Climate change leaves no sector with more to gain—or more to lose—than the insurance industry. The risk management community could help improve sustainability practices across the global economy through its vast financial assets, expertise, and influence. It touches virtually every sphere of human activity; insurers’ ability to effectively grant or revoke permission to operate affords them singular leverage when it comes to curbing high-risk behaviors. At the same time, the sector stands to incur catastrophic losses if climate change continues to follow its current trajectory.

Whether the sector will serve as a fulcrum for addressing climate change will depend on the standards established by regulatory bodies worldwide. Some regulators have already recognized the importance of placing greater emphasis on climate change, sustainability, and other non-traditional risks. In an April 2018 report (Making Waves: Aligning the Financial System with Sustainable Development), the United Nations Environment Program (UNEP) called for unleashing the full power of the financial industry to address acute environmental and societal challenges in the twenty-first century. The considerable potential referenced by the UN is largely a function of the multiple roles the insurance sector plays as a shock absorber, risk manager and investor.

Both the International Association of Insurance Supervisors (IAIS) and the UN acknowledge that environmental challenges, especially climate change, could greatly impact the industry. In these discussions, three primary risk areas come to the fore:

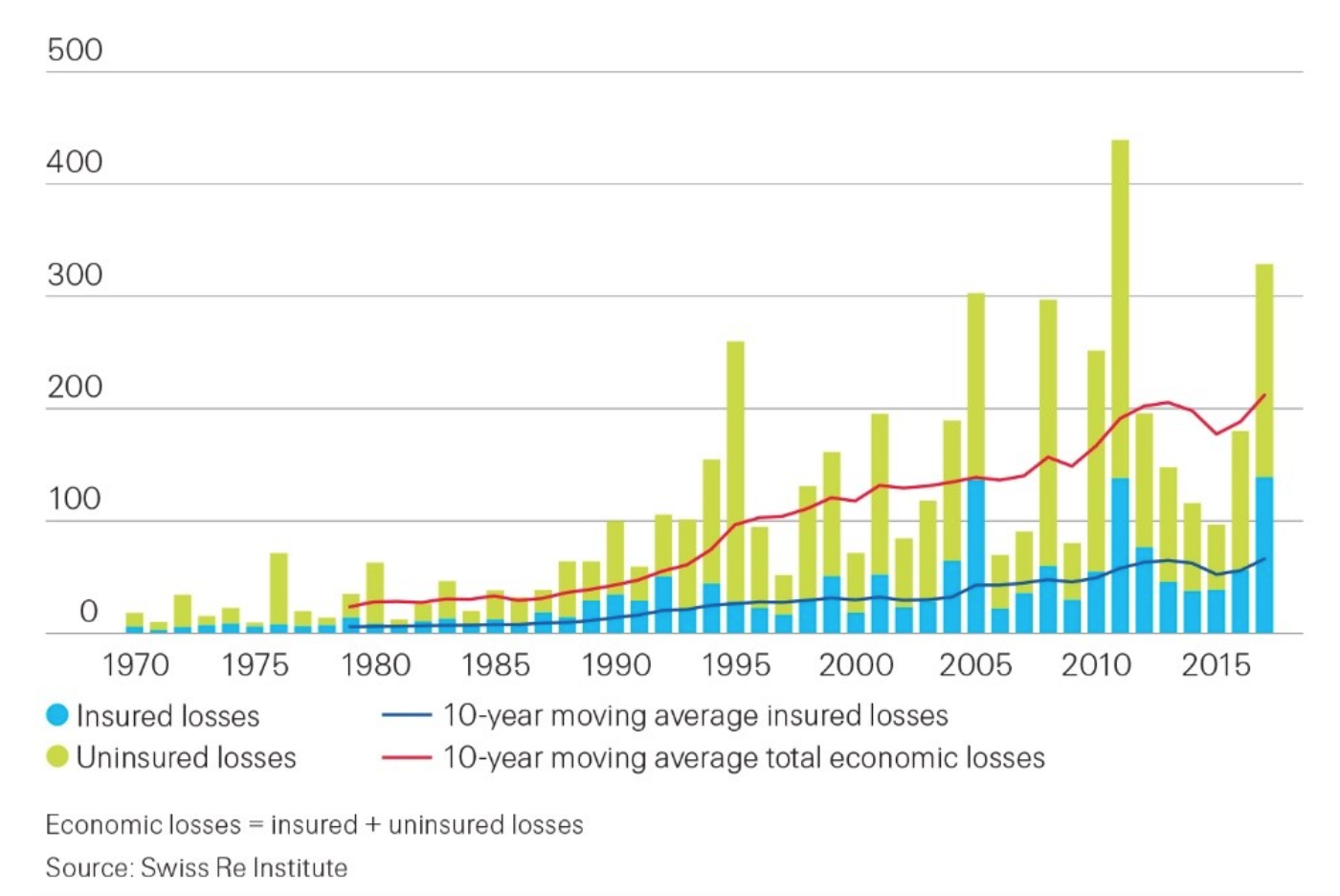

- Physical Risks. Global climate change is already exacerbating natural disasters. As extreme weather events become ever more extreme, the insurance industry could see dramatically higher payouts. In 2017, global insured losses from natural disasters and catastrophe events reached $144 billion (Figure 1), a 158 percent increase from 2016 and an all-time high since the Swiss Re Institute’s Sigma survey began collecting information on disaster events 50 years ago. Extreme weather events such as Hurricanes Harvey, Irma, and Maria led to combined insured losses of $92 billion, which, according to Swiss Re, is equal to 0.5 percent of the U.S. Gross Domestic Product (GDP).1 Data also shows that the climate-risk protection gap—the gap between the insured and the uninsured—remains large. On average, about 70 percent of global economic losses from natural disasters were not covered by insurance companies from 2007 to 2017.2 The inevitable economic victims of climate change depend on a strengthened protections by the insurance industry.

