Table of Contents

Applying the Full Cost Framework to Non-Degree Programs at Community Colleges

One of the fundamental building blocks of NFF’s work to improve the financial health and resiliency of the nonprofit sector is the concept of full cost.

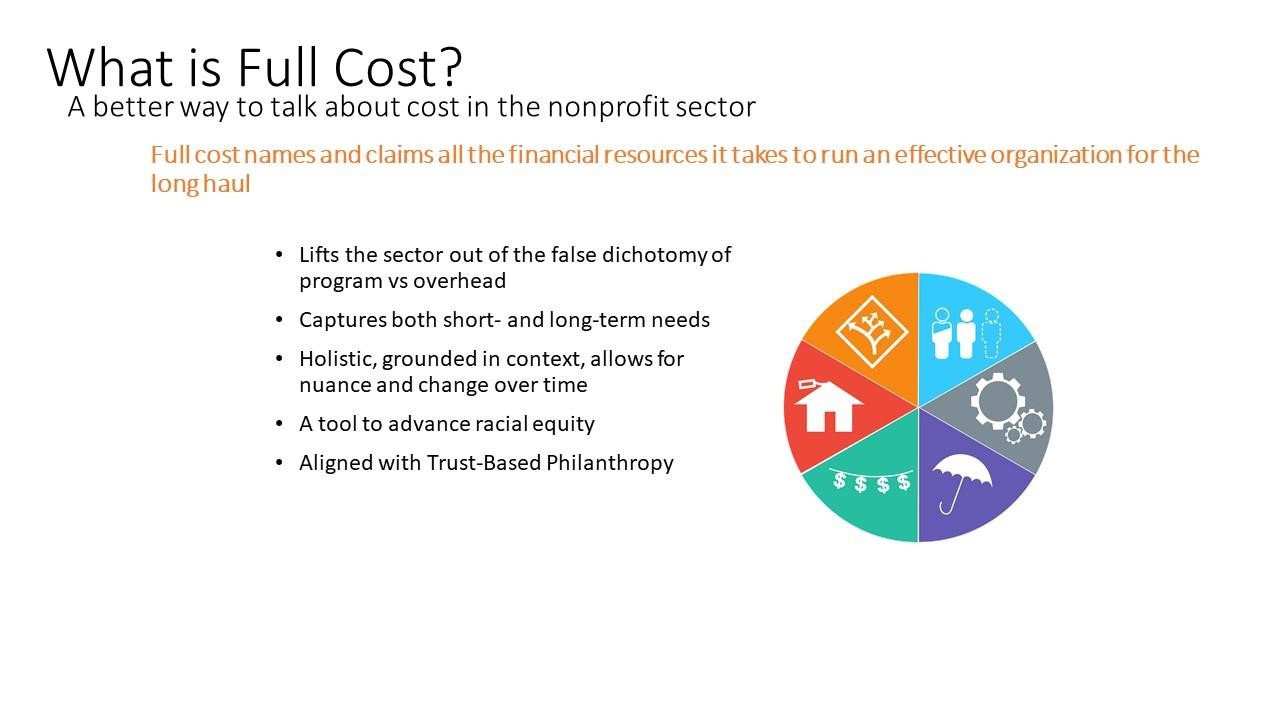

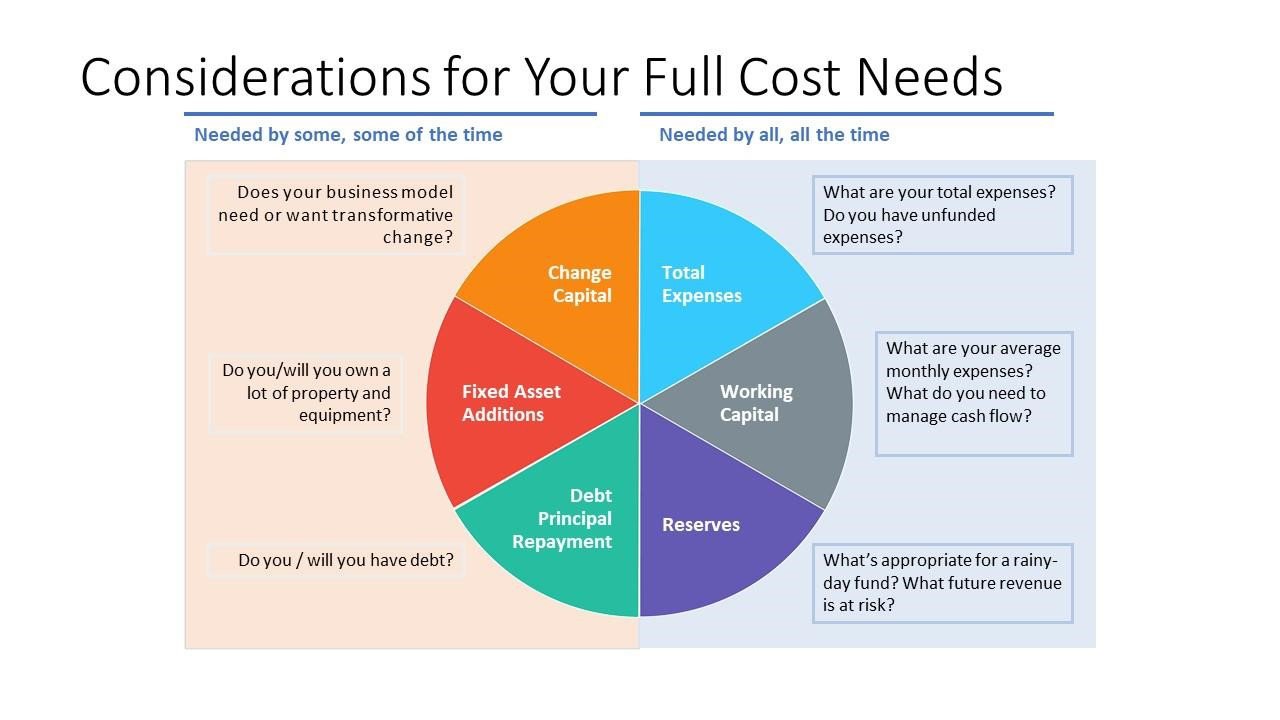

We define full cost as all the financial resources it takes to run an effective organization for the long haul. We believe that healthy organizations can respond and adapt to the changing needs of their communities.

When calculating full cost, our definition incorporates an organization’s expenses and budgeting needs and is comprised of categories that are both needed by all organizations all of the time and needed by some organizations some of the time:

- Total expenses: Funds to cover day-to-day direct and indirect, program and overhead, and unfunded expenses

- Working capital: Funds to keep operations going

- Reserves: Funds to navigate the unexpected, survive a crisis, or act on a new opportunity

- Debt principal repayment: Funds to pay back what has been borrowed

- Fixed asset additions: Funds to pay for new equipment, buildings, and other fixed assets

- Change capital: Flexible funds to reposition an organization’s business model

NFF’s full cost exercise takes an organization-level view because an organization’s income and balance sheet are both part of the full financial picture. An organization’s ability to cover its full costs is tied to its ability to generate consistent surpluses. However, there are several key differences between how community colleges and other nonprofits operate financially. Nonprofits typically view full cost exercises at the organizational level, but, generally, taking an organizational-level view is not possible for non-degree programs at community colleges, as it is standard that any unspent funds at the program or department level are incorporated into the college’s general funds.

View our technical assistance webinar recording addressing How Community Colleges can Leverage Full Cost Budgeting to Finance Non-Degree Programs

Why Talk About Full Costs?

Full cost calculations can be a powerful advocacy tool that community college leaders can use to guide discussions around resource allocation for non-degree programs both internally–with faculty, leadership, boards, and staff, and externally with funders, employers, unions, alumni, economic and community development partners.

