Table of Contents

- The Emerging Millennial Wealth Gap: Opening Note

- Building Ladders of Success for the Rising Millennial Generation: An Initiative Funded by the Citi Foundation

- Part 1: Generational Wealth and Financial Health

- Framing the Millennial Wealth Gap: Demographic Realities and Divergent Trajectories

- Trends, Origins, and Implications of the Millennial Wealth Gap

- The Millennial Racial Wealth Gap

- The Young and (Economically) Restless: The Nature of Work for American Millennials

- The Financial Lives of Millennials: Evidence from the U.S. Financial Health Pulse

- Part 2: Components of the Millennial Balance Sheet: Assets and Liabilities

- Wealth and the Credit Health of Young Millennials

- Millennials and Student Loans: Rising Debts and Disparities

- Young Adults and Consumer Debt: The Quiet Crisis Next Time

- Homeownership and Living Arrangements among Millennials: New Sources of Wealth Inequality and What to Do about It

- Part 3: Implications for Social Policy

- Public Policy Implications of the Millennial Wealth Gap

- Addressing the $1.5 Trillion in Federal Student Loan Debt

- Policy Responses to the Millennial Wealth Gap: Repairing the Balance Sheet and Creating New Pathways to Progress

Millennials and Student Loans: Rising Debts and Disparities

Wesley Whistle

One measure of inequality in America today is the widening earnings gap between college-educated workers and those with only a high school diploma. The good news is Millennials who earn a college degree are more likely to earn higher wages. Yet many young adults have found that pursuing education beyond high school can have downsides too. Tuition costs are up, wages have been stagnant, some start but don’t finish their degree programs, and the increased reliance on student loans have all driven down the value of pursuing a college education. With rising costs and increased enrollment—particularly at the height of the Great Recession—overall student debt was bound to increase. Still, it has reached dramatic levels, and tripled over the last 15 years. With total outstanding federal student debt of $1.5 trillion, some have decreed a “student debt crisis” is afflicting the Millennial generation.

Sharpening an effective policy response requires distinguishing among the factors that have contributed to its rise. Part of this increase is directly related to rising costs of college—both from tuition as well as living expenses. Another source of increased student debt is higher college attendance. Since 2000, undergraduate enrollment has increased by more than 3.5 million students.1 More people are getting graduate degrees too.2 For many, borrowing money to pay for training and education can yield returns over a lifetime. Since student loans are often repaid over extended periods of time—as much as 30 years—the theory is that these debts can be managed along with other financial obligations. This means that some debt borrowed years ago still contributes to the cumulative numbers today.

Unfortunately, for a growing number of borrowers, student debt consumes a larger share of income for years on end. Consequently, the burden of student debt has become a source of widespread generational anxiety, and increasingly is garnering attention from policymakers.

This piece focuses on student debt, particularly from the perspective of Millennials. First, it will discuss how the Millennial experience has impacted trends in student loan debt and borrowing. Then, it will examine the data available on student debt to understand what Millennials’ debt looks like beyond the cumulative loan balance. Next, it will discuss research on the nuances of student debt and identify the groups of people with the most excessive debt loads, as well as discuss the existing protections available to borrowers today. Finally, it will provide policy recommendations to improve the student loan experience of Millennials and ways to provide relief to the most vulnerable.

Millennials and the Rise in Student Debt

Millennials came of age during a time of transition in the economy and in the landscape of higher education. During their lifetimes, the costs of attending college rose significantly, with the net price of tuition, fees, and room and board at a public, four-year college increasing 68 percent since the 1999-2000 academic year.3 The sheer amount of loans borrowed annually for higher education has doubled since that same year.4 Despite growing evidence that a college degree leads to higher incomes and career success, students’ perceptions of debt are deeply negative. In a recent poll, 57 percent of Millennials thought student debt was the largest source of consumer debt, even though student pales in comparison to mortgages.5

Although the Great Recession was a catalyst for Millennials’ student debt, the impact varied for students of different ages within the generation. Unemployment for 18- to 35-year-olds hit 13 percent at the height of the recession in 2010, a time when many Millennials were high school.6 Due to such poor labor market conditions, college enrollment spiked as many enrolled in college though they hadn’t planned to originally.7 Others who were already working lost their jobs and enrolled in an effort to reskill and increase their chances of better employment once the economy recovered. And while public institutions—making up for the difference in state appropriations through higher tuition charges to students—absorbed most of the increase, the for-profit sector more than doubled its undergraduate enrollment within six years.8 A sector already more expensive on average, for-profit institutions have been plagued with dismal graduation rates, low job placement success, and even fraud, leaving students saddled with debt they often can’t afford. As the economy has recovered, the problems of the for-profit sector have persisted.

Graduate enrollment also increased as the economy slowed.9 When Millennials with college degrees lost their jobs, some decided to pursue graduate degrees, often with loans. Millennials graduating college were faced with few job prospects and many opted to continue their education. This increase in graduate enrollment has mostly remained steady, and some believe this has led to a tightening job market where people continue to pursue graduate degrees—often with student loans—to remain competitive in the labor market.

Distinguishing among Millennial Student Debt

Data on student debt is somewhat limited, inhibiting experts’ ability to diagnose problems. The federal student loan portfolio offers a snapshot of the existing cumulative debt for Millennials. As of Q2 of the 2019 fiscal year, for borrowers ages 25 to 34—a significant share of the Millennial population—there were $497.6 billion dollars in outstanding student loan debt for about 15.1 million borrowers.10 This translates to an average (mean) student debt of around $33,000 dollars for each borrower. For those ages 24 and younger, there was a cumulative loan balance of $124.6 billion for 8.1 million borrowers—an average of about $15,000 per borrower, though many of those borrowers may still be in school.

