with high-interest loans.14

Carla’s Story: Trapped Paying Double Her Original Loan

When Carla first signed her loan paperwork, the excessive interest rates were shocking. But an unexpected car problem and no other line of credit access, left her feeling trapped. To Carla, payday loans were a necessary evil. Every month, the loan would steadily deplete her savings. By the end of her payment cycle, Carla had paid double what she owed, and undergone an enormous amount of mental stress. The experience, what she aptly describes as ‘robbing Peter to pay Paul’, is one she warns others to be cautious of.

Citations

- Charron-Chenier, R. “Predatory Inclusion in Consumer Credit: Explaining Black and White Disparities in Payday Loan Use” Social Science Research, Vol. 35, No. 2, June 2020.

- Bianchi, N. and Levy, R., “Know Your Borrower: Four Need Cases of Small-Dollar Consumers.” Center for Financial Services Innovation (now Financial Health Network). 2013.

- CFPB Finds Four Out Of Five Payday Loans Are Rolled Over Or Renewed | Consumer Financial Protection Bureau. Consumer Financial Protection Bureau. 2014.

- Bianchi and Levy, 2013

- “Illinois Trends Report: Select Consumer Loan Products Through 2020” Illinois Department of Financial and Professional Regulation. 2021.

- “Illinois Trends Report: Select Consumer Loan Products Through 2019” Illinois Department of Financial and Professional Regulation. 2020.

- “Payday Lending in America: Who Borrows, Where They Borrow, and Why” Pew Center for Responsible Lending, 2012.

- “Small Dollar Credit and Financial Health: A Policy Perspective” Financial Health Network. 2020.

- “Illinois Trends Report: Select Consumer Loan Products Through 2020” Illinois Department of Financial and Professional Regulation. 2021.

- Eisenberg-Guyot, J. et al. “From Payday Loans To Pawnshops: Fringe Banking, The Unbanked, And Health” Health Affairs 2018 37:3, 429-437

- Bianchi and Levy, 2013.

- “Online Payday and Installment Loans: Who Uses Them and Why?” Manpower Demonstration Research Corporation (MDRC). 2016.

- “Payday Lending in America: Who Borrows, Where They Borrow, and Why” Pew Center for Responsible Lending, 2012.

- Fitzpatrick, A and Fitzpatrick, K. “Health Insurance and High Cost Borrowing: The Effect of Medicaid on Pawn Loans, Payday Loans, and Other Non-Bank Financial Products.” prepared for the Federal Reserve 2019 biennial Community Development Research Conference, 2019.

Predatory Loans Hit Chicago’s Black and Latino/a Communities Hard

Exorbitant interest and fees have cost Black and Latino/a communities dearly, as those same communities struggled with fewer assets, lower incomes, and lesser access to banks and affordable financial products. Over the years, predatory loans have taken a major financial toll in Black communities in the Chicago area, especially, making it more difficult for families to build a cushion of assets to weather major disasters and build a secure future.

Nationally, studies on payday loans specifically have shown that the majority of users are non-white. In 2016, nearly half of the households who used payday loans were non-white (47 percent). Black households were 2.5 times more likely than white households to have used a payday loan.1 Although these loans allow traditionally excluded households access to cash, this access is provided under high-pressure conditions, along with extremely high-interest rates, that ultimately threaten long-term financial stability. While individuals often use these loans to make ends meet, the incredibly high-interest rates end up taking money needed for living expenses, throwing people into a wrenching cycle of debt.

Our analysis of two types of payday loan data shows a similar pattern.2 Across the state, two major types of predatory borrowing, payday and installment payday loans, were much more concentrated in majority Black, majority Latino/a, and majority-minority ZIP codes than majority white ZIP codes.3 In Chicago, by the sheer number of loans and dollars borrowed, payday and installment payday loans were almost ten times more common on average in majority Black ZIP codes and over seven times more common in majority Latino/a ZIP codes than white ZIP codes.

