Displaced in America – Executive Summary

Table of Contents

- Executive Summary

- Introduction: Past, Present, and COVID

- Methodology and Definitions

- Housing Loss and Poor Data

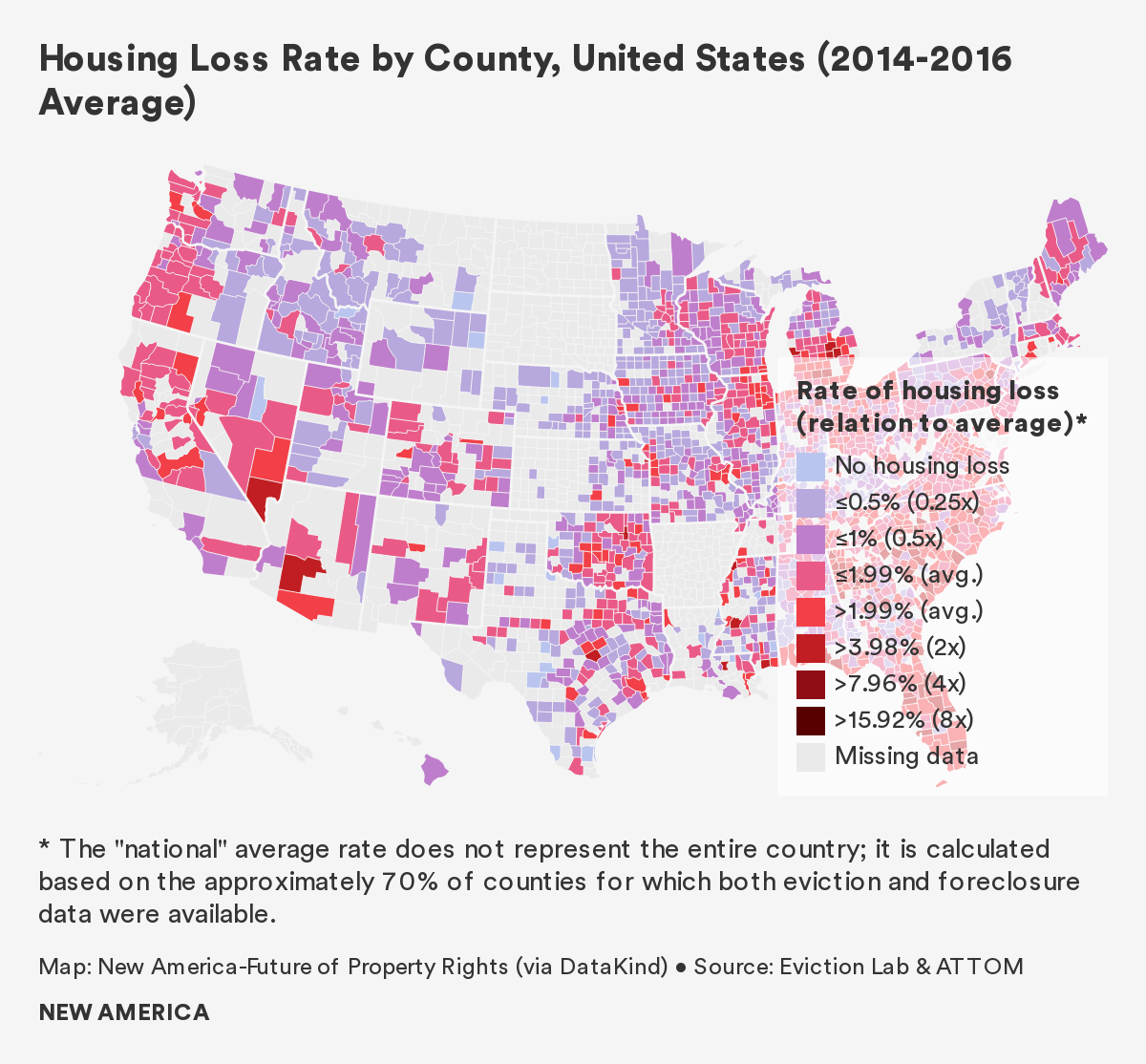

- Housing Loss in the United States: Our National Rankings and Maps

- Housing Loss in Forsyth County, North Carolina

- Housing Loss in Maricopa County, Arizona

- Housing Loss in Marion County, Indiana

- Policy Recommendations

- Conclusion

Abstract

Each year, nearly 5 million Americans lose their homes through eviction and foreclosure. These forced displacements are intensely traumatic financially, physically, and emotionally. Children have to switch schools, parents lose their jobs, families’ possessions end up on the sidewalk, and suicide rates spike.

Yet, as our nation braces for a tsunami of housing loss as a result of the COVID-19 economic fallout, we know very little about these life-changing events. Where is forced displacement most acute? Why does housing loss occur? Who is most at risk? And what happens to people after they lose their homes?

This report, Displaced in America, visualizes housing loss at the county level nationwide, and includes a new metric on forced displacement: a National Housing Loss Index, which ranks U.S. counties based on their combined eviction and foreclosure rates. Also included are census tract-level quantitative and qualitative findings for the three case study locations of Forsyth County, North Carolina; Maricopa County, Arizona; and Marion County, Indiana.

We know that housing loss—both evictions and foreclosures—persistently affects the same communities, and that the people and places most vulnerable to housing loss to begin with are often the ones who experience it most acutely in times of crisis. By identifying and examining which places have traditionally experienced the most acute housing loss, we can predict where future housing loss will occur as a result of the COVID-19 crisis and who will be impacted, and direct resources to prevent the harm before it proliferates.

Acknowledgments

Contributing Authors

Abbey Chambers, Alexandria Drake, Jack Portman, Alex Cattermole, Roderick Setzer, Michael Dowd, Dona Stewart

Technical Reviewers

Sherri Lawson Clark, Molly Martin, Lora Phillips, Craig Richardson, Scott Schang, Patricia Solis, Andy Beck, Emily Benfer, Stephanie Brewer, Natalie Chyi, Leah Humphrey, Dan Kornelis, Breanca Merritt, Amy Nelson, Sylvia Oberle, Dan Rose, Joan Serviss, and Pambana Uishi

Acknowledgements

This report results from a year’s worth of meetings, phone calls, email exchanges, research, and collaboration. We received feedback, advice, and assistance from countless individuals.

In particular, we would like to thank the following individuals for helping us to initially brainstorm this project, and for providing us with feedback throughout the research process: Joshua Akers, Dan Alban, Andrew Aurand, Brian Blacker, Paul Bradley, Maya Brennan, Mychal Cohen, Nick Downer, Noah Durst, Tim Fella, Brandon Frazier, Judy Fox, Jorge Gonzalez, Solomon Greene, Jim Kelly, Thomas Mitchell, Elizabeth Nash, Jerry Paffendorf, Anthony Piaskowy, Tony Pickett, Enrique Silva, Katherine Smyth, Esther Sullivan, Joshua Walden, Heather Way, Jake Wegmann, and Brad Westover.

In Indianapolis, we would like to thank our New America colleague Molly Martin, an absolutely invaluable partner, for introducing us to the city and its many stakeholders. Deputy Mayor Jeff Bennett, Amy Nelson, Hailey Butchart, Chase Haller, and Breanca Merritt were also critical to our research. We would like to thank Jacob Sipe, Tim Evans, Larry Williams, Michael Chapuran, and Gina Davis for their time and insights, as well. Drew Carlson was extremely helpful in sharing tax foreclosure data for Marion County, and so was Matt Nowlin in providing data on COVID-related unemployment.

In Winston-Salem, we would like to thank Scott Schang, Craig Richardson, and Sherri Lawson Clark for their collaboration, and for connecting us to the area’s housing space. We would also like to thank the CSEM team for their advice and insights: Alvin Atkinson, John Railey, Zach Blizard, and Benjamin Lewis. Dan Kornelis, Dan Rose, and Sylvia Oberle were a huge help to our research, and thank you as well to Marla Newman, Kevin Cheshire, Tina Adkins, Chelsea Franzese, Emily McCord, Eddie Garcia, Bethany Chafin, Sharon Thomas, Michael Suggs, and Garret Bolden for their contributions to our initial research. Jason Clodfelter was instrumental in providing data on evictions, mortgage foreclosures, and tax foreclosures for Forsyth County.

In Phoenix, we would like to thank our former New America colleague Megan Garcia for showing us around the Valley of the Sun, and for facilitating introductions. A big thank you to Patricia Solis, Lora Phillips, and Crystal Alvarez from the Knowledge Exchange for Resilience at Arizona State University for their partnership and support of our work. Stephanie Brewer, Silvia Urrutia, Terry Benelli, Melissa Kovacs, Erica Quintana, Jon Riggins, Lee Anne Wade, Cosmin Tomuta, Whitney Silence, Joanna Sagar, Jackie Taylor, Laura Skotnicki, and Ty Rosensteel all contributed to our initial research in Arizona. Scott Davis was immensely helpful in providing local eviction data. Last, thank you to Mayor Corey Woods and Vice Mayor Lauren Kuby of the City of Tempe, Arizona, for championing our work.

We would also like to thank the Eviction Lab at Princeton University for sharing critical data on evictions and for providing feedback on our work, particularly Peter Hepburn, Alieza Durana, Lavar Edmonds, and Anne Kat Alexander. Thank you, too, to Cassandra Johnson Gaither from the U.S. Department of Agriculture for sharing findings on heirs property in North Carolina.

This project would not have been possible without our partnership with DataKind. Aman Ahuja was critical during the early phases of this project, asking tough questions and helping us think through any and all challenges. Thank you to the DataCorps volunteer team, Diana Lam, Alice Feng, Dominic White, Anurag Gandhi, and Shreya Vaidyanathan, for their superhuman work on the report's housing loss data and data visualizations. And thank you to Caitlin Augustin and Mallory Sheff for their continued support.

Nor would this work have been possible without funding from Omidyar Network/PlaceFund and technical support from The Rockefeller Foundation. In particular, we would like to thank Amy Regas and Peter Rabley from Omidyar Network/PlaceFund, as well as Hunter Goldman and Evan Tachovsky from The Rockefeller Foundation, for their support.

Last, but certainly not least, we would like to thank all of our former and current colleagues at New America that assisted with this report: Chris Mellon, Andrew Hagopian, Natalie Chyi, Malcom Glenn, Alison Yost, Maria Elkin, Joanne Zalatoris, Naomi Morduch Toubman, Joe Wilkes, Brittany VanPutten, Rina Li, Samantha Webster, Brigid Schulte, and Fuzz Hogan.

Executive Summary

Each year, nearly 5 million Americans lose their homes through eviction and foreclosure. These forced displacements are intensely traumatic financially, physically, and emotionally. Children have to switch schools, parents lose their jobs, families’ possessions end up on the sidewalk, and suicide rates spike. Research links housing loss to a litany of adverse impacts, from financial ruin and increased obesity for adults, to educational attainment gaps and chronic homelessness for children.

And yet, as our nation braces for a tsunami of housing loss as the result of the economic fallout of the COVID-19 pandemic, we know very little about these life-changing events. Where is forced displacement most acute? Why does housing loss occur? Who is most at risk? And what happens to people after they lose their homes?

Displaced in America attempts to answer these questions and in doing so help municipal leaders better understand where the pandemic might exacerbate already established patterns of housing loss.

New America and its partners visualized the scale and breadth of displacement across the United States through a National Housing Loss Index, which ranks U.S. counties based on their combined eviction and foreclosure rates. We also examined census tract-level displacement across three case study locations: Forsyth County, North Carolina (Winston-Salem); Marion County, Indiana (Indianapolis); and Maricopa County, Arizona (Phoenix, Tempe, Mesa).

We found that the United States has an acute housing loss problem. The pandemic has exacerbated the effects of stagnant wages, the lack of affordable housing, insufficient federal housing assistance, and discriminatory policies that contribute to housing loss. And while emergency measures like eviction and foreclosure moratoriums will prevent many from losing housing in the near term, they will not address the systemic policies and economic factors that lead people to lose their homes.

Evictions and foreclosures persistently affect the same areas and communities. While shock events like the 2008 foreclosure crisis and the COVID-19 pandemic add to the volume of housing loss, these surges often follow familiar patterns: the people and places most vulnerable to housing loss during steady-state periods are often the ones who experience it most acutely in times of crisis. By identifying and examining which places have traditionally experienced the most acute housing loss, we can predict where future housing loss will occur and who will be impacted, and direct resources to prevent the harm before it proliferates.

What Does Housing Loss Look Like in the United States?

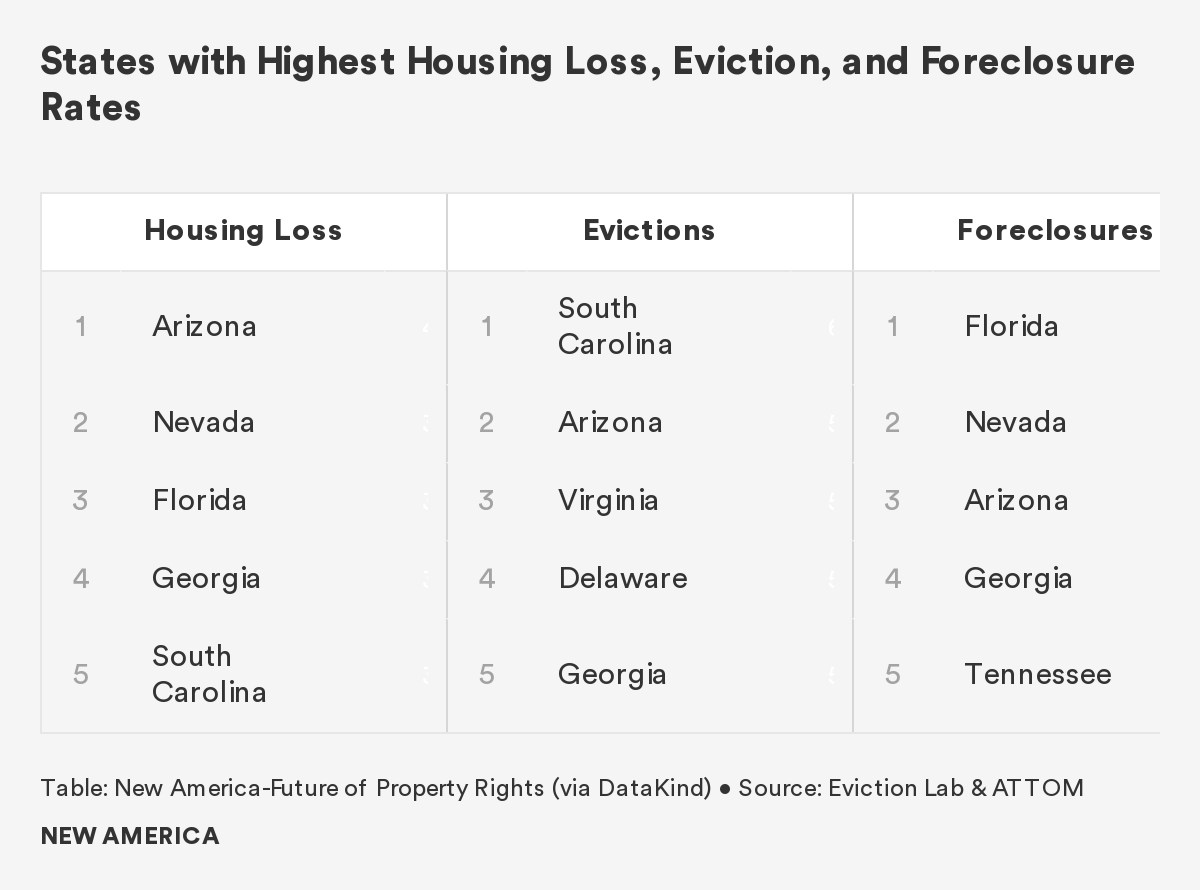

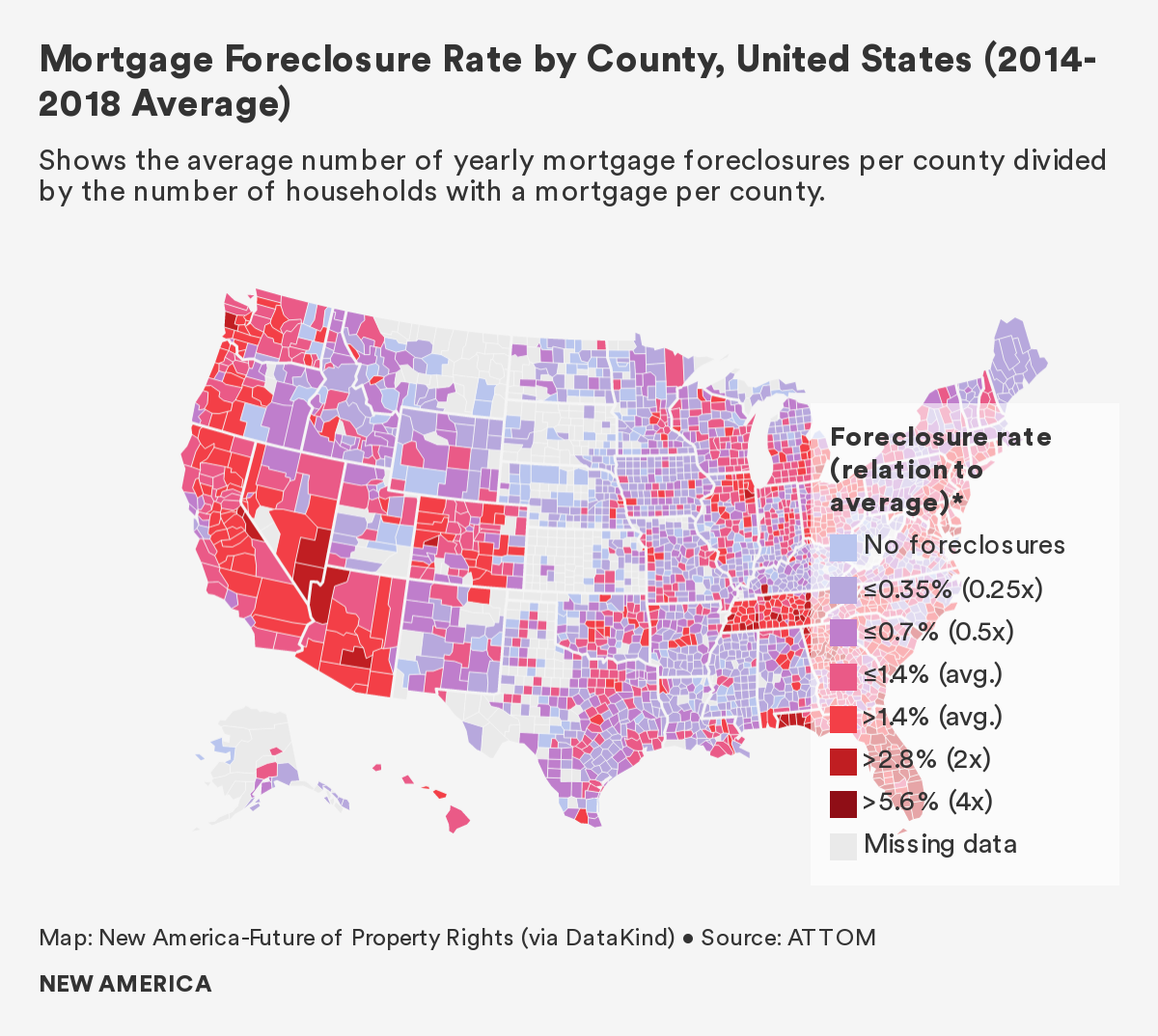

Between 2014 and 2016, the national average housing loss rate was 2 percent, meaning that each year, two out of every 100 households who either rent or have a mortgage experienced an eviction or mortgage foreclosure. Housing loss was most acute in Arizona, Nevada, and Florida, where rates of housing loss were greater than 3.8 percent, almost twice the national average. As of June 2020, each of these states also had unemployment rates at or above 10 percent. Given that non-payment of bills is the most common cause of housing loss, and given their pre-existing housing vulnerability, we expect these states to be disproportionately impacted by the COVID-19 housing crisis.

Based on our examination of data from 2014 to 2016, we found:

- The national average eviction rate was 2.6 percent. More than 900,000 renter households were evicted from their homes each year.

- South Carolina experienced the highest eviction rate of any state (6.2 percent) with an average of 26,430 evictions per year. Other states with high eviction rates include Arizona, Virginia, and Delaware.

