The Emerging Millennial Wealth Gap

Table of Contents

- The Emerging Millennial Wealth Gap: Opening Note

- Building Ladders of Success for the Rising Millennial Generation: An Initiative Funded by the Citi Foundation

- Part 1: Generational Wealth and Financial Health

- Framing the Millennial Wealth Gap: Demographic Realities and Divergent Trajectories

- Trends, Origins, and Implications of the Millennial Wealth Gap

- The Millennial Racial Wealth Gap

- The Young and (Economically) Restless: The Nature of Work for American Millennials

- The Financial Lives of Millennials: Evidence from the U.S. Financial Health Pulse

- Part 2: Components of the Millennial Balance Sheet: Assets and Liabilities

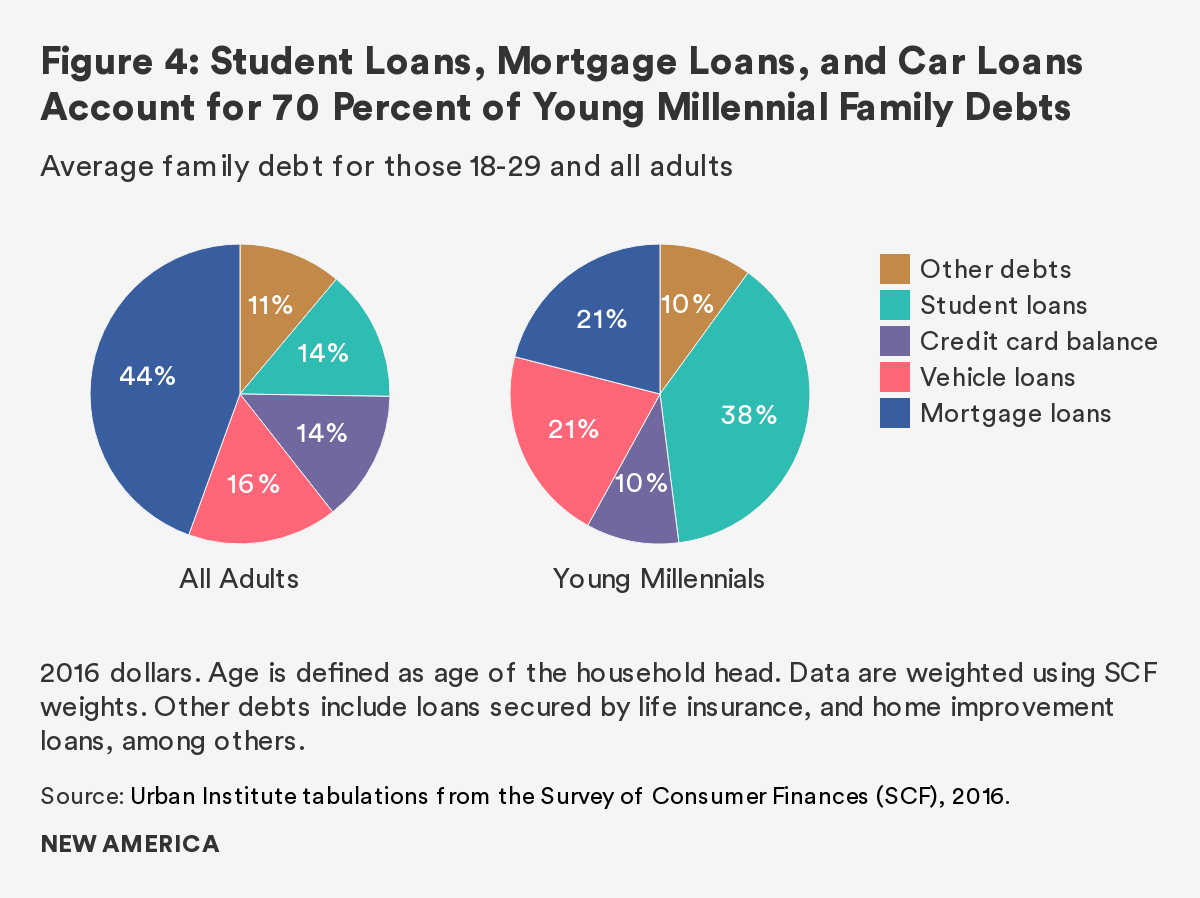

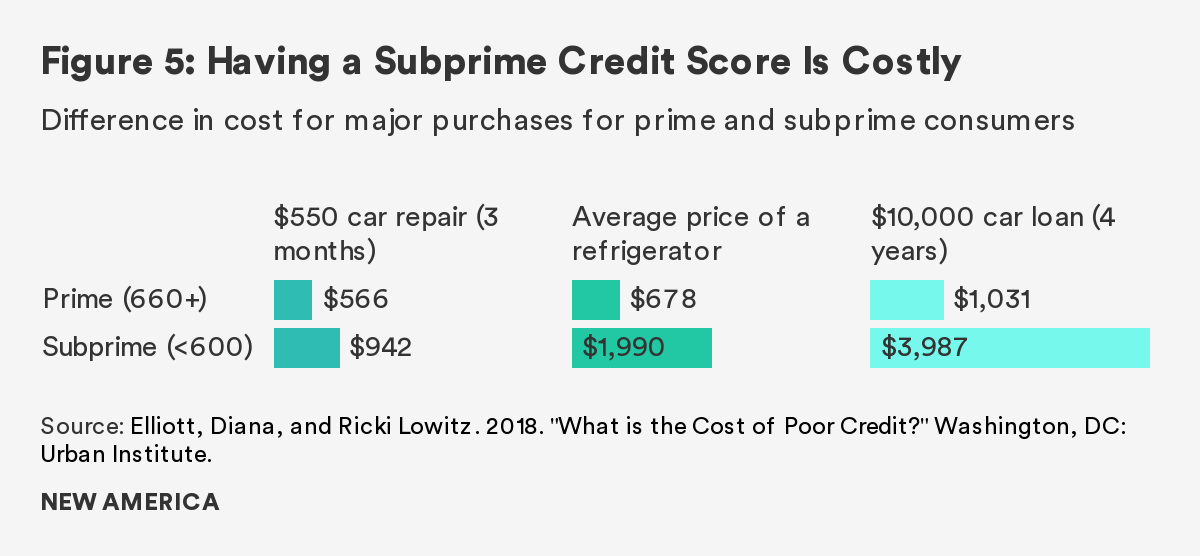

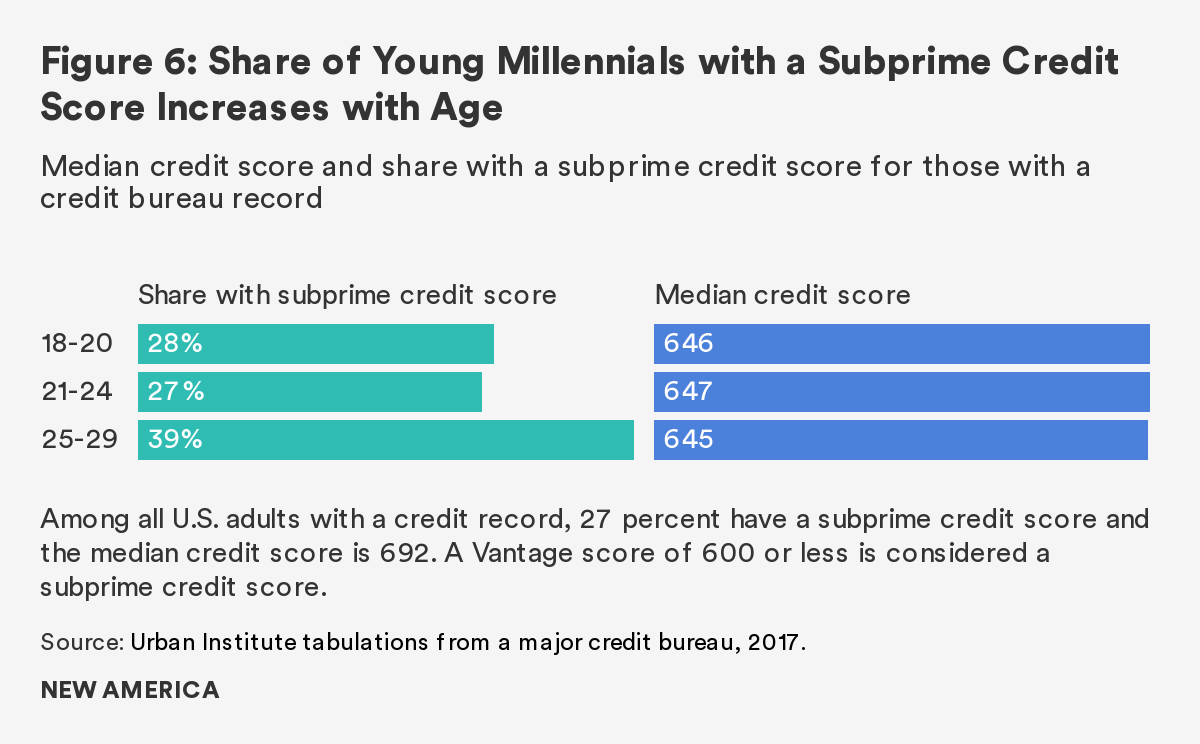

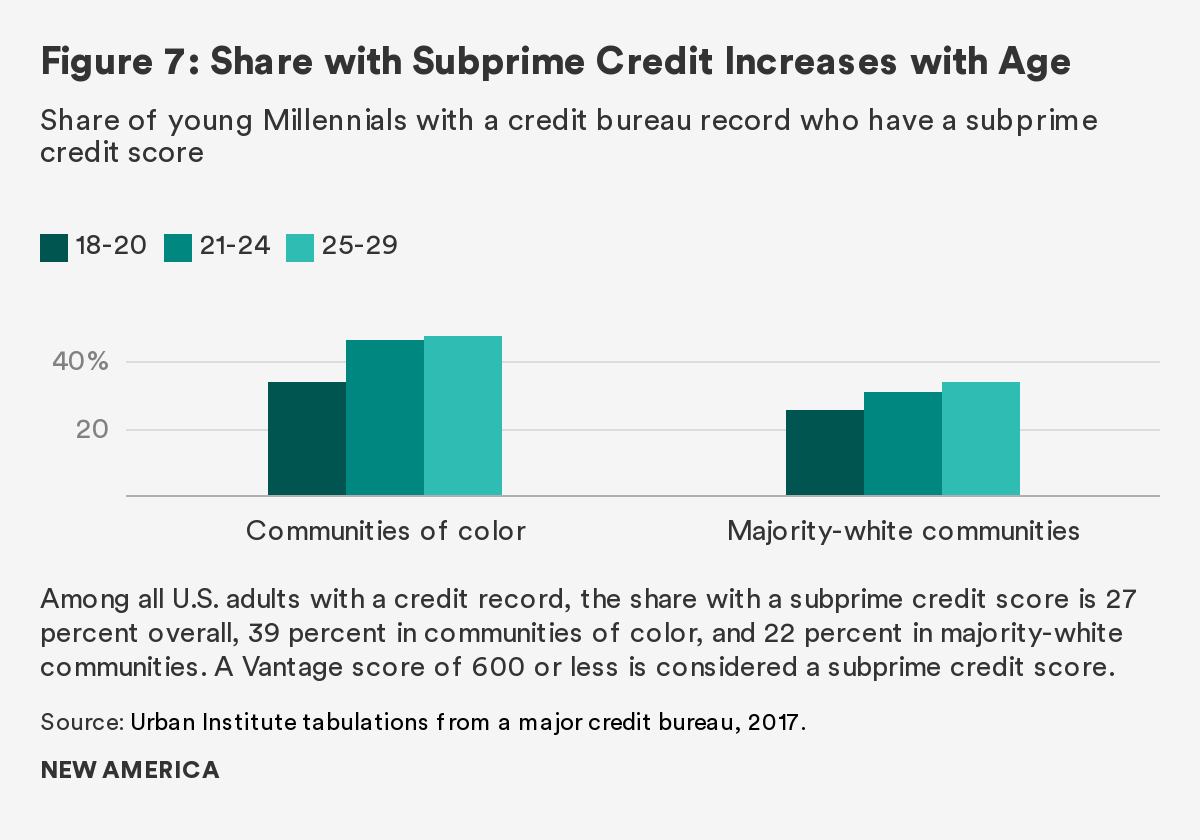

- Wealth and the Credit Health of Young Millennials

- Millennials and Student Loans: Rising Debts and Disparities

- Young Adults and Consumer Debt: The Quiet Crisis Next Time

- Homeownership and Living Arrangements among Millennials: New Sources of Wealth Inequality and What to Do about It

- Part 3: Implications for Social Policy

- Public Policy Implications of the Millennial Wealth Gap

- Addressing the $1.5 Trillion in Federal Student Loan Debt

- Policy Responses to the Millennial Wealth Gap: Repairing the Balance Sheet and Creating New Pathways to Progress

Abstract

The Millennial generation is on a much lower trajectory of wealth accumulation than their parents and grandparents. Dramatically so. Their generational balance sheet, tabulating assets and liabilities, is historically poor. Despite its dramatic emergence and real world consequences, the Millennial wealth gap has received scant attention to date. This publication is an attempt to address that. By examining the data, identifying trends, and exploring the underlying dynamics of the generational distribution of wealth in America today, the authors included in this volume have committed to participating in a constructive policy discourse to address the misalignment between public policy and the lived experience that threatens to undermine the potential of an entire generation. It is time to incubate large-scale policy interventions to respond to the economic vulnerability of the Millennial generation and create new pathways to progress. Absent a concerted policy response, the troubling disparities in wealth and opportunity will persist for years to come.

Acknowledgments

This publication has been made possible by support from the Citi Foundation. Through their Pathways to Progress initiative, they are advancing a range of efforts to expand opportunities for a diverse set of young adults, in the U.S. and worldwide. Julie Hodgson has been an outstanding program officer and thought partner. Her colleagues at the Citi Foundation, especially former President Brandee McHale and current Director of Programs Florencia Spangaro, have been long-term leaders in the field of youth services. Their engagement and encouragement to pursue this project has been greatly appreciated.

I am particularly grateful to the authors whose work is presented in this collection: Fenaba R. Addo, Colleen Campbell, Jung Choi, Brent J. Cohen, Cathy Cohen, William R. Emmons, Matthew Fowler, Thea Garon, Charlotte Hancock, Liz Hipple, Julie Hodgson, Ana H. Kent, Signe-Mary McKernan, Vladimir Enrique Medenica, Genevieve Melford, Ben Miller, Ida Rademacher, Caroline Ratcliffe, Lowell R. Ricketts, Trina Shanks, Wesley Whistle, and Yiling Zhang. Each has contributed their insights, analysis, and time in order to elevate a set of issues impacting the lives of others.

Much of my own thinking on this topic was sharpened as a result of a daylong convening held at the Washington DC office of New America in April 2019. It was an interdisciplinary and cross-cutting day of discussion. Many of the authors initially shared their work there and responded to feedback from a broad array of experts in the room. I would like to acknowledge and thank the participants at the convening: Davide Azzolini, Velvet Bryant, Allie Aquilera DiMuzio, Reginald Exum, Hala Farid, Jennifer Fernandez, Rachel Fishman, Jessica Fulton, Melissa Grober-Morrow, Mark Huelsman, Elisabeth Jacobs, Rob Levy, Jonathan Lykes, Mary-Alice McCarthy, Jen Mishory, Julie Margetta Morgan, David Newville, Sophie Nguyen, Chayenne Polimédio, Mark Schmitt, PJ Tabit, Jonathan Vespa, and Taylor White.

Their collective expertise and critical feedback helped strengthen the final versions of the essays featured here. I’d like to give a special shout-out to Amarins Laanstra-Corn, who served as our rapporteur for the day, and Reniqua Allen, a New America fellow alum who shared highlights from her new book, It Was All A Dream: A New Generation Confronts the Broken Promise to Black America.

The agenda for the convening and this subsequent publication has been shaped by extended conversations with two long-time colleagues, Ray Boshara and Signe-Mary McKernan. For years, I have benefited from their insights. Ray was the inaugural director of New America’s Asset Building Program when he hired me away from OMB in 2003. In the years since he has been a mentor, intellectual partner as well as a friend. Under his leadership, the Center for Housing Financial Stability at the Federal Reserve Bank of St. Louis informs and enriches the public discussion of family finances by producing the most sound and insightful analysis, relentlessly. His whole team deserves our collective kudos. Signe-Mary has been a guiding light from her perch at the Urban Institute, where she has served as a long-term director of the Opportunity and Ownership Initiative. In this capacity, she has had a hand in producing some of the most insightful and reliable analysis of data impacting the economic lives of families, which has provided a foundation for the best type of policy reform discussions—those that are actually informed by evidence.

As this project got under way, I was inspired by the work of a political science professor at the University of Chicago, Cathy J. Cohen. She is the founder and principal investigator of the indispensable GenForward Survey, which conducts policy-relevant public opinion work focused on Millennials and the diverse voices that make up the generation. When she committed her team to the convening, I knew it was going to be a success. I am very pleased to feature their work here and expose more people to their ongoing analysis.

I am especially grateful to Melody S. Frierson, who introduced me to Dr. Cohen’s work, and also was among the most capable project managers I have ever worked with. From 2017 to 2018, she ran New America’s Millennial Public Policy Fellowship program, which produced an impressive body of work that this publication has built upon.

Finally, I’d like to thank my colleagues at New America who assisted with the production of this book as well as the planning and execution of the convening. The competence and poise of our events, communication, and production team is high, and I’d like to specifically thank Maria Elkin, Fuzz Hogan, Angela Spidalette, James Stewart, Narmada Variyam, Alison Yost, Joanne Zalatoris, and Joe Wilkes.

It is a collective task to create a more equitable future, where people can thrive regardless of their economic standing at birth, how long their parents have been in the country, or their membership in any particular racial or ethnic community. This work is dedicated to all those who believe America can do better. We can.

Reid Cramer

Director, The Millennials Initiative

New America

Downloads

The Emerging Millennial Wealth Gap: Opening Note

Reid Cramer

A popular story line took hold only a few years ago, depicting Millennials in America as an ascendant generation. Their parents were attentive, the technology was dazzling, and they grew up optimistic about the future. Along the way some of their elders felt they were coddled and prone to an inflated sense of entitlement and privilege. Yet less encumbered by tradition, they were open to cooperation and more tolerant of differences among their peers. They were poised to seize the day and remake society in their image.

As they have entered adulthood, this narrative picture has crumbled. The generalizations foisted upon them didn’t quite capture the actual diversity and complexity of their experiences. If there is an overarching force coalescing this generational cohort, it is more likely to be their shared sense of economic insecurity, born from coming of age in the wake of the Great Recession.

Even as memories of the recession recede, disruptive ripples launched by the financial crisis continue to upset the economic lives of this rising generation. Although they bore no responsibility for creating the economy, or failing to regulate it effectively, young adults have had to live with the consequences. Just as Millennials approach their prime work and family-forming years, poor finances are complicating how they assemble the building blocks of success. Stagnant incomes, rising debts, and a broadly weakened financial profile have contributed to creating a new story line: Millennials appear unlikely to replicate the economic success of their parents and grandparents. Central to this unfolding era of uncertainty is their relative failure to begin the process of accumulating wealth and assets.

By many measures, America remains a prosperous country—among the richest in the world—and many individuals are thriving financially. While the distribution of wealth has never been equitable—the country was founded with the enslavement of Africans on land previously inhabited by native peoples—there has been a sense of generational progress. A growing middle class and expanding civil rights fostered a widely held belief that prosperity might increasingly be shared. The recent performance of the economy has undermined this expectation. Instead, more Americans recognize that there has been an increasing concentration of resources among those at the top of the economic ladder. As concern about inequality has grown, wealth inequities have been widely acknowledged. Yet less attention has been given to the emergence of a new and generational dimension to wealth inequality. Simply stated, the Millennial generation has less wealth and a poor generational balance sheet. While the income of a typical Millennial is only slightly below levels predicted by the experience of past generations, young adults in America today are on a much lower trajectory in their wealth accumulation than their predecessors. Dramatically so.

One insightful distillation of the Millennial wealth gap and the relative failure of young adults to begin their lifelong wealth building process has been described by scholars with the Center for Household Financial Stability at the Federal Reserve Bank of St. Louis. Using the most comprehensive data of household wealth to compare the net worth of young adults over time, they found that the typical Millennial today holds 41 percent less wealth than a similarly aged adult in 1989. Whether or not this cohort gets back on track or misses out on the experience of wealth building altogether will have long-term impacts and broad ramifications.

A closer look at the data shows how the Great Recession essentially has catalyzed the Millennial wealth gap. While the initial destruction of wealth was widespread, the recovery experience has been uneven generationally. Two particular trends stand out when summarizing the experience of age cohorts in the economy since 2008. First, older households have rebuilt their balance sheets and grown their wealth holdings, while young adults have lagged behind. Second, wealth gains made by Black and Hispanic families over the preceding decades were largely wiped out and have been slow to recover, which has amplified historic inequities and created new sources of inequality. As a result, the overall racial wealth gap has not narrowed over the last 30 years. The gap remains a chasm.

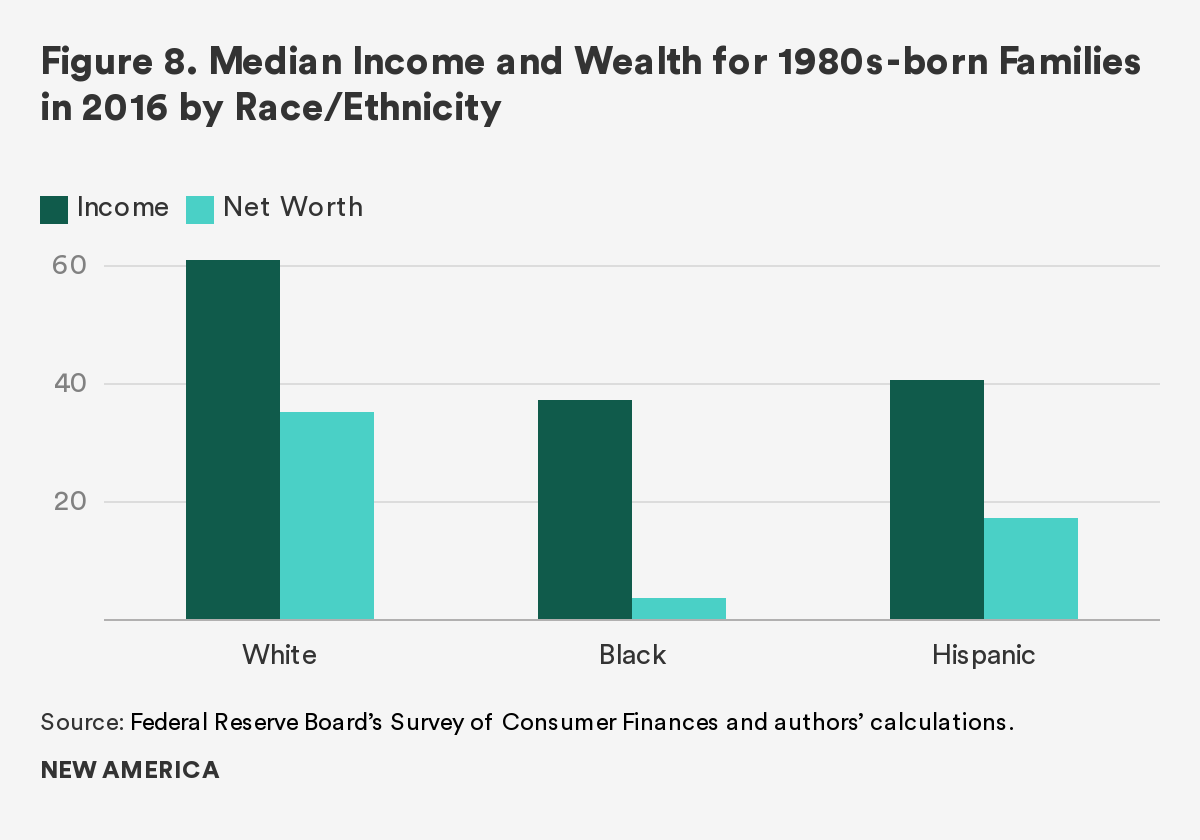

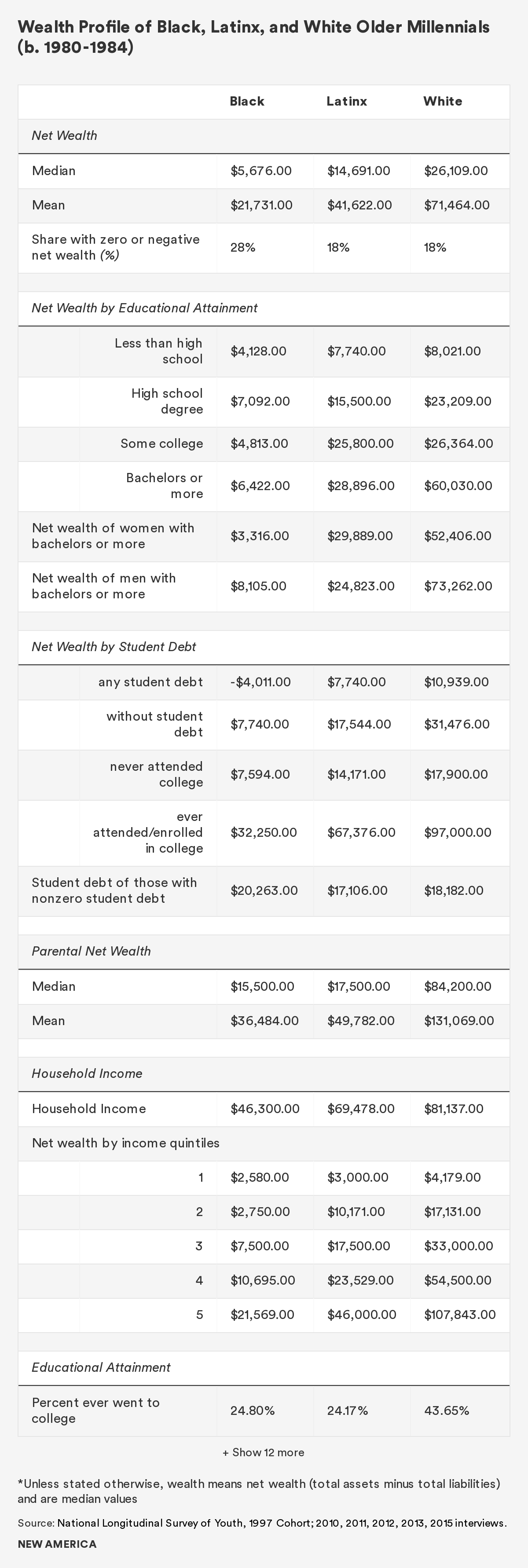

Given the increasing diversity of the Millennial generation—one of its most salient characteristics—the racial wealth gap is clearly exacerbating the Millennial wealth gap. The most recent wealth data from the Federal Reserve shows that the average wealth holdings of the typical Black Millennial are approximately $5,700, compared to $26,100 for White Millennials, while the typical Hispanic Millennial had a net worth of $14,690. And while there are disparities in the distribution of both income and wealth according to race and ethnicity, the wealth gap is wider. Among Black and White Millennials, wealth inequality was 2.6 times greater than income inequality, according to the most recent data; among Hispanic and White Millennials it was 1.5 times greater. These findings should motivate increased scrutiny on the role of race and ethnicity in the emerging Millennial wealth gap, and focus attention on solutions to address it.

Unfortunately, there is a growing disconnect between the economic conditions the diverse generation of Millennials face and their government’s response. This misalignment between public policy and lived experience threatens to undermine the potential of an entire generation, and handicap the next. This is because Millennials are not just the future—they are already powering our workforce, steering our economy, and poised to exert their influence as the largest generation. Perhaps most significantly, they are the ones deciding if, when, and how to start families, and will be assuming responsibility for raising the country’s most prized resource: the children of the next generation. We all have a stake in their welfare.

Guiding Insights

Despite its dramatic emergence and real world consequences, the Millennial wealth gap has received scant attention to date. This publication is an attempt to address that. By examining the data, identifying trends, and exploring the underlying dynamics of the generational distribution of wealth in America today, the authors included in this volume have committed to participating in a constructive policy discourse. Collectively, we seek to promote policy reforms capable of responding to current conditions and expanding access to viable pathways to progress. In this opening note, a few of the primary ideas, assumptions, and aspirations that have guided this inquiry will be clarified.