Predatory Loans are Particularly High in Black Chicago Metro Area Communities

These loans are particularly high in Chicago metro area Black communities, with a substantial number of loans in Latino/a areas as well. A considerable amount of these loans are concentrated in primarily Black suburbs. Dolton, Broadview, and Robbins have some of the highest rates of payday and installment payday loan usage in the entire state. The first two have just over 20 loans per 100 people. Robbins has almost 19 payday loans per 100 people. The residents of Dolton are over 92 percent Black, and all three suburbs are over 75 percent Black. Several other suburbs with high concentrations of Black residents include ZIP codes with some of the highest rates of payday loans statewide (see Appendix B for a detailed list).

In the city of Chicago proper, payday and installment payday loans were highest in highly segregated Black ZIP codes. Looking at how common these loans are and taking population size into account, the seven ZIP codes in Chicago with the highest number of loans per person are all over 87 percent Black, with the exception of one ZIP code in the Loop. The highest number of payday loans per capita is found in 60619, which also has the highest percentage of Black residents in the city. The area includes Burnside and Chatham, among other neighborhoods, and has nearly 17 payday and installment payday loans per 100 people. Following close behind, 60620, which includes parts of Auburn Gresham and Washington Heights, among other neighborhoods, is second in per capita payday loans and is also over 95 percent Black. These two ZIP codes alone paid over $30 million in interest on just the payday loans made in one year. Yet both communities have median annual incomes between $37,000 to $39,000. In 60620, the interest paid would have consumed the average mortgage payments for an entire year for 1,300 families.

Latino/a Areas Less Concentrated but Pay Millions in Exorbitant Interest Each Year

In the Chicago area and all over the state, there are much fewer concentrated Latino/a ZIP codes. So, targeting these ethnic communities based on geographic location is more difficult to do and there are fewer obvious patterns in loan usage. Payday loans are less common in concentrated Latino/a ZIP codes than in concentrated Black ZIP codes. However, payday loans are still much more common on average in majority Latino/a ZIP codes than in majority white ZIP codes in Chicago. In particular, the average number of loans and amount of loans is considerably higher in majority Latino/a ZIP codes in the city than in white areas. The Latino/a areas with the highest payday borrowing dollar amounts also tend to have lower median incomes than other areas. Payday loans show a slightly different pattern than installment payday loans suggesting they may have been more common in Latino/a areas.

Payday borrowing was somewhat higher in 2019 in Latino/a areas of the city ($16.2 million) than majority Latino/a suburban areas ($12.3 million). Across Latino/a metro areas, the highest amount owed in payday loans was found in the city in 60629 (Chicago Lawn and West Lawn). This was followed by 60639 (Belmont-Cragin and Hermosa) and 60623 (North and South Lawndale). While city of Chicago majority Latino/a areas lead overall in the amount of dollars borrowed, one suburban area edged out city ZIP codes in per person incidence. Across metro area ZIP codes with high concentrations of Latino/a residents, the highest number of payday loans per 100 people was in 60432 (Joliet) despite a lower dollar amount, followed by 60639 (Belmont-Cragin) and 60623 (North and South Lawndale). The other two areas rounding out the top five were both suburban 60165 (Stone Park) and 60160 (Melrose Park). Across the majority Latino/a areas of the metro area, 60623 had the lowest median income at $34,431, over $12,000 less per year than any other majority Latino/a ZIP code (see Appendix B for a detailed list).

In just one year, people in highly concentrated Chicago Black and Latino/a ZIP codes borrowed $65.3 million in payday and installment payday loans. With average interest rates and fees equaling 299 percent for payday loans and 233 percent for installment loans, this means these 17 ZIP codes lost another $158.2 million in interest just from 2019 loans. Including majority Black and Latino/a communities across the city and suburbs, these communities paid $261.9 million in exorbitant interest rates for loans made in 2019.