These numbers mask several important distinctions. Many of these loans are already in repayment and have been for some time—particularly for the older borrowers. This means they have left school already and begun to repay their loans. Some are reducing their debt, and those who are paying something but not enough to cover their full obligations may actually be seeing their debts grow. The cumulative balance also includes those from graduate school, likely increasing the average debt load per borrower, given that undergraduates are tightly limited in how much they can borrow. Unfortunately, the data does not reflect if a student has graduated, dropped out, or is still enrolled.11

Millennial Undergraduate Debt by Degree

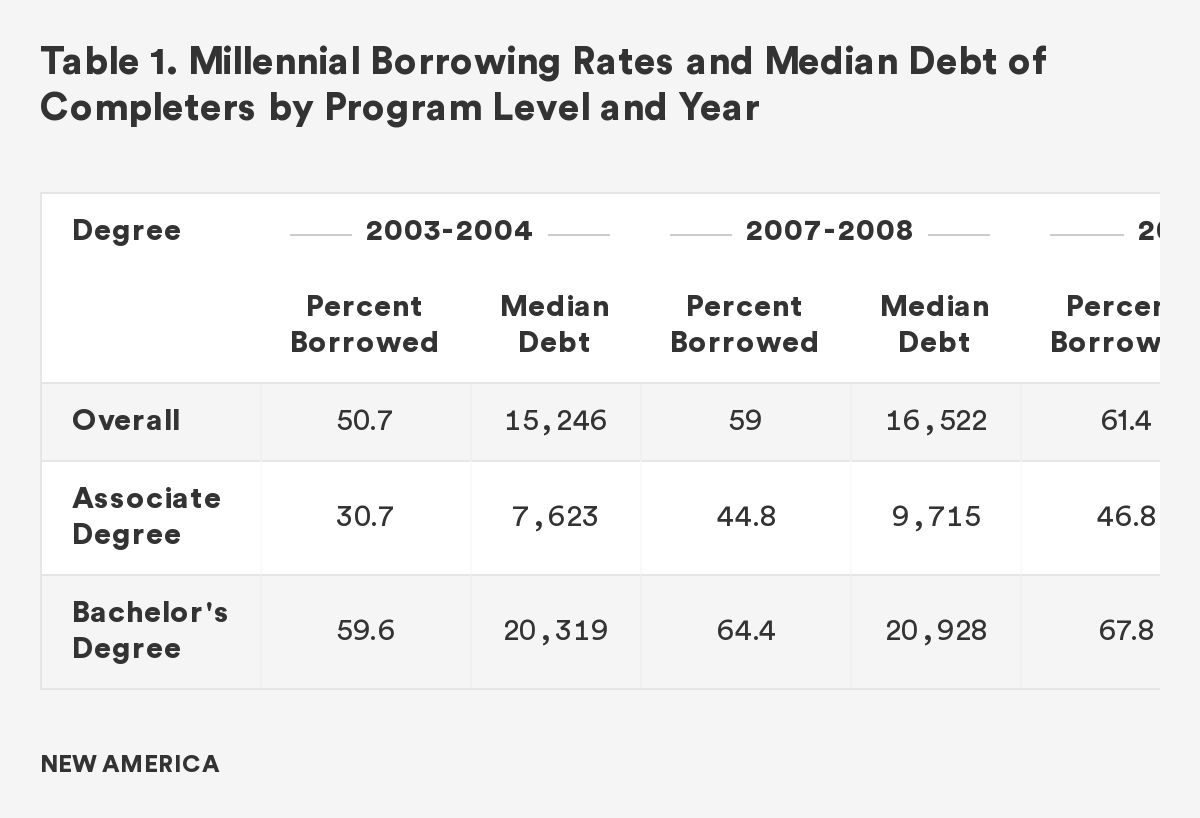

Data from a survey of borrowers conducted by the U.S. Department of Education allows us to see how Millennials borrowed for their undergraduate degree at different times. Table 1 depicts the borrowing of Millennials for their undergraduate education across four separate snapshots of academic years in which they received their degrees. It shows the percentage of graduates who borrowed and, of those students who borrowed, their median debt at graduation. Depending on the year in which a student graduated, they borrowed at different rates and borrowed differing amounts.

As college costs increased, more students borrowed and they borrowed more. While rates increased for both bachelor’s and associate degree recipients, borrowing for 2-year associate degrees increased much more, at 46 percent, compared with a 13 percent increase for bachelor’s degree graduates. Dollar amounts—adjusted for inflation—also increased over time. Not surprisingly, the largest increase in total borrowed was from the 2007-2008 graduates to the 2011-2012 graduates, during the height of the Great Recession.

