Table of Contents

- Checklist

- Introduction

- Household Economy

- Community Resilience

- A Pandemic of Racism

- Election Integrity

- Healthcare Surge Capacity

- Supply Chain Management

- Universal Access to Digital Services

- Banking and Payment Systems

- Economic Resilience

- Future of Work

- Epidemiological Readiness

- Porous Lines of Defense

- Institutions

- Policy Considerations

Banking and Payment Systems

Banking and payment systems are vitally important to creating a competitive economy. The freer and the broader the access the better, as basic banking services and the ability to freely spend, send, save, and secure money are in many ways the arterial system of a modern economy.

Indeed, as bipartisan economic stimulus bills and economic recovery efforts to the tune of $5.5 trillion so far have been deployed to counter the deleterious economic effects of the pandemic, the country’s banking and payment networks were the conveyors of this economic relief. And yet, certain challenges have emerged that underscore the fundamental vulnerability of financial systems that do not speak to one another in terms of interoperability and are hard to mobilize quickly when the first come first serve lines of businesses formed to receive payroll protection support.

Much of this funding, particularly the early rounds, went to larger firms with already established banking relationships and credit histories, whereas reaching the more vulnerable intended beneficiaries of this support, namely small- to medium-sized businesses (SMEs) that are in many ways the jobs and economic engines of the U.S. economy employing more than 58.9 million people before the pandemic struck, was more challenging—they were hard to serve in part because they were hard to find. The net result was that over $1 billion of potentially forgivable Paycheck Protection Program (PPP) loans went to publicly traded companies. In some cases, following public and reputational pressure, many large firms who exploited loopholes in these programs ended up returning the money.

The maladministration of economic and direct relief to an entire country, a complicated matter in normal times, for example in processing tax filings and returns, would be all the more complicated by the need for speed and precision to stave off economic crisis. The reality that America’s banking and payment systems do not speak to each other and that the neediest of people and small businesses are hard to find in this system or were either unbanked or underbanked was a precondition before the pandemic that the crisis only made worse.

In order to effectively target stimulus to prop up the faltering economy as the effect of the lockdown functionally paralyzed most commerce, policymakers resorted to “blunt force” and analog methods. This included mailing $1,200 stimulus checks to 130 million Americans, a process that could take as long as 5 months from initial pledges to actual physical checks arriving. Others received comparatively faster direct deposits as the principal methods of reaching individual households. If you were not in the financial system before the pandemic, neither of these methods of direct relief supported you very well.1

In all, 24 million American households were considered unbanked or underbanked before the crisis. Even in “normal” times, these people must often turn to usurious and predatory solutions for alternative banking options. These include payday loans to bridge the check-to-check float that is a confounding reality for far too many U.S. households barely able to get by before the crisis and now pushed over the edge.

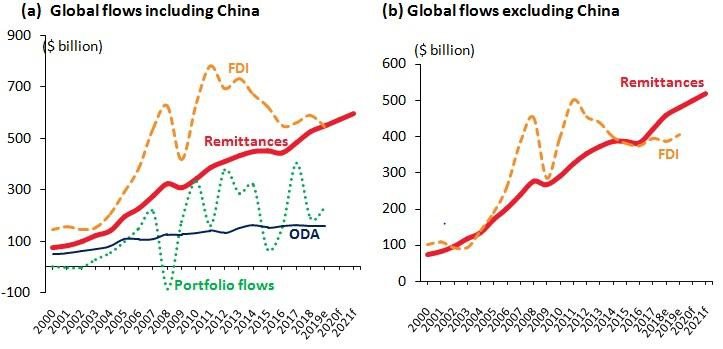

From payday lending to tax refund loans, to the over-reliance on credit with disproportionately high interest rates, often pushing 400 percent APR or higher on average, low-income families and those on the margin of the formal economy, including small businesses, were the hardest to reach and the hardest hit. This much is true for the more than 44 million people who make up America’s diaspora population coming from all over the world to power various aspects of the U.S. economy. For many of these people, as with the more than 272 million economic migrants around the world who send remittances to their loved ones in their home countries, the lack of low-cost, non-physical payment options is a clear vulnerability.

