Table of Contents

- The Emerging Millennial Wealth Gap: Opening Note

- Building Ladders of Success for the Rising Millennial Generation: An Initiative Funded by the Citi Foundation

- Part 1: Generational Wealth and Financial Health

- Framing the Millennial Wealth Gap: Demographic Realities and Divergent Trajectories

- Trends, Origins, and Implications of the Millennial Wealth Gap

- The Millennial Racial Wealth Gap

- The Young and (Economically) Restless: The Nature of Work for American Millennials

- The Financial Lives of Millennials: Evidence from the U.S. Financial Health Pulse

- Part 2: Components of the Millennial Balance Sheet: Assets and Liabilities

- Wealth and the Credit Health of Young Millennials

- Millennials and Student Loans: Rising Debts and Disparities

- Young Adults and Consumer Debt: The Quiet Crisis Next Time

- Homeownership and Living Arrangements among Millennials: New Sources of Wealth Inequality and What to Do about It

- Part 3: Implications for Social Policy

- Public Policy Implications of the Millennial Wealth Gap

- Addressing the $1.5 Trillion in Federal Student Loan Debt

- Policy Responses to the Millennial Wealth Gap: Repairing the Balance Sheet and Creating New Pathways to Progress

The Young and (Economically) Restless: The Nature of Work for American Millennials

Vladimir E. Medenica, Matthew Fowler, and Cathy J. Cohen

The portrayal of the Millennial generation in the popular press has unwittingly flattened the experiences of those who belong to what is now the largest generation of citizens in the country. The public has become familiar with the disparagement of this generation, labeled notably on a Time cover as “lazy, entitled narcissists who still live with their parents.” While no doubt increasing numbers of young adults live with their parents, this trend might have more to do with the economic challenges this generation has faced, rather than a failure to launch. Millennials have come of age just as neoliberalism was deepening its roots in their communities; where a controlled disinvestment in too many communities, often poor communities of color, was contained by policing and mass incarceration. They have experienced the reality of globalization, learning that national political institutions had diminishing control over their economic futures, while watching the living-wage jobs of their parents become part of the past.

Millennials now confront the increasing financialization of the economy, which benefits, as some authors note, “takers instead of makers.”1 And we can add on to their coming-of-age economic experience the fact that many Millennials entered the labor force just as the job market was disrupted by the Great Recession of 2008. Millennials have lived the restructuring of our economy and the increasing polarization of our politics. It therefore seems critical not to belittle this generation, but instead to understand how they see the world and more fundamentally how they understand their economic futures.

Far from being lazy, Millennials now constitute the largest share of the workforce in this country, and they seem to be working so hard that they are now becoming, as Anne Helen Petersen writes in BuzzFeed News, "the burnout generation”:

Financially speaking, most of us lag far behind where our parents were when they were our age. We have far less saved, far less equity, far less stability, and far, far more student debt. The “greatest generation” had the Depression and the GI Bill; boomers had the golden age of capitalism; Gen-X had deregulation and trickle-down economics. And Millennials? We’ve got venture capital, but we’ve also got the 2008 financial crisis, the decline of the middle class and the rise of the 1 percent, and the steady decay of unions and stable, full-time employment.2

And while Petersen describes a daunting economic picture for many Millennials, she readily admits that such challenges are exacerbated for those without college degrees and many Millennials of color. Surprisingly, however, not enough is known about Millennials’ economic lives, financial insecurities, perspectives on economic policies, and aspirations for their economic futures. To explore how young adults experience the economy, structure their work, and assess proposed economic policies, we use data from the GenForward Survey at the University of Chicago, paying special attention to how race and ethnicity influence the financial landscape for Millennials.

The GenForward Survey

The GenForward Survey was founded in 2016 with the goal of expanding our understanding and amplifying the voices of Millennials, in particular Millennials of color. Part of the work of the GenForward Survey is to generate reliable and rigorous data that will facilitate the inclusion of the preferences of Millennials and other emerging generations into our national political conversations. Founded by Dr. Cathy J. Cohen and housed at the University of Chicago, the GenForward Survey is a nationally representative survey of young adults between the ages of 18 and 34 that is conducted every other month and pays special attention to how race and ethnicity shape people’s attitudes and experiences. To date, the GenForward Survey is the most frequent survey of young adults in the United States.

A defining feature of the Millennial (and subsequent rising) generation is their racial and ethnic diversity. As the United States continues to rapidly diversify demographically, examining differences between racial and ethnic groups must be an essential component of any analysis, but especially generational analyses of the United States population. GenForward data allow us to not only shine a spotlight on young Americans writ large, but further disaggregate the larger category often referred to as Millennials by race and ethnicity. By doing so, our data clarify when and how race and ethnicity are associated with different attitudes, experiences, and behavior. We pay attention to identities such as race and ethnicity because previous research has shown important differences in the experiences, attitudes, and behavior of young adults from different racial and ethnic backgrounds.3

In order to speak meaningfully about communities of color, each GenForward Survey includes oversamples of at least 500 African American, 500 Latinx, and 250 Asian American respondents and is offered in both English and Spanish and via telephone and web modes. Oversampling non-white racial and ethnic groups allows us to compare group attitudes with a higher degree of confidence than other surveys. For instance, the 2016 survey of the American National Election Studies (ANES)—a long-running survey typically considered the gold standard of national political opinion data—interviewed only 122 African Americans, 161 Latinxs, and 41 Asian Americans between the ages of 18 and 34. Low sample sizes such as those of the ANES present a challenge to researchers by introducing substantially more uncertainty into the inferences analysts can draw about those populations, as well as limiting the ability to explore subgroup differences along lines of gender or education, to name only two examples.

In this chapter, we try to address gaps in our knowledge about the economic lives of young adults, especially African American, Latinx, and Asian American young adults. In the following pages, we present a high-level overview of some our data as it relates to young people and work, highlighting important differences by race and ethnicity. We draw from two GenForward data sets, February 2019 and April 2017, covering five main themes. First, we will present data outlining the structure of work and economic lives of Millennials; second, young adult perceptions of their economic futures; third, experiences with credit, banking, and retirement planning; fourth, readiness for financial emergencies and external support; and lastly, economic policy preferences.

What the Data Tell Us about Millennials’ Economic Attitudes and Experiences

The Structure of Work / Economic Lives

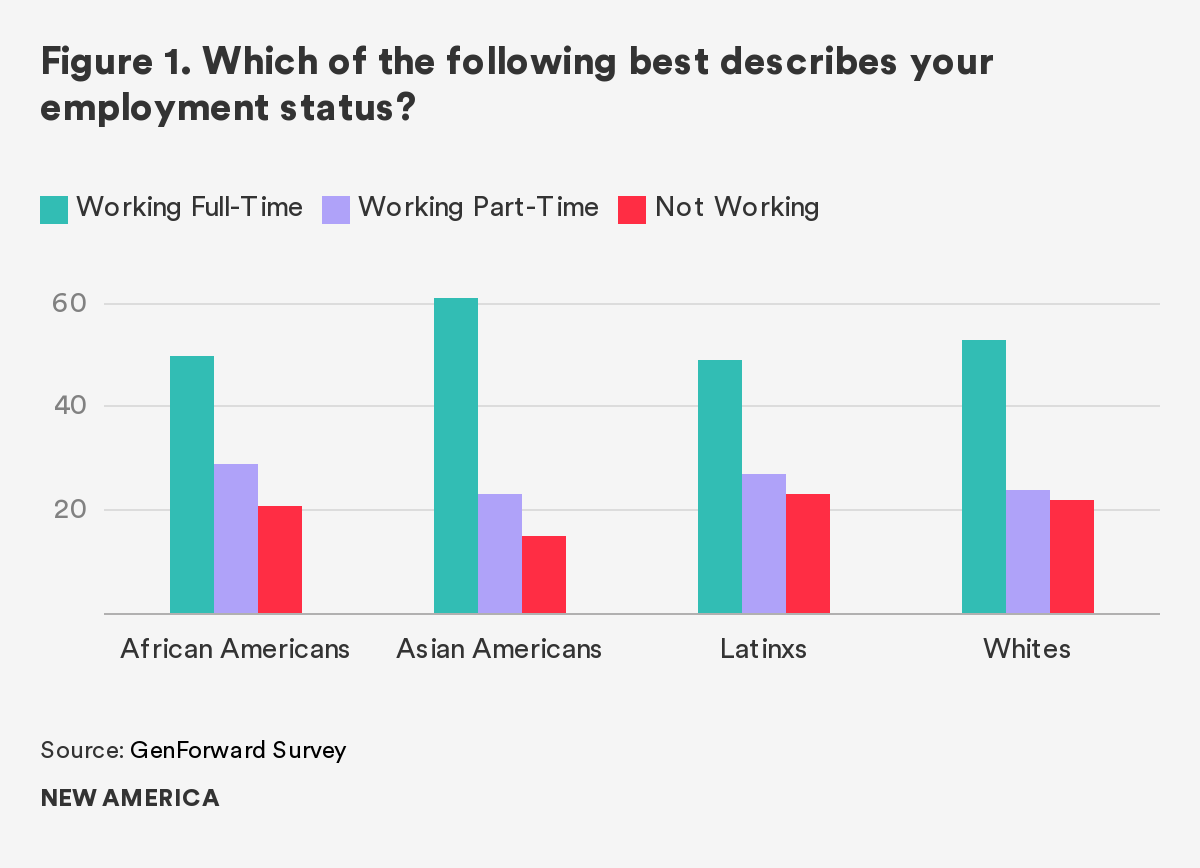

A natural starting point for considering the structure of work for Millennials is employment. How many Millennials are actually working, and how does that number vary by race and ethnicity?4 According to our February 2019 data, we find that Asian American Millennials are more likely to say they’re working full-time (61 percent) when compared to their African American (50 percent), Latinx (49 percent), and white (53 percent) peers. This represents a slight change from April 2017, when 61 percent of white Millennials reported being employed in full-time work compared to 52 percent of Asian Americans and 44 percent of both Latinx and African American Millennials. In fact, more Millennials of color seem to be working in 2019 than 2017 overall; the percentages of African American, Asian American, and Latinx Millennials who reported not working in 2019 dropped 8, 11, and 10 points, respectively, compared to 2017. We should note that the Bureau of Labor Statistics (BLS) does an excellent job of providing detailed employment data, and our estimates of the employment rate for 18- to 34-year-olds are virtually identical to those reported by the BLS.