Millennial Undergraduate Student Debt by Race

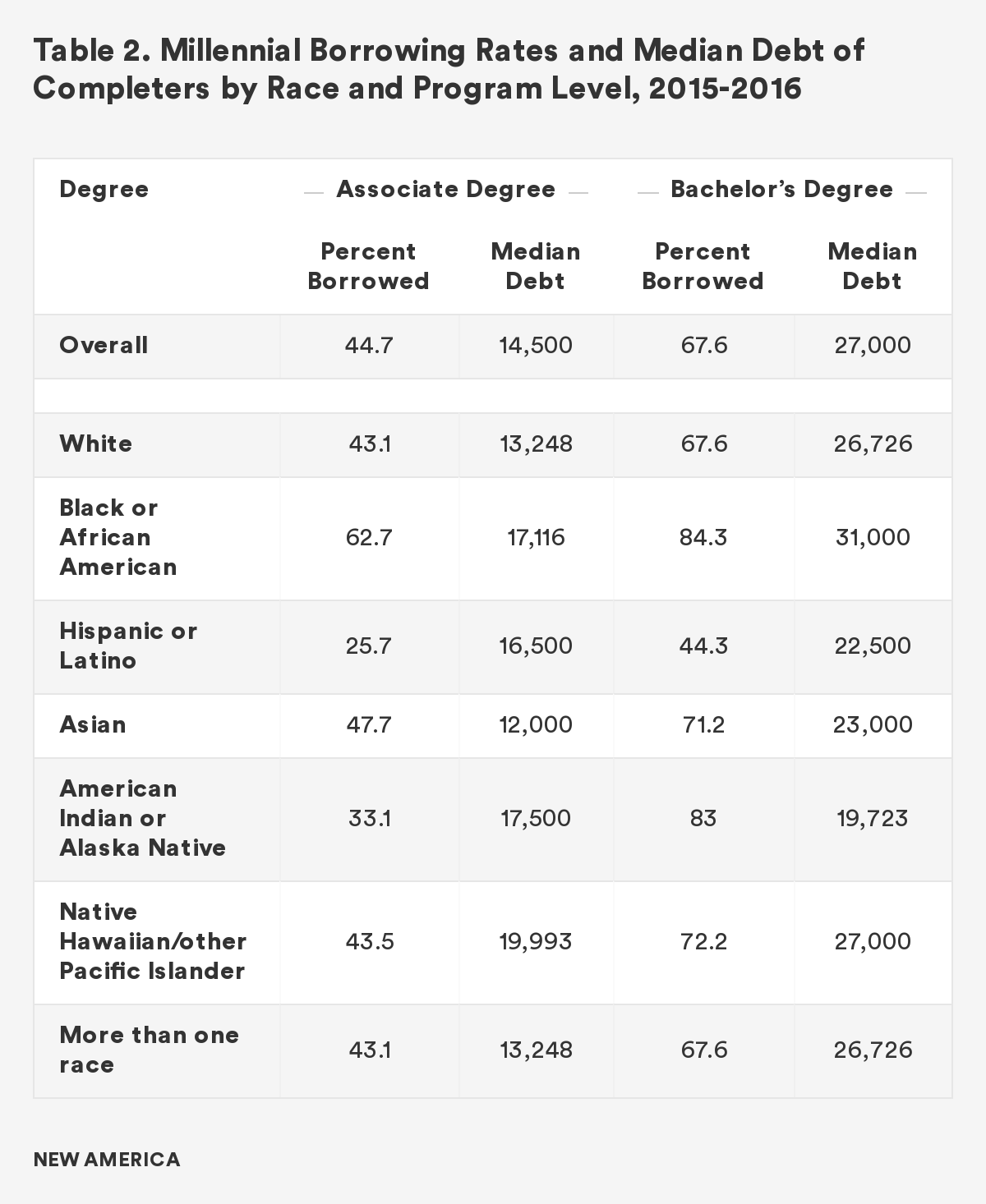

Borrowing trends among racial/ethnic groups can help us understand how debt impacts groups of students differently. Table 2 presents the borrowing rates and the amounts for Millennial graduates by race and ethnicity in the 2015-2016 academic year.

The data shows that Black Millennial graduates are much more likely to take out loans for their education, at a rate 17 percentage points higher than their White peers for a bachelor’s degree and 20 percentage points higher for an associate degree. And Black students borrowed more. This is likely due to the racial wealth gap where Black families have fewer resources on hand than other families. As a result, 31 percent of Black families have education loans compared with only 20 percent of White families, despite the lower college-going rate for Black students than White students.12

Conversely, even though they suffer from racial wealth disparities Latinx Millennial graduates borrow at a lower rate compared with their White peers, especially at the associate degree level.13 Research has shown that Latinx students are more likely to be loan-averse than White students.14 Latinx students also borrow smaller amounts than their White peers, something that can be attributed to White students generally attending more expensive schools.15