Wealth is a Foundation for Economic Security

In the pantheon of economic variables, income is revered. It attracts attention because it represents the flow of resources into a household and correlates closely with consumption of other resources, such as food and housing. It’s also easier to count. But besides the flow of money, having a stock of economic resources matters a great deal for a household’s welfare. Access to wealth—in the form of savings, assets, and even access to credit—is one of the most impactful variables determining long-term social and economic outcomes.

Wealth takes many forms. Tangible and intangible. Real and unrealized. Values change over time and can fluctuate arbitrarily. Yet savings and assets also can accrue over time, as can debt and liabilities. Studies of household wealth often use net worth as a proxy because it is the amount left over after liabilities are subtracted from the market value of assets. While wealth and net worth are harder to track than income, and are subject to external market forces, the overall condition of one’s balance sheet can create opportunities or obstacles, impacting a person’s life and work choices.

Wealth is a key to financial security and economic mobility for a number of reasons. It has an insurance function that can be activated to smooth over unexpected income fluctuations, respond to emergencies, and avoid debt. Wealth also has an investment function: it can be strategically deployed in ways that trigger future benefits, such as paying for tuition, making a down payment on a home, capitalizing a small business enterprise, or buying into other enterprises that can become more productive and increase in value. Although wealth connotes luxury, it is shorthand for things of value, and is most relevant to those who have less.

Income can be a source of wealth in the sense that income not immediately consumed becomes part of the stock of resources that can be available for later use. It is this extended time horizon which makes wealth unique, and confers it special properties. Research pursued in the last 20 years has identified a number of significant “asset effects” that can accrue to the holders of wealth.1 Research confirms that even small amounts available at key moments can make a difference, and can be especially valuable to those with low incomes living in poverty.2 One of the most significant asset effects is how owning financial assets can trigger a sense of economic security and promote mental health that facilitates the ability to plan for the future. Conversely, those with low or no access to wealth are by definition financially insecure, limited in many ways from participating in the economy and reaching their full potential.

The study of wealth and economic security opens up a window to consider what impacts the generational balance sheet. Changes in net worth can be linked to business cycles of the economy, behavioral trends at the household level, and the revision of public policies, such as levels of taxation and subsidies. Beyond individual households, aggregate net worth trends can identify patterns of wealth holding among groups of people, revealing degrees of equity. This applies to racial and ethnic groups, regions of the country, and even generations. There should be widespread special concerns if large groups of people or communities are unable to access wealth or begin an extended asset building process.

Wealth Building Public Policies Should Match the Life Cycle

By its nature, wealth building is a long-term process. In fact, many benefits compound over time and are often realized at a much later date than when initially acquired. For many families, there is a distinct life cycle pattern to wealth holding in America, and we should aim to match public policies to promote wealth building with distinct stages of the life course.

Most young adults start out with negligible savings. As they begin to form households and grow their earnings during their 30s, their assets start to modestly grow, before accelerating into the 50s in preparation for retirement in the late 60s. This is what’s typical. Median wealth figures describe those precisely in the middle, with half having more and half having less. There are many who don’t own anything and never will accumulate much wealth. Still, these patterns of generational wealth building, and changes since the Great Recession, offer clues to the moments in the life course that are associated with greater potential for wealth accumulation.

This approach creates a window to think more generationally. Evidence abounds that contemporary finances have altered life choices and shifted previously prevalent milestones of adulthood. For instance, fewer young people today are getting married, forming households, buying homes, and having children. Some of these socioeconomic trends may have begun before the financial downturn took hold, while others have been intensified by it.

Especially for young adults, there are key moments in the life course that have long-term impacts on economic outcomes. These include moments such as the birth of a child, pursuing an education, entering the workforce, forming a household, starting a family, and even the end of life. Public policy can be designed to take advantage of these moments. There is a special role for public policy to support young families at the time when they are raising children. Unfortunately, this is precisely when the feeling of financial stress is greatest. Similarly, the prime work years are economically formative, and exert a strong influence on longer-term trajectories.

Generational Fairness is Part of the Social Contract

Just as with families, our society is bound together by mutual obligations among the generations that form the basis of an implicit intergenerational contract. Different generations support each other depending upon where they are in the life course. Children depend on their parents, the elderly are assisted to age with dignity, and there is an expectation that each generation can do better than the last.

The emergence of the Millennial wealth gap presents a particularly acute challenge to the concept of “generational fairness.” With persistently poor finances, Millennials are having difficulty assuming their responsibilities. If the young adults raising families and powering the workforce feel they are shouldering more burdens than they can handle financially, basic assumptions about social responsibility may be upended. There is a collective interest in ensuring that sufficient generational assets are available to Millennials to meet their obligations.

Previously, conceptions of the intergenerational contract informed what government could and should be able to do. Societal assumptions are actually codified in public policy. At times people contribute by paying taxes, and at other times they receive benefits based upon their place in the life course. There are expectations that our government will provide support for us when we need help the most. Often these benefits have been delivered as incentives to employers to pass along to their workforce. Yet over the last 30 years, there have been a series of policy shifts—in areas such as health care and retirement—that have transferred the responsibility for managing economic risks from employers and government to individual households. Increasingly, families are expected to build up resources to meet their individualized responsibilities. This risk shift has raised the stakes for wealth building, both for individual households and among generations.

A comparative cohort analysis of wealth trends reveals clear tensions, both economic and cultural, which have the potential to trigger a larger political reckoning that will play out in policy debates. The Millennial wealth gap may increasingly become the context for calls to cut benefits for the elderly or address the level of debt passed on to the next generation. Despite inherent tensions, a more constructive approach is to design policies that address concerns of both the young and the old. In doing so, a number of choices will have to be made to address equity imbalances, distinguishing among different types of households and incentivizing certain types of behaviors. Given current trends and our national history, issues of race and ethnicity should be broadly assessed. If fairness and equity receive proper attention, social and economic justice will be included in the discussion, creating an opportunity to consider reparations. Policy choices can and should be made that will impact the distribution of resources, implemented with changes in taxation and subsidies. The goal should be to rebuild and rebalance the intergenerational contract by taking account of generational fairness and reciprocity, as well as fairness in the distribution of wealth and power.

Policy Should Align with Millennial Attitudes and Preferences

In designing policies that are capable of responding to mounting generational challenges, it matters how those affected think about current affairs and participate in the political process. In the years ahead, Millennials will lead shifts in public opinion, creating opportunities for large-scale policy change. This creates an imperative to develop policies that can respond to contemporary conditions and align with the prevailing attitudes and behaviors of the rising generations.

With preferences that diverge from those of older Americans, Millennials have already had an impact on a number of social-issue policy debates—such as marijuana legalization, gun control, and gay rights. However, as a cohort, Millennials remain skeptical of political parties; 44 percent identified as political independents in 2017, far exceeding GenX-ers (39 percent) and Baby Boomers (32 percent).3 Although Millennials are not monolithic in their political beliefs, as a group they tilt toward the liberal side of the political spectrum. When “lean” is considered in survey answers, more Millennials associate themselves with the Democratic Party (59 percent) than the Republican Party (32 percent); the 27 percent spread exceeds those for GenX (6 percent) and Boomers (2 percent).4 Yet only 49 percent of Americans ages 18 to 35 voted in the last presidential election, compared to about 70 percent of Boomers.5

In crafting a policy response to the Millennial wealth gap, it will be necessary to consider the contemporary political dynamics which are shaping the policy discourse and influencing the extent of their future political participation. There’s little doubt that the current political moment presents major challenges in crafting a Millennial public policy agenda. Chief among these is the prevailing political polarization that has weakened the norms of governance and poses significant obstacles to policy reform efforts. Still, there is value in the task of identifying durable policy solutions that respond to current conditions and can be effective when implemented at scale.

This will be particularly relevant during the unfolding presidential campaign of 2020, which will drive discourse and set the course for future policy changes. The extended campaign season will create an opportunity for new ideas to emerge that might gain momentum. Accordingly, it is a time to incubate large-scale policy interventions and a broad agenda to address the issues faced by the current generation of Millennials as well as those who will come next. Absent a concerted policy response, the troubling disparities in wealth and opportunity may persist for years to come.

Guide to the Volume

Exploring the connections between wealth and financial health, the first section of this book uses a generational perspective to clarify how large cohorts of Americans are indeed on different trajectories, reflected in their financial profiles. My opening chapter seeks to frame the inquiry by establishing a set of reference points for a generational analysis and describing some of the prevailing demographic realities shaping the Millennial generation, including the extent of their relative diversity and how their group experience is diverging from those of their predecessors.

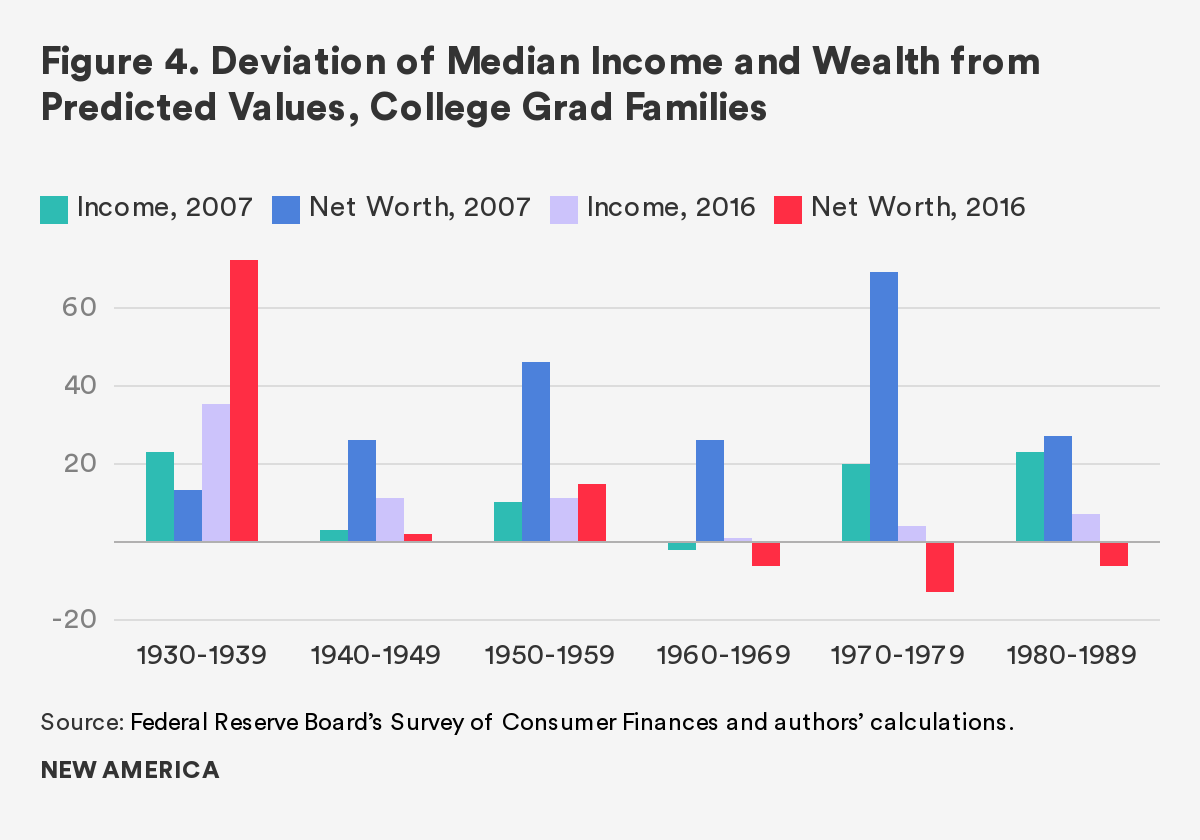

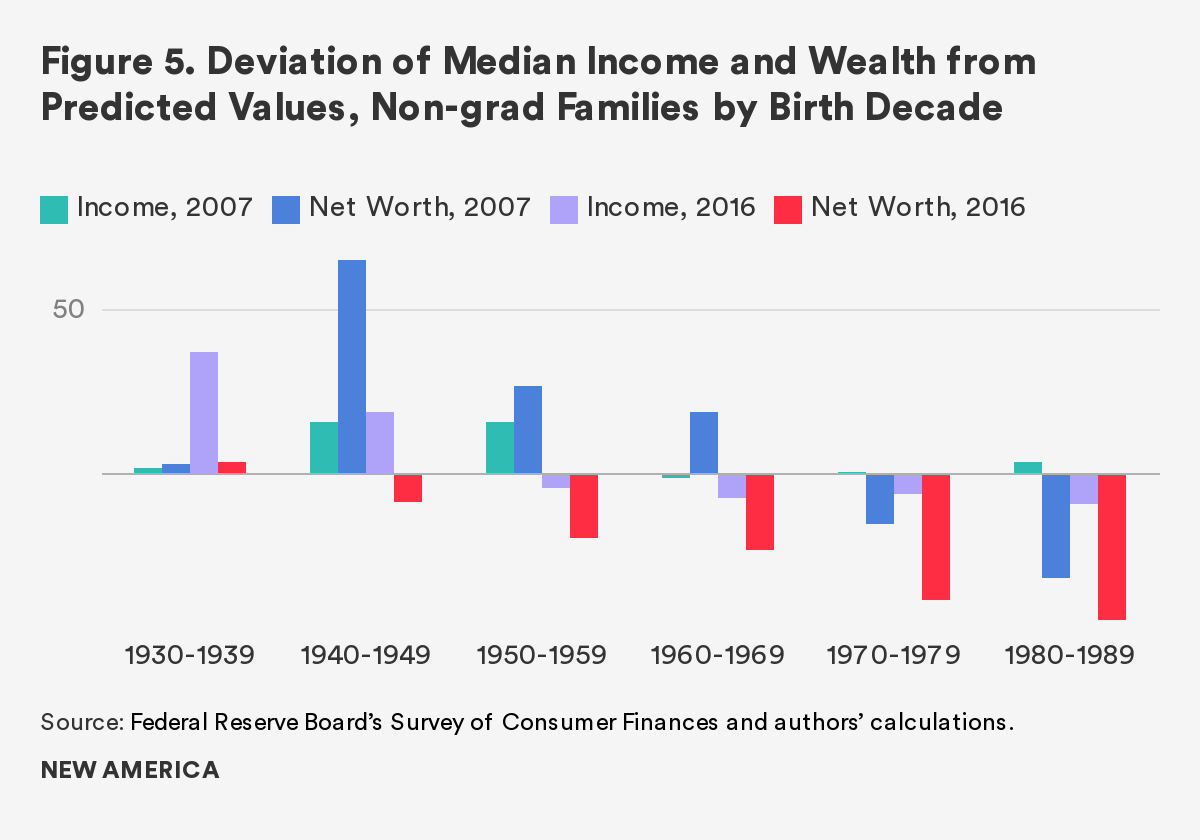

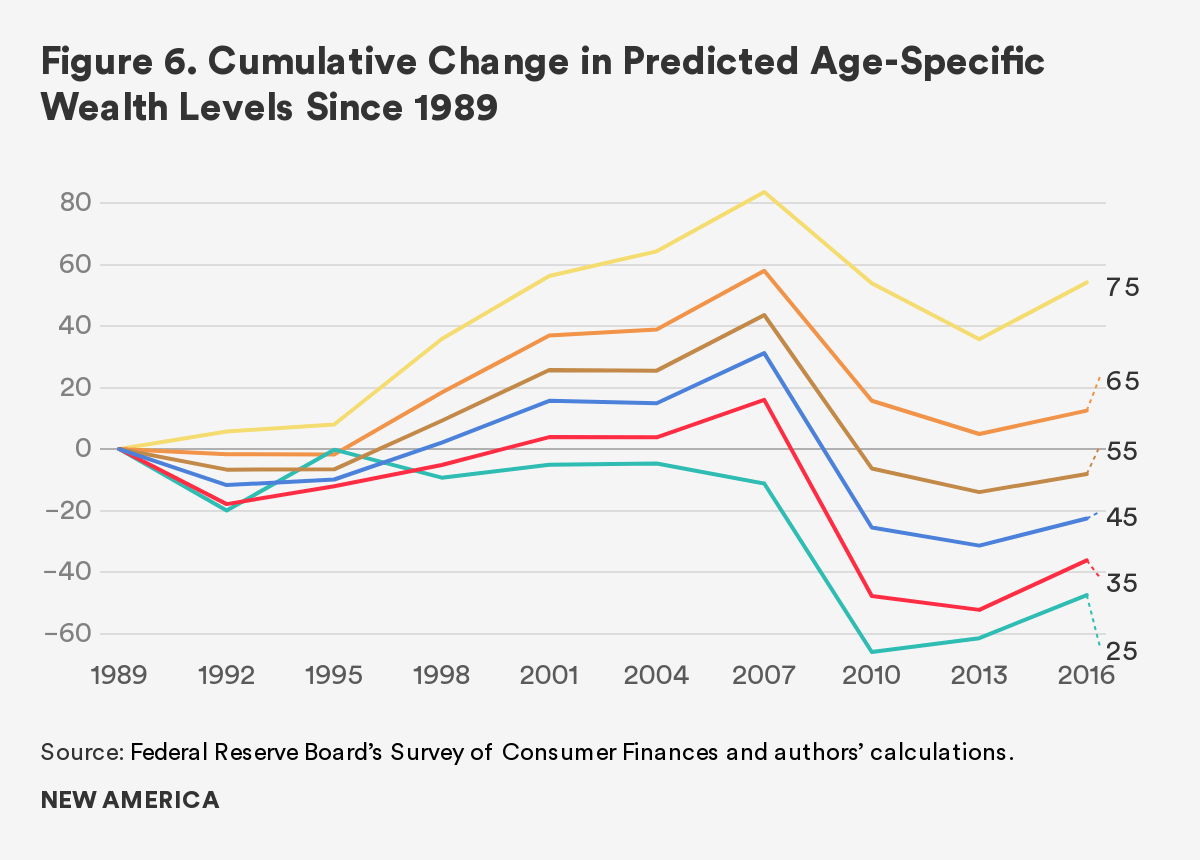

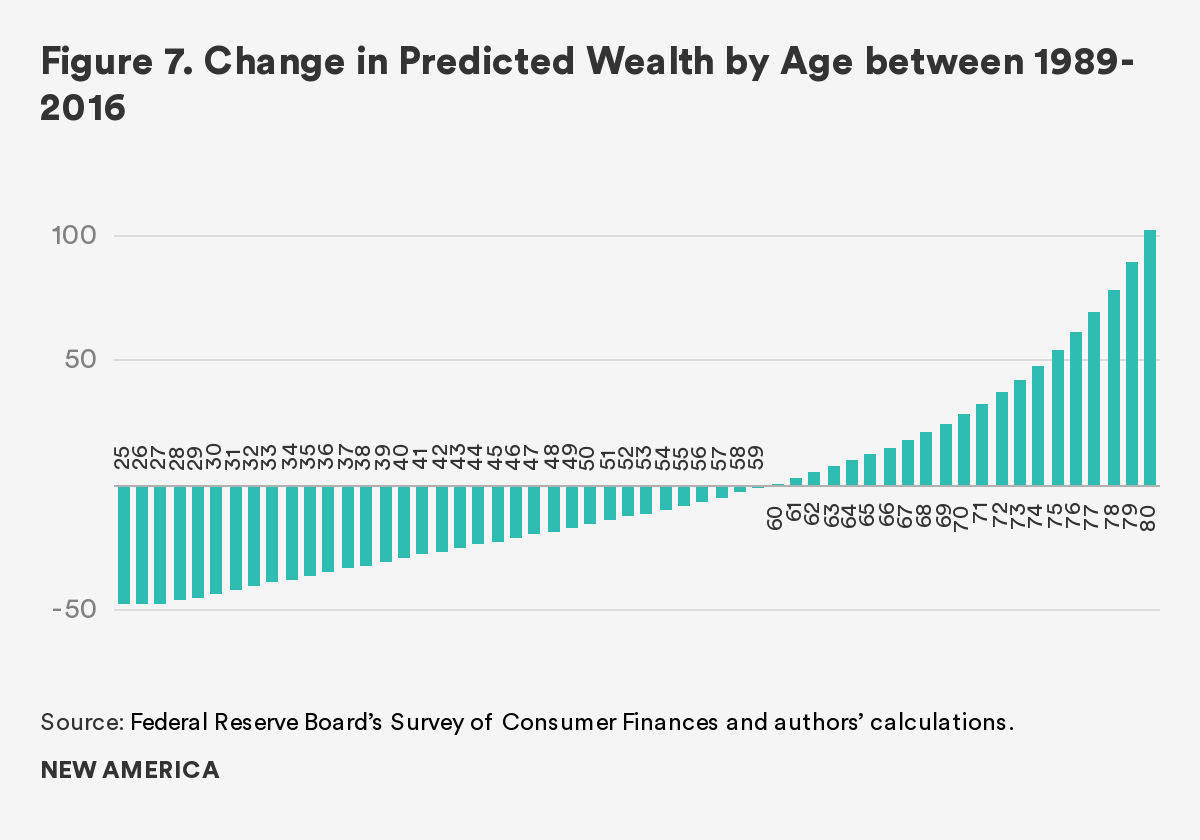

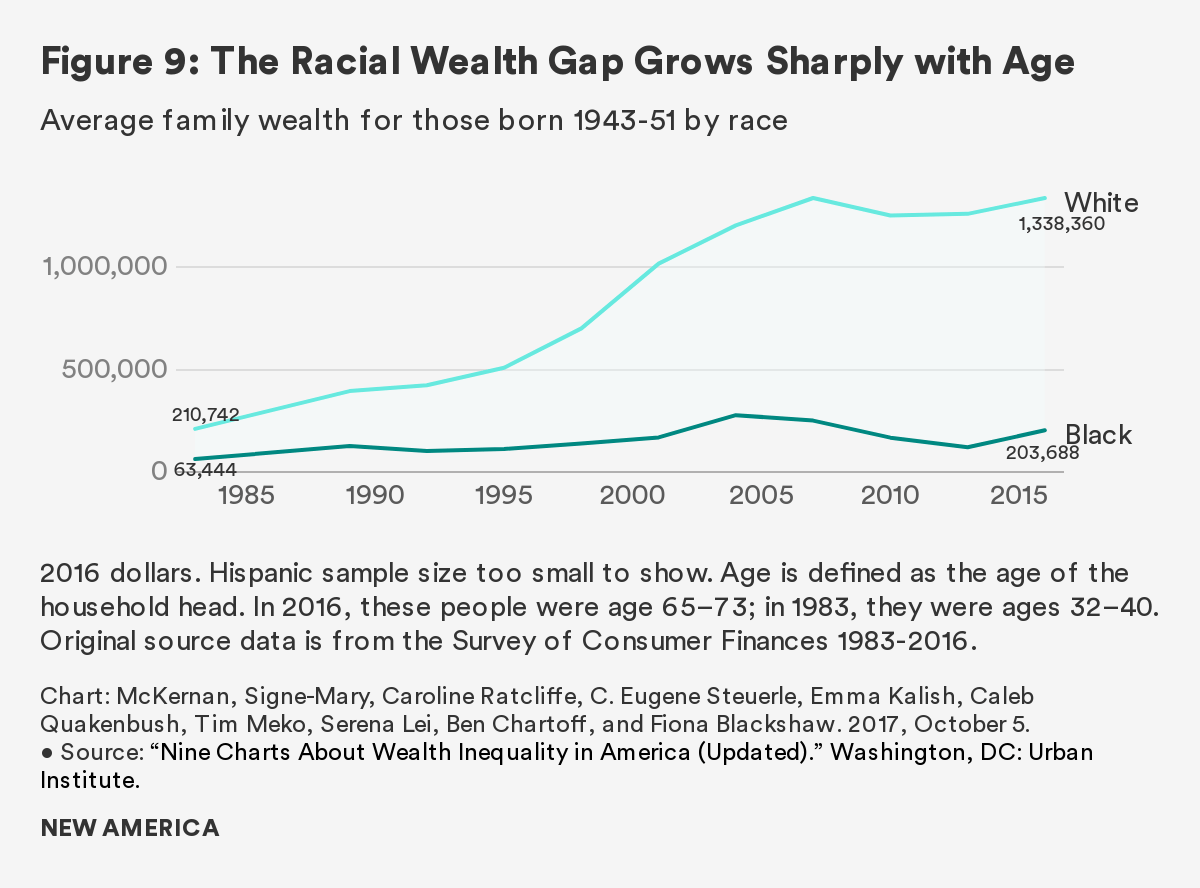

The two chapters that follow offer insight into the most prevalent wealth trends as they are playing out generationally. William Emmons, Ana Kent, and Lowell Ricketts of the Center for Household Financial Stability at the St. Louis Federal Reserve Bank present an innovative analysis of age and net worth. Working with the most comprehensive wealth data supplied by the Fed’s Survey of Consumer Finances, they are able to compare the amount of wealth we expect a typical young adult to have accumulated, given past performance of the economy, against what that typical young adult actually owns. The results are striking. Not only are Millennials behind previous cohorts, but they demonstrate how older households are faring particularly better. This move of equity up the generational ladder represents a profound shift in the distribution of wealth, raising a number of policy questions.

Another striking trend is the erosion of wealth held by families of color and the persistence of the racial wealth gap that many had expected to close in the post–civil rights era. Instead, this gap endures. Fenaba Addo and Yiling Zhang, scholars at the University of Michigan, innovatively describe several vital manifestations of the racial wealth gap, with a focus on young adults. Recognizing that racial wealth inequities have been a central feature of American history, they show how they have been reproduced and actually extended among Millennials in recent years. Their findings are sobering and should motivate a deeper consideration of ways policy might respond. They offer additional insights into key drivers of these outcomes, specifically through pathways that include relative access to higher education, degree completion, and marriage to others with education and economic resources.