In many ways, NFF’s discussions with community college program and institutional leaders about how to effectively and sustainably finance non-degree workforce programs mirrored the conversations that we have with nonprofit leaders throughout the country and across sectors.

Most nonprofit enterprises and programs, including non-degree programs at community colleges, are not accustomed to naming the resources they need to do their work, because they have been conditioned not to do so.

This is because nonprofit organizations operate in a system where funders—including governments, philanthropists, corporations, and foundations—determine how much they will pay for services and set restrictions on how their money can be used. In addition, nonprofits must often rely on constrained public funding streams, which creates an environment of resource scarcity.

As a result, many organization and program leaders are accustomed to “taking what they can get” and “making it work,” and thus do not account for the range of financial resources that it takes to maintain a healthy program within a healthy organization.

Full Cost as a Tool for Internal Advocacy

Leadership can bring strong financial management to their organizations by understanding their organization’s current financial condition, recognizing short-and long-term full cost and needs, and striving to address these needs when planning and budgeting.

Consider the following hypothetical example:

Andréa is creating a new information technology boot camp program at her community college with her employer partners, a consortium of companies in the region’s highest-growth IT companies. Employers are providing financial and in-kind support for instructional design, instructional costs, space, and specialized equipment. Andréa has a grant to provide stipends to students for lost wages while they are in training. She needs to convince her leadership team to use general funds to cover wraparound services for transportation specifically for her boot camp program because she wants to recruit students from neighborhoods where rates of car ownership are low and public transportation is unreliable. Further, she does not know how many years the industry’s financial support will continue and needs to ensure that there are resources available in the future for equipment replacement.

Andréa’s ability to articulate the needs of her program and its students, as well as the different types of revenue associated with them, will help the college’s financial planning and budgeting staff understand the full scale and scope of the program’s budget, and contextualize the amount of funding she is requesting in light of that budget. These data can also help leaders plan for future sustainable investments in the program.

Full Cost as a Tool for External Advocacy

Understanding full cost is a way of naming and claiming the resources than an organization needs to meet its mission in the short and long term. The needs of an individual organization, and the community it serves. This pattern plays out in an organization’s ability to cover its full costs: our society remains segregated by race and class, and philanthropic giving tends to follow these same patterns and networks.

In higher education, governments and local businesses often underinvest in community colleges, and the students they serve are frequently those most excluded from higher education and the labor market on the basis of race, ethnicity, socioeconomic status, and gender. Community colleges and the individuals they serve have financial needs that are different from private and four-year public institutions and their students.

For community colleges, understanding and presenting the full program cost to funders, government, and employers can inform a more realistic conversation about the investment required to move people into better jobs while building the case for longer-term investments in community colleges. Consider the example below:

After several years of running the boot camp mentioned above, Andréa has the opportunity to present the program to state legislators as an example of why her college’s non-degree workforce programs should be included in the state budget. She has data to show strong labor market outcomes, including job retention, earnings, and estimated contributions to economic mobility for underrepresented communities in addition to local tax revenue.

State reimbursements for non-degree programs have typically only covered the instructional costs of programs, but Andréa wants to make a case for increasing the reimbursement rate and having more flexibility in what the state funds can cover, including wraparound supports to make participation in the program and subsequent employment opportunities more accessible to students. Articulating the full cost of the program in the context of the strong outcomes the program has produced lays the groundwork for a more realistic, data-driven conversation about what level of investment the state will need to make in order to meet its economic development goals, and it helps Andréa advocate for increased funding for her program and others like it.

What Are the Full Costs of Delivering High-Quality Non-Degree Programs?

The core business of community colleges is instruction, but the non-degree program leaders we consulted identified a range of non-instructional costs that are critical to their students’ success and their efforts to advance equity goals: serving students from communities that have historically been denied access to resources, ensuring and measuring strong labor market outcomes, and promoting occupational diversification.

In order to articulate their full costs, non-degree program leaders must account for total expenses—including direct, indirect, and unfunded costs—as well as fixed asset additions and change capital.

