Great Power Resource Competition in a Changing Climate

Table of Contents

Abstract

Natural security, or having enough energy, food, minerals, and water, is essential to supporting stable and prosperous societies. A growing global population, however, needs more resources to meet rising standards of living, even as the industrial age’s bill is coming due in the form of sweeping environmental degradation. Climate change is reshaping global natural security, affecting water availability, weather patterns, agricultural productivity, the energy trade, and the demand for critical minerals. Put simply: natural security is under threat around the world.

China and the United States, the two biggest global economies, are also the biggest polluters and consumers of the world’s resources. Their natural security affects everyone else’s, both in terms of meeting demand and dealing with the consequences of high consumption. Moreover, the United States has declared a new era of “great power competition” and singled out China. Natural security will be a key part of the rivalry, especially as these two countries already rely on some of the same suppliers for key resources—including each other, for now.

New America’s Natural Security Index compares the natural security of China and the United States and identifies their top resource allies and trade partners. By comparing the countries’ resources, production, imports, and exports, the index finds that the United States has a comparative natural security advantage over China, though China has a more diversified resource trade and investment portfolio, according to our analysis. Altogether, this project suggests that natural resources will help shape the competition between the United States and China for geopolitical influence and investments—and that competition will, in turn, shape global natural security.

Acknowledgments

The Natural Security Index draws on the original research of Wyatt Scott and Francis Gassert, who sifted through numerous international and U.S. databases and analyses and combined observations and data in novel ways. This involved both calculation and creativity. The project first started as a collaboration with the Joint Global Change Research Institute to look at what the Global Change Assessment Model suggested about the ways in which climate change might affect great power competition. As part of that exploration, the Program Director, Sharon Burke, asked Wyatt Scott to identify China’s key resource trade partners through systematic analysis and by building a matrix of key attributes. This report grew out of Wyatt’s initial data search, greatly enhanced when Francis Gassert joined the team, adding rigor on the data analysis and leading the climate change portion of the report. This was a ground up research effort, in the sense that we did not have a pre-cooked hypothesis, beyond the assumption that natural resources are important, and we looked to the data to suggest key findings. Maria Elkin of New America provided invaluable editorial advice and guidance, and Elise Campbell supported the project team throughout the process. We’re also grateful to Chris Roney, Leon Clarke, Jae Edmonds, and Sha Yu of the Joint Global Change Research Institute for starting the conversation with us, and for their model runs, analysis, and subject matter expertise. One of the most important sources of information for our work is a relatively unsung government agency: the U.S. Geological Survey, an amazing national resource. Finally, we thank the Skoll Global Threats Fund, which has since closed shop, for their support of our work.

Introduction

Grigvovan / Shutterstock

Natural security, or having enough energy, food, minerals, and water, is essential to supporting stable and prosperous societies. A growing global population, however, needs more resources to meet rising standards of living, even as the industrial age’s bill is coming due in the form of sweeping environmental degradation. Climate change is reshaping global natural security, affecting water availability, weather patterns, agricultural productivity, the energy trade, and the demand for critical minerals. Put simply: natural security is under threat around the world.

China and the United States, the two biggest global economies, are also the biggest polluters and consumers of the world’s resources. Their natural security affects everyone else’s, both in terms of meeting demand and dealing with the consequences of high consumption. Moreover, the United States has declared a new era of “great power competition” and singled out China. Natural security will be a key part of the rivalry, especially as these two countries already rely on some of the same suppliers for key resources—including each other, for now.

New America’s Natural Security Index compares the natural security of China and the United States and identifies their top resource allies and trade partners. By comparing the countries’ resources, production, imports, and exports, the index finds that the United States has a comparative natural security advantage over China, though China has a more diversified resource trade and investment portfolio, according to our analysis. Altogether, this project suggests that natural resources will help shape the competition between the United States and China for geopolitical influence and investments—and that competition will, in turn, shape global natural security.

Key findings

- The United States has inherent natural security, an advantage in global great power competition, though private sector and market forces largely shape the patterns of U.S. global natural resource engagement. National power investments (diplomacy, economic engagement, military cooperation) sometimes coincide with key resource trade partners, but not always.

- China has significant natural resources, including agriculture and critical minerals, but not enough to meet the demands of such a large population. The government meets this challenge with a diversified, centrally-controlled global trade and investment strategy. National power investments (diplomacy, economic engagement, military cooperation) generally are consistent with these resource relationships.

- The United States’ strongest resource relationships are with its closest neighbors. While China has a more diversified mix (i.e., Brazil and Indonesia are equally important to China), Russia is a top partner.

- Australia may be a point of contention or convergence, as a top natural security partner for China and a key strategic ally for the United States.

- In the future, as the United States and China jockey for the competitive edge in high tech industries and renewable energy technology, that will increasingly drive competition over critical mineral resources and major producing countries, such as Australia, Brazil, Chile, Indonesia, South Africa, and the Democratic Republic of the Congo.

- Global climate change is already affecting natural resources, especially agriculture, a trend that will worsen over the course of the century. Although China is positioning to maintain its natural security, that may be at the expense of global markets, which the United States counts on for its own natural security.

- Even in a worst-case climate change scenario, the United States should remain a major agricultural producer by mid-century, though growing regions may shift northward and there may be fewer exports. These shifts have the potential to be economically and socially disruptive. The Chinese may have to increase their dependence on agricultural imports, particularly for corn and wheat. Russia and Canada may be relative winners, with increases in arable land, though many uncertainties remain about the effects of drought and more volatile weather worldwide.

- Although natural security could become a sore point in the relationship between the United States and China, it could also be a source of cooperation and confidence building. In particular, these competitors could work together on critical minerals, including research and development on less destructive ways to mine and refine these materials. Moreover, as climate change challenges agricultural productivity worldwide, international cooperation and trade will play an important part in adapting to changing conditions.

Methodology

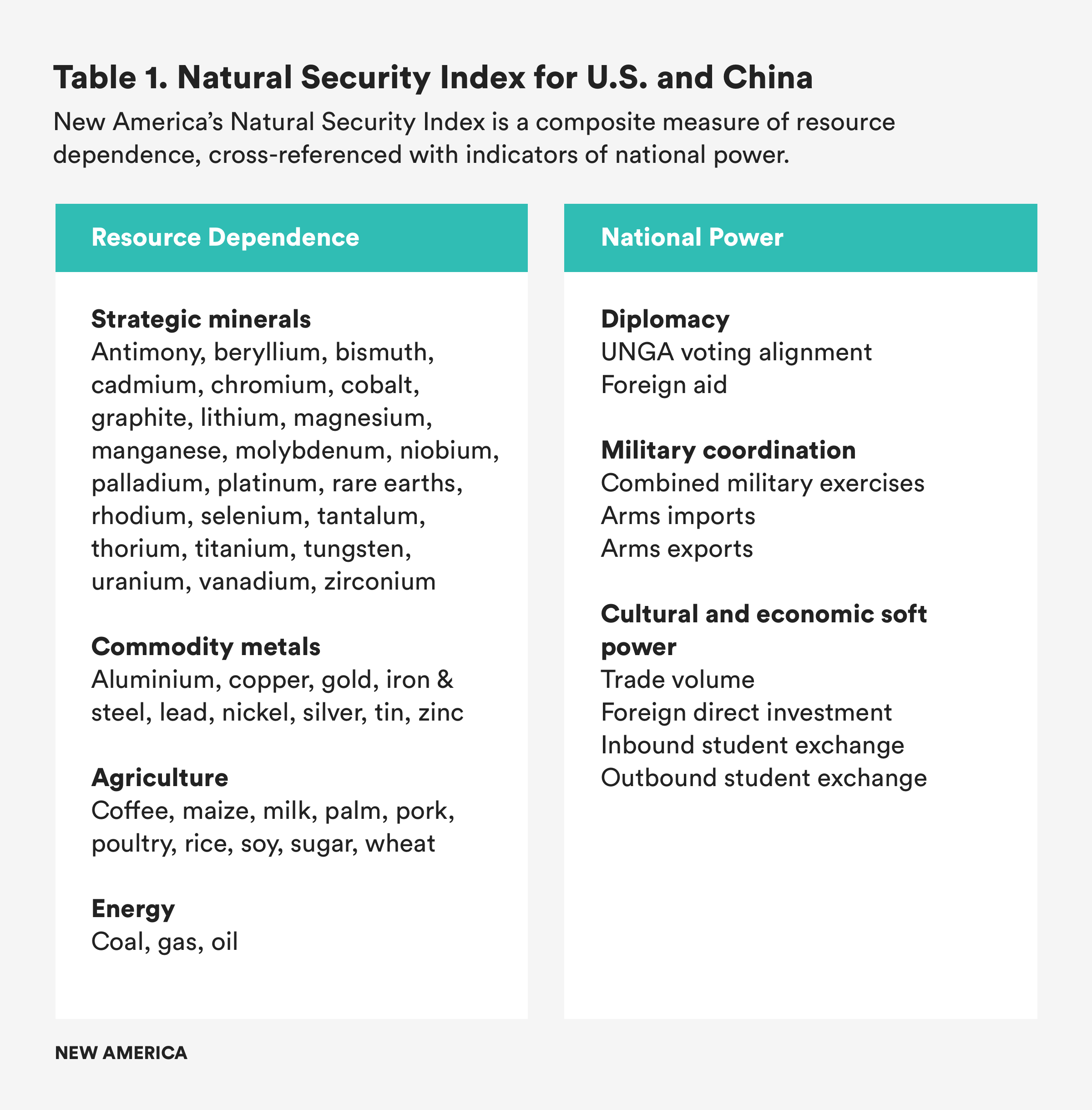

The goal of the Natural Security Index is to quantify the importance of bilateral trade relationships to the national security of the United States and China, with a focus on key natural resources. It provides a contemporaneous snapshot of countries’ natural resources, military, diplomatic, and soft-power relationships, and functions as a means of comparison between states’ military alignments, their international objectives as represented through formal posturing, and organic relationships of their citizenry and economies.

The Natural Security Index aggregates thousands of data points for resources that are of significant value to the world economy or are considered “strategic” by the Chinese and American governments. We also looked specifically at how climate change may affect key resources and cross-referenced natural security with national power indicators, such as number of combined military exercises, commercial activity, and cultural engagement. The goal was to look at how well resources lined up with other investments of national power. Across the board, we selected indicators based on their relevance to U.S. and Chinese national security, data availability, coverage and consistency.

Table 1 summarizes the indicators in the Natural Security Index. See this technical note for more detail on how the New America team calculated the Index.

Table 2 displays the key metal and mineral resources referenced throughout this report, as well as the countries that provide the largest share of the United States’ and China’s supply and the key industries that utilize each resource. For more details on each resource in Table 2 see Appendix A in the technical note.

Amber Waves of Grain: Natural Security Index for the United States

Dan Thornberg / Shutterstock

The United States is largely self-sufficient in agriculture, well-endowed with mineral and metal resources, and increasingly self-sufficient in energy. For some resources, the United States is a major world exporter, including staple crops and proteins (e.g., corn and beef). Although a small part of this resource production is on public lands, it is all done by private businesses. Despite this inherent natural security, U.S. companies also import and invest in oil, natural gas, commodity metals, agricultural products, and, increasingly, critical minerals essential to the digital age and clean energy technologies.