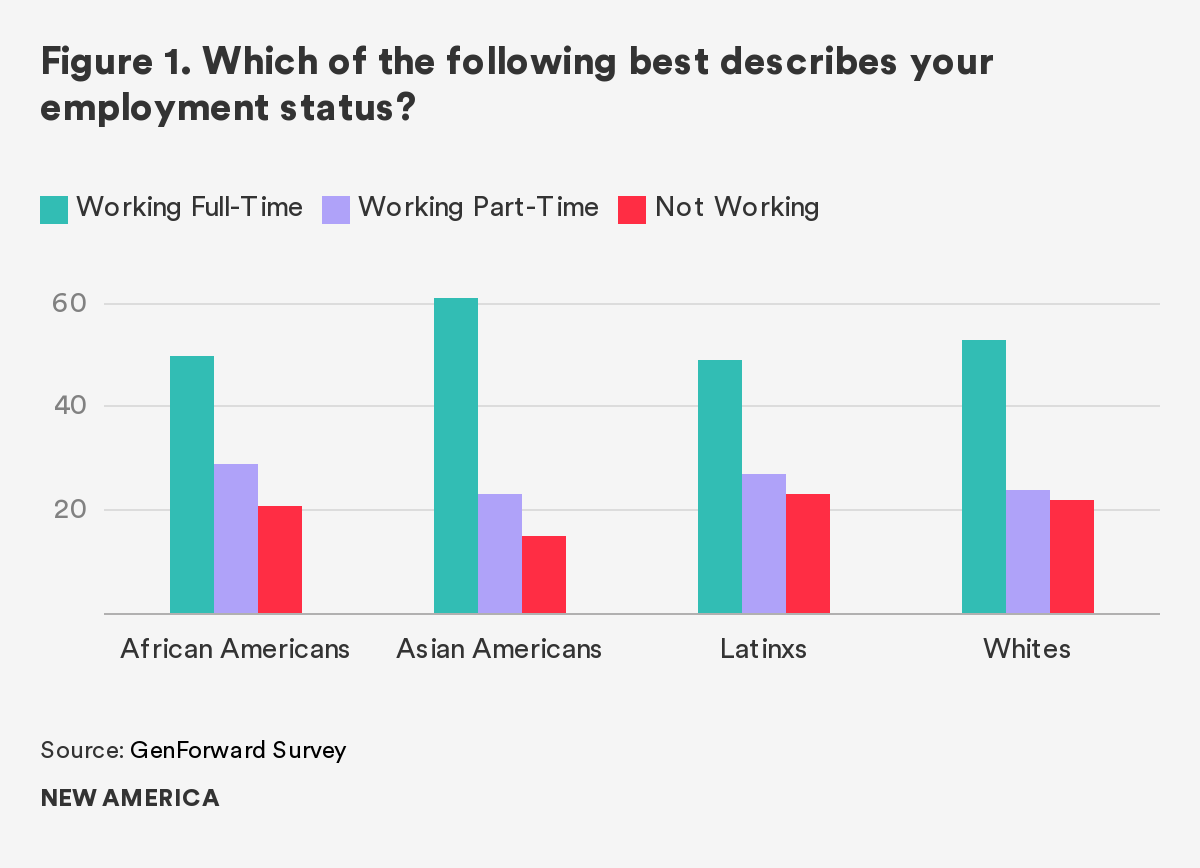

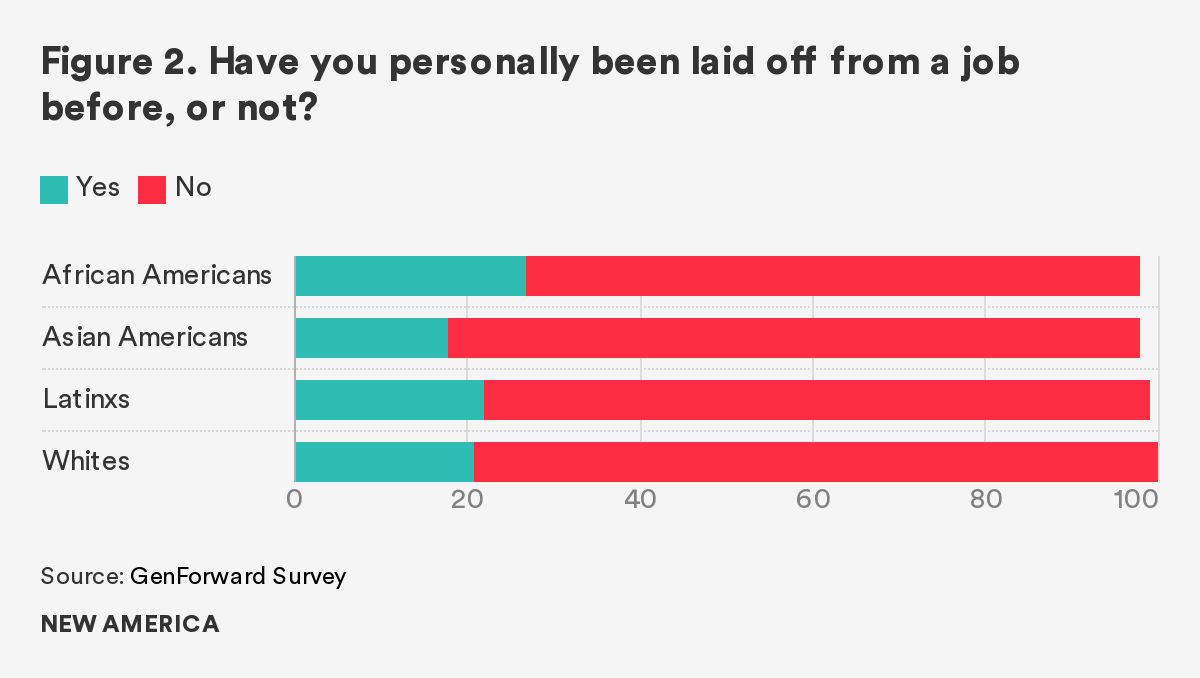

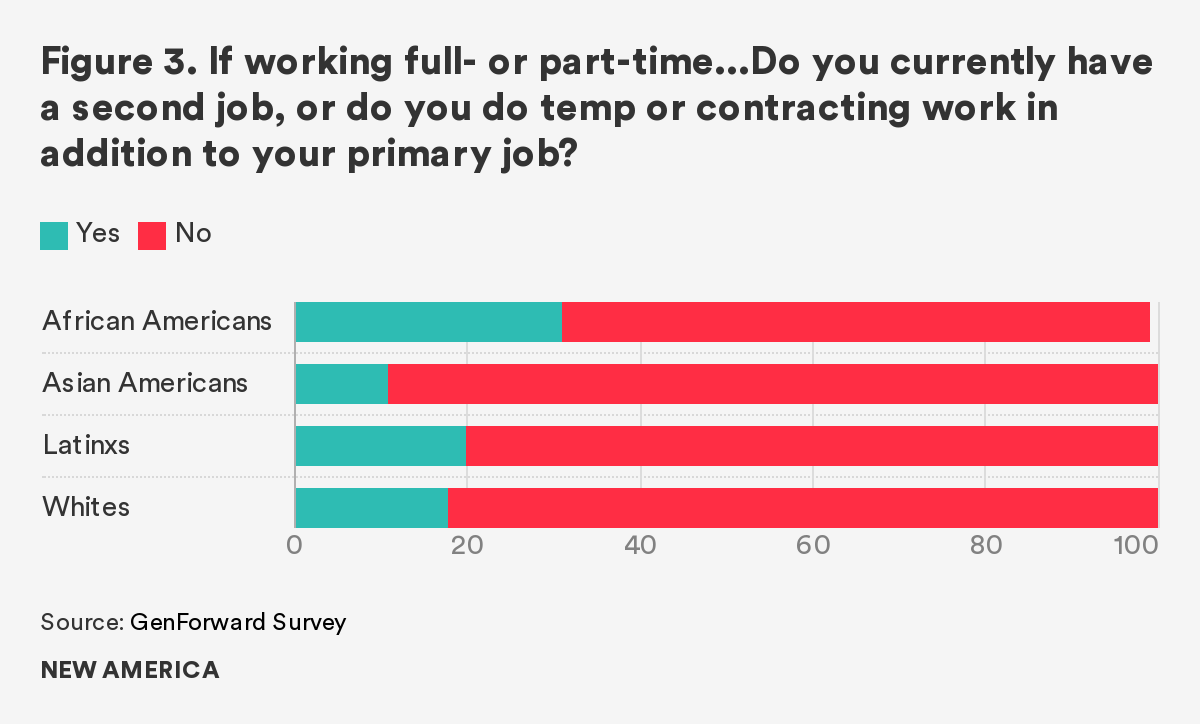

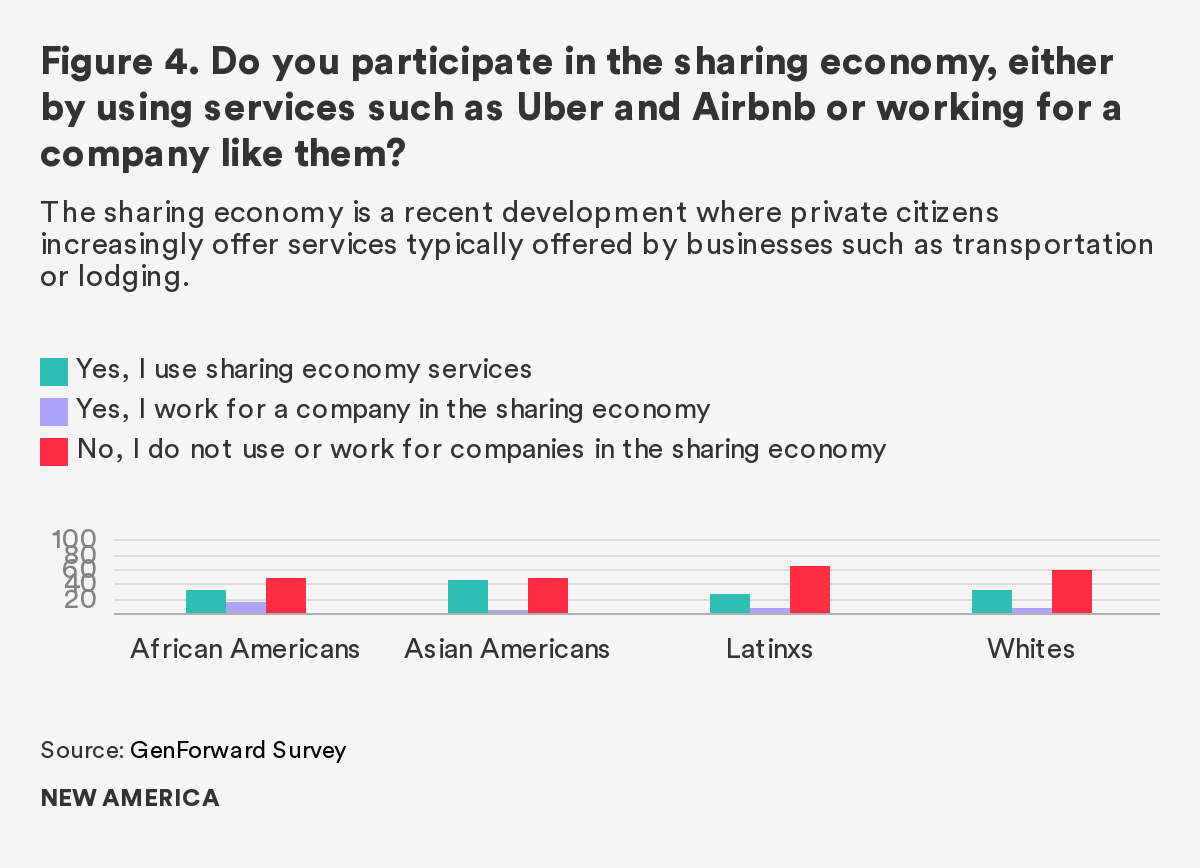

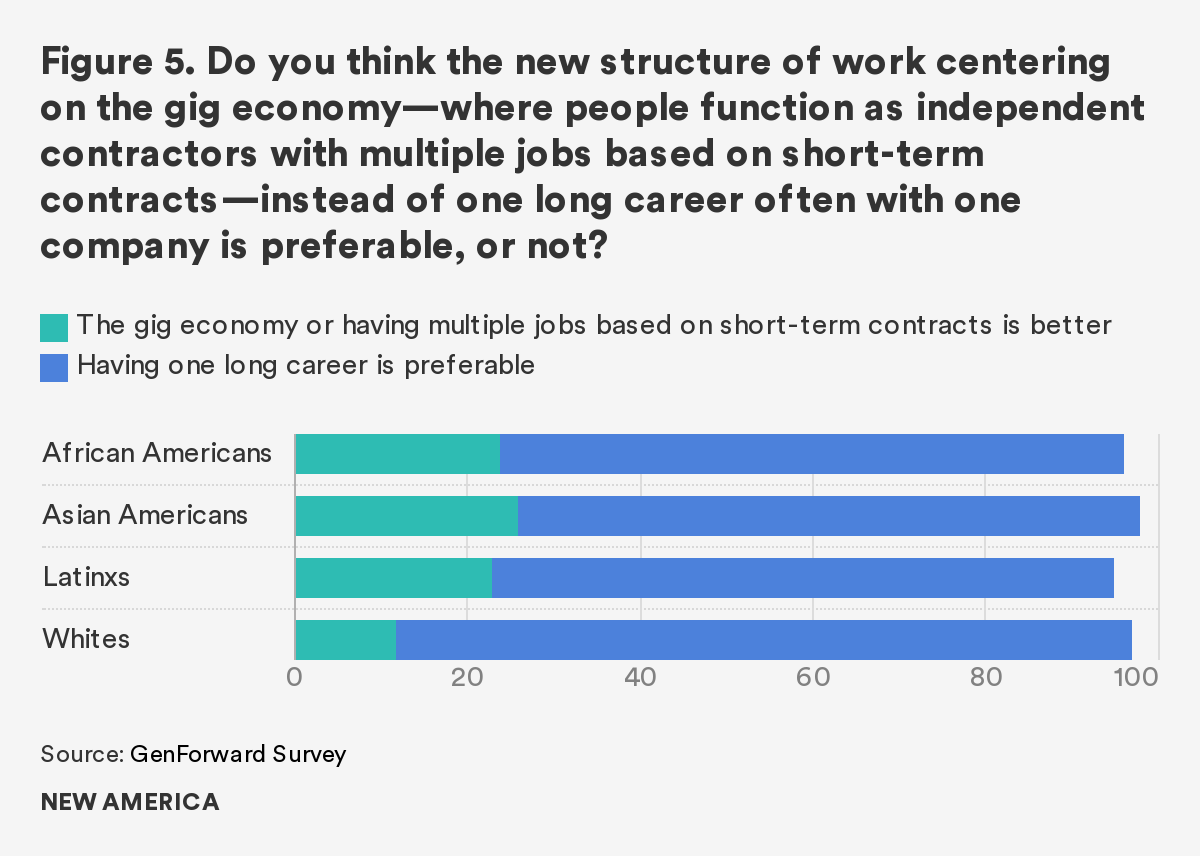

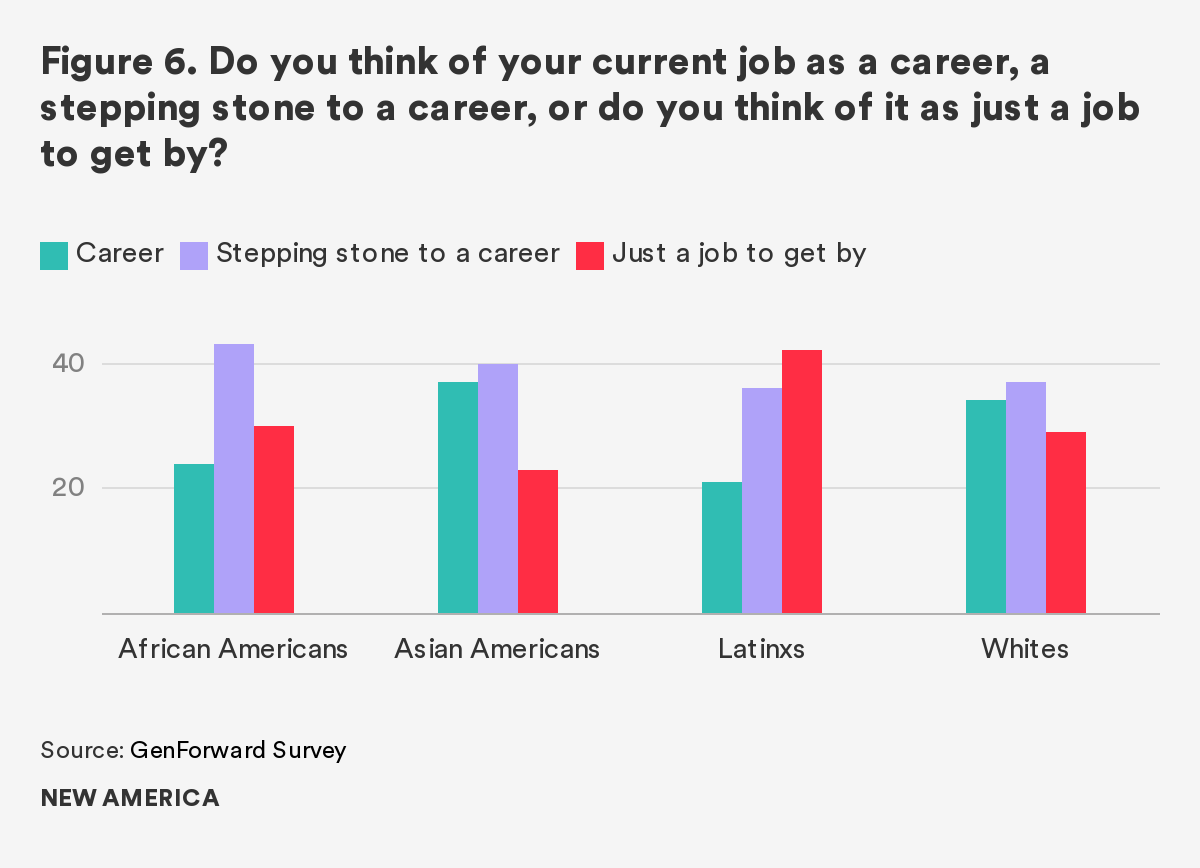

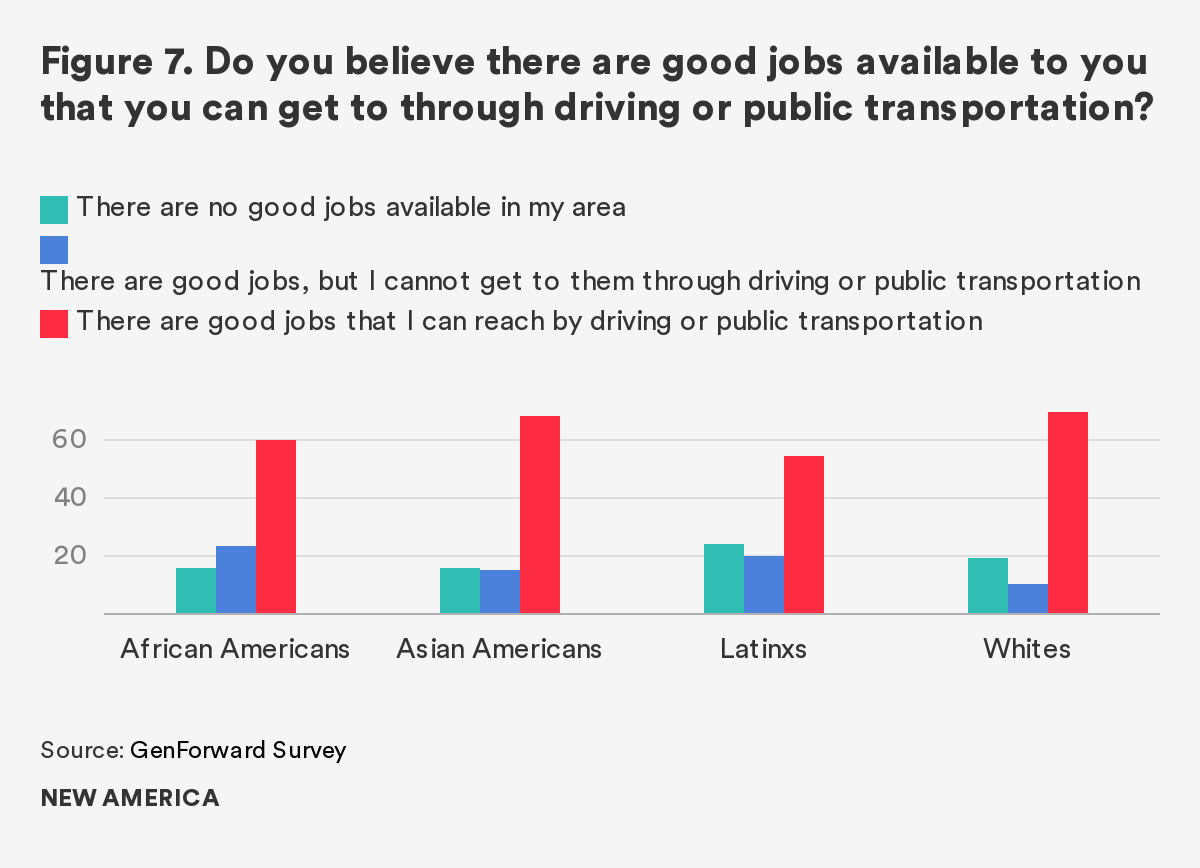

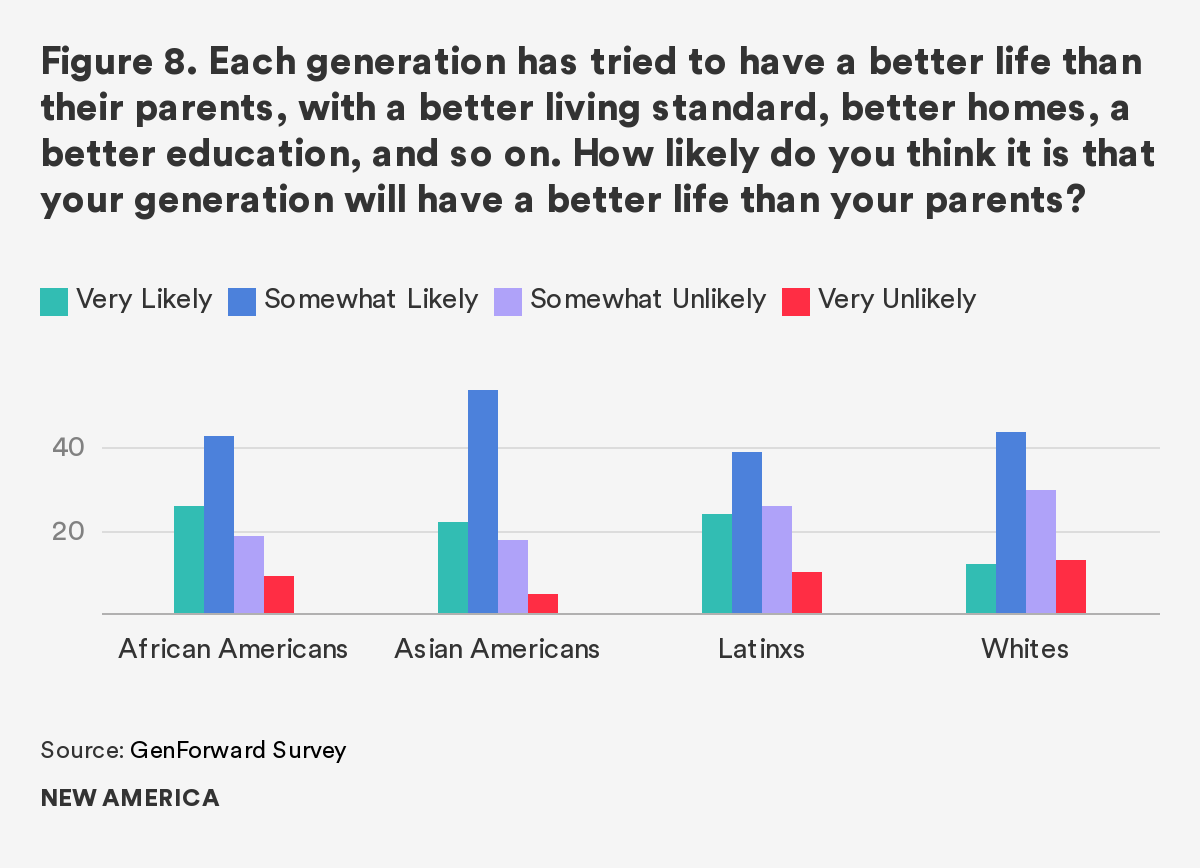

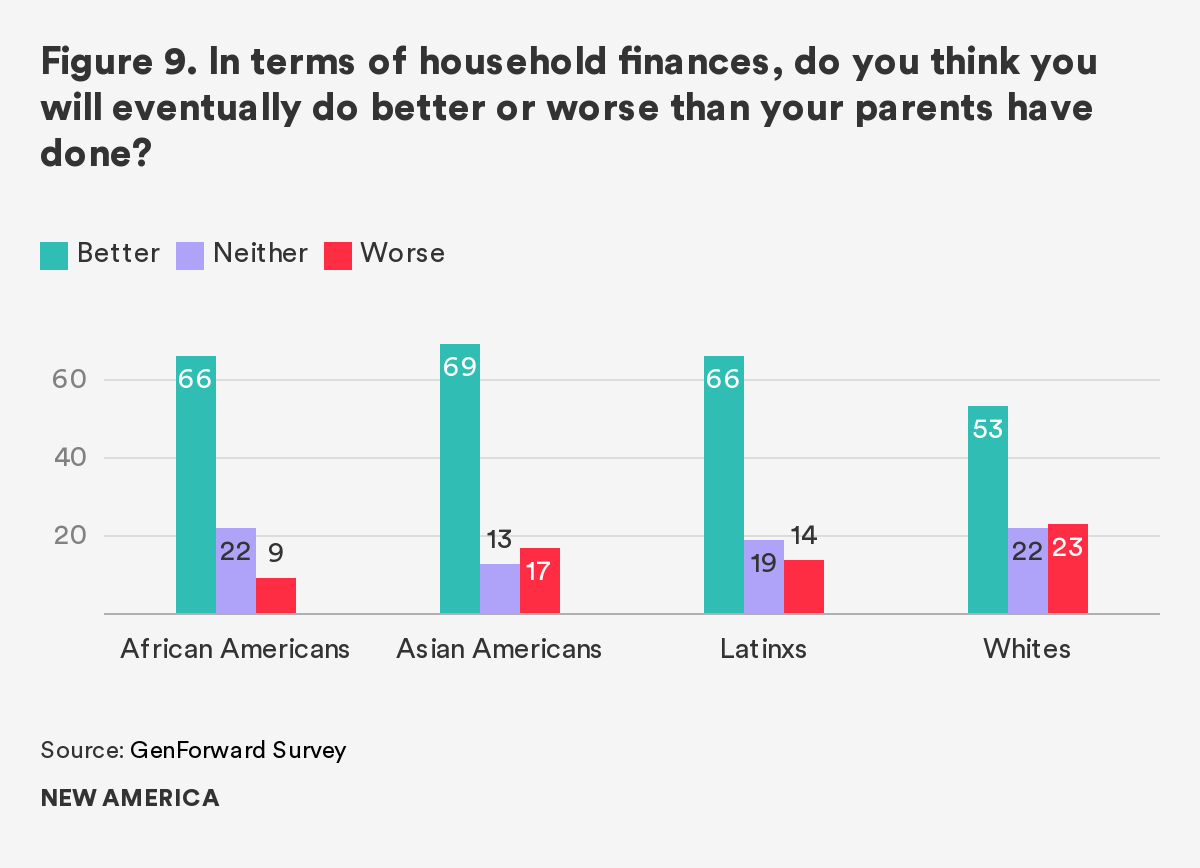

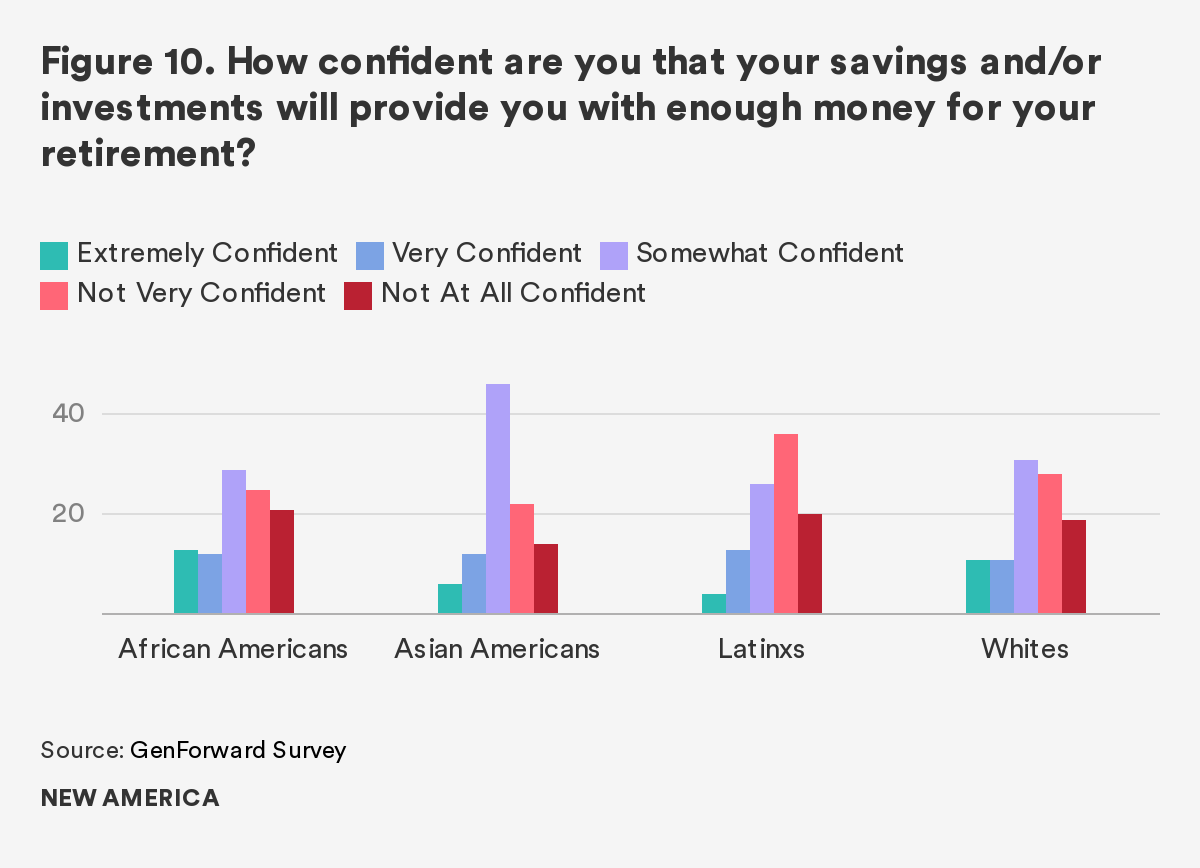

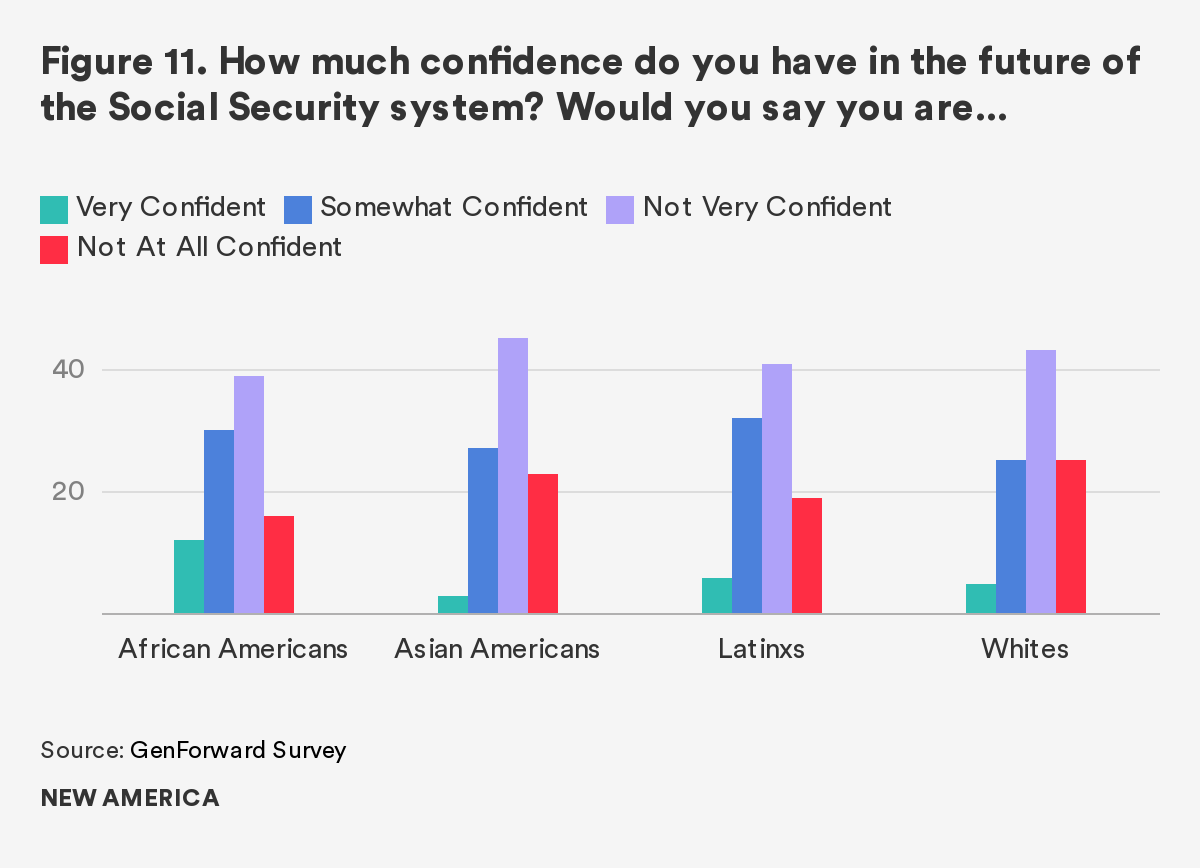

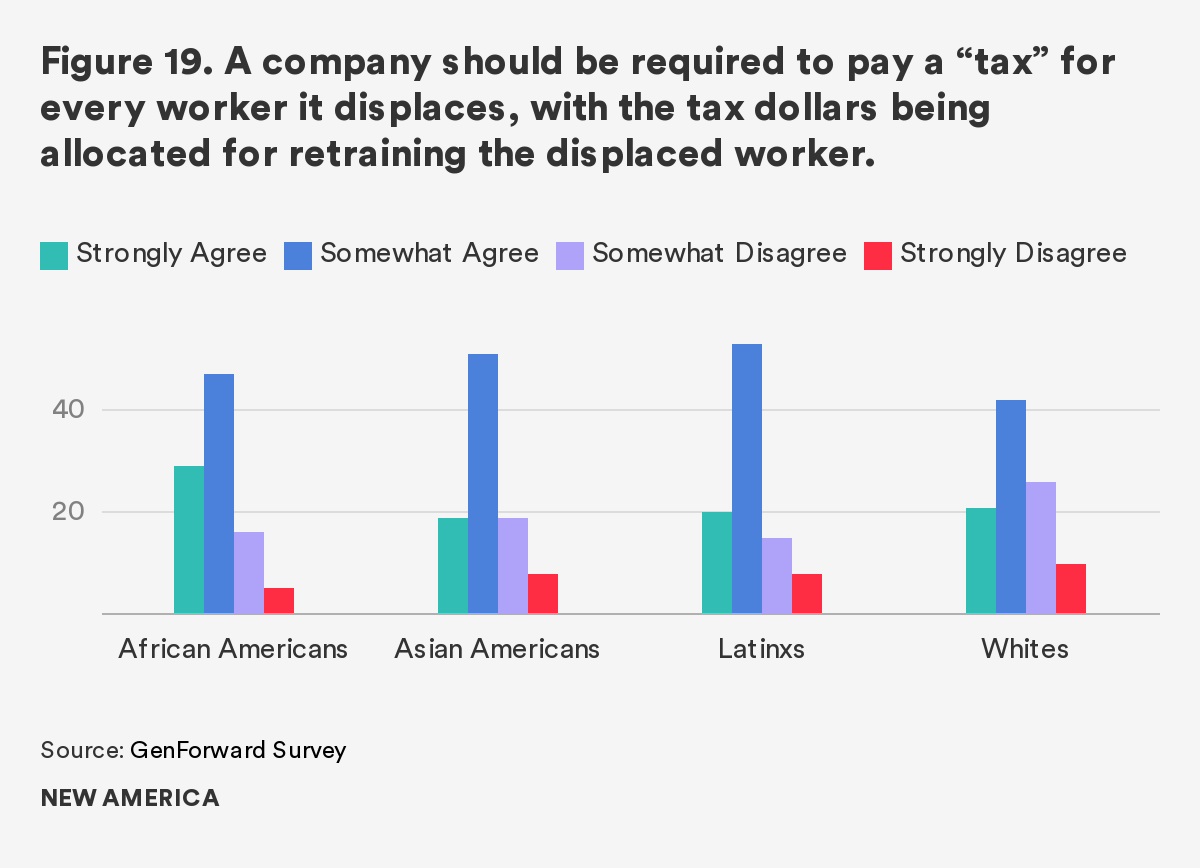

In order to assess how young people are experiencing the economy, it helps to ask them. Vladimir Enrique Medenica, Matthew Fowler, and Cathy Cohen present an analysis of Millennial public opinion as collected by the GenForward Survey at the University of Chicago , a nationally representative survey of young adults that pays special attention to how race and ethnicity shape people’s attitudes and experiences. Specifically, they report on how young people feel about work and the economy. Their analysis elevates how distinct racial and ethnic groups experience changes in the economy differently. The variations they uncover in perceptions, attitudes, and behaviors can and should be used to inform policy interventions.

This section concludes with an article by Thea Garon summarizing evidence from the U.S. Financial Health Pulse, an innovative project of the Financial Health Network designed to track the totality of people’s financial lives by considering how they spend, save, borrow, and plan. Among the innovations of this project is a metric of financial health that can distinguish people who are financially vulnerable, coping, or healthy, depending upon their behaviors. When applied to Millennials, this metric indicates that only a quarter of the population can be considered financially healthy, and deeper analysis reveals wide gaps among racial and ethnic groups. This work reflects how widespread financial security is among this generation, with the overwhelming majority living as poor, near poor, or one calamity away from financial hardship.

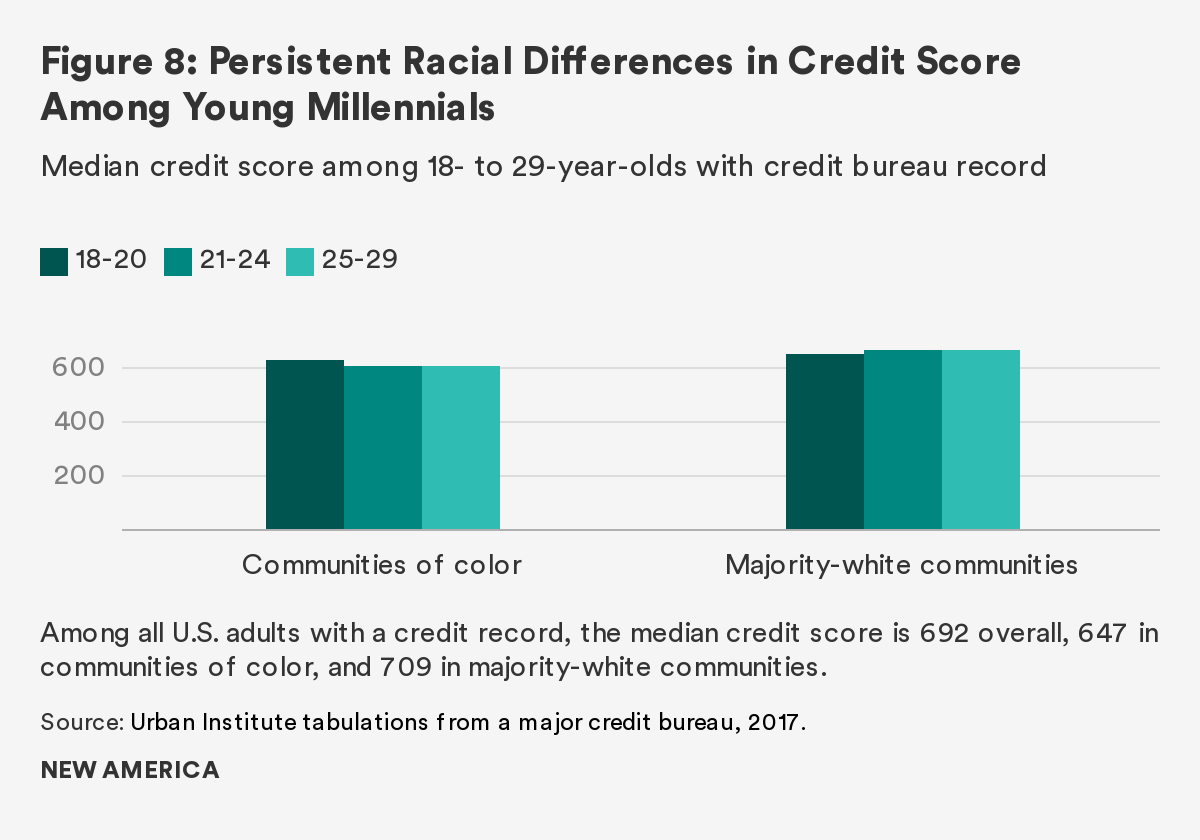

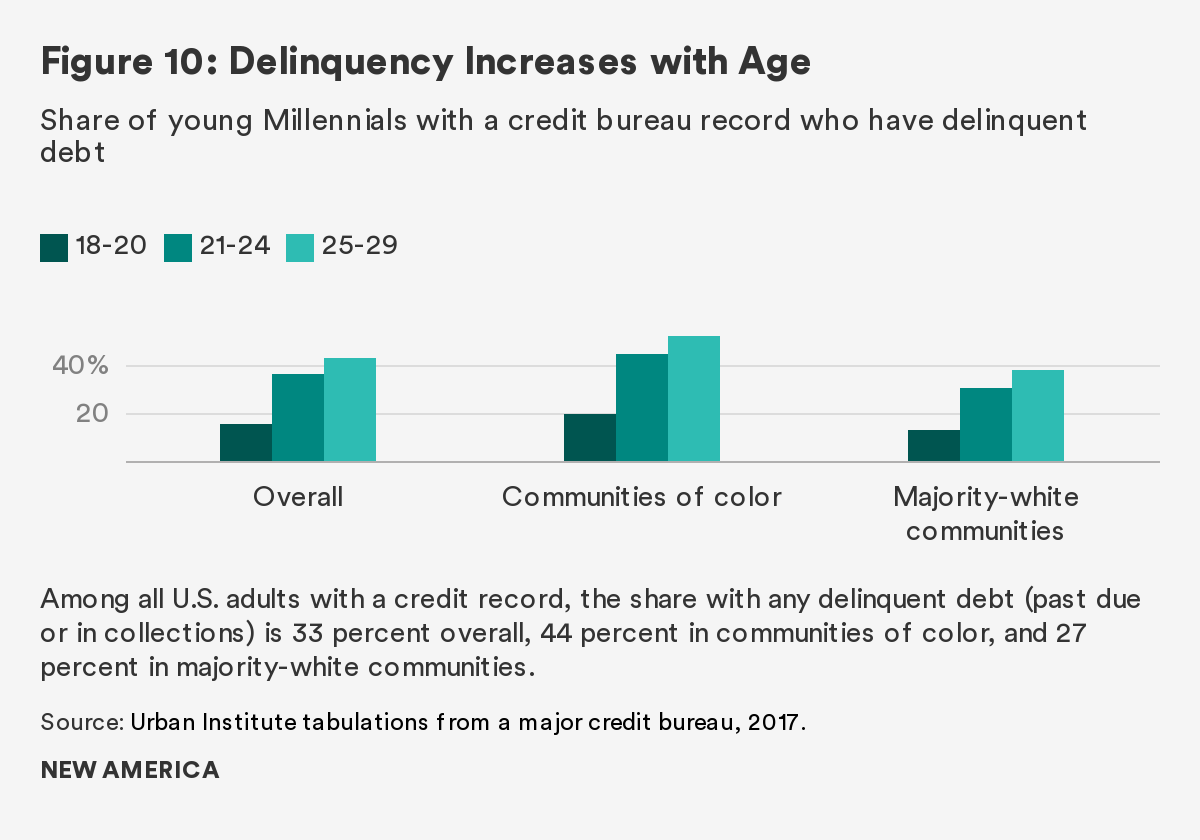

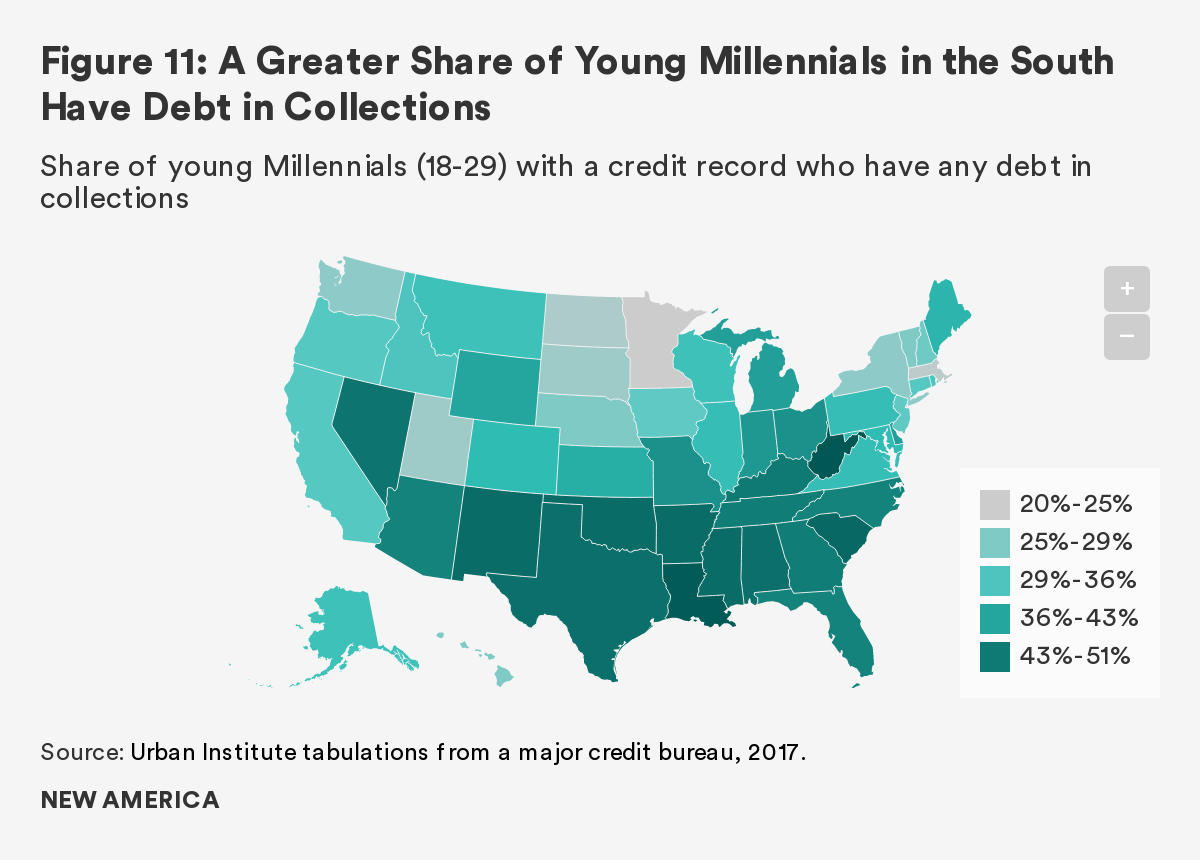

The book’s second section examines key components of the Millennial balance sheet in greater detail, which features changing relative shares of assets and liabilities. Signe-Mary McKernan and Caroline Ratcliffe of the Urban Institute, and Trina Shanks of the University of Michigan, use an innovative approach to assess the current financial position of the Millennial generation. They look at both wealth data and collateral evidence provided by private-sector credit agencies that track consumers’ borrowing and payment behaviors. The credit scores assigned to borrowers are a proxy for financial health, and also subsequently determine the cost of accessing future credit. Extending their analysis of wealth and credit health among Millennials to geography, they reveal how financial hardship is also regionally concentrated, an insight that has important policy ramifications.

The next set of chapters examines the liability side of the generational balance sheet. Rather than building wealth, many Millennials have accumulated debt, but the nature of this debt has changed. Instead of mortgage debt, which previous generations have historically begun to accrue by the time they reach their early thirties, Millennials have accumulated rising levels of consumer and student loan debt.

The current state of federal student loan portfolio reveals a staggering $1.5 trillion in outstanding debt. In his analysis of the federal student loan system, Wesley Whistle from New America’s Education Policy Program is able to describe trends in student debt and distinguish among different types of borrowers. Looking at debt levels, defaults, and loans in collection, he describes the relatively poor outcomes by those that don’t finish their degrees, have excessive repayment burdens given their subsequent income, attended a for-profit school, and African Americans generally. Along with his analysis of the data, he presents a series of policy reform ideas targeted to borrower characteristics that can reduce extended financial hardship, if implemented at scale.

Beyond student loans, other consumer debt among young adults has increased too. Ida Rademacher and Genevieve Melford of the Aspen Institute’s Financial Security Program assess this growth and argue that debt has reached such unsustainable levels that it is sowing the seeds for the next financial crisis. They highlight work in the field that is beginning to identify innovative solutions to address consumer debt, specifically with reforms in the management of student loans, the reduction of government fines, and the regulation of collection agencies.

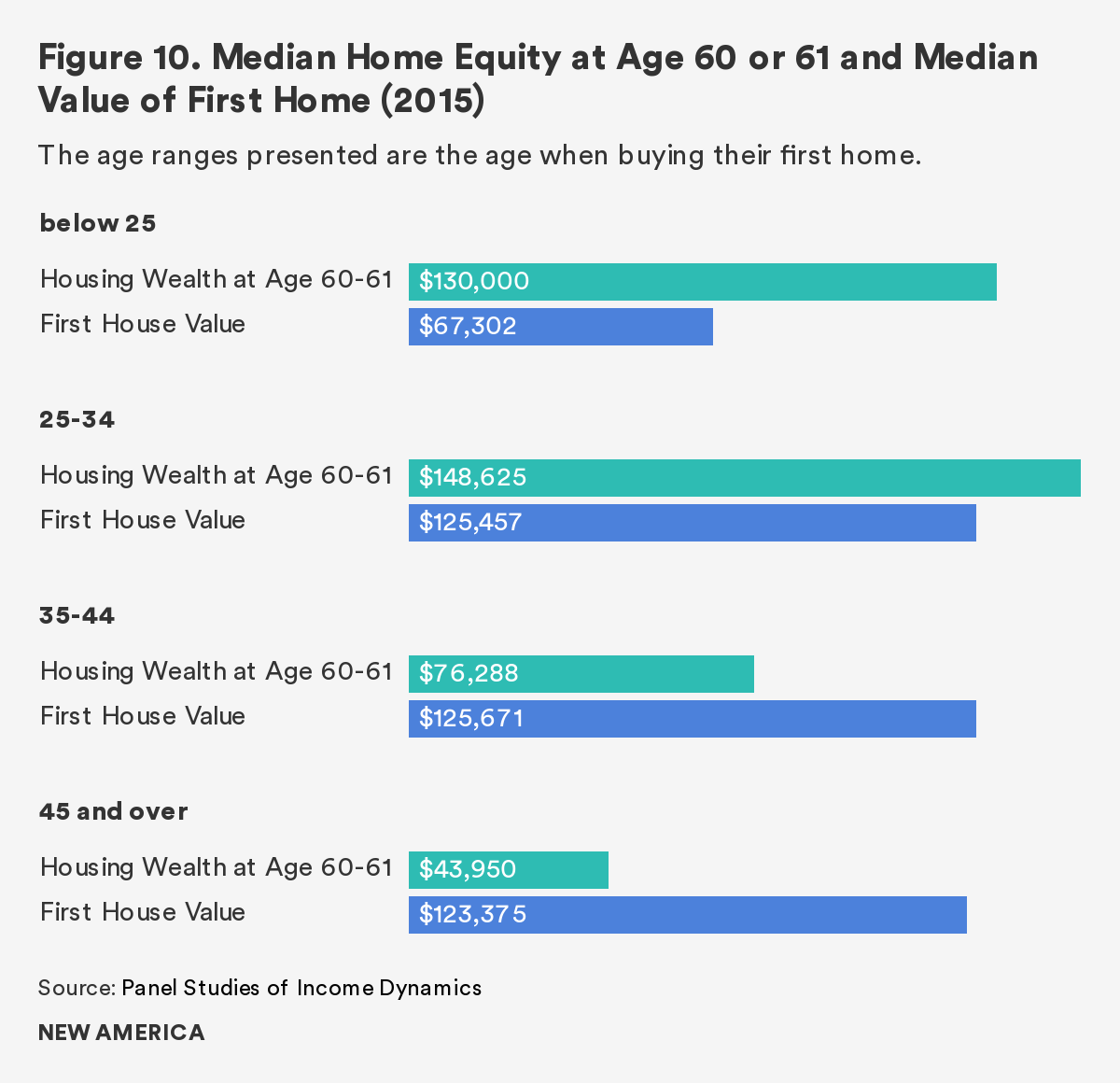

The section concludes with a closer look at the changing relationship of Millennials to housing. Analysis by Jung Choi of the Urban Institute’s Housing Finance Policy Center shows that not only do Millennials have a lower rate of homeownership as traditionally measured, but they have lower rates of household formation generally. The increasing prevalence of living with parents or relatives is a logical response to income and debt constraints, but it can undermine wealth building prospects. By considering both the lower homeownership rate and the lower household formation rate, Choi is able to provide a more realistic estimate of the potential wealth loss experienced by Millennials. In this sense, changing patterns of living arrangements, which have led to declines in homeownership, are actually among the most significant new sources of wealth inequality that have taken hold since the Great Recession.

The final section features articles that explore the policy implication of the emerging Millennial wealth gap. Liz Hipple of the Washington Center for Equitable Growth reviews the accumulating social science research that attests to the relationship between a family’s economic resources and a child’s subsequent outcomes, and identifies a key measure of intergenerational mobility. She argues that this should be the foundation for a policy response. Further, she makes the case for going beyond solutions that merely equalize access to activities that support human capital development, such as education and skills attainment, to solutions which ensure that young adults can benefit from deploying their potential in the economy. In doing so, she focuses on the need for higher wages and coherent career ladders, as well as the need to address discrimination experienced by people of color, which she shows to be a persistent feature of American society and its economy.

