Designing Better Small Dollar Loans

Abstract

New America Chicago’s CivicSpace program invited 32 residents from neighborhoods targeted by predatory lenders to participate in three design sessions between 2022 and 2023 in which they discussed who borrowers trust for loan information, what constitutes a trusted lender, and what small dollar loan features may be most appealing. The paper ends with nine ways to improve lending practices in low- and moderate-income communities and nine policy recommendations to help Americans access safer loan products.

Acknowledgments

Thank you to Woodstock Institute and the many nonprofit partners around the country who have led the fight against predatory lending for many years. We are also profoundly grateful to the CivicSpace community members who shared their experiences with us.

We would like to thank The Chicago Community Trust and our other major donor for their generous support of this work.

Note: We have changed the names of session participants, loan products, and in one case replaced the term Community Development Financial Institution (CDFI) with the term credit union in participant activities to maintain their confidentiality and for research methodology purposes.

Editorial disclosure: The views expressed in this report are solely those of the authors and do not reflect the views of New America, its staff, fellows, funders, or its board of directors.

Introduction

In 2022 and 2023, New America Chicago hosted its first series of community design sessions as part of a new community engagement initiative called CivicSpace. Targeted at areas around Chicago with high predatory lending rates,1 these sessions asked borrowers to respond to alternatives to predatory loans and to consider what would help improve uptake of more affordable financial products. In 2019, individuals in 40 Chicago-area majority minority zip codes took out over $65 million in small dollar loans (not including interest and fees),2 so responsible lenders would do well to pay attention to the needs of these borrowers.

Partnering with 32 residents living around Chicago who had recent experience accessing small dollar loans, the attendees worked together to answer two questions: (1) Where do you go for information you can trust about small dollar loans; and (2) what features make those loans safe and useful? Answers to these questions are important now, when the cost of living has jumped, making it more difficult for many Americans to feed and house their families.

These Chicago residents generated an abundance of policy and practice ideas for designing small dollar loans to help people solve cash flow challenges. Participants also described their ideal ways to learn about loans and gain the financial literacy skills to leverage those loans. They were interested in simple loan processes, flexible options, ways to build credit, and wealth-building opportunities, in addition to short-term emergency assistance.

Understanding the perspectives and preferences in lower-income Black and Latino communities is important, as Black and Latino households in Cook County are far more likely to be financially vulnerable than their counterparts nationwide (39 percent versus 20 percent). Around half of Black and Latino Cook County residents (51 percent and 46 percent, respectively) say their household debt is not manageable.3

Participants who had some experience with high-interest personal loans were recruited, particularly those living in areas around Chicago that were hardest hit by exorbitant predatory loans prior to the passage of Illinois’s 36 percent cap on loan annual percentage rate (APR) via the Predatory Lending Prevention Act (PLPA). The first community design session was held at The Chicago Community Trust in September 2022, with 10 participants of different races and ethnicities. The second session was held in June 2023, in collaboration with local nonprofit Palenque LSNA, with 11 Latina participants recruited from Belmont Cragin, Logan Square, and the surrounding area. The final session was held in August, at the Woodson Regional Library, with 11 participants, most of them Black, recruited from the southern suburbs and area around Washington Heights.

“Many times people don’t want to talk about money, but they don’t ask until it is too late. Everyone needs to help each other, especially disenfranchised and minorities. It tends to be Black and Brown communities. We all need to help each other. Doesn’t matter if you’re Black or Brown. You should help each other to live because at the end of the day, poverty affects everyone.” —Gaby, 34, Irving Park

This report outlines the ideas that residents expressed the most agreement with and offers a summary of the pain points they experience with short-term, small dollar borrowing. For details about the demographics of the participants, please see Appendix A. For details on the methodology and research process for our sessions, please see Appendix B or read our Chicago Residents Design Better Small Dollar Loans brief for more about this approach.

Meegan Dugan Adell/New America

Citations

- Meegan Dugan Adell, Kathie Kane-Willis, Spencer Cowan, Hala Kourtu, and Vanessa Rangel, Ill-gotten Gains: Predatory Lending and the Racial Wealth Gap in Chicago (Chicago: New America, 2022), source.

- Adell et al., Ill-gotten Gains, source.

- Necati Celik, Meghan Greene, Wanjira Chege, and Angela Fontes, Financial Health Pulse 2022 Chicago Report (Chicago: Financial Health Network, January 2023), source.

Summary of Challenges

In each of the three sessions, different challenges were mentioned that made access to small dollar loans more difficult for residents. This section explores those barriers so that loan providers in the financial industry, as well as nonprofits and policymakers, can make the lending process less intimidating and easier to navigate.

Gaps in Information

- The most frequent challenge mentioned was knowing where to obtain a loan. Most people simply did not have a clear sense of where to go to borrow money at reasonable rates when they had a major unexpected purchase or regular cash flow issues. Many felt that finding $2,000 for an emergency would be extremely difficult.

- Participants perceived borrowing at traditional banks as a time-consuming, complicated process, so they would avoid taking out small loans there. Some borrowers described experiences with long and complicated forms, extensive documentation, and probing personal questions about their lives that made them feel unfairly scrutinized despite a good payment history or steady income.

- Lack of clarity about the approval timeline and potential loan amounts made more reputable lenders less attractive than high-interest lenders. Going through the lengthy process of applying for a bank or credit union loan only to be denied or not get as much money as they needed made many residents hesitant to even try. Conversely, with high-interest payday loans, borrowers knew they would get the amount they needed quickly. The importance of transparency in eligibility and the application process is also supported by user testing with low- to moderate-income consumers conducted by ideas42.1

Confusion about Playing the Credit Game

- Paying off bills on time didn’t necessarily improve people’s credit, leaving them confused about the ideal time to pay their bills and how to obtain a higher credit score.

- With online lending apps, a few participants found they weren’t always able to prove to the lender that they were paying their other bills on time. Not having a bank account was a barrier to using some online apps.

- Those who had emigrated to the United States found it almost impossible to build their credit score or build for future financial security with or without an Individual Taxpayer Identification Number (ITIN). A few had successfully obtained car loans and credit cards after significant effort, but the dream of purchasing a home or sending their children to college felt less attainable due to their immigration status.

- Residents perceived that missing a loan payment even by a day or two can hurt credit quickly and puts borrowers in a vulnerable position if lenders contact their employers or family members. However, when they paid early or on time it did not seem to help their credit scores.

- Lenders may not drop old loans from borrowers’ credit reports after seven years. Some borrowers had to contact lenders to start that process.

“Immigrants are still going through the same situations. You ask for a loan, you have to meet certain requirements. You almost always do not qualify, and they give you a high interest rate. When there are no requirements, they ask you to have a good record or background. Even then, when they see how much you earn, they tell you no and they keep taking more and more money that you don’t have.” —Mariana, 33, Logan Square

High Fees and Unfair Practices

- Unlike other bills, customers often cannot choose on which day of the month loan payments are deducted. This can lead to missed payments and high fees that people cannot afford.

- Loans can end up costing much more than the amount needed through fees and high interest rates, particularly prior to the PLPA. Some residents said that a high interest rate for them would be above 10 percent. Additional fees weren’t always clear to residents either and were often hidden in the fine print of loan terms.

- Several people had liens put on their property or their cars repossessed without any warning. This was particularly galling when the value of the car was less than the loan.

Susan Montgomery/Shutterstock

Access Differs by Location, Work Type, and Race/Ethnicity

- Using zip codes to decide who gets a loan means that Black and communities of color may have less access to loans, regardless of actual income.2

- While some lenders offer loan applications in multiple languages, educational materials and customer service are not always translated.

- Discrimination was an issue in multiple ways. Some Black residents experienced discrimination when applying in person at a bank branch. Some immigrants who hadn’t yet become citizens felt they were poorly treated and that resources were reserved for citizens.

- Immigrants who hadn’t yet become citizens faced a number of challenges, both with and without an ITIN. An ITIN wasn’t always accepted by banks, credit cards, or mortgage companies. Even making regular payments and having a good credit score didn’t necessarily help them get a loan, especially if they were self-employed. Not being able to get a bank account makes it difficult to use banks or other lenders at all.

- Participants felt that loan advertisements can be predatory, whether online or in neighborhoods. Predatory online ads and social media posts were particularly attractive to young people.

- In Black and Latino communities, self-employment is common, either to supplement an income or as a main source of income. People can make considerable money in these jobs (for example, as a nanny or barber), but it can be difficult for them to prove their income because lenders want to see a W-2 form.

- People felt like they just couldn’t win. If they had a good income but were self-employed or had an account at an online bank, lenders said no. If they had a steady payment history but not enough income, they were denied. If they did receive a loan, they felt they would have to pay a much higher interest rate than others.

“I think when it comes to income, they don’t have a lot of options for self-employment. They want [a] W-2. Some people make a lot of money doing hair, etc. and have the receipts to prove it, but if they don’t have a W-2 then they don’t give them a loan.” —Tiffany, 38, East Chatham

Citations

- Vivien Caetano, Dan Rosica, Tahan Menon, Evelyn Stark, and Manasee Desai, Increasing Applications for Small Dollar Loans: A Behavioral Design Guide for Financial Providers (New York: ideas42, July 2023), source.

- For more information about geographical distribution of credit scores see Taz George, Robin Newberger, and Mark O’Dell, “The Geography of Subprime Credit,” ProfitWise News and Views 6 (2019), source.

Insights for Better Loan Offerings

During the last two design sessions, participants spent time writing down and then talking about where they would go first to find money for one of two scenarios. This allowed people to first share their thoughts with us, without external influence, and then to work through different options as a group. The two scenarios were:

- Scenario A: A big bill is always due one week before your paycheck. You need $200–$250 every month, knowing you will be able to pay it off soon.

- Scenario B: An unexpected emergency costs you $1,000–$2,000 and you will need to pay it off over time.

In the first session, people also discussed where they had learned about loans in the past and designed their own loans for similar scenarios. These discussions showed us who borrowers trust for loan information, who is considered a trusted lender, and what loan features may be most appealing.