It’s important to note that auto title and auto purchase loans, which had no cap prior to the PLPA, are not included in these figures. This suggests that the financial hit to Black and Latino/a communities is much higher than realized. Over many years, the combined cost to communities represents billions of dollars in lost wealth.

Illinois Consumers Are Still Struggling to Pay Pre-PLPA Loans

In fall 2021, New America Chicago conducted interviews with borrowers from the Chicagoland area who have taken out short-term, high-interest loans within the last two years to better understand their experiences and how these loans have impacted their financial well-being. Interviewees who had taken loans out prior to the passage of PLPA were still struggling to pay them back. In particular, unclear terms as well as high fees and interest rates had jacked up the cost of the loans and made them difficult to pay off.

The interviews confirmed much of the current literature on consumer borrowers. Interviewers found that the participants all took out loans for commonly cited reasons, including lapses in income (e.g., laid off from work, money tied up somewhere else), planned expenses (e.g., bills, rent, the holiday season), and unexpected expenses (e.g., medical bills, car repairs). However, we also found that the pandemic unexpectedly impacted many people’s employment situations and exacerbated their need for money. Hours were cut at work, or they were laid off entirely, with no clear sign as to when they were going to return. Fortunately, many participants are currently in a better place financially and attributed that to the additional support provided in response to COVID-19 like the extended and enhanced unemployment insurance benefits, the expanded Child Tax Credit (CTC), and more. Small dollar lending in Illinois also dropped following the beginning of relief dollars to individuals. Lending dropped substantially in April through August of 2020 compared to the first three months of 2020.4

“I have been fully booked [for work] for 20 years, every summer for weddings. So I'm fully booked by January…So everything gets shut down in May and canceled. I just bought my house. We just put everything into it. OK? So my husband is a carpenter. It was horrible. It was scary and it was horrible.” – Tracy, former auto title loan borrower

One common factor amongst nearly all of the participants was time. People stressed how payday, auto title, and payday installment loans seemed to be the best option for getting small amounts of cash quickly. Those that were banked mentioned attempting or contemplating borrowing from their financial institution but that the process was too cumbersome for the amount they needed. On the other hand, high-cost lenders pride themselves on “quick cash,” so one could apply for one of these short-term, high-interest loans and receive funds as soon as the next day, if not the same day. Ironically, while getting the cash was especially quick, getting out of the ensuing cycle of debt was unexpectedly long.

Misaligned income and emergencies happen. However, a lack of accessible, fast lending options combined with predatory lenders’ robust marketing and easy-to-find products drive consumers to high-interest products, which unfortunately have been designed to fit this very niche. As inflation increases the costs of basic living essentials and relief funding comes to an end, access to cash is likely to become more of an issue over time for Chicago residents.

Citations

- Charron-Chenier, R. “Predatory Inclusion in Consumer Credit: Explaining Black and White Disparities in Payday Loan Use” Social Science Research, Vol. 35, No. 2, June 2020

- Data made available from the Illinois Department of Financial and Professional Regulations only included two types of loans, payday and installment payday. Several other types exist and also have historically had very high average interest rates and in some cases no caps on interest rates.

- Our analysis uses ZIP Code Tabulation Areas (ZCTAs) from the Census Bureau an approximation of ZIP codes from the USPS. We use the term ZIP code for readers who aren’t familiar with ZCTAs.

- Woodstock Institute analysis of 2020 data from the Illinois Department of Financial and Professional Regulation.

Potential Threats to Consumer Protections in Illinois

As these numbers demonstrate, predatory APRs on small dollar loans have taken an incredible financial toll on Black and Latino/a communities in Chicago. The passage of the PLPA made it illegal to charge exorbitant interest and fees on personal loans in Illinois. However, while the PLPA is an essential piece of protective legislation for Illinois’s Black and Latino/a communities, the effectiveness of the law is threatened by two main issues.

- Opposition to the PLPA is strong in the high-interest lending industry. The pawnbrokers and high-cost installment lenders have been especially vigorous. The strong industry lobby is continually introducing loophole legislation.