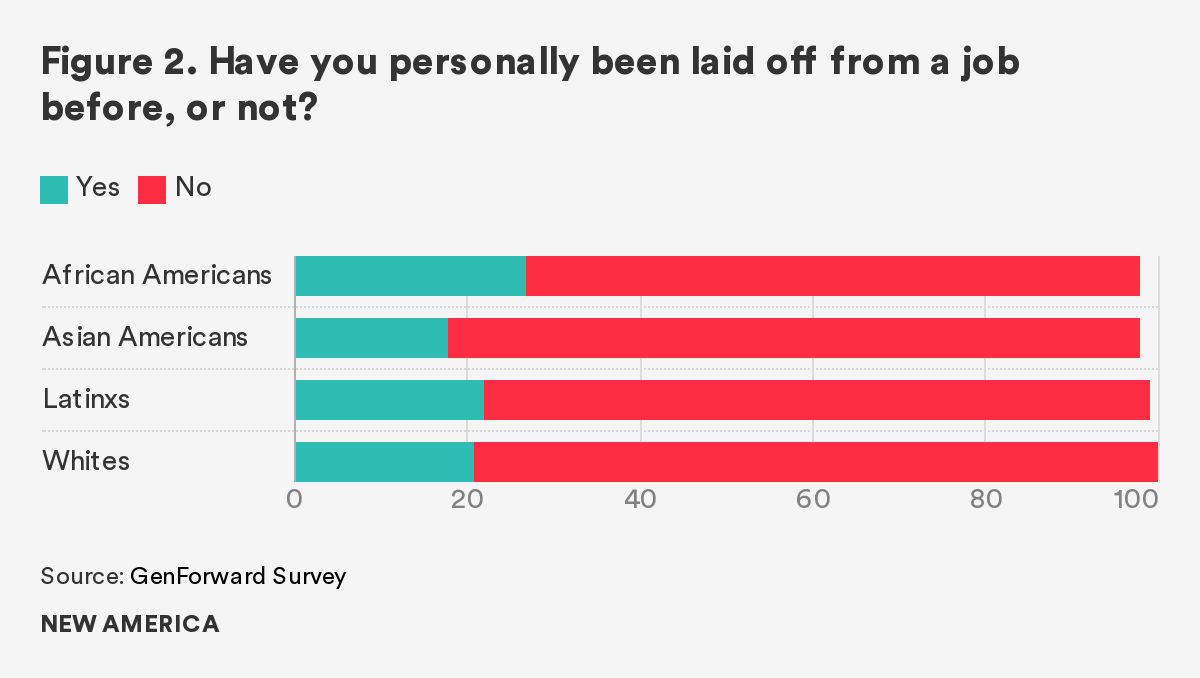

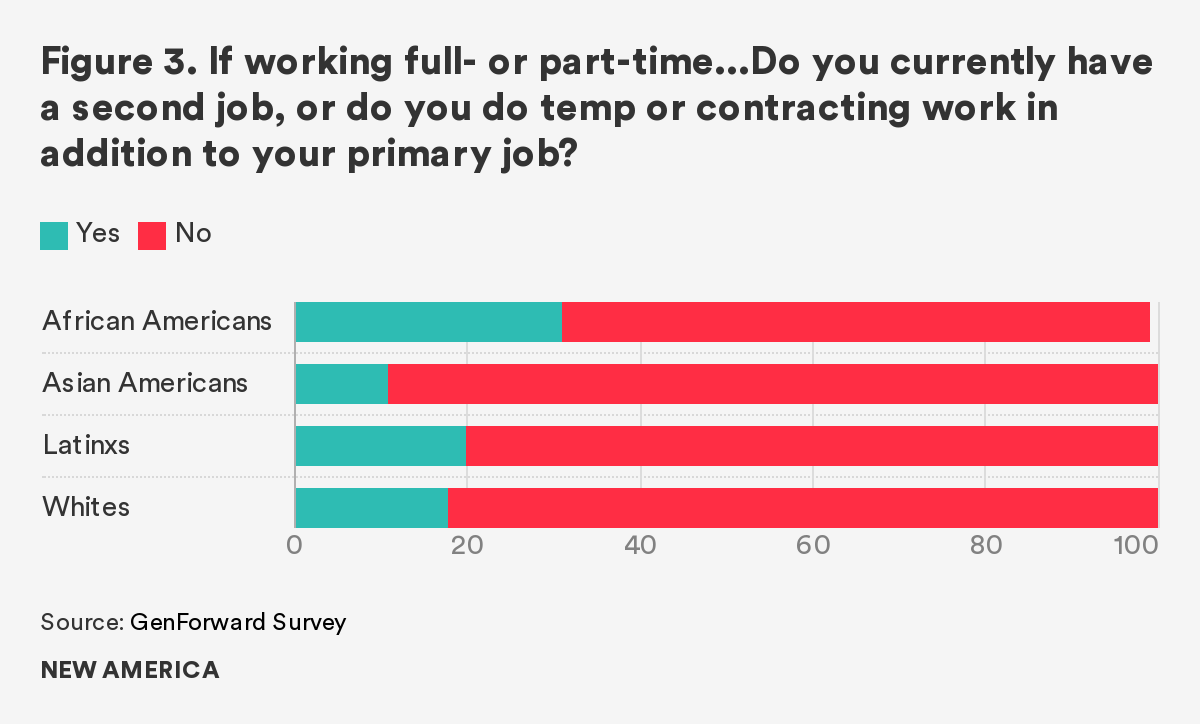

However, employment data reveals only one part of a larger economic story, and the GenForward data allows us to go beyond employment and dig deeper into the economic lives of Millennials. Looking beyond employment offers the opportunity for a more thorough understanding of the economic landscape Millennials face and how it varies by race and ethnicity. For instance, while we find that the overwhelming majority of Millennials in the aggregate—about 77 percent—have not been personally laid off from a job before, over a quarter of African American Millennials say that they have personally experienced a job layoff in their lives. African Americans are also the most likely to be engaged in supplementary employment, meaning they currently hold a secondary job or are engaged in temp or contract work outside of their primary employment. Among employed Millennials, approximately 31 percent of African Americans report engaging in supplementary employment, compared to 20 percent of Latinxs, 18 percent of whites, and 11 percent of Asian Americans.

We know that employment can take a number of forms outside of holding one job, and indeed meaningful percentages of Millennials report working multiple jobs. Working multiple jobs demands a large investment of time. Among those who report being engaged in supplementary work, about 38 percent of African Americans say they spend at least 16 hours per week working outside of their primary employment, the most of any racial or ethnic group in our sample. Approximately 29 percent of whites, 28 percent of Latinxs, and 19 percent of Asian Americans say they spend at least 16 hours per week on their supplementary employment.

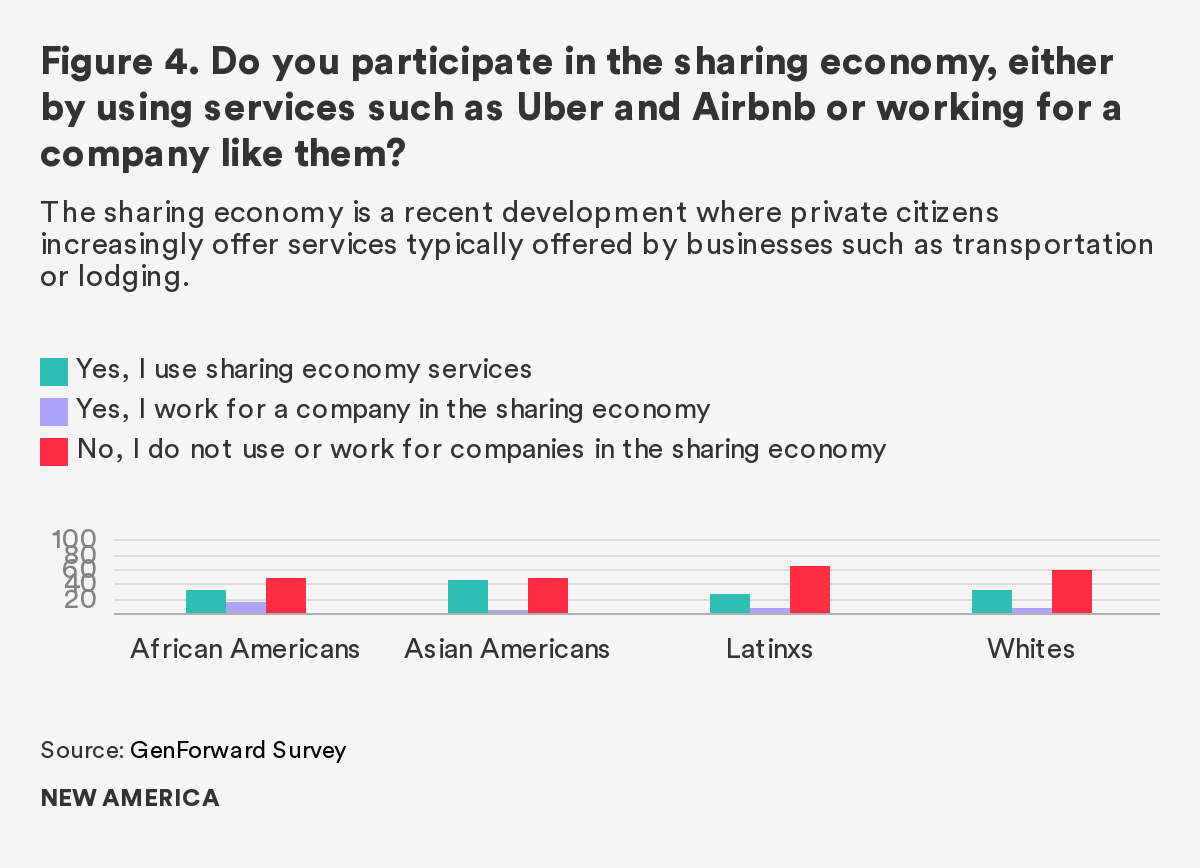

Interestingly, despite working multiple jobs, we do not find strong evidence that Millennials are as plugged into the sharing or gig economy—either by working for or using services provided by companies like Uber or Airbnb—as we might expect, given popular narratives about Millennial preferences for short-term contract work. That said, the data does suggest that African Americans are the most likely to work for a company in the sharing economy. Approximately 17 percent of African Americans say they work for a company in the sharing economy, perhaps a modest percentage on its face but substantially more than the 6 percent of Asian American, 7 percent of white, and 9 percent of Latinx Millennials who respond similarly.