- Evictions spike in the summer months. Eviction rates across the country are on average 40 percent higher in July and August than at their low point in March. In some cities, like Dallas, Texas and Richmond, Virginia, eviction rates double from spring to summer.

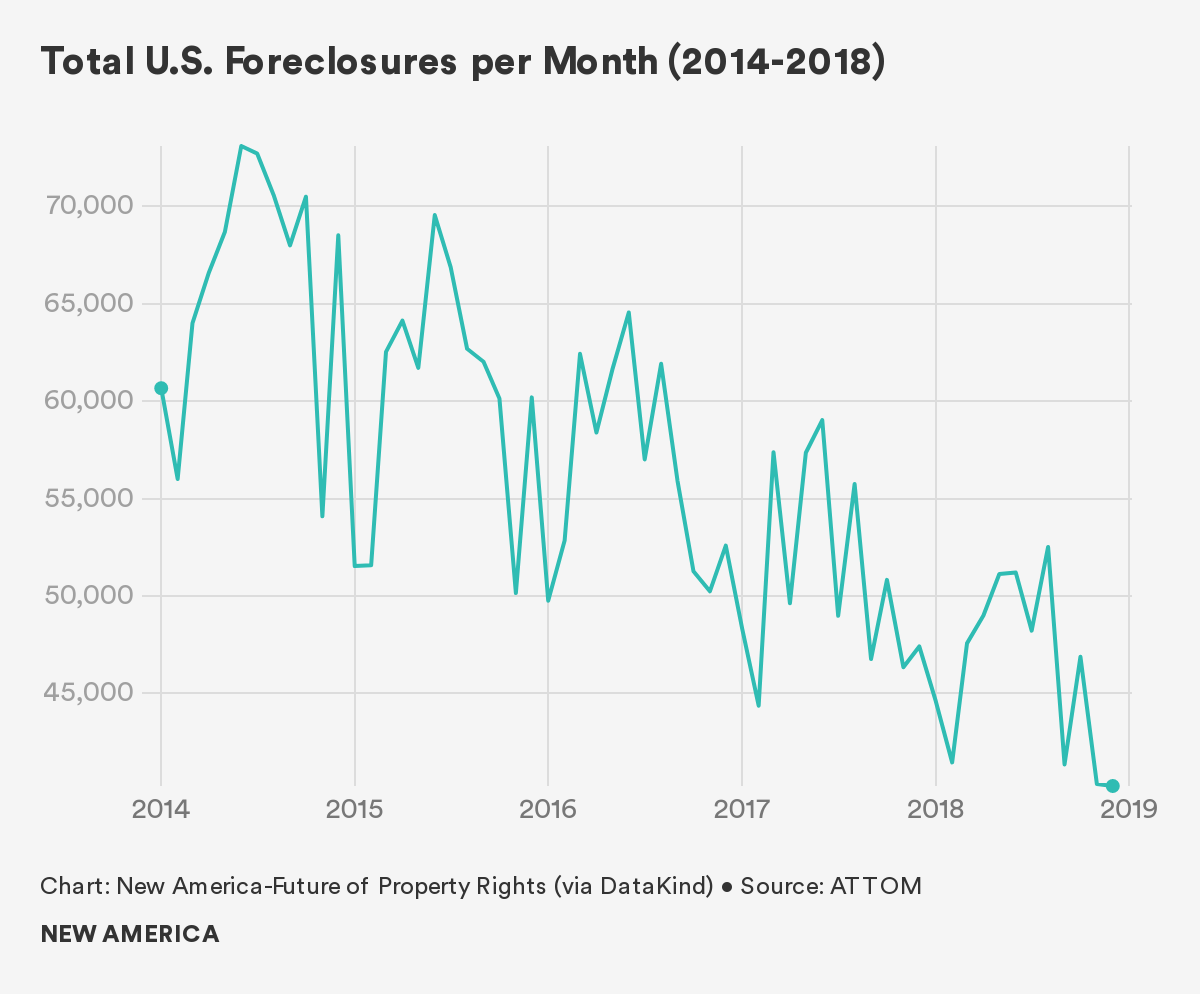

- Between 2014 and 2018, approximately 670,000 households, or 1.5 percent of homeowners with a mortgage, lost their homes to foreclosure each year. Overall, mortgage foreclosure rates fell during these five years, but remain more than twice the foreclosure rates prior to the 2008 housing crisis.

- Florida experienced the highest foreclosure rate nationally, at 3.7 percent. Nearly 105,000 Floridian households lost their home through foreclosure during the study period. Nevada, Arizona, Georgia, and Tennessee also saw high rates of mortgage foreclosure, all over 2.2 percent.

Who is Most at Risk?

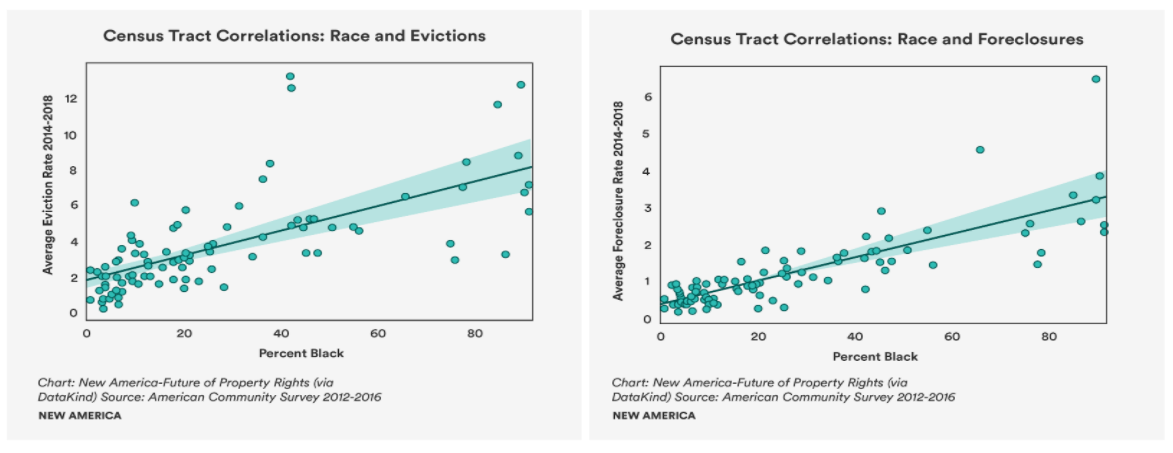

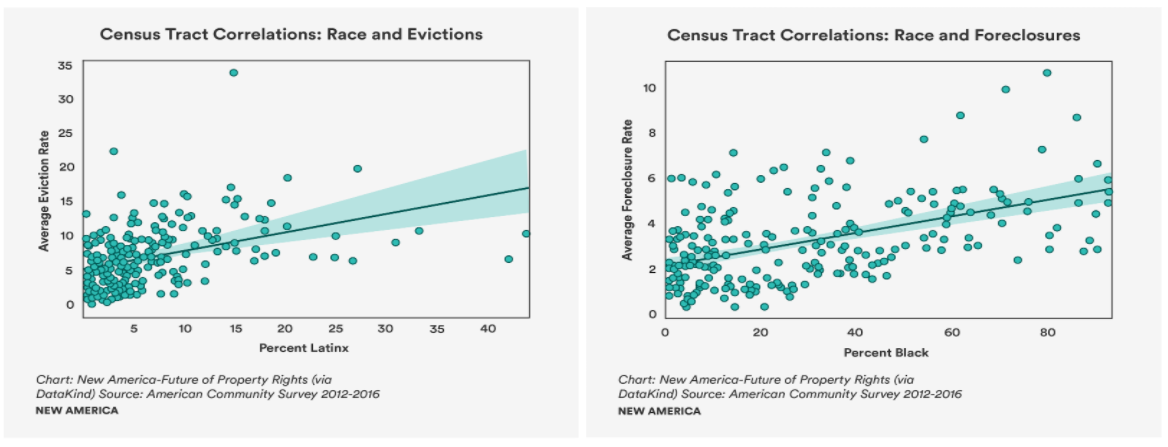

Counties with predominantly non-white households see higher rates of evictions and overall housing loss than those with predominantly white households. This finding was consistent across the national and case study analyses, though we observed important nuances across geographies. As the percentage of rent-burdened households in a county increases, so do rates of eviction and foreclosure. Across the United States, more than 20 million households spend more than 30 percent of their income on rent, of which 10 million spend 50 percent or more of their income on rent.

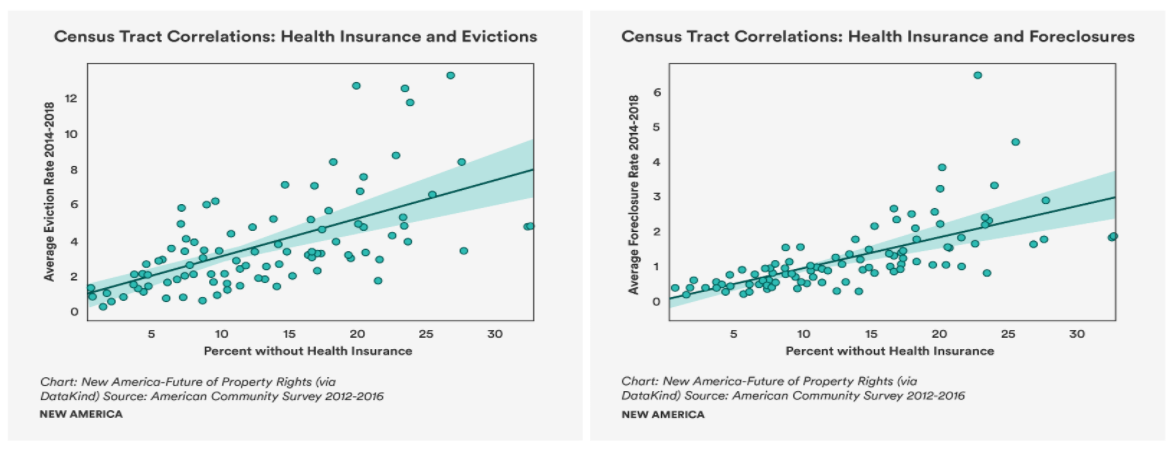

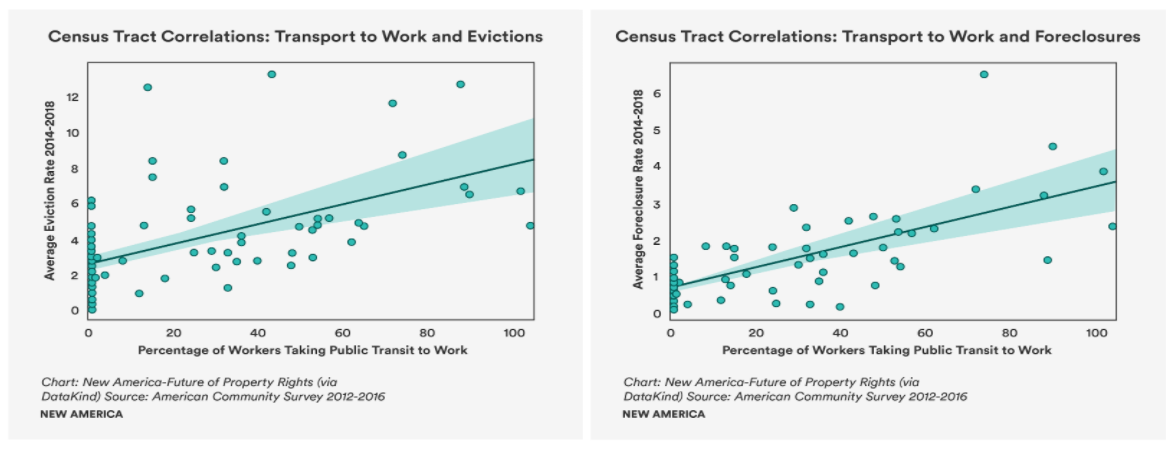

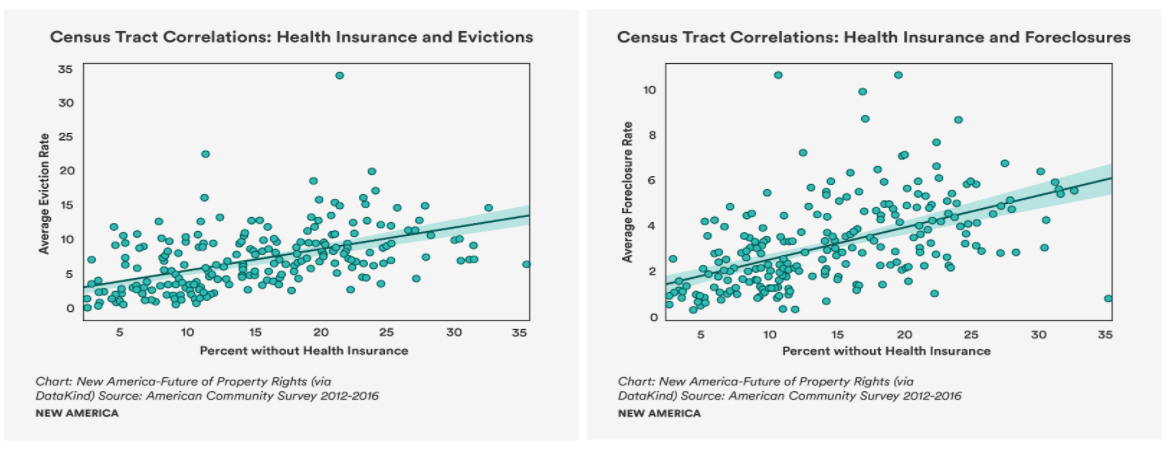

Across all three case studies, census tracts where residents lacked health insurance, and census tracts in which more residents took public transit to work, had higher rates of housing loss.

Counties with high proportions of households living in mobile homes have higher rates of foreclosure. We do not know whether this is because owners of mobile homes are uniquely vulnerable to foreclosure, or because foreclosed-upon homeowners are likely to move into mobile homes; the relationship between housing loss and mobile homes is an emerging area of study deserving of further research.

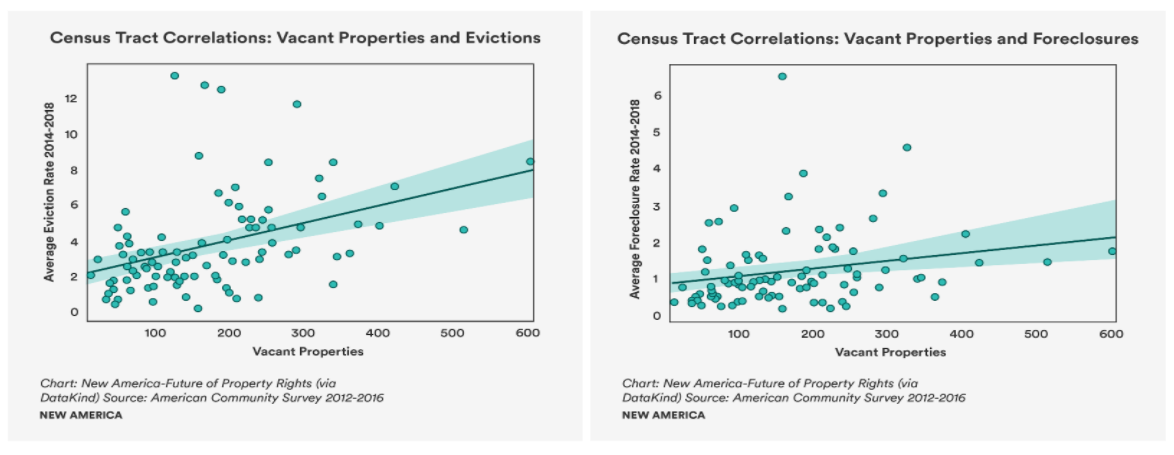

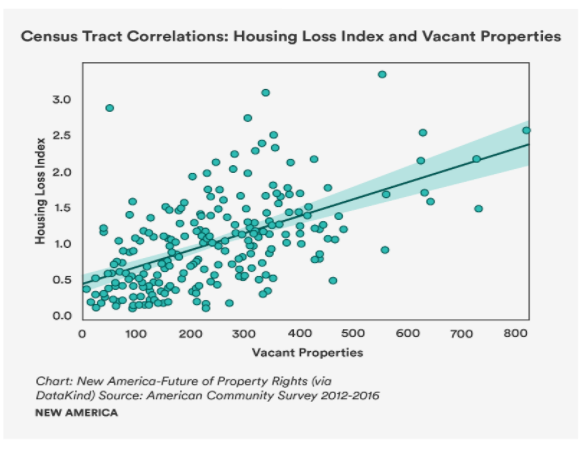

We also found higher mortgage foreclosure rates in counties with high numbers of vacant properties and single-parent households.

Why do People Lose Their Homes?

Low wages and rising housing costs: In all three case study counties, increases in housing costs have outpaced income growth. The resulting disparity between income and housing costs places increasing strain on households to keep up with rent and mortgage payments.

Affordable housing shortage: No state in the United States has a sufficient supply of low-income rental housing, meaning there are not enough units available for rent at rates that households living below the poverty line can afford. Across the country, there are only 36 affordable homes available for every 100 extremely low-income households.

Insufficient tenant rights: Tenants almost never have a right to counsel in eviction court. In many cities and states, landlords are not required to provide a reason for the eviction of tenants, and in some states tenants are unable to withhold rent for substandard living conditions.

What are the Consequences of Displacement?

Displacement destabilizes households and neighborhoods: children might be displaced from schools when their family is forced out of their home, families may become homeless or may move to areas of concentrated poverty with poorer access to resources, jobs, and public transit. Displacement can also have impacts on neighborhoods that contribute to neighborhood neglect and blight: for example, a 2017 report found that each foreclosed, vacant home can lead to losses of $170,000 for its community, measured in crime, blight, and decreased property value.

Policy Recommendations

- Improve housing loss data by creating public eviction, mortgage foreclosure, and tax foreclosure databases.

- Increase wages to keep pace with rising housing costs and expand socioeconomic benefits to reduce other household expenditures on healthcare, childcare, and transit.

- Expand affordable housing options through voucher programs, trust funds, and tax credit programs, and by supporting projects that rehabilitate blighted communities.

- Increase parity between landlords and tenants by expanding tenants’ legal rights, providing tenant representation in eviction court, and expanding tenant education.

- Reconsider state preemption laws that limit local housing solutions such as inclusionary zoning, minimum wage laws, or increased regulation of short-term rentals like AirBnb.