Millennial Undergraduate Debt by Gender

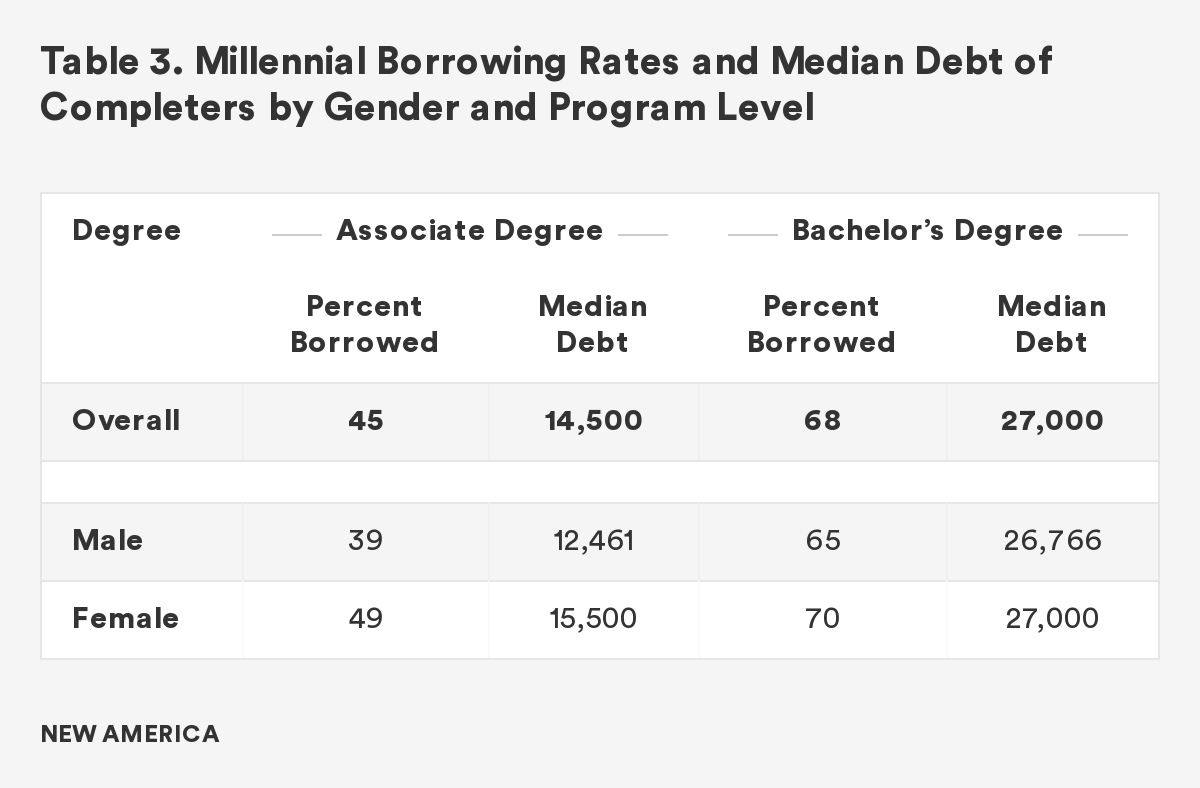

Women are more likely to enroll in college than men.16 Differences in borrowing exist across genders, though they are smaller differences. The median amounts borrowed for a bachelor’s degree are less than $300 apart. Female borrowers also borrow at a higher rate, though only five percentage points higher than males. The biggest disparity is at the associate degree level, where female borrowing is 10 percentage points higher and about $3,000 more total.

Millennial Undergraduate Debt for Low-Income Students

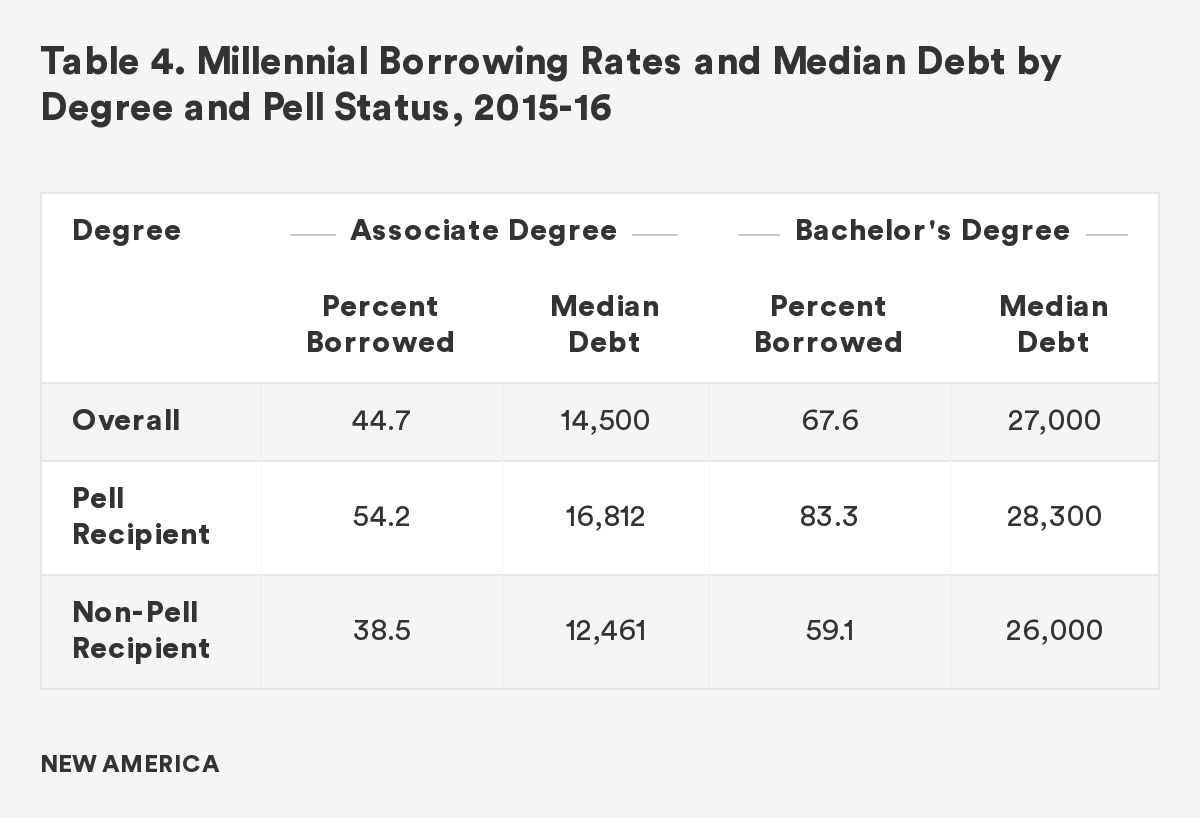

The federal government provides one primary source of financial aid to low-income students—the Pell Grant. Depending on a student’s family income and family size, low-income students can receive a Pell Grant to lower the net cost of higher education. The amounts vary depending on the determined “need” of a student. The maximum grant in the 2019-20 academic year is just over $6,000. Table 4 shows the borrowing rates and amount borrowed for Millennial graduates, broken out by whether students received a Pell Grant in the 2015-2016 year or not.17

In the 2015-16 academic year, students who received Pell Grants borrowed at a much higher rate than their higher-income peers. To earn an associate degree, Pell students borrow at a rate almost 16 percentage points higher. For a bachelor’s degree, the difference is greater, at 24 percentage points. These disparities point to the fact that the Pell Grant has not kept up with the cost of college. Not only do they borrower at much higher rates, Pell students borrow more, reflecting a reality that the grant is not adequately “leveling the playing field” for these students.