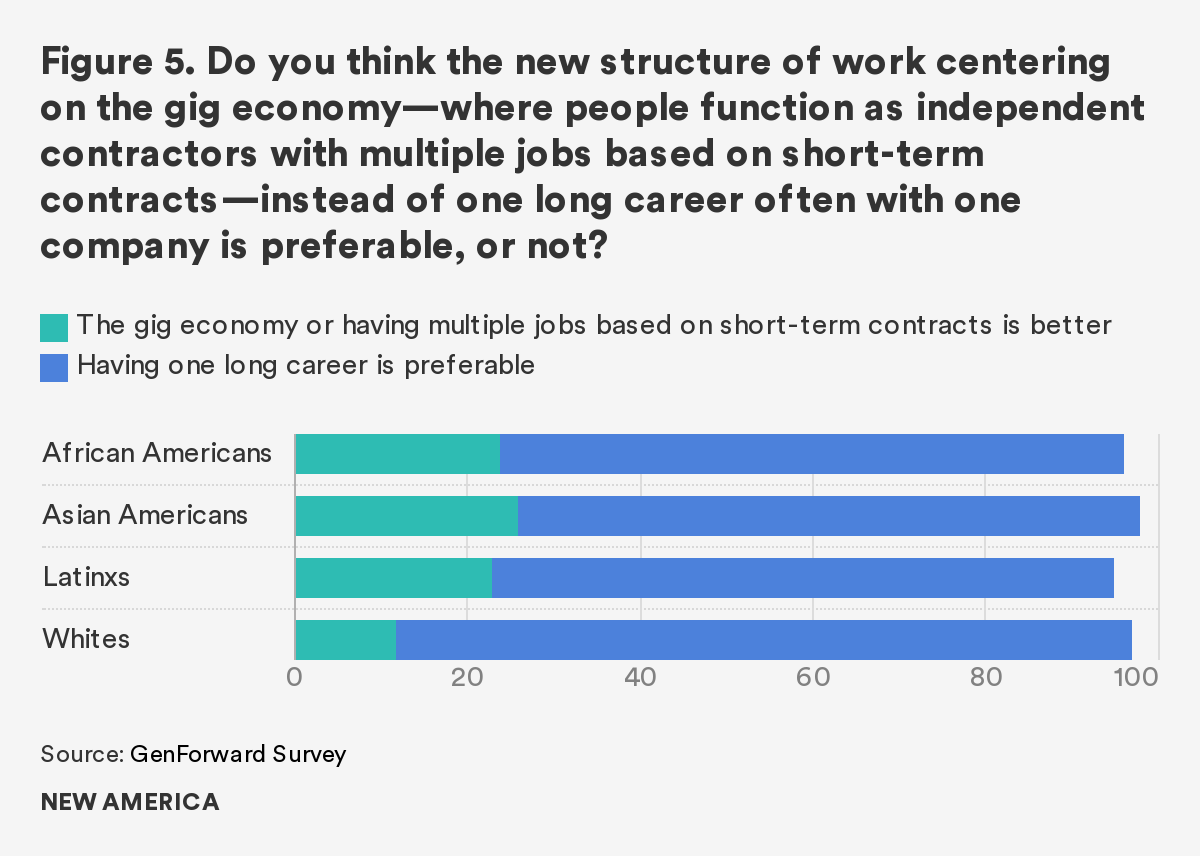

Indeed, when asked if the new structure of work centering on the gig economy—where people function as independent contractors with multiple jobs based on short-term contracts, instead of one long career, often with one company—is preferable, we find that strong majorities of Millennials, and especially white Millennials, believe that having one long career is preferable. Approximately 72 percent of African American, Asian American, and Latinx Millennials and fully 85 percent of white Millennials would prefer having a more traditional job arc spanning one long career to working multiple gigs in the sharing economy.

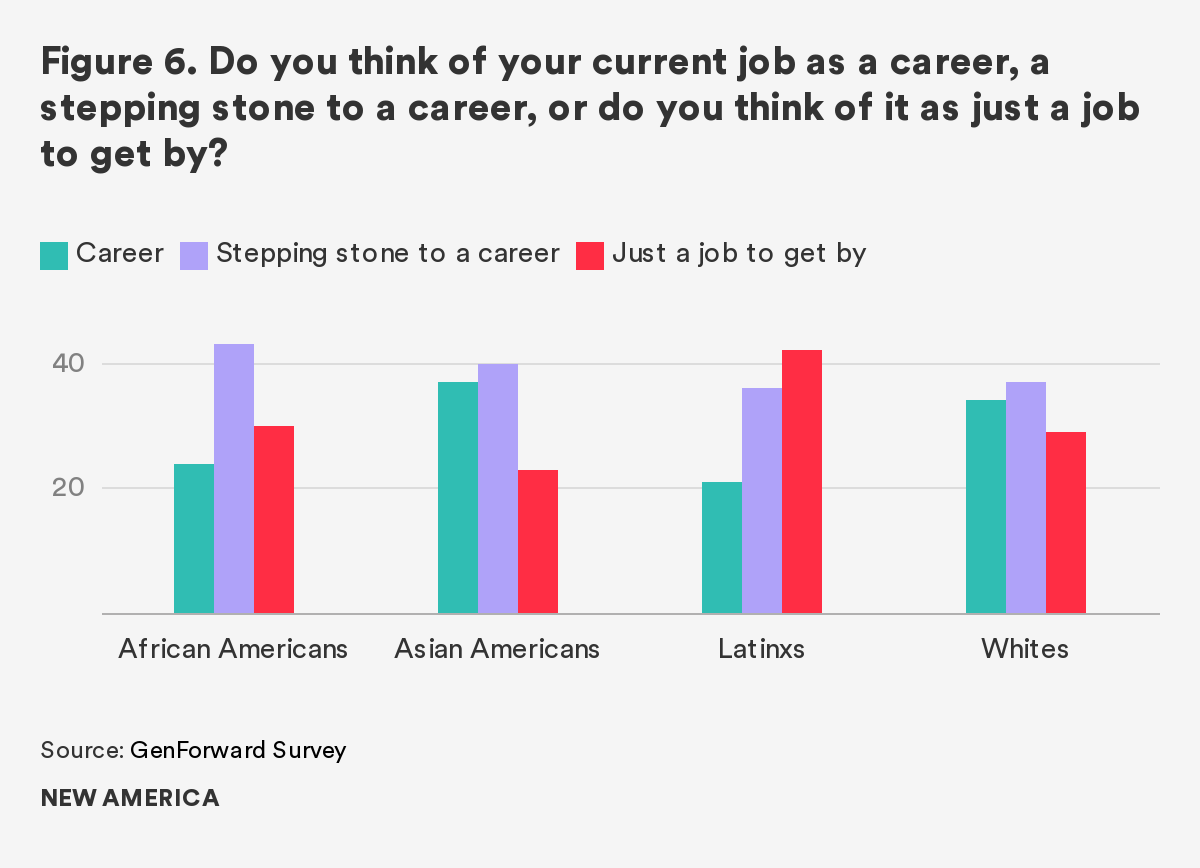

Unfortunately, most Millennials are not engaged in work related to their careers; about 69 percent of Millennials overall consider their current job to be just a job “to get by” or a stepping stone to a career. This is especially true among Latinx and African American Millennials, 78 percent and 73 percent of whom, respectively, say their job is something to get them by or a stepping stone, compared to 63 percent of Asian Americans and 66 percent of whites. Our data further suggests that many of these jobs are not providing Millennials with adequate resources for a strong economic future. Roughly 27 percent of Latinx, 19 percent of white, 16 percent of Asian American, and 14 percent of African American Millennials report not receiving any benefits at their current jobs.

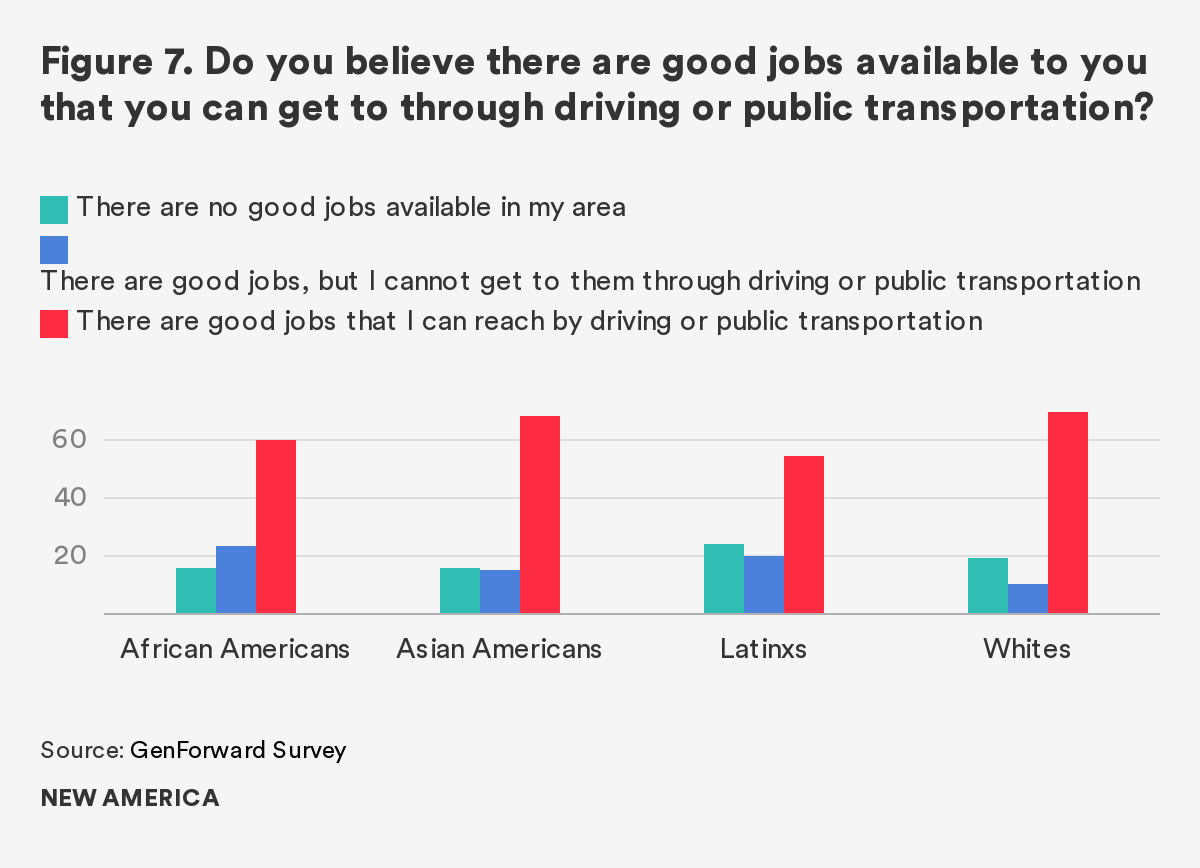

While these data paint a bleak portrait of Millennial employment, those who are employed are fortunate compared to their unemployed peers. Indeed, many Millennials report not having many available options when looking for a job. Roughly 30 percent of young adults between the ages of 18 and 34 say that they do not have access to good jobs, either because such jobs do not exist in their area or because they have no viable transportation options to reach the good jobs that do exist. Once again, African American and Latinx Millennials are particularly disadvantaged when it comes to job options. Nearly 40 percent of African Americans and 44 percent of Latinx Millennials report not having access to good jobs, compared to 29 percent and 31 percent of their white and Asian American peers, respectively. A lack of job options may be a reason why strong majorities of Millennials across race and ethnicity—more than 72 percent overall—say that they are willing to relocate for the right job opportunity.