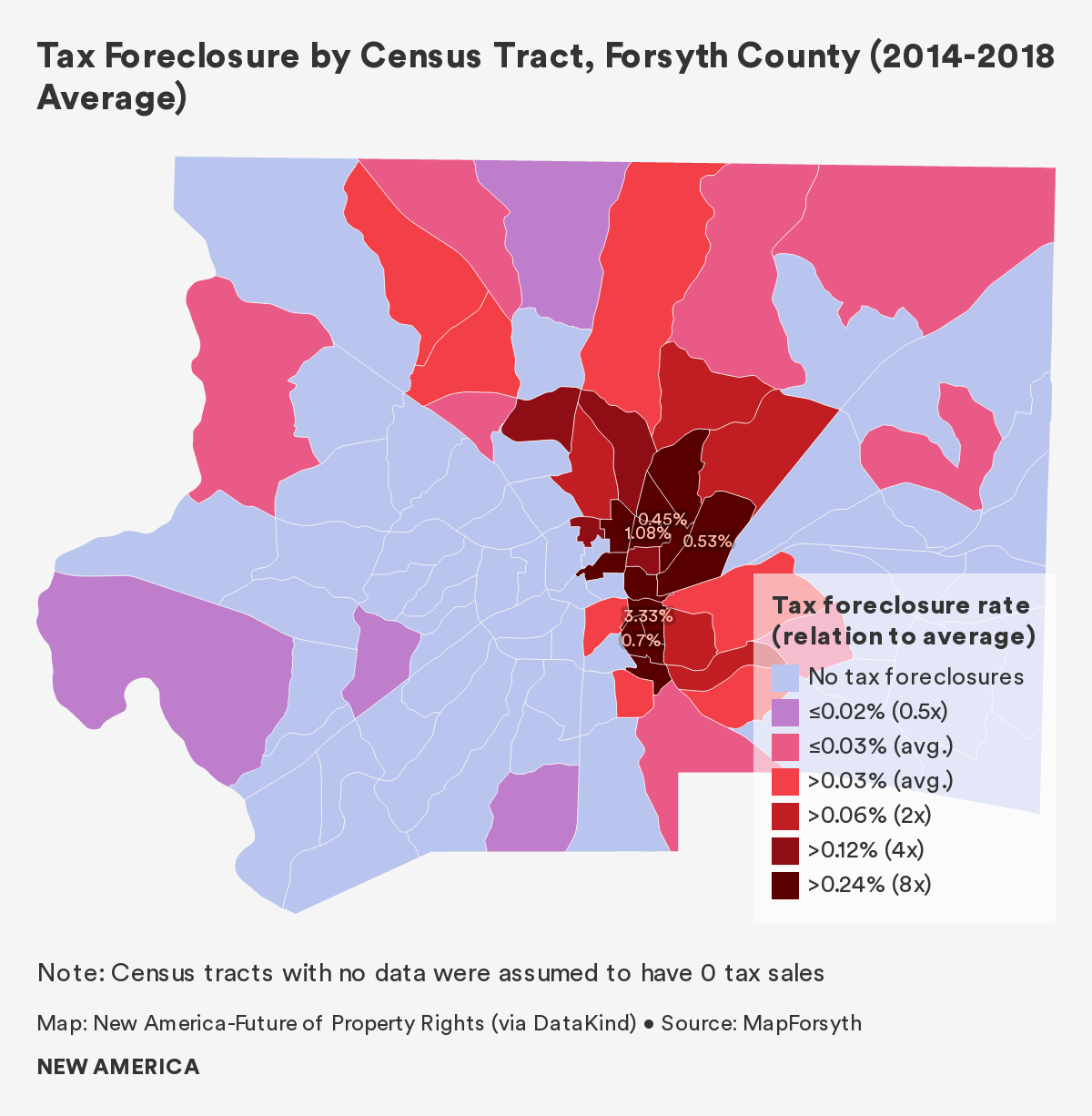

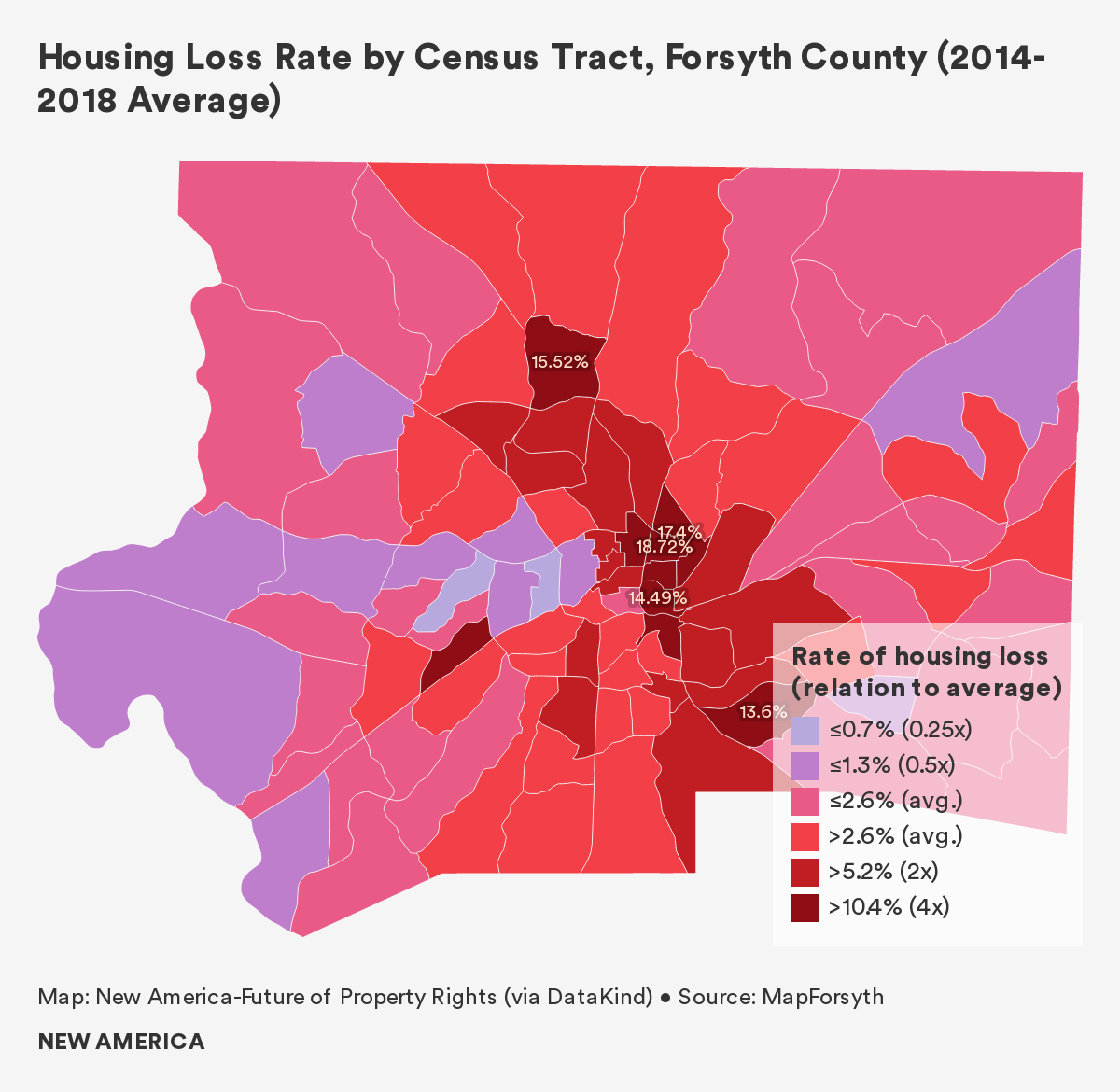

Findings from Forsyth County, North Carolina

To view the interactive data visualization, visit https://tinyurl.com/FPRForsythHomeLoss

Forsyth County residents experienced housing loss at a rate of 2.6 percent between 2014 and 2018. Based on our examination of data from this five-year period:

- 12,276 households were evicted in Forsyth County, a 4.4 percent eviction rate.

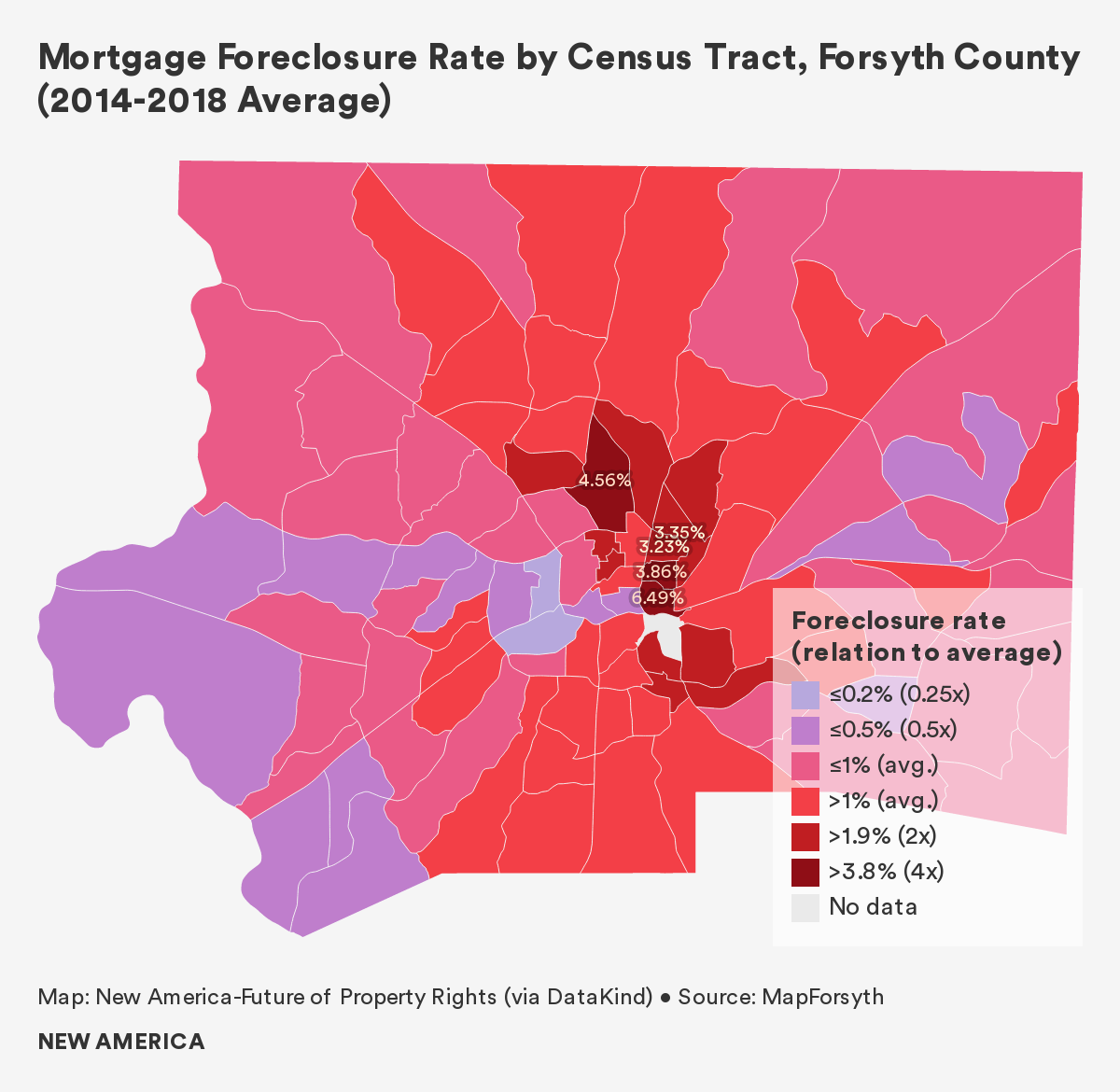

- 2,902 households were foreclosed upon in Forsyth County, a foreclosure rate of 1 percent. Between 2014 and 2018, the foreclosure rate decreased by approximately 64 percent.

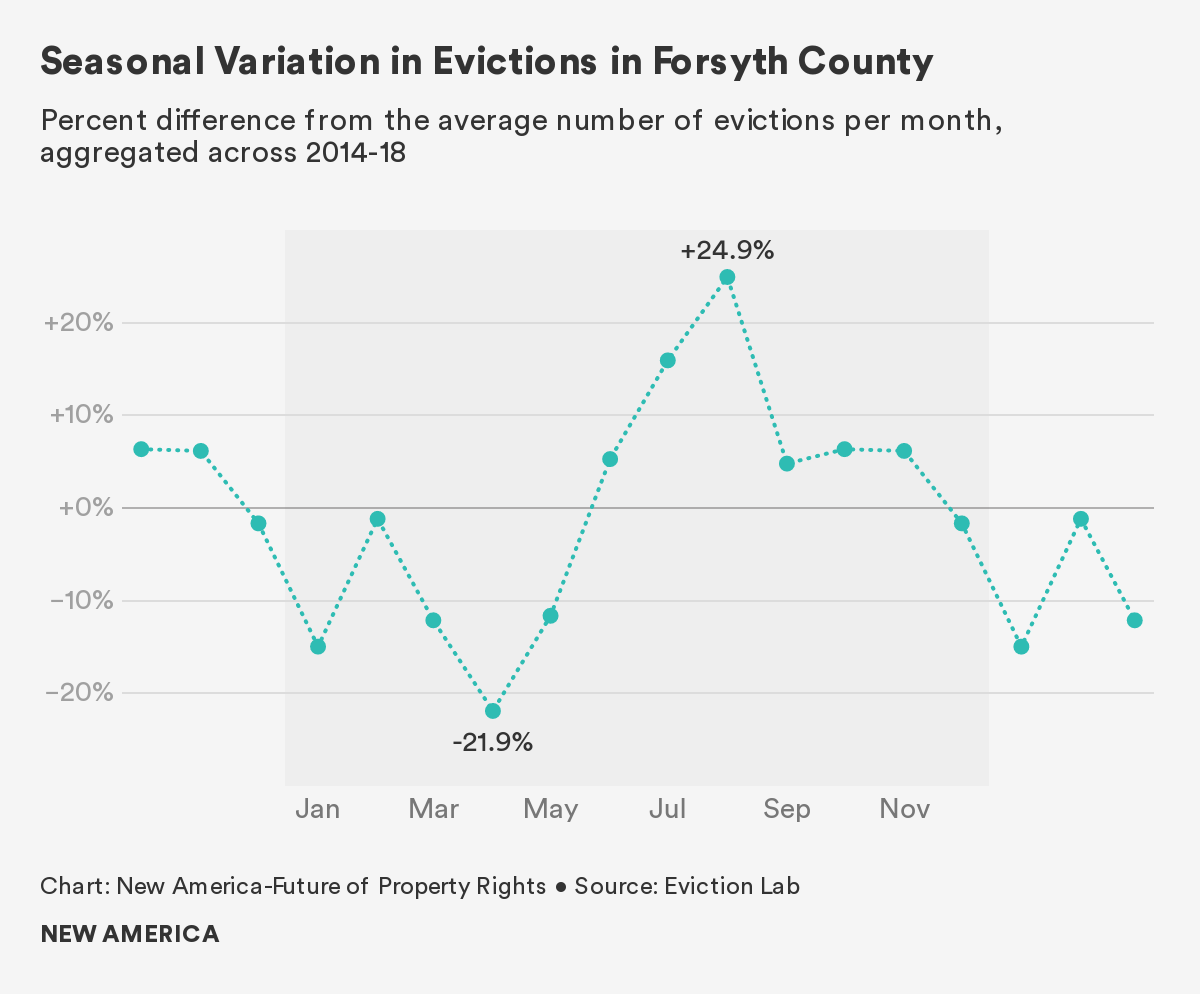

- Evictions spike in summer months. August had the highest average number evictions (256), a 60 percent increase over April, which had the lowest average number of evictions (160).

- When evictions go to court, tenants lose. Evictions in Forsyth County often exceed 3,000 per year, but only 200 cases or so receive pro-bono legal representation, according to a local journalist.

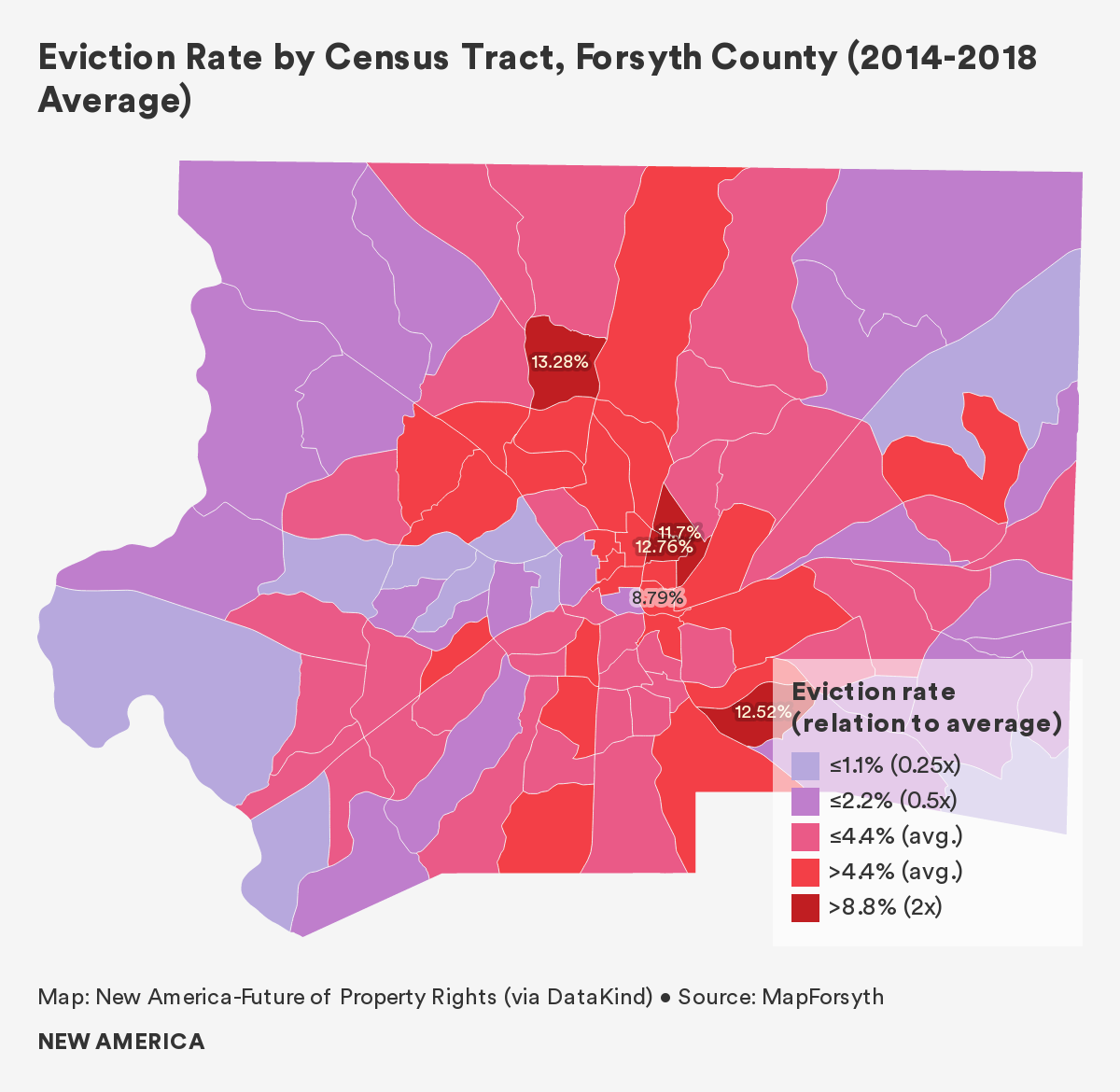

- Census tracts with the highest rates of housing loss are primarily located in East Winston. Each year 9.6 percent of residents in these tracts lose their homes. A few of these tracts lie directly to the east of U.S. Route 52, while others lie between Smith-Reynolds Airport, the Wake Forest University athletic stadiums, and the local fairground.

- Census tracts with larger minority populations as well as tracts with more households living below the poverty lines generally see higher eviction rates. The highest eviction rates, in some places as high as 13 percent, are concentrated to the east of downtown Winston-Salem, in East Winston.

- About half of Forsyth County census tracts have foreclosure rates of less than 1 percent, however foreclosure rates jump to 3-7 percent in East Winston and the southeastern region of Winston-Salem.

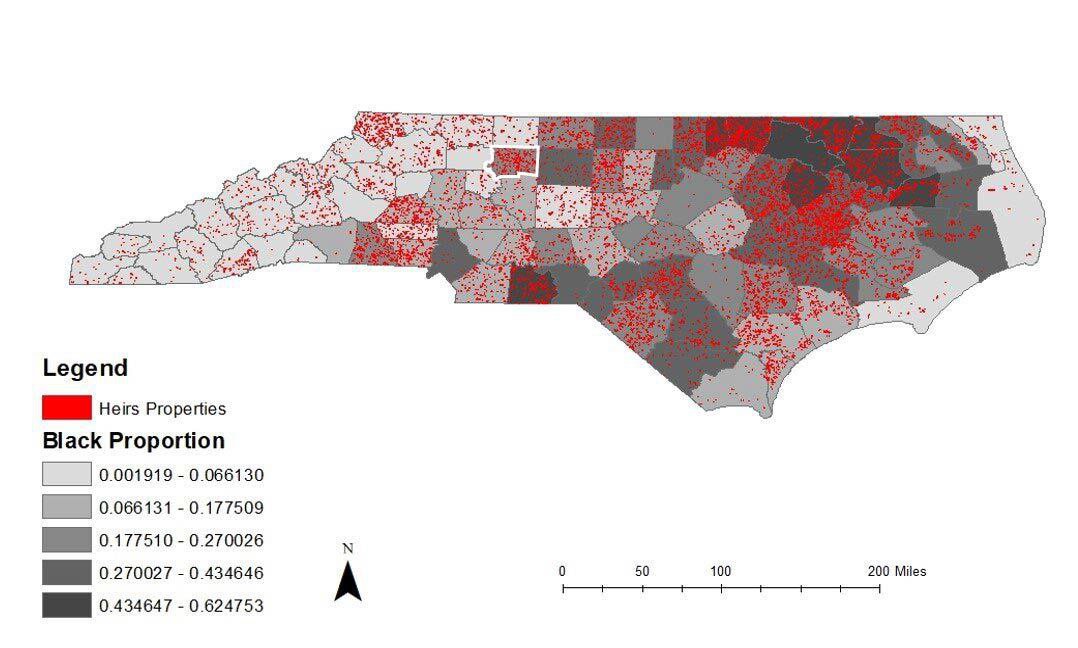

- Forsyth County has 1,524 heirs properties, the fifth highest number in North Carolina. Heirs property is passed down through generations outside of the formal probate process and often lacks “clear title.” Disproportionately present in Black communities, this form of property ownership exposes owners to significant vulnerability.