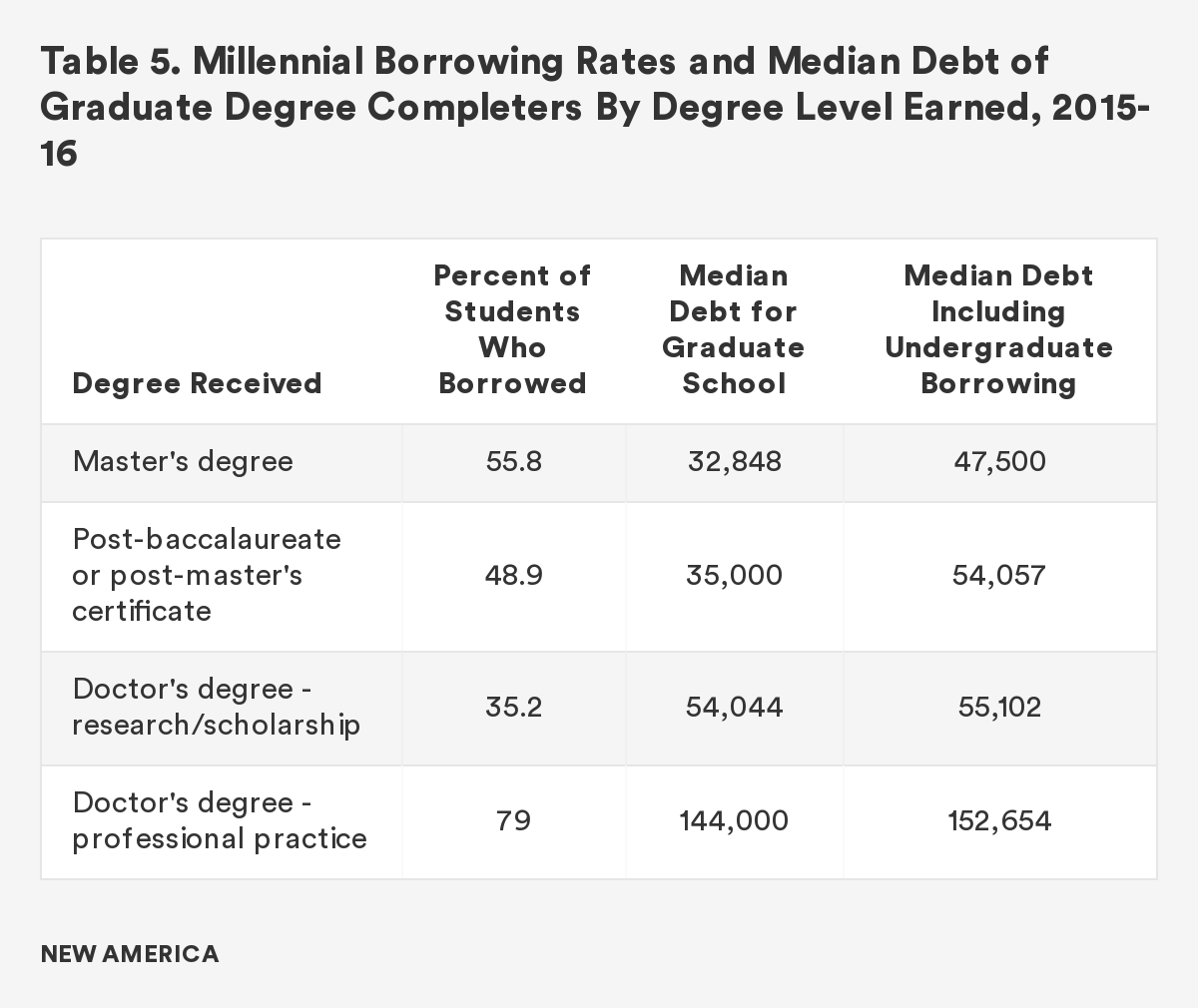

Millennial Graduate Degree Debt

Borrowing for graduate school is another component of Millennial student debt. This is especially true since graduate enrollment greatly increased—as did undergraduate enrollment—during the Great Recession, and has remained steady since. As more students went to college, more also went to graduate school, and increased their debt loads in the porcess. While undergraduate students have strict annual limits on federal loans, graduate students can borrow up to the full cost of attendance as defined by the college—a number that includes tuition, fees, and living costs.

Borrowers who attend graduate school have higher cumulative debt—from both their graduate and undergraduate degrees. Master’s degree students borrow less than those who pursue doctoral degrees, who are usually in school longer.

Although many news stories feature borrowers with high debt loads, often exceeding $100,000, the typical borrower at every graduate education level at the median, doesn’t approach six-figure debt. In fact, only one degree level surpasses $100,000 in student loan debt—professional doctorates. “Doctor’s degree – professional practice” as shown in Table 5 is just a technical way of saying professional school graduates. Those degrees—MDs, JDs, etc.—are the ones who become physicians, dentists, lawyers, and more, and they often end up earning six-figure salaries that ensure they can afford to repay the debt. The next highest level of debt is other doctorates (PhDs), with a median debt of about $55,000. Borrowers with a master’s degree have just under $50,000, on average, including their debt from undergraduate borrowing.