Perceptions of Their Futures

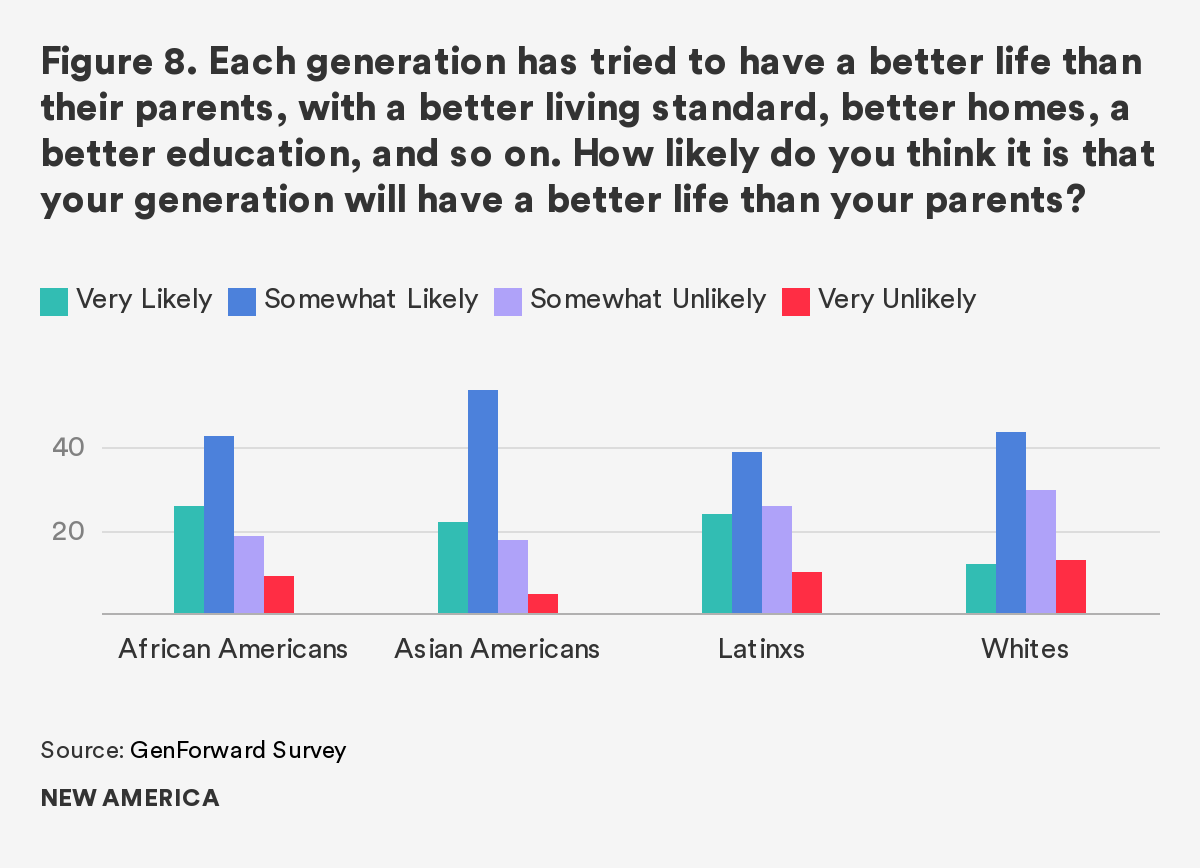

Despite challenging employment prospects and economic conditions, Millennials are generally optimistic that their generation will have a better life than their parents’ generation. African American and Asian American Millennials express particular optimism, with 69 percent and 76 percent saying that they believe it is somewhat or very likely that their generation will have a better life than their parents. Latinxs and white Millennials are not quite as optimistic, though majorities (63 percent and 56 percent, respectively) do say they believe it is at least somewhat likely their generation will have a better life than their parents’ generation.

Compared to responses on this same measure in 2017, we find that, overall, Millennials are not significantly more or less optimistic in 2019. On average, 59 percent of Millennials across race and ethnicity in 2017 felt their generation would do better than their parents, compared to 60 percent in 2019. Aggregate perceptions have remained relatively stable despite popular narratives that perceptions of the economy have actually improved over the last couple of years.

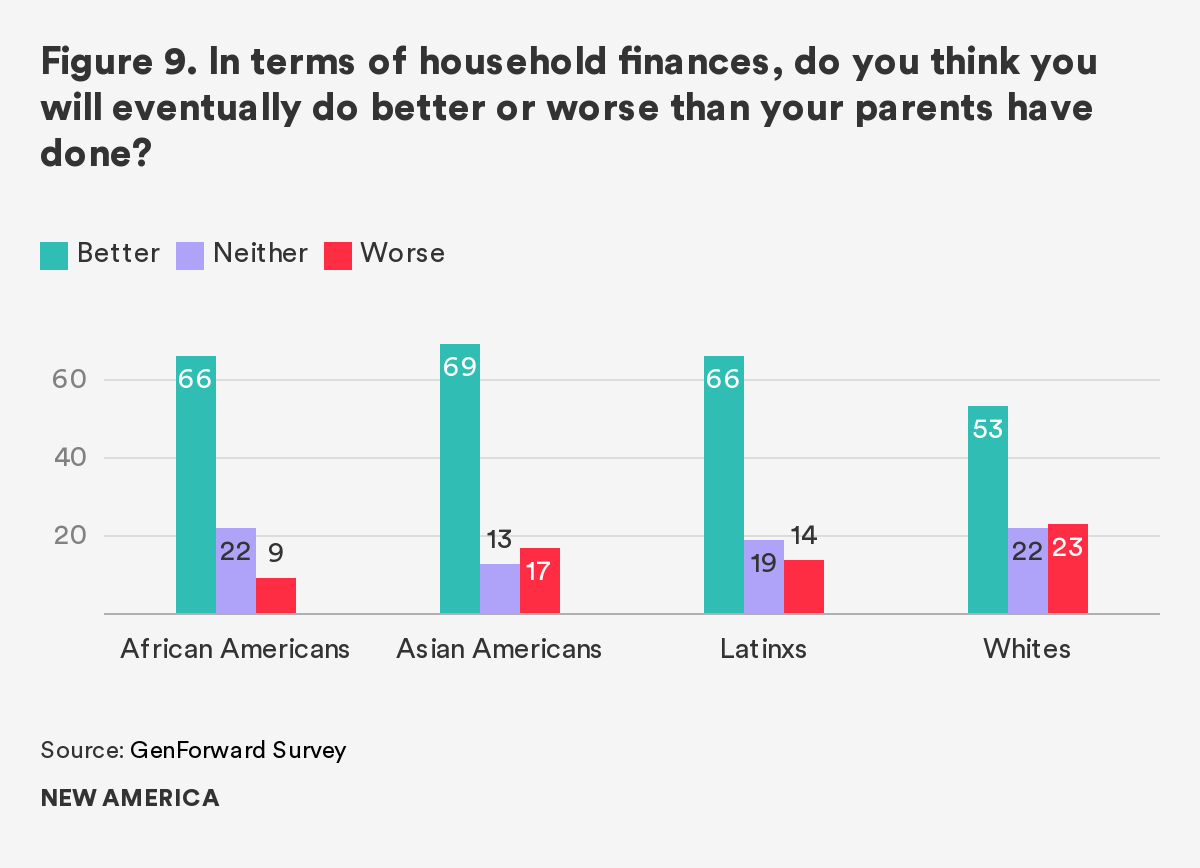

Optimism about their generation extends to optimism about their own economic futures. When we change the focus from the generation at large to their own personal prospective evaluations, we find that Millennials generally think they personally will also do better than their parents. Approximately 66 percent of African Americans and Latinxs, 69 percent of Asian Americans, and 53 percent of whites think they will eventually do better than their parents in their household finances. While this perception is somewhat lower among whites than their peers of color, interestingly it is higher among whites than it was in 2017 when we first asked the question. In 2017 less than a majority of white Millennials (47 percent) believed they would do better than their parents financially. This finding makes sense when considering the activation of white concerns around loss of status and standing in society as evidenced by the 2016 presidential election, and the uncertain economic future that Millennials have faced following 2008’s Great Recession.