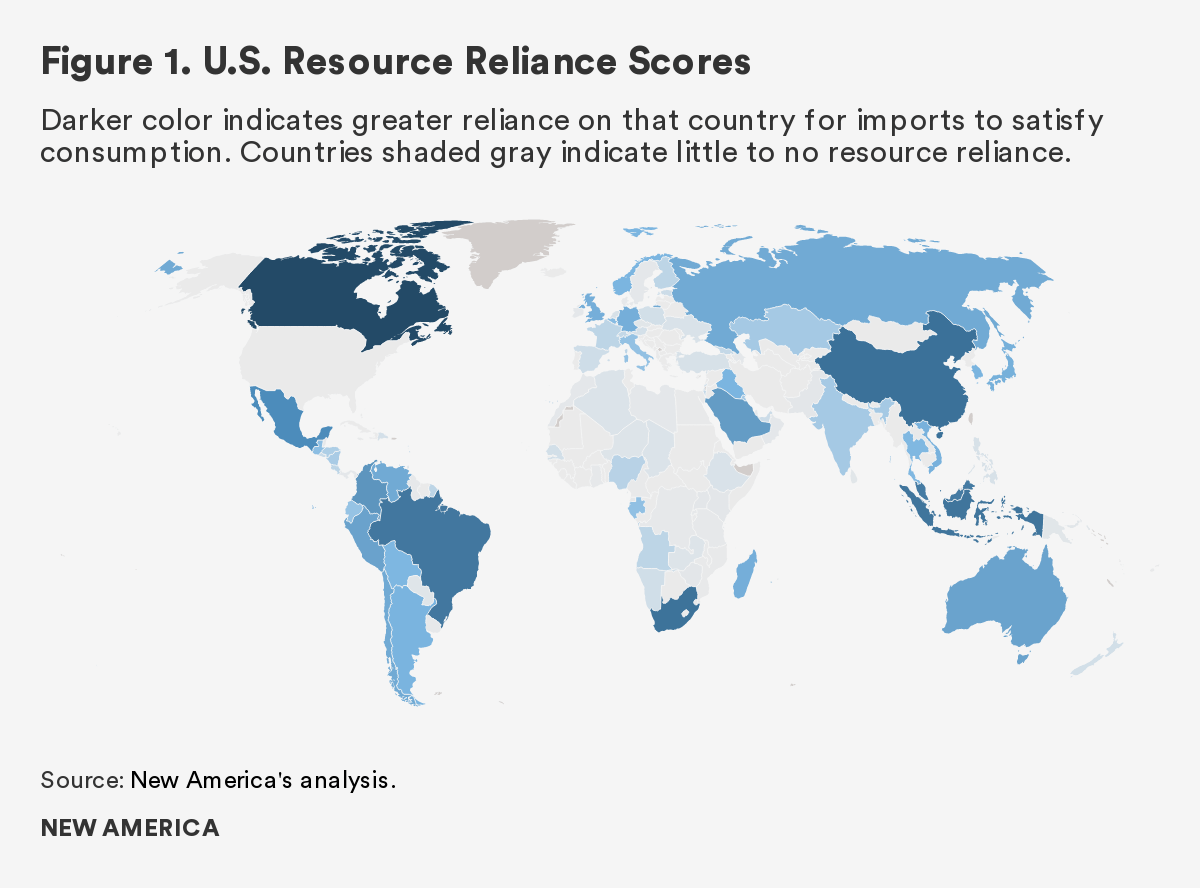

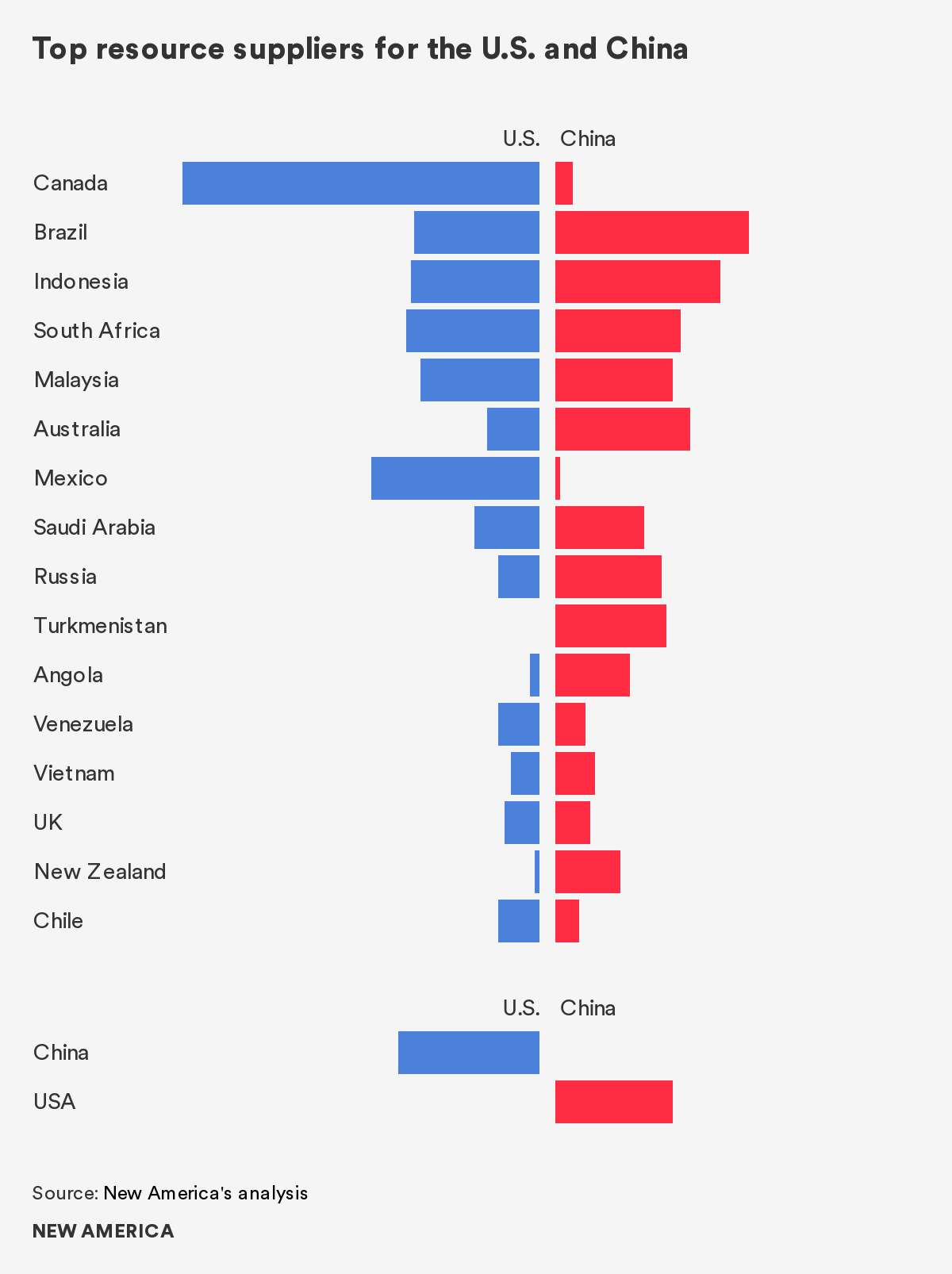

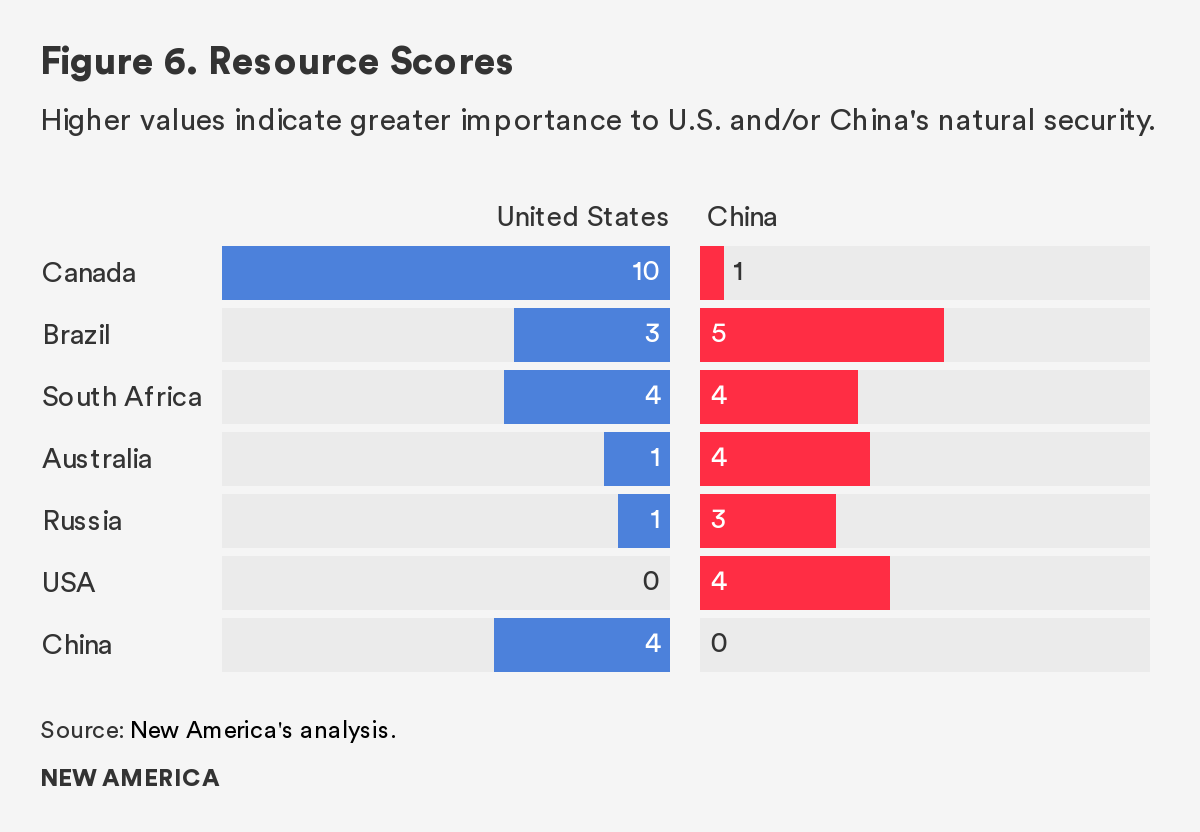

According to New America’s Natural Security Index (Figure 1), Canada is by far the most important natural security partner for the United States. In particular, Canada is the top supplier for cadmium, aluminum, nickel, zinc, lead, and imported oil, and comes in second for a handful of other resources. The United States also has considerable defense, diplomacy, economic, and cultural investments in its neighbor to the north. The importance of Canada and Mexico to the United States highlights the power (and efficiency) of proximity and the North American regional resource trading bloc.

Mexico is the next most important natural security partner, largely for sugar, commodity metals, and oil. Diplomacy, military, and cultural and economic investments are likewise high, though there are new strains in the relationship over border security and trade, and it is difficult to say the long-term effects on the relationship.

After Canada and Mexico, the United States’ most critical resource partners are South Africa, Brazil, Indonesia, and, indeed, China.

China is third in line as a U.S. resource partner. Throughout the 1990s, as China opened its economy to the world, heightened economic interdependence was a major U.S. foreign policy goal. More recently, however, the United States has identified China’s economic policy in certain areas, including critical minerals, as a strategic vulnerability. Despite labeling Russia a “great power competitor,” along with China, the United States also relies on Russia for platinum group metals (PGMs).

These interdependencies are not necessarily a strategic weakness, however. Indeed, relying on each other may not only mean a mutual economic benefit, it may also deter conflict or build confidence. Right now, the United States, Russia, and China still have a stake in each other’s success. A disproportionate dependency can be used as a weapon, however, as the United States has shown recently with tariffs on a range of Chinese imports, to which the Chinese responded with tariffs on soy. In the past, China has restricted exports of rare earth elements as a means of applying political pressure.