This approach is particularly relevant given the dramatic rise in student loan debt and its role in undermining future wealth building and economic security. Ben Miller, Colleen Campbell, Brent Cohen, and Charlotte Hancock of the Center for American Progress and Generation Progress present four specific policy options to address the $1.5 trillion of outstanding federal student loan debt. To facilitate a comparative assessment, they articulate a set of criteria with which to assess the merits of a policy response. Their options vary in scale and take into account different borrower characteristics. For instance, many young adults carry student loan debt even though they did not complete a degree. This group has a relatively high rate of default, which makes them particularly vulnerable financially. Those who completed a degree, especially at the graduate level, are less likely to default, but may still face struggles related to repayment. These are the nuances that should inform a policy response to one of the most pervasive problems afflicting the Millennial generation.

Finally, I seek to advance a forward-looking policy agenda to respond to the unfolding reality of the Millennial wealth gap. The last chapter presents a set of specific policy responses that can be pursued at scale to reduce generational inequities. These responses are intended to address the dual imperatives of helping the current generation repair their balance sheets and simultaneously creating new pathways to progress for future generations.

Without a dramatic change in the fortunes of Millennials, an entire generation will miss out on the chance to reach their full potential, imperiling our democracy in the process. If the diverse cohort of young adults who constitute the Millennial generation can’t improve their financial balance sheets by earning more, increasing their assets, and lowering their liabilities, their climb up the economic ladder won’t be delayed—it won’t occur at all. There is a role for all of us, and particularly our policymakers, to help this generation chart a new course.

Citations

- Robert Lerman and Signe-Mary McKernan. “Effects of Holding Assets on Social and Economic Outcomes: A Review of Theory and Evidence.” U.S. Department of Health and Human Services. 2008.

- Reid Cramer, Justin King, and Elliot Schreur. “Flexible Savings: The Missing Foundation for Financial Security and Economic Mobility.” New America. 2014.

- Pew Research Center. “The Generation Gap in American Politics.” 2018.

- Pew Research Center. “Trends in Party Affiliation among Demographic Groups.” March 20, 2018.

- Richard Fry. “Millennials and Gen Xers Outvoted Boomers and Older Generations in 2016.” Pew Research Center. July 2017.

Building Ladders of Success for the Rising Millennial Generation: An Initiative Funded by the Citi Foundation

Julie Hodgson

Young people today face a number of significant challenges as they strive to achieve financial security. Stagnant incomes, extended periods of unemployment, rising student debt, and scarcity of affordable housing have created conditions that make the transition to adulthood much more difficult. The youth unemployment rate is three times higher than that of adults, and the widening income gap continues to threaten the financial stability of this rising generation.1 Allowing economically disadvantaged young people to grow into economically disadvantaged adults contributes to a destructive cycle that hinders the growth of communities, cities, and economies. Yet, despite these realities, we know that young people are optimistic, entrepreneurial, and realistic about what they need to succeed.2

For this and coming generations to thrive, young people need to be able to access tools, resources, and networks to navigate the obstacles presented by our contemporary economy. Over the last several decades, the Citi Foundation has focused its resources on supporting interventions that were considered traditional pathways to success. Specifically, efforts to increase post-secondary degree attainment, promote homeownership, and help individuals adopt positive financial behaviors can be beneficial when they lead to reduced levels of debt and higher levels of short- and long-term savings. While we still believe that these asset-building approaches are key milestones, my colleagues and I increasingly recognize that today’s youth face greater uncertainty about their future than prior generations. Career trajectories have been altered, definitions of success have changed, and even the decision of when and if to start a family has been impacted. For many of today’s youth, the pathway to success is far from linear.

As part of our Pathways to Progress initiative, the Citi Foundation is investing in innovative interventions to help young people pursue their career and economic ambitions by connecting them with on-ramps to opportunity. In 2017, the Citi Foundation announced its largest philanthropic commitment with the global expansion of Pathways to Progress to continue our efforts tackling youth unemployment beyond the U.S. By 2020, we will have invested $150 million to impact the lives of 600,000 youth globally.

As part of our commitment, the Citi Foundation partnered with New America to further the knowledge and dialogue on the issues facing young people in the U.S. today. We believe that the magnitude and complexity of these challenges have implications for us all and require a holistic, multi-sector response. Government, corporations, civic leaders, and young people need to continue working together not only to better understand the unique challenges facing Millennials and Generation Z, but also to collectively charter a productive path forward. In response, we supported a convening in the spring of 2019 at New America that brought together a diverse group of policymakers, thought leaders, practitioners, and philanthropists to discuss the issues at hand, share knowledge, and engage in a solutions-oriented conversation on how the country can ensure access to opportunity and upward mobility for future generations. It was an enlightening and dynamic day of discussion.

Many of the themes raised in conversations from this convening are reflected in the essays that follow. Our hope is that the ideas set forth here will help spark your own thinking, and prompt us all to further evaluate how we can better support today’s youth. Ultimately, it will require the strengthening of the entire youth-serving ecosystem to ensure that young people have what they need to rise above the challenges they face and create opportunities for themselves, their families, and their communities.