- The new law is part of the solution, but consumers still need financial support. For it to be truly effective at increasing wealth-building in Black and Latino/a households, more affordable alternatives and other resources are essential to address the demand for cash.

“The first loans I ever took out, I was 21 or 22. My interest rate went up to like 400 percent… I owed $1,000 on the $500 loan and $900 on the $498 loan. I took them out because I was trying to catch up on my bills.” – Chris, former payday loan borrower

Protecting Consumers Against Loopholes

To some degree, high-interest lending can be like a hydra-headed dragon. Laws may cut off one head only to have another source of high-interest credit take its place. Policymakers who are intent on ensuring that people have access to credit at reasonable interest rates must consider all of the ways that lenders might work to circumvent the law.

Research indicates that after state legislation that limits payday lending, companies find policy loopholes and create other products that can be used in place of payday loans. For example, in Ohio, with the passage of the Short-Term Loan Law, the state of Ohio effectively banned the payday lending industry with binding fee restrictions. However, small loan products and second mortgages increased dramatically, despite the fact that in the wake of the housing financial crisis, credit was severely restricted. Payday lenders in Ohio effectively relicensed under other types of small loan lenders, which allowed them to keep operating.1 Creating clear and thorough policy ensures that the small lenders are not pushed to other areas where they can operate the same sorts of business under differing licensure.

The Illinois Predatory Loan Protection Act includes several provisions to protect consumers from some of the most common loopholes exploited by lenders to erode consumer protections. Namely, lenders in other states have sought to circumvent interest rate caps through (1) online lending, (2) partnerships with Native American tribes who hold sovereign immunity (similar to ‘Rent-a-bank’ schemes2), and (3) operating under open-end credit statutes.3 Due to limited enforcement power on the internet, online lenders have a history of attempting to evade state laws and licensing requirements.4 This has been seen in California and Virginia, where reforms have now been made to strengthen provisions against online predatory lending.5 Small dollar lenders in states that have restrictions and bans frequently form partnerships with Native American tribes, who are immune to consumer protection laws, to skirt regulations. This practice has been seen in states such as Illinois, Arizona, Oklahoma, and Colorado, where lenders fraudulently operate as tribal businesses, despite only a small percentage of profits going towards said tribes.

The Act includes a sweeping anti-evasion provision that accounts for lenders using this bank-partnership model, and applies to open end-credit as well as online lending. However, it should be noted that borrowers can still travel to or obtain loans online from states that do not enforce restrictions. Lawmakers must ensure these anti-evasion provisions are enforced, and be wary of bills that seek to circumvent them. In the spring of 2021, SB 2306/HB 3192 was introduced in Illinois to overturn the “all-in” annual percentage rate (APR) similar to the Military Lending Act (MLA) in favor of the Truth in Lending Act (TILA) definition of APR.6 Under TILA, the APR calculation excludes “add-on” products and fees, allowing predatory lenders to disguise the true cost of loans to borrowers.

“It depressed me. It really did… It’s a vicious cycle. You find yourself just spinning and spinning” – Carla, former payday loan borrower

During the Illinois General Assembly’s fall veto session in 2021, lawmakers also explored the introduction of regulatory sandbox legislation that could have opened the door to exclusions to caps on interest. Regulatory sandboxes were introduced in 2015 in the U.K. as a place for financial technology (fintech) firms, in particular, to test new products without immediately running into regulatory issues.7 In the United States, states have enacted sandboxes to enable companies to operate without a license. While regulatory sandboxes can be used to incentivize innovations to improve financial inclusion, according to the World Bank, there is little evidence that they actually improve inclusion. In addition, well-designed sandboxes can cost regulatory agencies as much as one million dollars to run, and they require thoughtful design to ensure they are not simply used as a loophole for lenders to escape interest rate caps.8 Perhaps most importantly, most sandboxes are not designed for consumers who have traditionally been excluded from mainstream credit.9 While a well-designed regulatory sandbox could theoretically improve financial inclusion, the process needs to be explicitly and carefully designed to ensure it has the intended impact without weakening consumer protections. To protect the integrity of the PLPA and prevent consumers from being exploited through hidden fees, lawmakers should be wary of similar bills in future years.