Meegan Dugan Adell/New America

Trusted Messengers and Lenders

With many payday and auto title lenders closing their brick-and-mortar locations in Illinois because they are unwilling to abide by the PLPA’s 36 percent APR cap, it is more important than ever for households to be steered toward safe, affordable lending alternatives. However, it can be difficult for consumers, particularly those from Black or other communities of color, to trust financial institutions that have been discriminatory in the past. We wanted to better understand where consumers go for information they can trust about small dollar loans. With a better understanding of what sources they trust, resources and financial information can be more effectively shared with these consumers. The points below outline issues and differences that lenders serving these communities should be aware of.

Lack of Trust in Financial Institutions

Several people in our groups mentioned that many in their communities feel safer keeping their money at home than in banks. This was particularly true among the Latina participants in our Logan Square design session. There was also significant fear in that community around taking out a loan and being trapped in a cycle of debt. Among Black participants in our groups, several mentioned a distrust of both banks and online apps. Several felt they are likely to be taken advantage of and that they lack power in the relationship. Some didn’t like the fact that lenders can sell their information to other companies. Participants in general were also worried about the risk of giving an app or lender direct access to their accounts, as they may not be able to manage when different payments are deducted. Others were concerned about or had experienced fraud on online apps, including scams that clean out a person’s bank account. Across races, multiple participants felt frustrated that lenders held borrowers accountable for their part of the original agreement but can change interest rates or make other changes that borrowers might not have agreed to.

Lack of Common Trusted Messengers

Residents didn’t identify one common source of trusted information about borrowing. People from all neighborhoods seemed to be unsure about where to go, particularly for higher amounts, and had a variety of different trusted messengers. Most residents said that family members, friends, credit unions, and online resources like Google searches, Credit Karma, Trustpilot, and the Better Business Bureau are the best way to learn about a loan or check out a lender. A handful of people trusted the banks they had accounts with. Several people said they would trust a local nonprofit if it offered help. A few people mentioned low- or no-interest options from their employers. At the end of each session, multiple people asked the facilitators if there was some trustworthy place where they could find information.

Differences between Generations

Respondents indicated that different generations seemed to trust different types of messengers, with younger people using social media sources such as Instagram, Reddit, TikTok, YouTube, or X (formerly Twitter). Middle-aged people mentioned relying on Google searches; websites like Credit Karma, NerdWallet, or WalletHub; Facebook groups and other social media; or online reviews of companies. Much older people trusted television shows or news programs, such as Univision in the Latino community. Some participants were worried that young people might be getting bad information on social media, while several Latina participants were impressed by how helpful these sources had been for teaching their teen or young adult children about money management.

Cultural Differences for Larger Loans

For larger expenses, like an emergency requiring $2,000, talking to family and friends was the first choice, with some variation. People in the Latino community expressed a strong cultural aversion to taking loans from financial institutions and strongly preferred to ask family and friends. Most didn’t even suggest taking out a loan as an option and would rather sell or possibly pawn something if they couldn’t receive help from family or friends. People in the third group of primarily Black residents considered a variety of options but were slightly more likely to mention taking out an online or loan-store loan as an option. Asking family or friends was a close second. Gig work was a popular choice as well. Only one person mentioned using a credit card.

Preference for Asking Family and Friends for Small Loans

For a smaller loan, like for a bill that comes before payday, there was not one common answer across groups, although asking family and friends was one of the most common answers. This was slightly more popular with people in the predominantly Black South Side design session. For people in the entirely Latina Northwest Side session, the answers varied more, including online loan options, saving money, and asking for an extension, in addition to support from family and friends.

Confusion about Credit Unions

In our two design sessions hosted within Black and Latino communities, several people seemed to be confused about how credit unions work, whether they qualified to use a credit union, or whether they had to be employed in a specific place to use one. Just a few people in each group had had a good experience taking out car, home, or other loans with credit unions, but they spoke of them in glowing terms, which interested others in the option. Our first group, recruited from multiple neighborhoods, seemed to be more familiar with and trusting of credit unions.

“Even nowadays, some people still don’t trust banks. Banks are not very friendly towards people with ITINs. It took me years to build credit, for example.” —Michelle, 44, Logan Square

“The best way [to find out about a loan] is a family member or friend. They’ve already gone through the experience, and they can help guide you.” —James, age unknown, South Chicago

Desirable Loan Features

Some literature has shown that even with the closure of payday loan stores, people still do not tend to switch to more traditional credit instruments like credit cards or small personal loans from banks, finance companies, and retail stores.1 Additionally, it has been found that most current payday borrowers prefer higher-priced but less restrictive standard payday loans over lower-priced but more restrictive alternatives offered by institutions like credit unions.2 Only a handful of participants in each design session thought of banks or credit unions as a source for short-term, small dollar loans, so understanding what residents were looking for could help these institutions better meet community lending needs in their service areas. The following are some of the features in small dollar loans that consumers in our groups were looking for but perceived were not available in existing products.

Clear, Simple Process with a Rapid Turnaround

Participants had made calculated choices to take on higher APR loans in part because they knew how much they would receive and that they would receive the loan within one-to-two business days. Consistent with other research, we know that loans with clear processes—just a handful of steps, quick turnaround, and simple parameters that determine who is eligible for how much money—are crucial for consumers, especially in times of emergency.3

Options for Eligibility

Across all of our groups, having different ways of getting approved for loans was important. Some had good payment history or income but were self-employed, had poor credit, or had an online bank account that wasn’t part of the data transfer network used by many banks. Many participants felt that loans should be granted based on pay history or proof of income rather than credit score.

Options for Online Access

Having an online application and multiple online options (for example, an easy-to-use website or app) was a must-have for most people. However, there were limitations. Many people were concerned about online fraud and identity theft, so some weren’t open to loans from apps rather than a brick-and-mortar location they could visit in case there was an issue. Many people were also concerned about giving online apps full access to their checking accounts.

Ability to Manage Monthly Costs

People want more flexibility with loan payments, dates, and options for how many payments are expected per month.

Credit and Wealth-Building Features

Many participants would welcome elements that help build their financial security and wealth, although this doesn’t surpass ease of use on the wish list. Consumers wanted rewards for early repayment and credit-building features, and they appreciated wealth-building features like earning shares in the lending institution.

Just-in-Time Financial Coaching

Financial literacy coaching to answer questions when they arise, as well as individualized support throughout the loan process, would help borrowers know about the options available to them and the best path toward financial security. This is consistent with substantial research that suggests that financial literacy education has a limited impact on behavior, in part because people don’t retain the information as early as six months later.4

“I lost a car going through a title loan. They didn’t call me or tell me anything; $300 for a $10,000 car. I lost it. This was not too long ago. It’s ridiculous, the sacrifices people make.” —Barbara, 56, Belmont Cragin

Designing Simple Loans

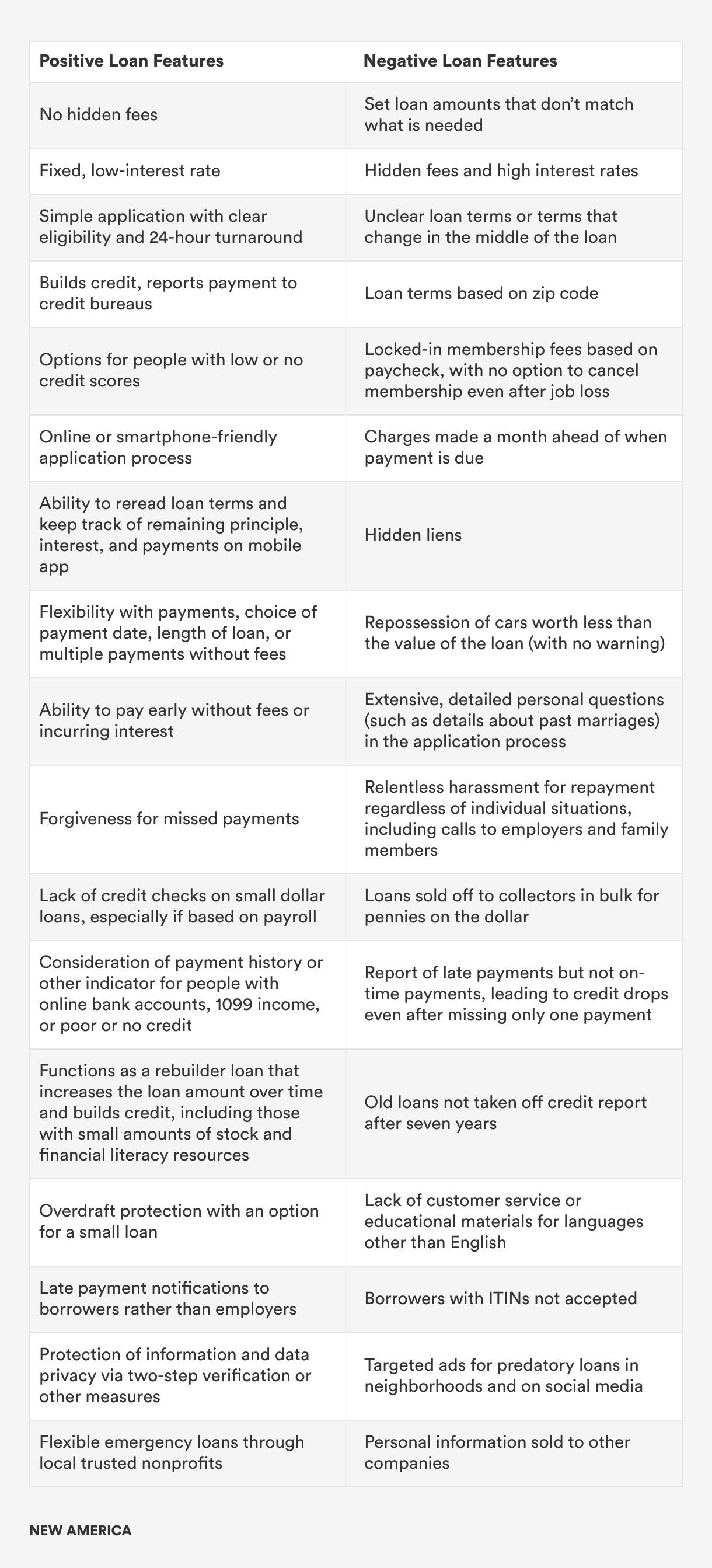

During our group activities, participants contributed to a list of the best and worst loan features from their experiences borrowing or needing small dollar loans.