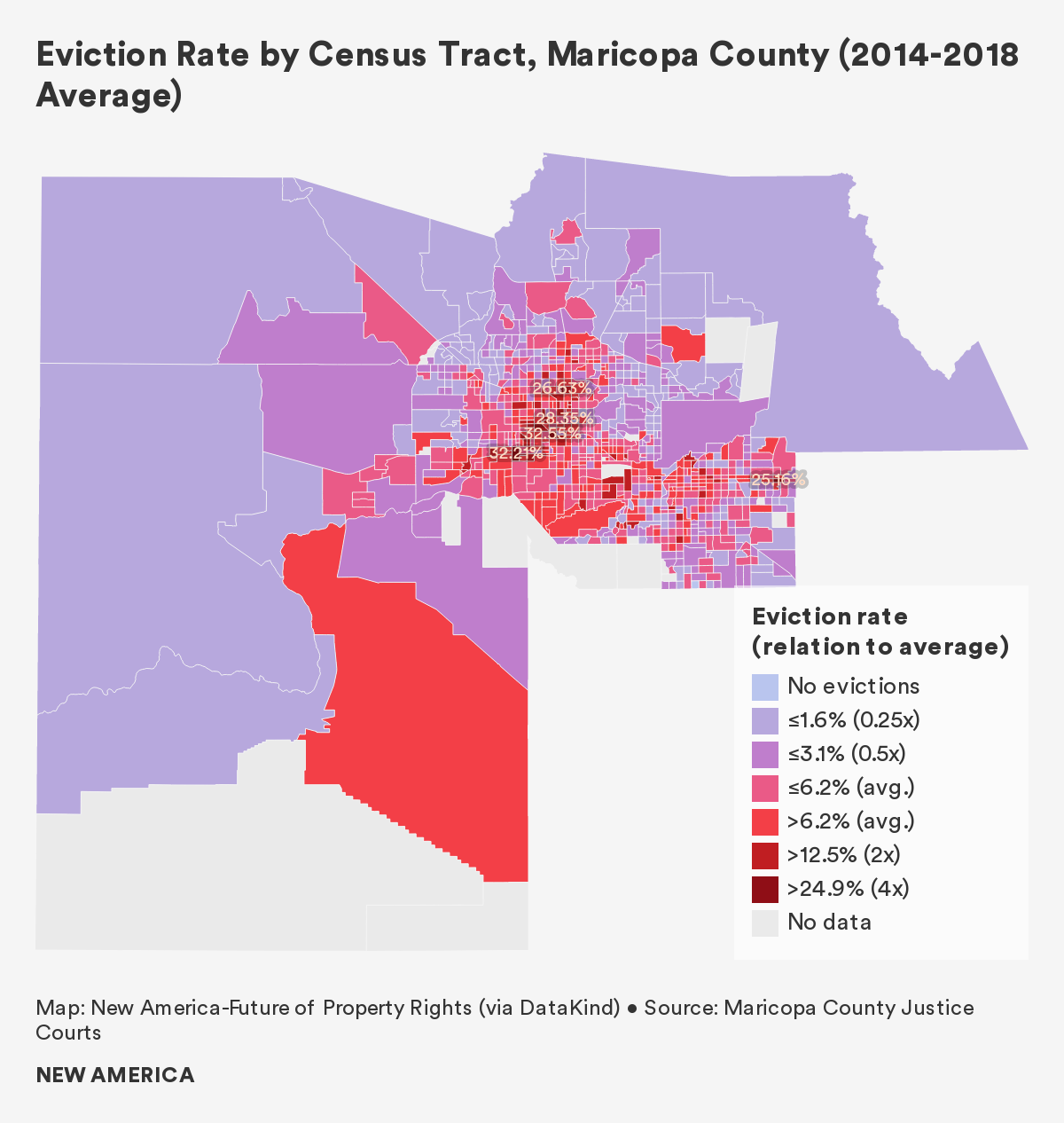

Findings from Maricopa County, Arizona

To view the interactive data visualization, visit https://tinyurl.com/FPRMaricopaHomeLoss

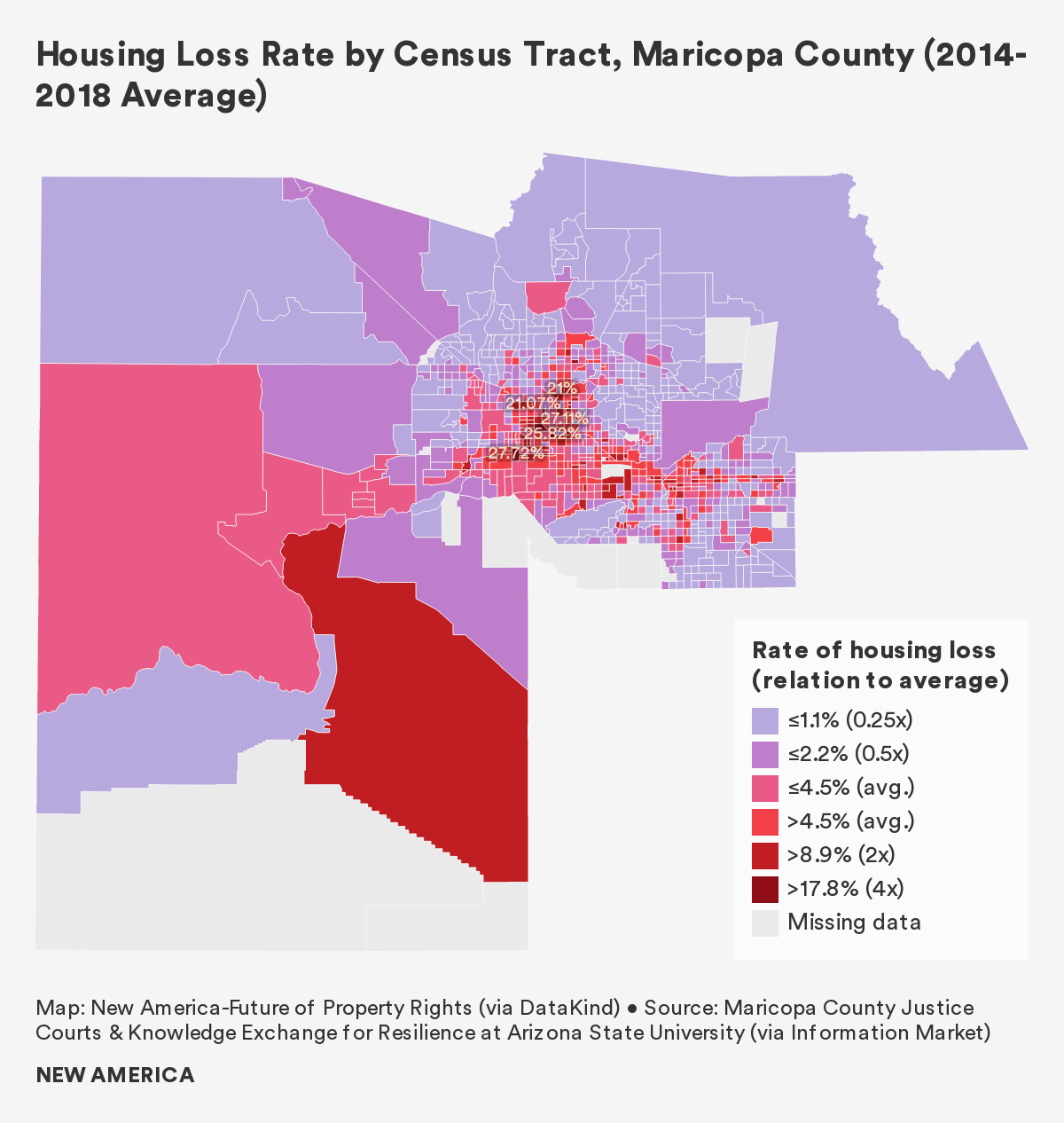

Maricopa County residents experienced housing loss at a rate of 4.5 percent between 2014 and 2018. Based on our examination of data from this five year period:

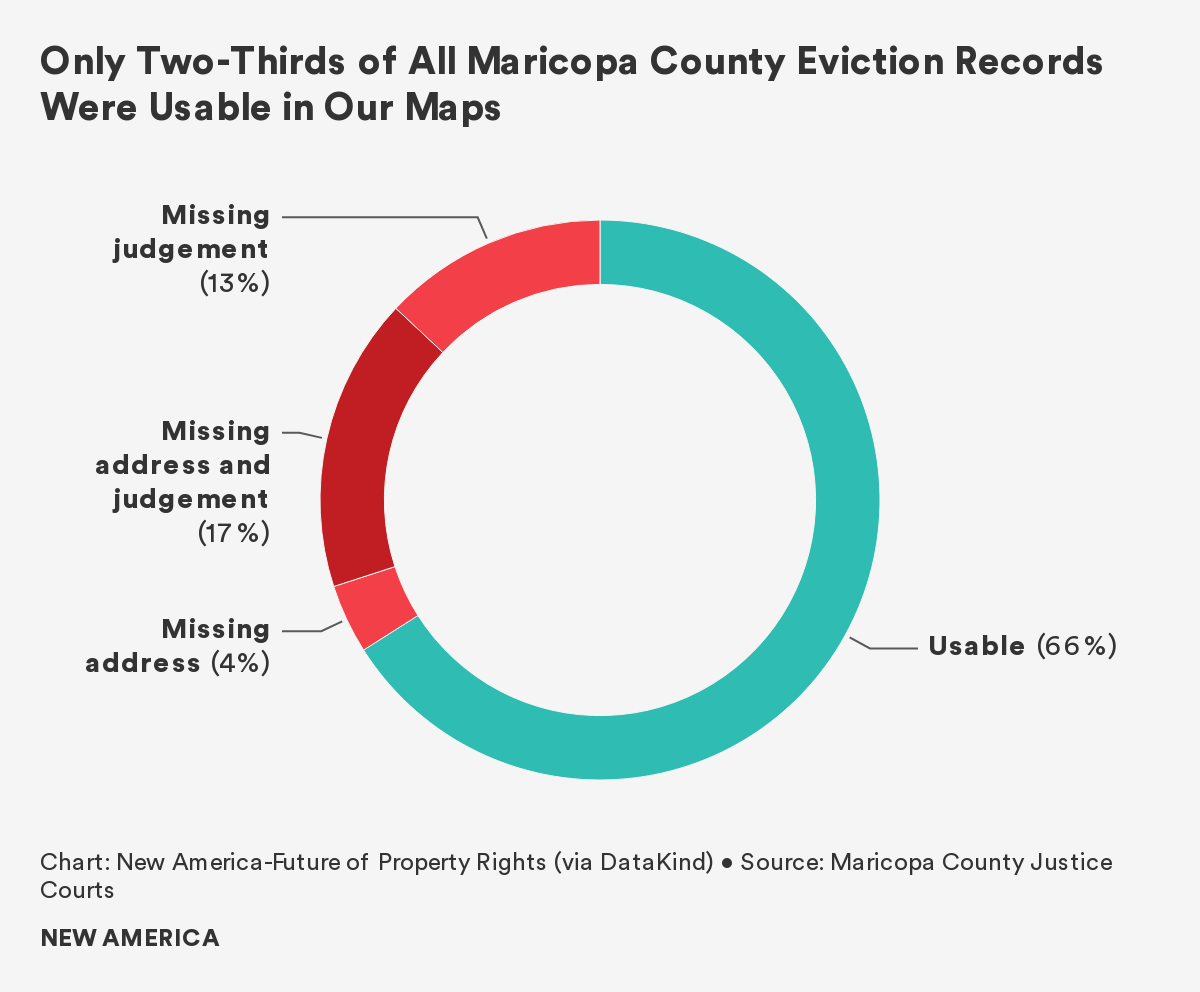

- 218,00 households were evicted in Maricopa County, a 6.2 percent eviction rate. This is despite the fact that one-third of eviction court records were incomplete and not included in our calculations. As a result we believe the county’s true eviction rate is significantly higher.

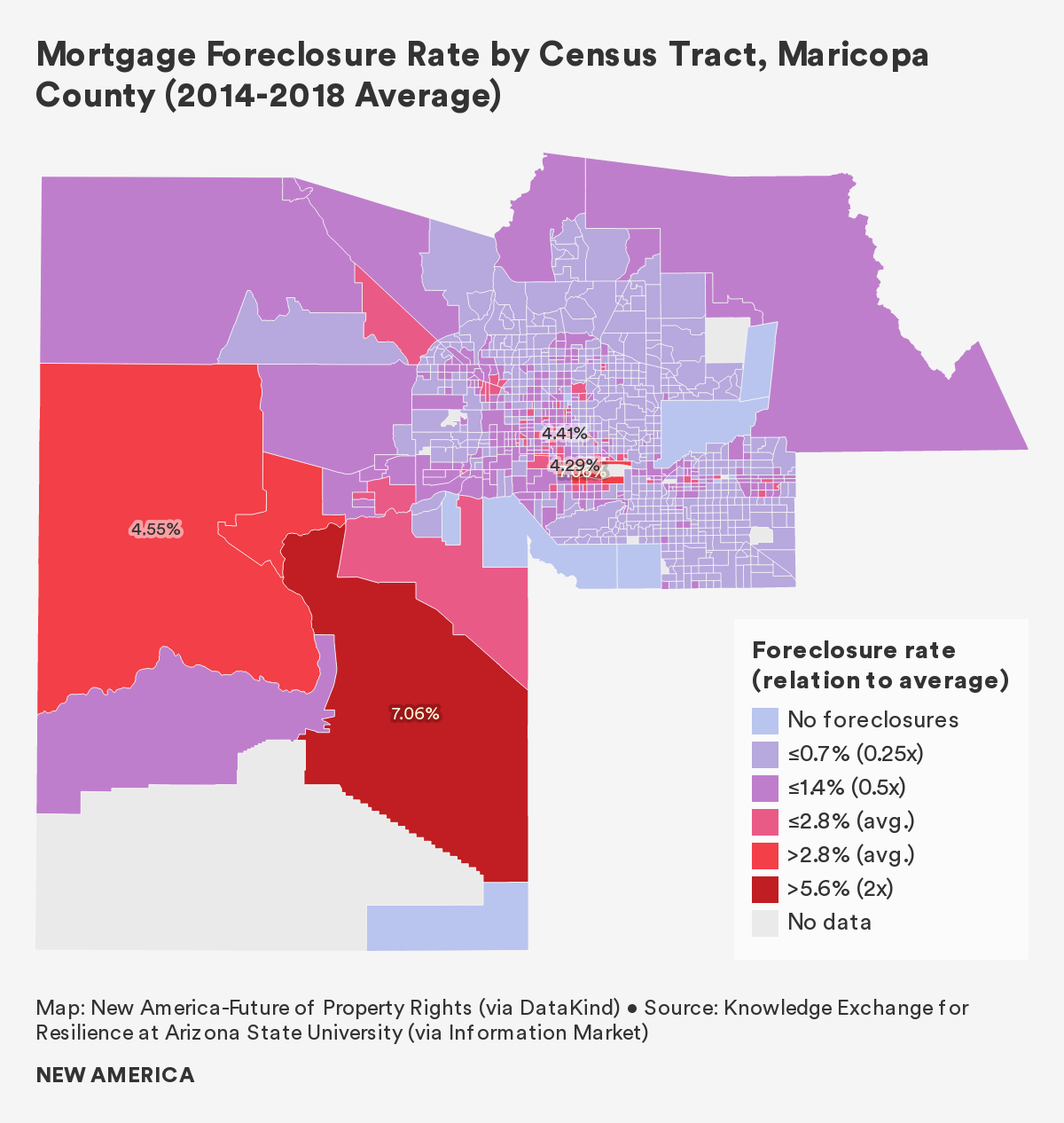

- 17,541 households were foreclosed upon in Maricopa County, a foreclosure rate of 2.8 percent.

- Evictions spike in the summer months. July had the highest average number evictions (4,253), a 52 percent increase over March, which had the lowest average number of evictions (2,809).

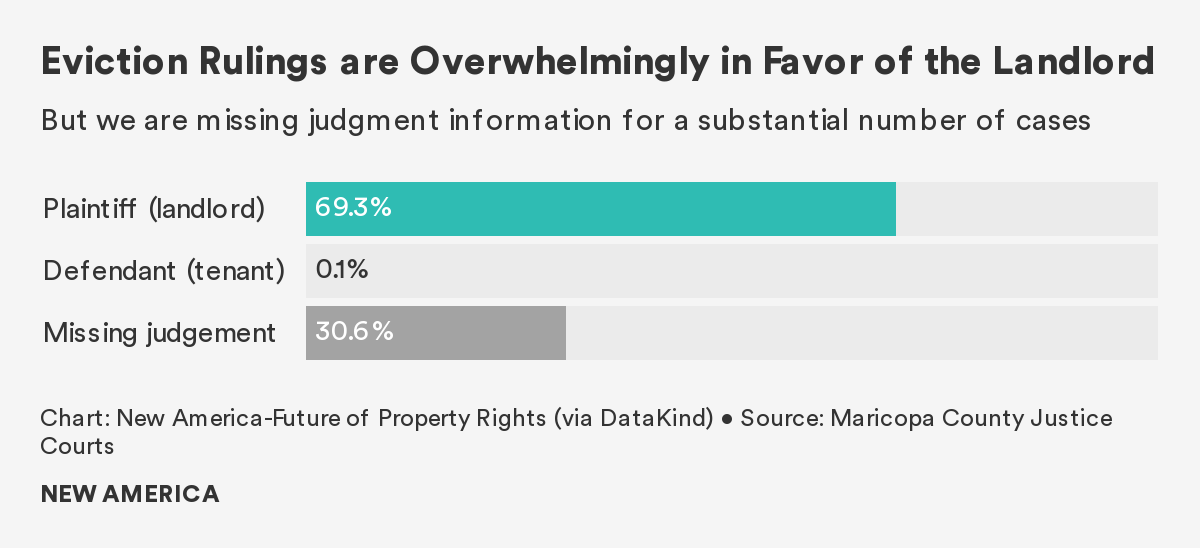

- When evictions go to court, tenants lose. 87 percent of landlords and only 0.3 percent of tenants had legal representation in court. Of cases with judgment information available, landlords win 99 percent of the time.

- Mobile home park redevelopments are a significant source of housing instability. 70,000 households in Maricopa County live in mobile homes, and can be forced to move when investors purchase mobile home parks for redevelopment. Investors have spent more than half a billion dollars buying up mobile home parks in the region since 2017.