Supporting Families by Addressing the Need for Cash

Across the country, a number of different states have implemented different regulations on payday and other high-interest loans. While the results have been mostly positive, consumers continue to need access to cash. Caps on interest rates such as Illinois’s PLPA and the national MLA, help put guardrails on the lending industry to keep rates reasonable for consumers, but they do not eliminate the need for gap funding or emergency funds. Predatory loans are most often taken to cover basic needs for a population that has less generational wealth and continues to be paid less income for similar work. As long as low-wage jobs and racism exist, there will always be people who simply don’t have enough income for monthly costs, major purchases, or one-time emergencies. Policy incentives to improve access to lower-cost lending alternatives, improve wealth creation, and credit are essential to ensure Black and Latino/a communities receive the full benefits intended by the legislation.

Citations

- Ramirez, S. An examination of firm licensing behaviour after a payday-loan ban Applied Economics, Volume 51, 2019 – Issue 46.

- In many states, lenders have historically dodged payday, installment, and car-title rate caps by partnering with banks exempt from restrictions, paying a fee for use of their name. President Biden signed a bill into law prohibiting such arrangements on a federal level, although not all of these types of arrangements have been banned.

- This tactic was utilized by lenders in Virginia before reform was introduced in 2020. The Rent-A-Bank Scheme. Center for Responsible Lending. 2021.

- Fraud and Abuse Online: Harmful Practices in Internet Payday Lending. The Pew Charitable Trusts. 2014.

- Skirting the Law: Five Tactics Payday Lenders Use to Evade Consumer Protection Laws. U.S. House of Representatives Financial Services Committee Report.n.d.; Horowitz, A. and Bourke, N.Virginia Fairness in Lending Act of 2020 Reforms Small Credit, The Pew Charitable Trusts, 2020.

- PLPA Coalition Fact Sheet. Illinois Asset Building Group, 2021

- Regulatory Sandbox. Financial Conduct Authority (U.K.), 2015.

- Appaya, S. et al. Global Experiences from Regulatory Sandboxes. 2020; Appaya, S and I. Jenik. Running a Sandbox May Cost $1 Million, Survey Shows, 2019.

- CGAP and World Bank survey 2019. Retrieved at source on 11/30/21.

Policy Recommendations

Ensuring that Illinois’s lowest-income communities are protected from exorbitant interest and have the resources they need to build wealth will require both strengthening affordable alternatives and ensuring the strength of the PLPA. Policy recommendations follow to address the remaining gaps. Most of these policy decisions are made at the state and federal levels.

Protect Consumers from Further Predatory Practices

- Ensure consumers can access credit without paying exorbitant interest. Protect the 36 percent cap on all consumer loans in Illinois. Nationally, expand the national Military Lending Act’s 36 percent rate cap on consumer loans, which currently protects active-duty military and their families, to all consumers in the United States

- Stop “rent-a-bank" predatory lending. Similar to a recent effort in the District of Columbia, the Illinois Attorney General’s office can monitor whether online lenders are making loans to Illinois consumers at rates in excess of 36 percent APR.

Improve Access to Banking and Lower-cost Alternatives to Predatory Loans

- Develop a State Fund to Increase Access To Low-Cost Loans. The Illinois State Treasurer’s Office currently has a program called Ag Invest that provides loan opportunities for Illinois farmers. We recommend a similar program be created to provide small-dollar loans for underserved cities and towns in partnership with trusted banks, credit unions, fintech, and nonprofits. A loan guarantee fund could mitigate the risk to banks and credit unions of creating affordable short-term loans and engage good fintech actors to expand online options.

