Table of Contents

- Checklist

- Introduction

- Household Economy

- Community Resilience

- A Pandemic of Racism

- Election Integrity

- Healthcare Surge Capacity

- Supply Chain Management

- Universal Access to Digital Services

- Banking and Payment Systems

- Economic Resilience

- Future of Work

- Epidemiological Readiness

- Porous Lines of Defense

- Institutions

- Policy Considerations

Household Economy

What began as a medical and epidemiological event with the spread of COVID-19 in the United States rapidly bled into a household economy and personal financial crisis. The pandemic merely revealed what Americans already knew: far too many people in the country are living paycheck to paycheck. Millions are barely able to make ends meet, struggling to grasp the stability that Americans enjoyed one generation ago but seems fleeting today.

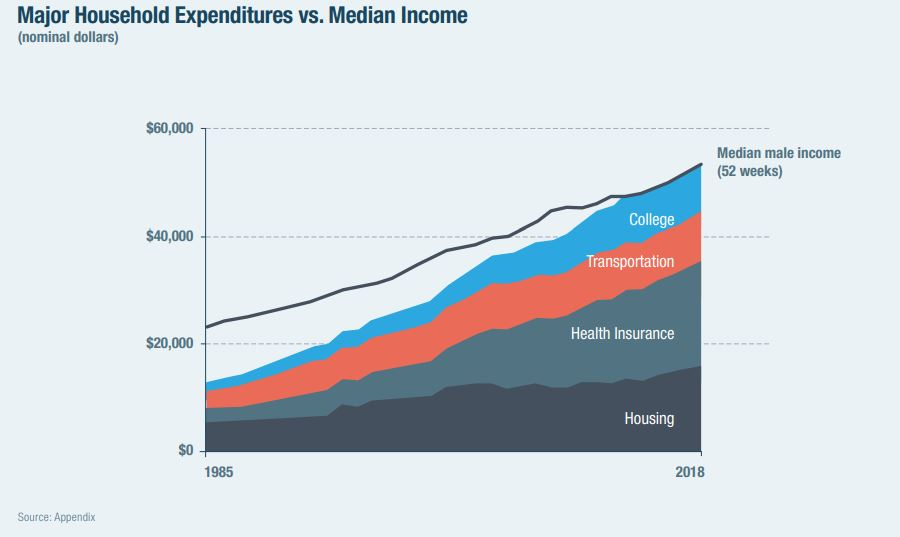

In a recent study that created an index to track the cost of thriving, researchers found that the middle class has to work a daunting 66 weeks a year for women and 53 for men with median household income—out of a 52-week work year—to provide for basic overhead, healthcare protection and costs of living. Thirty-five years ago, these same basic benefits required between 30 and 45 weeks of work, at which point the remainder of earnings could be deployed to savings (a key ingredient in economic resilience), education, real estate, and time off.

What the risk and resilience community refer to as liquid asset poverty, or simply cash poor, is a harsh reality for far too many Americans. According to a survey by the Federal Reserve, 40 percent of the population pre-pandemic could not afford a $400 financial setback without tapping credit. Some are often dismissive of credit indebtedness in the United States as a sign of people’s spendthrift, materialistic tendencies, as hordes of people trample over each other on Black Friday. The sum of these consumption patterns produces an eye-watering $14 trillion in consumer debt. The real debt burden under which millions of Americans labor is the $1.5 trillion of student debt, which was once an economic down payment their forebears could make for social mobility and economic security. Neither social mobility nor economic security were guaranteed before the pandemic; they are further imperiled now. At root, restarting the economic mobility engine in the United States requires the creation of a vibrant middle class and a business operating model where companies can compete in the world market, while advancing standards of living at home.

The pathways to the middle class seem blocked at every turn or the tollbooth fee at each off ramp to white picket fences, a house, dog, decent employment, and retirement savings seems to be cost-prohibitive for far too many people. In an environment where the labor force participation rate has been falling since 2000, a global health threat as serious as COVID-19 was liable to push millions of people over the financial brink. In just three months since the crisis began, one in four American workers have filed for unemployment protection. In order to remedy this, the U.S. Department of the Treasury’s proposed solution was the unprecedented use of direct payments to everyone in the United States of $1,200, in addition to other measures under the Coronavirus Aid, Relief, and Economic Security Act (CARES Act) to shore up the economy beginning at the household level.

These extraordinary measures put a spotlight on basic social security levels, healthcare access and unemployment benefits for all sectors of the economy. In an incredible volte-face, the once vulnerable gig economic freelancing side hustlers for delivery and livery platforms, had more personal resilience for a short time than other sectors of the employment spectrum. Hard hit sectors, including travel, hospitality, restaurants, and in-person retail, collectively laid off 40 million workers in the first ten weeks of the crisis. In all, jobless claims in the United States rose to 26 percent of the workforce, making up the largest number of unemployed people as a share of the U.S. population since the Great Depression. Indeed, we can liken the global economic consequences of the pandemic to a “Great Correction,” as the societal costs of systemic income inequality, eroding competitiveness, and social mobility, along with a tattered safety net, are tallied.

Not only did the pandemic shatter the longest bull run on Wall Street lasting more than 132 months, it hurt Main Street with equal force, grinding the United States and global economy to a halt as social distancing and strict quarantine measures took effect. The strict economic definition of a recession is two consecutive quarters of no growth. Two consecutive quarters of no economic activity at all, a veritable flatlining of the U.S. economy, prompted a rare moment of bi-partisanship in Washington as the CARES Act was passed, along with further stimulus of $484 billion for small businesses with the expansion of the Payroll Protection Program (PPP). This Act provides relief across a range of areas, in all totaling more than $2.4 trillion. Borrowing from the insurance principles of the law of large numbers and indemnification, where insureds are made whole after a loss, recuperating this investment, which will forestall many retirements, educational, personal, and professional aspirations, will require strategic long-range thinking.

To begin with, we must reconsider what levels of standardized healthcare, unemployment, and paid medical leave options are made available to every U.S. citizen. Having nearly 29 million people who were uninsured, notwithstanding historically low unemployment and under-employment numbers, meant that the pandemic lockdown did not have to push very hard or for very long against the American household and businesses before they were pushed to the brink. Indeed, this explains the false choice millions of people faced in the United States and around the world between adhering to public health advice on self-isolation and social distancing, while bearing the risk of financial ruin because of the absence of paid medical leave policies either at the national or individual company level.1 Like all insurance structures, it is prudent to pre-fund expected losses in the future thus creating a financial pool to draw down, rather than funding these costs ad hoc or not funding them at all.

While improvements in household and personal economy depend on a range of variables, including U.S. economic competitiveness, minimum wage and protection standards, among others, the pandemic revealed just how vulnerable we are as a society due to the fleeting American dream.

Citations

- To learn more about this work at New America, see the Better Life Lab’s work on paid family and medical leave, source