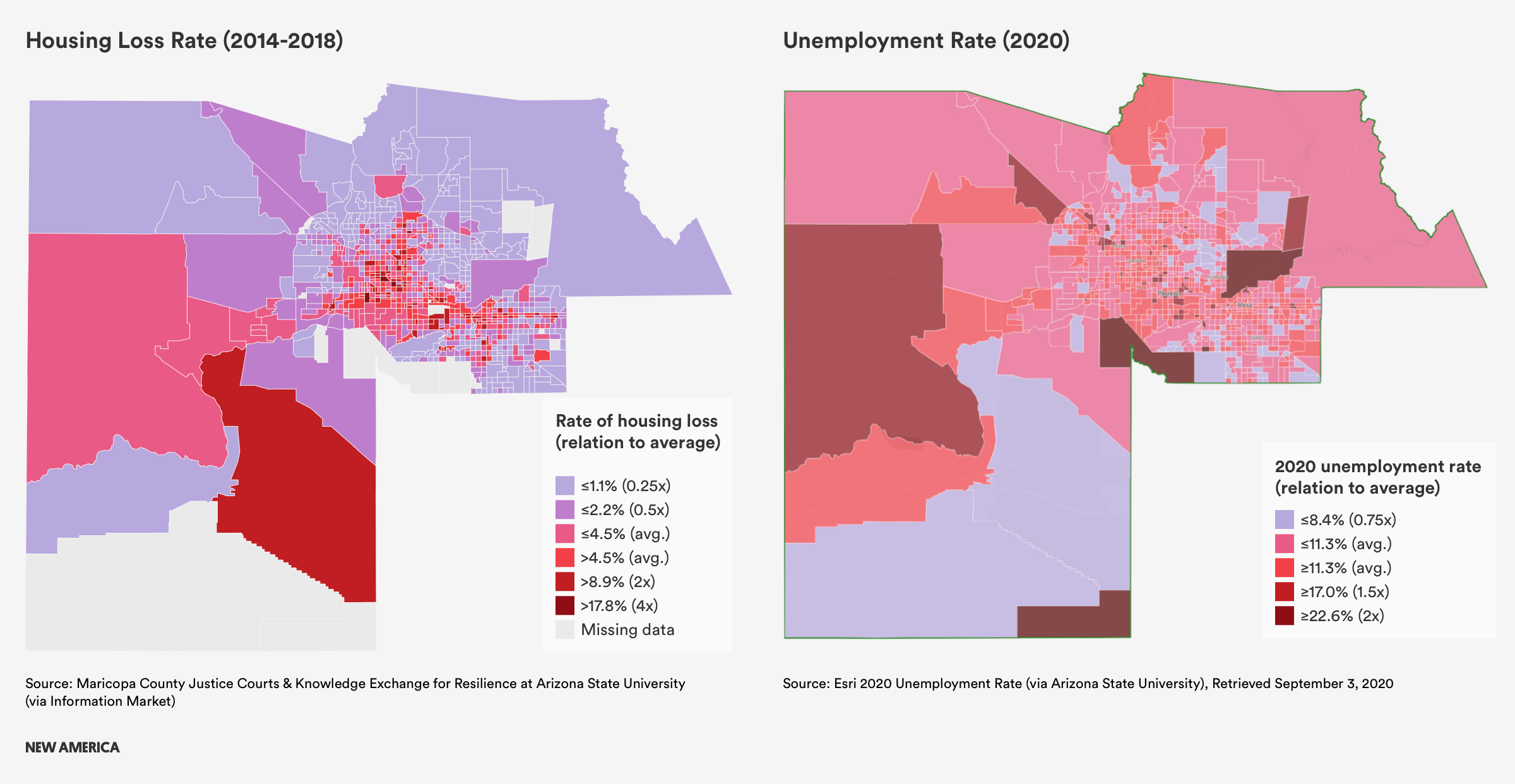

- The highest eviction rates are concentrated near the center of Phoenix, notably the neighborhoods of Maryvale and Westridge Park. In these tracts, one in three renter households get evicted every year.

- Most Maricopa County census tracts have average foreclosure rates of less than 1 percent, however foreclosure rates jump to 5-7 percent in the southeast and southwest portions of the county, as well as those closer to the Phoenix city center. Neighborhoods near Sky Harbor Airport have foreclosure rates of 7 percent.

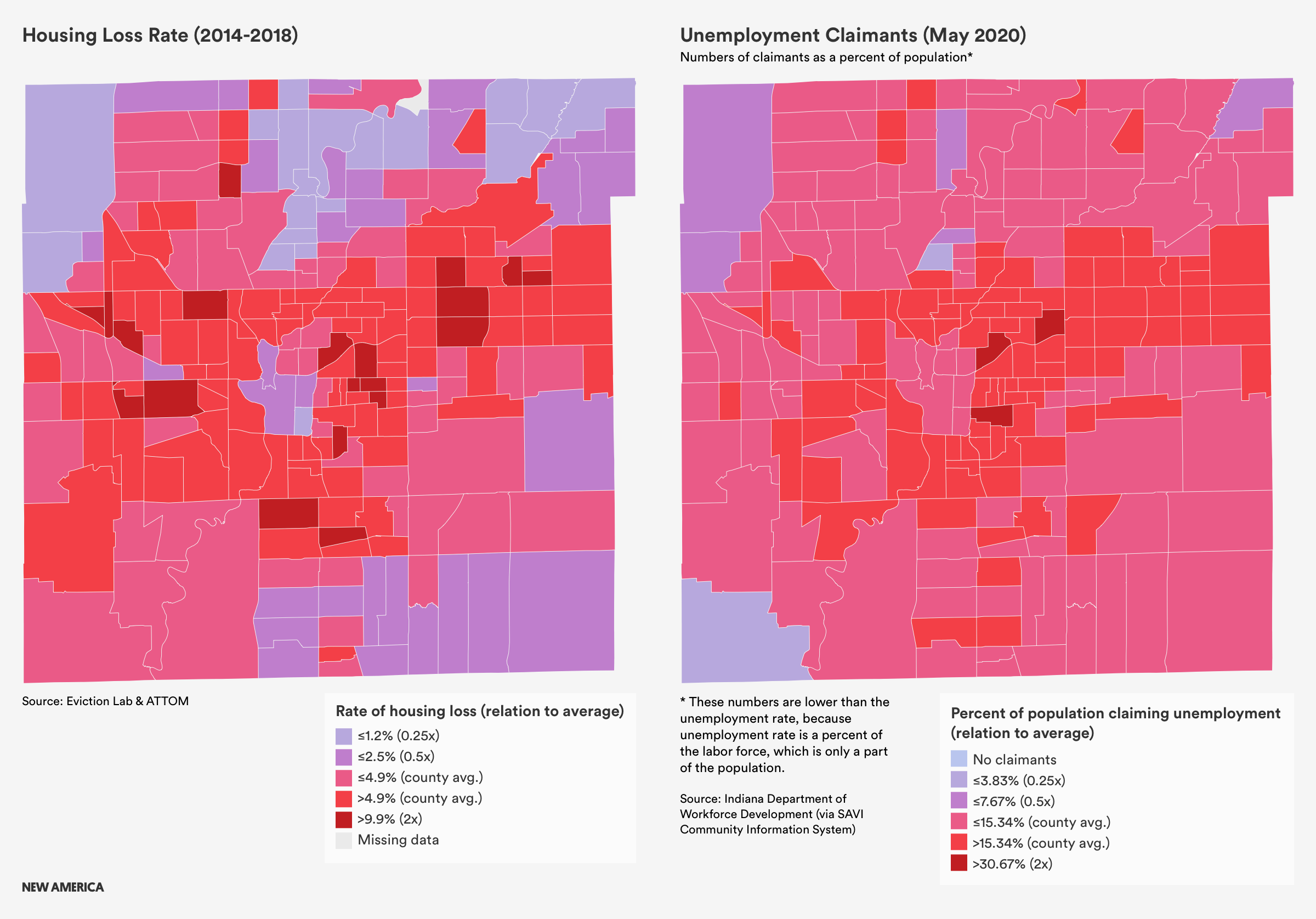

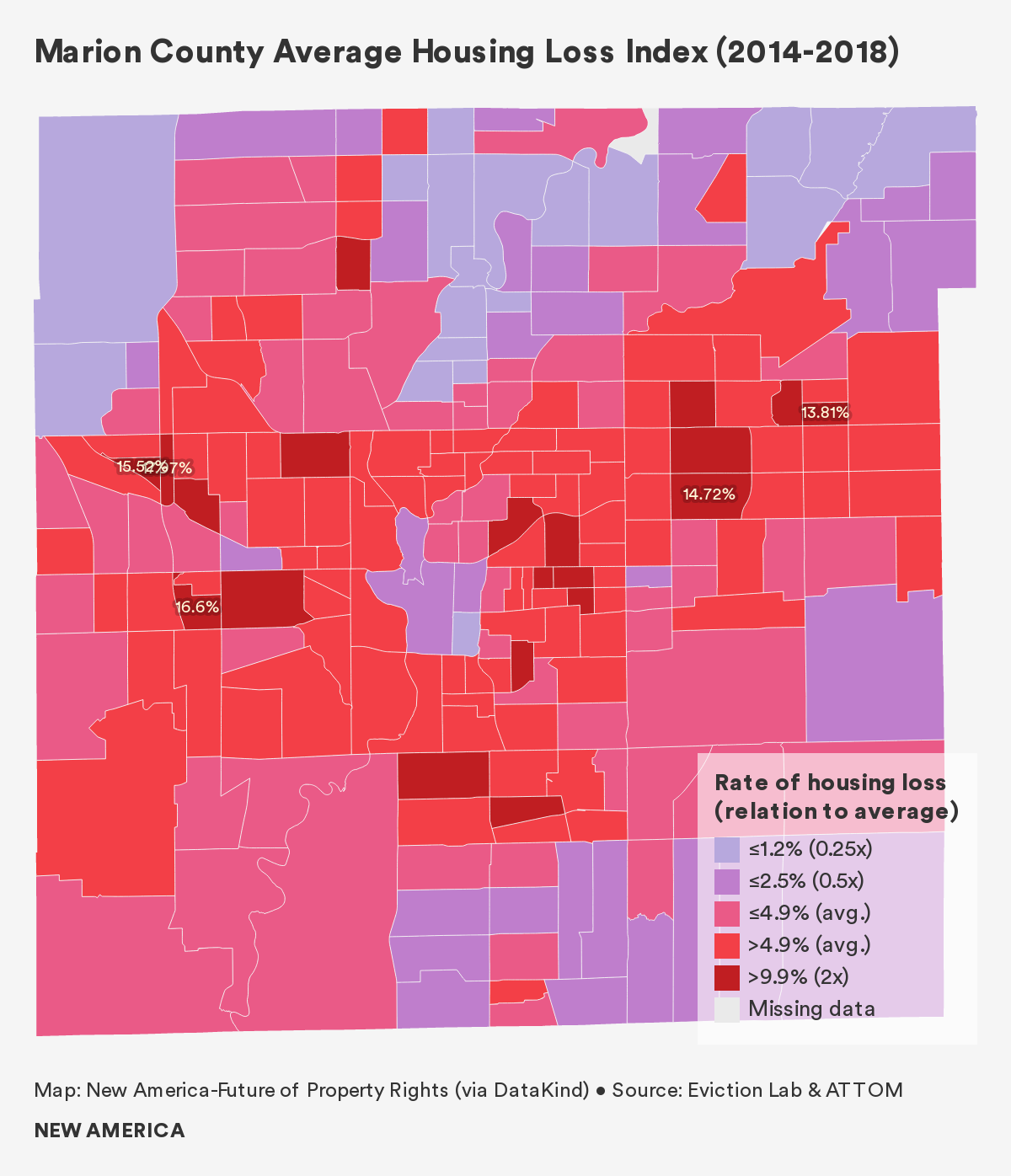

Findings from Marion County, Indiana

To view the interactive data visualization, visit https://tinyurl.com/FPRMarionHomeLoss

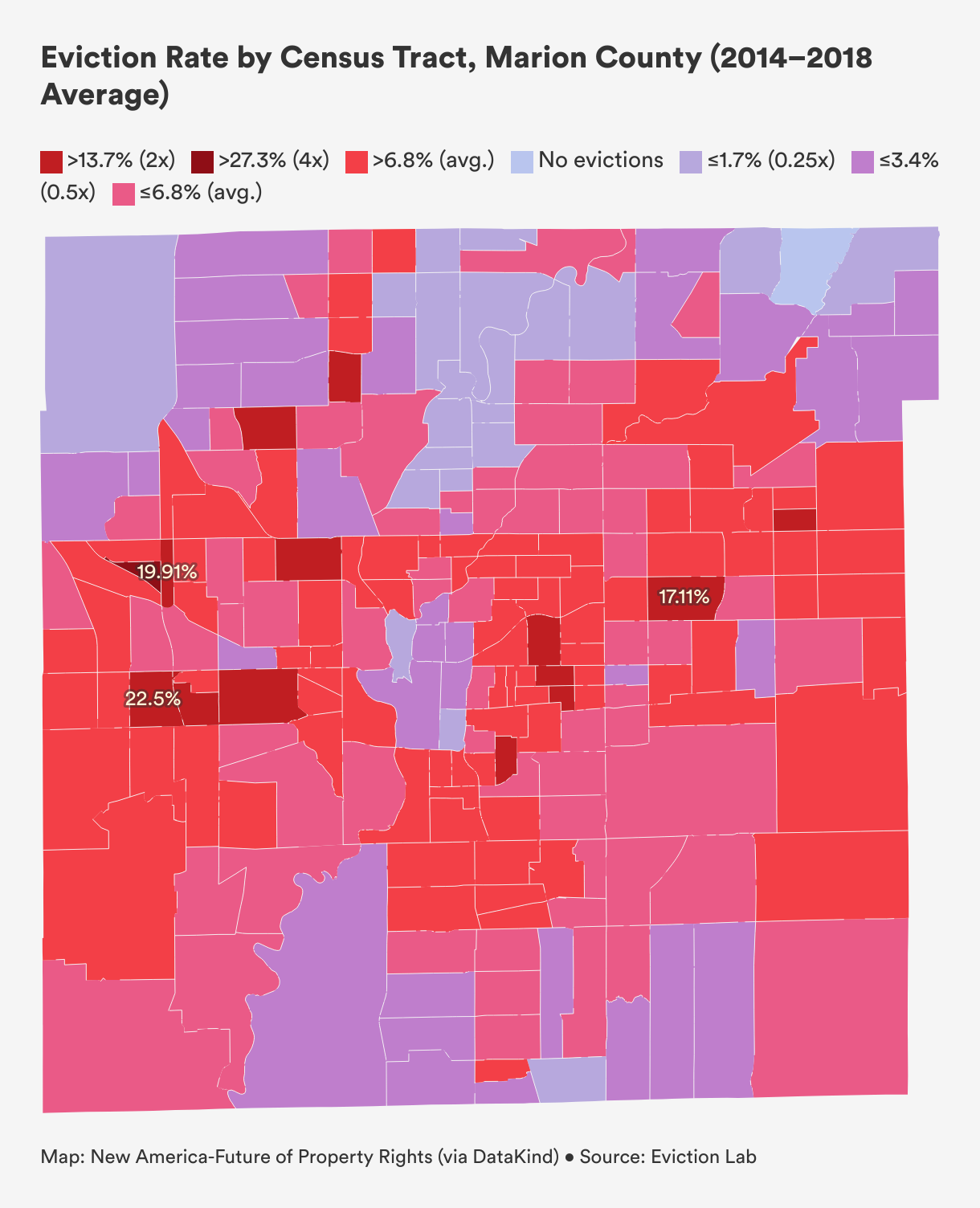

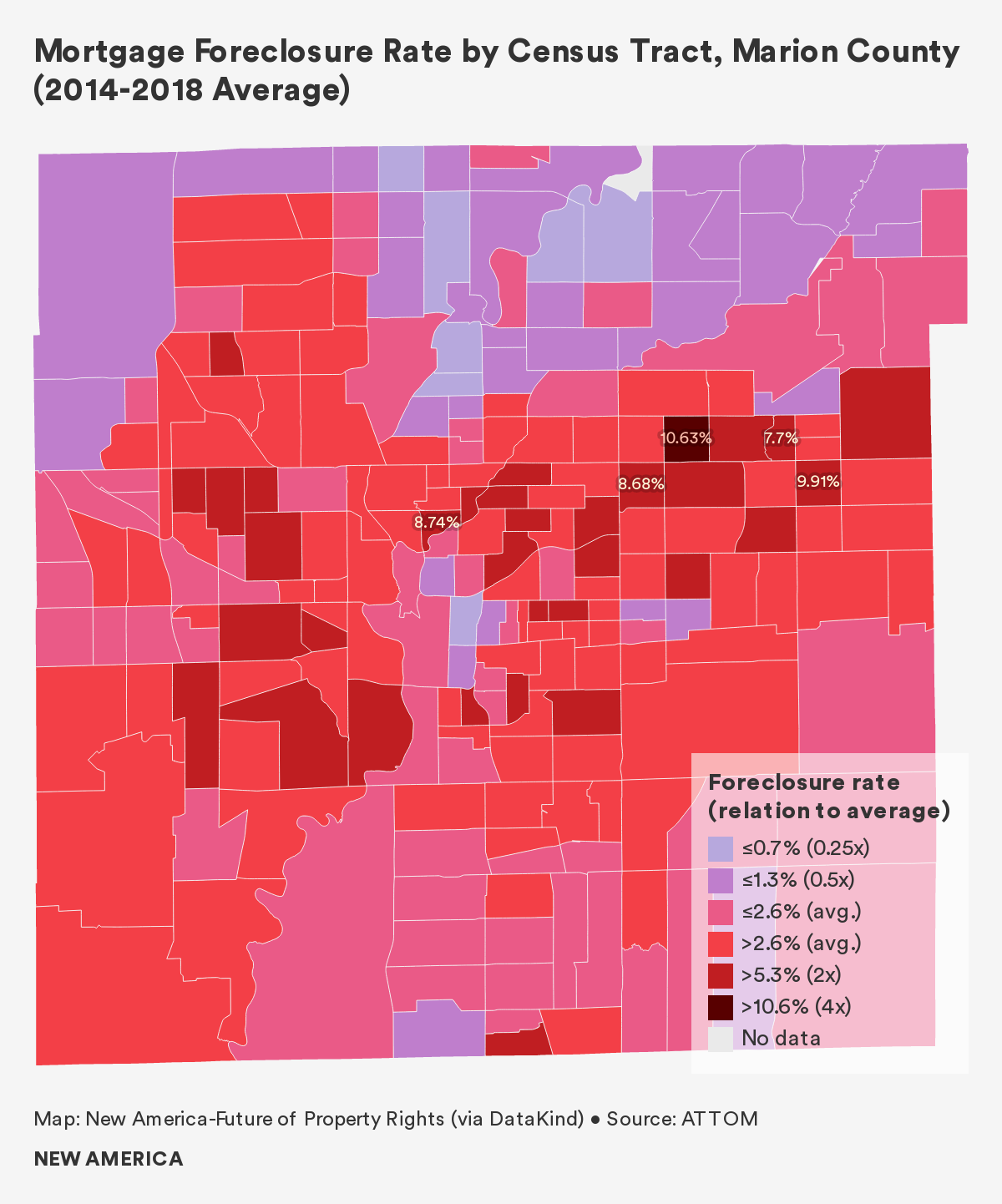

Marion County residents experienced acute housing loss at a rate of 4.9 percent between 2014 and 2018. Based on our examination of data from this five-year period:

- 57,960 households were evicted in Marion County, a 6.8 percent eviction rate.

- 18,765 households were foreclosed upon in Marion County, a foreclosure rate of 2.7 percent. Mortgage foreclosure accounted for 24 percent of all housing loss in Indianapolis during this five year period.

- Evictions spike in summer months. August had the highest average number evictions (1,220), a 54 percent increase over March, which had the lowest average number of evictions (791).

- Wayne and Center Townships exhibit the most acute housing loss, with many tracts in these areas reporting housing loss rates between 14 and 17 percent.

- The census tract with the highest rate of loss in Marion County is located in Wayne Township, and sits in both Indianapolis and the independent enclave of Speedway. In this tract, the housing loss rate is 18 percent, 3.6 times the county average.

- The worst tract for evictions lies just outside Speedway—more than one-third of renters (34 percent) are evicted there every year. Perhaps unexpectedly, the tract is relatively wealthy, with a median household income 20 percent above the county median.

- Generally, census tracts with above-average eviction rates are on the periphery of downtown Indianapolis. These tracts are home to more Black households, the demographic group with the second-strongest association with evictions, behind Latinx households.

- The census tract with the highest foreclosure rate in the county—10.6 percent—sits in the northeast township of Lawrence.