At the end of the first event, participants were asked to design their own ideal loan and vote on each other’s designs to uncover the most popular features. Participants were split into two groups: one group designed a $200 loan that a borrower would need consistently each month, and the other group designed a $1,000 loan for a one-time emergency. From the lists of features they generated, participants picked two “positive” features and one “negative” feature to form a loan that would be useful to them and identify trade-offs they were willing to make.

The most popular loan for consistent access to a smaller sum included one that had no credit check and a low interest rate with no increase if it is paid on time, with the downside that borrowers get approved through their current debt status rather than their paycheck. For the $1,000 one-time infusion loan, the most popular loan was one that had no fees and helps borrowers build or rebuild their credit, with the downside of harassment for late payments. Residents defined harassment for late payments as incessant phone calls and email reminders about payment status.

The least popular loan option for consistently borrowing a smaller sum offered forgiveness for a missed payment and no fees, but also included a membership that borrowers were not able to opt out of even if they no longer needed the loan option. For the larger emergency loan amount, the least popular featured design was a loan that had a flexible payment plan with an accessible mobile app but offered no customer service.

Vanessa Rangel/New America

Consumer Responses to Currently Available Loans

Updated at 2:19 p.m. on April 3, 2024: This section has been changed to clarify the use of the term “credit union” as it pertains to the research methodology. The term was also removed from both tables.

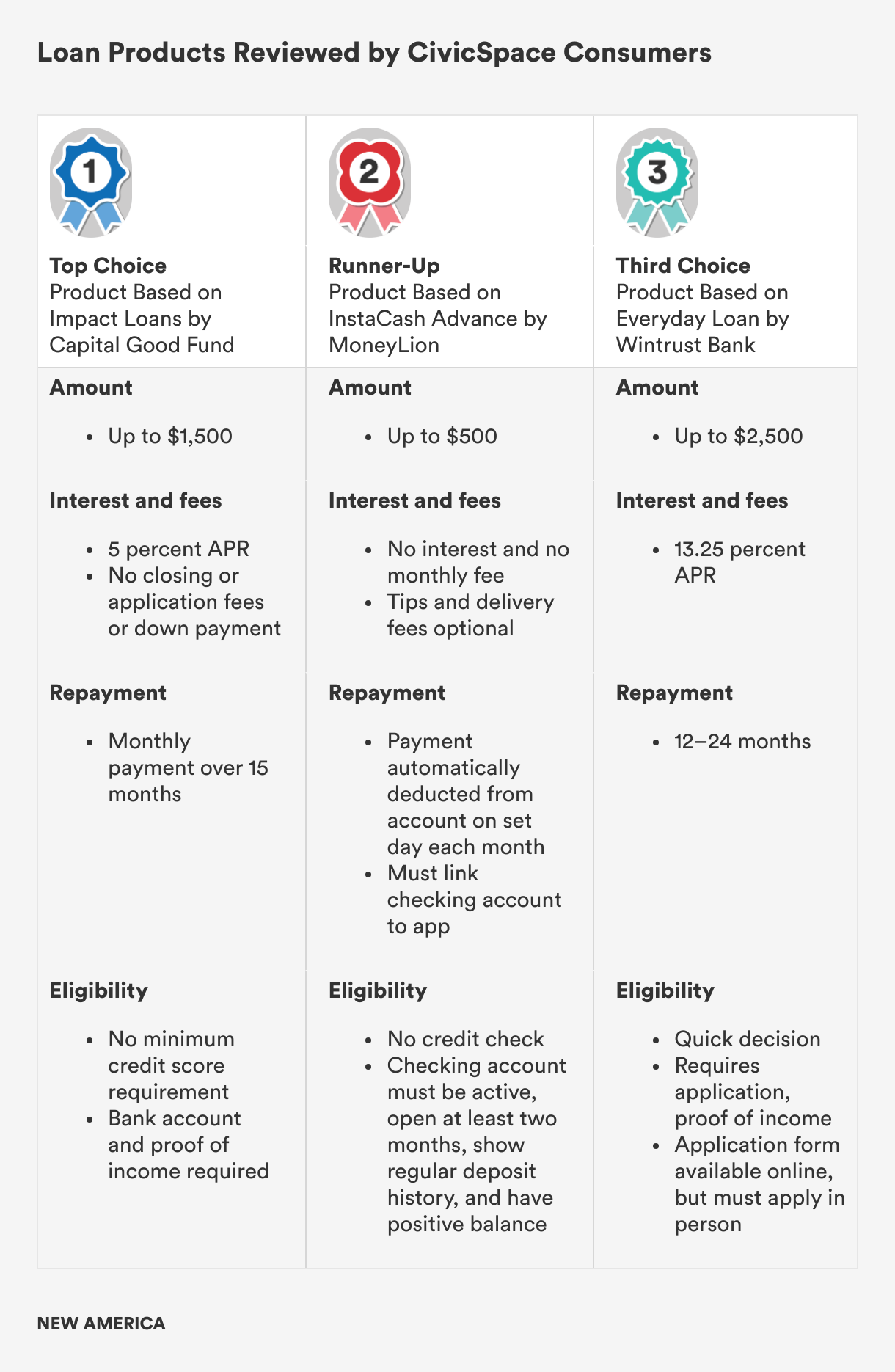

In the last two groups, we again split participants into two scenarios and asked them to respond to three real loan products with the two scenarios in mind: a regular $250 loan for an ill-timed bill or a one-time emergency loan of $2,000. We increased the loan amounts for each scenario in the last two design sessions to reflect the higher cost of living in 2023. We also concealed the sources of these loan products and only shared a description of the products and key features.

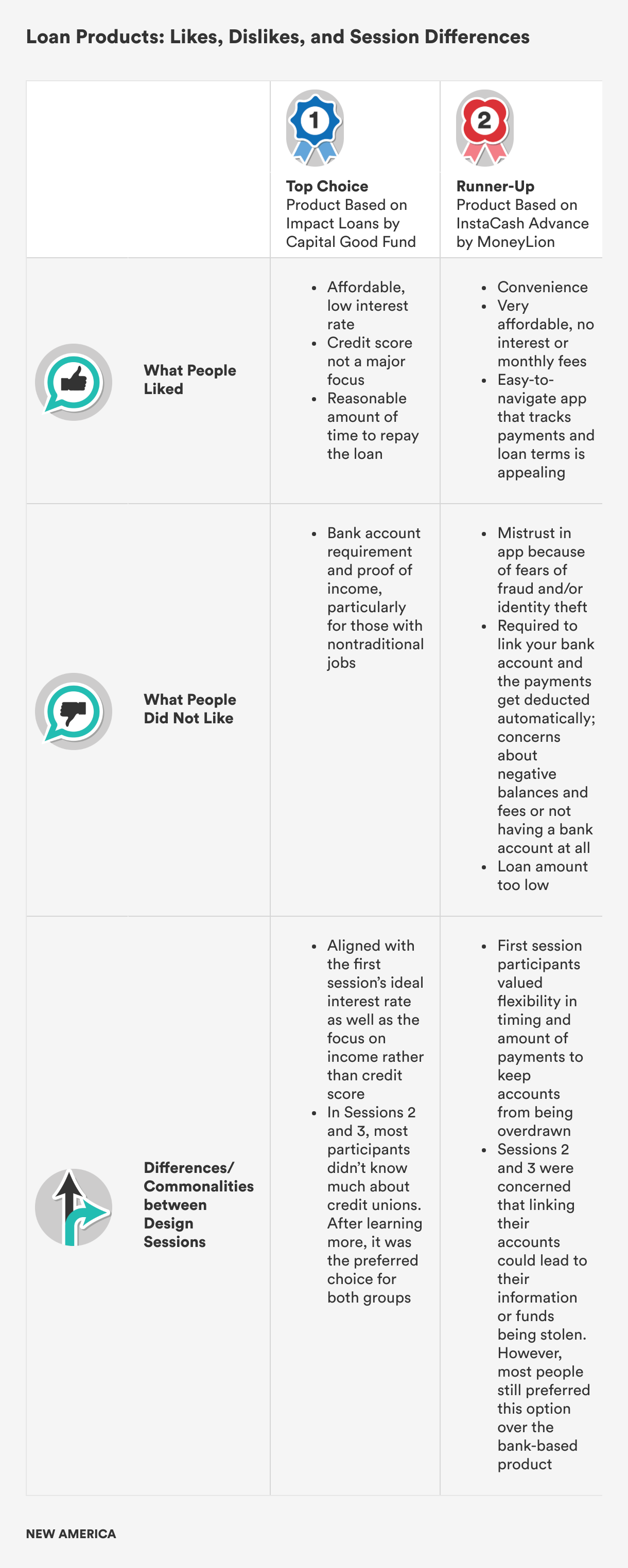

The credit union loan was the most popular choice for both scenarios. (Note: Capital Good Fund is a community development financial institution. However, in order to understand people’s reactions to online, credit union, and bank products, we left out the lender names and used the word credit union to describe this product.) In both groups, once residents learned more about how credit unions worked from their peers, the credit union loan product was the top choice due to its fair and affordable loan terms.

The least favorite loan product among the two groups was the bank branch product. Many participants from the predominantly Latina and Black groups were concerned about whether they would even be approved for a traditional bank loan and felt that it would be a waste of their time to apply in person. They assumed there would be requirements for eligibility that are not listed and that they likely would not meet. Both groups also thought the 13.25 percent interest rate was high compared to the other products and questioned how quick the approval process would actually be.

The online app-based loan fell in the middle. Some participants loved the idea; others hated it, especially those who had had experiences with identity theft. Participants really appreciated the convenience and affordability of the product, but it was difficult for most to overcome the fact that it was a completely online product not attached to a physical institution and that the loan was directly linked to a personal checking account. It gave the lender too much power over their finances without enough online security to reassure participants that their checking accounts were protected. The risk did not feel worth the $500 loan amount; however, this design shows promise, particularly if the security concerns are addressed.

Citations

- For example, see Neil Bhutta, Jacob Goldin, and Tatiana Homonoff, “Consumer Borrowing after Payday Loan Bans,” Journal of Law and Economics 59, no. 1 (February 2016): 225–59, source.

- See Victor Stango, “Some New Evidence on Competition in Payday Lending Markets,” Contemporary Economic Policy 30, no. 2 (April 2012): 149–61, source.