Credit, Banking, and Retirement

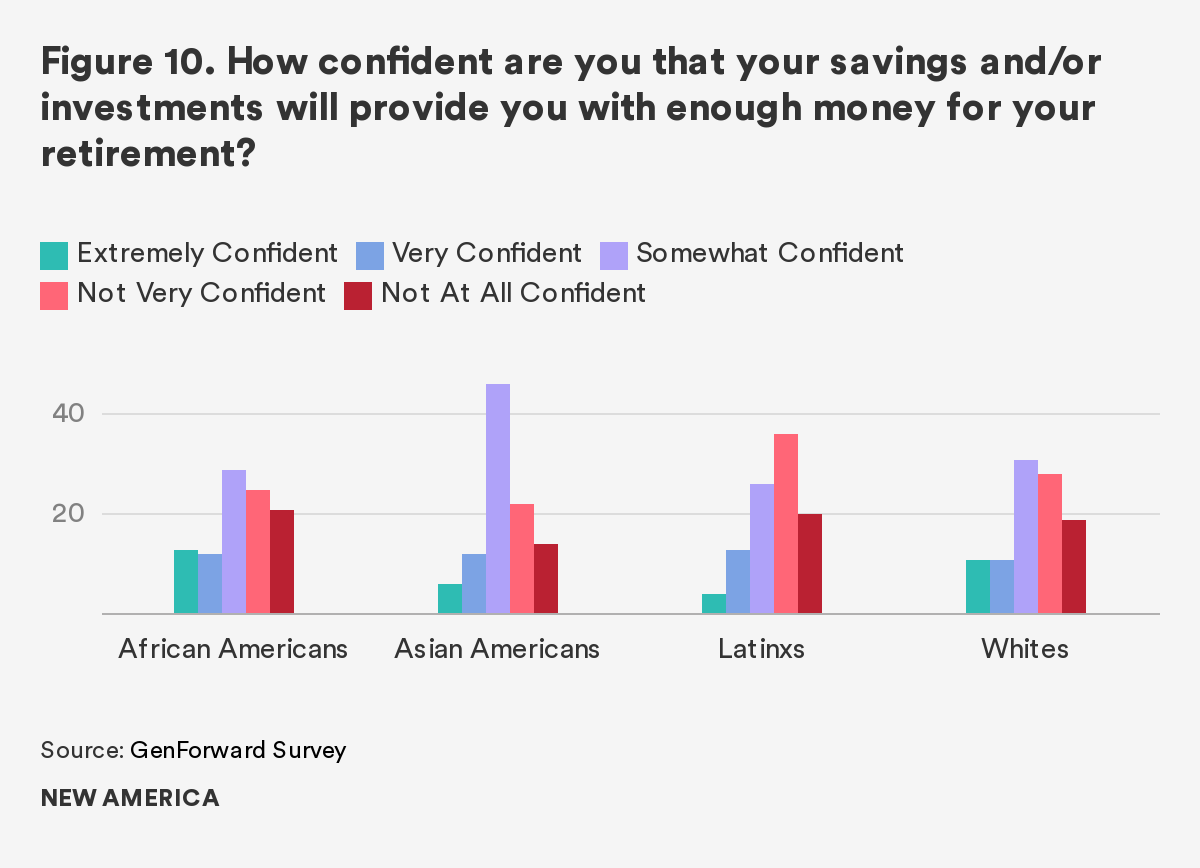

Unfortunately, Millennials’ confidence in their economic futures does not extend to retirement. Young adults feel insecure about the future of their savings and investments. In our February 2019 data, we find that nearly half of African American (46 percent) and white (47 percent) Millennials, and over half of Latinx (56 percent) Millennials, are not very or not at all confident that their savings and/or investments will provide them with enough money for their retirement. Asian Americans feel relatively more confident about retirement than their peers, though substantial numbers—36 percent—do not feel very or at all confident that they will have enough money to retire.

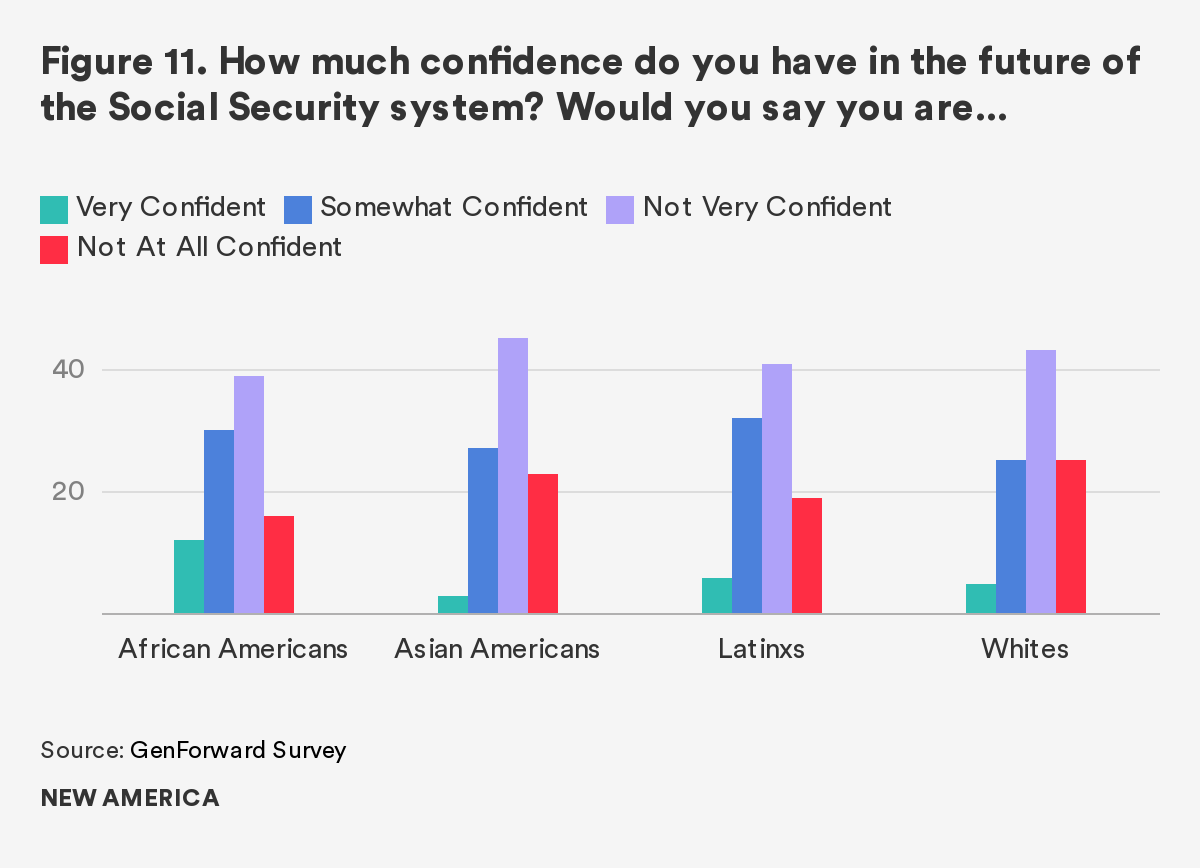

Confidence is also low across the board when respondents are asked about the future of Social Security as opposed to their own savings and investments. Majorities of Millennials, regardless of race and ethnicity, report having very little confidence in the future of the Social Security system. Roughly 55 percent of African Americans, 68 percent of Asian Americans, 60 percent of Latinxs, and 68 percent of whites say they do not feel very or at all confident in the future of Social Security. This is a modest, though by no means insignificant, change from 2017, when large majorities of Millennials also reported feeling not very or not at all confident about Social Security. In 2017, 73 percent of African Americans, 79 percent of Asian Americans, 66 percent of Latinxs, and 77 percent of whites reported feeling not very or not at all confident. Importantly, 62 percent of Millennials in 2017 said that they were planning to rely on Social Security at least a little when they retire. African American and Latinx Millennials were the groups most likely to say they were planning to rely on Social Security a lot, with 21 percent and 16 percent of each respective group reporting planning to rely on Social Security a lot.

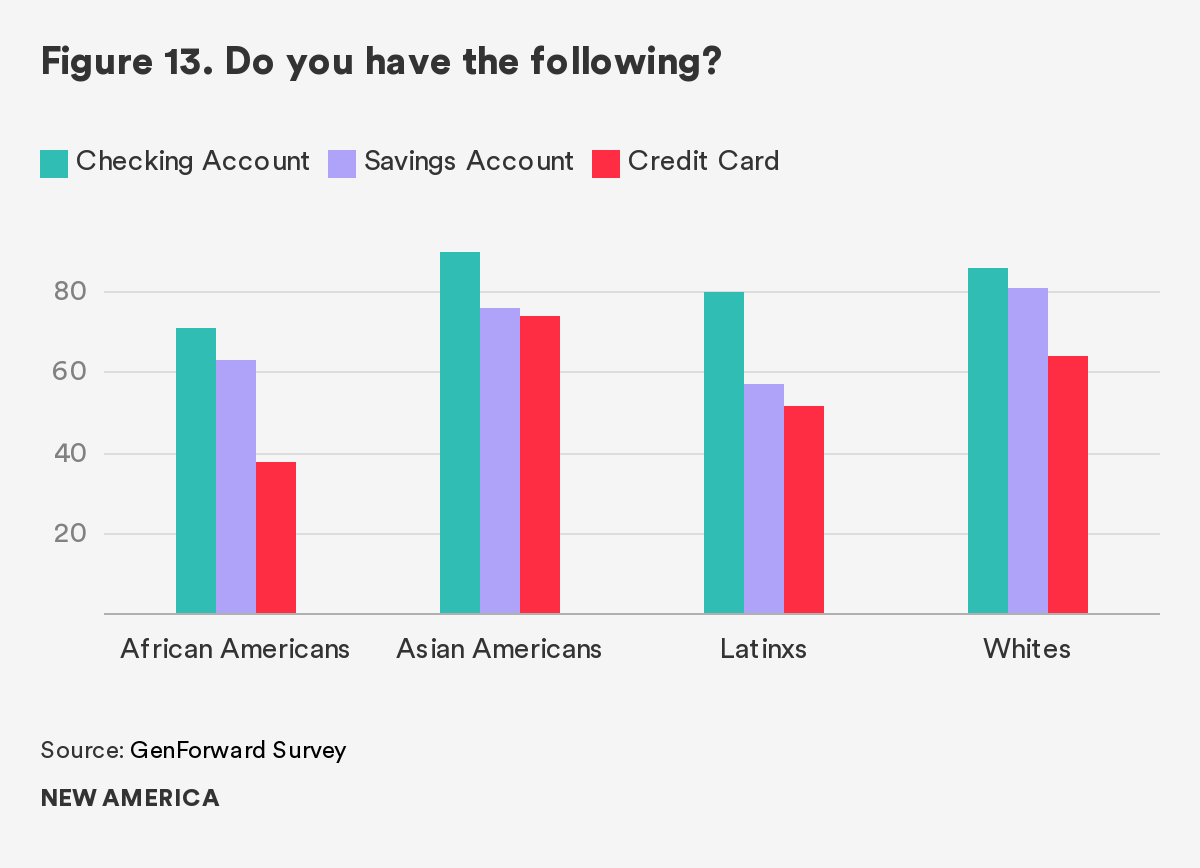

Millennials’ reliance on Social Security is not terribly surprising when placed in the larger context of their economic lives. In our same April 2017 survey, significant numbers of Millennials, regardless of race and ethnicity, indicated that they did not have any sort of retirement or pension plan. Approximately 39 percent of Asian American, 41 percent of African American, 42 percent of white, and over half—52 percent—of Latinx Millennials reported not having any retirement savings or pension. Latinx and African American Millennials were also the least likely to have a savings account. Approximately, 57 percent of Latinxs and 63 percent of African Americans said they had a savings account compared to 76 percent of Asian Americans and 81 percent of whites.

In addition to retirement savings, many Millennials lack access to credit in the form of credit cards. Once again, significantly fewer Latinxs and African Americans reported having a credit card compared to other racial and ethnic groups surveyed. Among African American respondents, only 38 percent reported having a credit card. The percentage was substantially higher among Latinx respondents, 52 percent of whom said they had a credit card. But both African Americans and Latinx respondents were much less likely to have a credit card than Asian Americans or whites, of which 74 percent and 64 percent, respectively, indicated they had a credit card. Interestingly, there were important differences in how white and Asian American Millennials reported using their credit cards; whites report being substantially less likely to use their credit cards for everyday expenses (34 percent) when compared to Asian Americans (62 percent).