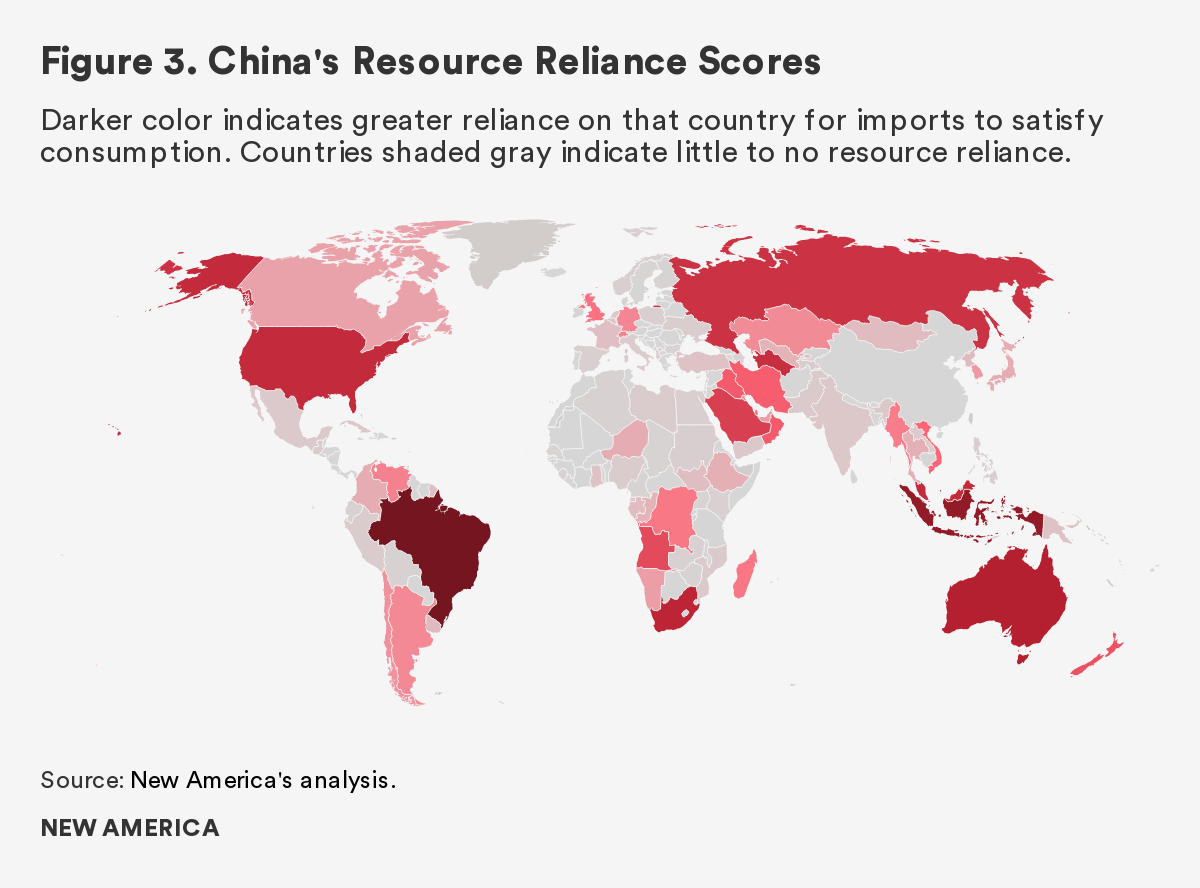

Generations to Come: Natural Security Index for China

Hung Chung Chih / Shutterstock

Despite China’s arable land, energy resources, and significant mineral wealth, its inherent natural security is insufficient to meet the needs of 1.4 billion people. Rising incomes and an economic shift to industry, emerging technologies, and services are further stressing demand for key resources.

In agriculture, while China has been self-sufficient in staple crops (such as corn, rice, and wheat), a growing middle class is changing consumption patterns. In particular, a growing demand for meat is driving up some imports, such as soy for animal feed.

China is a major producer of critical minerals, but it also relies on imports for a select few minerals, such as lithium and niobium, which are important for the country’s consumer electronics, construction, battery, and renewable energy industries. These materials are in everything from smartphones to the steel in bridge spans.

China relies on a more diversified, evenly spread range of trade partners for resources than does the United States, including countries that are resource powerhouses in global markets, such as Brazil, South Africa, and Australia. At this time, the United States also ranks highly in importance to China’s natural security, especially for agricultural commodities, and China invests in the U.S. energy sector.

The Democratic Republic of the Congo (DRC), while not a high-volume resource supplier, is a critical partner, given that China depends on the DRC for over 80 percent of a key resource: cobalt. Cobalt is important for batteries, consumer electronics, metal alloys, and medical applications.

In Brazil, Indonesia, Australia, South Africa, the United States, Saudi Arabia, and Angola, China’s resource relationships are highly correlated with military, cultural, diplomatic, and economic investments. Across all military and soft power indicators, Russia is China’s most important partner, and it is also a key supplier of energy, minerals, and metals. While proximity is important, it is not as dominant a factor as it is for the United States; for China, for example, Brazil is as important as Indonesia.

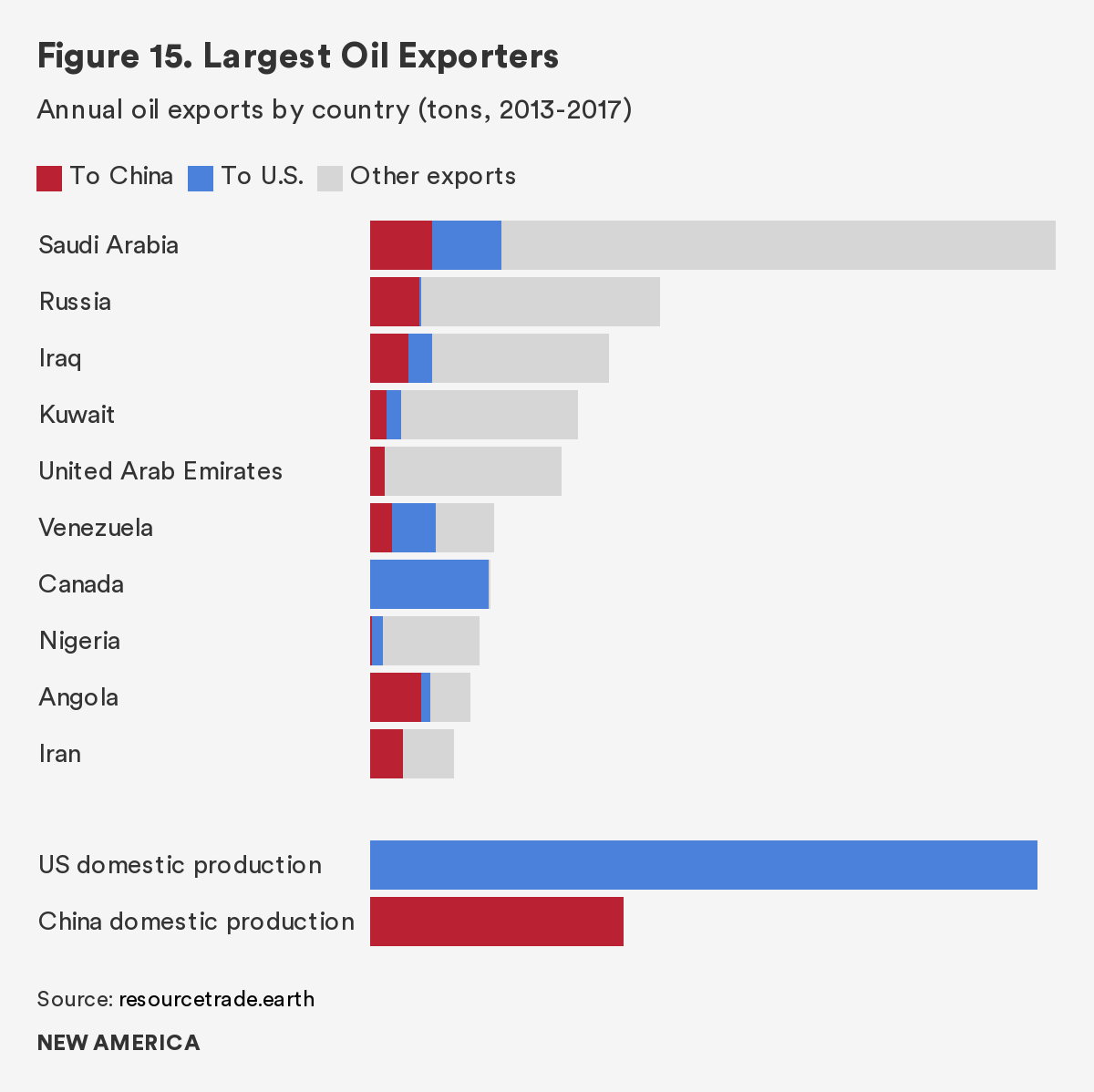

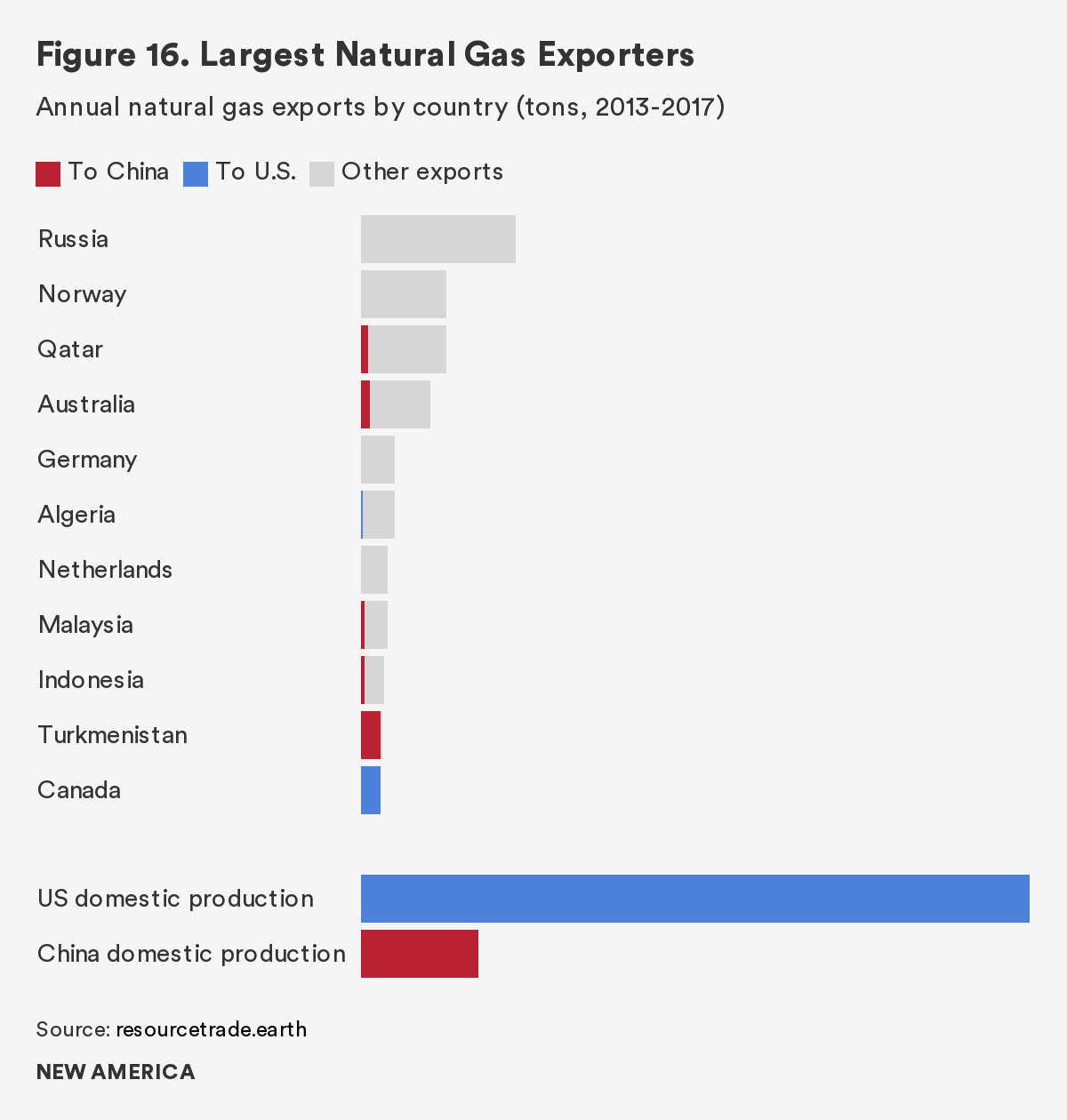

Although China is investing in renewable energy, the country remains highly dependent on fossil fuels. Domestically produced coal accounts for the majority of fossil fuel consumption, but China is import-dependent for oil and gas. In fact, China’s petroleum dependence closely resembles that of the United States a decade ago. According to our analysis of global trade from 2013-2017, China relies on imports to meet roughly 62 percent and 30 percent of its oil and natural gas needs, respectively, with Saudi Arabia, Russia, and Iran as top suppliers. All three countries are also top priorities for Chinese military, economic, diplomatic, and cultural investments.