- See Caetano et al., Increasing Applications for Small Dollar Loans, source.

- For example, see Daniel Fernandes, John G. Lynch, and Richard G. Netemeyer, “Financial Literacy, Financial Education, and Downstream Financial Behaviors,” Management Science 60, no. 8 (August 2014): 1861–83, source.

Implications for Lending Practices and Policy

Around two-thirds of short-term borrowers seek to cover bills that come before payday or simply earn too little to cover basic household expenses, with around one-third of borrowers taking out loans for an unexpected expense.1 Having a lower-cost alternative to high interest loans can keep these households from losing their bank accounts or having their electricity shut off. Addressing this issue is important for lower-income households in Cook County, as well as the 39 percent of Black households and 32 percent of Latino households in Cook County without a savings account.2

Most people have an aversion to high-interest debt regardless of income, numeracy, or financial literacy.3 People choose high-interest debt most likely because they know they can get approved quickly when they don’t know where else to go, don’t have a clear sense of how it compares to other types of debt, underestimate payments needed to get out of debt, or overestimate their ability to pay the debt off in the future.4 Nearly half of payday loan borrowers in one large-scale study couldn’t remember their APR and most thought the dollar cost for one month was the dollar cost for three months of borrowing.5

Ensuring that there are clear, affordable alternatives that improve financial health over time can help build a virtuous cycle of economic growth across the region. We believe our findings, combined with broader research around borrowing behavior, can help lenders and policymakers design better products and public policy around the rules of play in consumer lending.

“I’m a former banker. I hated having to turn away people.…I think we need to talk about different products for people with different backgrounds and income so that they have an option. Where is the product for those people?” —Ashley, age unknown, Woodlawn

Beneficial Community Lending Practices

Banks, community development financial institutions (CDFIs), credit unions, financial technology (fintech) firms, and local nonprofits could keep customers longer, increase uptake of new products among existing customers, and open new markets by offering alternatives to predatory loans in low- and moderate-income communities. This could simultaneously be incredibly useful for building financial health in these communities. Unfortunately, many times these products aren’t well marketed or have complicated applications and slow and opaque approval processes. The following practices can ensure products are both attractive to customers and build economic stability in underserved communities.

Clear, Simple Loan Eligibility and Quick Processes

Both our research and that of others has shown that people consistently choose more expensive loan products because they know they qualify and will receive the money within a day or two. People will not choose lower-cost alternatives unless it is crystal clear that they compare favorably with the products they are accustomed to using, especially in communities that do not trust traditional financial institutions. Clearly stating, in simple terms, who is eligible; providing a short, simple application process; and creating a one-to-two-day turnaround will help replace high-interest loans with better alternatives.6

Tech-Enabled Alternatives to Credit Checks

Merchant websites have a number of ways of assessing risk for payment plans that do not involve credit checks. Offering alternatives to credit checks can make low-interest loans more accessible to Black and Latino communities where avoidance of taking on credit is common, credit scores tend to be lower,7 and affordable financing can be harder to find.

Just-in-Time Financial Education

Most people do not understand compound interest well, have anxiety about math that hinders computation, and overestimate their ability to pay back debt, so building knowledge about how debt can be used responsibly could be hugely beneficial.8 Because most people quickly forget what they have learned about finance, financial education programs have shown almost no impact on behavior.9 Bite-sized financial lessons and coaching at times of decision can help. For example, giving people quick summaries of good versus bad debt when they are making financial decisions has been shown to help them make better financial choices.10

Choices Shown in Real Dollars and APR

Multiple studies have found that people routinely take out higher-interest loans when cheaper credit is available.11 When thousands of payday borrowers were shown the cost in dollars of their loan over two weeks, one month, two months, and three months compared to the same costs using a credit card, the amount borrowed went down by 24 percent and future borrowing went down by 11 percent.12

Default Choice Architecture Used for Good

People are likely to take the default option offered to them, even if it is more expensive.13 Socially conscious lenders can flip this on its head to make the default option the choice that is most optimal for the customer’s financial health. This could include automatic enrollment and small deposits in a savings or simple investment account.14 Smart defaults based on customer attributes or adaptive defaults based on previous consumer choices can help make sure this approach meets consumer needs.15

Repayment Time Improved

Breaking debt down into smaller amounts for specific items leads people to allocate 19 percent more money to repayment, and starting with the smallest debt first can make people more likely to follow through on debt pay-down plans.16 Including this element in lending apps, online account interfaces, or bills could help improve consumer credit usage and repayment.

Temporal Framing to Increase Savings

Pairing small, low-interest loans with an automatic savings or investment program that shows the contribution in daily or weekly payments is more likely to increase uptake, using the pennies on the dollar principle.17 A nonprofit loan program could put a portion of the interest payment in a savings account, for example, rather than simply giving out a savings planner, which is less likely to work.18

Loans that Improve Credit with Regular Repayment

Offering small dollar credit-builder loans that report on-time payments to credit bureaus can be helpful for underserved communities. Nonprofits or credit unions can also use choice architecture to offer two or three clear repayment options, with the one that is financially best for the consumer selected as the default.19

Overdraft Fees Replaced with Small, Short-Term Loans

While overdraft fees can be very lucrative, banks and credit unions can close fewer accounts and hold onto customers longer by offering an alternative.20 Creating a regular, low-interest line of credit under $250 for account holders that is available until payday, and that can be automatically approved based on customer payment and deposit history, could help build customers’ financial health.21 Since people make more shortsighted choices when money is tight, reminding people right after payday to take action to avoid a pattern of shortfalls may improve financial stability.22

Policy Considerations

Solve for Multiple Problems

Any policy solution that eliminates high-interest loans but doesn’t help people make ends meet is a partial solution. Incentivizing banks, credit unions, fintech, and nonprofits to provide low-cost help for regular expenses that come before payday and for financial emergencies is essential to improving financial health in low- to moderate-income neighborhoods. Only providing financial education when people simply don’t make enough money has limited impact.

Enact Federal Caps and Guidance

Having a patchwork of banking regulations in 50 states makes it harder to protect consumers, leaves them vulnerable to gouging, and makes it difficult to enforce safe lending policy in the Wild West of online and nonbank lending. The federal government should enact a cap of 36 percent APR on lending and enforce the cap across the board. This includes regulating interest rates and fees for pawnshops and other high-interest lenders that people may turn to when payday loans aren’t available.23

Require Honest Lending

Federal regulations should require a standard, simple table of actual borrowing costs for all loans across the country. Use lessons learned from the 2009 Credit Card Accountability Responsibility and Disclosure Act to improve immediate consumer information, in simple language, about payments and the total cost of paying off loans over time compared to other types of credit.24 The language should clearly describe how costs increase if the borrower borrows more or rolls over a loan.

Expand Programs to Meet the Size of the Problem

Programs such as the CDFI Fund Small Dollar Loan Program are important, but the annual funding in Illinois alone represents a tiny fraction of the small dollar loan market and most CDFIs focus on other types of loans.25 While credit unions and other CDFIs are an essential resource, credit unions are greatly limited in scope and the number of total CDFI awards each year is dwarfed by the size of the need. Not only is additional funding necessary, but creative solutions that leverage different sources of capital are also sorely needed. Creating new funding sources that allow for collaboration among nonprofits, CDFIs, credit unions, fintech, employers, and state agencies could make a difference. Expand funding for community-based solutions similar to Capital Good Fund, the Kansas Loan Pool Project, Ko’olau Federal Credit Union, Common Wealth Charlotte, Common Wealth Athens, and the UPI Loan Fund.26

Create Incentives for Financial Institutions

Using tax policy and the Community Reinvestment Act to incentivize financial institutions to provide affordable, short-term capital in low-income neighborhoods with limited banking options could also increase financial stability.

Regulate and Harness Fintech

Fintech and online banking have the potential to improve banking access and solve problems mainstream banks do not, but they also have great capacity for harm. It can be incredibly difficult to enforce state caps on interest rates and other laws with the explosion of online financial services. The federal government must enact clear guidelines and require a federal registry and common data reporting for online lending.27 Regulation of online financial services should be approached in a way that allows for creative solutions to old problems.

Make Artificial Intelligence a Force for Good

Artificial intelligence (AI) could be a powerful tool for educating consumers, if regulated well. With the right protections in place, generative AI that only draws from confirmed, accurate sources could provide consumers with useful, just-in-time financial advice.28 However, there is just as much, if not more, capacity for spreading inaccurate or predatory information, so this requires well-informed, well-reasoned regulation at the federal level.

Integrate Financial Health Concepts into Government Programs

The government could integrate elements into safety net programs to help build healthier financial practices. For example, increasing savings and investment account amounts allowed for benefits recipients and integrating just-in-time financial education into current activities could both help if framed in appealing language. Individuals receiving government benefits like food stamps (SNAP) or the Special Supplemental Nutrition Program for Women, Infants, and Children (WIC) could receive a small automatic matching deposit in a savings account, since people are more likely to save when it is automated.29 Since people tend to overspend what they see as windfall, reframing tax refunds and connecting them to recurring, semi-regular expenses people may overlook could help build financial stability. Combining government messages about savings with messages about the relative cost of low-interest savings versus paying off high-interest debt when people receive funds could also help build healthier habits.30

Recognize that Lending Policy Doesn’t Exist in a Vacuum

Policymakers can help reduce reliance on high-interest lending products by enacting policies that alleviate financial pressure on families. For example, expansions in Medicaid have been directly linked to reductions in high-interest loan uptake.31 Reinstating the expanded monthly Child Tax Credit or policies that improve access to well-paying jobs can reduce the need for loans.

New America

Citations

- For more, see Nicholas Bianchi and Rob Levy, Know Your Borrower: Four Need Cases of Small-Dollar Consumers (Chicago, IL: Center for Financial Services Innovation, December 2013), source.

- Celik, Greene, Chege, and Fontes, Financial Health Pulse 2022 Chicago Report, source.

- Adam Eric Greenberg, Abigail B. Sussman, and Hal E. Hershfield, “Financial Product Sensitivity Predicts Financial Health,” Journal of Behavioral Decision Making 33, no. 1 (January 2020): 15–26, source.