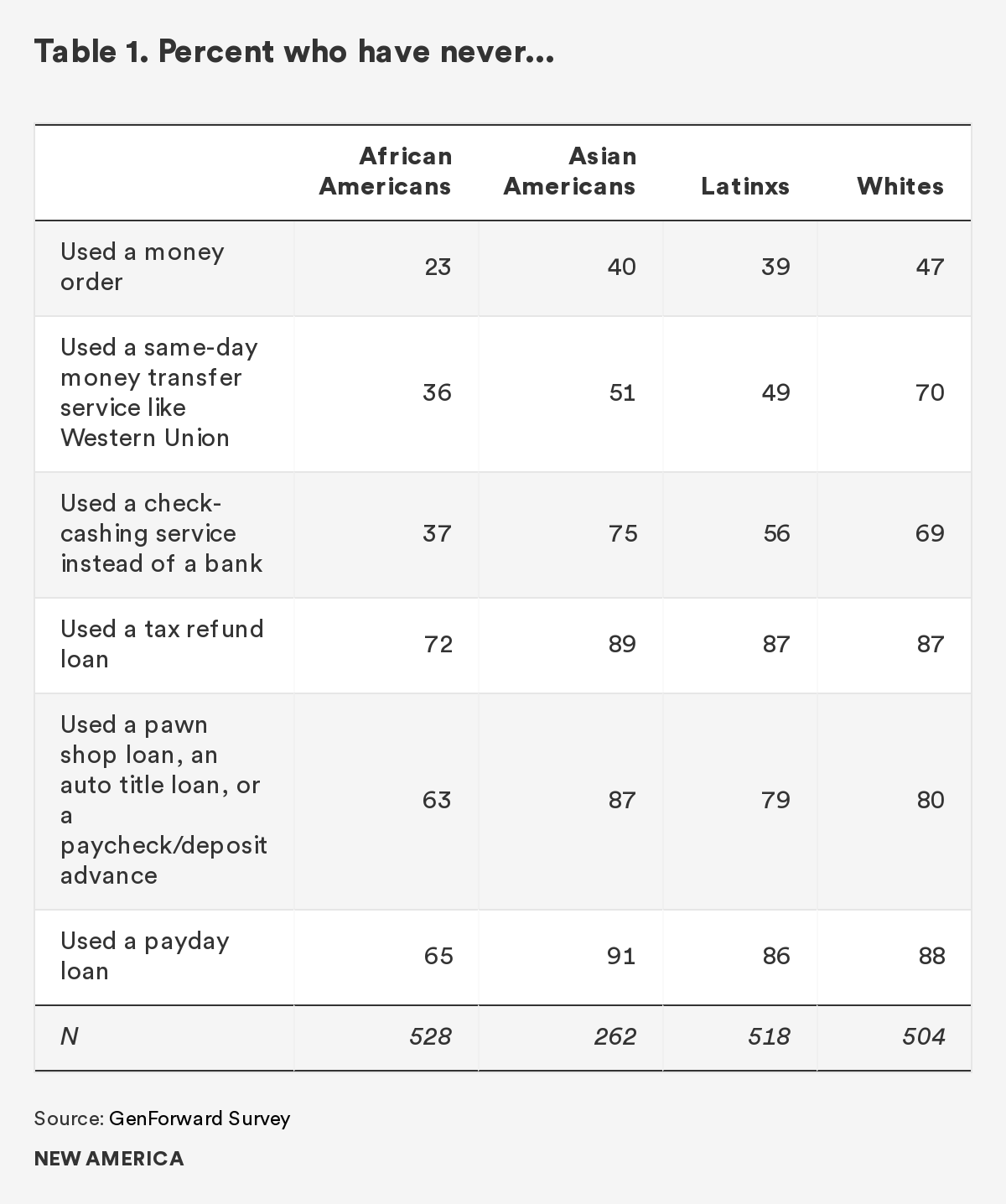

Notably, African Americans were the least likely to have a checking account. Approximately 71 percent of African Americans reported having a checking account, compared to fewer than 80 percent of Latinxs, 86 percent of whites, and 90 percent of Asian Americans who responded similarly. Lack of access to banking services is likely a contributing factor in African Americans’ reliance on non-banking financial services, such as payday loans, check cashing services, and pawnshop loans. Services such as these are known to be predatory and negatively impact the financial health of those who rely on them, which our data suggests is often people of color. A significantly higher number of whites say that they have never used these services when compared to their peers of color. Inversely, African American Millennials seem to rely on or at least use these services more than their peers. For example, 88 percent of white Millennials say they have never used a payday loan, compared to 65 percent of African American Millennials. When asked about check cashing services, 69 percent of white Millennials report never having used a check cashing service. On the other hand, far fewer African Americans—approximately 37 percent—say they have never used a check cashing service instead of a bank.

Financial Emergencies and Family Support

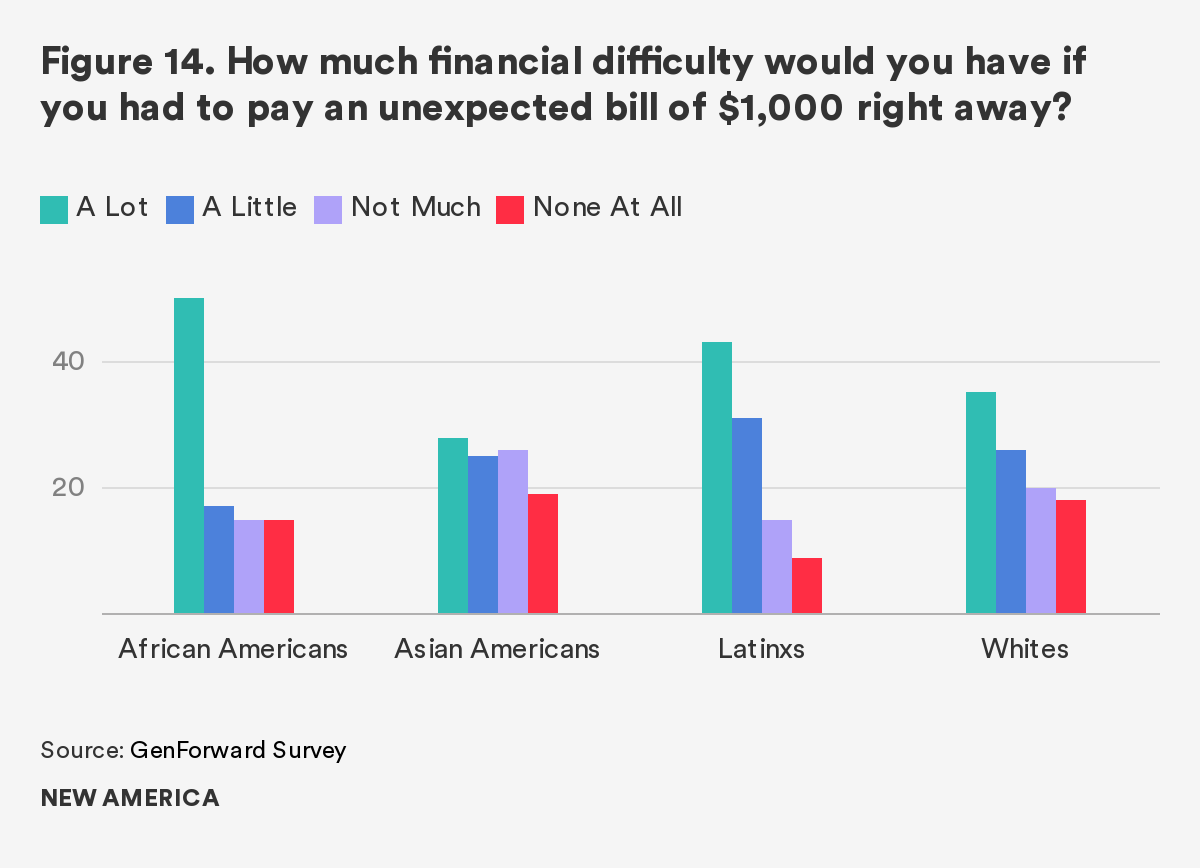

Encountering a financial emergency would have severe deleterious effects on the economic health of many Millennials. Nevertheless, facing an unexpected financial emergency would have disparate impacts on Millennials depending on their race and ethnicity. These effects would be most severe for Millennials of color. For example, in our April 2017 survey, exactly half of African American Millennials we sampled said they would have a lot of financial difficulty paying an unexpected bill of $1,000. Approximately 43 percent of Latinx Millennials also reported that paying an unexpected bill of $1,000 would cause them a lot of financial difficulty, compared to 35 percent of white and 28 percent of Asian American Millennials.