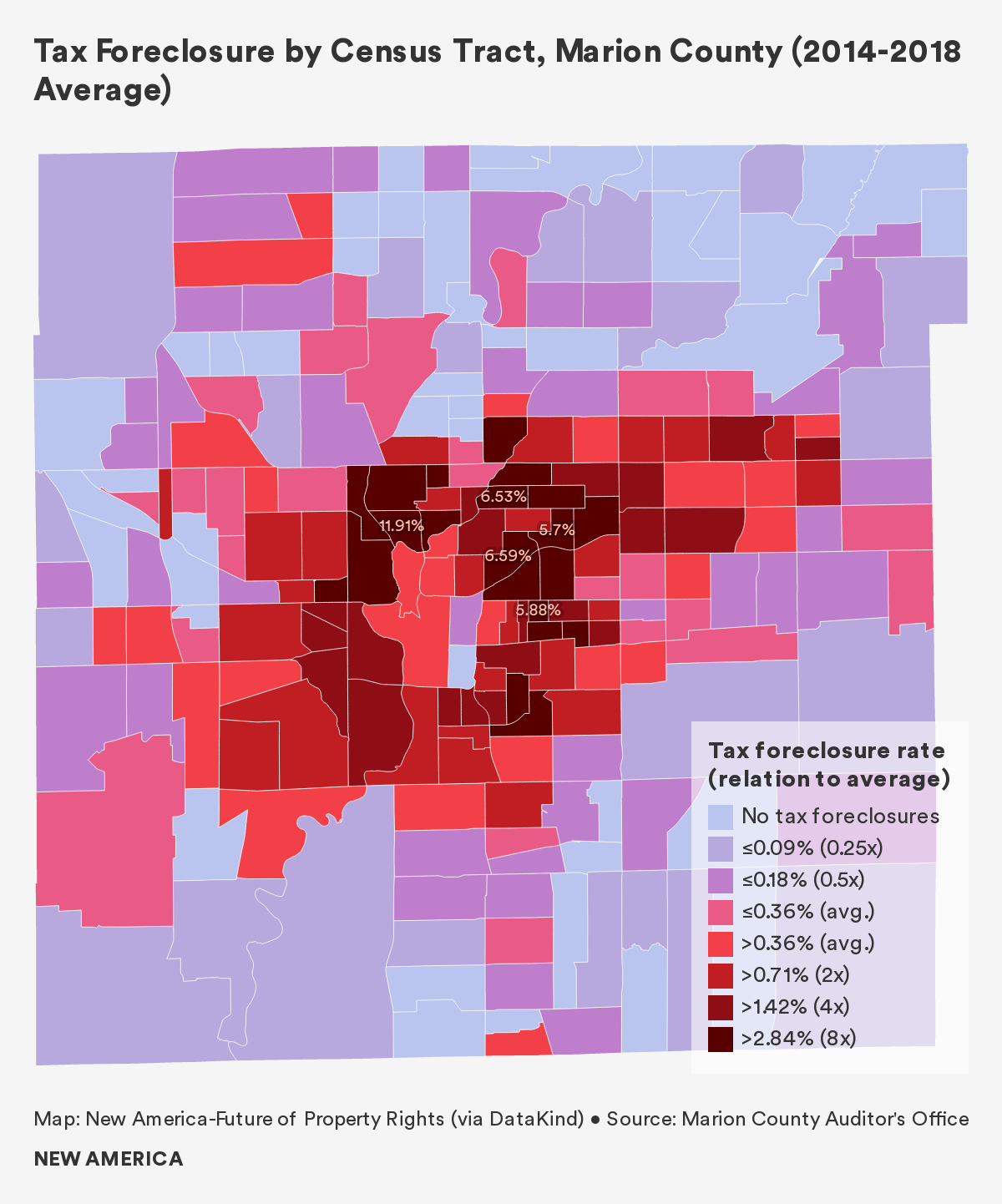

- Tax foreclosures occurred in a “ring” around downtown Indianapolis. The ring of tax foreclosures aligns with previously redlined areas of the city, and our data shows that census tracts with more non-white households experienced higher rates of tax foreclosure.

Introduction: Past, Present, and COVID

When we embarked on this project more than a year ago, we could have never predicted its salience today. As the COVID-19 pandemic swept across the United States, it rapidly became clear that we would release this report at a time when millions of Americans are without jobs and at risk of losing their housing. This report became more than a way to document historic housing loss, but a tool municipal leaders could use to better understand pandemic-related housing loss in their own communities.

Every year, almost 5 million Americans lose their homes through eviction and foreclosure. But this year, as a result of the COVID-19 crisis and the severe economic downturn it spurred, we anticipate that number to be magnitudes greater. An Aspen Institute report released in August predicts that 30 to 40 million people are at risk of being evicted by the end of 2020, to say nothing of foreclosures.

As we write, more than a quarter of Americans and 43 percent of renting families have reported that they cannot pay their rent or mortgage. This, combined with 51 percent of U.S. households reporting that at least one person in their household has lost employment income due to COVID-19, does not bode well for the millions of already struggling households. In 2019, the Global Property Rights Index found that 13 percent of Americans were housing insecure. Looking at the U.S. Census Bureau’s Housing Pulse Survey, we know that housing insecurity has roughly doubled this year—a staggering increase.

In many cities, although evictions continue to occur, the tsunami of housing loss has not yet begun. But soaring unemployment figures, coupled with quickly depleted rental assistance programs, sharp increases in food pantry requests, and tenants taking on financial risk to pay the rent, tell us it’s coming. On September 1 the Centers for Disease Control (CDC) announced a ban on evictions for nonpayment of rent in order to prevent the spread of COVID-19. The order is effective through December, and serves to delay housing loss through the end of this year, but there is no support for tenants to pay back rent, and no mention of what happens on January 1.

Forced displacements are intensely traumatic—financially, physically, and emotionally. Children have to switch schools, parents lose their jobs, families’ possessions end up on the sidewalk, and depression, anxiety, and suicide rates spike.

Yet even as our nation braces for a flood of housing loss, we know very little about these life-changing events. What is the actual rate of displacement? Where is displacement most acute? Who is most at risk? And why do people lose their homes?

Over the past year, the Future of Property Rights program and our research partners have attempted to answer these questions by visualizing the scale and breadth of housing instability and displacement across the United States, and telling the stories of communities impacted by these losses. We developed a National Housing Loss Index, which ranks U.S. counties based on their combined eviction and foreclosure rates between 2014 and 2016. In addition to analyzing county-level displacement across the United States, we examined census tract-level housing loss between 2014 and 2018 across three case study locations: Forsyth County, North Carolina (Winston-Salem); Marion County, Indiana (Indianapolis); and Maricopa County, Arizona (Phoenix, Tempe, Mesa).

We found that the United States has an acute housing loss problem. The pandemic has exacerbated the effects of stagnant wages, the lack of affordable housing, insufficient federal housing assistance, and discriminatory policies that contribute to housing loss. And while emergency measures like eviction and foreclosure moratoriums will prevent many from losing housing in the near term, they will not address the systemic policies and economic factors that lead people to lose their homes.

The pandemic may have shone a light on the rot in American housing, but that rot was there all along.

So how does studying past housing loss help us combat the current crisis?

First, we know that housing loss—both evictions and foreclosures—persistently affect the same areas, and the same communities. While shock events like the 2008 financial crisis and the current COVID-19 pandemic add to the volume of housing loss, these surges often follow familiar patterns: The people and places most vulnerable to housing loss to begin with are often the ones who experience it most acutely in times of crisis. By identifying and examining which places have traditionally experienced the most acute housing loss, we can predict where future housing loss will occur and who will be impacted, and direct resources to prevent the harm before it proliferates.

Second, knowing past housing loss at the local level gives us a baseline from which to assess the magnitude of the current problem, and to understand which areas are being disproportionately impacted. At a national level, we already have pre-pandemic data about housing insecurity. In 2019 the Global Property Rights Index, in partnership with the Gallup World Poll, found that 13 percent of Americans are housing insecure. Through the U.S. Census Bureau’s Housing Pulse Survey, we know that number has roughly doubled this year—a staggering increase. But we have no such comparison at the local level.

Third, examining the drivers of past housing loss gives us the opportunity to develop a long-term plan to redress housing precarity. Our data reveals that even before 2020, the United States’s flawed housing system disadvantaged significant parts of the population. Without intervention, the current crisis will dramatically exacerbate these pre-existing conditions. While today’s emergency certainly demands a rapid response of moratoria paired with significant cash infusions, these solutions are stopgap measures and will not address the root causes of housing instability. Rather, they provide the opportunity to pause housing displacement, so that we may finally implement more lasting solutions that make quality housing more affordable and accessible, and ensure that all Americans are afforded the fundamental human right to adequate housing.

Methodology and Definitions

Methodology

About two-thirds of Americans, or 76 million households, own their homes while the remaining one-third, or 43 million households, rent.1 Of owner-occupied housing units, 62 percent, or 46 million, have a mortgage. This report examines housing loss due to eviction and foreclosure, and presents findings from mixed methods research on housing instability and loss in the United States.

In addition to a brief section on our national-level findings, we focus on case studies on three U.S. counties: Forsyth County, North Carolina; Maricopa County, Arizona; and Marion County, Indiana. The purpose of these case studies is to evaluate housing insecurity and loss at a more granular level of analysis, in different geographies and social contexts.

We analyzed and visualized the available geospatial data on evictions, mortgage foreclosures, and tax foreclosures nationally and in each case study location. To supplement these quantitative findings, we utilized American Community Survey (ACS) data from the U.S. Census Bureau and tested for statistical relationships between housing loss and a number of socioeconomic variables. For each case study location, we further conducted key informant interviews (KIIs) to better understand the causes of home loss, as well as the consequences of displacement. These KIIs, along with desk research, helped to provide geographic, demographic, economic, social, political, and historical context to our housing-related findings.

Housing Loss Rate and Housing Loss Index

Limitations of Prior Studies: Prior studies on housing loss tend to examine different mechanisms of loss in silos. Eviction, mortgage foreclosure, and tax foreclosure are analyzed separately, rather than as components of the same, broader problem: housing instability and loss. The processes of eviction and foreclosure may be different, yet the underlying causes are often the same, and each result in displacement and trauma—financially, physically, and emotionally. In most U.S. cities, a worker on minimum wage will be unable to make housing payments—either rent or a mortgage. The impact on a child who switches schools three times a year due to housing instability is likely similar whether home loss occurs via eviction or foreclosure. And residents of a blighted neighborhood likely do not care if their block of empty homes is a result of foreclosures or chronic evictions.

Our Scoring Metrics: For the reasons above, we decided to develop a single “score” of housing loss in the United States, capturing the overall magnitude of both eviction and mortgage foreclosure.

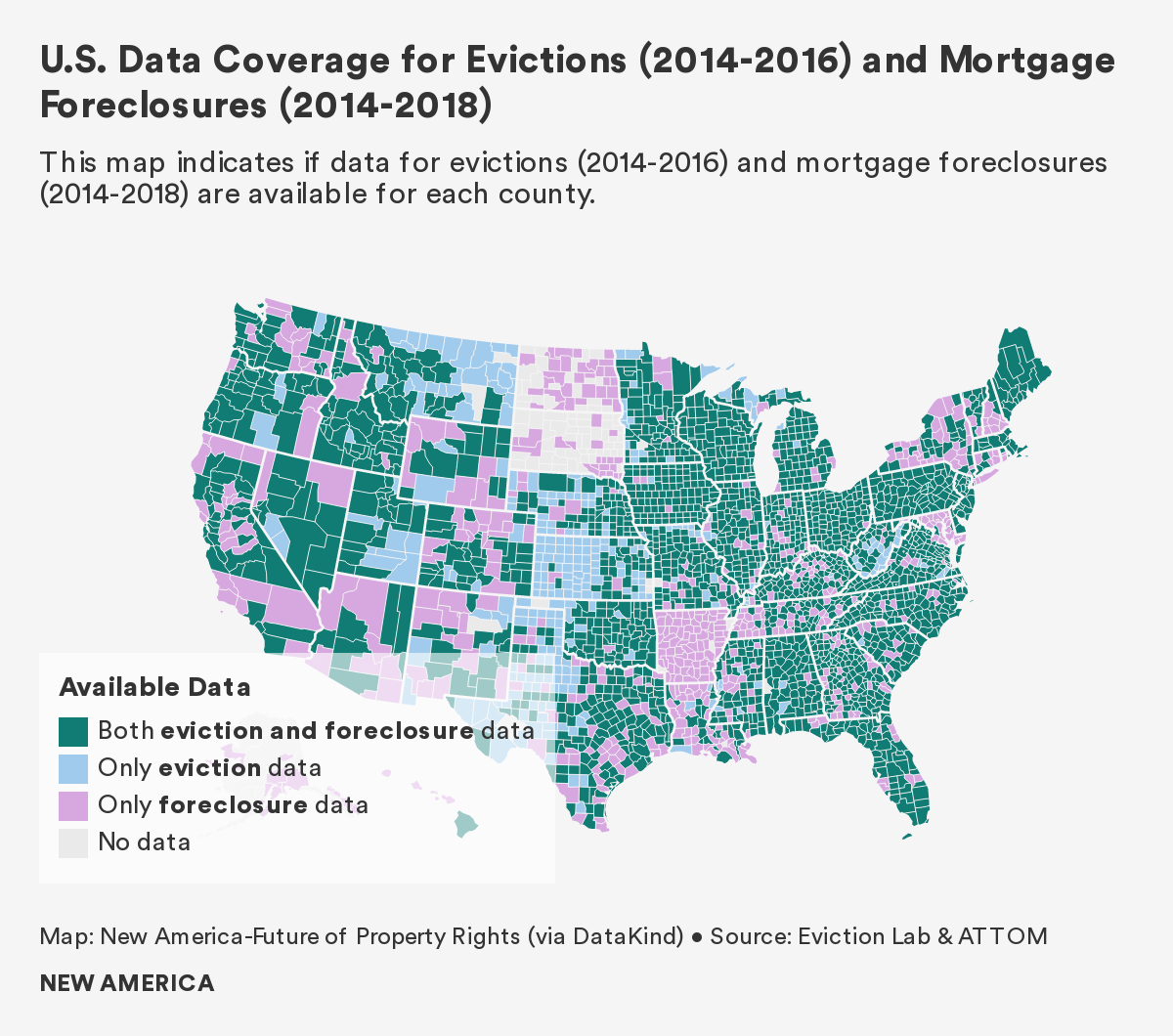

In order to generate an indicator of housing loss that is based on the total number of evictions and the total number of mortgage foreclosures, we created two new measures: a housing loss rate and a housing loss index. These two scores were calculated for the counties for which both eviction and mortgage foreclosure data are available for 2014 to 2016. At the national level, this data is available for 2,221 counties, out of the 3,143 counties in the United States.2 The national housing loss index compares rates of housing loss in each county against the national average. In each of the case studies, the housing loss index compares the housing loss rate in each census tract against the county average.

Housing Loss Rate: The housing loss rate captures loss by combining the total number of evictions and the total number of mortgage foreclosures for a given geography, and then normalizing that sum by the total number of renters and the total number of homeowners with a mortgage within the given geography. As a result, this rate shows the scale of housing loss within a given geography in relation to the number of households who could potentially experience such a loss.

The unit of analysis at the national level is the county, and the unit of analysis in each case study is the census tract.3

We note, however, that the rate does not capture any trends related to housing loss, or whether loss has increased or decreased over the study period, nor does it inherently express which mechanism of loss—eviction or foreclosure—has the greater impact on overall housing loss. A "housing loss dashboard" included below separately reports the proportion of housing loss accounted for by eviction and foreclosure to provide insight into the predominant mechanism of instability in each county or county-equivalent.

Housing Loss Index: The housing loss index compares the housing loss rate against an average: the national average of all counties for which data was available, in the case of our national research, and the county average in our case studies.

As a benchmark for interpretation, at the national level, a county with a housing loss index score of 1 experiences a housing loss rate equal to the average of all other counties in the United States for which we have data. An index of 3 indicates that the county under consideration experiences a housing loss rate that is three times the national average. A housing loss index of less than 1 implies that the county under consideration is doing “better” on average (i.e., experiencing less housing loss) than all other counties in the country.

Case Study Selection Criteria

Early research involved the exploration of various U.S. counties for inclusion in case studies. We selected our locations based on a number of requirements:

- An early assessment of the prevalence of housing loss and instability.

- The availability of granular and mappable data for evictions and mortgage foreclosure, as well as tax foreclosure, to a lesser extent.

- The availability of a university partner and/or a New America Local office, in order to conduct key informant interviews “on site,” and to leverage existing networks in order to engage with local stakeholders.

- Regional variation, in order to account for differences in economics, politics, demographics, and histories.

Qualitative Methodology

After we selected our case study locations, we finalized research partnerships with: New America Indianapolis and the Institute for American Thought at Indiana University-Purdue University Indianapolis, in Marion County, Indiana; the Environmental Law and Policy Clinic at the Wake Forest University School of Law, the Department of Anthropology at Wake Forest University, and the Center for the Study of Economic Mobility at Winston-Salem State University in Forsyth County, North Carolina; and the Knowledge Exchange for Resilience at Arizona State University in Maricopa County, Arizona

From November 2019 to June 2020, graduate and undergraduate students from these institutions conducted key informant interviews (KIIs) with a wide variety of stakeholders, including government officials, housing advocates, real estate developers, journalists, lawyers, service providers, and community members to gain an in-depth understanding of local issues related to housing loss. Questions were developed collaboratively, and focused on how often residents lost their homes—and whether through eviction, mortgage foreclosure, or another mechanism; who was most at-risk of losing their home; where within the relevant county this loss was most acute; why people were losing their homes; and what happened after they did. In total, researchers conducted 31 interviews in Marion County, Indiana; 15 in Maricopa County, Arizona; and 20 in Forsyth County, North Carolina.

The researchers provided us with recordings and transcripts of the KIIs, a written summary of each interview, and a summary of findings.

Quantitative Methodology

Together with our data science and visualization partner, DataKind, we located, cleaned, standardized, and visualized the data on evictions, mortgage foreclosures, and, in certain cases, tax foreclosures. In our analysis, we tested for any statistical relationships between housing loss and a number of socioeconomic variables via correlation analysis.

Our nationwide index is limited to eviction and mortgage foreclosure data from 2014 to 2016. We were unable to include tax foreclosure due to the lack of accessible data for most U.S. counties. However, we have included tax foreclosure in our case studies for Marion County, Indiana and Forsyth County, North Carolina, as we were able to obtain the relevant data.

Project Data Sources

| National | Forsyth County, North Carolina | Maricopa County, Arizona | Marion County, Indiana | |

|---|---|---|---|---|

| Unit of Analysis | County | Parcel | Parcel | Parcel |

| Unit of Visualization{{4}} | County | Census Tract | Census Tract | Census Tract |

| Eviction | Eviction Lab at Princeton University | Forsyth County Geographic Information Systems (GIS) Office (MapForsyth) | Maricopa County Justice Courts | Eviction Lab at Princeton University |

| Mortgage Foreclosure | ATTOM Data Solutions | Forsyth County GIS Office (MapForsyth) | Information Market / Arizona State University | ATTOM Data Solutions |

| Tax Foreclosure | N/A | Forsyth County GIS Office (MapForsyth) | N/A | Marion County Auditor’s Office |

National data on evictions was supplied by the Eviction Lab at Princeton University,4 and data on mortgage foreclosures was provided by ATTOM Data Solutions.5 Using this data, DataKind generated nationwide, county-level maps depicting rates of eviction, mortgage foreclosure, and housing loss rate, as well as a map indicating overall data coverage for U.S. counties. Using the national data, we also analyzed the correlation between select five-year (2012–2016) ACS census estimates and the eviction rate, mortgage foreclosure rate, and the housing loss rate at the county level.

For our three case studies: we supplemented data from Eviction Lab and ATTOM with data acquired from local agencies, as described in the table above. In each case study location, we complemented the data with key informant interviews to better understand the context behind the data. We also analyzed the correlation between select five-year (2012-2016) ACS census estimates and the eviction rate, mortgage foreclosure rate, and the housing loss rate at the census tract-level.

Definitions

Eviction

Definition: An eviction occurs when a landlord forcibly expels a tenant from their rental property, resulting in the renter’s involuntary move from their home. Landlords may evict a tenant for “just causes,” such as the renter’s failure to pay rent, taking on boarders, damaging property, causing disturbances, or breaking the law. But in many American cities, landlords can evict renters even if they pay rent on time and follow their lease agreement. Based on our estimates, on average 2.6 percent of all renter households were evicted each year between 2014 and 2016. Yet the scale of the issue varies by state, and even within states.

Legal Process: Typically, an eviction court record is generated after a landlord files an eviction notice with the local court and serves a tenant with a notice to appear in court. At the hearing, the judge may rule that the eviction is justified and order the tenant to leave by a particular date, or the judge may dismiss the eviction. Almost all formal evictions in the United States take place in civil court, where renters lack the right to an attorney. As a result, most renters do not appear in eviction court and receive a default eviction judgment. Because eviction data, including the data used here, is gathered primarily from court documents, the numbers reflect these “formal evictions” conducted through the court system.

But evictions can occur informally, or outside of the legal system entirely, such as when a landlord imposes a rent hike, gives verbal notice to vacate, or performs an illegal lockout. In some places, experts estimate that these “informal evictions” account for half or more of all evictions. However, informal evictions often elude tracking, limiting attempts to fully account for housing loss.

As such, while the eviction data reported below provides some insights into the breadth of eviction in U.S. states, it does not capture the significant scope or impacts of informal processes that forcibly displace tenants.