Frame China / Shutterstock

Analysis: Natural Security and Great Power Competition

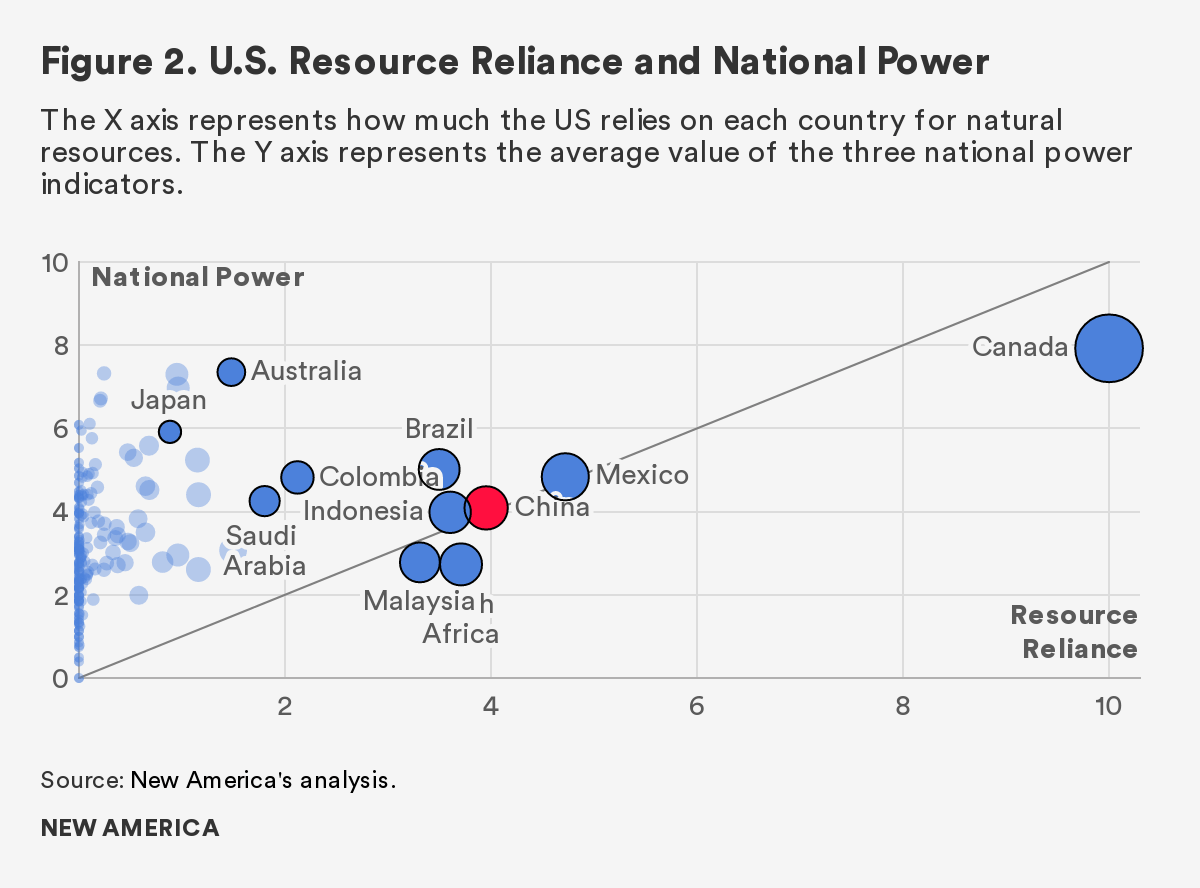

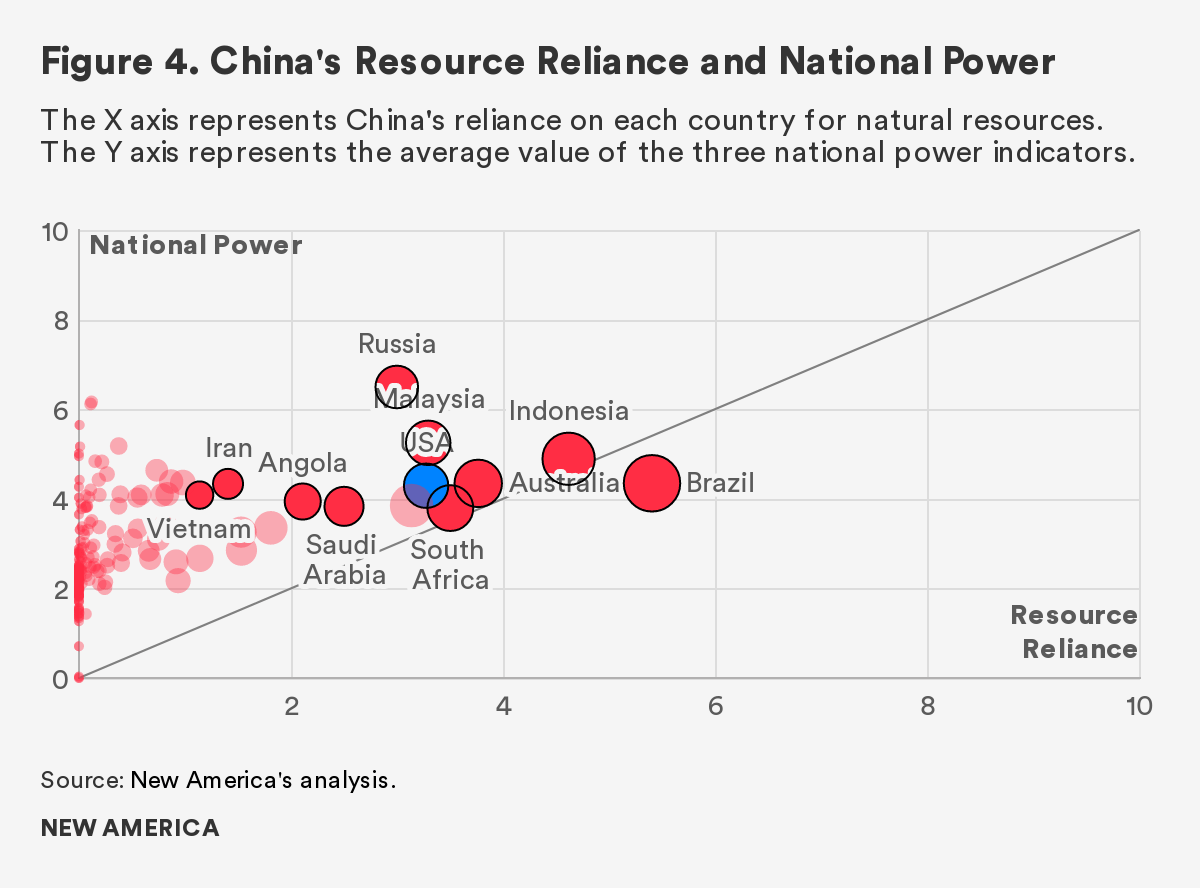

The United States and China rely on many of the same suppliers for natural resources: Brazil, South Africa, Indonesia, Malaysia, Australia, and Russia—as well as each other. Specific country profiles follow.

In general, in these overlapping countries (according to Figures 2 and 4), China invests more effort in diplomacy compared to the United States, but U.S. cultural and economic soft power outpaces China’s. The United States has more military engagement and coordination around the world than China, including with key resource partners.

China and the United States

At this time, the United States and China rely on each other for resources, and have made considerable soft power and military investments in each other (see Figures 2 and 4), as well. The United States depends on China mainly for critical minerals: China is a top supplier for antimony, bismuth, graphite, and rare earth elements. China depends on the United States mostly for agricultural products: the United States is China’s second-largest supplier of pork, poultry, and soy.

It is difficult to say if these ties will continue to the same degree, given current trade disputes and rising animosity. However, it would not be easy for either country to find a new primary trading partner for these resources. Specifically for critical minerals, the source of China’s comparative advantage is both its geology and its capacity for processing. The global demand for critical minerals is relatively new, and most current known reserves were discovered more or less by accident, as veins found in association with copper, gold, or some other commodity metal. There may be more commercial amounts of these high tech minerals buried in the Earth, including in the United States, but exploration is expensive. Even with reserves that have already been identified, financing and building a new mine takes years. Finally, the raw ore from a mine has to be crushed, heated, and bathed in chemicals, such as sulfuric acid or sodium hydroxide, in order to obtain useful minerals, and it can be difficult to permit and site such highly polluting plants.

In agriculture, pivoting to a new trade partner is not as difficult as it is for mining, in terms of the time and investment required, but a shift is not without consequences. Soy is instructive: as U.S. soy exports to China have declined in the last three years, exports from Brazil have increased, accelerating deforestation in the Amazon to make way for farmland.