Repayment Outcomes and Defining a Student Loan “Crisis”

Students borrow to attend college in hope of a return on their investment in the form of greater employability and increased earnings. Even though costs for college—and eventually loan payments—can be significant, it can still be a worthwhile investment, particularly considering the alternative of never enrolling in the first place. College graduates see immediate earnings bumps and they earn more over time. Bachelor’s degree graduates earn about $1 million more throughout their lives than people with only a high school degree, and are far less likely to be unemployed or underemployed. This means that for many debt can be both affordable and a good choice.18

One measure of how borrowers are doing in managing their debt is to assess their ability to repay their loans. Most Millennial borrowers are up to date on their payments. According to data from the Direct Loan portfolio by delinquency status, 86 percent of non-defaulted borrowers ages 25 to 34 are current on their loans.19 Five percent are 31 to 90 days delinquent, meaning they are just a little late on their payments, leaving just nine percent of those in this group who are more than 90 days delinquent.

The average balance for those who are delinquent in this age group is about $10,000 less than those who are current on their loans. And the more delinquent the borrower, the lower the average balance on their loans. The average balance for severely delinquent Millennials is almost $20,000 lower than borrowers who are up-to-date on their payments. This indicates that the amount of debt outstanding on a loan might not always reflect the degree of financial hardship to stay current on payments. Most recent data shows us that about 11 percent of borrowers default within three years of leaving school and it is likely that most of them are Millennials.20

$1.5 trillion in student loan debt is a big number and it has grown dramatically in recent years. But is it a “crisis?” Some argue that debts of this magnitude are hindering the economy because borrowers may be unable to spend more elsewhere, are unable to pay their existing debt, or cover their living expenses. However, that misses the varying experiences of borrowers. Some large-balance borrowers may struggle, but they are the exception for high-debt students. Challenges in repaying student loans are much more prevalent among smaller-balance borrowers struggling to manage their finances. Several groups of borrowers who are experiencing particularly acute financial hardship deserve greater attention, and should be the focus of the struggling borrower conversation.

Non-Completers

Quality varies across institutions of higher education. Many colleges and universities would be labeled dropout factories if they were a K-12 school given their abysmal graduation rates.21 Students who enroll in college, but don’t complete, default on their loans at nearly three times the rate as those who do.22 The majority of defaulters (65%) have relatively low loan balances, under $10,000. On average, a college degree pays off for most borrowers—even accounting for cost—as long as they graduate.23 If they don’t graduate, they typically don’t reap the earning premium and can have the most difficulty repaying their obligations. Even if their outstanding balances are below average—sometimes just a few thousand dollars—non-completers are often in greater financial crisis.

Borrowers of Color

Income and wealth inequality are an enduring and cross-cutting problem in the United States, but this is an endemic crisis hitting families of color the hardest. Stemming from historic racism and the legacy of slavery, the racial wealth gap has left borrowers of color instantly disadvantaged when—and even before—they enter higher education.

Black students are more likely to borrow for their education, and when they do, they borrow more. Once they graduate, Black students face a discriminatory labor market paying them less, meaning they often can’t recoup the costs of their degrees at the same rate as others.24 Borrowing more but making less is connected to higher default rates. Research confirms that a Black graduate with a bachelor’s degree is more likely to default on his or her loans than a White student who dropped out of college with student debt—an astounding finding.

Latinx students borrow at a lower rate and borrow less when they do. This may result from a cultural aversion to debt.25 First, this is a problem because it is possible debt aversion hinders Latino students from enrolling in college, or from enrolling in four-year degree programs where their earnings potential will be greatest, making it difficult for those student to build wealth going forward. Secondly, research has shown that some students don’t borrow enough, making them less likely to graduate.26 If students who are more risk-averse don’t borrow enough and end up not graduating, it still leaves them with debt and no degree. They won’t see the wage gains from a college degree and they are more likely to default.

Students of color often attend schools with lower graduation rates, putting them at a greater disadvantage from the moment they enter higher education. One reason for these low graduation rates is that students of color disproportionately attend under-resourced schools, such as community colleges and Historically Black Colleges and Universities (HBCU). And worse, predatory for-profit institutions with dismal student outcomes often recruit students of color to attend them. Thirteen percent of Black students enroll in for-profit colleges, compared with four percent of White students.27

Low-Income Students

Low-income students face some of the struggles that students of color face, and of course some are students of color themselves. Low-income students are less likely to go to college and, as the data show, they borrow at much higher rates to attend college and borrowed more to do so. Low-income students often attend under-resourced community colleges or regional universities that cannot provide sufficient supports to students. On average, low-income students also graduate at a lower rate than their higher-income peers, and at some schools that disparity is massive.28 So these students risk being left with debt and no degree and without family resources to rely on in that scenario.

For-Profit Institutions

Graduation makes students much more likely to repay their debt successfully and the quality of the school a student attends is directly connected to the likelihood a student will do so. The for-profit higher education industry is one rife with problems. The graduation rate for first-year, full-time students—those most likely to graduate—at for-profit, four-year schools was about 40 percentage points lower than at public four-year schools. For-profit schools often charge students more, even in certificate programs, where completion rates tend to be very high as a result of very short instructional programs. In some cases, the costs to students for a for-profit certificate is higher than a comparable program in the public sector, and the payoff can be far lower.29 Beyond poor graduation rates, some for-profit schools have defrauded students by misrepresenting job placement rates; engaged in predatory recruitment practices designed to get students in the door without adequate time to consider their options; and/or operated with unstable finances, causing them to close the doors abruptly leaving students in the lurch. The rise of the for-profit higher education sector has contributed significantly to the rise in student debt and related financial hardship.