- Invest in an Emergency Fund Program through Fintech and Local Credit Unions. Pilot a state model to provide funding for emergency needs in low-bank access areas. Streamlining delivery and investing in good marketing could help improve access for people who need cash quickly. The program could also be made available to small businesses.

- Establish and Enforce Robust Community Reinvestment Requirements. The new Illinois Community Reinvestment Act should establish affirmative obligations for banks, credit unions, and mortgage companies covered by the law to lend to, invest in, and serve Black and Latino/a communities.

- Bring Public Banking to the Post Office. The U.S. Postal Service is currently conducting a pilot program of banking, similar to other countries and a prior U.S. program. Partnering with fintechs to provide access to low-cost credit in addition to basic check cashing would expand access to needed banking in urban and rural areas that lack a bank branch. In Chicago Urban League’s focus group findings, people felt the post office could offer good locations to improve access to fair banking practices.

- Invest in Nonprofit Financial Institutions to Establish Affordable Small-Dollar Loan Programs. The federal Community Development Financial Institutions (CDFI) Fund enables CDFIs to provide loans to underserved communities. One such CDFI, Capital Good Fund, provides affordable loans to borrowers who have an average credit score of 580. We support increasing the FY 2022 CFDI Fund appropriation from last year’s appropriation of $270 million.

- Pass the Overdraft Protection Act. Federal legislation would limit the number of overdraft fees banks can charge to one per month and no more than six per year, and end overdraft fees based solely on debit ‘holds’ still in process. Protecting consumers from abusive overdraft practices would partially eliminate the need for payday borrowing and may alleviate some of the racial inequality in exposure to risky credit products documented in this paper.

- Address Credit Algorithm Bias. Algorithms used to make lending decisions often perpetuate existing systems of racial inequity. New, more equitable methods of assessing creditworthiness are possible. Regulating the use of algorithms and what inputs are allowable would be a benefit to people of color who often lack access to more traditional credit options.1

Give Consumers New Tools to Manage Credit

- Pass Legislation to Ensure Accuracy of Credit Scores. Ensure that credit scores are accurate through legislation amending the Fair Credit Reporting Act.

- Create Transparency Around Consumer Credit Scores or Create a Public Scoring Agency. Currently, credit scores are considered “trade secrets,” but there appears to be implicit bias inherent in the scores that has cost the economy trillions of dollars and has kept three-quarters of a million Black borrowers from homeownership.2 Creating a public credit scoring agency could address this issue.

Citations

- Bruckner, M. “The Promise and Perils of Algorithmic Lenders’ Use of Big Data” Chicago-Kent Law Review. Volume 92, Issue 1. 2018.

- Peterson, D. and D. Mann. Closing the Racial Inequality Gaps: The Economic Cost of Black Inequality in the U.S. CitiGPS. 2020

Conclusion

Billions of dollars in potential wealth have been stripped out of Chicago’s Black and Latino/a communities since the 1980s. The exorbitant interest and fees charged by payday, installment, auto title, pawn, and other short-term, small-dollar loans has accelerated the drain of potential assets from these communities. When taken as a whole with generational losses due to high-interest student loans, racist housing valuation practices, higher mortgage interest, and a multitude of other inequitable financial practices, the impact on financial health is astounding. The Predatory Loan Prevention Act of 2021 is a start. To truly protect Black and Latino/a wealth and build a prosperous community, the law must be protected, and further steps must be taken to address the underlying issues and provide new opportunities for communities. The future of the entire Chicago region will rise or fall depending on the outcome.

Appendices

Appendix A: Methodology

Data for the analysis of patterns of predatory consumer lending came from three sources:

- The first data source was a list of all payday and installment payday loans made between January 2019 and December 2020. The Illinois Department of Financial and Professional Regulation (IDFPR) provided the data in response to requests Woodstock Institute made under the Freedom of Information Act. The data included the loan date, loan amount, and the ZIP code of the borrower. The initial data that IDFPR provided covered the period from January 2019 through August 2020. IDFPR later supplemented the data to include loans made through December 2020, although we were not able to complete analysis of 2020 data prior to writing this report.