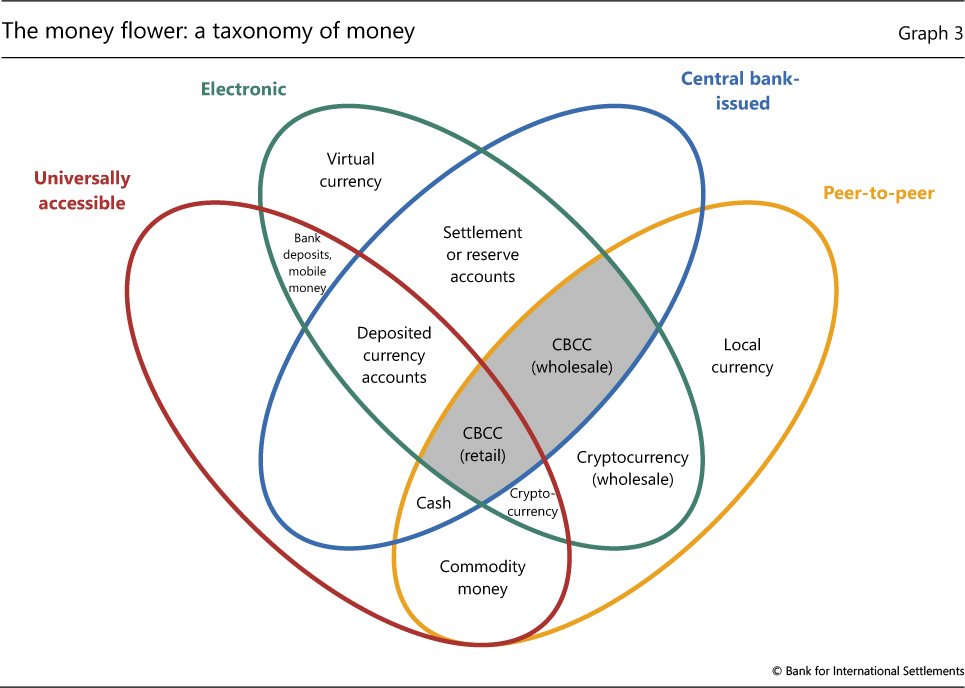

Indeed, one of the challenges amplifying financial marginalization is that we now have to factor digital and technological inequality into assessing economic marginalization. This is true as physical cash, already on the decline around the world and certainly in the United States with the rise of cashless alternatives from retail payment endpoints to phone-based nearfield computing options. The spread of COVID-19 literally gave new meaning to money laundering, as countries resorted to physically washing their national currencies or advising against their use as a potential conveyor of the disease. The net result is an increasingly louder call for digitization of payments and currencies, including a growing wave of central banks exploring ways of adding central bank digital currencies (CBDCs) to their national money in circulation.

Digital numismatists have been advocating for the role cryptocurrencies and blockchain technology can play not only in democratizing access to the financial system, but in creating a multidirectional, user-controlled payment landscape. Indeed, the struggles and the amount of time needed to execute direct relief, let alone being able to target it to those in greatest need, certainly speaks to the limitations of having a one-sided economic relationship between the state and the citizen, rather than a bidirectional one. Adding greater optionality, lowering holding, transfer, and switching costs, while enhancing the openness of payment networks can ensure faster, more targeted relief in the next crisis, while addressing stubborn problems for economically marginalized people who pay the most for even basic financial services.

World Bank-KNOMAD staff estimates, World Development Indicators, and International Monetary Fund (IMF) Balance of Payments Statistics.

Citations

- For additional background, New America’s Public Interest Technology program recently studied the disbursement of these stimulus checks and recommended technical fixes and future reforms for helping the payments reach those who needed them most, source