Alf Ribeiro / Shutterstock

Brazil

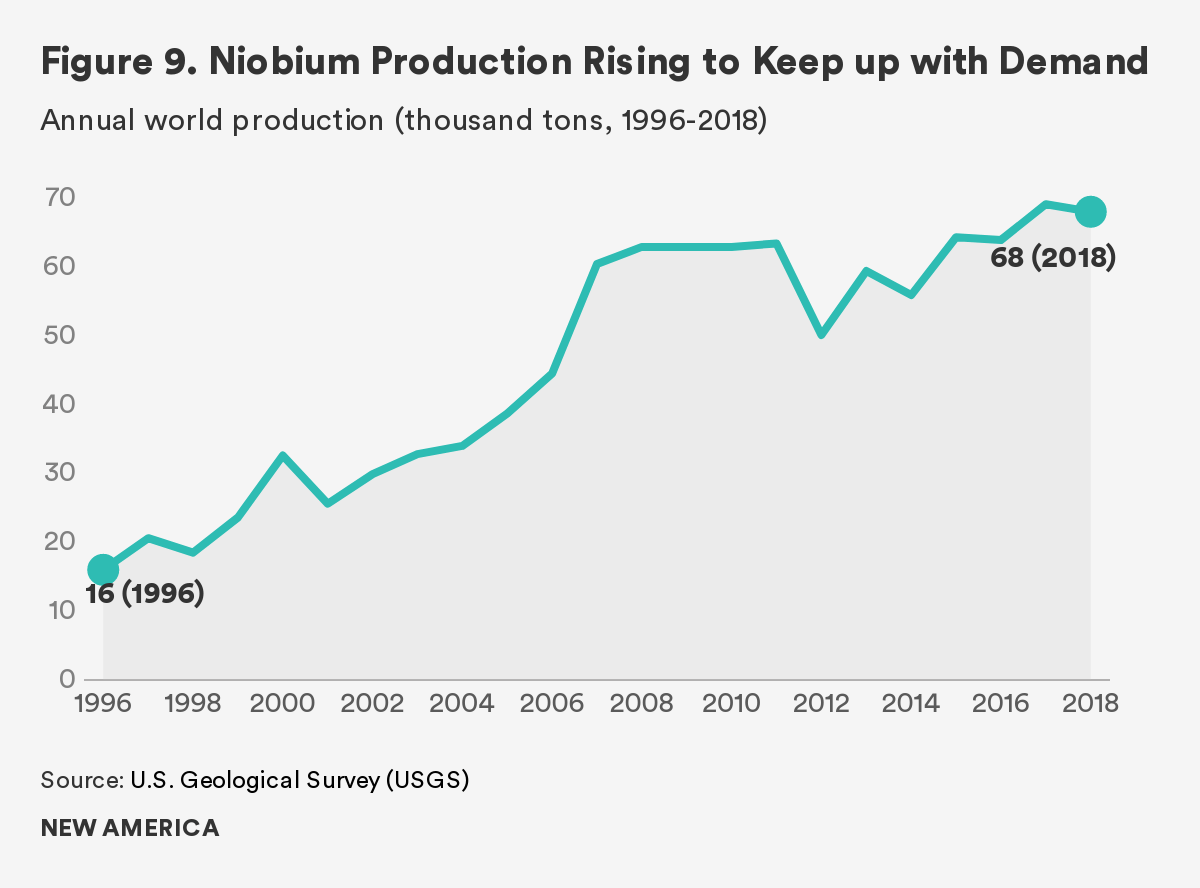

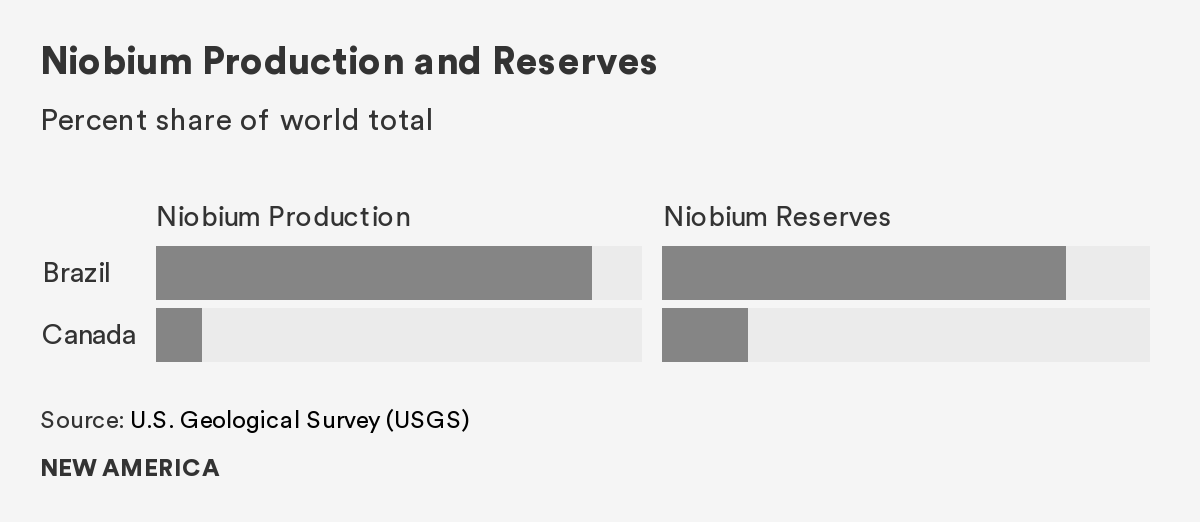

Arguably the world’s most important natural resource power (outside the United States and China), Brazil exports a range of commodities, especially minerals and agricultural products, and supplies over 75 percent of the U.S. and China’s total supply of niobium. Niobium is essential for high-tech devices such as cell phones and laptops, though most niobium in the United States and China goes to high-strength steel, a higher-volume, lower-value use. Although there are substitutes for niobium, other metals may result in degraded performance. According to our data analysis, Brazil is also a significant agricultural producer, supplying 43 percent (and growing) of China’s soy imports and 14 percent of its sugar imports. The United States produces enough soy to meet its own needs, but relies on Brazil for a quarter of its coffee supply. Both the United States and China have considerable national power investments in Brazil—diplomatic, economic and cultural, and military.

South Africa

South Africa ranks first for the United States and China in critical mineral dependence, supplying chromium, manganese, zirconium, and several platinum group metals (palladium, platinum, and rhodium) to both countries. Manganese is used in steelmaking; chromium is critical for making stainless steel for pipelines, machinery, and home appliances; and zirconium has unique properties that make it important for the nuclear industry. Platinum group metals have several characteristics that make them important to industrial economies, specifically properties that help reduce dangerous emissions from vehicle exhaust and oxidation resistance in electronics. As with Brazil, both the United States and China have a range of national investments in South Africa, with China trending more diplomatic than military.

Australia

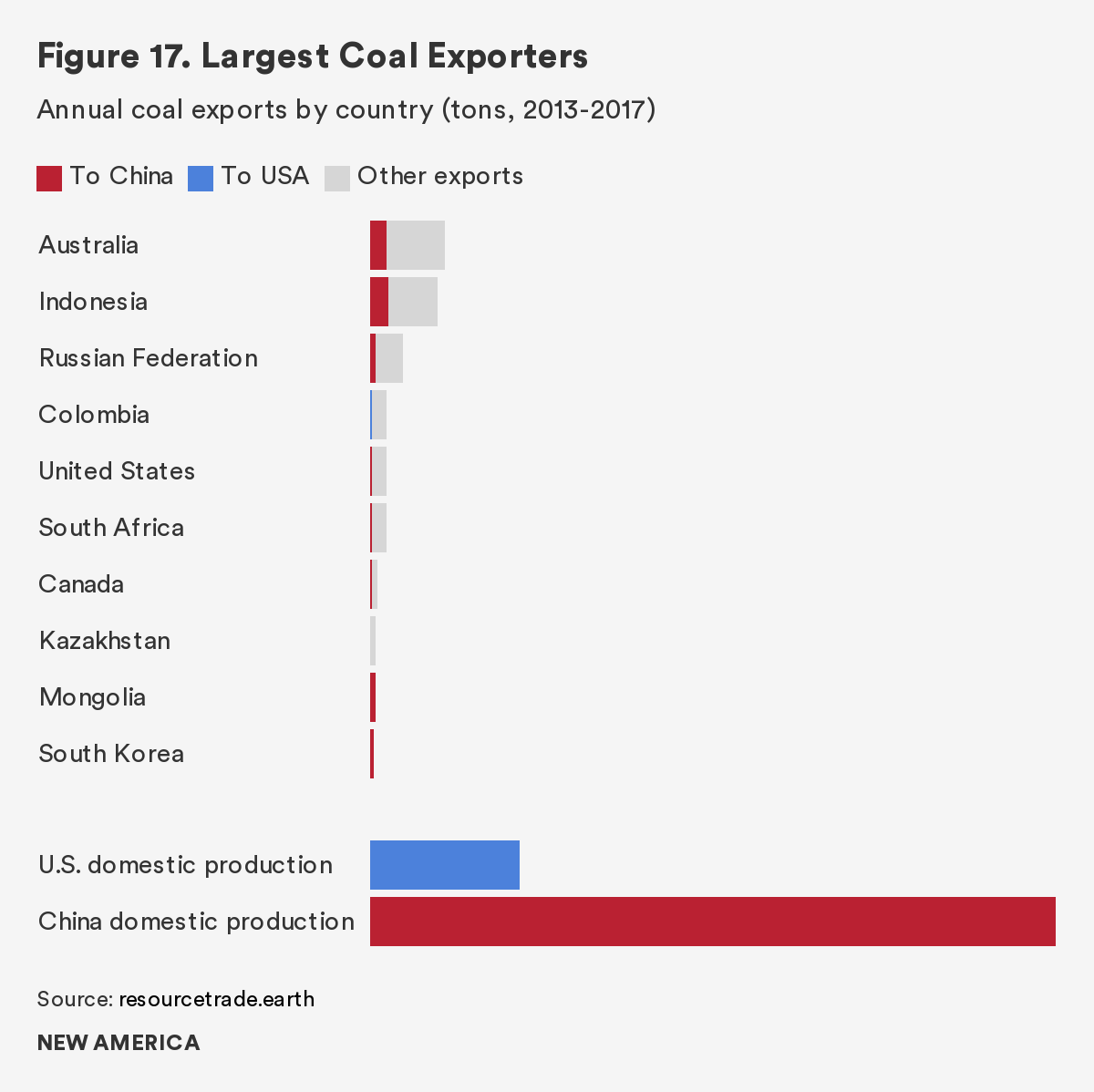

Natural security and national power indicators all suggest Australia is a key country of contention between the United States and China. Australia’s resource wealth and proximity to China make it a critical partner; Australia is China’s number one supplier of zirconium and silver, and comes in second for manganese, gold, coal, and gas. China has a range of national power investments in Australia, including military coordination, cultural engagement, and economic investment.

Australia is a top military ally for the United States, enshrined in the 1951 Australia New Zealand United States (ANZUS) treaty and the Five Eyes intelligence sharing agreement. Australian forces have fought alongside Americans in every conflict since World War I, though a recent Lowy Institute poll suggests that a younger generation of Australians may feel less beholden to that shared history. The United States also relies on Australia for a range of resources, including uranium, manganese, and cadmium, though the dependency is less concentrated than it is for China.

Lingkar Hari / Shutterstock

Indonesia

Indonesia has become an increasingly important agricultural supplier globally in recent years due to the world’s embrace of palm oil. Indonesia also exports fossil fuels and coffee to China, and tin to the United States. The country is of high strategic importance due to its central location in the Pacific astride the Malacca Strait, a critical shipping corridor between the South China Sea and Indian Ocean. Indonesia has ties to both the United States and China, and ranks relatively high in military coordination with China.

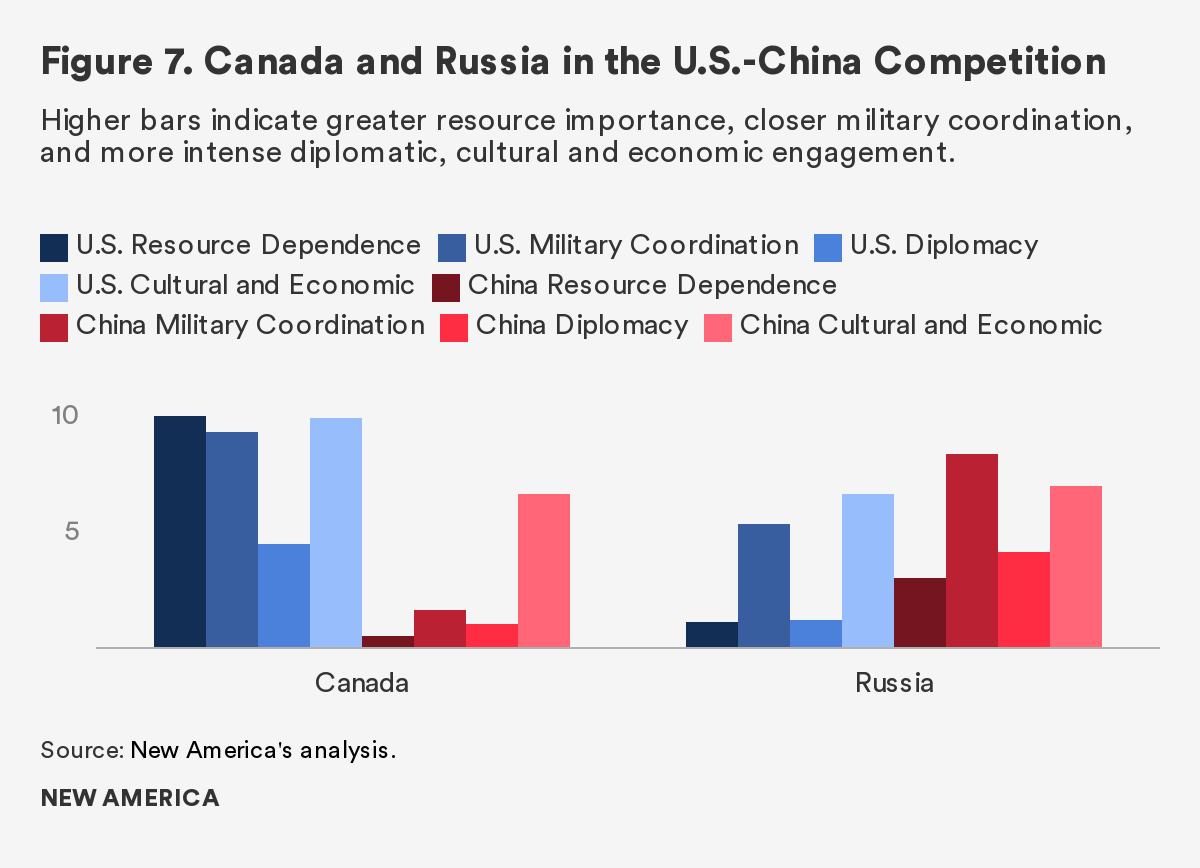

Canada and Russia

The U.S.-Canada and China-Russia relationships are analogous; these are regional partnerships that cut across indicators, from resources to military to economic to cultural. At the same time, the United States relies on Russia for resources such as palladium and rhodium, and has cultural and economic engagement with Russia that rivals that of China. China likewise looks to Canada for cadmium and niobium, with about the same degree of cultural and economic engagement that the United States has with Russia.