- The second data source was the 2019 American Community Survey (ACS) 5-year estimates for ZIP Code Tabulation Areas (ZCTA) in Illinois. The data included counts of the population in each ZCTA broken down by whether the respondent identified as Hispanic/Latino, non-Hispanic Black, non-Hispanic White, and non-Hispanic of some other race. ZCTAs are the geographic area that the Census Bureau publishes as its approximation of ZIP code geographies, which the United States Postal Service defines. While the boundaries of ZCTAs do not align perfectly with those of ZIP codes, ZCTA data are commonly used as a proxy for ZIP code data.

- The third data source was the annual Illinois Trends Report: Select Consumer Loan Products, prepared for IDFPR annually by Veritec Solutions, LLC, for all years from 2012 to 2019, as well as the subsequent report for all years from 2012 to 2020. Those reports present summaries of payday loans, installment payday loans, and auto title loans, including the total number of loans, customers, and fees for each category of consumer loan.

Analysis aggregated the payday and installment payday loan data for 2019 by ZIP code and linked those data with the ZCTA data on ethnicity/race. The linked dataset showed the correlations between, and the magnitude of, the disparities in the use of payday and installment payday loans and the ethnic or racial characteristics of the ZIP code in which the borrower lived. That analysis showed strong correlations between the racial or ethnic composition of the ZCTA and the number and amount per capita of payday and installment payday lending, with the highest levels in ZCTAs with the highest percentage of Black or Latino/a population.

For the purpose of this report, after much discussion the coalition agreed to use disaggregated Census data to do both ethnic and racial analysis. Unless otherwise stated, white refers to people who identified themselves as white, not Hispanic. Black refers to those who identified themselves as Black, not Hispanic. Latino/a numbers include anyone of any race who considers themselves ethnically Hispanic.

The next part of the analysis used data from the Trends Reports for the annual total number and amount of payday, installment payday, and auto title loans, and estimate the total fees charged in connection with each category of loan. The reported amount of fees in each successive Trends Report is an average amount based on the sum of fees charged for each category of loan from January, 2012, to the end of the reporting year (the “Reporting Period”). Estimating the average amount of fees per loan in 2019, therefore, meant determining how high the average fees per loan would have had to be in 2019 to raise the average from what it was in 2018. The average total fees for payday loans were $52.06 in 2019 and $51.24 in 2018. The product of the number of loans in the Reporting Period for 2019 times the average fees ($52.06) is the total fees paid between January 2012 and December 2019. The product of the number of loans in the Reporting Period for 2018 times the average fees ($51.24) is the total fees paid between January 2012 and December 2018. The difference between the total for 2019 and the total for 2018 is the amount of fees paid in 2019. That difference was $476.6 million in total fees for payday, installment payday, and auto title loans combined.

The third part of the analysis compared the number and amount of payday and installment payday loans, by ZIP code, for the period between January and March 2020 and the period from April through August 2020. That comparison showed the difference between the levels of payday and installment payday lending before and after the major impacts of COVID-19 began to affect the economy, and COVID relief programs began providing support to people adversely affected by the pandemic. The analysis showed a substantial decrease in the use of payday and installment payday loans in the period after the beginning of the pandemic.

Appendix B: Payday and Installment Loans and Interest In Majority Black and Latino/a ZIP Code Tabulation Areas

Click on the header of each column to sort by that column.

More About the Authors

Spencer Cowan

Meegan Dugan Adell

Director, New America Chicago

Kathie Kane-Willis

Hala Kourtu

Vanessa Rangel

Senior Program Associate, New America Chicago

Issues

Programs/Projects/Initiatives

Related

Chicago Residents Design Better Small Dollar Loans