What Debt Protections Exist Now?

There are several public programs designed to protect students from having loan payments they cannot afford. In addition to the standard ten-year plan, Congress created options to spread out the length of repayment so that students would have lower payments, especially when they are starting their careers and their incomes may be lower.

Congress also created income-based or income-driven repayment plans, which currently enroll approximately 3.6 million Millennial borrowers. These plans lengthen the periods of repayment and limit payments to a percentage of students’ discretionary income—defined as 150 percent of the federal poverty line for their family size. If borrowers’ wages are not above that threshold, then the government deems their income is not sufficient to pay any amount and the borrower will have a “$0 payment” for that time period. This offers protection when incomes are low or fluctuate. Because payments are income-based, rather than based on the amount of debt to be repaid, balances that remain at the end of the payment period (20 or 25 years, depending on the program) will be forgiven.

Borrowers have other options for loan forgiveness depending on their type of work. For teachers, there is the Teacher Loan Forgiveness program. To attract teachers to work in low-income schools, this program allows the Department of Education to forgive a portion of their student loans. Teachers can receive forgiveness of up to $5,000 after working in those low-income schools for five years. They are eligible for up to $17,500 in forgiveness if they teach math, science, or special education.

Additionally, student borrowers may access the Public Service Loan Forgiveness program (PSLF). Because PSLF was created in 2007, Millennials are likely to be the first generation to take advantage of it. People who choose to work in the public sector often receive lower pay than if they worked in similar positions in the private sector. Congress, seeing the value to the public of having people work in government, public education, and non-profit organizations, created this program to alleviate the debt burden for those borrowers who want to work in public service. After 10 years of working in public service, while making payments under income-based repayment, borrowers are able to receive forgiveness for any remaining balance, tax-free.

Policy Recommendations

Despite these protection programs, many student borrowers struggle financially with repayment. There is a case for additional policy changes to alleviate the financial pain felt by Millennials as a result of their student debt burden. Policymakers should consider pursuing reforms to simplify payment, help non-completers finish their degrees, end the taxation of loan forgiveness, and fix the Public Service Loan Forgiveness Program, and provide more targeted forgiveness to certain groups of borrowers.

Simplify Repayment

Currently, there are eight different repayment plans, including the standard repayment plan, two plans that extend the repayment period, and another five income-based plans. While the plethora of options was meant to meet the differing needs of borrowers, having this many options creates confusion for those entering repayment. Currently, these programs are too difficult to access—especially for those facing hardship. Congress should reduce the number of payment options to future borrowers to a standard ten-year plan and a single income-based repayment plan. Congress should also ease paperwork burdens by automatically recalculating borrowers’ payments each year, instead of requiring annual applications, and automatically placing delinquent borrowers in income-based repayment. These steps will help ensure borrowers are up-to-date on payments by making them more affordable and place them on the path to eventual forgiveness, if needed.

Help Non-Completers Complete Their Degrees

Because non-completers are most likely to default on their loans, strategies should be devised and refined to help them through re-enrollment and repayment. When non-completers go on to finish their degree they are not only less likely to default on—and therefore repay—their loans, but they are more likely to reap the benefits of a higher salary contributing more in taxes and into the economy. The federal government should make sure these students have access to the needed aid and should eliminate their lifetime cap on Pell Grants.

End Taxation of Loan Forgiveness

Income-based repayment programs can be immediately improved by changing their tax treatment. Currently, if a borrower has their loan balance forgiven after the end of their income-based repayment period, the amount forgiven is deemed as taxable income. Since an outstanding balance reflects a chronically low income, this contradicts the goals of the program. As this is a relatively new program, borrowers are just now getting to the end of their loan terms and are receiving this forgiveness. Congress should implement this change as soon as possible to maximize its impact.

Fix the Public Service Loan Forgiveness Program

While the Public Service Loan Forgiveness program is generous (particularly for the highest-debt borrowers), it has had severe problems in implementation. Policymakers should reform PSLF to ensure borrowers are not mistakenly denied benefits they have rightfully earned. The Department of Education should work with the loan servicer responsible for these borrowers to increase outreach and identification of eligible borrowers by using data to proactively identify these public servants. Applying for forgiveness and certifying—or verifying—employment should be simplified and streamlined with an electronic system to process these documents. These efforts can ensure these borrowers are provided the forgiveness they were promised when the time comes.

Currently, PSLF has no limit on the amount of forgiveness for which borrowers can qualify. With expensive graduate degrees in fields like law and medicine, some worry that costs will lead to the elimination of the program. The Trump Administration and House Republicans have proposed to eliminate this program. To ensure its longevity, some—including the Obama Administration—have proposed limiting the amount eligible for forgiveness, either to a specific dollar amount or to undergraduate loans given the increased costs of forgiving graduate loans. Others have suggested providing more frequent forgiveness at periodic intervals over the ten years. This would allow borrowers to achieve some forgiveness even if they choose to work for shorter, but still meaningful, amounts of time.