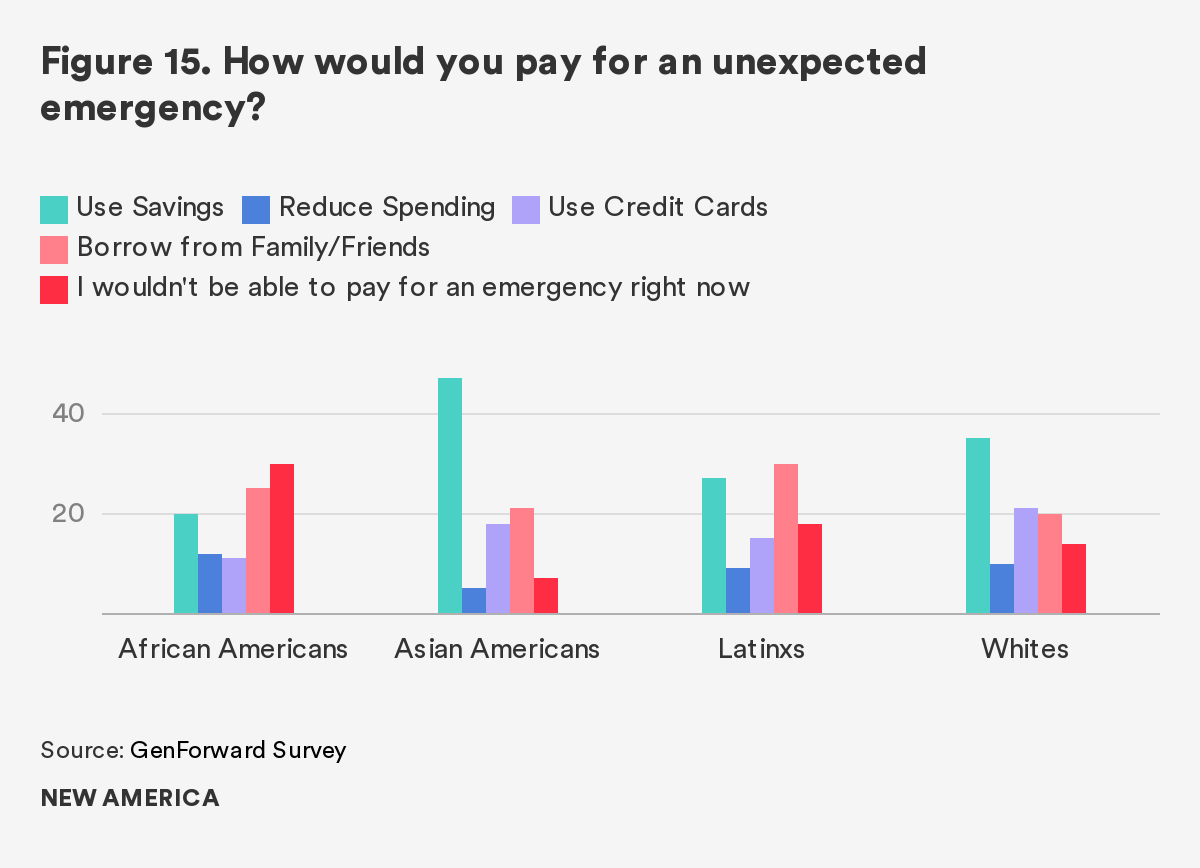

Moreover, fully 30 percent of African American Millennials reported that they would not be able to pay for an unexpected emergency. Only 7 percent of Asian Americans, 14 percent of whites, and 18 percent of Latinxs said they would not be able to pay for an emergency. Asian American (47 percent) and white (35 percent) Millennials in particular reported simply paying for the emergency using money from their savings. Fewer Latinx respondents said that they would pay for the financial emergency using savings (20 percent). Instead, the plurality of Latinx respondents, 30 percent, said that they would borrow money from family and friends to pay off the unexpected expense.

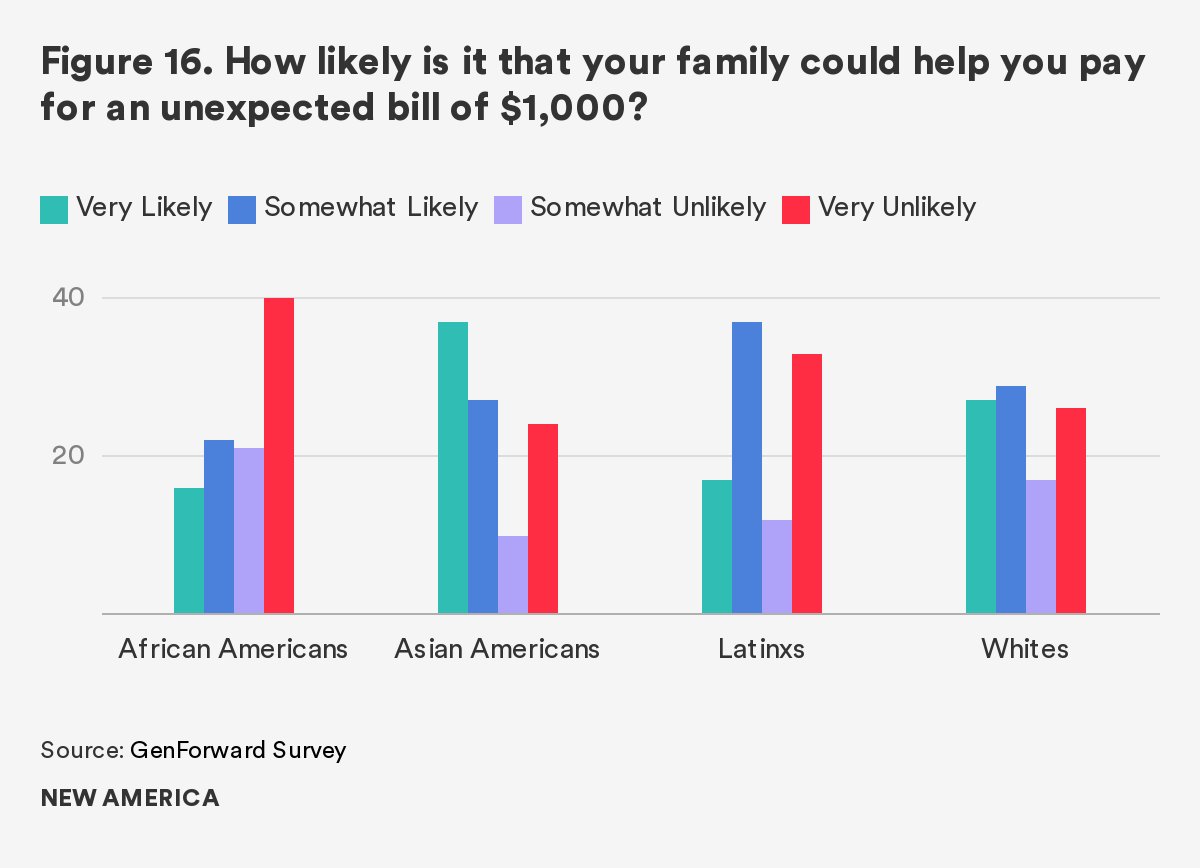

Despite indicating that they would rely on family and friends, 45 percent of Latinxs reported that it would be somewhat or very unlikely that their family could help pay for an unexpected bill of $1,000. This percentage of Latinx Millennials is still lower than that of African Americans, roughly 61 percent of whom say it would be somewhat or very unlikely that their parents could help pay for a financial emergency. What is more, of those 61 percent of African Americans, a full 40 percent indicate that it would be very unlikely, which is substantially higher than their Latinx (33 percent), Asian American (24 percent), and white (26 percent) peers.

Economic Policy Preferences

Taken together, the data presented above on the nature of work for Millennials, their perceptions of their financial futures, and access to savings, credit, and external financial support by family complement and strengthen recent narratives of Millennials as a generation facing real economic challenges. These data also provide important contextual information for understanding their economic policy preferences. On average, the preferences of young adults are significantly more progressive than those of older citizens.5

By and large, Millennials express strong support for more government action aimed at reducing economic inequality, and endorse progressive economic policy prescriptions put forward by political elites like Sen. Elizabeth Warren.

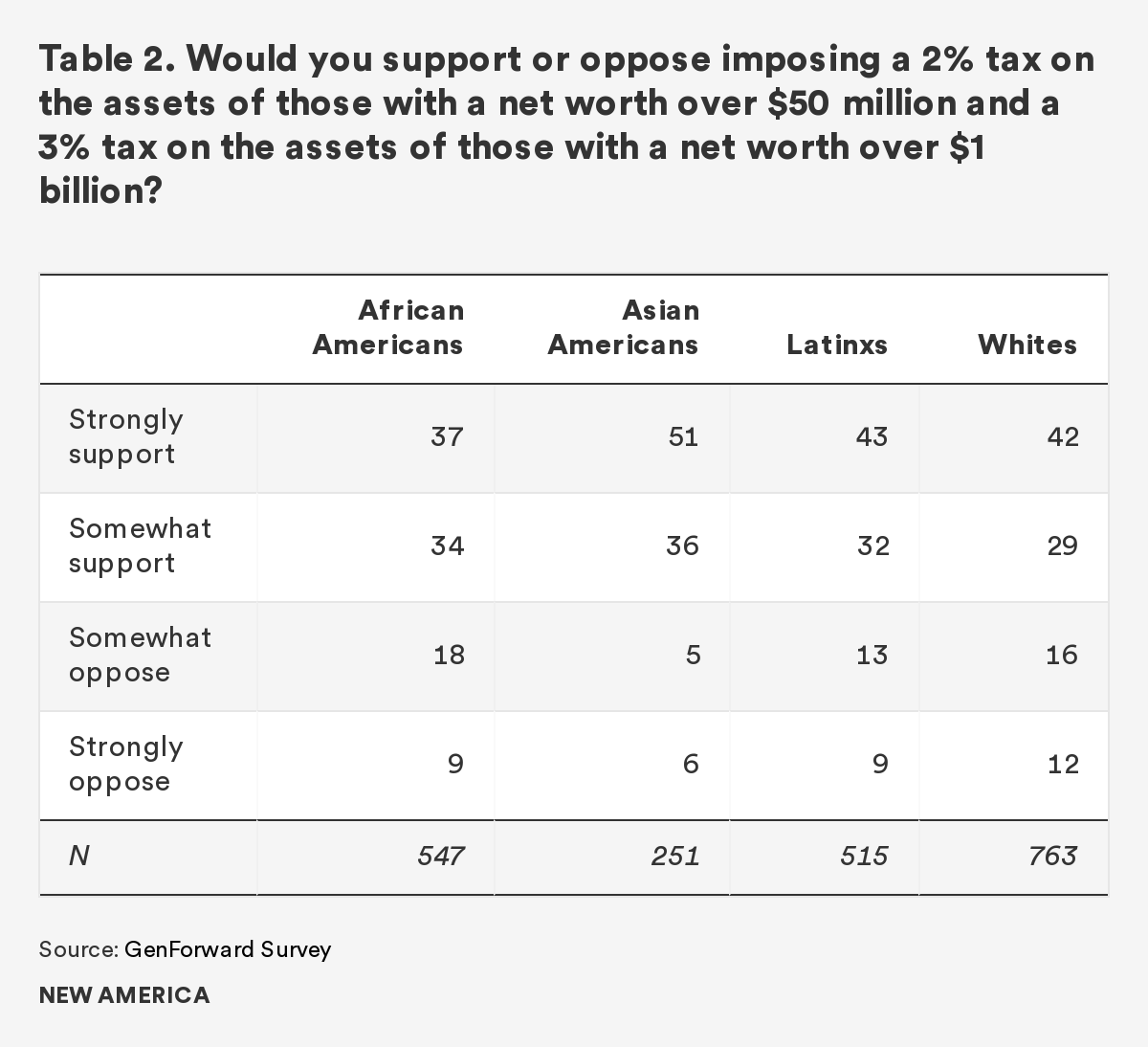

In her current campaign for president, Sen. Warren has announced a number of detailed policy proposals. One of her earliest and most discussed proposals centers on a new wealth tax that would impose a 2 percent tax on the assets of people with a net worth over $50 million and 3 percent tax on the assets of those with a net worth over $1 billion. The proposal has caused a flurry of debate and controversy at a national level, but our 2019 data suggests it is overwhelmingly popular among 18- to 34-year-olds, regardless of race and ethnicity. Approximately 71 percent of African American, 75 percent of Latinx, 87 percent of Asian American, and 71 percent of white Millennials support Sen. Elizabeth Warren’s proposed wealth tax.