Finally, we want to thank New America, and namely Reid Cramer, for partnering with us on this journey and assembling the insightful essays that follow. Taken together, these pieces make a valuable contribution in helping to illuminate the obstacles that exist for young people today, and also clarifying what is needed to build accessible ladders of success. All of us have a stake in creating new pathways to progress that enable the rising generations to pursue their dreams.

Part 1: Generational Wealth and Financial Health

Part 1 includes:

- Framing the Millennial Wealth Gap: Demographic Realities and Divergent Trajectories by Reid Cramer

- Trends, Origins, and Implications of the Millennial Wealth Gap by William R. Emmons, Ana H. Kent, and Lowell R. Ricketts

- The Millennial Racial Wealth Gap by Fenaba R. Addo and Yiling Zhang

- The Young and (Economically) Restless: The Nature of Work for American Millennials by Vladimir E. Medenica, Matthew Fowler, and Cathy J. Cohen

- The Financial Lives of Millennials: Evidence from the U.S. Financial Health Pulse by Thea Garon

Framing the Millennial Wealth Gap: Demographic Realities and Divergent Trajectories

Reid Cramer

The generational experience of Millennials is far from uniform and differences among them abound, but they do appear to be sharing a pervasive anxiety about their finances. As resources have become increasingly concentrated, economic divides in the country have grown rather than expectations of shared prosperity. Even though achieving economic security is often seen as a result of individual characteristics and behaviors, it is the performance of the overall economy, with its boom-and-bust business cycles, which ultimately creates the opportunity for financial success. Emblematic of the challenges facing young adults in America today is that—for a substantial majority of them—accumulating savings and wealth is turning out to be an elusive proposition.

Although there are regional and local variations in a national economy, macroeconomic trends produce conditions that everyone must navigate. How people respond to changes in the economy depends on a number of factors, including where they are in their life cycle. In this sense, a generational perspective is particularly useful in understanding how economic conditions have large-scale impacts over time.

By considering the demographic foundations, economic realities, and divergent trajectories that are shaping the Millennial generation, this chapter will frame the emerging generational wealth gap. The relative diversity of Millennials, described in the first section, is sowing the seeds for new type of generation gap—one that is fundamentally cultural but which will have economic implications. The second section focuses on the divergent experiences of Millennials in the economy, as reflected in the range of their financial profiles, socioeconomic outcomes, and changing milestones of adulthood that distinguish them from their generational predecessors. In this analysis, two factors loom large: the uneven impacts of the Great Recession and the enduring role of race and ethnicity. The third section offers a description of the most basic contours of the Millennial wealth gap, which is being driven by relatively flat incomes, low savings, decreased housing equity, and higher consumer debt and student loans as well as a widening racial wealth gap. Narrowing this gap and improving their economic prospects is likely to require a concerted policy response aimed at strengthening their generational balance sheet.

Demographic Realities of the Millennial Generation

Assessing the world through the perspective of generations is an analytical approach that has both inherent value and limitations. On the one hand, there are insights to be gleaned from discerning how people born about the same time and in the same place share characteristics and behaviors that shape their experiences. Just as cultures can be studied and compared by examining beliefs, practices, and customs, generational cohorts enable comparisons to contemporary or historic peers. On the other hand, a generational perspective fosters an imprecision, imposing arbitrary demarcations that collapse differences across the life course and force an aggregated analysis. Grouping people within large spans of time and assuming they share characteristics can be presumptuous—consider the differences in a single person’s outlook when they are in their early 20s from when they are in their mid-30s.

Still demographers have traditionally and successfully employed cohort analysis to study variations among geographies and communities, where there is an intermingling of effects related to a person’s age, the period of time when they live, and the variations among a group moving across time. Even though everyone in a society may experience a specific event, the impact of that experience on attitudes and behaviors may differ depending on a person’s age and place in the life cycle. At the generational level, comparing discrete age cohorts can reveal key distinctions in the links between experiences and outcomes.

Generational Cohorts Defined

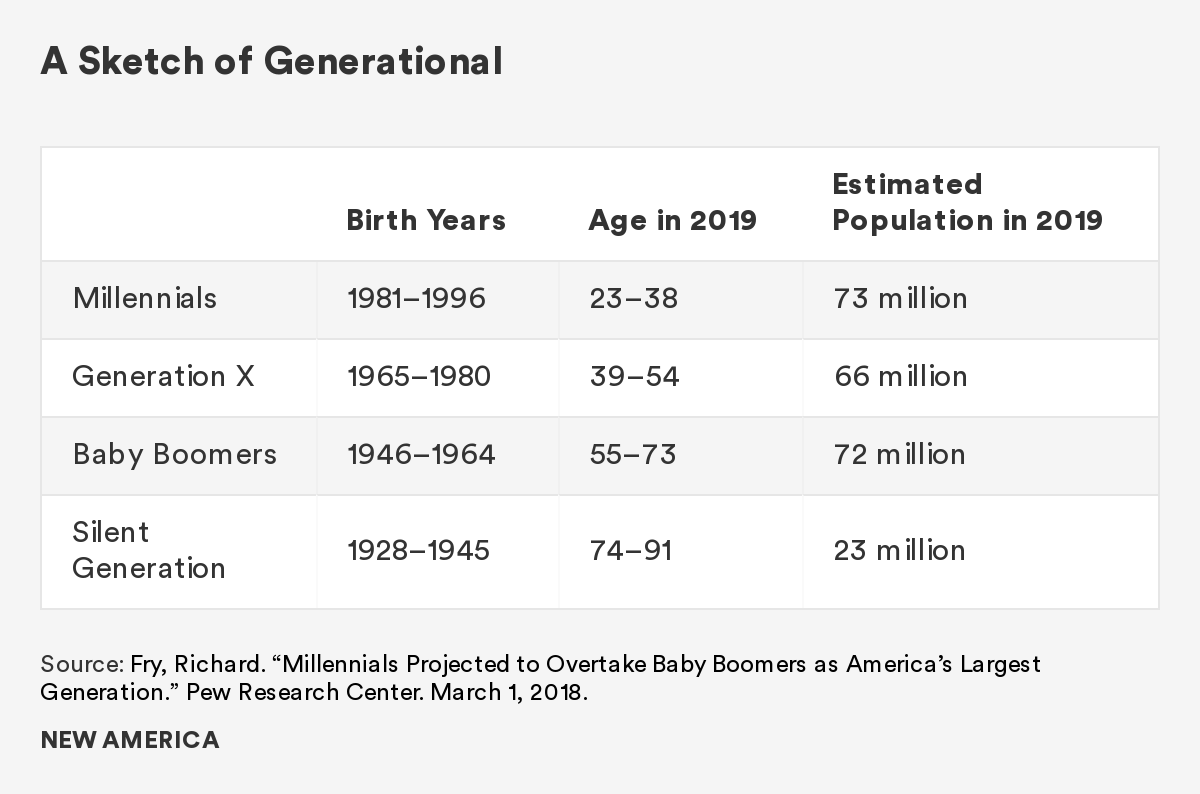

While generational labels have become ubiquitous in popular culture, they often are loosely applied. For instance, many different cutoff dates have been used to define the Millennial Generation, which variously have fallen between the years 1980 and 2000. The Pew Research Center, a leading source of generational analysis, recently called for a tightening of the Millennial span.1 Based on their assessment of demographic, labor market, attitudinal, and behavioral measures, they proposed a definition of all those born between 1981 and 1996. This means that as of 2019, Millennials are in their early 20s to late 30s, and they can be compared to Gen-Xers (ages 39–54), Baby Boomers (ages 55–73), and the Silent Generation (ages 74–91).

Using these generational labels, basic demographic realities for the United States—products of birth, death, and net migration—can be observed. The general outline of the country’s population pyramid reveals the unfolding dynamic between the large but aging Baby Boomer generation, born after World War II, the smaller number of Gen-Xers, and the increased number of births and immigrant arrivals that created the relatively large Millennial generation.

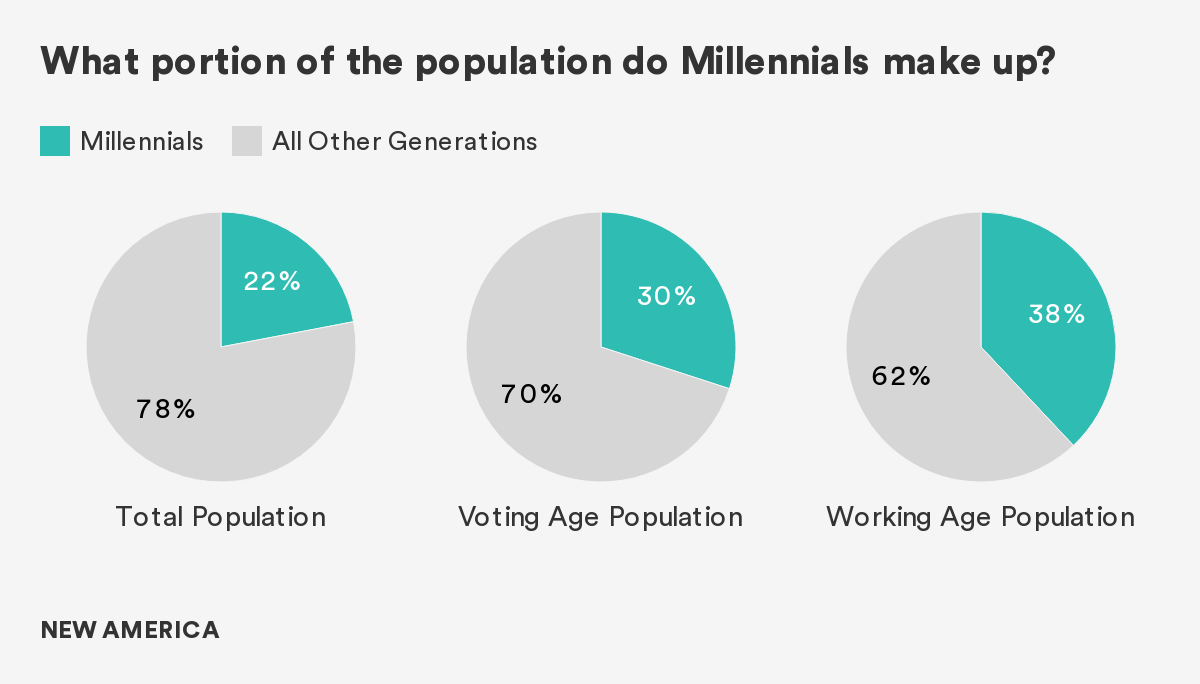

According to the U.S. Census Bureau’s projections, the population of the United States will surpass 328 million during 2019. Over 23 percent of Americans (over 73 million) will be between the ages of 22 and 38 in 2019.2 Recently exceeding the total number of Baby Boomers, Millennials already represent the nation’s largest living adult generation. Currently, Millennials are just over 30 percent of potential voters and are 38 percent of working-age adults; by 2025, they will constitute 75 percent of the workforce.3

While Boomers were more dominant at their peak (33 percent of the population in 1980), their numbers are projected to dwindle to 16.6 million by mid-century.4 In contrast, the influence of Millennials will only expand. Even though Millennials have recently become the largest cohort in absolute numbers, the country’s population will continue to age. This means that seniors are expected to account for much higher proportions of the overall population in the future than they did in the past.5 One implication of an aging population is the potential for a declining share of the population to be in the prime of working life. In 2010, the U.S. had 49 dependents per 100 working-age people; in 2050 that number is expected to rise to 66. As the child and middle-age populations in the U.S. are expected to increase at about the same pace, this increase is a result of the population’s aging.

Having fewer people in the workforce can slow economic growth, especially without increases in productivity. At the same time, more children and seniors may be depending on that shrinking workforce for support. This will have implications, as younger people work to fund the pensions and healthcare of the older generation. Regardless of how these tensions play out in national politics, the relative size of the Millennial generation, especially during their prime working years, is destined to exert a defining influence on the national economy and society.

Shared Experiences

Although individual preferences undoubtedly vary, Millennials do share a range of cultural, historic, and formative experiences that contribute to a generationally distinct worldview. These include early memories of traumatic national events, such as the Oklahoma City bombing in 1995 and Columbine school shooting in 1999, and political developments, such as the impeachment and acquittal of President Clinton in 1998, and the contested results of the presidential election of 2000.

Millennials were between 5 and 20 years old when the 9/11 terrorist attacks occurred, followed by the extended wars in Iraq and Afghanistan. Seven years later, Millennials were between 12 and 27 years old during the 2008 election campaign, when the force of the youth vote helped elect Barack Obama, the first Black president. Their adolescence and early adulthood were spent in the shadow of the Great Recession, with an economy wracked by job losses, business failures, and a slow recovery. The unexpected results of the 2016 election were relatively unpopular among Millennials, creating a new political landscape the entire country is continuing to navigate.

Beyond politics and events, Millennials have clearly been exposed to a dramatically different social landscape enabled by technological innovation and communication tools. The oldest of them came of age along with the internet and the proliferation of cell phones. The youngest have no memories of life before connectivity. Along with advances in telecommunications, many socioeconomic indicators improved. Violent crime in the U.S. fell sharply, as did smoking, drinking, and teen pregnancy. In many respects, the world became much safer. At the same time, there was a growing scientific consensus that environmental changes on a global scale, associated with the large-scale burning of fossil fuels, would increasingly become a source of disasters and displacement.

Millennial Diversity

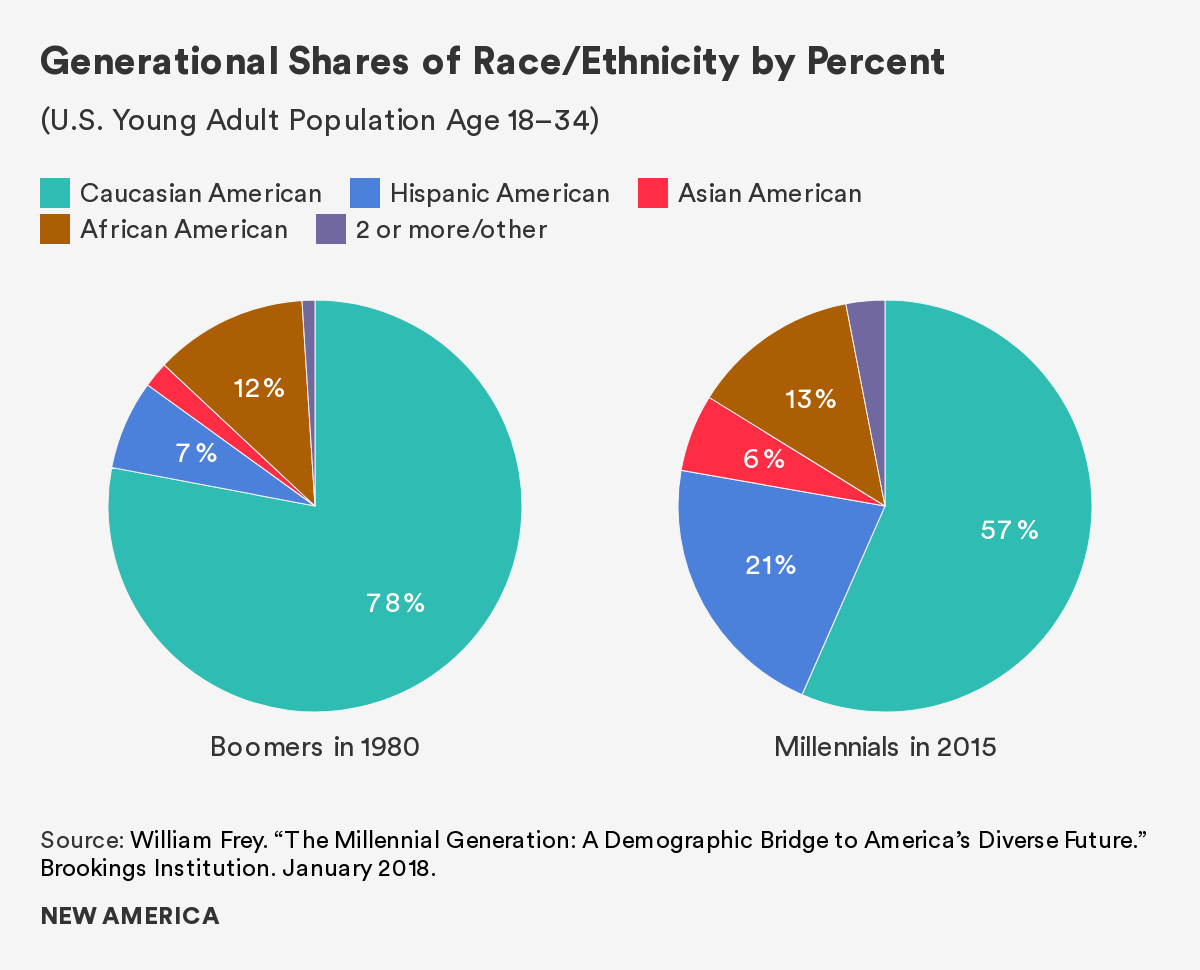

While Millennials share cultural touchstones that distinguish them from older generations, broad generalizations about their preferences and behaviors will miss their diverse experiences. Indeed, the Millennial generation is defined by its diversity. Large waves of immigration to the U.S. in the 1980s and 1990s, coupled with the aging of the White population, have produced a rising share of new minority groups, particularly people with Hispanic and Asian origins.6 Today, 44 percent of Millennials identify as something other than non-Hispanic Caucasian, greatly exceeding the minority share of any of their predecessor generations.7 It is fair to conclude that Millennials are reordering the country’s race and ethnic composition, and serving as a bridge to a more diverse future.

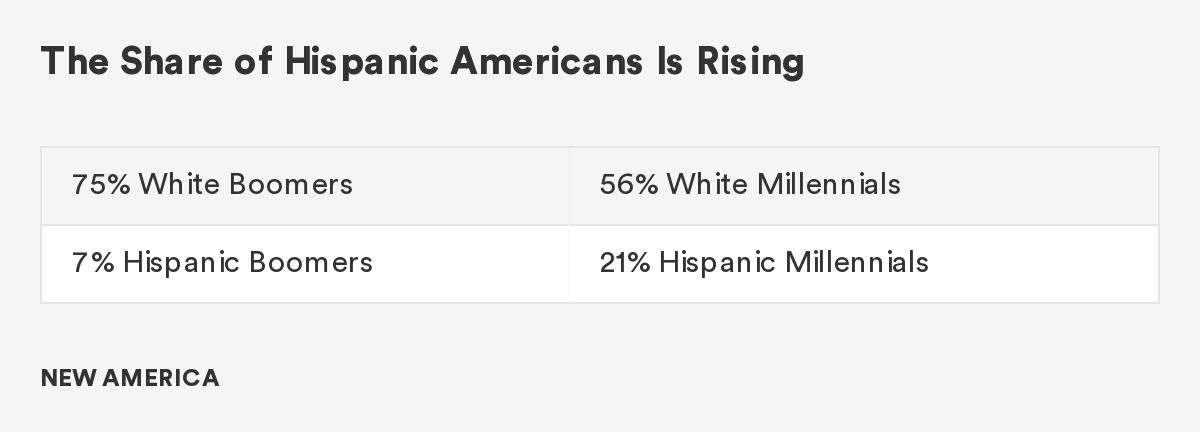

Although Americans of European origin remain the largest among racial and ethnic groups, they will soon no longer be a majority of the country. The Pew Research Center estimates that this will happen by 2055. Specifically, the Hispanic and Asian American slices of the population pie are dramatically increasing, predicted to triple over the next 40 years. While 9 percent of Boomers identify as Hispanic, 19 percent of Millennials identify as being of Hispanic (or Latinx) origin.8 Given current trends, the population of Asian Americans is expected to exceed the total population of African Americans by 2055.

These trends are making the Millennial generation more diverse than its predecessors in a number of respects—such as their country of family origin, languages spoken at home, and patterns of marriage and child rearing—all reflecting a wider range of experiences among the rising generation of Americans.

The experiences of Millennials from newer minority groups are particularly distinct, as both Asian American and Hispanic American Millennials are overwhelmingly made up of first- and second-generation Americans. Immigration by members of these and other groups has been both a primary driver of population growth in the U.S. and a source of diversity. In fact, the share of the U.S. population that is foreign born is among the highest in the world, approximately 14 percent today as compared to 5 percent in 1965.9 The 2015 Census Report predicts that the percentage of the U.S. population that is foreign-born will continue to increase, reaching 19 percent by 2060. More specifically, well over half of Asian American Millennials are foreign born, compared with 36 percent of Hispanic Americans, 10 percent of Blacks, and fewer than 4 percent of Whites. At home, the share of those speaking a language other than English has increased from 11 percent in 1980 to 25 percent in 2015. For Hispanic and Asian American Millennials, more than seven in 10 speak a language other than English with their families.

Since members of these ethnic groups tend to live in proximity, there is a geographic dimension to Millennial diversity. Racial and ethnic minorities make up more than half of the Millennial population in 10 states, including Texas, Arizona, Florida, Georgia, and New Jersey. In another 10 states, minorities account for more than 40 percent of Millennial residents (New York, Illinois, Virginia, and North and South Carolina). Only nine states are home to largely (over 80 percent) White Millennial populations, including Wyoming, Iowa, West Virginia, and Maine.

Given these demographic trends, the transition to a country with more racial and ethnic diversity will continue. Not only have immigrants added to the population generally, but their higher fertility rates are offsetting the steady declines in fertility among native-born women. Without the growth of Hispanic American children, the nation’s child population would have declined from 2000 to 2010.10 Beginning in 2011 and continuing through this year, the majority of babies born in the United States have parents who were traditionally identified as minorities.

Though 75 percent of older Americans—those over age 55—were White in 2015, this percentage drops to half for children under the age of 5.11This means that in only a few years, most children in the United States will likely identify as something other than White.

This change is reflected in the rising number of people in the country who identify as Hispanic American. While only 7 percent of Baby Boomers were of Hispanic origin, this has tripled to 21 percent of Millennials. The cultural experience is decidedly different, as most White Baby Boomers were born when immigration to America was historically low, and those who did arrive were mostly White Europeans. At that time, the country’s minority population was mostly African Americans, and there was widespread residential segregation. Today Millennials are heralding the arrival of a new national demography. In the near term, the working population will increasingly have more racial and ethnic diversity, while the nonworking will be overwhelmingly White Baby Boomers. This is creating what demographer William Frey has called a “cultural generation gap,” triggered by the transformation from the “mostly white baby-boom culture that dominated the nation during the last half of the 20th century to the more globalized, multiracial country that the United States is becoming.” With the growing share of racial and ethnic minorities among the young adult population, the country’s future diversity is foreshadowed. In the long term, this new demography will undermine generalizations, remake institutions, and change the country.

Divergent Experiences among the Millennial Generation

The Millennial generation is not monolithic. No generation is, but the combination of their unique demographic composition and the extended impact of the Great Recession have sparked a divergence from past trajectories. Transitioning to adulthood in the years following the financial crisis has had an impact on financial health, which in turn influenced behaviors and life choices that have become a source for many of the divergent experiences that have defined the Millennial generation.

Millennials in the New Socioeconomic Landscape

Initially the financial crisis eroded the value of a large set of assets, which collapsed the overall distribution of wealth. As the stock and real estate markets recovered, inequality rose as those with significant asset holdings did comparatively better, while the majority, and especially young adults, had to navigate a tough economy. For Millennials, entering the workforce immediately after the Great Recession has dramatically altered work and employment trajectories. The labor market consequences have been large, negative, and long lasting.12

In 2007, before the economic downturn, more than 50 percent of college graduates had a job offer lined up when they graduated; for the class of 2009, fewer than 20 percent did.13 The subsequent job losses and the slow recovery, reflected in an unemployment rate that stayed above 8 percent until 2013, have depressed incomes and undermined workforce attachment. Today, over half of the unemployed are young adults, greatly exceeding their share of the workforce. While the unemployment rates have come down in recent years, and currently are near historic lows, wages have barely increased and the labor force participation rate for those between the ages of 18 and 34 remains near its lowest level in four decades.14

Since the Great Recession, young people have experienced substantial declines in labor force participation, which was above 65 percent until 2000, and then dropped to 54.9 percent by 2014.15 These changes have been driven by two distinct dynamics. More young people choose to stay in school, complete high school, and pursue postsecondary education. As a result, Millennials are better educated and credentialed than their predecessors, and may be more skilled as they approach their prime working years. In 1960, only 11 percent of those aged 25 to 29 had a college degree; by 2015, this share had risen to 36 percent.16 Unfortunately, Millennials have had to pay dramatically more in tuition as the costs of going to college and graduate school have risen and access to loans has declined. At the same time, there were increases in the number of people not engaged in education, employment, or training who also had a high school degree. Incorporating people from this group into the future labor force may prove difficult.

These trends have translated to lower incomes generally for the Millennial cohort. In the aggregate, Millennials currently earn 20 percent less than Boomers did at the same stage of life, despite being better educated.17 Specifically, the median earnings today for 18- to 34-year-olds are lower than they were in 1980, and income flows are more volatile.18 Between 1970 and 2002, the probability that a working-age American would unexpectedly lose at least half her family income more than doubled.19 A rise in freelance and contract work associated with employers’ drive for flexibility has shortened employment tenure, weakened access to employee benefits, and contributed to an overall decline in income.

Poverty remains pervasive. Millennials were more likely to be living in poverty than Gen-Xers and Baby Boomers at similar ages, with one in five Millennials officially classified as poor.20 From 1979 to 2014, the poverty rate among young workers with only a high school diploma more than tripled to 22 percent.21 Beyond distinctions in educational attainment, race and ethnicity continue to be associated with large differences in economic outcomes.