- Fernandes, Lynch, and Netemeyer, “Financial Literacy, Financial Education, and Downstream Financial Behaviors,” source; Marianne Bertrand and Adair Morse, “Information Disclosure, Cognitive Biases, and Payday Borrowing,” The Journal of Finance 66, no. 6 (December 2011): 1865–93, source; Jack B. Soll, Ralph L. Keeney, and Richard P. Larrick, “Consumer Misunderstanding of Credit Card Use, Payments, and Debt: Causes and Solutions,” Journal of Public Policy & Marketing 32, no. 1 (April 2013): 66–81, source; Hal E. Hershfield, Abigail B. Sussman, Rourke L. O’Brien, and Christopher J. Bryan, “Leveraging Psychological Insights to Encourage the Responsible Use of Consumer Debt,” Perspectives on Psychological Science 10, no. 6 (November 2015): 749–52, source; and Adam Eric Greenberg and Hal E. Hershfield, “Financial Decision Making,” Consumer Psychology Review 2, no. 1 (2019): 17–29, source.

- Bertrand and Morse, “Information Disclosure, Cognitive Biases, and Payday Borrowing,” source.

- For useful details about how to restructure processes and instructions for loans see Caetano et al., Increasing Applications for Small Dollar Loans, source.

- George, Newberger, and O’Dell, “The Geography of Subprime Credit,” source.

- Greenberg and Hershfield, “Financial Decision Making,” source; and Greenberg, Sussman, and Hershfield, “Financial Product Sensitivity Predicts Financial Health,” source.

- For example, see Fernandes, Lynch, and Netemeyer, “Financial Literacy, Financial Education, and Downstream Financial Behaviors,” source.

- Greenberg, Sussman, and Hershfield, “Financial Product Sensitivity Predicts Financial Health,” source.

- Bhutta, Goldin, and Homonoff, “Consumer Borrowing after Payday Loan Bans,” source; Sumit Agarwal, Souphala Chomsisengphet, and Cheryl Lim, “What Shapes Consumer Choice and Financial Products? A Review,” Annual Review of Financial Economics 9, no. 1 (November 1, 2017): 127–46, source.

- Bertrand and Morse, “Information Disclosure, Cognitive Biases, and Payday Borrowing,” source.

- N. Craig Smith, Daniel G. Goldstein, and Eric J. Johnson, “Smart Defaults: From Hidden Persuaders to Adaptive Helpers,” SSRN Electronic Journal (2008): source.

- Philip Fernbach and Abigail Sussman, “Teaching People about Money Doesn’t Seem to Make Them Any Smarter about Money—Here’s What Might,” MarketWatch, October 27, 2018, source.

- Smith, Goldstein, and Johnson, “Smart Defaults: From Hidden Persuaders to Adaptive Helpers,” source.

- Keri L. Kettle, Remi Trudel, Simon J. Blanchard, and Gerald Häubl, “Repayment Concentration and Consumer Motivation to Get Out of Debt,” Journal of Consumer Research 43, no. 3 (October 2016): 460–77, source; and Alexander L. Brown and Joanna N. Lahey, “Small Victories: Creating Intrinsic Motivation in Task Completion and Debt Repayment,” Journal of Marketing Research 52, no. 6 (December 2015): 768–83, source.

- Hal E. Hershfield, Stephen Shu, and Shlomo Benartzi, “Temporal Reframing and Participation in a Savings Program: A Field Experiment,” Marketing Science 39, no. 6 (November 2020): 1039–51, source; and Greenberg and Hershfield, “Financial Decision Making,” source.

- Bertrand and Morse, “Information Disclosure, Cognitive Biases, and Payday Borrowing,” source.

- Hershfield, Sussman, O’Brien, and Bryan, “Leveraging Psychological Insights to Encourage the Responsible Use of Consumer Debt,” source.

- Consumer Financial Protection Bureau, “CFPB Research Shows Banks’ Deep Dependence on Overdraft Fees,” press release, December 1, 2021, source.

- Patrick L. Hayes, “A Noose around the Neck: Preventing Abusive Payday Lending Practices and Promoting Lower Cost Alternatives,” William Mitchell Law Review 35, no. 3 (2009): 1134, source.

- Greenberg and Hershfield, “Financial Decision Making,” source.

- Bhutta, Goldin, and Homonoff, “Consumer Borrowing after Payday Loan Bans,” source.

- Greenberg and Hershfield, “Financial Decision Making,” source; Agarwal, Chomsisengphet, and Lim, “What Shapes Consumer Choice and Financial Products?” source; and Soll, Keeney, and Larrick, “Consumer Misunderstanding of Credit Card Use,” source.

- CDFI Annual Certification and Data Collection Report (ACR): A Snapshot for Fiscal Year 2020 (Washington, DC: U.S. Department of the Treasury, October 2021), source.

- M. A. Caplan, “Communities Respond to Predatory Lending,” Social Work 59, no. 2 (April 1, 2014): 149–56, source; UPI Loan Fund, “New Arizona Nonprofit Offers Low-to-No Interest Loans for Qualified Individuals,” press release, PRWeb, October 20, 2020, source; and Sheila Bair, Low-Cost Payday Loans: Opportunities and Obstacles (Baltimore, MD: Annie E. Casey Foundation, June 2005), source.

- Jessica Silver-Greenberg, “Major Banks Aid in Payday Loans Banned by States,” New York Times, February 23, 2013, source.

- Abigail Sussman, Hal Hershfield, and Oded Netzer, “Consumer Financial Decision Making: Where We’ve Been and Where We’re Going,” Journal of the Association for Consumer Research 8, no. 4 (October 2023), source.

- Agarwal, Chomsisengphet, and Lim, “What Shapes Consumer Choice and Financial Products?” source.

- Hershfield, Sussman, O’Brien, and Bryan, “Leveraging Psychological Insights to Encourage the Responsible Use of Consumer Debt,” source.

- Heidi Allen, Ashley Swanson, Jialan Wang, and Tal Gross, “Early Medicaid Expansion Associated with Reduced Payday Borrowing in California,” Health Affairs 36, no. 10 (October 2017): 1769–76, source.

Conclusion

At the start of each of our community sessions, residents gave a few reasons why they were interested in helping design better small dollar loans. All of them felt impacted by their experiences accessing loans. Some had more positive experiences than others, but regardless of whether accessing a loan helped or hurt them, they saw the need for better financial resources in their communities. They said that the cost of living was getting harder to afford, that financial literacy isn’t taught well in schools, and that people old and young were struggling to pay off bills. Gaps in information and access to safe alternative lending products prevented many residents from getting the resources they want and need to create financial stability for themselves and their families. These 32 residents spent their evening codesigning loans and solutions in the hope that policymakers and lenders will take their advice and create or amend programs and products to serve people like them. Additional testing with hundreds or thousands of clients would be an ideal next step to explore the potential impact of these concepts. With more affordable, timely, and flexible options; better financial education systems; and more inclusive loans geared toward credit building, socially conscious lenders can offer better options that serve Chicago residents and people all over the country, ultimately creating opportunities for residents to thrive.

“With the times that we are in, life is a whirlwind. When everything shut down [due to the pandemic], I feel like people need more options. Now that things are settling down, I think it’s something we need to talk about.” —Raymond, 52, Woodlawn