Spotlight on Highly Contested Resources

Photo by Michael Robinson Chavez/The Washington Post via Getty Images

Cobalt and Lithium

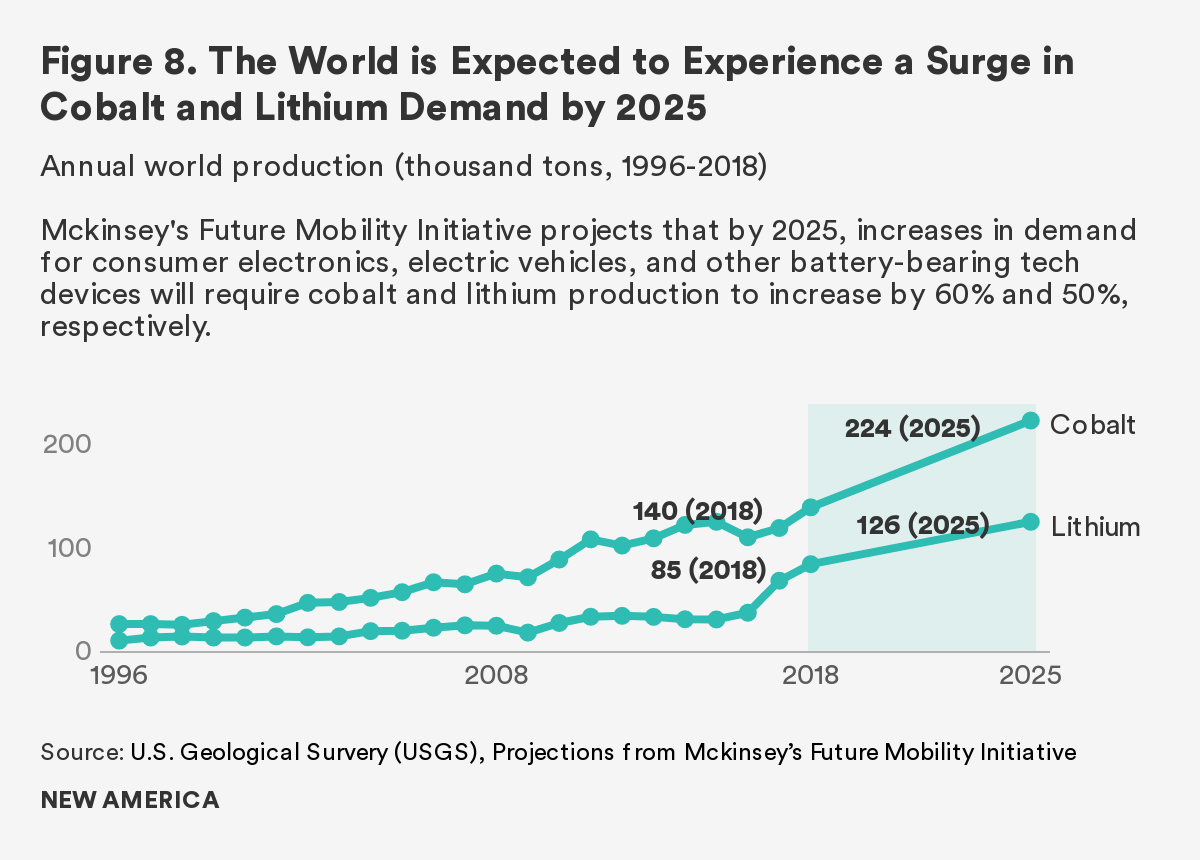

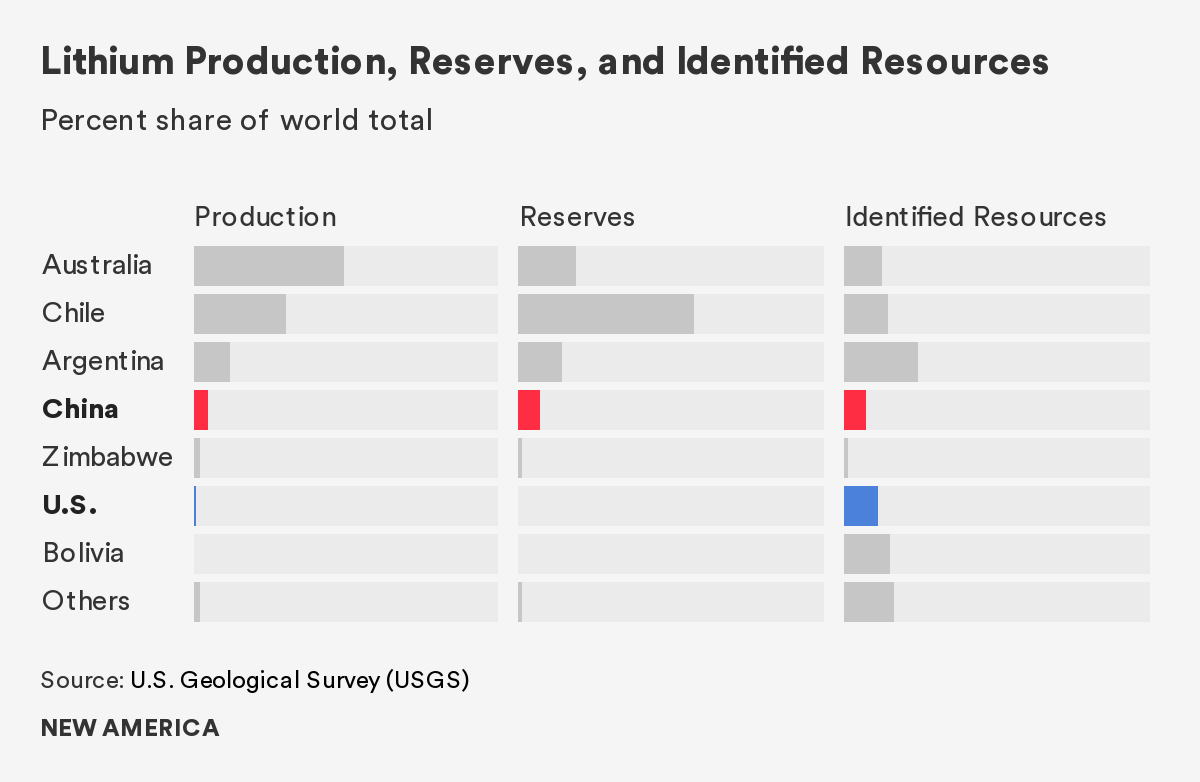

Lithium and cobalt have a wide range of industrial and commercial uses, with batteries for portable electronics and electric vehicles driving increased demand in recent years. In the coming years, the electric vehicle (EV) industry, in particular, will continue to push demand for both minerals. According to McKinsey’s Future Mobility Initiative, global EV production is expected to reach as high as 13 to 18 million units by 2025, a 200 percent increase from 2018 levels. Based on the U.S. Geological Survey’s most recent data for global production, that means lithium production will have to increase 50 percent and cobalt by 60 percent by the year 2025 to meet demand. China’s 2017 EV sales were up 53 percent from 2016, and the nation’s pollution-reduction policies aim to continue this trend. For perspective on how this may influence demand, a typical smartphone contains 5 to 20 grams of cobalt, while an EV needs between 4 to 30 kilograms. China and the United States are likely to increase imports of cobalt and lithium to meet this escalating demand. The United States does produce some lithium at home, though the exact amount is proprietary, and there’s modest potential for growth with additional, untapped reserves. China produces some lithium at home, as well, and could potentially be producing more, given the estimated size of its reserves. Nonetheless, both countries import more than 50 percent of the lithium they currently consume, mostly from Argentina and Chile, where China has significant investments in lithium mines.

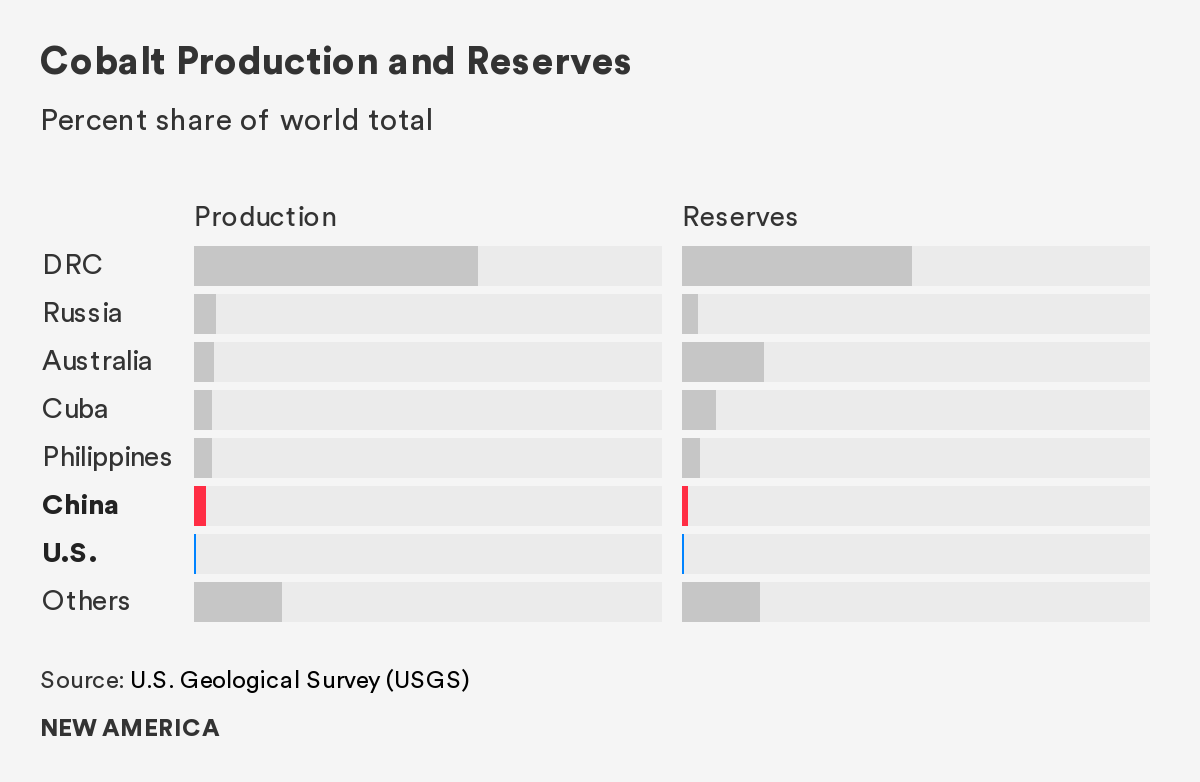

As for cobalt, 82 percent of China’s total supply comes from the Democratic Republic of the Congo, the largest producer of cobalt ore. Yet China is increasingly integrating itself as a critical step in the cobalt supply chain, investing in cobalt mining in the DRC and processing domestically.1 China now possesses over half of the world’s cobalt refinery capacity. The United States primarily imports refined cobalt, and looks to Norway (14 percent), Japan (9 percent), and China (9 percent) for its supply (note that the cobalt did not originate in these countries).

Niobium

Niobium’s primary use is in producing stronger, less corrosive, and more heat-resistant steel for everything from jet engines and rocket subassemblies to superconducting magnets for MRI machines and smartphones. Niobium production is highly concentrated in Brazil, with Canada being the only other significant global producer. Geologically, niobium is fairly rare, especially in economically recoverable concentrations, and Brazil will continue to dominate world supply. Both China and the United States import niobium for electronics and related technologies, as well as for steel alloys.