Changing Milestones of Adulthood

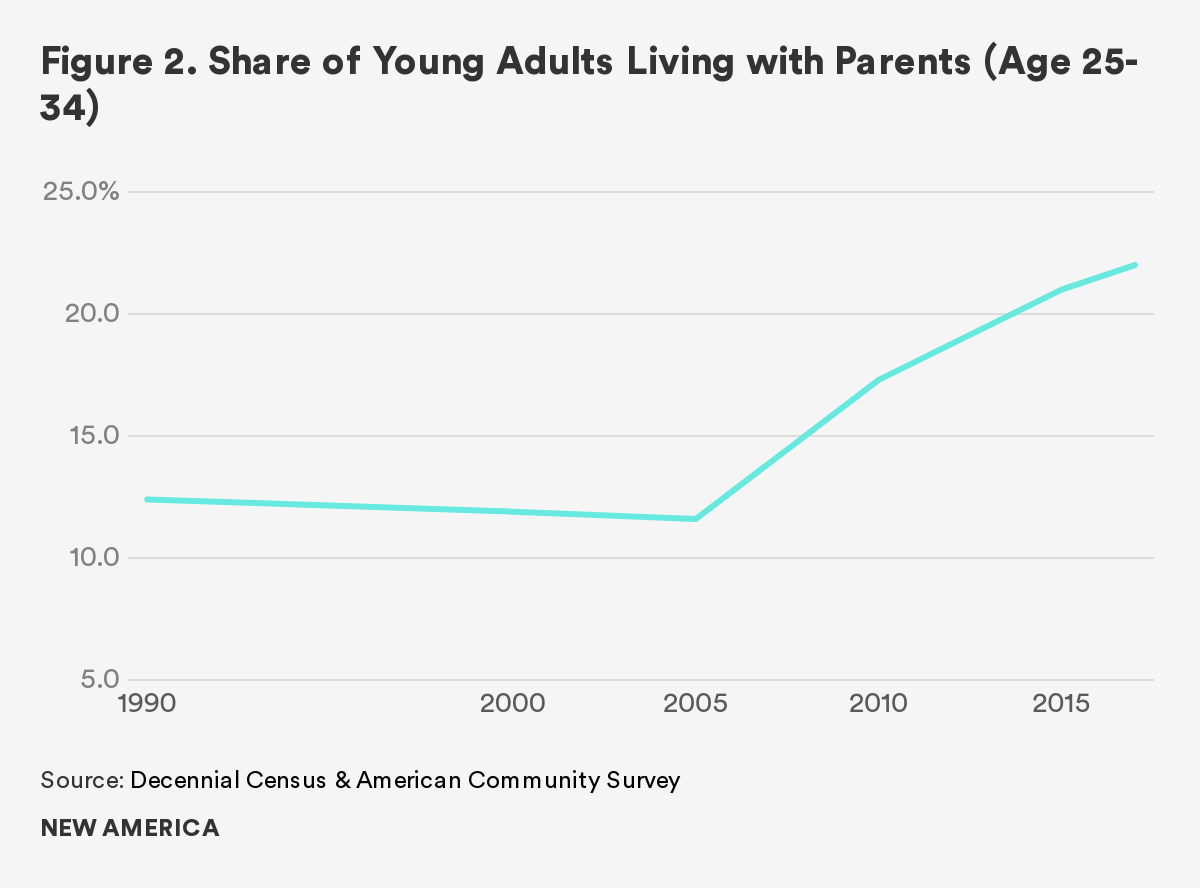

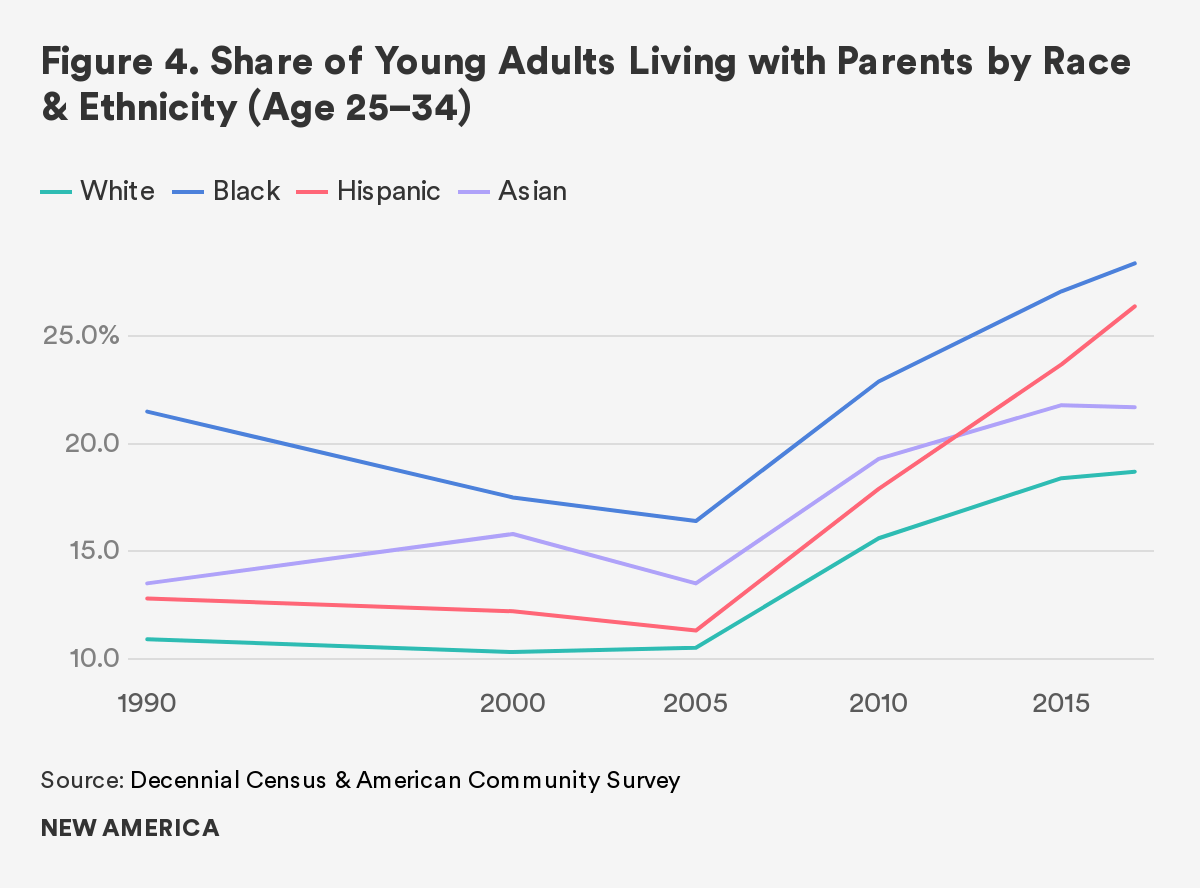

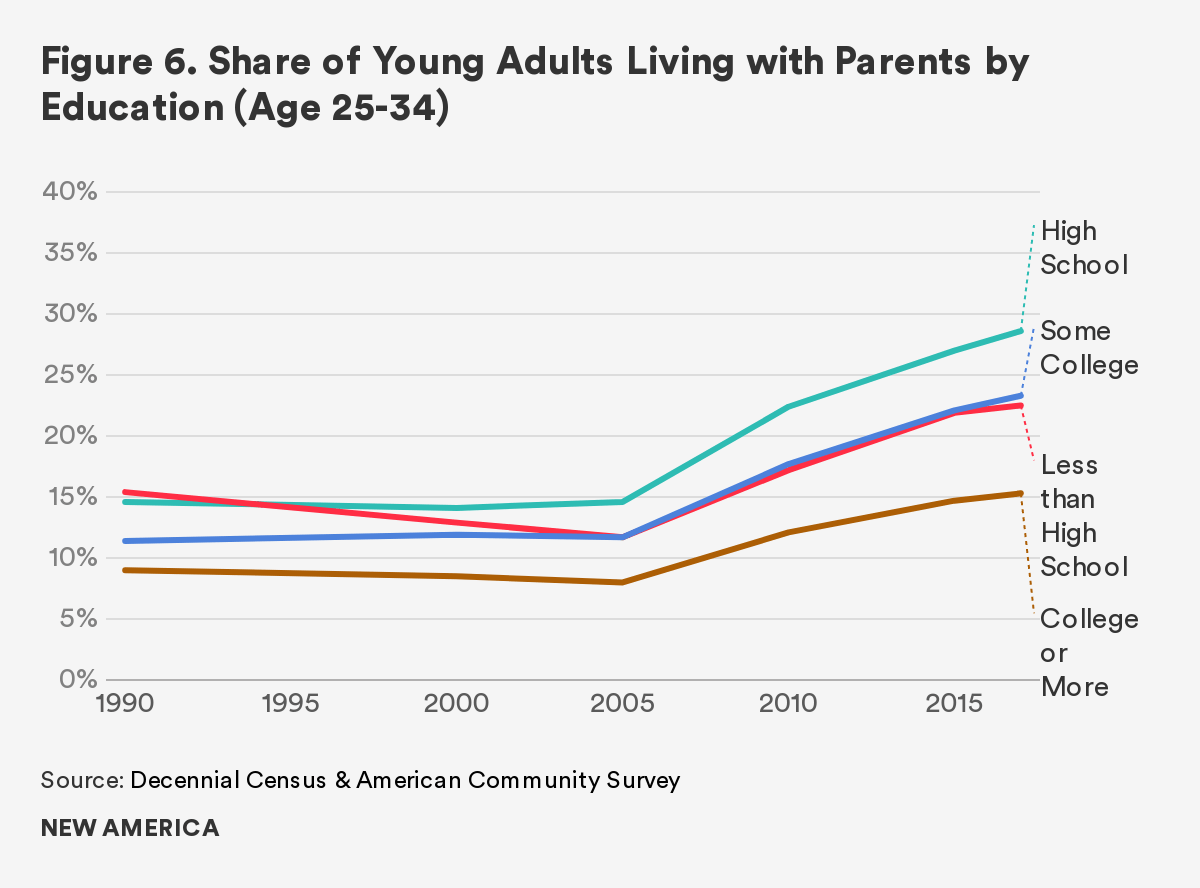

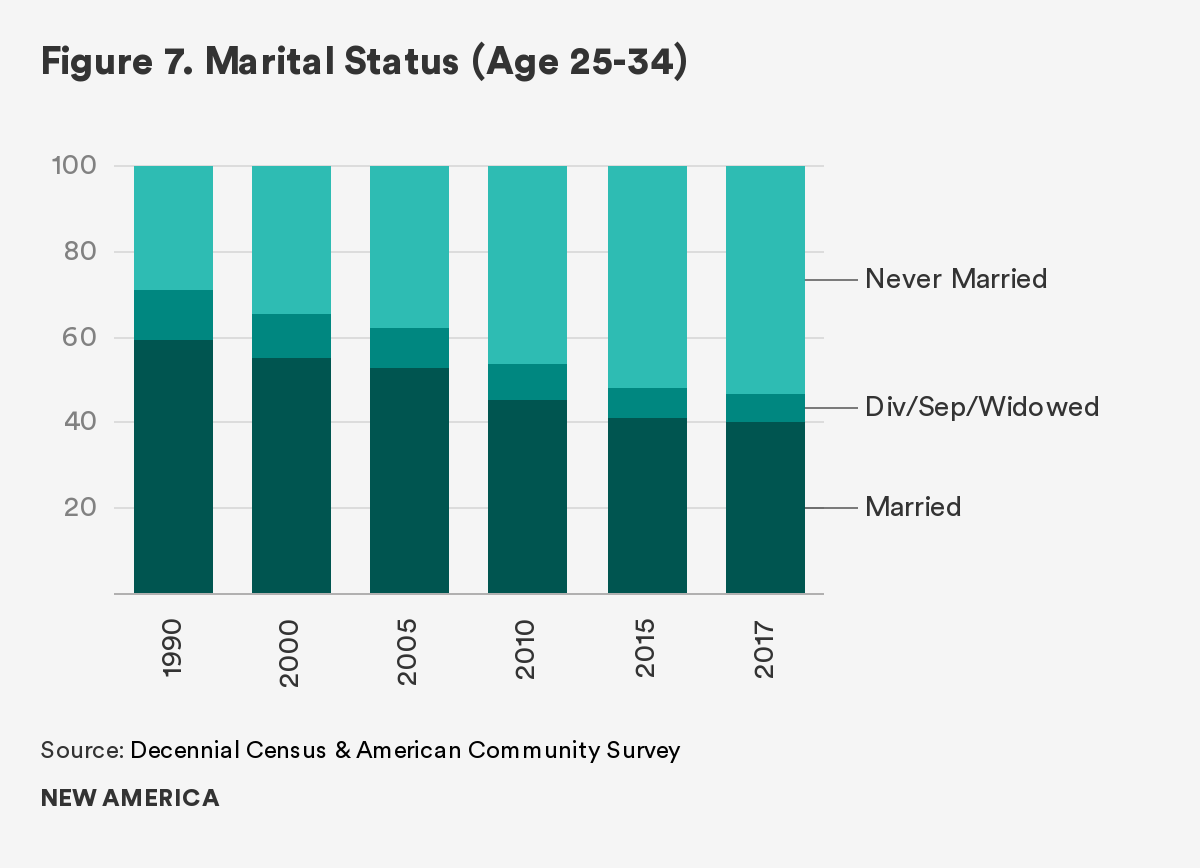

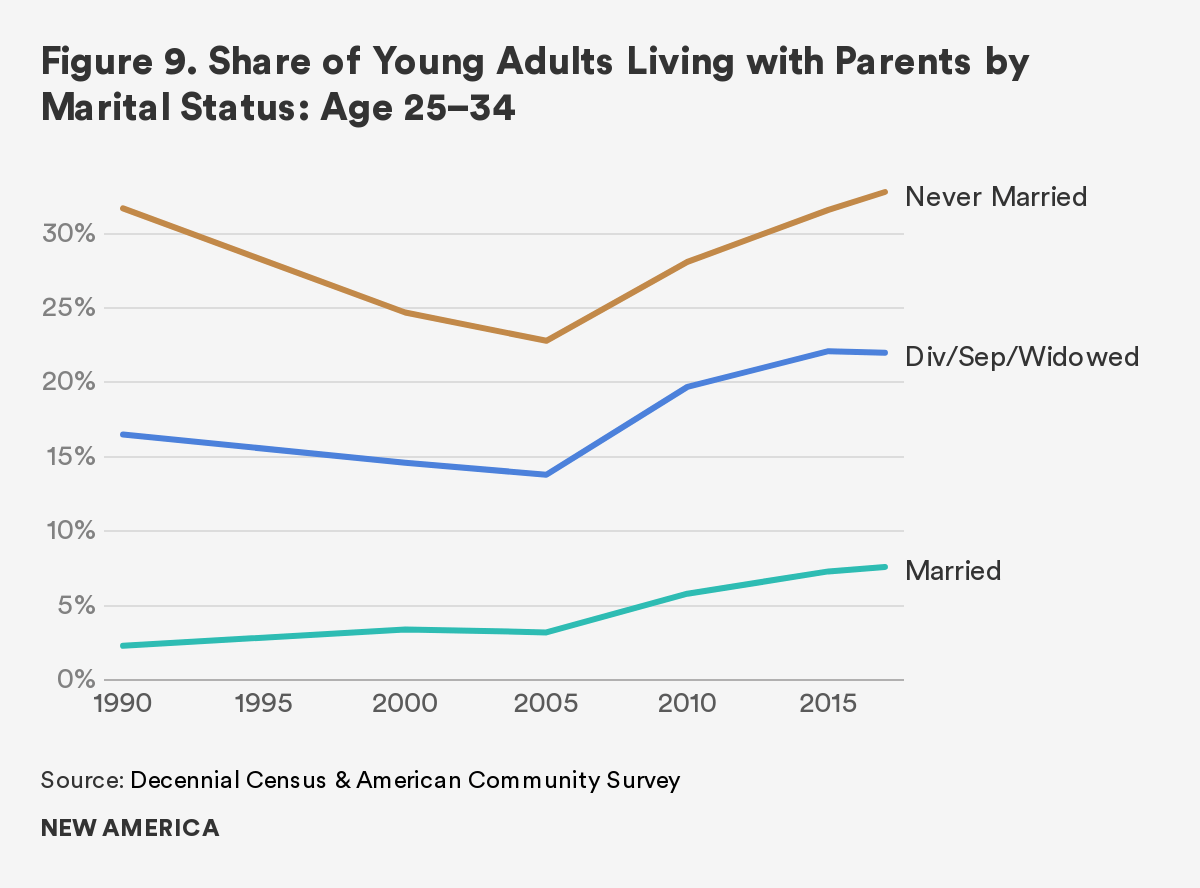

Poor finances appear to be playing a role in redefining how Millennials mark reaching adulthood. Specifically, Millennials today are less likely to marry than their parents. When they do, they do so later. The median age for a first marriage today is about five years older than it was in the 1960s.22 Among young adults, cohabitation with a committed partner is increasingly common, rising to over 9 percent today from around 6 percent in 1997.23 In recent years, the social acceptance and legal sanction of same-sex marriages has created new opportunities for family formation, as has the rise in interracial marriage, which has increased from 5 percent in 1980 to 14 percent in 2015. Still, Millennials are less likely to form independent households; instead, more of them are opting to live with their parents, relatives, or other unrelated adults than previous generations.

Regardless of marital status, child rearing is on the decline. The overall birth rate hit a record low in 2018, dropping for the seventh straight year.24 Today’s fertility rate is 1.72 percent, significantly below the “replacement” rate of 2.1 percent. Only 29 percent of women ages 18 to 29 have ever had children, down from 41 percent in 1998.25 Some of these declines may be attributed to trends that began before the Great Recession took hold, including the rise in women’s labor force participation and pursuit of higher education, along with greater access to birth control and fewer teen pregnancies.