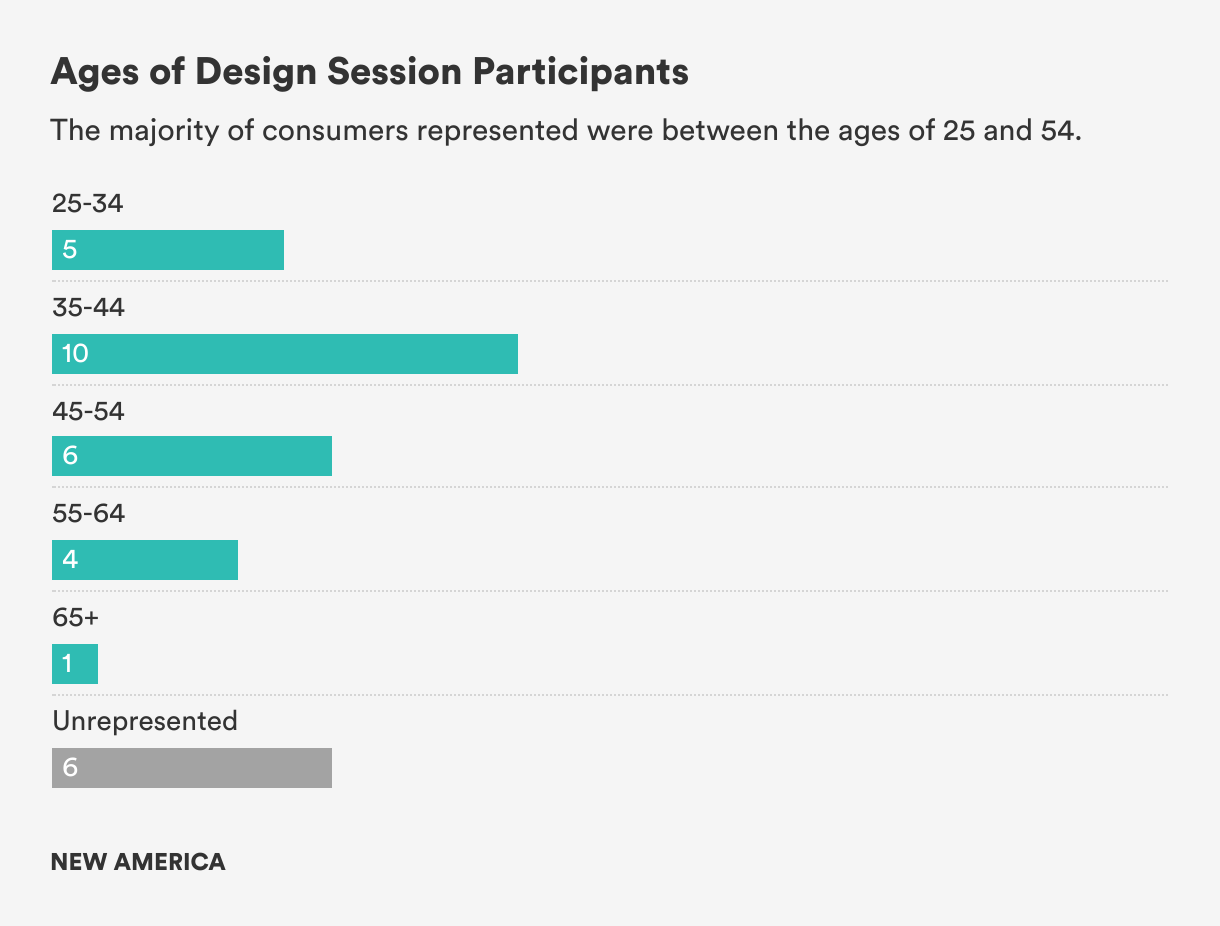

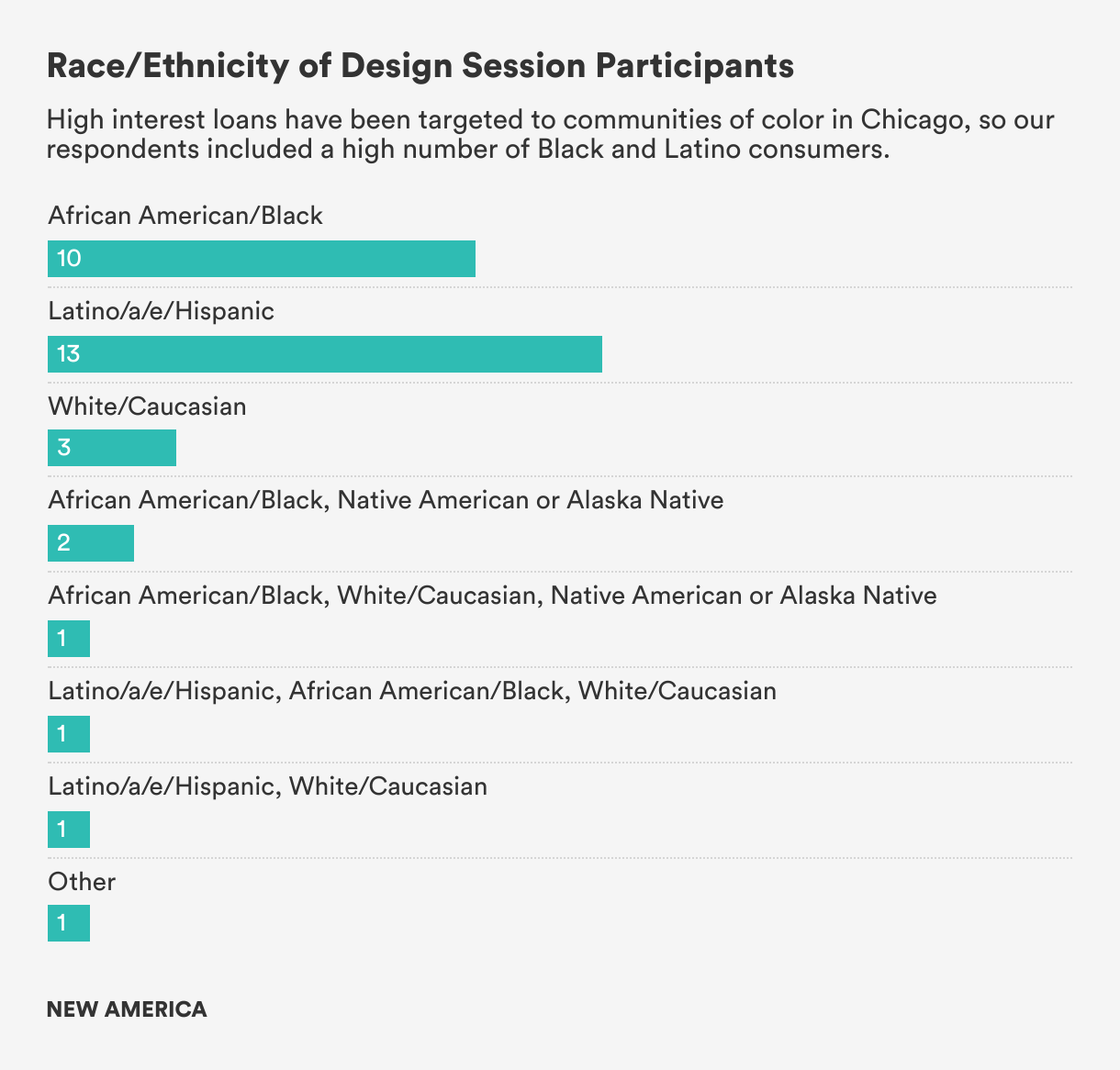

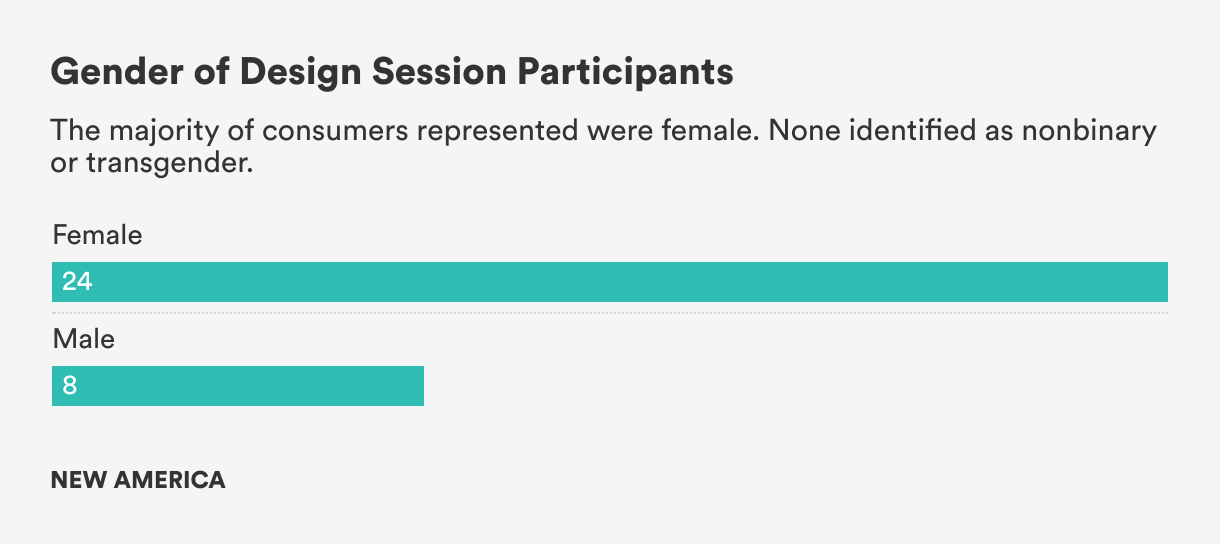

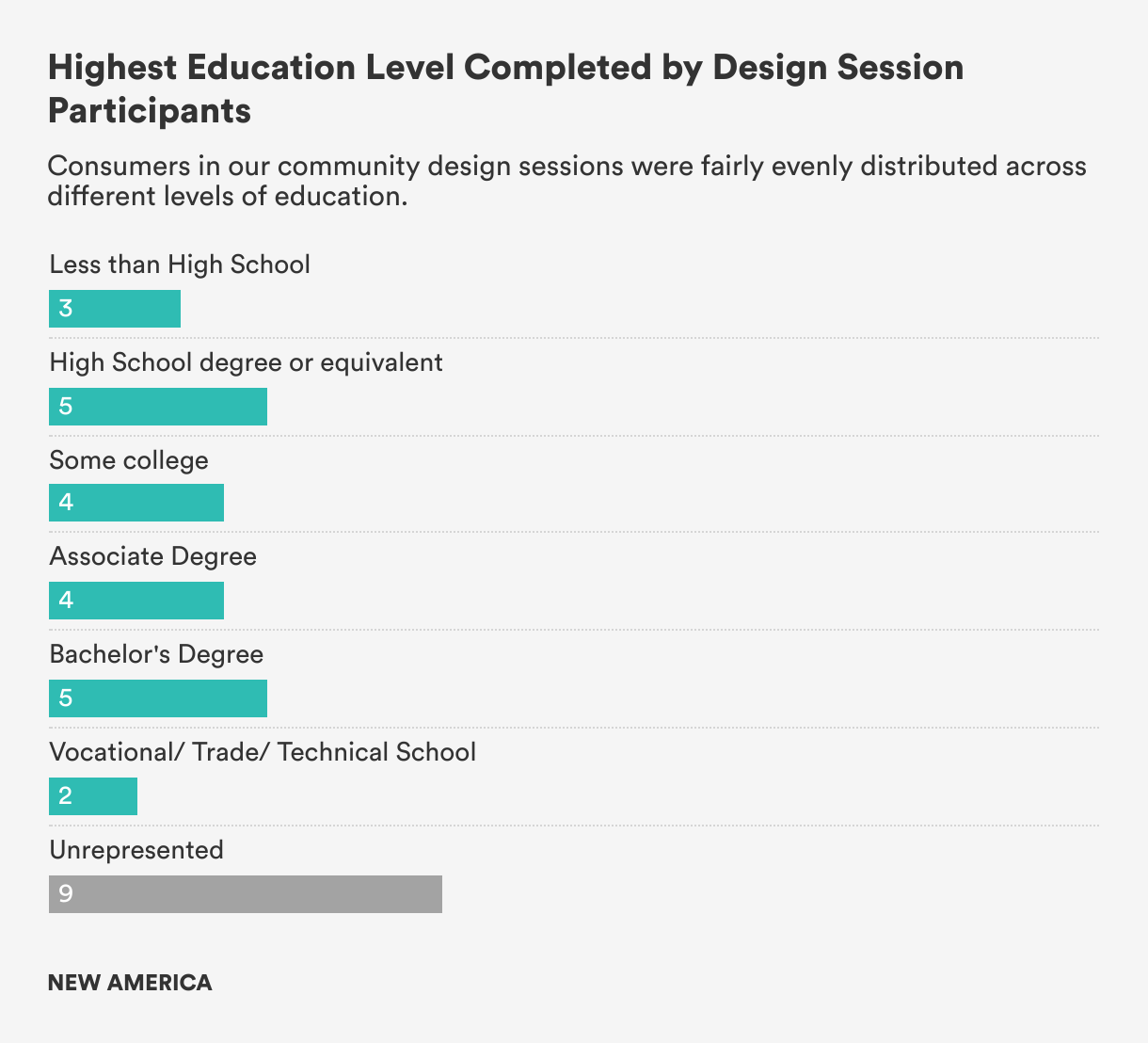

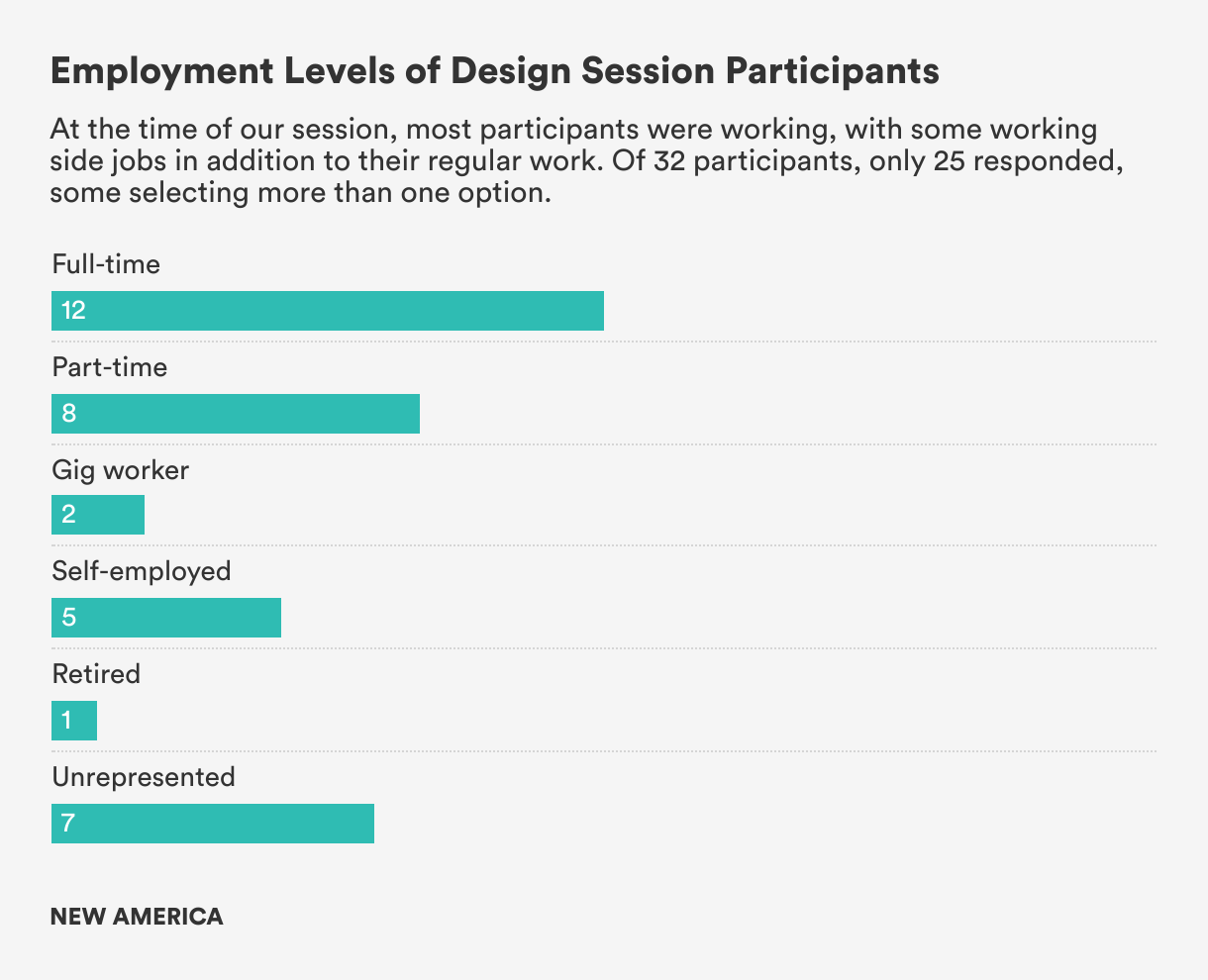

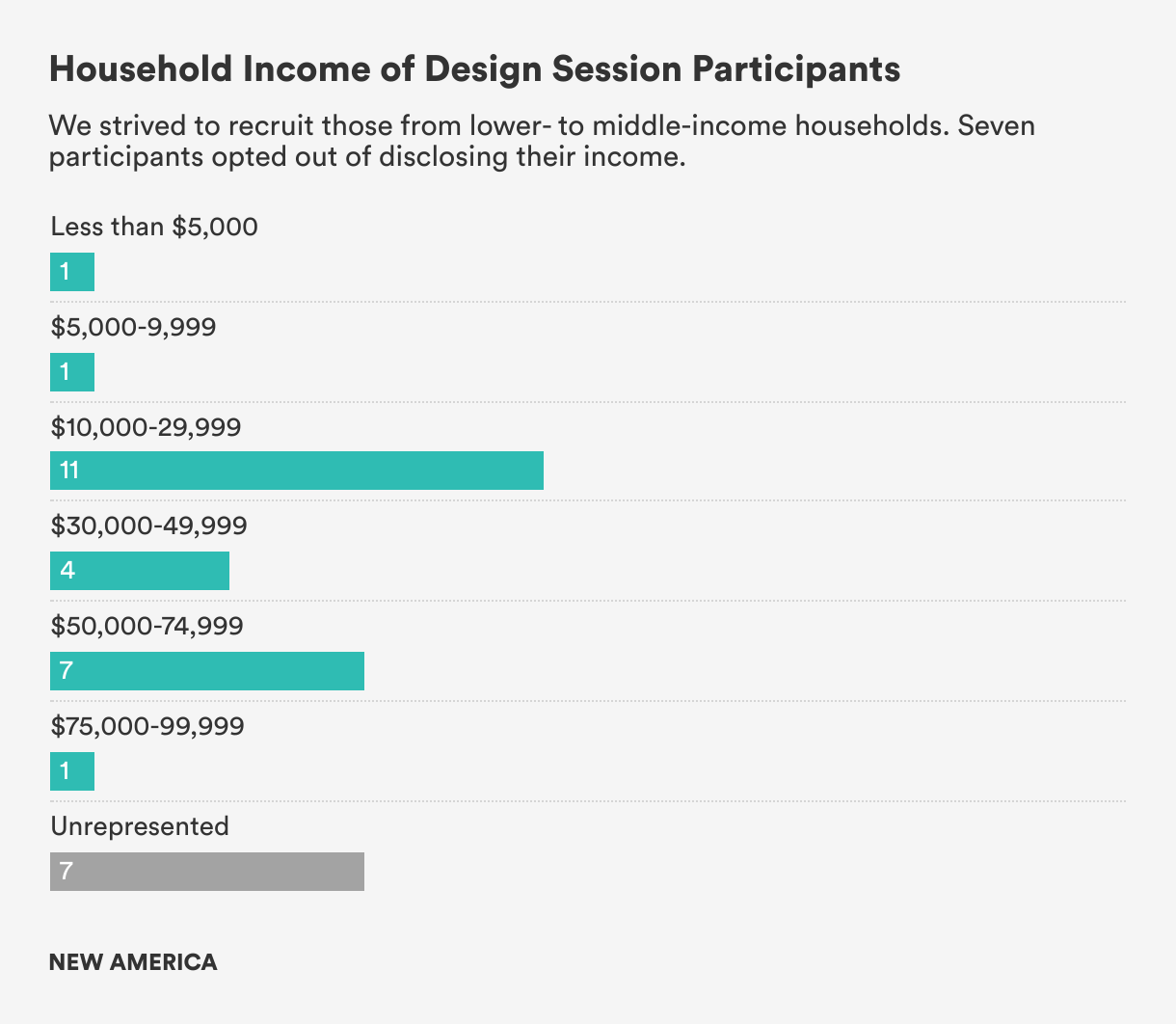

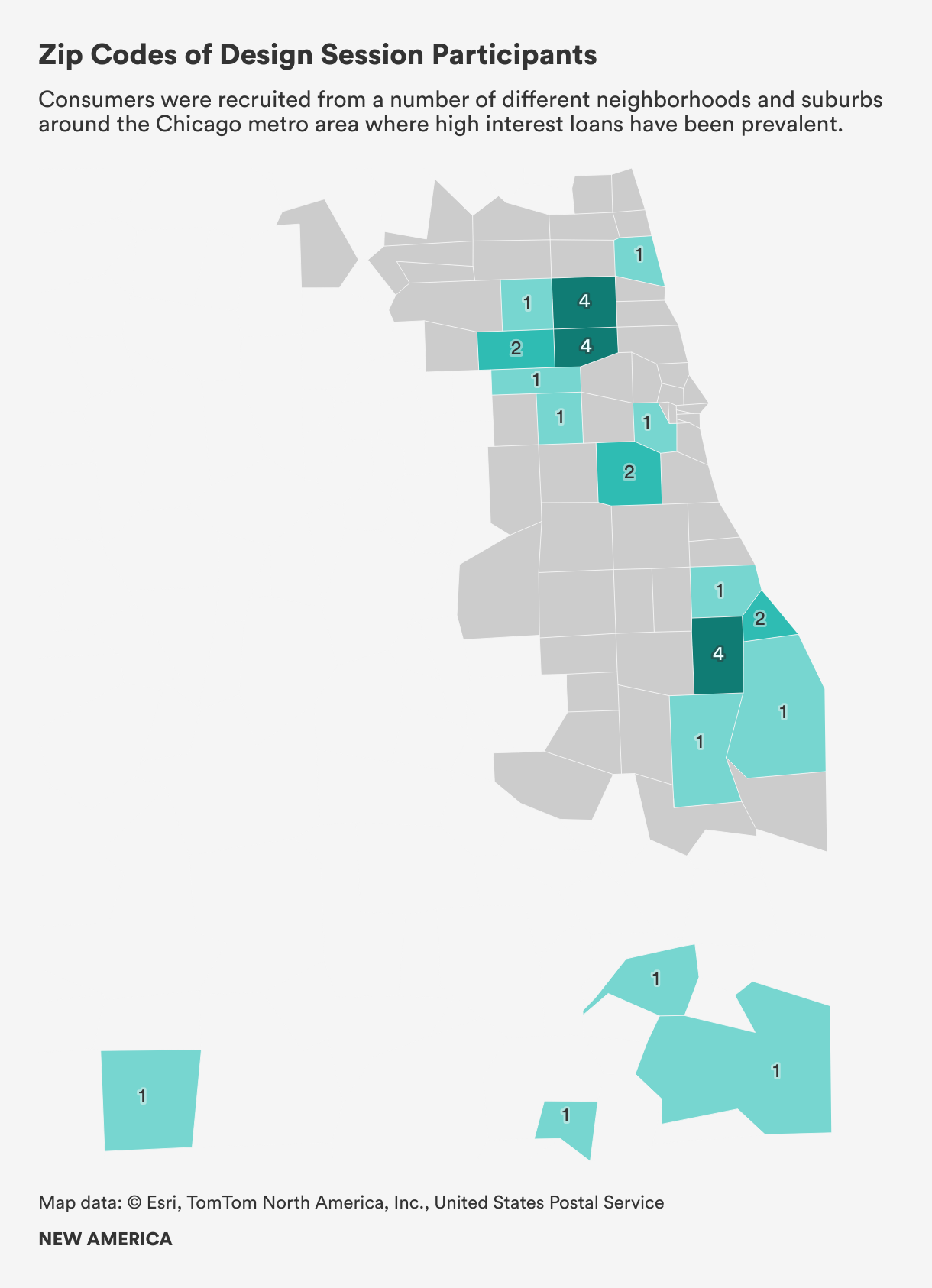

Appendix A: Participant Demographics

Participants had the option to share demographic information with us. The demographics for those who responded is included below. The community design sessions included a total of 32 people.

Appendix B: Session Design

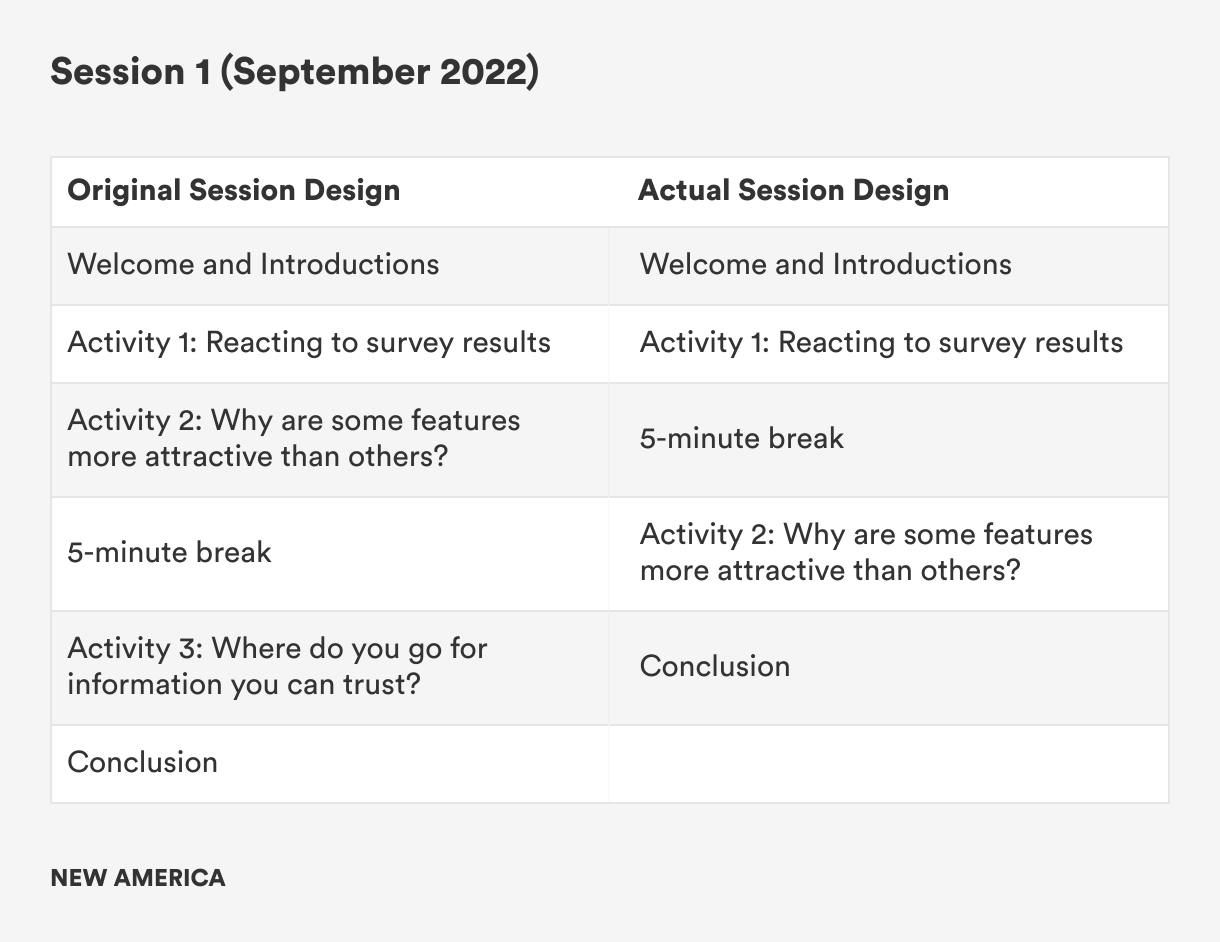

The CivicSpace team wanted the community sessions to use human-centered design principles, so a New America colleague with this expertise helped with planning and facilitation. For the first session, we planned on having a welcome and introductions portion, where we described the purpose of the group and the research questions of the session; three interactive activities; and a conclusion, where we held space for final comments to be either said or written down by participants and then discussed next steps.