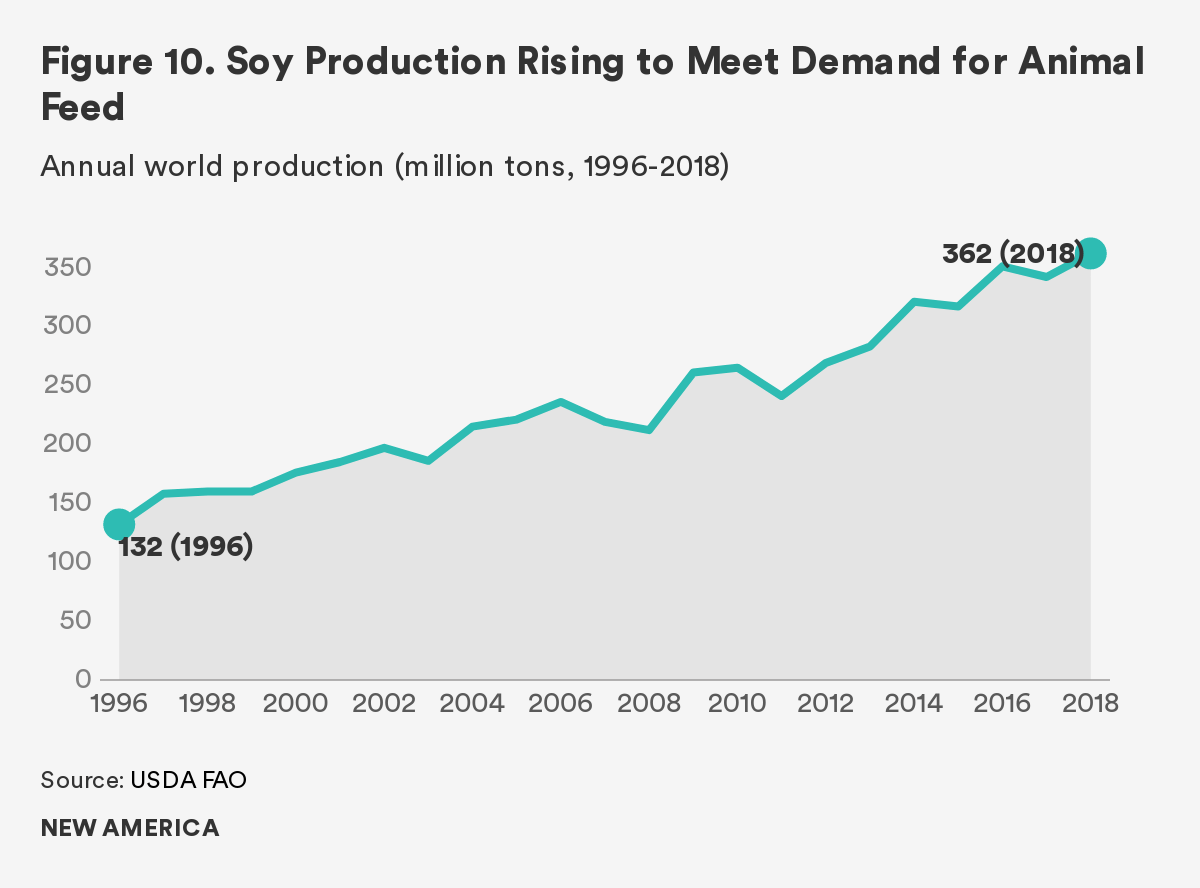

Soy

The United States is the world’s largest soy producer, followed by Brazil and Argentina. China, the world’s largest consumer, domestically meets 13 percent of demand, and imports the rest from the United States, Brazil, and Argentina.

While the soybean is native to China and remains a cornerstone of the Chinese diet, it is the rising demand for meat among China’s growing middle class that is pushing up the demand for soy as animal feed, beyond what the domestic supply can meet.

Given China’s political emphasis on agricultural self-sufficiency, its dependence on imports for a native crop is striking. With only 9 percent of the world’s arable land to feed 21 percent of the global population, it would be a challenge for China to increase domestic cultivation by much.

The United States owes its status as a soy powerhouse to China. While U.S. soy production increased steadily in the latter half of the twentieth century, it skyrocketed only when Chinese demand took off in the mid-1990s.

The high-volume, high-value international soy market is vulnerable to disruption, including from weather. In 2010, global soy production dipped when Canada experienced a wet summer, while Brazil and Argentina suffered a drought; the price of soy increased nearly 50 percent. Climate change will increase the frequency and severity of such extreme weather, so erratic changes in the price of agricultural goods on international markets may become more common.

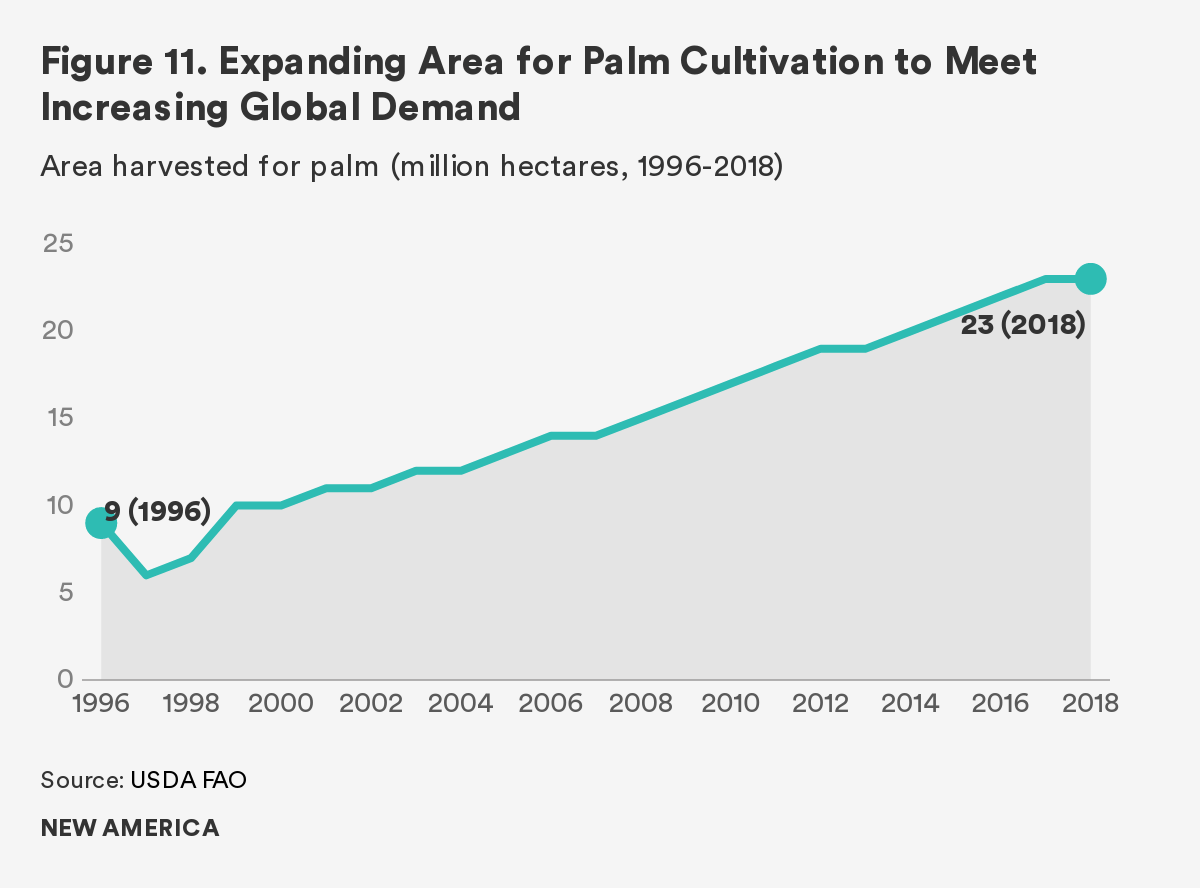

Palm Oil

Palm oil consumption is rapidly growing. It now accounts for a third of vegetable oil used globally, replacing hydrogenated vegetable oil and butter in processed food, and is used in a wide variety of other products, such as cosmetics and shampoos.2 Palm oil-derived biofuel consumption has also increased as governments race to displace greenhouse gas emissions and issue biodiesel use mandates. Palm oil production is heavily concentrated, with Indonesia and Malaysia as the most prominent global suppliers. As neither America nor China produce palm, both countries rely overwhelmingly on Indonesia and Malaysia to fulfill demand.

Increasing the land devoted to palm oil production has consequences, however. Palm grows best in the same climate as tropical forests. Since 2000, the land area devoted to producing palm has increased by 125 percent, which has resulted in a pushback from local communities and international organizations due to associated deforestation, air pollution from land-clearing fires, and resulting greenhouse gas emissions. Worryingly, other countries, including Brazil, are looking to increase palm production, putting tropical ecosystems at risk.

Citations

- Andrew L. Gulley et al., “China’s Domestic and Foreign Influence in the Global Cobalt Supply Chain,” Resources Policy 62 [August 2019], pp. 317-323.

- Garrett McDonald and Arif Rahmanulloh, Indonesia Oilseeds and Products Annual 2019, USDA Foreign Agricultural Service [March 15, 2019].

Looking Ahead: How Climate Change Will Affect Natural Security

Shutterstock

Over the coming years, the changing climate will shape natural security in two important ways. First, rising global temperatures will affect resource availability. The changes will shift agricultural productivity poleward, increasing the length of growing seasons in cold climates, while high heat wilts crops closer to the equator. Second, as the world transitions from fossil fuels to renewable energy sources, the relative importance of resources will shift. There will also be effects on water—both freshwater and oceans—which we considered but did not fully examine for this report.

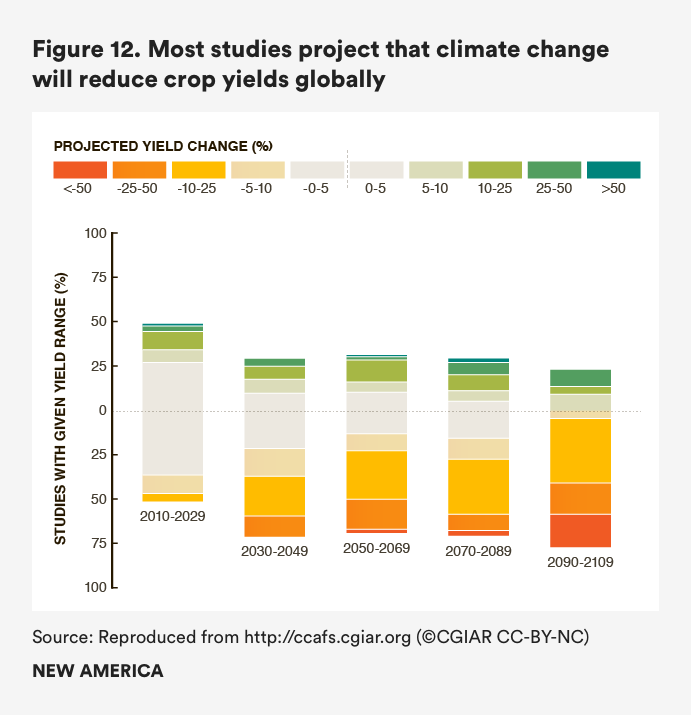

Although there is considerable uncertainty in crop yield projections, the majority of models agree that global crop yields will decline in the coming decades. Moreover, increasing global food demand will likely require development of new agricultural land and substantially increased international trade from water-abundant areas to water-scarce regions. Greater variation in weather may increase risk of drought and water stress. In the breadbaskets of the U.S. heartland and northern China, groundwater tables are already falling.