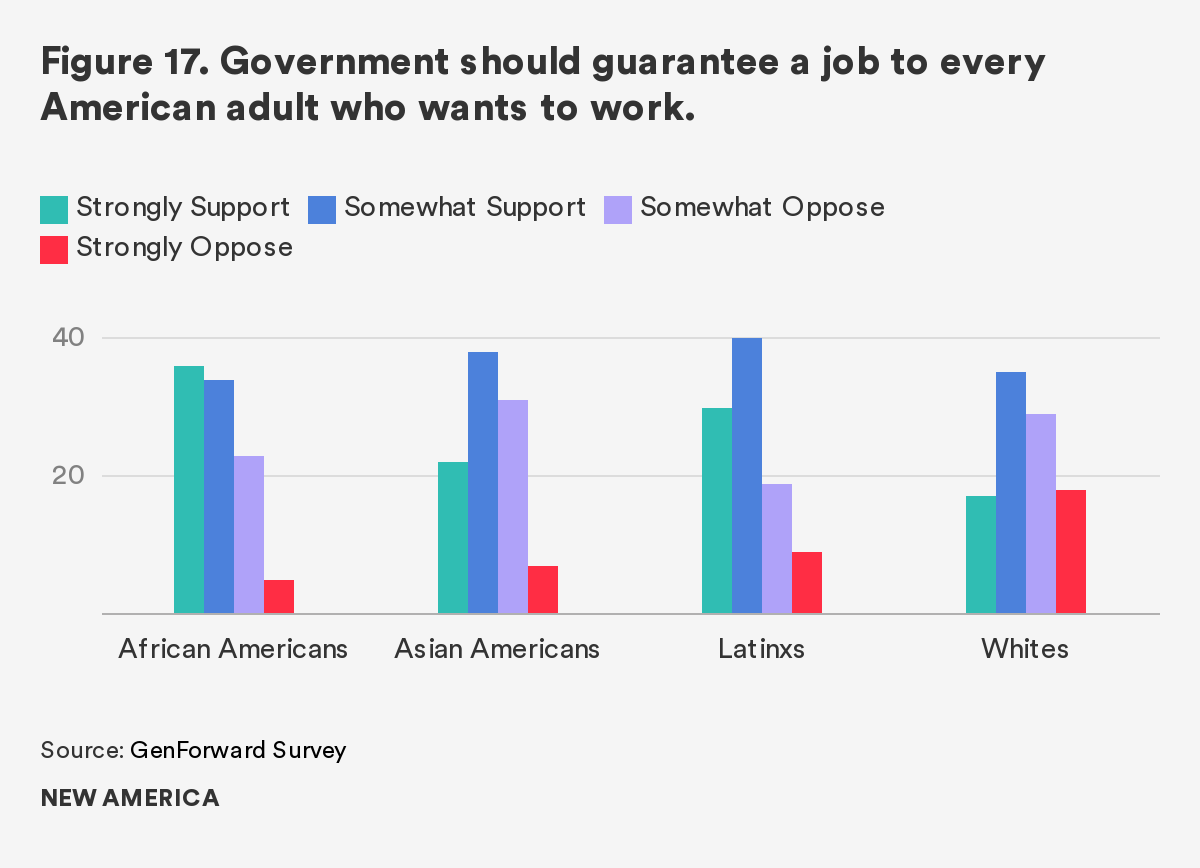

We find similar support for a perhaps even more controversial policy proposal put forward by the left flank of the Democratic Party and other political progressives: a universal job guarantee. Approximately 70 percent of African Americans, 70 percent of Latinxs, 60 percent of Asian Americans, and 52 percent of whites in our February 2019 survey believe that the government should guarantee a job to every American adult who wants to work. Notably, support is highest among Millennials of color, especially African American and Latinx Millennials, compared to white Americans. When considering the racial ethnic divides in the larger portrait of Millennials’ economic lives, however, the expressed differences in policy preferences between white Millennials and Millennials of color are not as surprising.

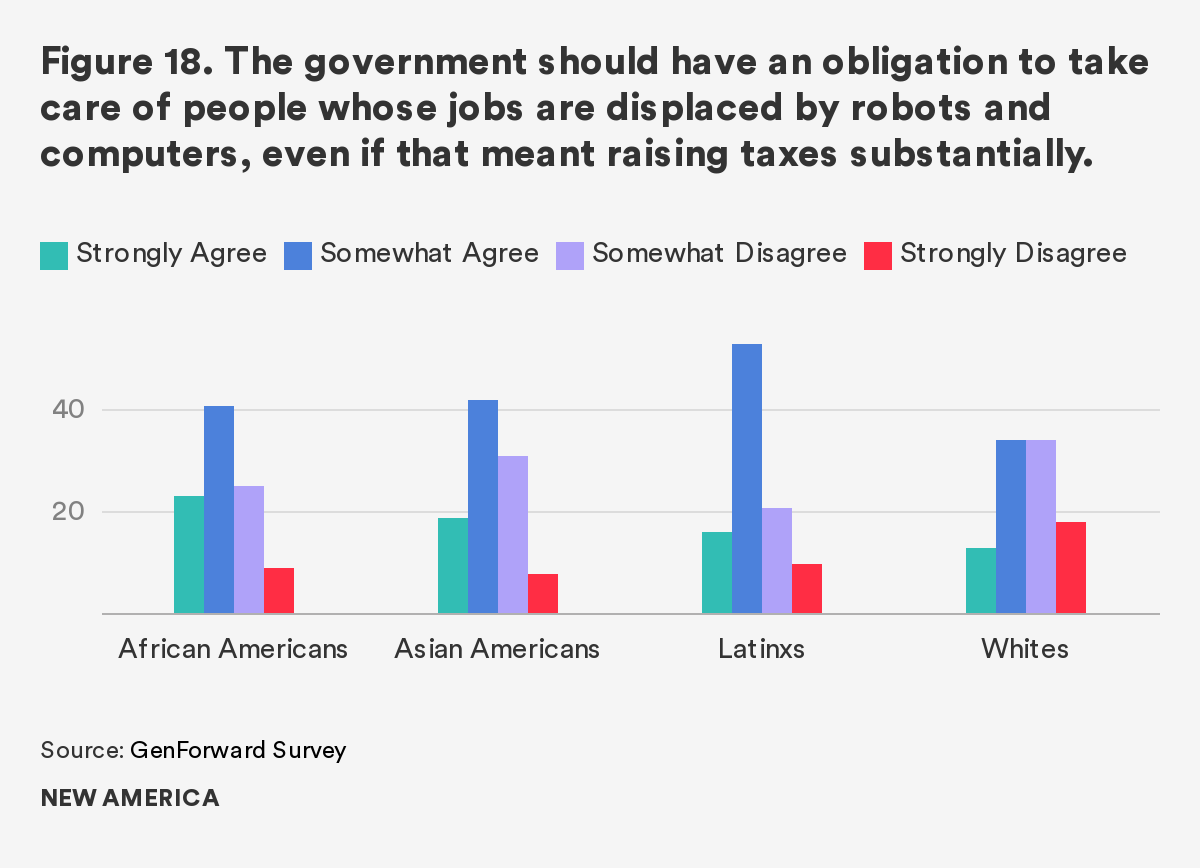

Millennials’ expressed preference for strong government protections remains steadfast even in the face of increased taxes. In general, Millennials report strong support for the government taking care of people whose jobs are displaced by robots and computers, even if that means raising taxes substantially. Approximately 72 percent of African Americans, 88 percent of Latinxs, 69 percent of Asian Americans, and 64 percent of whites strongly or somewhat support a policy that requires companies to pay a tax that goes to retraining displaced workers. And support among Millennials of color doesn’t drop as much as analysts might expect when they are explicitly told that enacting such a policy would mean raising taxes substantially. Support remains high, with about 64 percent of African Americans, 69 percent of Latinxs, and 61 percent of Asian Americans indicating they strongly or somewhat support the government having an obligation to take care of workers displaced by robots and computers, even if it means raising taxes substantially. Support drops to under a majority, or less than half of respondents, only among whites, roughly 47 percent of whom say that they support the government taking care of displaced workers even if it means raising taxes.

However, Millennials do not view being taken care of by the government as the ideal outcome. Instead, large majorities of Millennials across race and ethnicity exhibit support for taxes being used to retrain displaced workers. Approximately 76 percent of African American, 73 percent of Latinx, 70 percent of Asian American, and 63 percent of white Millennials say they somewhat or strongly support companies being required to pay a tax for every worker they displace, with the tax dollars being allocated to retraining the displaced workers.

Conclusion

While Millennials share unique cultural touchstones that distinguish them from older generations, universalizing generalizations about their preferences and behaviors miss their diverse perspectives. It is true that Millennials as a generation face common realities, as they have experienced the same shifts in the American economy. Nevertheless, different subsets of Millennials encounter and experience these economic shifts in very different ways as a function of their distinct social histories and group positions.

Millennials are not a monolith, and as such, it is crucially important that analysts acknowledge and examine the Millennial generation with a deliberate understanding that race and ethnicity structure the lives of individuals distinctly. Understanding when and how race and ethnicity shape the lived experiences of Millennials is vitally important from a practical policy perspective. Privileging race and ethnicity in analyses of Millennials has important implications for how we understand the economic issues Millennials confront, and, perhaps more importantly, for how we design policy in the face of that understanding. Ignoring or overlooking demographic differences will continue to produce misalignment between public policy and the lived experiences of individuals. Gathering and sharing more nuanced data by race and ethnicity allows us to more accurately diagnose and prescribe policy interventions aimed at closing the economic gaps both between and within generational cohorts.

Citations

- Rana Foroohar. Makers and Takers: The Rise and Fall of American Business. New York, NY: Crown Publishing Group. 2016.

- Anne Helen Petersen. “How Millennials Became The Burnout Generation.” BuzzFeed News. January 5, 2019. source

- Vincent L. Hutchings and Nicholas A. Valentino. “The Centrality of Race in American Politics.” Annual Review of Political Science 7(1): 383–408. 2014.

- While we recognize that generational cutoffs are the subject of ongoing debate, we use the term Millennials to describe all individuals between the ages of 18 and 34 for ease of explication.

- Stella M. Rouse and Ashley D. Ross. The Politics of Millennials: Political Beliefs and Policy Preferences of American’s Most Diverse Generation. Ann Arbor, MI: University of Michigan Press. 2018.