- Transition Risks According to the Geneva Association 2018 report, (Climate Change and the Insurance Industry: Taking Action as Risk Managers and Investors), “transitioning to a low-carbon economy has profound socio-economic implications for many sectors, requiring investments in critical infrastructure, labor training, education and trade.”3 These implications can be translated into reduced asset values or increased volatility in asset prices, both of which will affect the investment portfolios of insurance companies.

The Bank of England has cautioned about the breadth of the potential consequences of transition risks, many of which are poised to impact the insurance sector: “If government policies were to change in line with the Paris Agreement, then two thirds of the world’s known fossil fuel reserves could not be burned. This could lead to changes in the value of investments held by banks and insurance companies in sectors like coal, oil and gas. The move towards a greener economy could also impact companies that produce cars, ships and planes, or use a lot of energy to make raw materials like steel and cement.”4

Given the potential impact of transition risks, insurance firms should consider them when formulating investment strategies. Reducing exposure in sectors with major polluters and disclosing material information on environmental, social, and governance (ESG) factors to regulators and investors could prove critically important insurers’ future. Regulators responsible for safeguarding the sector’s stability and viability ignore these challenges at their own peril.

- Actuarial Risk (Model Error) As the effects of climate change take hold, particularly in advanced economies with relatively high insured rates, flaws in actuarial models are being revealed. For example, the issue of longevity risk—where people outlive their financial reserves—represents a major balance sheet strain for life insurers and pension funds. Insurers tend to calibrate this long-term strain by being among the largest commercial property owners. Similarly, property insurers face the compounding effects of multiple disasters in highly built up areas, all without claim-free time sufficient to build up adequate financial reserves, let alone calibrate pricing. Houston, Texas—the fourth largest city in the United States—has had 3 500-year flooding events in three consecutive years, compounding to 1,500 years of catastrophic flooding. Hurricane Harvey alone had the highest recorded rainfall of any weather event in the United States. While many property insurers face acute losses on the liability side of their balance sheets, they also face the slow-burn effects of eroding property values on the asset side as well, where they are largely exposed.

Meanwhile, prohibitively high insurance expense ratios, ranging 30-50 percent for large insurers, places pressure on broadening coverage for consumers against catastrophic risks, such as floods, wildfires, wind storms, among others. Breaking this actuarial trap requires regulatory stress tests against climate risks and broadening the severity of catastrophic loss scenarios and how they might show up on both the asset and liability sides of insurer balance sheets.

Global Insured and Uninsured Catastrophe Losses (USD Billion) from 1970 to 2017 at 2017 prices

The insurance industry will likely suffer from the destructive effects of extreme weather and the economic transitions resulting from climate change, yet with these risks come opportunities. The sector may greatly benefit from sustainable development across industries and become a leader in efforts to encourage responsible growth. Ban Ki-moon, former Secretary General of the UN, once said that “for years, insurers have been at the forefront of the corporate world in alerting society to the risks of climate change and, more recently, threats such as the loss of biological diversity and the growing pressures on forests, freshwater and other essential ecosystems.”5 Coupled with adroit regulatory action, the insurance industry could build on this role—harnessing its intrinsic financial interest in sustainability and leveraging its unparalleled analytic tools and early warning capabilities to great effect.

The UN’s Environment Program has identified three primary mechanisms through which the insurance sector contributes to the promotion of global sustainable development:6

First, it serves as a shock absorber, increasing the resilience of society and individuals to physical and economic losses. Second, insurance companies can facilitate green financing by incorporating climate change factors into their investment decisions.7 Aligning insurance funds and regulation with sustainable development goals and best practices could be a powerful driver for efforts to build a more sustainable economy. Finally, the insurance sector acts as a risk manager—helping global communities understand, identify, and manage sustainability risks. By incorporating environmental concerns into risk modeling and pricing, the industry can create incentives for its wildly diverse client base (private companies, governments, and individuals) to implement better sustainability risk reduction practices. In the process, it could spark a virtuous cycle, building a sustainable global future.

Citations

- Swiss Re Institute, “At USD 144 Billion, Global Insured Losses from Disaster Events in 2017 Were the Highest Ever, Sigma Study Says,” April 10, 2018, source.

- Swiss Re Institute.

- Maryam Golnaraghi, “Climate Change and the Insurance Industry: Taking Action as Risk Managers and Investors,” January 19, 2018,,source.

- “Climate Change: What Are the Risks to Financial Stability? | Bank of England KnowledgeBank,” accessed August 1, 2018, source.

- Ban Ki-moon, “Message from the UN Secretary-General,” accessed August 1, 2018, source.

- Jeremy McDaniels, Nick Robins, and Butch Bacani, “Sustainable Insurance: The Emerging Agenda,” August 2017, 50.

- *According to estimates by TheCityUK, an industry-led advocacy group representing British financial services, the total global assets under management (AUM) by the insurance industry reached USD $24 trillion by the end of 2016, accounting for almost 15 percent of total investment assets under management worldwide.# As the third largest category of asset manager after mutual funds and pension funds, the sector plays a vital role in the global financial system.