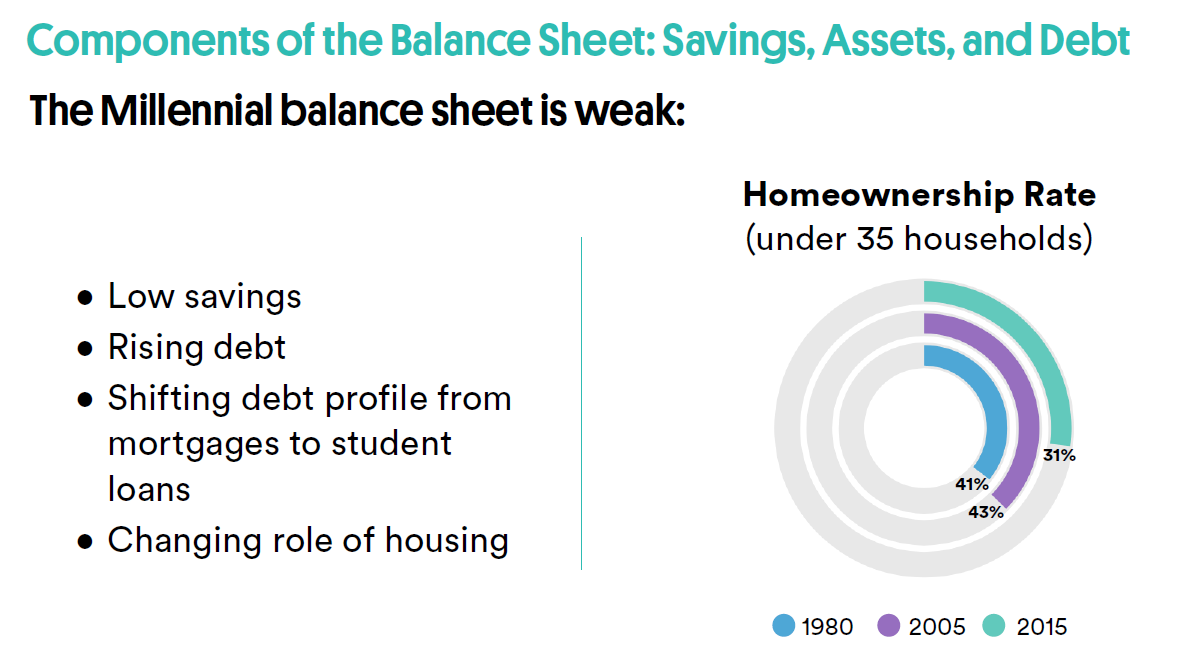

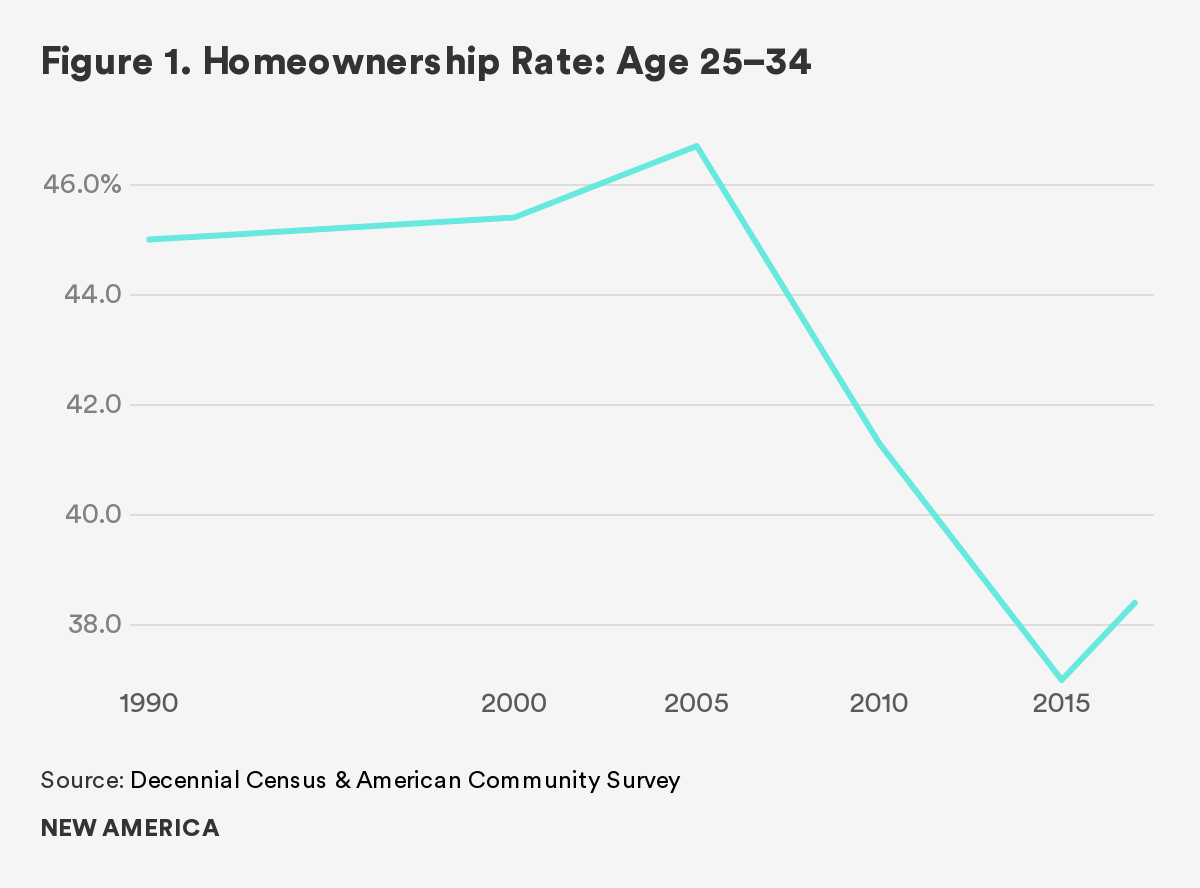

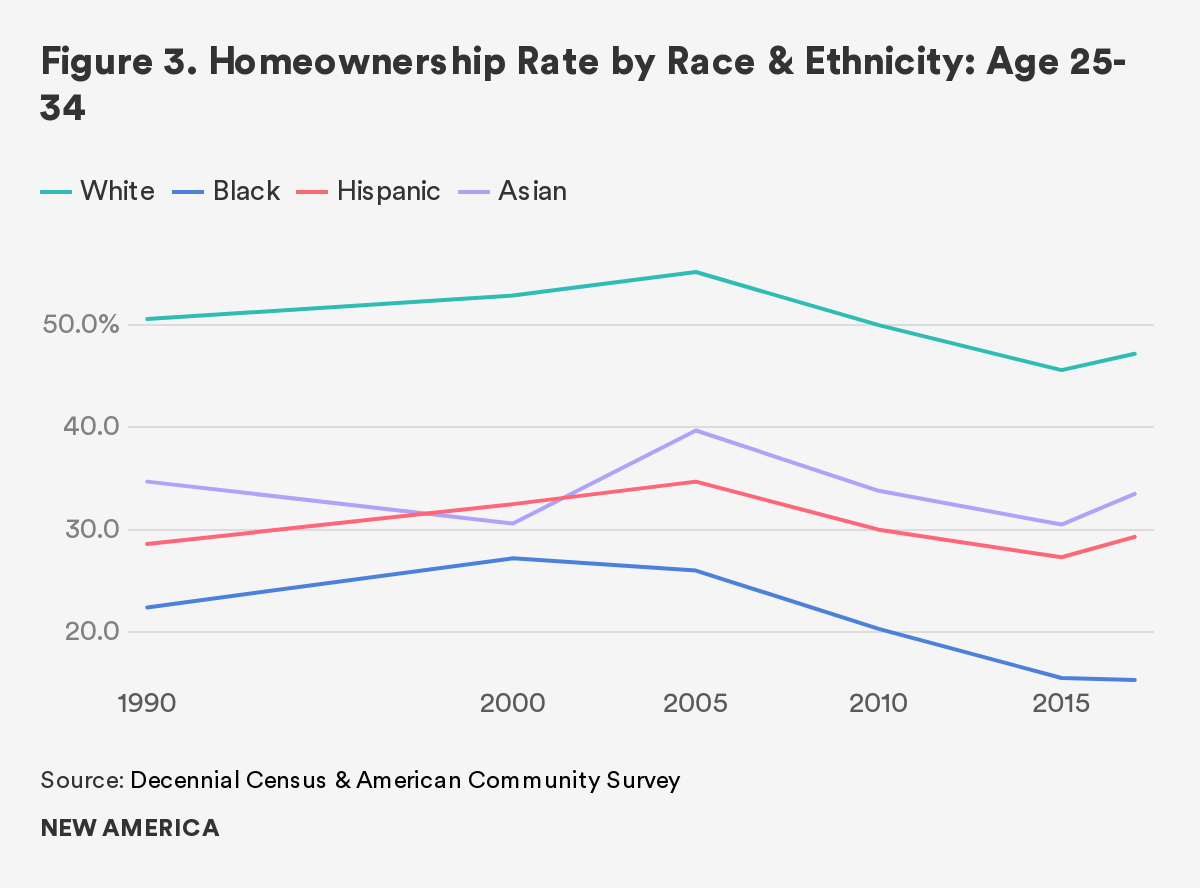

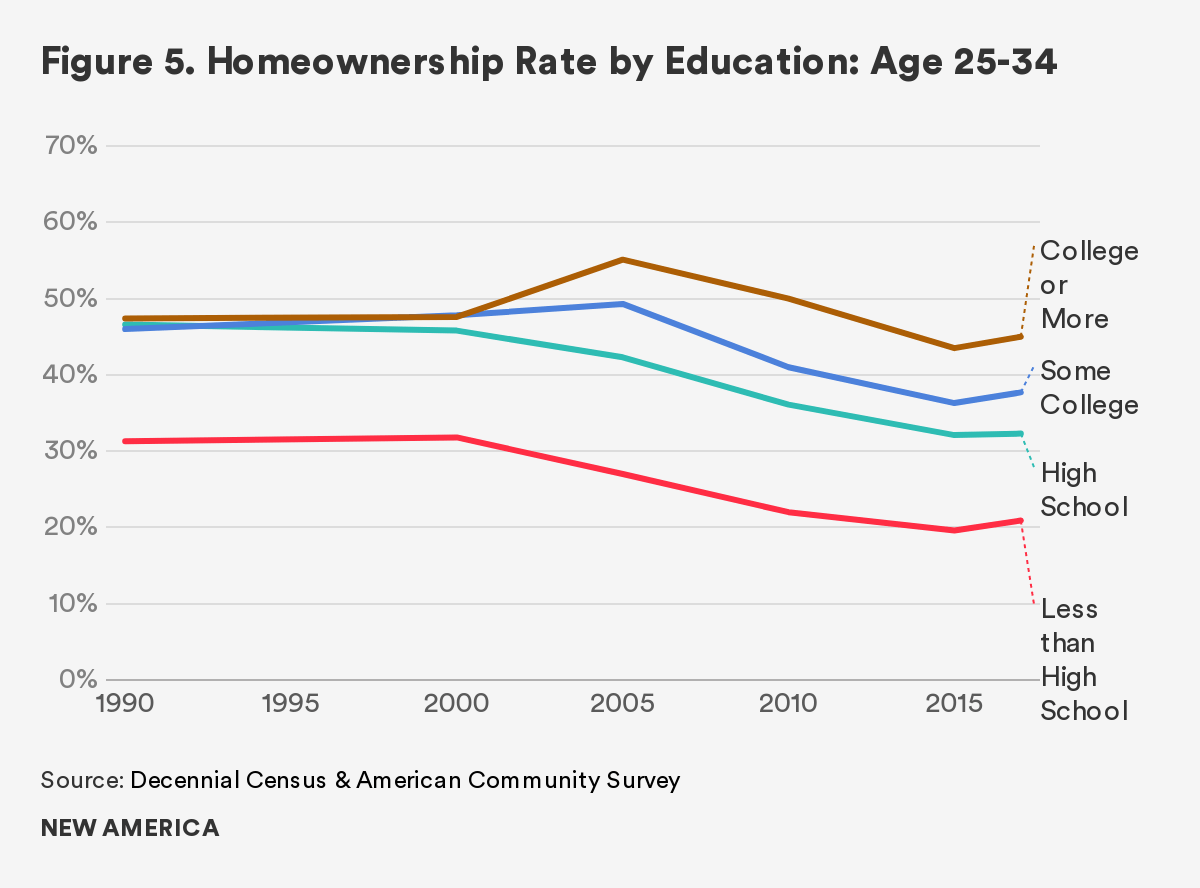

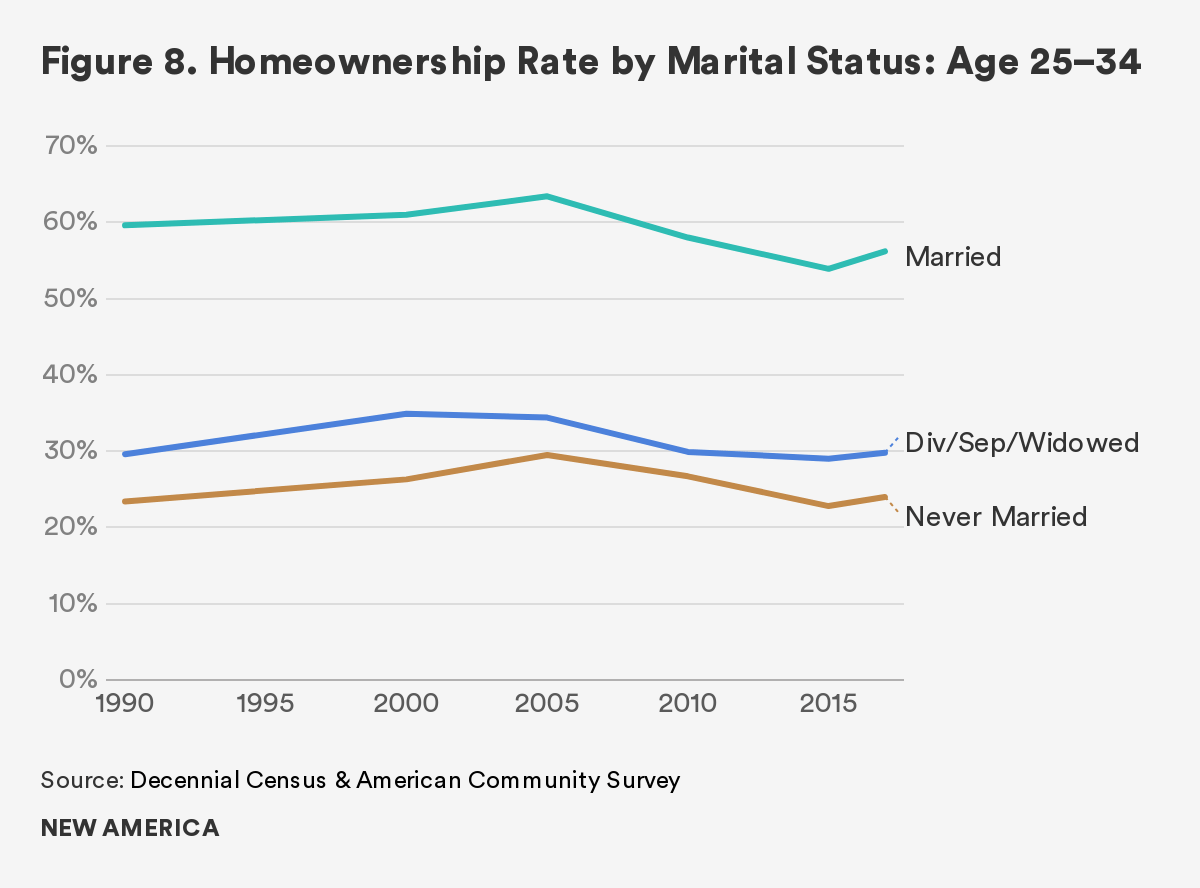

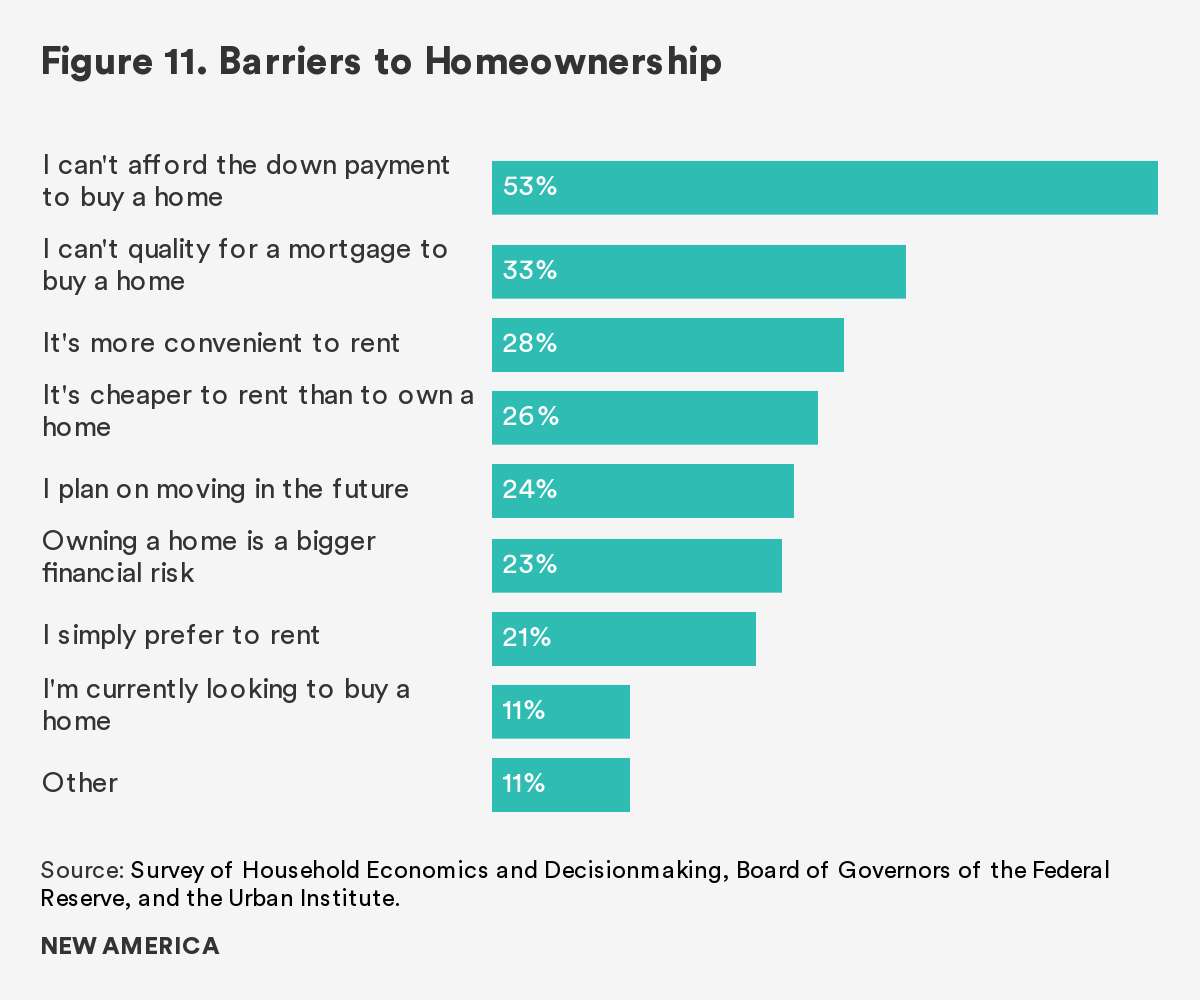

Along with fewer children, marriages, and independent households, fewer Millennials have become homeowners compared to previous generations at the same age. While the homeownership rate peaked at 47 percent in 2005, it fell to 37 percent by 2015. In addition to changing preferences, the severity of this decline likely reflects the increased difficulty in saving for a down payment or qualifying for a mortgage loan, which became progressively harder in the years following the financial crisis.

These trends in marriage, children, and home purchase—previously key features of the American Dream—provide hints at the new economic realities that are complicating how young people assemble the traditional building blocks of success. The divergent outcomes experienced by Millennials have made financial security its own aspiration.

Diverse Outcomes among Communities of Color

To acknowledge the diversity of the Millennial generation is to acknowledge that the experiences of Millennials of color are particularly distinct—and perilous. Specifically, Millennials of color are faring decidedly worse than many White and Asian American Millennials on a number of socioeconomic measures, such as educational attainment, employment levels, household income, and homeownership rates.26

While the economy and employment levels have gained ground in recent years since the post-recession lows, poverty levels for African Americans and Hispanic Millennials, aged 25–34, are 24 percent and 21 percent respectively, far outpacing the 11 percent poverty rate for White Millennials.27 Among Millennials of color, unemployment rates are substantially higher, as is involvement with the criminal justice system.

Given the range of these socioeconomic outcomes, race and ethnicity should be included as an essential component of any generational analysis. Taking a closer look at the impact of race and ethnicity on a person’s financial profile reveals clear disparities in some of the fundamental components that make up a person’s balance sheet, such as amount of savings, homeownership status, and debt levels. These analyses offer an opportunity to break down simplistic explanations of universal experience and increase our understanding of the diverse variables contributing to the emerging Millennial wealth gap.

The Emerging Millennial Wealth Gap

The most recent findings from the Federal Reserve Board’s Survey of Consumer Finances confirm that the wealth holdings of young adults in America today have fallen dramatically below historic trajectories. The accumulated wealth of Millennials has failed to match previous generations of young adults and significantly lags behind older households. Digging deeper into the data reveals several other significant factors, namely the influential experience of the Great Recession, a new dynamic between wealth and age, the continued role of homeownership, and the enduring and expanded racial wealth gap.

The Impact of the Great Recession

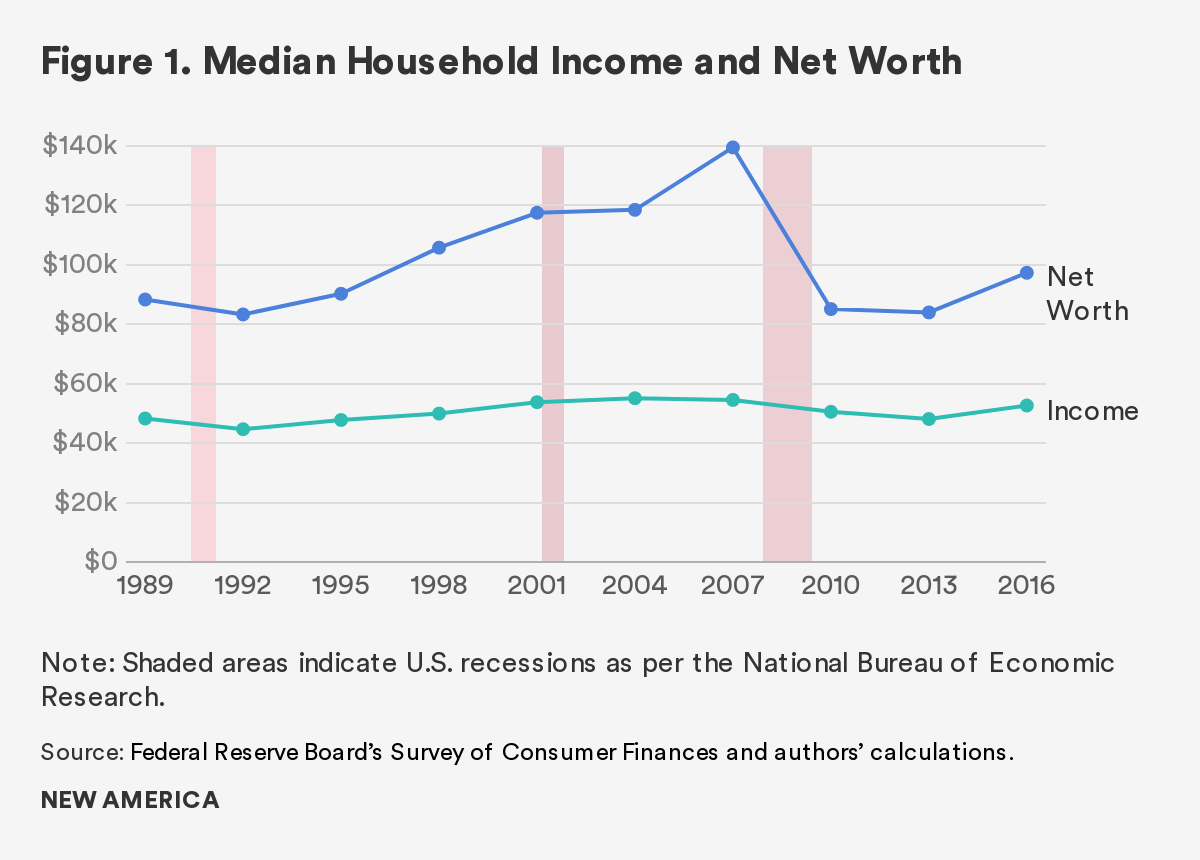

From a variety of perspectives, it is clear that the Great Recession was responsible for dramatic declines in wealth that were broadly experienced. Regardless of household characteristics, such as income, race, and ethnicity, and educational attainment, families lost net worth with the onset of the economic downturn. Although the recession began in 2007 and officially lasted only until 2009, the wealth of a typical family was 30 percent lower in 2016 ($97,300) than it was in 2007 ($139,000), when measured in constant dollars.28

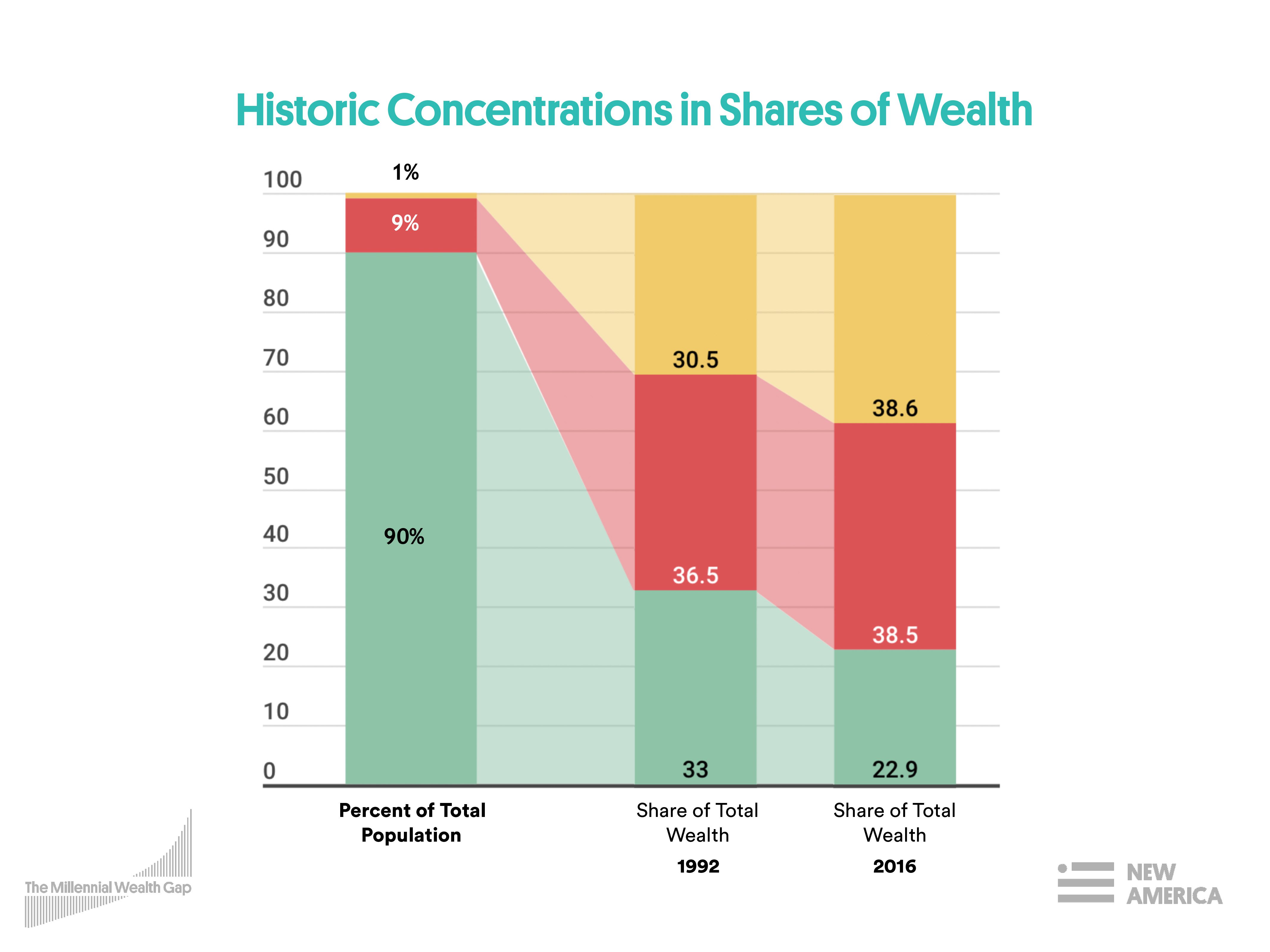

Even as the economy steadily added back jobs lost, the protracted recovery was experienced unevenly, with well-off households doing better at the expense of others. According to economists at the Federal Reserve, the concentration of “shares of income and wealth held by affluent families have reached historically high levels.”29 This is particularly apparent when looking at the top 10 percent of households, as ranked by both income and wealth.30

Ranked by income, the top 10 percent received 50 percent of the country’s total income. In 1992, this figure was 38 percent. During the same period, the top 1 percent of income earners have fared even better, doubling their share. They garnered 24 percent of total income in 2016, up from 12 percent in 1992. Ranked by wealth, the richest 10 percent held over 77 percent of wealth, while the richest 1 percent of households owned almost 40 percent of the nation’s wealth in 2016. In 1992, it was 30 percent. Conversely, the wealth share of the bottom 90 percent of families has been falling over the past 25 years, dropping from 33 percent in 1989 to 23 percent in 2016.

Divergent Fortunes of the Young and the Old

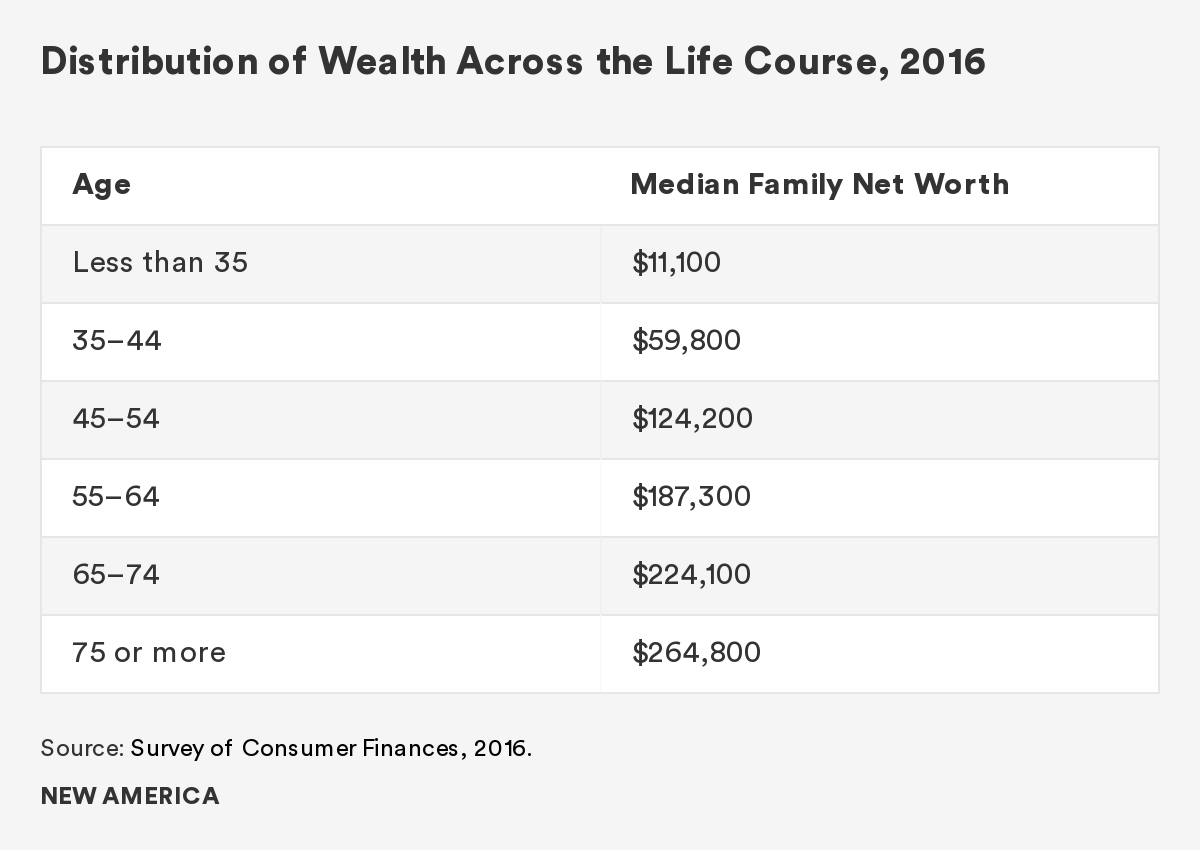

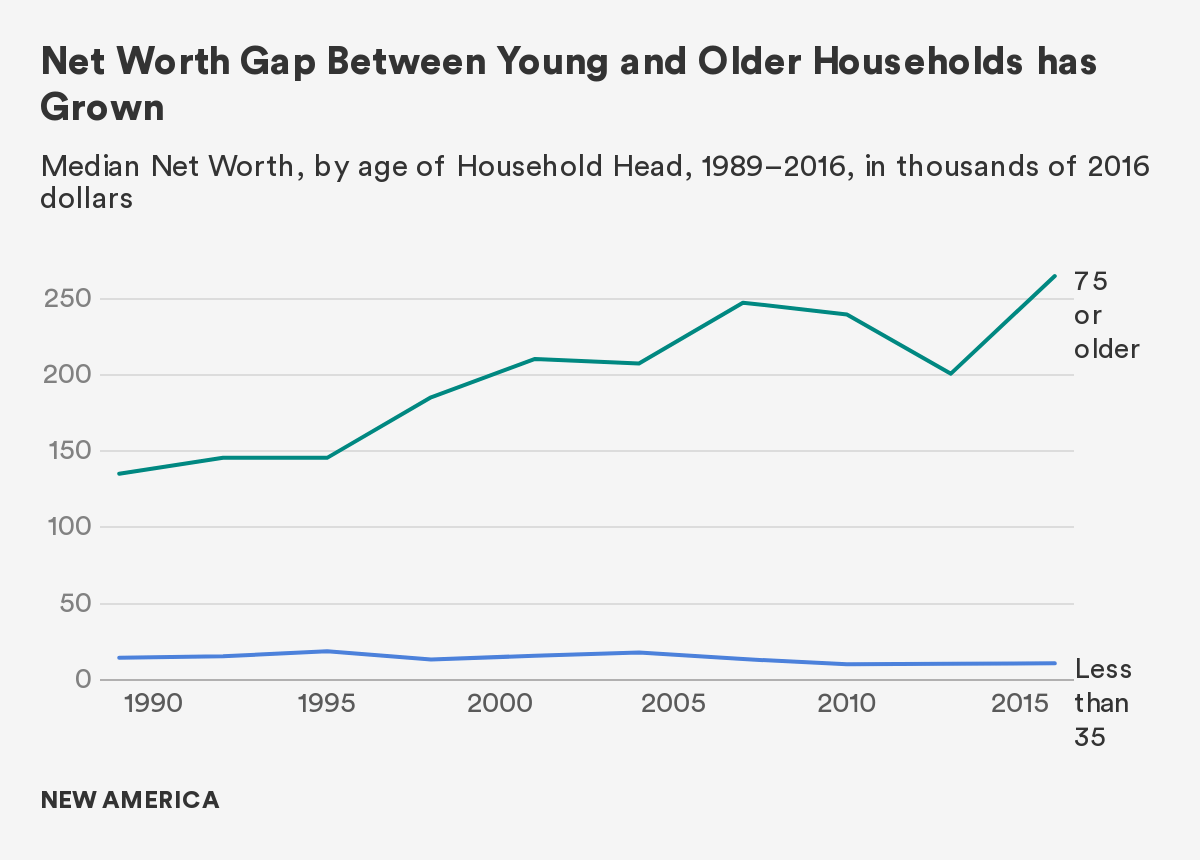

Beyond these levels of concentration at the top, a snapshot of the wealth distribution as grouped by age offers an indication of a new life cycle pattern for the typical family. While there remains evidence of increasing assets as a head of household ages through their mid-30s to mid-50s, median wealth has continued to grow for households aged 75 and older, and it has done so at a higher rate. This is remarkable, since it counters the expectation that these households will begin to draw down on their wealth as they leave the workforce and their incomes decline.

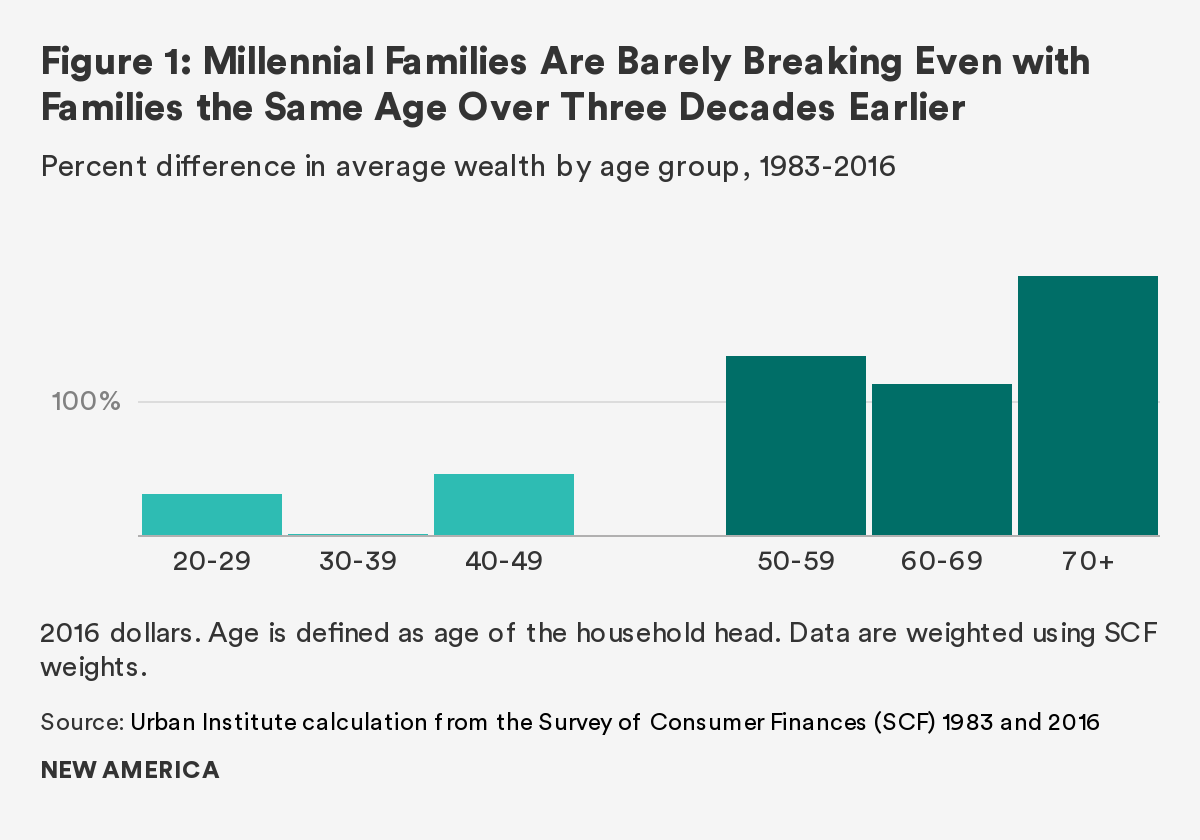

While the net worth for all households has increased by 16 percent from 2013 to 2016, young families haven’t fared as well. The median net worth for families headed by a person under the age of 35 is $10,900, which is a 2 percent rise over the previous three years but still $8,000 less than it was in 1995, a 41 percent decline (in 2016 dollars).31 In contrast, households over age 75 have seen their wealth dramatically rebound, rising 32 percent in the last three years to $264,000.32

For families headed by an individual under the age of 35, net worth was 41 percent lower in 2016 than 1995. In contrast, households headed by someone over age 75 have seen their wealth rise. The recent growth of net worth among older households has been especially pronounced. It has increased 32 percent from 2013 to 2016, reflecting new growth in the generational wealth gap.