A Note About the Eviction Measure We Focus On: Some studies suggest that anywhere between 60 to 80 percent of all eviction filings eventually result in the removal of a tenant from their home, regardless of the court case outcome.6 Yet we sought to be absolutely certain that our data, as well as the resulting analysis, represented actual evictions. While we admit that our eviction-related findings are most likely an undercount, the numbers still paint a bleak picture in many localities across the country. The decision to focus on recorded instances of eviction fits within our general belief that formulation of housing policy must be increasingly data-driven if decision-makers are to sufficiently direct outreach, funding, and resources to the most distressed communities.

It is important to note, however, that an eviction filing can have deleterious impacts itself—even if a case does not lead to a formal eviction judgment. In many jurisdictions, an eviction filing enters the public record and becomes part of an individual’s rental history, unless the eviction is formally dismissed in court.7 As a result, an eviction filing often appears on background check results as a red flag, and may dissuade potential landlords from renting to these individuals.8

Mortgage Foreclosure

Definition: A mortgage foreclosure occurs when a person who has taken out a mortgage to pay for a house, known as a borrower, loses their rights to that property. Usually, if a borrower fails to make multiple mortgage payments in a timely manner, the foreclosure process begins. The lender—most often a bank—applies to a court for authority to sell the property. Money received from the resulting sale is applied to debts on the property, including payments to the lender.9 Based on our estimates, 1.5 percent of all homeowners with mortgages were foreclosed upon between 2014 and 2018. Yet the scale of the issue varies by state, and even within states.

Legal Process: In states with a judicial foreclosure process, proceedings typically take place before a judge, who determines whether the homeowner is in default, assigns property ownership to the mortgage lender, and determines a date upon which the property will be sold. These proceedings usually last between six and 18 months. Once the foreclosure is completed, the individual or family living in the house—usually the homeowner, but sometimes a renter—must vacate, and the property is put up for sale at public auction. In the case that there is no highest bidder or no bids are made at the minimum asking price, the title remains with the mortgage lender.

In states with a non-judicial foreclosure process, a mortgage lender can immediately send a “notice of foreclosure” or “notice of default” to a borrower in default, as well as to the recorder of deeds. In these states, the lender can set the date of the property’s sale, while the homeowner can sue to stop the foreclosure process.10

In the event of foreclosure of a rental property, tenants are subject to immediate eviction upon transfer of title.

A Note about the Mortgage Foreclosure Measures We Focus On: To be sure that we only counted instances where a homeowner defaulted on their mortgage payments and lost their house in a foreclosure, we avoided any “pre-foreclosure” datasets, which record any homeowners in default. This is because many of these houses may be foreclosed upon but never actually sold. We chose instead to analyze mortgage foreclosure sales exclusively. For the purposes of this report, a “mortgage foreclosure sale” includes foreclosure sales, short sales, and REO sales—three common types of real estate transactions resulting from payment default and foreclosure processes.

Tax Foreclosure

Definition: Tax foreclosures occur when a local government sells a homeowner’s property after the homeowner falls exceedingly behind on their property taxes. All U.S. states have laws that permit the placing of a lien on the property for the amount of property taxes past due. If the taxes remain unpaid after a certain period of time, municipalities auction the lien or the property to private purchasers and investors. Prior to tax foreclosure, most owners have a right to redeem their property by paying the tax sale purchaser the purchase price, plus interest, penalties, and other costs. A failure to redeem leads to tax foreclosure.

Many argue that tax foreclosure laws serve an important purpose in ensuring that local governments recover tax revenue needed to provide essential services. However, these laws often produce profits for tax sale purchasers at much higher rates than ordinary investments. Most banks, for example, provide interest on savings accounts at less than 1 percent, while many states permit tax sale purchasers to recover interest at rates of 18 percent or more. Such excessive penalties can make it near impossible for homeowners to stave off tax foreclosure.

Citations

- U.S. Census Bureau ACS 1-year estimates, 2018 source

- Data were collected at the county or county-equivalent level. In the United states, a “county-equivalent” is an area that is not within the geographic boundaries of any county but is defined as equivalent to a county by the U.S. Census Bureau for statistical purposes. For example, in Maryland, Missouri, Nevada and Virginia, one or more cities are independent from any counties and are considered county-equivalents.

- The ‘national’ housing loss rate described here and used as the denominator for the national Housing Loss Index does not represent the entire United States, but rather is calculated based on the 2,221 counties in our dataset for which both eviction and foreclosure data were available. This represents about ⅔ of the entire United States, and excludes 922 counties.

- The DataCorps team utilized their count of evictions and calculated rates based on the number of renter households provided by ACS 2012-2016 data. The renter households may differ slightly from the numbers used by Eviction Lab which used a proprietary source of this data (ESRI), which accounts for any (typically small) variation between rates and averages reported by DataKind and Eviction Lab. In addition, eviction data for Maricopa County was provided by Maricopa County Justice Courts as it was not available from Eviction Lab.

- There was considerable variation in the amount of foreclosure data available among the counties for which data was available. For the five years between 2014 and 2018, some counties had data for all 60 months, while other counties had data for less than 20 percent of this period. Unfortunately, it is not clear from the ATTOM dataset if the absence of recorded foreclosure sales for a county in a given month reflects a genuine absence of sales, or is merely missing data.

- For example, see Collinson & Reed, The Effects of Evictions on Low-Income Households, 2018; Shelton, Mapping dispossession: Eviction, foreclosure and the multiple geographies of housing instability in Lexington, Kentucky, Geoforum, 2018; and Immergluck, D., Ernsthausen, J., Earl, S., & Powell, A. (2020). Evictions, large owners, and serial filings: findings from Atlanta. Housing Studies, 35(5), 903-924.

- Raymond et al. Cityscape

- source

- Wisconsin Homeownership Preservation Education, Understanding Default and Foreclosure, Madison, Wisconsin: University of Wisconsin-Extension, Winter 2010, source

- Urban 2009 report

Housing Loss and Poor Data

“You can’t manage what you can’t measure.” – The New Republic

Our project began ambitiously and, as we found out, naively. We had set out to build a comprehensive, nationwide map of total home and land loss throughout the United States. We wanted to display everything from evictions and mortgage foreclosure to more obscure forms of loss like civil asset forfeiture, takings via eminent domain, partition sales of heirs property, and the privatization of public land.

Last summer, we gathered a dozen of the nation’s foremost property rights experts to brainstorm on how to execute this grandiose plan. The experts were extremely polite and helpful, but their occasional looks of befuddlement betrayed their skepticism about the scope of our effort. As we learned over the previous year, they were right.

The dirty secret of the housing space is that a significant amount of the data needed to comprehensively illustrate property loss is either inaccessible, of poor quality, or simply does not exist.

Over the last 12 months, our project scope narrowed to focus on mechanisms of loss that are best represented in spreadsheets and databases: evictions, mortgage foreclosures, and, to a lesser extent, tax foreclosures. Yet efforts to obtain even this data and prepare it for mapping and analysis took several months, as we encountered myriad issues. Datasets were missing entire years or sets of census tracts. Critical information, such as addresses and court case verdicts, was not recorded. Court-provided eviction datasets did not capture informal evictions, and many are plagued by well-known issues related to quality control. Finally, there was a striking absence of standardization across datasets, exacerbated by often bewildering idiosyncrasies.

Yet within other areas of the U.S. housing space, such as affordable housing and homelessness, public policy and funding allocation is increasingly data-driven. The Department of Housing and Urban Development (HUD), for example, utilizes its voucher management system to fund, monitor, and manage the use of housing choice vouchers by public housing agencies. Homeless service providers are also required by federal mandate to collect and share information on homeless populations with HUD, which helps to steer funding for Continuums of Care across the country.

The real estate sector is also heavily data-driven. Companies such as Zillow, CoreLogic, ATTOM, and Black Knight comprise a lucrative industry focused on collecting granular real estate data, bundling it, and selling it to brokerages, rental sites, insurance companies, and even government agencies. Other firms provide landlords and property management groups with information on households’ rental histories, or investors with aggregated tax sale lists.

And yet, data on an essential component of the housing space—housing loss—is often difficult to obtain, cost-prohibitive, of poor quality, or non-existent, even after the mortgage foreclosure and eviction crises resulting from the Great Recession. The federal government did create the National Mortgage Database in 2010, in order to track delinquent mortgage payments and foreclosures, but according to the New Republic, the database only includes 5 percent of all mortgage holders nationwide. Despite calls for an eviction database, such as in Senator Michael Bennett (D-CO)’s 2019 Eviction Crisis Act, no such tool has materialized.

Publicly available, high quality data is critical for crafting effective housing policy, and we would be remiss not to mention the tremendous efforts of organizations such as the Eviction Lab, Loveland, City Life/Vida Urbana, the Anti-Eviction Mapping Project, Tenants Together, JustFix NYC, and countless others that provide open data on evictions, tax foreclosures, and other types of housing loss. Various city and county GIS offices around the country provide invaluable geospatial tools, too. During trips to South Bend, Indiana and Winston-Salem, North Carolina, for instance, we met civil servants more than ready to assist in our search for data. But issues related to accessibility, data quality, and data coverage persist at many levels of government, making it nearly impossible for anyone to carry out a comprehensive analysis of housing loss in the United States.

Why It Matters

“If you don’t know how many people are being evicted in America, then who’s to say it’s a serious problem?” – Researcher, Eviction Lab1

The limits that poor data create for decision-making around housing policy cannot be understated, especially within the context of increased housing insecurity amid the pandemic. Municipal leaders simply cannot make smart decisions about housing solutions if they do not know the scale of the problem, where housing loss is most acute, and who is most impacted. One high-ranking city official told us that he had rental assistance funds to distribute, but had no idea where within his city eviction rates were highest, and was in the dark about how to direct the money.

Not only that: In the absence of data, it is easy for politicians, the media, and advocates to shape narratives based on anecdotal or incomplete information. For example, last year the tremendous efforts of ProPublica and the Atlantic, among others, shone a spotlight on Black land loss as a result of heirs property. But, experts say that heirs property is not only a problem for the Black community: it impacts colonias in Texas, white communities in Appalachia, and Native lands. However, without good data on heirs property, media attention has shaped this issue as solely a Black problem.

The Road to a National Dataset

The ability to create a national database for housing loss is stymied by a number of factors. The data may be too difficult to generate, or data storage is so decentralized that aggregation at scale would be extremely resource-intensive and time-consuming. Local policies, differences in institutional capacity, and a lack of standardization across jurisdictions countrywide further compound the problem.

Many of the most vulnerable forms of housing and land tenure are informal, existing outside of the legal system by definition. It is likely that hundreds of thousands of Americans—perhaps even millions—own property informally, without any title or deed. For instance, roughly half a million people live in Texas’ colonias, makeshift houses extralegally built on subdivided plots of land near the Rio Grande and elsewhere. Heirs property, or land passed down from generation to generation without a will, is estimated to comprise more than one-third of Black-owned land in the southern United States. Outside of a few pioneering, albeit limited, geographic studies, nobody is able to provide an actual figure regarding informal property ownership, a crucial datapoint for research and policy. Without any way to prove a negative, the data remains out of reach.

But even more mainstream forms of housing loss are marred by coverage gaps.

Most notably, tax foreclosure, which most often occurs due to the long-term non-payment of property taxes, is omitted from our national-level analysis. No entity publicly publishes or even sells nationwide tax foreclosure data, according to multiple academic experts and industry leaders.

This lack of data does not imply that tax foreclosure is an insignificant issue. In fact, we were motivated to look at tax foreclosures after seeing that Detroit, Michigan experienced 143,958 tax foreclosures between 2002 and 2016, based on research by Loveland Technologies. Aside from disproportionately impacting poor, usually minority, households, these tax foreclosures led to vacancy, blight, and the deterioration of entire neighborhoods. But when we attempted to replicate Loveland’s research nationwide we found that the only data available was on tax sales, far upstream from actual tax foreclosures. So, while we had an idea of how many properties entered the tax foreclosure process, we had no idea how many people actually lost their homes. Industry experts told us that the “conversion rate” from tax sale to tax foreclosure hovers around 0.5 percent to 5 percent nationally, but our Indianapolis dataset suggests otherwise. The conversion rate in Marion County is approximately 25 percent.

The decentralized governance structure of mortgage foreclosure data similarly frustrated our efforts to collect a national dataset and led to our decision to purchase data from ATTOM Data Solutions. Private firms such as ATTOM possess the resources, networks, and experience to collect mortgage foreclosure data at scale. These companies provide a valuable service, and their products are not cheap, unsurprisingly. Access to the data is cost-prohibitive to many stakeholders, resulting in unequal power dynamics and information asymmetries.

The geographic coverage of ATTOM’s nationwide dataset is extensive. Yet gaps clearly exist in the middle of the United States, and in a few other sparsely populated areas, such as the Upper Peninsula of Michigan, northern Alaska, and southeast Utah. In total, mortgage foreclosure data is not reported in 409 U.S. counties and county equivalents, or 13 percent of the country. Because ATTOM is a commercial actor, its decisions around data collection are driven by profit: In some counties an overall lack of real estate transactions means that data collection is not worth ATTOM’s efforts.

The eviction dataset created by Eviction Lab, by far the most comprehensive aggregation of eviction data in the United States, also contains noticeable gaps in coverage. The initiative’s methodology report outlines various difficulties encountered during the data collection process. County-level data from Alaska, Arkansas, and North and South Dakota is omitted from the dataset, for example, because local governments reported eviction data too inconsistently between 2000 and 2016. Other state policies and local idiosyncrasies created additional barriers to data collection: the extremely decentralized court structure in Upstate New York, sealed eviction files in California, inconsistent court records in New Jersey, and a widespread inability to access data in rural counties throughout the American South, to name a few.

Quantitative analysis of available data also does not provide a full idea of the scope of evictions, because of the prevalence of "informal evictions," which occur outside of the formal legal process. A landlord might remove a unit’s door or change locks to force a tenant out. Other times, a hike in rent or the mere threat of an eviction filing is enough to convince tenants to pack their bags and move. Research by Matthew Desmond, author of Evicted and principal investigator at the Eviction Lab, suggests that in Milwaukee two informal evictions happen for everyone one formal eviction. We are uncertain if rates are similar in other communities, but if the occurrence of informal evictions are anything close to what Desmond found in Milwaukee, then we are severely undercounting the problem.

On the Ground: Binders Full of Foreclosures

“This is on hold. I have multiple other things going on…” – County clerk, in response to request for data2

The United States contains 3,143 counties and county-equivalents, each with its own laws, government offices, and court systems. Individual counties and municipalities collect, maintain, and share data on housing loss through many different methods. Within jurisdictions, various government offices can hold overlapping and fractured land administration mandates. A lack of coordination between these units, along with disparities in institutional capacity, often results in unstandardized data with varying levels of reliability.

No two counties are the same, and it can be difficult to ascertain what data is available, where it is stored, and who can share it. Aside from a quick visit to the Eviction Lab or Loveland website, locating open data on housing loss requires a significant allocation of resources and time.

Our own data search led us across the country, with varying degrees of success. Occasionally, we connected with the right civil servant or government office, someone with intimate knowledge of the available data, its storage location, and how to access it. A short conversation with MapForsyth, the local geographic information office in Winston-Salem, North Carolina, for example, resulted in access to neatly organized Excel spreadsheets on evictions, mortgage foreclosures, and tax foreclosures. The clean and granular data more or less matched project needs, and maps were generated with relative ease as a result.

The data search was entirely unsuccessful at other times. We greeted a sheriff’s office clerk in a mid-sized Midwestern city one morning, inquiring about mortgage foreclosure data, and were unenthusiastically handed a stack of binders. Short on time, we were unable to sort through the many pages and extract any information. Back in Washington, D.C., we asked if the office could scan the documents. The clerk replied that our request was not a priority, and soon became unresponsive to our emails.

In a major Sun Belt city, we spent half a day trekking from government office to government office, asking about tax foreclosure data. No office possessed any readily available data, and after an additional six months of emails and phone calls, we were told that the relevant information did not exist in a mappable format.

Data was inaccessible or nonexistent even if the problem of home loss was widely acknowledged. Housing advocates, researchers, service providers, and decision-makers in Indianapolis repeatedly mentioned that mortgage foreclosures were a still significant issue in Marion County, a full decade after the Great Recession. But no one was able to provide the data—not the mayor’s office, the courts, the Chamber of Commerce, nor the research universities. After exhausting all options, we paid ATTOM thousands of dollars for relevant data.

Quirky Data and No Verdicts

“That could be because the clerk did not enter that…” – Communications Officer, Arizona, explaining data gaps3

Locating and obtaining the necessary datasets for this project was only half the battle. Because housing data is not standardized to a national, or even state, level, each dataset came with its own quirks and caveats.

For example, the eviction data provided by MapForsyth contained successive, repeat addresses. But these were not entry mistakes. Rather, this repetition signified that multiple tenants were evicted from the same address, perhaps a multi-family rental building. Our contact at MapForsyth thankfully shared this peculiarity with us, otherwise we might have de-duplicated the data, leading to an undercount of 2014-2018 evictions by 7,078.

Other datasets were significantly incomplete. Approximately 30 percent of 2014-2018 eviction filings in Maricopa County, Arizona, or over 97,000 cases, lack judgment information. The reasons vary: the case was dismissed; pre-trial mediation between the landlord and tenant worked; both parties won something; or the clerk simply failed to enter the information. With so many possible outcomes, we were unable to discern whether an eviction occured in each of these cases, and these filings were omitted from our data visualizations. As a result, this report’s maps under-represent evictions in Maricopa County.

We wrestled with whether producing an incomplete map was worse than producing no map at all, and in the end decided that visualizing two-thirds of evictions with appropriate disclaimers was better than not visualizing any evictions. Other researchers have come to the opposite conclusion: Eviction Lab, for example, excludes Phoenix from its map and rankings because they determined the data was too poor to be trustworthy, even though by our count the city has some of the highest eviction rates in the country.

Geocoding, or assigning latitude and longitude to each instance of housing loss, was another significant issue. In order to map county-level data for the entire country, we had to ensure that geocoded data were adjusted to a standard appropriate coordinate reference system (as in the case of Forsyth County), and in cases where the datasets we acquired needed to be geocoded (as in the case of evictions in Maricopa County), we had to navigate unstandardized collection of address data. It required significant time to translate this data into a mappable format.

Worse, some datasets were missing GIS information. Almost a quarter of 2014-2018 eviction filings in Maricopa County, or roughly 66,500 cases, lacked granular geocodes. We were able to incorporate these filings into our overall eviction rate for the county, but were forced to exclude the evictions from our maps. So while the absence of geocoding in a housing loss dataset does not preclude all analysis, it hinders the ability for researchers, housing advocates, and policymakers to know who are losing their homes, and where. This and similar issues contribute to imperfect policy development, as funding, resources, and outreach could be misdirected into the wrong communities and neighborhoods.

Power Dynamics and Policy Implications

“Some don’t want heirs property to be identified. Investors can use that information to do unscrupulous things” – Government researcher4

Licensed data on housing loss, such as privately-bundled mortgage foreclosure data, is usually expensive. Local nonprofits, community-based organizations, and even some cash-strapped municipal government offices may lack the funds to purchase these datasets.

This lack of open data creates significantly unequal power dynamics in the U.S. housing space, and leads to inadequate policy solutions at various levels of government. In some cases, it leads to exploitation of the very communities who are experiencing property loss, as better informed opportunists swoop in to take advantage of communities with precarious property rights.

Wall Street’s exclusive access to information on mortgage foreclosures following the Great Recession, for instance, fundamentally altered the U.S. housing space. Private equity, hedge funds, and other investors purchased hundreds of thousands of single-family homes in foreclosure, totaling over $60 billion in value. Many times, firms such as the Blackstone Group bought these properties at discounts of 30 to 50 percent. According to the New York Times, 95 percent of distressed mortgages managed by Freddie Mac and Fannie Mae were auctioned off to Wall Street.

By contrast, the lack of a government database on mortgage foreclosures resulting from the 2007 to 2009 economic downturn contributed, in part, to the insufficient response from policymakers to better protect vulnerable homeowners.

After the mortgage foreclosure crisis, entire neighborhoods were purchased and converted into rental properties; the United States added less than 1 million owner-occupied homes between 2007 and 2017, but 6.5 million in renter-occupied homes. The information asymmetry between government and Wall Street irrevocably changed cityscapes and put communities at risk.

The rental market provides another example of powerful information asymmetries. Many landlords subscribe to online services that flag individuals with prior evictions, or even eviction filings, and frequently deny rental applications based on this data. And yet community-based organizations, created to help these very same renters find stable housing, cannot access this information.