Here, and in Figure 1 (page 5), we give a representative, though not exhaustive, list of the types of costs that high-quality non-degree programs incur:

Direct costs, the costs associated with program delivery, would not exist if a program was not offered. They may fluctuate with levels of service. Based on our conversations, we identified the following types of direct costs in non-degree programs:

Indirect costs are made up of the overhead contributed by the institution itself, including administration, financial and grants management, and non-instructional space. These are costs that cannot be tied directly to program delivery but that are critical to providing the college’s infrastructure that supports program delivery.

Unfunded expenses are costs that are not currently part of the budget but that, if included, would allow an organization or program to work at its current level without putting unreasonable expectations or strains on the organization and its employees. Common examples in the nonprofit sector include paying staff low salaries, not increasing pay to reflect greater responsibilities or cost of living adjustments, and giving staff members tasks and responsibilities in excess of what can be achieved in a standard work week. Examples of potentially unfunded expenses for non-degree programs include tasks that are considered essential but are added onto into existing staff roles in the absence of adequate resources, including data collection around student outcomes or employer satisfaction; training and professional development of faculty to meet employer needs; instructional design; employer or job placement engagement; fundraising to support ongoing program delivery or wraparound services; and administration of wraparound support programs.

For programs that rely on community-based organizations or other external partners to provide wraparound services, the cost of the partner’s work may also be an unfunded expense in a program budget. If this support is critical to student success, program leaders should try to quantify it in order to capture the full scope of resources need to ensure student success.

Fixed asset additions are the dollars needed to purchase new equipment, buildings, furniture, and land and make leaseholder improvements, all of which depreciates over time. Fixed asset additions do not include small equipment purchases included in annual or program expense budgets or the simple maintenance of existing fixed assets. Examples of fixed assets for non-degree programs include dedicated instructional space, including labs, workshops, and other spaces for hands-on learning. These spaces may include specialized equipment that needs to be updated on a regular or periodic basis in order to keep the instruction relevant and in line with industry needs and employer expectations. For example, some colleges addressing diversity issues may make use of mobile labs, which allow the college to take a classroom experience into the community where underrepresented students reside.

Change capital is the term NFF uses to describe a large, periodic investment into an organization to change its business model, like the size or reach of its mission and/or how it makes and spends money. NFF’s full cost framework is an organization-level framework, but we did see some applications of and need for change capital at the program level for piloting, designing, and launching new programs. New programs, for example, can represent emerging areas of work for a community college, which may require different partnerships, more areas of expertise to be developed, and additional facilities. Or the up-front costs associated with pivoting to an online instructional model might require change capital.

Figure 1: What Are the Full Costs of Delivering High-Quality Non-Degree Programs?

| Full Cost Component | Definition | Examples from Non-Degree Programs |

|---|---|---|

| Direct Costs | Day-to-day expenses incurred during program and organizational operations | Instructional costs Wraparound supports for students Program planning and management costs Data collection Partnership development and management Communications and marketing |

| Indirect Costs | Overhead and administrative costs not directly tied to program delivery | Registrar and enrollment servicesAdministrative offices |

| Unfunded Expenses | Expenses not reflected in spending but that, if included in the budget, would allow staff to work in a reasonable and fair way | Fair-market salaries for staff including overtime compensation Wraparound services provided by the college or by partners |

| Working Capital | Financial resources to maintain operations and meet regular financial obligations | Not applicable at program level |

| Reserves | Financial resources to navigate unexpected events, survive a crisis, or act on a new opportunity | Not applicable at program level |

| Debt Principal Repayment | Financial resources to pay back loans | Not applicable at program level |

| Fixed Asset Additions | New equipment, buildings, furniture, and other larger one-time purchases | Instructional equipmentSpecialized facilities for instruction |

| Change Capital | Money with few or no restrictions that can be used to reposition how an organization earns and spends money in service of its mission | Launching new degree programs or revenue-generating lines of businessOnline instruction platform development and launch |