Provide Targeted Forgiveness

Broad loan forgiveness disproportionately benefits borrowers with graduate degrees, particularly White borrowers in fields such as law and medicine where they earn higher salaries and people of color are underrepresented. Targeted loan forgiveness could eliminate the burden of those struggling most to repay their loans. Too often schools—particularly predatory for-profit schools—load students up with debt but don’t set them on a path toward higher incomes. A solution to address this is to provide relief for borrowers who attended these types of schools—and hold those schools accountable so they stop offering low-value, high-cost programs. If most graduates have unmanageable debt because their degree has failed to get them a good-paying job, then that school or program has failed to do its job and those students should be able to experience some relief.

Students who are delinquent on their loans should have cancellation as an option if it is clear their educational investment is not paying off. This could be targeted to those borrowers who have been forced to rely on social safety net programs like Medicaid, Supplemental Security Income (SSI), or Supplemental Nutrition Assistance Program (SNAP) for a determined number of consecutive years of repayment. If borrowers are living in poverty, the government is likely to never recoup this money, and the strains of debt collection activities may undermine other anti-poverty efforts.

Conclusion

Concerns regarding college costs and debt are legitimate, especially for a generation where many entered the workforce at a time when the economy was weak. However, it is important to understand that for most borrowers with a degree the debt is manageable and affordable. Many people, especially low-income people, rely on student debt to attend college and would not be able to do so without it. Millennials used student debt to become a more educated generation and set them up for the lifetime of benefits a college degree offers. A narrative overstressing the “crisis” of the cumulative loan debt or the rare borrower with six figure debt ignores that success and can have some negative consequences. It can even create anxiety about borrowing that could lead people to avoid college in the first place. There are certainly issues with student debt for specific groups of borrowers, and it is these groups that should garner the attention of policymakers.

Citations

- “Digest of Education Statistics: Table 303.70.” National Center for Education Statistics, U.S. Department of Education, 2019. source

- “Postbaccalaureate Enrollment.” National Center for Education Statistics, U.S. Department of Education, 2019. source

- “Trends in College Pricing: Figure 9, 2018.” The College Board. source

- “Trends in College Pricing: Figure 6, 2018.” The College Board. source

- Fishman, Rachel, Sophie Nguyen, and Alejandra Acosta. “Varying Degrees.” New America, 10 September 2019. source

- “15 Economic Facts About Millennials.” U.S. Council of Economic Advisors, October 2014. source">source

- “Digest of Education Statistics: Table 303.70.” National Center for Education Statistics, U.S. Department of Education, 2019. source

- “Digest of Education Statistics: Table 303.70.” National Center for Education Statistics, U.S. Department of Education, 2019. source

- “Postbaccalaureate Enrollment.” National Center for Education Statistics, U.S. Department of Education, 2019. source

- “Federal Student Loan Portfolio.” Federal Student Aid, U.S. Department of Education, 2019. source

- “National Postsecondary Student Aid Survey.” National Center for Education Statistics, U.S. Department of Education, 2019. source ; The data are from surveys fielded in academic years 2003-2004, 2007-2008, 2011-2012, and 2015-2016. Data are limited to the students who would fall into the appropriate age range for Millennials in each year. Debt was adjusted for inflation.

- Detting, Lisa, et. al. “Recent Trends in Wealth-Holding by Race and Ethnicity: Evidence from the Survey of Consumer Finances.” The Federal Reserve. 27 September 2017. source ; “Postbaccalaureate Enrollment.” National Center for Education Statistics, U.S. Department of Education, 2019. source

- “Latinx” covers both Hispanic non-White and Latino households.

- Boatman, Angela, Brent Evans, and Adela Soliz. “Understanding Loan Aversion in Education: Evidence from High School Seniors, Community College Students, and Adults.” 17 January 2017. source

- Huelsman, Mark. “The Debt Divide: The Racial and Class Bias Behind the “New Normal” of Student Borrowing.” Demos, 19 May 2015. source

- “Postbaccalaureate Enrollment.” National Center for Education Statistics, U.S. Department of Education, 2019. source

- Some borrowers may have received a Pell Grant in other years, but did not due to changed financial or family situations.

- Carnevale, Anthony P., Stephen J. Rose, and Ban Cheah. “The College Payoff: Education, Occupations, Lifetime Earnings.” The Georgetown University Center on Education and the Workforce, 5 August 2011. source

- “Federal Student Loan Portfolio.” Federal Student Aid, U.S. Department of Education, 2019. source

- “Official Cohort Default Rates for Schools.” Federal Student Aid, U.S. Department of Education, 2018. source

- Leonhardt, David and Sahil Chinoy. “The College Dropout Crisis.” The New York Times, 13 May 2019. source

- “Investing in Higher Education: Benefits, Challenges, and the State of Student Debt.” The Executive Office of the President, July 2016. source

- Webber, Douglas. “Is College Worth It? Going Beyond the Averages.” Third Way, 18 September 2018. source

- Scott-Clayton, Judith. “The Looming Student Loan Default Crisis is Worse Than We Thought.” The Brookings Institution, 10 January 2018. source

- Boatman, Angela, Brent Evans, and Adela Soliz. “Understanding Loan Aversion in Education: Evidence from High School Seniors, Community College Students, and Adults.” 17 January 2017. source

- Marx, Benjamin M., and Lesley J. Turner. “The Benefits of Borrowing.” Education Next, Vol. 19, No. 1. source

- “Digest of Education Statistics: Table 306.50.” National Center for Education Statistics, U.S. Department of Education, 2019. source

- Whistle, Wesley, and Tamara Hiler. “The Pell Divide: How Four-Year Institutions are Failing to Graduate Low- and Moderate-Income Students.” Third Way, 1 May 2018. source

- “Fact Sheet: Department of Education Announces Release of New Program-Level Gainful Employment Earnings Data.” U.S. Department of Education. source