Conclusion: A Critical Policy Recommendation

The report text that follows surfaces dozens of findings and puts forward multiple policy recommendations. And yet, if the reader were to take away only a single recommendation from this report, it would be this: That there is an urgent need for all levels of government—federal, state, and local—to work together to improve the quality and availability of housing loss data. It is impossible to solve a problem that is poorly understood, and with the lack of records available we simply do not fully grasp the issue of housing loss in the United States. Our report and similar efforts shine some light on particular components of this problem, in particular places. But these studies are far from comprehensive. Only after open, accurate, and up-to-date data is available on who is losing their homes, where, when, and how, we will be able to protect at-risk families from the terrible consequences of displacement.

Citations

- From an interview with the authors.

- From a conversation with the authors.

- From a conversation with the authors.

- From an interview with the authors.

Housing Loss in the United States: Our National Rankings and Maps

We estimate that nearly 5 million Americans are forcibly displaced from their homes every year due to eviction, mortgage and tax foreclosure, and other mechanisms of loss. This year, as a result of the COVID-19 crisis, we anticipate that number will be magnitudes greater. As we write, more than a quarter of Americans have reported that they cannot pay their rent or mortgage. On September 1 the Centers for Disease Control (CDC) announced a nationwide ban on evictions until the end of the year. However, rent will still be due on January 1, and thus far the government has not offered rent forgiveness and only limited relief.

We also know that affordability was the major driver of housing instability, even before the COVID-19 crisis. Housing is the largest expenditure for most American households, and is becoming increasingly unaffordable. The growth of housing costs has outpaced income growth over the last sixty years, contributing, in part, to an ongoing affordable housing crisis. Between 1960 and 2016, the median monthly rent across the United States increased by 61 percent while median income among renters increased by only 5 percent. Among homeowners, the median home value increased 112 percent while the median homeowner income increased by 50 percent.1 These disparities result in greater housing cost burdens for both renters and homeowners, and put both groups more at-risk for missing rent or mortgage payments, which very often lead to home loss through eviction or mortgage foreclosure. In some instances, these two processes are interrelated, such as when a renter is evicted because their landlord is experiencing a foreclosure.2

But beyond that, we know very little about where housing loss is most acute, and who is most at risk. As mentioned in the previous section, U.S. housing loss data is poor and incomplete, leading decision-makers to underestimate housing loss across the country and leaving them in the dark as to how to remedy the issue. Likewise, this report certainly under-represents the actual scale of home loss across the country. We were not able, for example, to capture partition sales that force Black families off their land, or the abandonment of Puerto Rican homes destroyed by Hurricane Maria, nor were we able to analyze tax foreclosures, informal evictions, takings via eminent domain or other forms of housing loss.

Instead, we chose to focus on two common forms of housing loss for which data does exist, albeit imperfectly—eviction and mortgage foreclosure. Although these two modes of loss are distinct in the timescales in which they occur and the category of tenure they impact, both forms of displacement bring about deleterious effects on the communities and neighborhoods in which they take place. In some cases, mortgage foreclosures on renter-occupied properties lead directly to the eviction of tenants; in other cases, foreclosures occur independently of eviction but high rates of both forms of displacement are found to be geographically concentrated. Our focus on these two mechanisms aims to characterize housing loss holistically and to identify regions at risk of experiencing the negative downstream impacts of housing instability, which are shared regardless of the particular mode of displacement.3

How Are People Losing Their Homes?

Housing Loss Index4

In order to measure housing loss that includes both evictions and mortgage foreclosures, we first calculated each county’s housing loss rate. The housing loss rate combines the total number of evictions and the total number of mortgage foreclosures for a given geography, and then normalizes that sum by the total number of renters and the total number of homeowners with a mortgage within the given geography.

We then converted the housing loss rate into a housing loss index by comparing a given county’s housing loss rate to the national average, across all counties for which we have data. A county with a housing loss index of 1 experiences a housing loss rate equal to the national average, while an index of 3 indicates that the county experiences a housing loss rate that is three times the national average.

Based on these calculations, we found that the national average housing loss rate was 2 percent between 2014 and 2016.

On a state-wide level, housing loss between 2014 and 2016 was most severe in Arizona, Nevada, and Florida. All three of these states saw rates of housing loss of more than 3.8 percent, almost twice the national average. As of June 2020, each of these states had unemployment rates at or above 10 percent. Given that non-payment of bills is by far the most common cause of housing loss, and given their pre-existing housing vulnerability, we expect these states to be disproportionately impacted by the pandemic-era housing crisis.

Conversely, the states reporting the highest unemployment rates as of June 2020—Massachusetts, New Jersey, and New York—have historically had below-average levels of housing loss.5

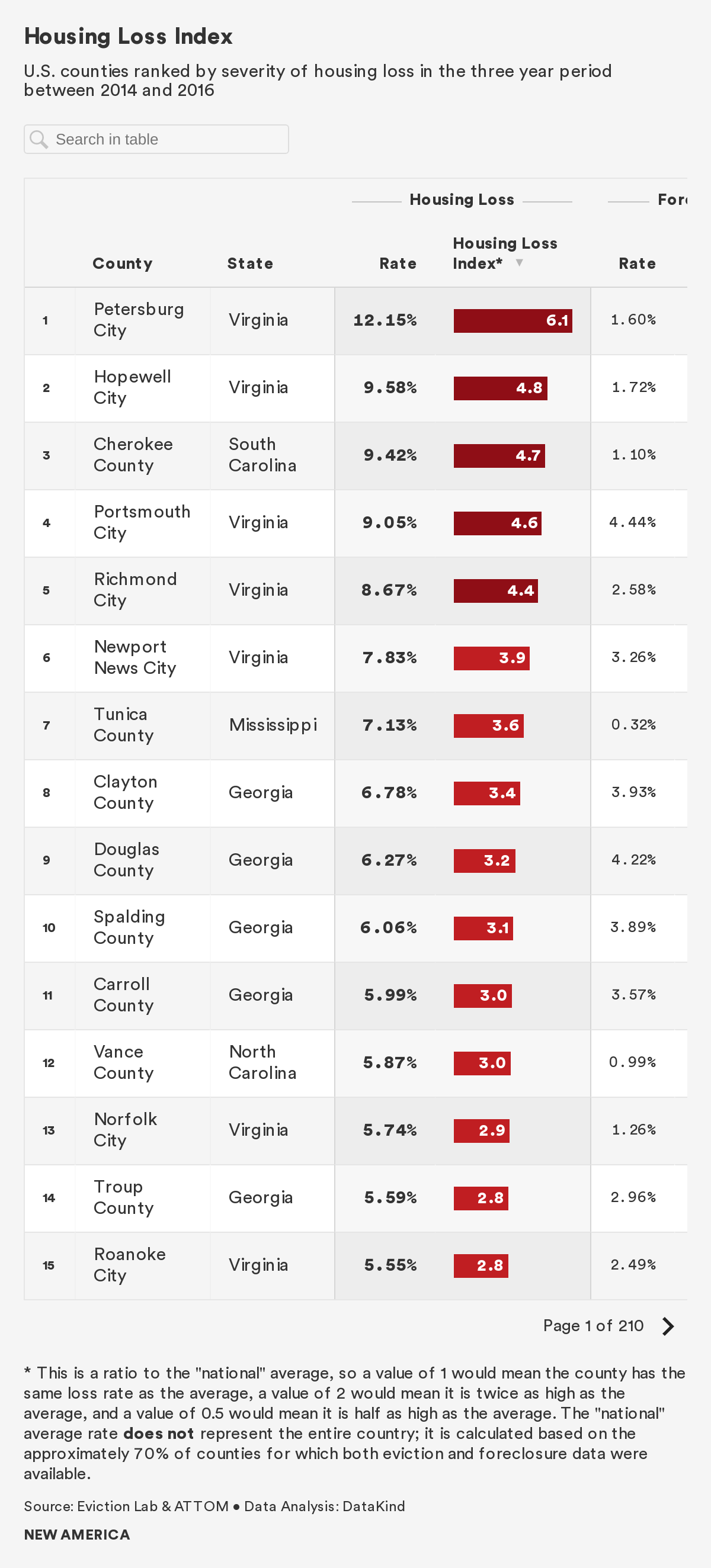

On a county and county-equivalent level, Petersburg City, just south of Richmond, Virginia, had the highest overall housing loss rate in the country. The housing loss rate in this independent city is roughly 12 percent, six times the national average. Eviction accounts for 96 percent of all housing loss in Petersburg City, affecting approximately one in eight renters, and drives the high overall housing loss rate. Foreclosure rates in Petersburg City are also slightly above the national average.

Of the counties or county-equivalents with the twenty highest housing loss rates, eight are located in Virginia, eight are located in Georgia, and the remaining four are located in Mississippi, North Carolina, Florida, and South Carolina, respectively. These 20 counties have rates of housing loss ranging from 4.4 to 12.2 percent—between two and six times the national average.

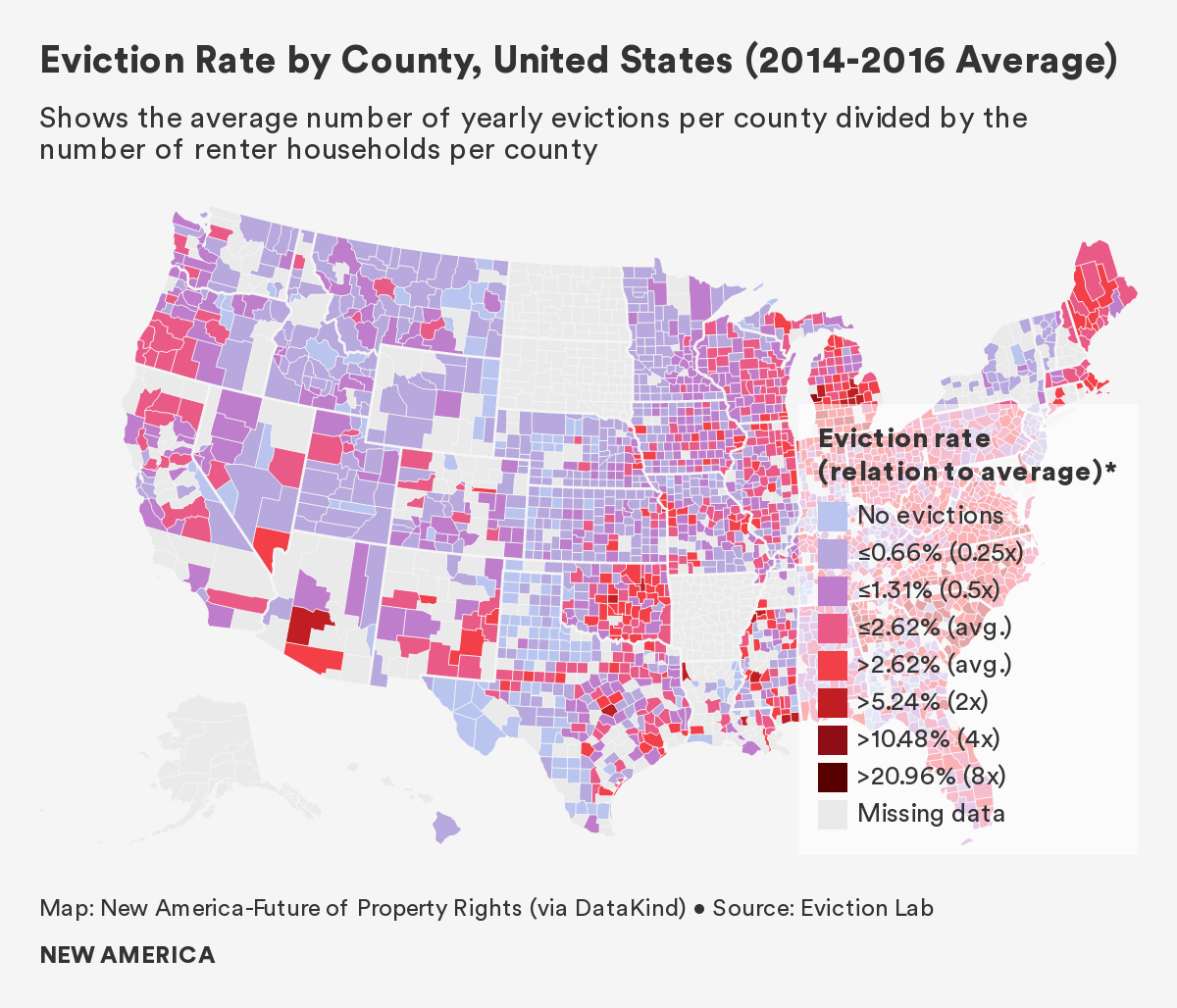

Eviction Findings: The national average eviction rate was 2.6 percent between 2014 and 2016. Based on available data, we know that approximately 900,000 renter households were evicted from their homes each year. However, data is unavailable for some counties and states, with North and South Dakota, Arkansas, and Alaska notably absent, as indicated on the map below.6

States with the highest rates of eviction are generally located in the Southeastern region of the United States, while those with the lowest rates of eviction are located in the Midwestern and Northwestern parts of the country. Though our findings suggest a geographic pattern, due to incomplete data we cannot determine whether these patterns are coincidental or due to common underlying mechanisms that relate to policy or demographics.

South Carolina experienced the highest eviction rate of any state between 2014 and 2016, at a rate of 6.2 percent and with an average of 26,430 evictions per year.7 Twenty of South Carolina’s 46 counties see rates of evictions greater than 5 percent, about twice the national average. Other states with high eviction rates include Arizona, Virginia, and Delaware.

By contrast, Minnesota had the lowest rate of eviction during the same period, at 0.8 percent and with an average of 4,802 evictions per year. Other states with low eviction rates include Montana, Utah, and Oregon. Given the prevalence of missing eviction data, it should be noted that our findings are limited to those states and counties for which data are available; as a result, states with large amounts of missing data such as North and South Dakota, are not represented in our analysis.

Cherokee County, a small county in northern South Carolina, had the highest eviction rate in the country: 17.9 percent, or nearly seven times the national average. Gaffney, the county seat, is known as the Peach Capital of South Carolina and also has the dubious honor of being the hometown of Frank Underwood, the fictional main character of the drama House of Cards. Evictions in Cherokee County account for 94.1 percent of all housing loss in the county, though renters comprise only a third of the population. Cherokee County had an 11 percent unemployment rate as of June 2020, portenting an even greater eviction rate in the coming months.

Perhaps most striking, six independent cities in Southern Virginia express eviction rates that rank in the top 10 nationally. Experts at the local RVA Eviction Lab point to several factors—including low court fees for filing evictions, and a lack of policies that protect renters—as driving the region’s high eviction rates.

Several counties in Georgia, Michigan, and Mississippi, respectively, also had acute eviction rates.

U.S. Counties With Highest Average Eviction Rates (2014-2016)

| Rank | County | State | Percent Renters | Eviction Rate |

|---|---|---|---|---|

| 1 | Cherokee County | South Carolina | 30% | 17.88% |

| 2 | Petersburg City | Virginia | 59% | 16.82% |

| 3 | Hopewell City | Virginia | 50% | 14.64% |

| 4 | Portsmouth City | Virginia | 46% | 13.01% |

| 5 | Richmond City | Virginia | 59% | 11.69% |

| 6 | Muskegon County | Michigan | 26% | 11.27% |

| 7 | Newport News City | Virginia | 51% | 10.99% |

| 8 | Hampton City | Virginia | 44% | 9.84% |

| 9 | Vance County | North Carolina | 40% | 9.80% |

| 10 | Houston County | Georgia | 35% | 9.71% |

| 11 | Anderson County | South Carolina | 29% | 9.49% |

| 12 | Berkeley County | West Virginia | 27% | 9.45% |

| 13 | Tunica County | Mississippi | 61% | 9.20% |

| 14 | Calhoun County | Michigan | 30% | 9.15% |

| 15 | Douglas County | Georgia | 34% | 9.09% |

| 16 | Clayton County | Georgia | 49% | 8.98% |

| 17 | Carroll County | Georgia | 36% | 8.87% |

| 18 | Clinton County | Michigan | 20% | 8.74% |

| 19 | Hinds County | Mississippi | 41% | 8.71% |

| 20 | Rockdale County | Georgia | 32% | 8.64% |

Evictions in each of these counties or county-equivalents is undoubtedly influenced by unique demographic, economic, political, geographic, and historical factors. Further research is required to determine the underlying causes that are driving high eviction rates in these locations.

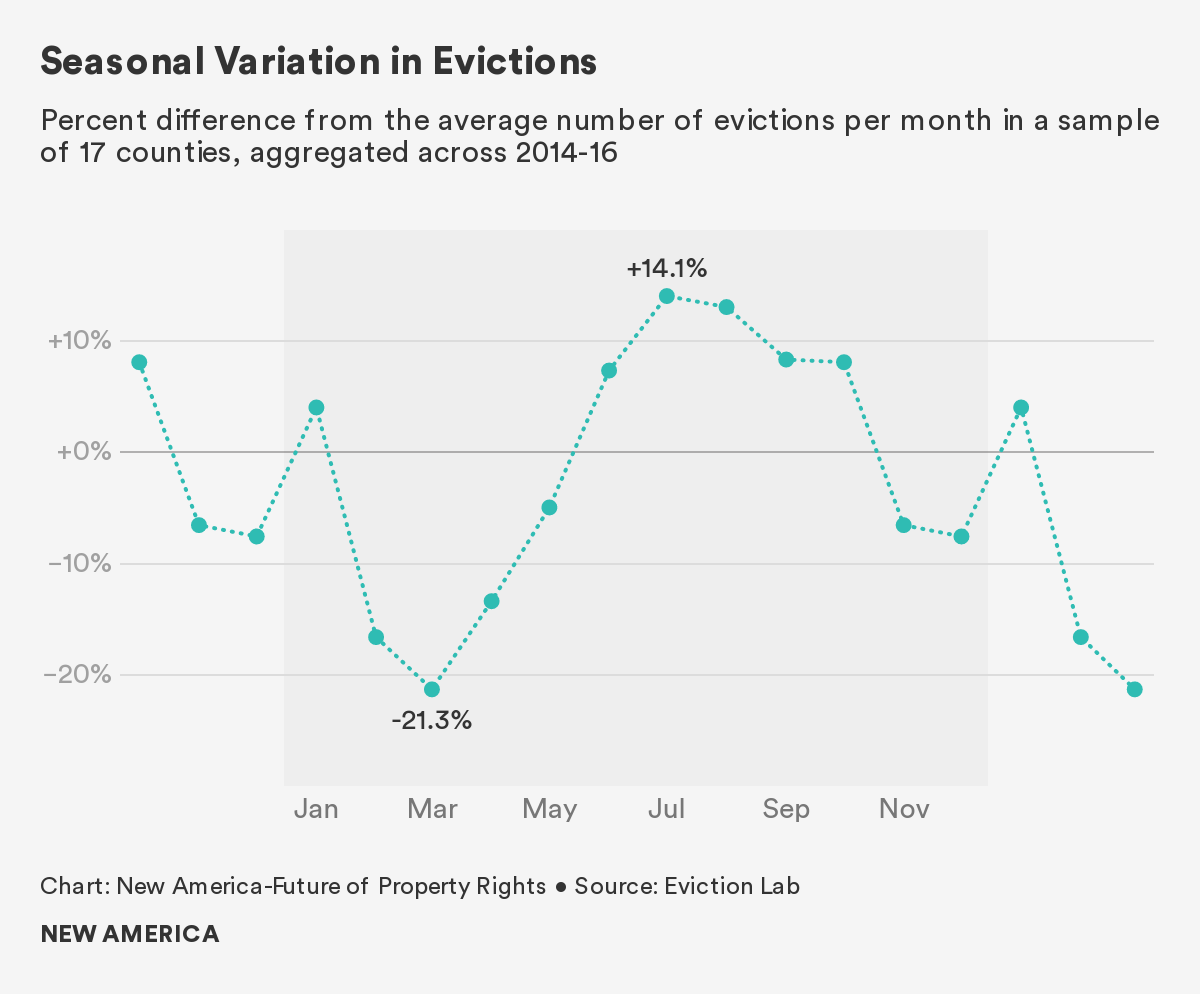

A Spotlight on Summer Eviction

An analysis of more than 300,000 evictions over a three-year period across 17 counties conducted by New America and Eviction Lab shows that evictions spike in summer. The increase is not subtle: Eviction rates across the country are on average 40 percent higher in July and August than at their low point in March. In some cities, like Dallas and Richmond, eviction rates double from spring to summer.

Little is known about why evictions spike in summer, though researchers have some guesses.