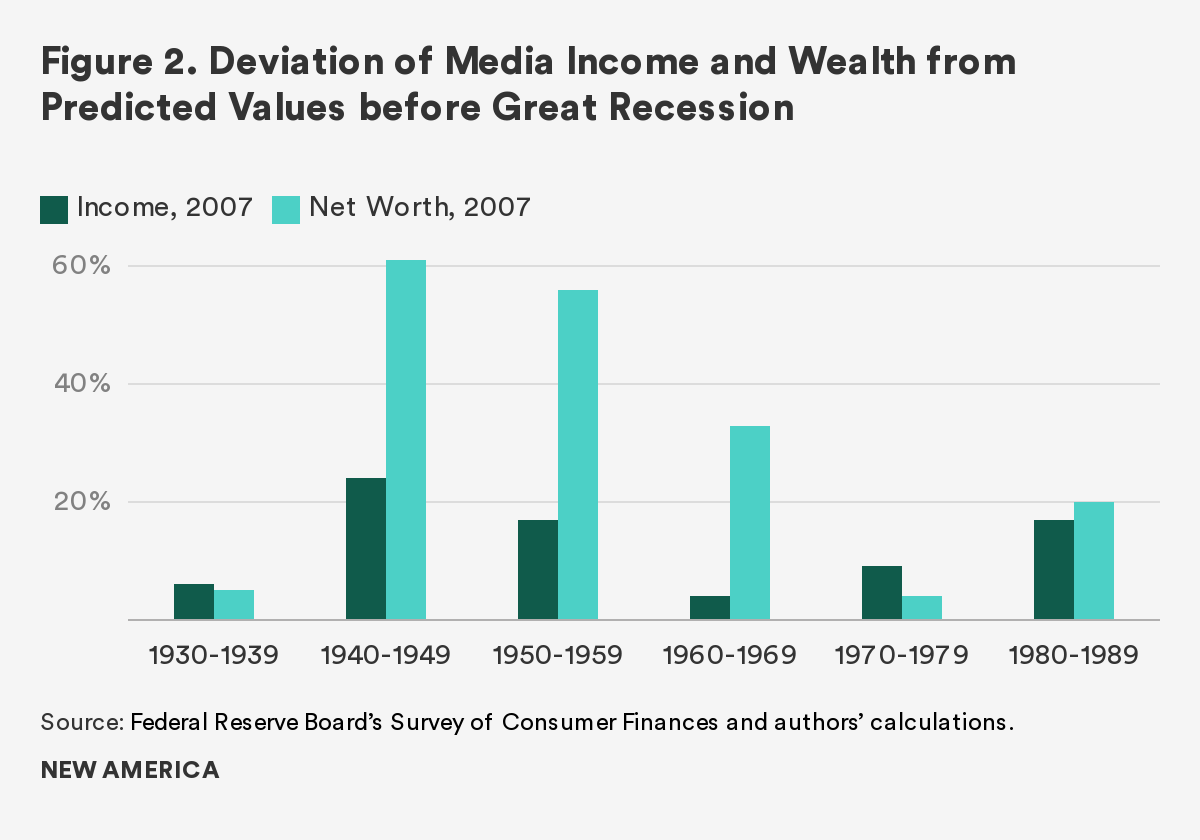

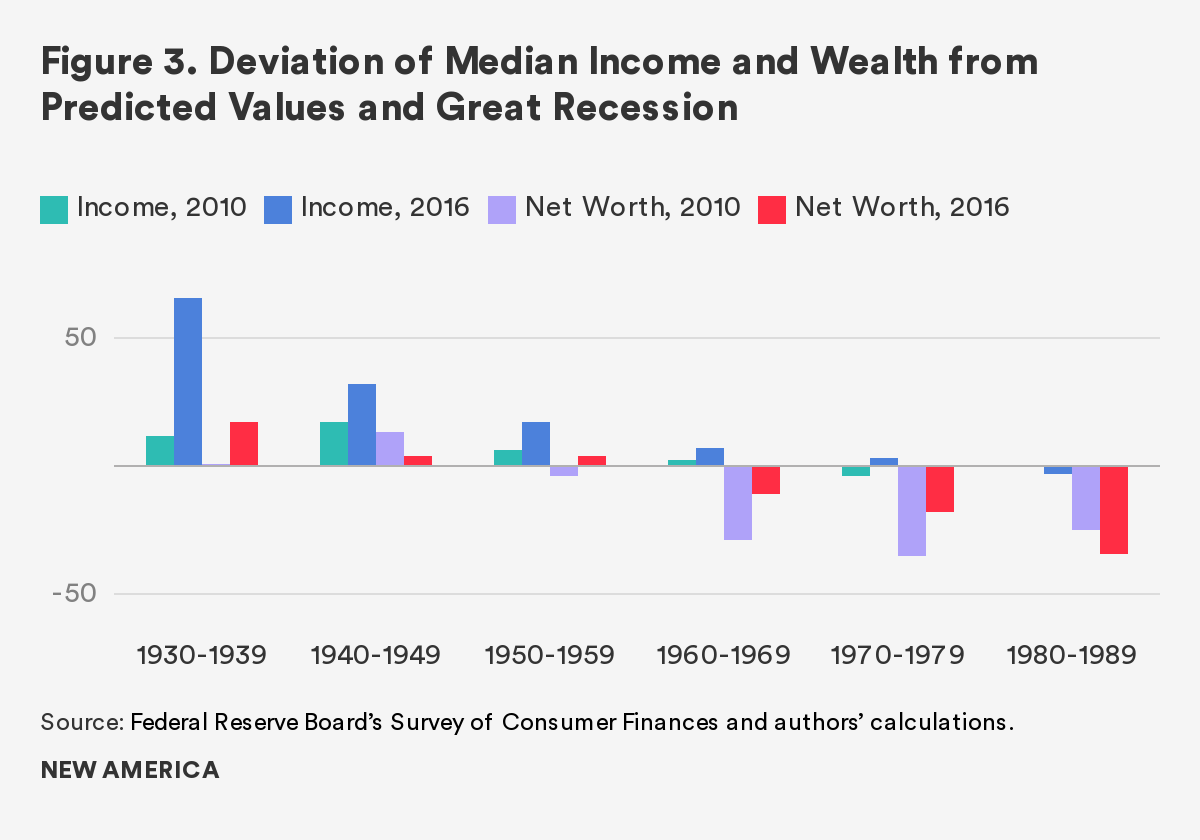

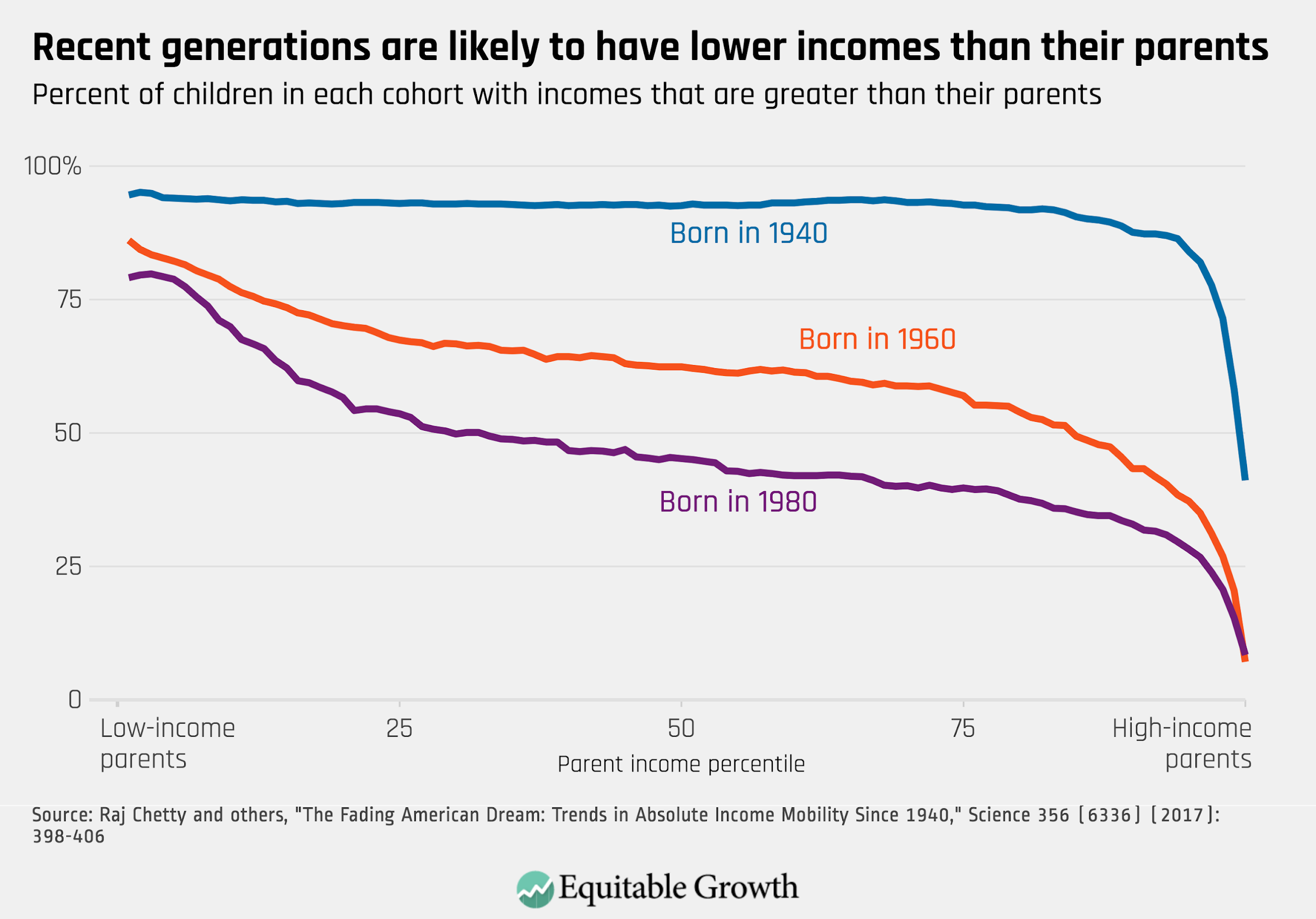

In their analysis of the historic links between birth year and wealth, economists from the Center for Household Financial Stability at the Federal Reserve Bank of St. Louis identified the amount of wealth we would expect a family to own at each age. They found that typical families headed by someone born in the 1960s, 1970s, and 1980s were “significantly below their wealth benchmarks in 2016.”33 More specifically, the 32-year-old cohort remained 34 percent below predicted levels in 2016. Alternatively, families headed by someone older (cohorts born in the ’50s, ’40s, and ’30s) were significantly above their age-specific targets.34

Another indication of trouble for Millennials revealed by their analysis is that the typical 32-year-old lost further ground between 2010 and 2016, a period of generally rising asset values in the stock and housing markets, while older cohorts saw their balance sheets strengthen. This leads them to conclude that while all age groups lost wealth after the Great Recession, younger families suffered the steepest losses, and are regaining lost ground more slowly.35 Since these younger families are entering or are in their prime earning years, this raises the question of whether they will be able to get back on track or risk becoming a “lost generation” in terms of wealth accumulation.

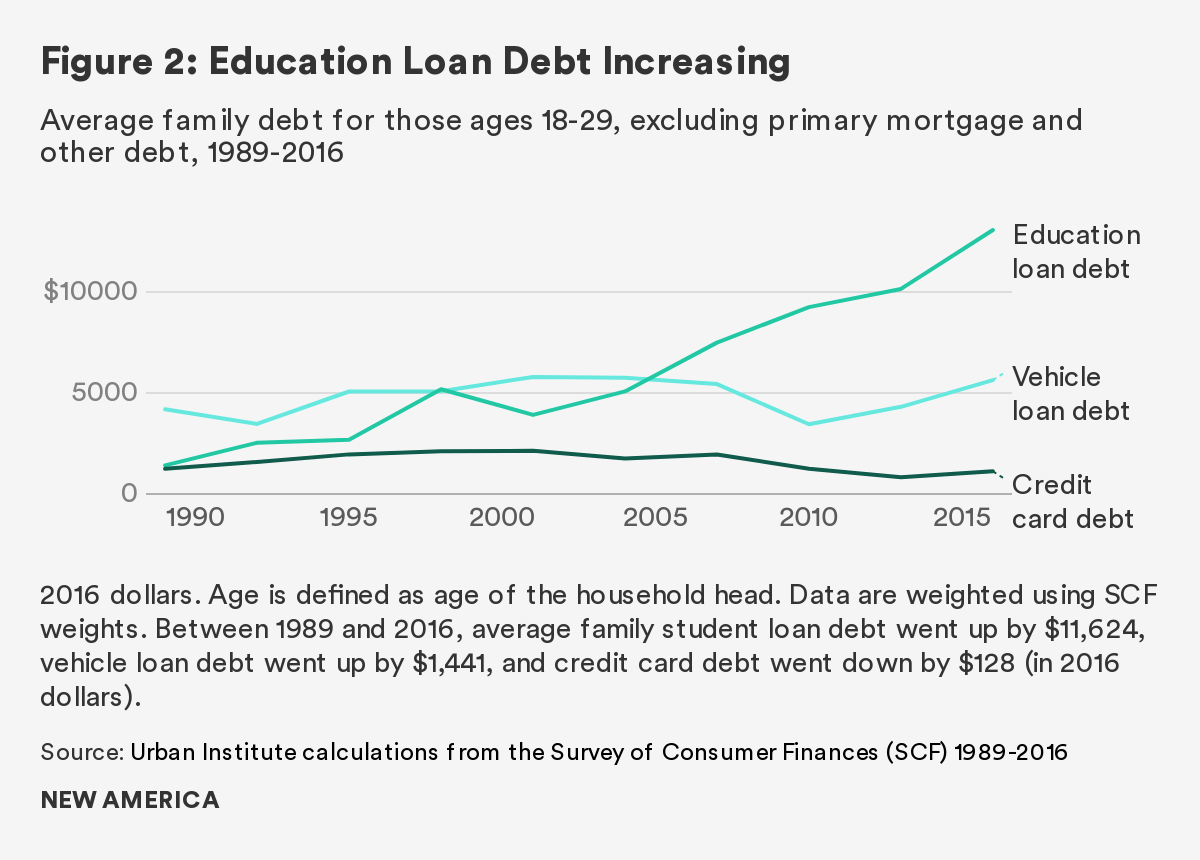

Rising Debt but Declining Homeownership

Rather than wealth, Millennials are accumulating debt. Not only does the typical Millennial have higher debt relative to both their income and their assets than any other previous generation at the same age, but their debt profile is distinct. In previous generations, starting families and forming households was associated with buying homes and taking out a mortgage. For Millennials, other forms of debt have replaced mortgage debt, including student loans, car loans, and credit card debt. These types of consumer debt cannot be used to finance the purchase of assets, like homes, that can appreciate in value. While there are advantages to investing in human capital development, student loans cannot be leveraged directly to boost wealth on the balance sheet.

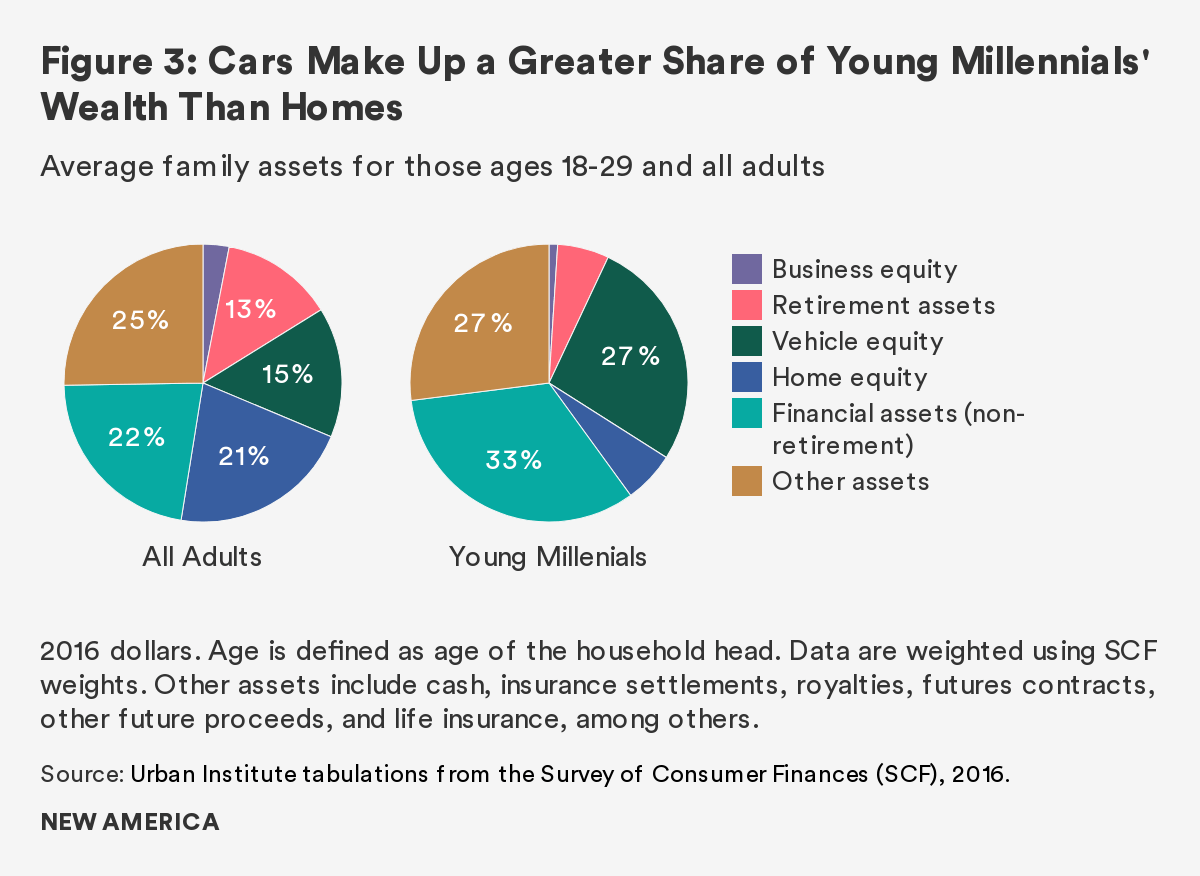

Over time, it may turn out that Millennials will benefit from responding to the recession by staying in school and pursuing more postsecondary degrees. They are clearly better educated and credentialed than earlier generations. However, this debt and delayed earnings have created a weak generational balance sheet and prevented more of them from the experience of homeownership, which is one of the most significant predictors of future wealth building.

The declines in homeownership may be especially consequential, in that they could pose an enduring challenge for Millennials’ wealth building. This is because for those families that do accumulate significant wealth holding, owning a home is often the largest asset on the family balance sheet—so much so that it is relatively uncommon for renters to accumulate even average amounts of wealth. While the typical homeowner had a net worth of $231,400 in 2016, the typical renter had a net worth of $5,200, making this single variable among the most significant in explaining different wealth trajectories among American households.

The disparity in wealth holdings among renters and homeowners should prompt a series of policy questions—e.g., what are the current impediments to homeownership? Are there alternative leverage opportunities besides housing to build wealth? How has historic discrimination against race and ethnicity groups historically cut off avenues to wealth building,s and what should be done about it now?

This last question is especially pertinent because homeownership rates vary significantly by race and ethnicity. As of 2016, homeownership rates ranged from approximately 45 percent for Black and Hispanic families to 73 percent for White families. Among those who do own their homes, White families have more housing equity ($215,800), compared to Hispanic families ($129,800) or Black families ($94,400).36 The racial wealth gap has been an enduring feature of American society, and with the increasing diversity of the rising generations, it is one of the primary drivers of the emerging Millennial wealth gap.

While subsequent chapters in this book will present a deeper analysis of both Millennial debt and declines in home purchases, the main point here is that these trends reflect the extent to which Millennials are in a fundamentally different economic “place” than previous generations. They are on a lower trajectory of asset building.

The Racial Wealth Gap

Describing the racial wealth gap with numbers on a balance sheet doesn’t do justice to the historic legacy of slavery and the entire African American experience. The history is brutal. Nor does it capture the experiences of the native people of the Americas, or those of the immigrant families of non-European origins who came to America from across the globe. Still, using the tools and categories of social science and economics to aggregate and broadly compare experiences among racial and ethnic groups in America is dramatically revealing. The racial wealth gap is a chasm, with roots at the core of American history, culture, and economy.

Throughout the country’s past, the traditional paths to wealth building—land, higher education, access to credit, and homeownership—have been systematically denied to African-Americans and other non-White persons. Even when wealth and resources have been accrued, they have also been systematically stripped through land theft and lynching. Disparities in wealth among race and ethnic groups in the U.S. are, simply put, enormous. It is this historic racial wealth gap, with its devastating consequences, that is compounding the emergence of the Millennial wealth gap launched by the Great Recession.

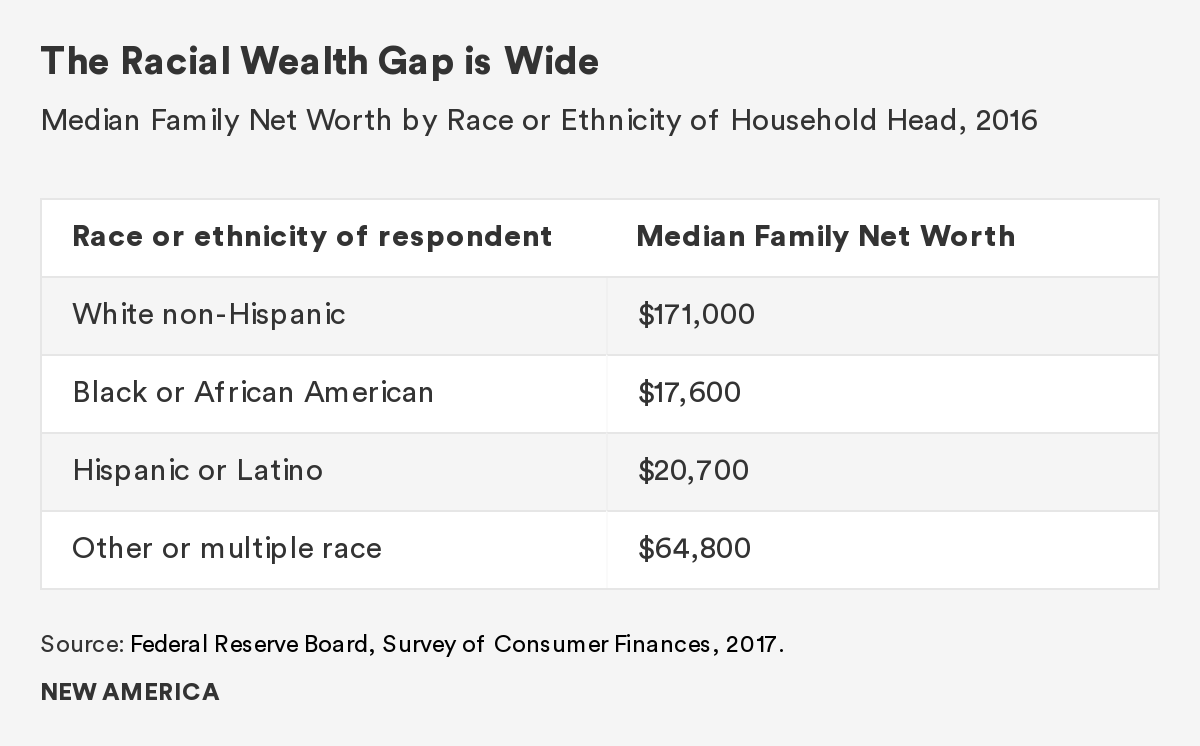

The most recent available data from the Federal Reserve’s Survey of Consumer Finances shows that in 2016 the median net worth of non-Hispanic White households was $171,000, almost 10 times the net worth of Black families ($17,600) and over eight times the net worth of Hispanic households ($20,700).37 For all race and ethnicity groups, the mean is substantially higher than the median, which reflects the concentration of wealth among the wealthiest in each category.

The racial wealth gap in 2016 is larger than it was in the early 2000s, when the average non-Hispanic White household had “only” six to seven times the wealth of the average African American household.

Looking exclusively at “median” or “average” figures masks variation. Although most families do have some wealth, some have zero or negative wealth (where debts exceed assets). These shares vary by race/ethnicity. Almost 20 percent of Black households and 15 percent of Hispanic households had zero or negative net worth, compared with 9 percent for White households.38

These outcomes cannot be viewed in isolation from the history of race in America. To take one example, housing, the earliest federal homeownership programs that began in the 1930s prevented minorities from accessing mortgage financing that enabled White families to build their wealth through housing equity. The Fair Housing Act of 1968, passed in the days following the assassination of Martin Luther King, Jr., made this discrimination illegal, and modest gains in homeownership for families of color eventually followed. Unfortunately, less attention was paid to policing the financial services marketplace, which allowed predatory lending practices and poor mortgage underwriting to spread without oversight.

As the housing market collapsed with the advent of the Great Recession, Black homeownership rates fell more than non-Hispanic Whites’, and their houses lost more value. In 2017, homeownership for Black American households was 28 percent lower than it was for non-Hispanic Whites, and many of the gains in Black homeownership since the Fair Housing Act was passed have been erased.39

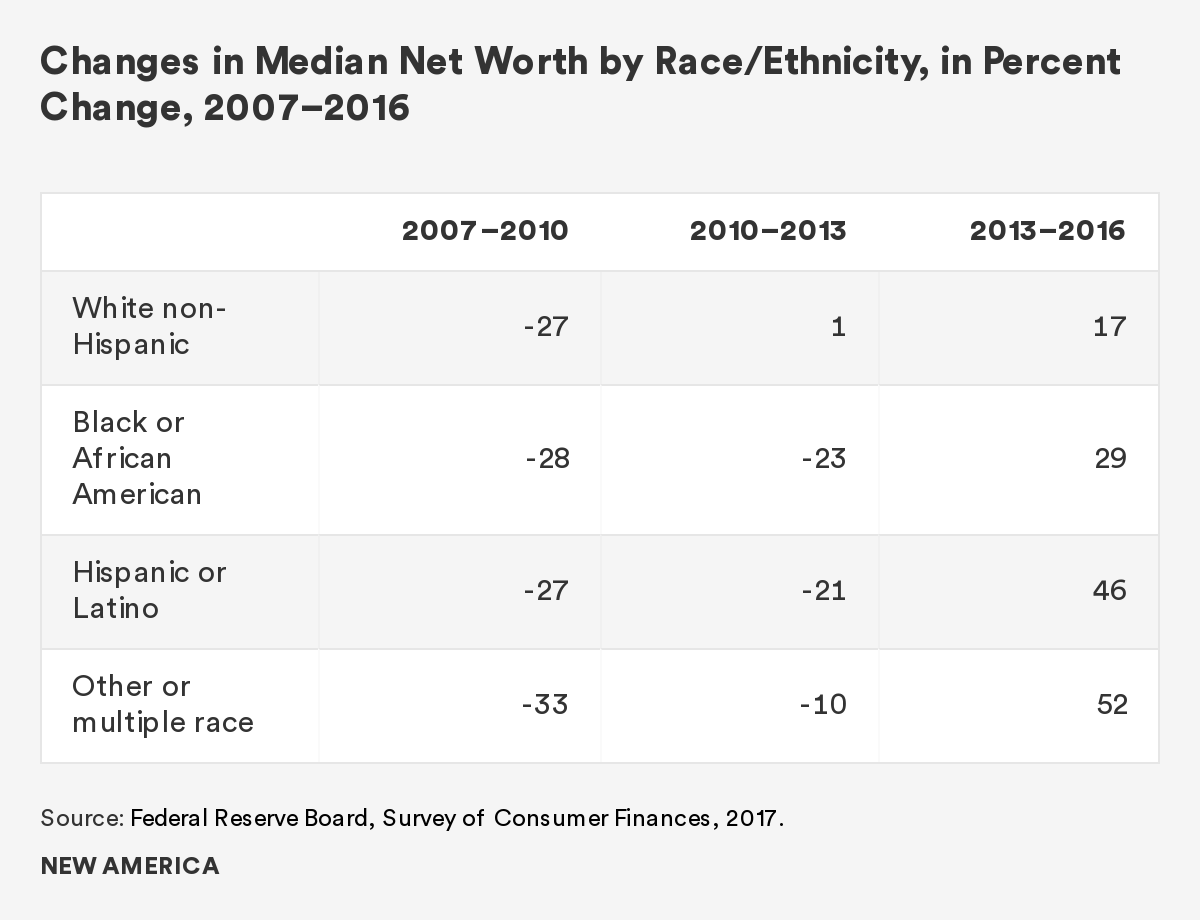

Not only did the Great Recession wipe out gains that had been made by communities of color in terms of their collective wealth holdings, but also for many minority families it has been harder to navigate the aftermath. While all groups lost net worth after the Great Recession, White families began to recover between 2010 and 2013, while minority families continued to experience net worth declines. It took until the 2013–16 period for all groups to experience gains. In fact, minority groups outpaced gains by White families over this period, but their delayed recovery reflects another source of inequality.

Additionally, declines in homeownership have been most pronounced for younger Black households. According to the Urban Institute, the homeownership rate for families headed by Black Americans between the ages of 35 and 44 fell from 45 percent in 1990 to 33 percent in 2015, lower than the Black homeownership rate in 1960.40 On top of that, in recent years, only 22 percent of younger Black Americans aged 24 to 34 were homeowners.41

Beyond homeownership, there are many variables that appear to influence wealth accumulation, which also vary by race and ethnicity. For example, 60 percent of White families own a retirement security account, while only 34 percent of Black families and 30 percent of Hispanic families do.42 Additional factors that vary by race and ethnicity are family formation, postsecondary education, and intergenerational transfers of money through inheritance and gifts during life. Twenty-six percent of White families report having received an inheritance, compared with 10 percent of Black and Hispanic families.43 Clearly, the historic legacy of slavery and sanctioned discrimination has undermined the ability of communities of color to build wealth and pass it along intergenerationally.

While the racial wealth gap is a long-standing feature of American society that impacts the current distribution of economic resources, there is evidence that it is not merely a historic phenomenon. As will be described in subsequent chapters, new developments have taken hold in the run-up to, and aftermath of, the Great Recession, and have exacerbated wealth disparities among racial and ethnic groups. Given the increased diversity of the Millennial generation, this new and expanded racial wealth gap deserves greater attention and should prompt a commensurate policy response.

Implications for a Policy Response