The first activity was to gather reactions to our 2021 community survey findings from Chicagoland residents on their experiences with small dollar lending after the passage of the PLPA, to spur discussion about where people had found out about loans in the past. The other two activities focused on answering our research questions related to trusted messengers and what features make those loans safe and useful. However, this proved to be too much for 90 minutes and we had to cut the final activity. Allowing the participants to lead the session and have room for discussion was more of a priority than trying to rush through all of the planned activities. For more on the rationale and planning process of our first session, see our first publication on our process.

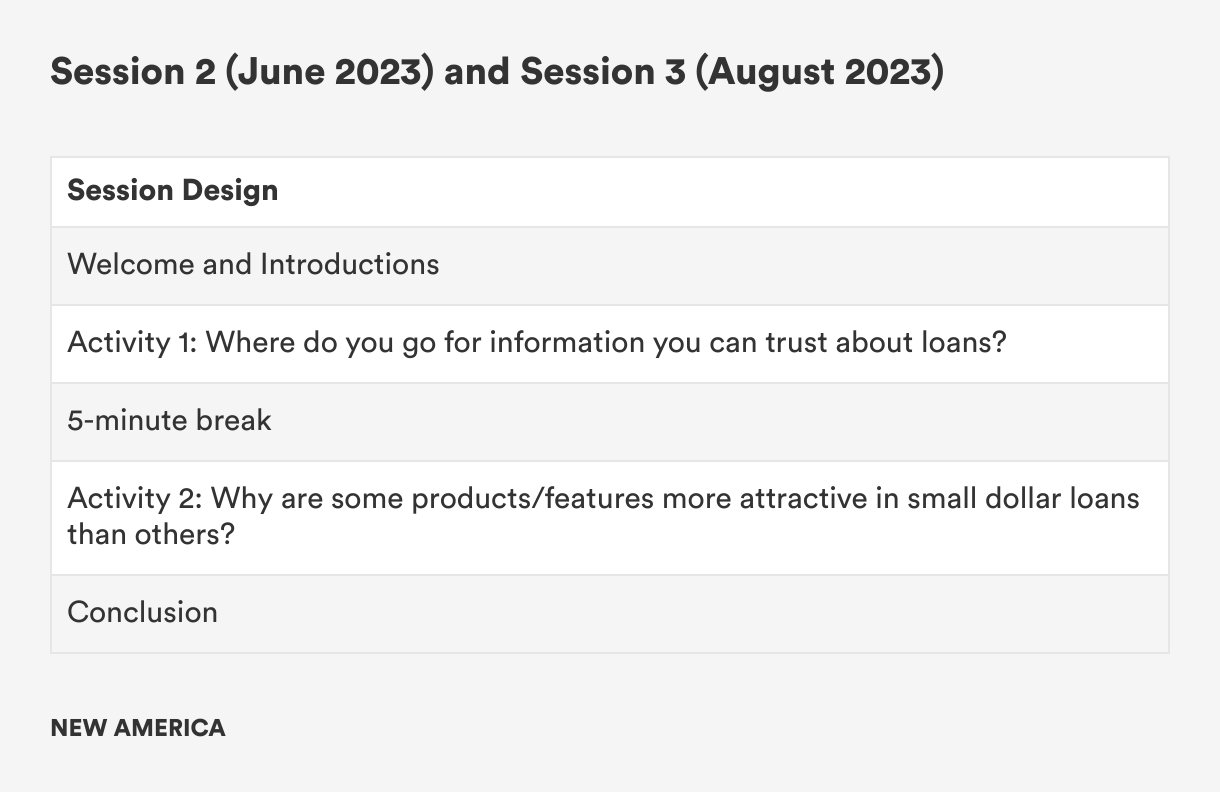

When it came to planning the second and third session the following year, the CivicSpace team knew we would have to cut down the agenda. We got rid of Activity 1, since it had already been over a year since the survey and we wanted to focus our time. We also switched the order of the two activities so they could more closely reflect participants’ actual lending process.

In the new Activity 2, rather than have the residents design their own small dollar loan and vote on a favorite, we used three loan products currently on the market in Chicago (a credit union lending product, an app-based loan, and a traditional bank loan) and removed all of their branding so that participants would not be biased. We split the residents into two scenarios, asked them to write down their questions and preferences, and had them vote on their favorite and least favorite products and discuss why. As a follow-up to our discussions with credible brick-and-mortar and fintech lenders, we wanted to learn more about why session participants chose certain products over others. Being able to adapt our research design after the initial session yielded rich insights that helped answer our research questions in more depth.

More About the Authors

Meegan Dugan Adell

Director, New America Chicago

Vanessa Rangel

Senior Program Associate, New America Chicago

Roselyn Miller Champion

Grant Analyst, City of Portland