Source: CGIAR (CC-BY-NC)

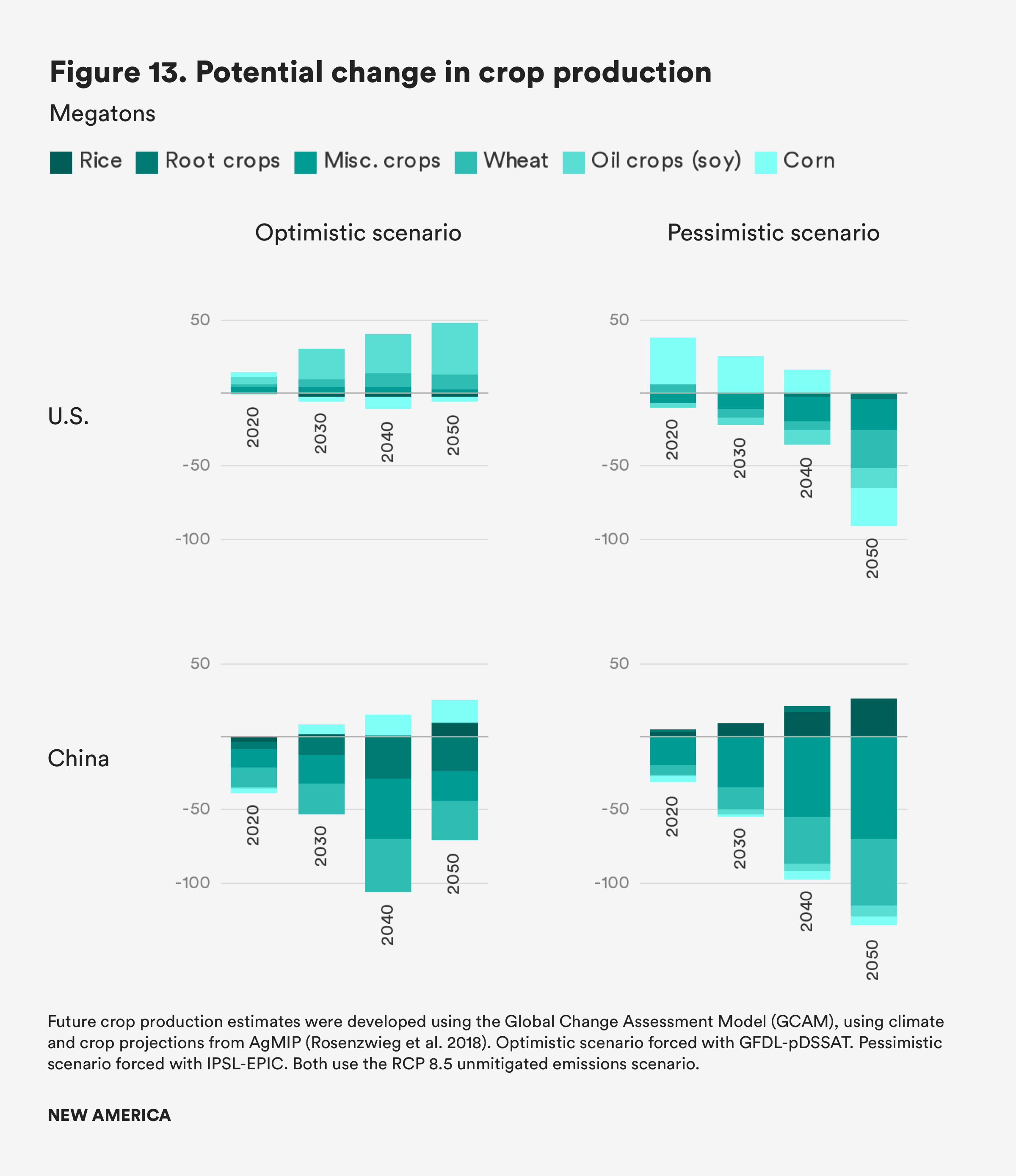

Together with the Joint Global Change Research Institute, we evaluated two global agricultural trade scenarios for 2050 and 2100 using the Global Change Assessment Model: an optimistic scenario where the net effects of climate change lead to short-term increases in productivity in the northern United States and China; and a pessimistic scenario where climate change leads to agricultural losses in both countries.1 Importantly, neither of these scenarios accounts for the possibility of increased competition for water or groundwater depletion, which may limit the availability of water for irrigated agriculture. The models also do not incorporate the effects of extreme events, such as floods, droughts, and wildfires, on agricultural productivity.

For the United States, the speed and magnitude of climate impacts will matter. In the optimistic scenario, agriculture in the south and west may suffer, but with few competing pressures for land, the United States can stay a major agricultural producer. If climate change impacts are more intense and water and heat stress put greater limits on crop productivity, U.S. farmers may no longer be able to produce a large export surplus. In both scenarios, Russia and Canada are likely to rise as important exporters.

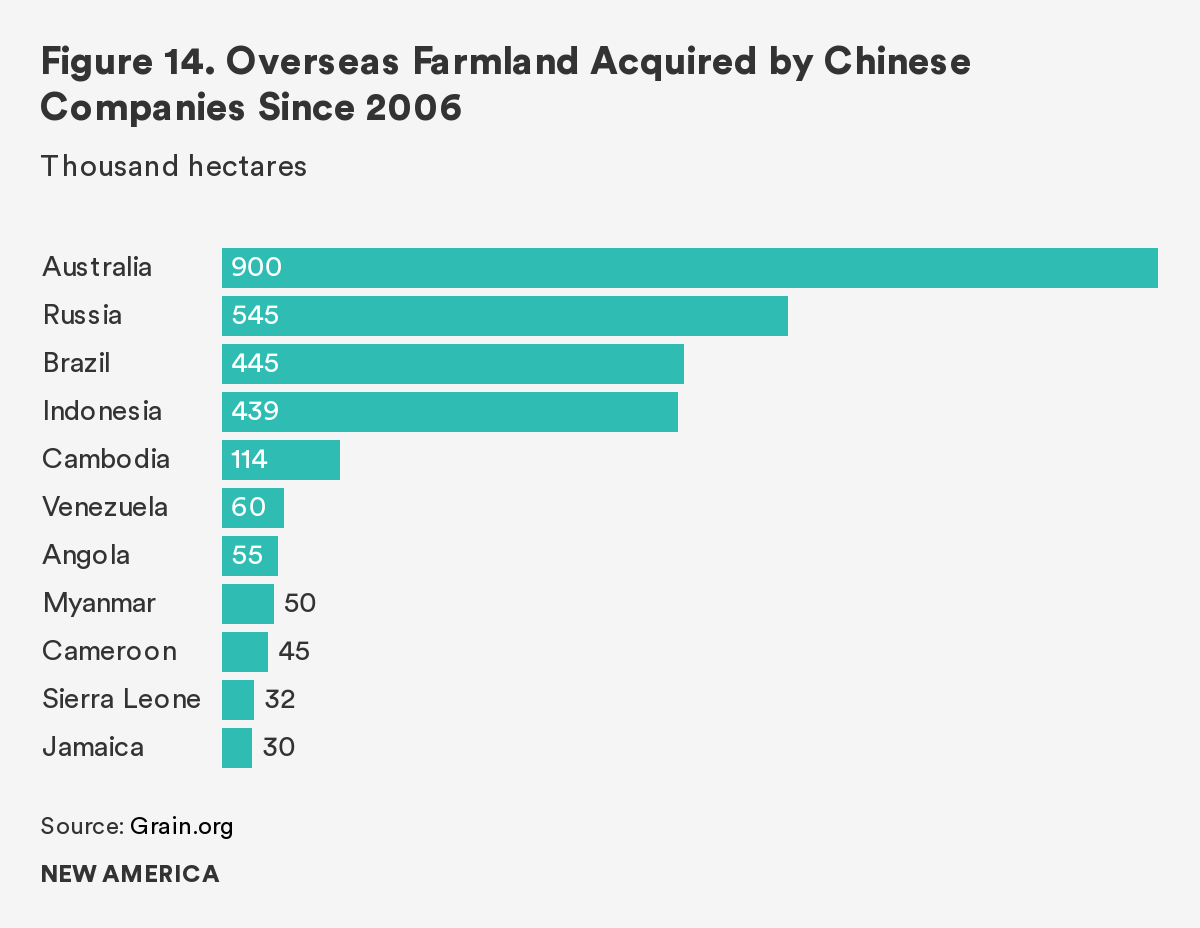

For China, the economics of land and trade are likely to mean greater imports under both scenarios, but with more urgency in the pessimistic scenario. While China currently grows enough corn, wheat, and rice to satisfy domestic consumption, climate change is likely to change this, especially for corn and wheat. Already China is increasingly looking outward for agriculture, as Chinese companies invest in purchasing agricultural land around the world. Soy producing giants such as Brazil and Argentina are likely to become more important suppliers in the short term as demand increases, especially if tariffs hamper U.S.-China trade.

The effects of these changes are likely to be felt across the world. Global agricultural markets are highly integrated, and droughts or other extreme weather events in major breadbaskets can create food price spikes around the world.

In addition to the effects on agriculture, climate change means a transition from traditional fossil fuel energy sources to renewables, though the pace of this transition is still unclear. In many places, wind and solar energy are already cost-competitive with coal-fired power plants. Automakers around the world are investing heavily in electric vehicles. Nonetheless, global greenhouse gas emissions rose in 2018.

For the United States, a shift away from fossil fuels may lead to a strategic shift away from major oil-producing countries, such as Saudi Arabia, toward suppliers of critical minerals. Domestic U.S. oil production has increased substantially over the past several decades, and the United States is projected to become a net oil exporter by 2020 for the first time since 1948. Depending on the speed at which the United States adopts climate policy, a shift from gasoline to electric vehicles will further decrease oil demand. This will affect U.S. producing regions domestically, in terms of tax revenue and jobs, which is likely to refract through national politics.

A shift to clean energy technologies will also require a significant increase in critical mineral consumption. Current battery technology requires lithium and cobalt, for example, while rare earths are essential to magnets in electric motors and generators. The United States depends on China for many of these resources. The United States could produce some of these minerals at home, though not competitively in current markets. In any case, ramping up domestic mining and refining of these materials would require considerable investment, permitting, and environmental consequences, and it may take years for production to come online.

A shift to clean energy technologies will require a significant increase in critical mineral consumption.

China is much less energy secure in terms of fossil fuels, although the country has substantial coal reserves and is seeking to diversify dependence on imported oil and cut greenhouse gas emissions through increased natural gas imports. China likewise is investing in renewable energy and electric vehicles, which will require increased consumption of both domestic and imported critical minerals, such as rare earth elements and cobalt. In addition to the threat of climate change, China faces domestic pressure to move away from coal due to air pollution concerns.

Energy security has long had geopolitical resonance. China’s relationships with major fossil fuel producers, such as Russia, Saudi Arabia, and Iran, have become increasingly important, with implications for the historically close ties between the United States and Saudi Arabia and the adversarial ones with Iran and Russia. In the future, as the two largest economies seek to gain a competitive edge in renewable energy technology, that will increasingly drive competition over critical mineral resources and major producing countries, such as Australia, Brazil, Chile, South Africa, and the Democratic Republic of the Congo.

The future of the world’s natural resource landscape will in large part depend on the fate of the U.S.-China relationship. Imports to the United States and China account for one quarter of the world’s trade in resources. If the two countries seek to disentangle their mutual dependence, it will result in major shifts to global supply chains and significant impacts on domestic industries. Meanwhile, new areas of resource competition are growing, and technological and climate change mean that the twentieth century’s understanding of resource security will no longer be valid. China is seeking to strengthen its natural security, investing in countries across the world. The United States’ response to this shifting landscape and the new competitive space will shape its security and prosperity in the century to come. Climate change will increasingly be a strategic driver when it comes to natural security, something China appears to be positioning for, with its diversified trade, investment, and national engagement strategy. The United States, on the other hand, appears to have no deliberate strategy when it comes to ensuring natural security in a changing climate.

Citations

- Both the optimistic and pessimistic scenarios assume business-as-usual increases in global greenhouse gas emissions (scenario RCP8.5), but use different models and assumptions in estimating climate change effects and impacts on crop productivity. The optimistic scenario uses GFDL for climate forcing and the pDSSAT crop model; the pessimistic scenario uses IPSL for climate forcing and the EPIC crop model. These scenarios do not account for increased probability of extreme weather events that may adversely impact agriculture.

More About the Authors

Francis Gassert

Sharon Burke